Taxation System in Bangladesh

Introduction

In Bangladesh, the principal direct taxes are personal income taxes and corporate income taxes, and a value-added tax (VAT) of 15% levied on all important consumer goods. The top income tax rate for individuals is 25%. For the 2004/05 tax year (July 1 2004–June 30 2005) the top corporate rate was 45%. However, publicly traded companies registered in Bangladesh are charged a lower rate of 30%. Banks, financial institutions and insurance companies are charged the 45% rate. All other companies are taxed at the 37.5% rate. Effective 1 July 2002, the VAT rate on computer hardware and software was reduced to 7.5%, and certain agricultural equipment and electricity supplied to the agricultural sector was exempted from VAT altogether. VAT on the transfer of land is also to be abolished. Essential agricultural implements and irrigation pumps had previously been excluded from certain taxes

Tax (definition)

To tax is to impose a financial charge or other levy upon a taxpayer (an individual or legal entity) by a state or the functional equivalent of a state such that failure to pay is punishable by law.

Taxes are also imposed by many subnational entities. Taxes consist of direct tax or indirect tax, and may be paid in money or as its labour equivalent (often but not always unpaid labour). A tax may be defined as a “pecuniary burden laid upon individuals or property owners to support the government a payment exacted by legislative authority.” A tax “is not a voluntary payment or donation, but an enforced contribution, exacted pursuant to legislative authority” and is “any contribution imposed by government whether under the name of toll, tribute, tallage, gabel, impost, duty, custom, excise, subsidy, aid, supply, or other name.”

The legal definition and the economic definition of taxes differ in that economists do not consider many transfers to governments to be taxes. For example, some transfers to the public sector are comparable to prices. Examples include tuition at public universities and fees for utilities provided by local governments. Governments also obtain resources by creating money (printing bills and minting coins), through voluntary gifts (contributions to public universities and museums),by imposing penalties (traffic fines), by borrowing, and by confiscating wealth. From the view of economists, a tax is a non-penal, yet compulsory transfer of resources from the private to the public sector levied on a basis of predetermined criteria and without reference to specific benefit received.

In modern taxation systems, taxes are levied in money, but in-kind and corvée taxation are characteristic of traditional or pre-capitalist states and their functional equivalents. The method of taxation and the government expenditure of taxes raised is often highly debated in politics and economics. Tax collection is performed by a government agency such as Canada Revenue Agency, the Internal Revenue Service (IRS) in the United States, or Her Majesty’s Revenue and Customs (HMRC) in the UK. When taxes are not fully paid, civil penalties (such as fines or forfeiture) or criminal penalties (such as incarceration) may be imposed on the non-paying entity or individual.

Tax Classifications

Direct tax:

A direct tax is a form of tax is collected directly by the government from the persons who bear the tax burden. Taxable individuals file tax returns directly to the government. Examples of direct taxes are corporate taxes, income taxes, and transfer taxes.

Indirect tax:

An indirect tax is a form of tax collected by mediators who transfer the taxes to the government, and also perform functions associated with filing tax returns. The customers bear the final tax burden. Examples of indirect taxes are sales tax and value added tax (VAT).

There are other types of taxes, which may either be direct tax or indirect taxes, including capital gains tax, corporation tax, consumption tax, inheritance tax, property tax, excise duty, retirement tax, tariffs, wealth tax or net worth tax, toll tax, and poll tax.

Purposes and effects

Money provided by taxation have been used by states and their functional equivalents throughout history to carry out many functions. Some of these include expenditures on war, the enforcement of law and public order, protection of property, economic infrastructure (roads, legal tender, enforcement of contracts, etc.), public works, social engineering, and the operation of government itself. Governments also use taxes to fund welfare and public services. These services can include education systems, health care systems, pensions for the elderly, unemployment benefits, and public transportation. Energy, water and waste management systems are also common public utilities. Colonial and modernizing states have also used cash taxes to draw or force reluctant subsistence producers into cash economies.

Governments use different kinds of taxes and vary the tax rates. This is done to distribute the tax burden among individuals or classes of the population involved in taxable activities, such as business, or to redistribute resources between individuals or classes in the population. Historically, the nobility were supported by taxes on the poor; modern social security systems are intended to support the poor, the disabled, or the retired by taxes on those who are still working. In addition, taxes are applied to fund foreign aid and military ventures, to influence the macroeconomic performance of the economy (the government’s strategy for doing this is called its fiscal policy – see also tax exemption), or to modify patterns of consumption or employment within an economy, by making some classes of transaction more or less attractive.

A nation’s tax system is often a reflection of its communal values or/and the values of those in power. To create a system of taxation, a nation must make choices regarding the distribution of the tax burden—who will pay taxes and how much they will pay—and how the taxes collected will be spent. In democratic nations where the public elects those in charge of establishing the tax system, these choices reflect the type of community that the public and/or government wishes to create. In countries where the public does not have a significant amount of influence over the system of taxation, that system may be more of a reflection on the values of those in power.

The resource collected from the public through taxation is always greater than the amount which can be used by the government. The difference is called compliance cost, and includes for example the labour cost and other expenses incurred in complying with tax laws and rules. The collection of a tax in order to spend it on a specified purpose, for example collecting a tax on alcohol to pay directly for alcoholism rehabilitation centres, is called hypothecation. This practice is often disliked by finance ministers, since it reduces their freedom of action. Some economic theorists consider the concept to be intellectually dishonest since (in reality) money is fungible. Furthermore, it often happens that taxes or excises initially levied to fund some specific government programs are then later diverted to the government general fund. In some cases, such taxes are collected in fundamentally inefficient ways, for example highway tolls.

Some economists, especially neo-classical economists, argue that all taxation creates market distortion and results in economic inefficiency. They have therefore sought to identify the kind of tax system that would minimize this distortion. Also, one of every government’s most fundamental duties is to administer possession and use of land in the geographic area over which it is sovereign, and it is considered economically efficient for government to recover for public purposes the additional value it creates by providing this unique service.

Since governments also resolve commercial disputes, especially in countries with common law, similar arguments are sometimes used to justify a sales tax or value added tax. Others (e.g. libertarians) argue that most or all forms of taxes are immoral due to their involuntary (and therefore eventually coercive/violent) nature. The most extreme anti-tax view is anarcho-capitalism, in which the provision of all social services should be voluntarily bought by the person(s) using them.

The Four “R”s

Taxation has four main purposes or effects: Revenue, Redistribution, Repricing, and Representation.

The main purpose is revenue: taxes raise money to spend on armies, roads, schools and hospitals, and on more indirect government functions like market regulation or legal systems.

A second is redistribution. Normally, this means transferring wealth from the richer sections of society to poorer sections.

A third purpose of taxation is repricing. Taxes are levied to address externalities: tobacco is taxed, for example, to discourage smoking, and a carbon tax discourages use of carbon-based fuels.

A fourth, consequential effect of taxation in its historical setting has been representation. The American revolutionary slogan “no taxation without representation” implied this: rulers tax citizens, and citizens demand accountability from their rulers as the other part of this bargain. Studies have shown that direct taxation (such as income taxes) generates the greatest degree of accountability and better governance, while indirect taxation tends to have smaller effects.

Tax incidence

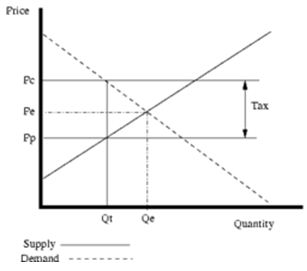

Law establishes from whom a tax is collected. In many countries, taxes are imposed on business (such as corporate taxes or portions of payroll taxes). However, who ultimately pays the tax (the tax “burden”) is determined by the marketplace as taxes become embedded into production costs. Depending on how quantities supplied and demanded vary with price (the “elasticities” of supply and demand), a tax can be absorbed by the seller (in the form of lower pre-tax prices), or by the buyer (in the form of higher post-tax prices). If the elasticity of supply is low, more of the tax will be paid by the supplier. If the elasticity of demand is low, more will be paid by the customer. And contrariwise for the cases where those elasticities are high. If the seller is a competitive firm, the tax burden flows back to the factors of production depending on the elasticities thereof; this includes workers (in the form of lower wages), capital investors (in the form of loss to shareholders), landowners (in the form of lower rents) and entrepreneurs (in the form of lower wages of superintendence).

To illustrate this relationship, suppose the market price of a product is $1.00, and that a $0.50 tax is imposed on the product that, by law, is to be collected from the seller. If the product has an elastic demand, a greater portion of the tax will be absorbed by the seller. This is because goods with elastic demand cause a large decline in quantity demanded for a small increase in price. Therefore in order to stabilise sales, the seller absorbs more of the additional tax burden. For example, the seller might drop the price of the product to $0.70 so that, after adding in the tax, the buyer pays a total of $1.20, or $0.20 more than he did before the $0.50 tax was imposed. In this example, the buyer has paid $0.20 of the $0.50 tax (in the form of a post-tax price) and the seller has paid the remaining $0.30 (in the form of a lower pre-tax price).

Types Of Taxes

Paying Taxes

Taxes are monies paid by citizens and residents to federal, state, and local governments. The money collected from these taxes help fund for services provided by the government. It is the one of the main sources of government revenue. Types of taxes include income tax, sales tax, and property tax.

Income Tax

These are paid on a federal level and in some cases to state or local governments as well. “Taxable income” is essentially money obtained through wages, self-employment, and tips and from things like sale of property. The large majority of people pay their income taxes by having the money withheld from their paychecks. The proportion of income tax an individual is required to pay will vary according to earnings. Income tax rates are generally lower for those who make less money. However, any individual who earns an income, live in the United States and satisfies certain criteria is needed to file a tax return and also pay any taxes that they owe.

Social Security and Medicare taxes

These types of taxes are usually withheld from your paycheck. Social security benefits are provided for retired workers and their families, for disabled workers and their families and also for certain family members of deceased workers. Medicare (healthcare) taxes provides for medical services (this applies for people aged 65 and above). In the large majority of cases, a will qualify for Social Security retirement benefits and Medicare benefits after having served a period of 10 years (or 40 quarters) over the course of your life. However, in the case of disability benefits for you or your family it is likely that you will require less than 10 years of work depending on your earnings.

Sales Taxes

Sales taxes are more or less state or local taxes and usually added to the buying cost of certain things. These taxes will be based on the cost of items and help fund for services provided by state and local government, such as roads, police, and firefighters.

Property taxes

These are also state and local taxes that are charged on your home and land. In most situations, these property taxes contribute to funding of local public schools and other services in the area person.

This is a concept summary. It aims to show how different types of taxes are categorized, and to highlight the strong and weak points of each type.

Government is supported by resources drawn from the economy. In return, government protects the economy from foreign and domestic enemies, undertakes large-scale infrastructure works of general benefit, and enforces the rights, obligations and bargains necessary for economic activity in a civil society. In modern industrial society, a tax either claims a portion of the flow of value in economic transactions between people, or takes a part of someone’s accumulated stock of economic value.

Bangladesh Income Tax Rates

Bangladesh personal income tax rates for assessment year 2010 – 2011 is progressive up to 25%.

Bangladesh Income Tax Rates for individuals other than female taxpayers, senior taxpayers of 65 years and above and retarded taxpayers – Assessment Year 2010 – 2011

First BDT 1,65,000 Nil

Next BDT 2,75,000 10%

Next BDT 3,25,000 15%

Next BDT 3,75,000 20%

Rest Amount 25%

Minimum tax for any individual assessee is Tk. 2,000

Non-resident Individual: 25% (other than non-resident Bangladeshi)

On Dividend income: 20%

Income tax is one of the main sources of revenue in Bangladesh. It is a progressive tax system. Bangladesh Income tax is imposed on the basis of ability to pay. The more a taxpayer earns the more tax he should pay. This is the basic principle of charging income tax in Bangladesh. The tax system aims at ensuring equity and social justice. Tax rates in Bangladesh also differs between male and female individuals.

Time to submit income tax return: Unless the date is extended, by the 30th day of September next following the income year.

Consumption tax

A consumption tax is a tax on spending on goods and services. The tax base of such a tax is the money spent on consumption. Consumption taxes are usually indirect, such as a value added tax. However it can also be structured as a form of personal taxation, as a sales tax, or as an income tax that deducts investments and savings. A direct consumption tax may be called an expenditure tax, a cash-flow tax, or a consumed-income tax, and can be flat or progressive.

Types

Value-added tax (VAT)

This tax applies to the market value added to a product or material at each stage of its manufacture or distribution. If a retailer buys a shirt for $20 and sells it for $30, this tax would apply to the $10 difference between the two amounts. A simple VAT is regressive in that lower-income consumers generally consume a higher fraction of their income than others, and the VAT does not apply to income that is saved/invested. VATs often exclude certain goods, with the intent of creating some degree of progressivity. It is widely used in countries within the European Union.

Sales tax

This tax typically applies to the sale of goods, and less often, to the sales of services. The tax is applied at the point of sale. Like VAT, simple sales taxes hit lower-income consumers harder than others, leading to exemptions for basic items such as food.

Excise tax

This tax is a sales tax that applies to a specific class of goods, typically alcohol, gasoline, or tourism. The tax rate varies according to the type of good and quantity purchased, and is typically unaffected by who purchases it.

Personal consumption tax

This tax applies to the difference between an individual’s income and increase/decrease savings. Like the other consumption taxes, simple personal consumption taxes are regressive. However, because this tax applies on an individual basis, it can be made as progressive as a progressive personal income tax. Just as income tax rates increase with personal income, consumption tax rates increase with personal consumption.

Value Added Tax (VAT)

Value Added Tax (VAT) a percentage tax on the value added of a commodity or service as each constituent stage of its production and distribution is completed. VAT may be classified in three ways: (i) on the basis of coverage of stages – throughout the production and distribution stages, or confined to limited stages – manufacturing plus wholesale, or wholesale plus retail; (ii) on the basis of the method of calculation – tax credit method, subtraction method, and addition method; and (iii) on the basis of tax treatment of final-product capital goods such as machinery, equipment, and supplies – the consumption form, the income form, and the product variety. Thus the three broad types of VAT are the gross national product (GNP) type, income type and consumption type. A consumption type VAT is an indirect tax. An income type or a GNP type VAT might be considered as a direct tax but a commodity tax cannot be considered so. Consumption type VAT is also considered as an alternative form of ‘sales tax’.

In April 1979, the Taxation Enquiry Commission (TEC) officially took up the issue of introducing VAT in Bangladesh as an alternate to sales tax. Until 1982, sales tax was being collected under the Sales Tax Act 1951, which was replaced by the Sales Tax Ordinance 1982 with effect from 1 July 1982. The World Bank played the pioneering role in introduction of VAT in Bangladesh. A World Bank Mission visited Bangladesh for preparing an agenda for tax reform in Bangladesh in December 1986. The mission submitted its final report on 15 October 1989. The report recommended the introduction of a manufacturing-cum-import stage VAT at a single standard rate within three years. Thereafter, a Bangladesh Tax Mission visited India, Indonesia, the Philippines and Thailand during 13 November – 04 December 1989. The Mission submitted its report in January 1990. The government discussed the issues relating to introduction of VAT with all related private and public agencies including the various leading Chambers of Commerce and Industry from time to time. The government prepared the Value Added Tax Act 1990 (Draft) in June 1990.

Final version of the Value Added Tax Act was promulgated 31 May 1991 as a Presidential Ordinance with eight sections (relating to registration under VAT system and the appointment and powers of VAT authorities). It was made effective from 2 June 1991. The Value Added Tax Bill 1991 was introduced in the Parliament on 1 July 1991 and the Parliament passed it on 9 July 1991. With the Presidential assent to the bill on the next day it came into effect as The Value Added Tax Act 1991. The VAT Act 1991 replaced the Business Turnover Tax Ordinance 1982 and the Sales Tax Ordinance 1982 with effect from 1 July 1991. It imposed VAT @ 15% on importer or supplier (producer) of taxable goods and provider of taxable services having annual turnover of Tk 1.5 million or more. It imposed Turnover Tax (TT) @ 2% (currently 4%) on supplier of taxable goods and provider of taxable services having annual turnover of less than Tk 1.5 million (Tk 2 million at present). The new law imposed VAT at zero-rate on export sales of any goods and services, brought excise duties on most goods under the VAT net, and imposed Supplementary Duty (SD) @ 10% to 85% on goods and services which are luxurious and non-essential and are socially undesirable.

The objectives behind introducing VAT in Bangladesh were to (a) bring transparency in the taxation system; (b) prohibit cascading taxation at different stages of production; (c) consolidate the tax administration; (d) activate the overall economy by mobilising more internal resources; and (e) bring a consistency in the tax-GDP ratio.

VAT introduced in Bangladesh in its initial form was a sort of consumption tax (by allowing purchase of capital goods as input), which extended its coverage up to the level of import, production or manufacture and service-rendering but not to export (which is zero-rated), wholesale or retail level. Since the financial year 1996-97, VAT in Bangladesh has become a broad-based consumption expenditure tax by covering the wholesale and retail levels. VAT is imposed on the following goods and services: all goods imported in Bangladesh except those mentioned in the First Schedule of the VAT Act; all goods supplied except those mentioned in the First Schedule of the VAT Act; and all services provided in Bangladesh except those mentioned in the Second Schedule of the VAT Act.

The standard tax rate for VAT has been fixed all along at 15% (for taxable goods and services). The adoption of truncated value-bases caused multiplicity of practical tax rates, but VAT rate is a single, flat or uniform one. The rate of turnover tax (TT) is also uniform at 4% (2% up to 11 June 1997). But the rates of supplementary duty (SD) are multiple. At the beginning (FY 1991-92), there were five different rates which ranged from 10% to 85%. Next rates were eleven in number and ranged from 5% to 350%. For FY 2000-01, there are 31 different rates that ranged from 2.5% as on coffee to 350% as on cigarettes.

The computation of actual value-addition requires detailed recording of payments for goods/services bought, which is not properly done in Bangladesh. To ease the administrative steps for taxation of services, in specified cases, a ‘truncated value-base’ was fixed with the option of waiving ‘input tax credit’. Under the VAT system, tax points depend on the stage of production and distribution. For goods imported by any importer, VAT is to be paid at the time of paying import duty under the Customs Act 1969.

For goods produced or manufactured or imported, purchased, acquired, or otherwise collected by any registered persons in the course of business operation or expansion, VAT is to be paid at the time of one of the following activities whichever occurs first: (a) when the goods are delivered or supplied; (b) when an invoice relating to the supply of goods is given; (c) when any goods are used personally or given for use to another person; and (d) when the price is received in part or full. For services rendered by any registered persons in the course of business operation or expansion, VAT is to be paid at the time of one of the following activities whichever occurs first: (a) when the services are rendered; (b) when an invoice relating to the rendering of service is given; and (c) when the price is received in part or full. For goods or class of goods for which the national board of revenue has ordered through the official Gazette notification to use stamp or banderole or special sign or mark having security system of specified value on package or carrier or container of the goods, VAT is to be considered as paid equivalent to the value of the stamp or banderole or special sign or mark used.

For services rendered by construction firms, indenting firms, travel agencies, motor garages and workshops, and dockyards and other services determined by the official Gazette notification, VAT is to be paid as withholding tax and VAT is collected, deducted and deposited by the receiver of the services or the persons paying the price or commission as the case may be. For any other goods and class of goods or services, VAT is to be paid at the time as indicated in the NBR rule.

Taxation remains a poor tool of government revenue collection in Bangladesh. Taxes to GDP (gross domestic ratio) ratios are usually not high in South Asia. But in case of Bangladesh the figure is alarmingly low – only a little higher than 9%, while the average for South Asian countries is 11%, the developing countries more than 15%, the industrialised countries 30%, and high income countries 24%. The introduction of VAT contributed significantly to raise the tax revenue collection in Bangladesh. The joint contribution of sales tax and excise duty to in the increase of total tax was Tk 696.9 million (28.8% of total increase) in 1979-80 and Tk 3.9 billion (44.8% of total increase) in 1989-90. In absolute volume, the annual increase in revenue from VAT and excise duty is more than the previous annual increase in revenue from sales tax and excise duty. However, in relative term, the share of sales tax and excise duty in total tax in the 1980s was almost similar to the share of VAT and excise duties in that under the VAT regime. The share of VAT as a per cent of different indicators (internal trade tax, external trade tax, indirect tax, total tax, total GDP and non-agricultural GDP) has usually an increasing trend and the shares are significant. On an average, around 75% of total tax come from indirect taxes, and more than a half of the indirect taxes is collected in the form of VAT. The scope of VAT mainly covers the ‘non-agricultural sector’ but with a standard tax rate of 15% the share of VAT as a percent of ‘non-agricultural GDP’ is only 3% to 4%.

VAT was introduced in Bangladesh as a consumption tax and allowed the full deduction of ‘machinery’ as an input from the ‘output value’ (sale proceeds of taxable goods and services) to compute the tax-base (i.e., value added). Although the initial coverage was up to import and production stages, the VAT-net is now expanded to wholesale and retail stages. Initially, the number of VAT taxable services were 25 (under 21 Heading numbers), but now the number is theoretically unlimited, although for practical purposes this number is kept limited to 70 services under 57 heading numbers for which the scope is defined. Goods other than primary unprocessed agricultural products and food items listed in the First Schedule of the VAT Act (live animals or poultry, human or animal hair, parts of animal body or animal products, parts of plant, green or dried vegetables, fruits, unprocessed spices, food items, oil seeds, natural gums or like products, wood, uncarded wool or cotton, and raw jute, etc) are subject to VAT. Thus almost the whole economy falls under the VAT-net and as a consumption tax, VAT is supposed to streamline the economic activities with corrective measures by applying supplementary duty.

Tax revenue Summary of Bangladesh

Bangladesh’s tax revenue income in the immediately past fiscal year ending in June fell short of target by around 1.19 percent as the world economic recession constricted imports growth, chopping off big slice of earnings from customs duties, officials said on Monday.

According to provisional statistics of the country’s National Board of Revenue (NBR), the board collected 523.71 billion taka ( about 7.48 billion US dollars) in tax revenues in the last 2008- 09 fiscal year (July 2008-June 2009).

Bangladesh’s total revenue collection target in the 2008-09 fiscal year was earlier set at 693.82 billion taka, of which the government set a tax revenue target of 545 billion taka.

Later on in May this year, the tax revenue target was reduced to 530 billion taka following a sluggish trend in earnings of import duties amid a volatile global economic situation.

Director (Research and Statistics) of the NBR, Sachindra Nath Sarker, said the fall in import duties was due mainly to decline in customs and supplementary duties, triggered by a big prices erosion of imported goods in the global market in context of financial tsunami.

The provisional statistics of the NBR, however, showed tax revenue earnings of the country was 10.41 percent higher than the collections in the previous 2007-08 fiscal year (July 2007-June 2008).

The South Asian country’s tax revenue income in the previous 2007-08 fiscal year stood at 474.35 billion taka, with nearly 27 percent growth over that of the 2006-07 fiscal year.

“We missed a large sum of customs and supplementary duties because of price fall of imported items,” a senior official in the customs department under the NBR said, requesting to be unnamed.

He said the NBR data showed the country’s tax revenue earnings growth steadily decelerated from 19.80 percent in the first quarter of 2008-09 fiscal year to 13.24 percent in the first half and 12.21 percent in the first nine months.

However, of three major revenue wings including income tax, customs and value added tax (VAT), the official said earnings from the customs department, which accounts for more than 40 percent of the NBR’s annual tax revenue collections, was 5.19 billion taka less than the revised target of 213.22 billion taka in last 2008- 09 fiscal year.

Apart from this, the provisional data showed earnings from VAT also fell short of target with around 4.55 billion taka in the last 2008-09 fiscal year, largely because of shortfall of supplementary duty collection.

The official of customs department said if the sliding trend in tax revenue collections continue, the government will face problem managing finance for its current 2009-10 fiscal year’s budget.

Bangladesh Parliament last month passed 1.14 trillion taka ( about 16.5 billion US dollars) national budget for the current 2009-10 fiscal year began from July 1.

The budget set a revenue earning target of around total 794.60 billion taka for current fiscal year. Of total, the tax revenue collection target for the country’s revenue board has been set at 610 billion taka. (1 US dollar equals about 70 taka)

Tax Expenditure

In recent years, analysis of tax expenditures has received much attention in the literature of public policy, particularly in the developing and transition economies. This policy note attempts to introduce the concept and size of tax expenditures in the context of Bangladesh with special

references to experiences of India and Pakistan. It shows that the amount of tax expenditures in Bangladesh is 2.52 per cent of GDP in FY05, in which expenditures in the direct taxes and indirect taxes are 0.28 per cent and 2.24 per cent, respectively. The note identifies that tax expenditure accounting is necessary to establish an efficient and effective tax system as well as fiscal accountability and transparency in the country, since tax expenditures are viewed as part of government expenditures. Thus, a detailed assessment of tax expenditures including an appropriate definition and a methodology for measuring ‘tax expenditures’ is essential along with restructuring the existing tax expenditure measures in Bangladesh.

Existing Tax Expenditure Measures in Bangladesh

The tax system of Bangladesh includes several tax expenditure measures under the broad headings of direct taxes and indirect taxes. These provisions, introduced with the enactment of the tax law, have been subject to changes from time to time. The major policy objectives behind the tax expenditure measures in Bangladesh are to accelerate the process of industrialization, to attract foreign currency through increasing exports and foreign direct investment (FDI) and to ensure social security and welfare of low and modest income groups. Tax expenditure measures exist in sectors such as Public Services, Agriculture, Labour and Employment Affairs, Transport and Communication and Social Security and Welfare, etc.

Tax Expenditure Measures under Direct Taxes

Various tax expenditure measures exist for corporate and personal income taxpayers under the existing income tax law. These are summarized below.

Corporate Income Tax

Tax holiday facility is allowed to newly set-up industrial undertakings, physical infrastructure facilities and tourism industry subject to certain specified conditions in order to promote industrialization and employment generation. Exemptions and deductions are applicable to incomes from firms in Export Processing Zone (EPZ), 50 per cent of income for export earnings, power generation companies, computer software businesses, agriculture-related industry, micro credit for NGOs, local government, welfare activities, etc. In particular, concessionary rate is allowed at the rate 20 per cent for those who do not enjoy tax holiday or accelerated depreciation, 15 per cent for textile and jute industries and 25 per cent for local authority, etc. Accelerated depreciation is allowed at the rate 100 per cent for new firms.

Personal Income Tax

Exemptions and deductions are admissible to individual incomes from agriculture-related activities, income of foreign technicians in EPZs, remuneration of diplomats and foreign employees of an embassy, income of an indigenous person of Hill Tracts region as individuals, income from specified savings instruments, etc. In addition, 15 per cent tax rebate is allowed on investment in provident fund, Deposit Pension Scheme (DPS), insurance, shares, bonds, etc.

Tax Expenditure Measures in Indirect Taxes

Under the various acts of indirect taxes, exemptions and deductions are given in the area ofcustoms duty, supplementary duty and Value-Added Tax (VAT).

Customs and Supplementary Duty

Exemptions are granted to local industrial units of a few specific sectors, viz. EPZ enterprises,power generation companies, poultry and dairy farms, etc. Concessionary rates are applicable toagro-processing, textile and leather industry, educational institutions, hospitals, privilegedpersons, etc. Incentives are also given to those sectors, which are complying with the international and bilateral agreements and conventions.

Value–Added Tax

Goods and services exempted from VAT include food and agricultural products, animal products,poultry sector, agriculture inputs, basic services for living, social welfare services, culture relatedservices, finance and financial activities related services, transport services, personal services, etc.

Tax Rebate for investment

Rate of Tax Rebate:

Amount of allowable investment is either actual investment in a year or up to 25% of total income or Tk. 10,00,000/- whichever is less. Tax rebate amounts to 10% of allowable investment.

Types of investment qualified for the tax rebate are:

– Life insurance premium

– Contribution to deferred annuity

– Contribution to Provident Fund to which Provident Fund Act, 1925 applies

– Self contribution and employer’s contribution to Recognized Provident Fund

– Contribution to Super Annuation Fund

– Investment in approved debenture or debenture stock, Stocks or Shares

– Contribution to deposit pension scheme

– Contribution to Benevolent Fund and Group Insurance premium

– Contribution to Zakat Fund (Zakat: Islamic Tax)

– Donation to charitable hospital approved by National Board of Revenue

– Donation to philanthropic or educational institution approved by the Government

– Donation to socioeconomic or cultural development institution established in Bangladesh by Aga Khan Development Network

– Donation upto five lac to (1) Shishu Swasthya Foundation Hospital Mirpur, Shishu Hospital, Jessore and Hospital for Sick Children, Satkhira run by Shishu Swasthya Foundation, Dhaka, (2) Diganta Memorial Cancer Hospital, Dhaka, (3) The ENT and Head-Neck Cancer Foundation of Bangladesh, Dhaka; and (4) Jatiya Protibandhi Unnayan Foundation, Mirpur, Dhaka;

– Asiatic Society of Bangladesh;

– Muktijudha Jadughar;

Tax Withholding Functions

In Bangladesh withholding taxes are usually termed as Tax deduction and collected at source. Under this system both private and public limited companies or any other organization specified by law are legally authorized and bound to withhold taxes at some point of making payment and deposit the same to the Government Exchequer. The taxpayer receives a certificate from the withholding authority and gets credits of tax against assessed tax on the basis of such certificate.

Major Areas for Final Settlement of Tax Liability in Bangladesh

Tax deducted at source for the following cases is treated as final discharge of tax liabilities. No additional tax is charged or refund is allowed in the following cases:

– Supply or contract work

– Band rolls of hand made cigarettes

– Import of goods

– Transfer of properties

– Export of manpower

– Real Estate Business

– Export value of garments

– Local shipping business

– Royalty, technical know-how fee

– Insurance agent commission.

– Auction purchase

– Payment on account of survey by surveyor of a general insurance company

– Clearing & forwarding agency commission.

– Transaction by a member of a Stock Exchange.

– Courier business

– Export cash subsidy

Tax Holiday

Tax holiday is allowed for certain industrial undertaking, tourist industry and physical infrastructure facility established between 1st July 2008 to 30th June 2011 in fulfillment of certain conditions.

Who is entitled to a Tax Holiday?

Tax holiday is allowed to industries subject to the relevant rules and procedures set by the National Board of Revenue (NBR) for the following period according to the location of the establishment.

In Dhaka and chittagong Divisions (excluding 3 hill districts): 5 years. In other divisions (including 3 hill districts of chittagong Division): 7 years.

The period of such tax holiday will be calculated from the month of commencement of commercial production. The eligibility of tax holiday to be determined by the NBR and the time of the commencement of commercial production is certified by the respective sponsoring agencies. The industrial establishment should be registered under the companies Act. 1994.

Tax holiday facility can be availed by industries coming into commercial production within 30 June 2000 A.D.

Tax avoidance

Tax avoidance is the legal utilization of the tax regime to one’s own advantage, to reduce the amount of tax that is payable by means that are within the law. By contrast, tax evasion is the general term for efforts not to pay taxes by illegal means. The term tax mitigation is a synonym for tax avoidance. Its original use was by tax advisors as an alternative to the pejorative term tax avoidance. Latterly the term has also been used in the tax regulations of some jurisdictions to distinguish tax avoidance foreseen by the legislators from tax avoidance which exploits loopholes in the law.

Some of those attempting not to pay tax believe that they have discovered interpretations of the law that show that they are not subject to being taxed: these individuals and groups are sometimes called tax protesters. An unsuccessful tax protestor has been attempting openly to evade tax, while a successful one avoids tax. Tax resistance is the declared refusal to pay a tax for conscientious reasons (because the resister does not want to support the government or some of its activities). Tax resisters typically do not take the position that the tax laws are themselves illegal or do not apply to them (as tax protesters do) and they are more concerned with not paying for particular government policies that they oppose.

Public opinion on tax avoidance

Tax avoidance may be considered to be the dodging of one’s duties to society, or alternatively the right of every citizen to structure one’s affairs in a manner allowed by law, to pay no more tax than what is required. Attitudes vary from approval through neutrality to outright hostility. Attitudes may vary depending on the steps taken in the avoidance scheme, or the perceived unfairness of the tax being avoided.

In the judiciary, different judges have taken different attitudes. As a generalization, for example, judges in the United Kingdom before the 1970s regarded tax avoidance with neutrality; but nowadays they regard it with increasing hostility.

Taxes and economic growth

The formula for economic development and curing poverty is well known: Security of property rights, low taxes, reasonably free trade and stable and readily convertible currency — the economic policy that has been demonstrated to be highly successful in moving countries from third world to first world

In the past century there has been an enormous improvement in human well being, almost all of it from economic development, almost none of it from redistribution. The most extreme exercises in redistribution created gigantic suffering, and resulted in the murder of about a hundred million people.

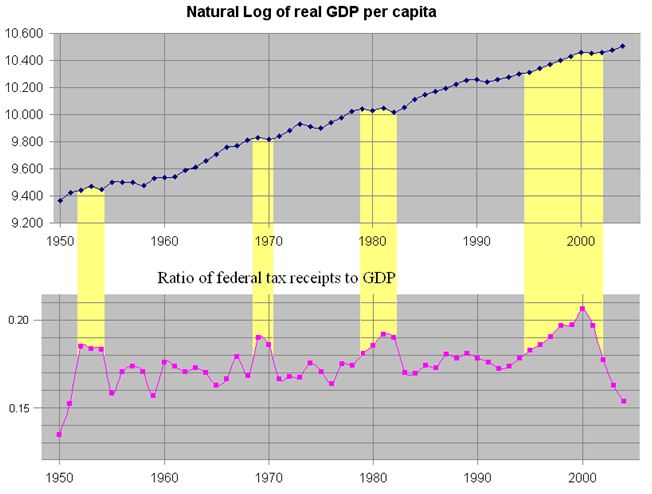

The question then is: Are taxes dangerously high in the advanced countries as well? Are taxes so high that cutting taxes will, in few years, increase the returns to the government? This is derided as “voodoo economics”, yet it is fairly obvious that ruinous taxation is a major part of why the third world is third world. Is then taxation also keeping the first world much poorer than it would otherwise be? For the United States, I defined “high taxes” as the federal government taking more than 18.1% of GDP, for during the Reagan Revolution, the archetype of “voodoo economics” the largest portion of GDP taken by the federal government was slightly more than 18%. Alternatively, I defined “a high taxes period” as any period where the federal government took substantially and persistently more than 18% of GDP.

I graph the natural log of GDP, rather than the actual GDP, so that you can read the growth rate directly from the slope of the graph: For example in 1983, first year of the Reagan tax cuts, log of GDP is 10.052, and in 1989, last year of the Reagan presidency, log of GDP is 10.250, so the log increased 0.198 in six years, 0.198/6= 0.033, so during those years GDP growth was 3.3% a year.

Average growth during high tax periods was 1.08%, average growth during normal times was 2.45%. Every high tax period was a long period of economic stagnation, malaise, or decline or else contained a long period of decline. Such events were rare during normal tax periods.

The graph suggests that taxes are well and truly on the wrong side of the Laffer curve — that increasing taxes will lead to decreased revenue after a fairly short period — at least if federal taxes seize more than 18.1% of GDP

Of course, this depends on who you tax, which the data I had available do not reveal. I suspect that if you tax the poor good and hard with heavy taxes on petrol, beer, and cigarettes, like those wonderfully redistributive welfare states in europe, you can collect a lot more than 18.1% of GDP without the economy going down the drain, for such taxes will cause the poor to work harder, while progressive taxes are likely to cause the rich to go underground, or retire to house on a hill overlooking the Coral Sea, unless, like certain progressive European countries, you have a few little loopholes here and there so that you can get the political credit for soaking the rich, without actually soaking them so much as to sink the economy.

Growth for the first three high tax periods was negative – possibly because they were trying to soak the rich, unlike Clinton, possibly because they did not have the internet boom increasing their revenues and boosting growth, unlike Clinton, possibly because Clinton “ended welfare as we know it”, whereas the early high tax periods were great society taxes. We really need statistics giving a breakdown on who is paying taxes to distinguish between these possibilities. We also need statistics giving hints as to who is goofing off and going underground. In third world countries it is largely the poor who go underground, which is consistent with the conjecture that it was “ending welfare as we know it” that made the difference, but the Reagan experience suggests that what smacks down the economy is high taxes on the rich, who have the option of fleeing or retiring.