Origin Of The Report

Credit risk is the primary financial risk in the banking system. Identifying and assessing credit risk is essentially a first step in managing it effectively. In 1993, Bangladesh Bank as suggested by Financial Sector Reform Project (FSRP) first introduced and directed to use Credit Risk Grading system in the Banking Sector of Bangladesh under the caption “Lending Risk Analysis (LRA)”. The Banking sector since then has changed a lot as credit culture has been shifting towards a more professional and standardized Credit Risk Management approach.

Credit Risk Grading system is a dynamic process and various models are followed in different countries & different organizations for measuring credit risk. The risk grading system changes in line with business complexities. A more effective credit risk grading process needs to be introduced in the Banking Sector of Bangladesh to make the credit risk grading mechanism easier to implement.

Keeping the above objective in mind, the Lending Risk Analysis Manual (under FSRP) of Bangladesh Bank has been amended, developed and re-produced in the name of “Credit Risk Grading Manual”. With the world moving towards Basle II the need to introduce a RGS for the industry is essential. In 2003, BB made the Core Risk Management Guidelines (CRMG) mandatory.

The Credit Risk Grading Manual has taken into consideration the necessary changes required in order to correctly assess the credit risk environment in the Banking industry. This manual has also been able to address the limitations prevailed in the Lending Risk Analysis Manual.

All Banks should adopt a credit risk grading system outlined in this manual. Risk grading is a key measurement of a Bank’s asset quality, and as such, it is essential that grading is a robust process.

1.1 Introduction

Credit risk grading is an important tool for credit risk management as it helps the Banks & financial institutions to understand various dimensions of risk involved in different credit transactions. The aggregation of such grading across the borrowers, activities and the lines of business can provide better assessment of the quality of credit portfolio of a bank or a branch. The credit risk grading system is vital to take decisions both at the pre-sanction stage as well as post-sanction stage.

At the pre-sanction stage, credit grading helps the sanctioning authority to decide whether to lend or not to lend, what should be the loan price, what should be the extent of exposure, what should be the appropriate credit facility, what are the various facilities, what are the various risk mitigation tools to put a cap on the risk level.

At the post-sanction stage, the bank can decide about the depth of the review or renewal, frequency of review, periodicity of the grading, and other precautions to be taken.

Having considered the significance of credit risk grading, it becomes imperative for the banking system to carefully develop a credit risk grading model which meets the objective outlined above.

The Lending Risk Analysis (LRA) manual introduced in 1993 by the Bangladesh Bank has been in practice for mandatory use by the Banks & financial institutions for loan size of BDT 1.00 corer and above. However, the LRA manual suffers from a lot of subjectivity, sometimes creating confusion to the lending Bankers in terms of selection of credit proposals on the basis of risk exposure. Meanwhile, in 2003 end Bangladesh Bank provided guidelines for credit risk management of Banks wherein it recommended, interlaid, the introduction of Risk Grade Score Card for risk assessment of credit proposals.

Since the two credit risk models are presently in vogue, the Governing Board of Bangladesh Institute of Bank Management (BIBM) under the chairmanship of the Governor, Bangladesh Bank decided that an integrated Credit Risk Grading Model be developed incorporating the significant features of the above mentioned models with a view to render a need based simplified and user friendly model for application by the Banks and financial institutions in processing credit decisions and evaluating the magnitude of risk involved therein.

Bangladesh Bank expects all commercial banks to have a well defined credit risk management system which delivers accurate and timely risk grading. This manual describes the elements of an effective internal process for grading credit risk. It also provides a comprehensive, but generic discussion of the objectives and general characteristics of effective credit risk grading system. In practice, a bank’s credit risk grading system should reflect the complexity of its lending activities and the overall level of risk involved.

1.2 Objectives of The Study:

This study is aimed at providing me invaluable knowledge on current business trend in Bangladesh. Southeast bank ltd is one of the fast growing 2nd generation bank in Bangladesh. I have been assigned to do my internship here. I have also been assigned with some objectives to be filled up during this internship program. The objectives of study are as following:

To collect information about Credit Risk Grading System

To analyze the data of different clients.

To learn about Credit Risk analysis

To identify strength and weakness of Credit Risk Grading system.

To gather comprehensive knowledge to measure risk grading.

1.3 Methodology of the Study:

For smooth and accurate study every one have to follow some rules & regulation. The study impute were collected from two sources:

(a) Primary sources

(i) Practical desk work.

(ii) Face to face conversation with the officer.

(iii) Direct observations.

(iv) Face to face conversation with the client.

(v) Data gathered from organization supervisor.

(b) Secondary sources

(i) Annual Report

(ii) Credit guideline of SEBL

(iii) Daily diary (containing my activities of practical orientation in SEBL) maintained by me,

(iv) Different books, Journals, Periodicals, News papers, Websites etc.

(v) Different circulars sent by Head Office and Bangladesh Bank.

1.4.1 Historical Background:

The second generation bank of the Southeast Bank Limited (SEBL) is a scheduled Bank under private sector established under the ambit of bank Company Act, 1991 and incorporated as a Public Limited Company under Companies Act, 1994 on March 12, 1995. The Bank started commercial banking operations effective from May 25, 1995. During this short period of time the Bank had been successful to position itself as a progressive and dynamic financial institution in the country. The Bank had been widely accepted by the business community, from small entrepreneur to large traders and industrial conglomerates, including the top rated corporate borrowers for forward-looking business outlook and innovative financing solutions. Thus within this very short period of time it has been able to create an image for itself and has earned significant reputation in the country’s banking sector as a Bank with vision. Presently it has forty one branches in operation.

The bank is managed by a team of efficient professionals. There prevails a positive organizational climate in the bank that generates feeling of dignity, trust, discipline and openness in the people and result in motivating them to post better result continuously in the bank. The Company Philosophy – “A Bank with Vision” has been preciously the soul of the legend of bank’s success.

It has been growing faster as one of the leaders of the second generation banks in the private sector in respect of business and profitability as it is evident from the financial indicators as a pioneer banking institute in Bangladesh and contribute significantly to the national economy.

Southeast Bank is today a synonym of quality banking products. It has a diverse array of carefully tailored product and services to cater to the needs of all customer segments. Today, Southeast Bank is one of the leading and most successful banking institutions in Bangladesh with a total assets base of TK. 68,544.71 million as on June 30, 2008. The credit rating of the bank for the June 30, 2008 was done by Credit Rating Agency of Bangladesh (CRAB). They have rated the bank A1 (pronounced single A one) (High safety) for the long term. Commercial Banks rated in this category are adjudged to be strong Banks.

1.4.2 Corporate Mission and Vision of Southeast Bank Limited

Mission

High quality financial services with the help of latest technology.

Fast and accurate customer service.

Balanced growth strategy.

High standard business ethics.

Steady return on shareholder’s equity.++

Innovative banking at a competitive price.

Deep commitment to the society and the growth of national economy.

Attract and retain quality human resource.

Vision

To stand out as a pioneer banking institution in Bangladesh and contribute significantly to the national economy.

1.4.3 Organizational Structure

The following hierarchy is the organizational hierarchy of SBL and it depicts the top-bottom relationship:

President and Managing Director (MD) |

Deputy Managing Director (DMD) |

Senior Executive Vice President (SEVP) |

Executive Vice President (EVP) |

Senior Vice President (SVP) |

Vice President (VP) |

First Vice President (FVP) |

Senior Assistant Vice President (SAVP) |

Assistant Vice President (AVP) |

Senior Principal Officer (SPO) |

Principal Officer (PO) |

Executive Officer (EO) |

Management Trainee (MT) |

Probationary Officer (PO) |

Senior Officer (SO) |

Officer (O) |

Junior Officer (JO) |

Trainee Junior Officer (TJO) |

Senior Officer (Computer) |

Officer (Computer) |

Junior Officer (Computer) |

Computer-Trainee |

Head Cashier |

Senior Officer (Cash) |

Officer (Cash) |

Junior Officer (Cash) |

Cashier-Trainee |

Messenger |

Bank Guard |

1.4.4 Comparative financial position of Southeast Bank Limited

Highlights on the overall activities of the Bank on June’ 2008

| 01. | Date of Incorporation | : | 12th March, 1995 |

| 02. | Date of Commencement of Business | : | 12th March, 1995 |

| 03. | Capital Authorized | : | Tk. 3500.00 Million |

| Paid-up | : | Tk. 2852.19 Million | |

| Total Capital | : | Tk. 6,724.37 Million | |

| 05. | Total Deposits | : | Tk. 59094.24 Million |

| 06. | Total Assets | : | TK. 68544.71 Million |

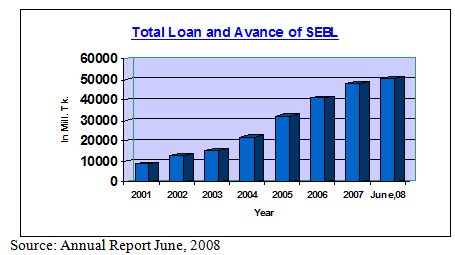

| 07. | Total Loan of Advances | : | Tk. 50715.26 Million |

| 08. | Operating Profits | : | Tk. 2916.20 Million |

| 09. | Loan as a % of Total Deposits | : | 85.82% |

| 10. | Profit After Tax and Provision | : | Tk. 479.78 Million |

| 11. | Cost of Fund | : | 9.53% |

| 12. | Global Relations | : | 598 Correspondents Worldwide |

| 13. | Number of Employees | : | 1116 |

| 14. | Percentage of Classified Loans against Total Loans and Advance | : | 5.64% |

| 15. | Provision kept against classified loan | : | Tk. 1,306.13 Million |

| 16. | Return on Assets | : | 0.70% |

| 17. | Return on Investment | : | 7.64% |

| 18. | Number of Branches | : | 41 |

| 19. | Earning & Net Income Per Share | : | 16.82 |

| 20. | Name of the Chairman of SEBL | : | Mr. Alamgir Kabir, FCA |

| 22. | It is a Publicly Traded Company | : | Share quoted daily in DSE & CSE |

| 23. | Credit Card | : | Member of Master & VISA Card |

| 24. | Banking Operation System | : | Both conventional & Islamic Shariah System |

| 25. | Technology Used | : | Member of SWIFTOnline Banking Computer SystemSWIFT: SEBDBDDHXXX E-mail: info@sebankbd.com Website: www.sebankbd.com |

Our Capital Structure

Southeast Bank Limited is a highly capitalized Bank. Its Authorized Capital is Tk. 3500 million while its Paid up Capital is Tk. 2852.19 million as on 30th June, 2008. The total shareholders equity reached Tk. 67243.77 million as on 30th June, 2008.

| Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | June,08 |

| Capital | 757.20 | 970.96 | 1300.14 | 1649.4 | 2236.84 | 4940.921 | 6468.36 | 6724.37 |

1.4.5 Our preparedness for Basel-ll

Guidelines prescribe under new capital Accord known as Basel-ll comprises the following components:

Minimum Capital Requirement.

Supervisory Review Process, and

Market Discipline.

The prescribed guidelines are being implemented in the bank. The banks aim to create an environmental for risk management to identify and measure risk and report all important risk information distributing capital within the framework of Basel-ll. We always try to maintain a minimum level of capital to act cushion against unexpected losses arising from our investment.

We are promoting safety and soundness in our financial system. Bangladesh Bank has taken a proactive approach in implementing Basel-ll for all banks in Bangladesh by January 1, 2009 and made credit rating mandatory for all Banks. The Credit Rating of Southeast Bank Ltd. Was done by Credit Rating Agency of Bangladesh (CRAB) and they rated the Bank A1 for the long term.

In order to ensure gradual and smooth transition to Basel-ll, Bangladesh Bank asked the Banks in Bangladesh to maintain Capital adequacy ratio at minimum 10% with effect from January 01, 2008. We have since increased our Capital. Now, our Capital adequacy is 13% as on 31st December 2007.

Our Assets

Asset of SEBL for the year 2000-2008

Year | 2001 | 2002 | 2003 |

2004 |

2005 |

2006 | 2007 |

June,08 |

Asset | 14468.66 | 18882.48 | 23135.74 | 33744.96 |

43294.81 |

53706.12 | 64370.69 |

68544.71 |

1.4.6 Main Operational Area

As a commercial bank, Southeast Bank does all traditional banking business including the wide range of savings and credit scheme products, retail banking and ancillary services with the support of modern technology and professional excellence. The bank has launched according to market demand a number of financial products and services since its inception. Our journey towards greater operational success continues with increased energy and enthusiasm. Our product-basket encompasses real time On-line any Branch Banking, Islamic Banking, Partial Merchant Banking, Dual Currency Visa Credit Card, ATMs, Education loan scheme, Double Benefit scheme, Consumer loan, SMS Banking, Corporate Banking, Syndicate Loan, Monthly Saving Scheme, Monthly Income Scheme, Pension Saving Scheme, and Wage Earner Pension Scheme etc. And Bank finances the Individual, Small Business, Commercial, Textile, Garments, Chemical & Cements area.

1.4.7 Operational Result

Alike preceding four years, Southeast Bank posted good growth in all areas of business operations. Our effort to push the Bank forward for future qualitative improvements will continue with added enthusiasm. The Bank achieved an operating profit of Tk. 1,495.36 million before necessary provision for advance and other assets and income tax during the first half-year ended on 30th June, 2008.

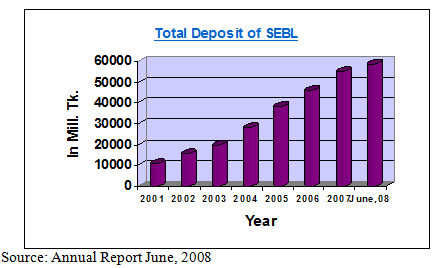

Our total Deposits stood at Tk. 59,094.25 million while its total outstanding loans and advances were Tk. 50715.26 million as on 30th June, 2008. During the first six month of the year 2008, the bank handled foreign trade business of Tk.53,390.80 million (both import and export) and earning Net profit after provision and income tax for the period stood at Tk. 497.78 million. Our operational result given below:

Operation | Increase (Percentage) |

Deposit | 14% |

Advance | 21% |

Import | 78% |

Export | 65% |

Bank guarantee | 104% |

Net profit | 14% |

A. Deposit Schemes

Bank has the following customer friendly deposit schemes:

Current Deposit Scheme (CD)

Savings Deposit scheme (SB)

Short Term Deposit Scheme (STD)

Pension Savings Scheme (PSS)

Education Savings Scheme (ESS)

Monthly Savings Scheme (MSS)

Double Benefit Deposit Scheme (SBDS)

Fixed Deposits ( 1, 2, 3, 6 & 12 months )

Year | 2001 | 2002 | 2003 |

2004 |

2005 |

2006 |

2007 | June,08 |

| Total Deposit | 10570.25 | 15343.45 | 19618..82 | 27930.84 | 38254.15 | 46056.18 | 55474.05 | 59094.25 |

B. Credit Schemes

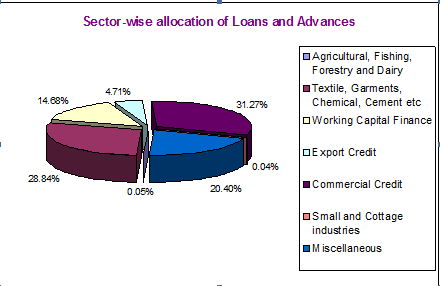

The loan portfolio of the Bank is well diversified and covers funding to a wide spectrum of business and industries including readymade garments, textile, edible oil, ship scrapping, steel & engineering, chemical, pharmaceuticals, cement, construction, health-care, real-estate and loans under consumer’s credit schemes allowed to the middle-class people of the country for acquiring various household items.

Loan Scheme | Lending Category | Lending Rate |

| Agricultural Scheme |

Loan to primary producers and Loan to agricultural input traders and fertilizer dealers/distributors11.50%

Commercial LendingJute Trading and Others Commercial Lending 15.00%Working CapitalJute and Other than Jute 13.00%House Building LoanReal Estate Developers and Individual/Housing Finance Co. 15.50%15.00%Other LoansSMEOthers

16.50%, 15.50%Small/Cottage IndustryTerm Loan 15.00%Finance To NBFIs 14.50%Large/Medium Scale IndustryTerm Loan 13.25%Post Import FinanceLIM/LTR Loan against ExportJute Goods Exports and Other Exports 7.00% FixedConsumer Credit Scheme 16.00%Credit Card 2.50% Per Month (fixed)

Note: 1. The Bank reserves the right to increase or decrease by 1.50% of the mid rate in each category.

2.Lending Rates against the Fixed Deposit will be fixed at minimum of 3.00%above the FDR rates, Issued by our Bank and this will not be applicable for others Banks’ FDRs.

Loan and Advance of SEBL for the year 2001-2008

Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | June,08 |

Advance | 9178.03 | 1327.13 | 15541.50 | 22001.70 | 32551.09 | 41147.28 | 48164.60 | 50715.26 |

C. “Foreign Trade Business (Import & Export)

Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 |

Foreign Trade Business | 14862.42 | 15080.46 | 19304.15 |

26992.15 |

42540.40 |

61000.73 |

67242.70 |

D. Business Guarantee

Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 |

Business Guarantee | 1854.50 | 2502.48 | 3391.19 | 4717.82 | 7975.00 | 8656.80 | 9008.32 |

E. Net Profit

Year | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | June,08 |

Net Profit | 270.74 | 253.56 | 256.06 | 294.69 | 374.20 | 909.88 | 1222.97 | 1495.36 |

F. Interest Income

Year | 2004 | 2005 | 2006 | 2007 | June,08 |

Interest Income | 2310.93 | 3568.20 | 5107.79 | 6408.96 | 3458.49 |

G. Interest Paid

Year | 2004 | 2005 | 2006 | 2007 | June,08 |

Interest Paid | 22001.70 | 32551.09 | 41147.28 | 48164.60 | 50715.26 |

H. Inflow of foreign Remittance

Wages earners’ remittance together with export proceeds exceeded the total import liability of the bank in 2007.

Source: Annual Report 2007

Fig in million Tk

Year | 2004 | 2005 | 2006 | 2007 | June,08 |

Inflow of Foreign Remittance | 654.24 | 1091.25 | 3507.40 | 13479.83 | 11040.17 |

1.4.8 Risk Management

Risk Management is the key element for sound corporate governance of the Bank. With a recent addition in regulatory mandates and increasingly active participation of shareholders, the Bank has become increasingly concerned to identify areas of risks in the business, whether it is financial, operational, ICT or reputation risk. Southeast Bank identifies, measures, monitors and manages all risks of the Bank. Sophisticated risk management framework is being implemented to carry out efficient risk management exercises of the Bank including documenting and assessing risks, defining controls, managing assessments and audit, identifying issues, implementing recommendations and corrective plans. In accordance with Bangladesh Bank Guidance Notes, the Bank has established a risk framework that consists of six core factors, i.e.

(i) Credit Risk

(ii) Asset and Liability/Balance Sheet Risk

(iii) Foreign Exchange Risk

(iv) Internal Control and Compliance Risk

(v) Money Laundering Risk and

(vi) Information and Communication Technology Risk.

The Bank has also identified the following four key infrastructure components for effective risk management programs:

(i) Proactive Board of Directors and Senior Management’s Supervision,

(ii) Adequate Policies and Procedures,

(iii) Proper Risk-Measurement, Monitoring and Management Information Systems and

(iv) Comprehensive Internal Controls.

1.4.9 SWOT Analysis

SWOT is an important part for evaluating the company’s Strength, Weakness, Opportunity and Threats. It helps the organization to identify how to evaluate its performance and scan the micro environment.

In the year 2008, Southeast Bank is celebrating 13 years of its success track record in Bangladesh. The Strength, Weakness, Opportunities & Threats of the bank are identified as follows:

Strength (S)

Southeast Bank is having the following strengths.

Transparent and quick decision-Making

Efficient team of performers

Satisfied customers

Internal control

Skilled risk management

Diversification to perform business operation

Weaknesses (W)

Southeast Bank Limited has the following weaknesses:

Poor market share (deposit and lending share around 1.5% in the total industry).

Low geographical coverage of service (only 43 branches at present)

Lack of succession plan

No research and development facilities for innovating new products.

Long management hierarchy

Absence of Total Quality Management (TQM)

Concentration on Large Loan.

Opportunity (O)

Southeast Bank Limited has the following opportunities:

Further diversification of product

Expansion of Branch network

Attraction of more customers through sophisticated service quality.

Threats (T)

Southeast Bank Limited encounters the following threats:

Increased competition in the banking sector

Market pressure to lowering interest rate.

Switching of the customers & employees to other banks or institute.

Threat of Bank Loan default

Globalization of banking business

Change in banking regulation

Political instability in the country.

1.5 Outlook for 2008

Southeast bank remains deeply committed to its vision of becoming a premier banking institution of Bangladesh and contribute significantly to the national economy. The Bank intends to embrace the best practices and technology. It provides first-class product, financial services and solution to its customers. The Bank is already in the process of choosing robust and integrated software to provide more value added services to them.

The network of the bank will be increased by (twelve) more branches to reach 50 in 2008 subject to license from Bangladesh Bank. We shall continue to make significant investments for more talented and experienced people to help our customer realize their dreams. We shall continue to follow and improve good corporate governance practices, sound risk management policy, modern human resources policy and strictly maintain quality of our assets to elevate the bank gradually to the pinnacle to glory.

We will make every effort to achieve Return on equity of more than 20%, operating profit of Tk.4,000 million in 2008, maintain required Capital Adequacy ratio and limit classified loan at a tolerable level. To create more value for shareholders, Customer, employees and the society. For obvious reasons, we look at the year 2008 with a considerable optimism. However, as forward looking statements involve risk and uncertainties, it should be viewed accordingly.

In January 2004, BIBM was instructed by Governor Bangladesh Bank to produce a Credit Risk Grading Manual (CRGM) based on the Core Risks Management Guidelines. BIBM constituted a Focus Group for this purpose. The CRGM was completed and submitted to BB (Bangladesh Bank) in Sept ’04.

This was reviewed by a Industry Review Group (IRG) consisting of members from NCBs,. PCBs and FCBs involved specifically in the credit approval and corporate banking functions. The IRG met a number of times in august and September 2005 and gave their recommendations. These were discussed and suitable amendments made in the Guidelines.

Some More Parts-

Credit Risk Grading(CRG) In Southest Bank Limited (Part-1)