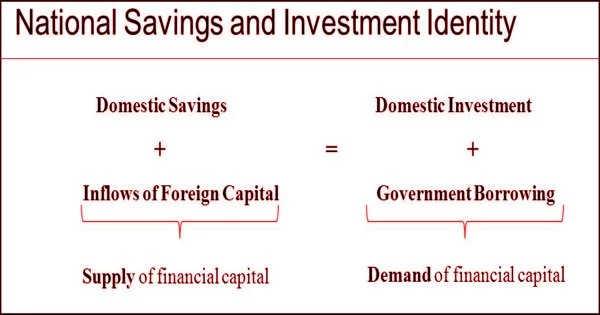

The saving identity, also known as the saving-investment identity, is a concept in national income accounting that states that the amount saved in an economy equals the amount invested in new physical machinery, inventories, and the like. More specifically, in an open economy (one with foreign trade and capital flows), private saving plus governmental saving (the government’s budget surplus or the negative of the deficit) plus domestic foreign investment (capital inflows from abroad) must equal private physical investment. In other words, the flow of variable investment must be financed by a combination of private domestic saving, government saving (surplus), and foreign saving (foreign capital inflows).

Saving equals investment is a fundamental macroeconomic accounting identity. Saving is defined as income-less spending. Physical investment, not a financial investment, is referred to as an investment. Saving equals investment follows from the identity of national income equals national product. It is more difficult to demonstrate that saving equals investment with the government. Government spending refers to the purchase of goods and services by the government. Negative taxes include transfer payments and interest on government debt.

This is an “identity,” which implies that it is true by definition. This identity is only valid because investment in this context includes both intentional and unintentional inventory accumulation. As a result, if consumers decide to save more and spend less, the drop in demand will result in an increase in business inventories. The change in inventories balances saving and investment without the business intending to increase investment. Furthermore, the identity holds because saving is defined as both private and “public saving” (actually public saving is positive when there is a budget surplus, that is, public debt reduction).

The national saving and investment identity is a useful tool for understanding the factors that influence trade and current account balances. In a country’s financial capital market, the amount of financial capital supplied at any given time must equal the amount of financial capital demanded for investment purposes. A country’s national savings are the sum of its domestic savings by households and businesses (private savings) as well as government savings (public savings). If a country has a trade deficit, it means that money from other countries is entering the country, and the government considers it part of the supply of financial capital.

As a result, an increase in savings does not necessarily imply an increase in investment. Indeed, increased inventories may cause businesses to reduce both output and planned investment. Similarly, a reduction in business output reduces income, forcing an unintended reduction in savings. Even if the end result of this process is a lower level of investment, the saving-investment identity will still be true at any given point in time.

The fundamental idea that the total quantity of financial capital demanded equals the total quantity of financial capital supplied must always be true. Domestic savings will always be part of the supply of financial capital, and domestic investment will always be part of the demand for financial capital. However, depending on whether the government budget and the trade balance are in surplus or deficit, the government and trade balance components of the equation can shift back and forth as suppliers or demanders of financial capital.