ORIGIN OF THE REPORT:

Internship means receiving practical training through attending particular work physically. Practically training means a way through which a person or a trainee can gather experience about the related subjects and be able to apply his theoretical experience in the field of real life action. Practical training is necessary to achieve complete knowledge about something. Internship program is actually a form of practical training.

As a student of MBA, major in Finance, internship is an academic requirement. For doing internship every student is required to work in a selected institution to enhance ones practical knowledge and experiences.

For my internship I was sent to the Investment Corporation of Bangladesh (ICB), under the supervision of MD SAJJADUR RAHMAN, Sr. Lecturer, Stamford University Bangladesh.

BACKGROUND OF THE REPORT:

I have got the opportunity to work in the Investment Corporation Bangladesh, as a part of the internship program. It was time for me to get real life experience. Having understanding this I decided to do my internship in renowned bank. Now days everybody wants to do there internship in private bank as they are performing well. As I came to know that ICB is an equity financer for the corporate investors and only disburse long term finance, and play a vital role in capital market, I decide to do my internship in ICB.

OBJECTIVE OF THE REPORT:

The Objectives of the report are:

To fulfill the requirement of MBA program as necessitated by Business Administration Department, Stamford UniversityBangladesh.

To analyze the performance of ICB, it’s Image and its role in the capital market of Bangladesh.

- To know the institution as national level organization contributing to the economic development of the country.

- To relate our theoretical learning with the practical situation.

- To learn the practical aspect of the Investment Corporation of Bangladesh.

- To get aware about the working environment in advance that will help in adjusting a student with the future working life.

- To review the overall performance of ICB Mutual fund.

- To gather knowledge of how ICB floats and manages the Mutual Fund.

- To focus on the overall performance of the ICB Mutual Fund.

- To know the product of ICB at the securities market in Bangladesh.

- SCOPE OF THE REPORT:

The scope of the report was basically the operations and practices of Investment Corporation of Bangladesh, in which I had undertaken the internship program. The scope of the study was in the organization, Investment Corporation of Bangladesh (ICB). The study was confined only on the Head office and gave more concentration on it. The data comparison was based on published information and an additional survey was performed to get in-depth information, as it was the part of the objective of the report. The empirical part included only published information and current practices of Investment Corporation of Bangladesh.

SOURCES AND METHODS OF DATA COLLECTION:

For the purpose of preparing this report, I have carefully observed all of the departments of ICB and got some information from the responsible officers at certain department. Sources of data collection are as follows:

Primary sources:

Primary sources data are those, which are collected from face to face discussion with the help of the officials of various departments of ICB in charge.

Secondary sources:

Secondary sources of data include:

Ordinance of ICB.

Annual reports of ICB.

Daily Newspapers, journals and books & various write up of Economic & Business.

Research Library.

Monthly review of DSE & CSE.

General Information.

Materials & documents of ICB.

Bangladesh Bureau of Statistics.

LIMITATIONS OF THE REPORT:

Limitations are obvious in any study so do here. Since this is an internship report, the limitations regarding the internship program has acted as the limitations of the study. In spite all these limitations I have tried to put in our efforts as far as possible. Among others the main limitations are:

Secrecy of the official’s.I had to go to almost every Department of ICB as part of the Internship program. There is a very short span of time to get in-depth knowledge about a massive organization like ICB.

Officials of ICB maintain a very busy schedule. So they were not always able to provide enough time to enlighten the internee students every time, even if they had the intention to do so. Data summarizing from description contain the chance of being vague.

Chapter -2

Overview of

Investment Corporation of Bangladesh (ICB)

BACKGROUND OF ICB:Investment Corporation of Bangladesh (ICB) is a statutory corporation. It is mainly an investment bank. As an investment bank is a financial institution, which mobilized fund from the surplus economic units by savings securities and developed funds to the deficit economic unit also by buying/underwriting securities. After Liberation in view of social economic changes, the scope for private sector investment in the economy was kept limited by allowing investment in projects up to taka 25 lacks. The new investment policy, which was announced in July, 1972 provides for an expanded role of private sector by allowing investment in a project up to taka 3 crores. The ceiling has further being raised to taka 10 crores in spite of the adequate facilities and incentives provided to the private sectors encouraging response was not for the coming. One of the reasons among other was the lack of institutional facilities, which provides underwriting support (Lick former ICB) to industrial enterprise that was required to raise much need equity fund. Thus, the need for reactivation for capital market, stock market was keenly felt.

The Investment Corporation of Bangladesh (ICB) was established on 1 October 1976, under “The Investment Corporation of Bangladesh Ordinance, 1976” (no. XL of 1976).The establishment of ICB was a major step in a series of measures undertaken by the Government to accelerate the pace of industrialization and to develop a well-organized and vibrant capital market particularly securities market in Bangladesh.ICB caters to the need of institutional support to meet the equity gap of the companies. In view of the national policy of accelerating the rate of savings and investment to foster self-reliant economy, ICB assumes an indispensable and pivotal role. Through the enactment of the Investment Corporation of Bangladesh (Amendment) Act, 2000(no. 24 of 2000), reforms in operational strategies and business policies have been implemented by establishing and operating subsidiary companies under ICB.

OBJECTIVES OF ICB:

- Ø To encourage and broaden the base of investment.

- Ø To develop the capital market.

- Ø To provide for matters ancillary thereto.

- Ø To mobilize savings.

- To promote and establish subsidiary companies for business expansion.

BUSINESS POLICY OF ICB:

- Ø To act on commercial consideration with due regard to the interest of industry, commerce, depositors, investors and to the public in general.

- Ø To provide financial assistance to projects subject to their economic and commercial viability.

- Ø To arrange consortium of financial institutions including merchant banks to provide equity support to projects and thereby spread the risk of underwriting.

- Ø To develop and encourage entrepreneurs.

- Ø To diversify investments.

- Ø To induce small and medium savers for investment in securities.

- Ø To create employment opportunities.

- Ø To encourage Investment in IT sector.

- Ø To encourage Investment in joint venture capital/project.

BASIC FUNCTIONS OF ICB:

- Ø Direct purchase of shares and debentures including Pre-IPO placement and equity participation.

- Ø Providing lease finance to industrial machinery and other equipments singly or by forming syndicate.

- Ø Underwriting of initial public offering of shares and debentures.

- Ø Underwriting of right issue of shares.

- Ø Managing investors’ Accounts.

- Ø Managing Open End and Closed End Mutual Funds.

- Ø Operating on the Stock Exchanges.

- Ø Providing investment counsel to issuers and investors.

- Ø Participating in Government divestment Program.

- Ø Participating in and financing of, joint-venture projects.

- Ø Introducing new business products suiting market demand.

- Providing Consumer Credit.

- Ø Providing Bank Guarantee.

- Ø To act as Trusty and Custodian.

- Ø Dealing in other matters related to capital market operations.

CAPITAL STRUCTURE:

The Capital structure as on 30 June 2010 was as follows: (Tk. In crore)

ICB | Consolidated(ICB & Its Subsidiaries) | |||||

| Particulars | 2010 | 2009 | Increase/decrease (%) | 2010 | 2009 | Increase/decrease (%) |

| Paid-up capital | 200.00 | 100.00 | 100.00 | 200.00 | 100.00 | 100.00 |

| Reserves | 176.61 | 164.61 | 7.29 | 213.56 | 185.56 | 19.09 |

| Retained profit | 222.25 | 128.08 | 73.52 | 413.61 | 242.50 | 70.56 |

| Long-term govt. loan | 3.50 | 3.85 | -9.09 | 3.50 | 3.85 | -9.09 |

| Debentures | 11.80 | 21.80 | -45.87 | 11.80 | 21.80 | -45.87 |

| Others | 10.60 | 12.07 | -12.18 | 26.89 | 15.98 | 68.27 |

| Total | 624.76 | 430.41 | 45.15 | 869.36 | 569.69 | 52.60 |

Figure: Capital structure as on 30 June 2010 of ICB (represent Tk. In crore)

SHAREHOLDING POSITION:

Shareholders | No. of Shareholders | No. of Shares | Percentage of Shareholdings |

| Government of Bangladesh | 1 | 5400000 | 27.00 |

| State owned commercial banks | 4 | 4545400 | 22.73 |

| Development financial institutions | 1 | 5126200 | 25.63 |

| Insurance corporation | 2 | 2471124 | 12.36 |

| Denationalized Private commercial banks | 2 | 1817050 | 9.08 |

| Private commercial banks | 7 | 5700 | 0.03 |

| Mutual Fund | 1 | 15900 | 0.08 |

| Other institutions | 72 | 55688 | 0.28 |

| General public | 1204 | 562938 | 2.81 |

| Total | 1294 | 20000000 | 100.00 |

Figure: Share holding pattern as on 30 June 2010

SHARE PRICE:

Market price of a share of ICB of Tk. 100 each varied from lowest Tk. 2170.5 to highest Tk. 5700.0 on the stock exchanges during the year. As on 30 June 2010, the market price of an ICB share was Tk. 4991.75 on DSC and Tk. 5020.0 on CSE.

TRANSFER OF SHARES:

The volume of shares transferred increased substantially during the year. A total of 665 shares were transferred during 2009-10 as against 99987 shares in 2008-09.

ACHIEVEMENTS OF ICB DURING 2009-10: (Tk. In crore)

| Particulars | Consolidated position(ICB & its subsidiaries) | Growth (Percentage) | |

2009-10 | 2008-09 | ||

| Income | 724.19 | 461.81 | 56.82 |

| Net profit | 305.67 | 165.83 | 84.33 |

| Earnings per share(Tk.) | 152.84 | 82.92 | 84.33 |

| Book value per share(Tk.) | 424.25 | 536.14 | -20.87 |

| Return on Equity(percentage) | 36.95 | 31.40 | -17.68 |

| Return on Investment(percentage) | 36.28 | 29.95 | 21.24 |

| Net profit to total income (%) | 42.21 | 35.91 | 17.54 |

| Dividend Yield(percentage) | 0.80 | 4.24 | -81.13 |

| Dividend Payout Ratio(%) | 26.17 | 63.32 | -58.67 |

| Price earnings ratio(times) | 32.66 | 14.94 | 118.61 |

| Debt-Equity ratio | 2 : 98 | 5 : 95 | |

| Capital Adequacy ratio | 40.47 | 27.96 | 44.74 |

| Value Added | 537.65 | 384.67 | 39.77 |

| Transaction of securities | 12435.32 | 5424.63 | 129.24 |

| Dividend performance(Tk.) | |||

| ICB | 15% cash,1B:4 | 5% cash, 1B:1 | -61.90 |

| ICB Capital Management Ltd. | 1B:5 | 3B:10 | -33.33 |

| ICB Asset Management company ltd. | 5% cash, 3B:4 | 3B:5 | 33.33 |

| ICB Securities Trading Company Ltd. | 2B:1 | 1B:1 | -50.00 |

| ICB Unit Fund | 26.00 | 22.00 | 18.18 |

| First ICB Mutual Fund | 400.00 | 310.00 | 29.03 |

| Second ICB Mutual Fund | 200.00 | 95.00 | 110.53 |

| Third ICB Mutual Fund | 140.00 | 85.00 | 64.71 |

| Fourth ICB Mutual Fund | 125.00 | 80.00 | 56.25 |

| Fifth ICB Mutual Fund | 100.00 | 56.00 | 78.57 |

| Sixth ICB Mutual Fund | 75.00 | 37.00 | 102.70 |

| Seventh ICB Mutual Fund | 70.00 | 35.00 | 100.00 |

| Eighth ICB Mutual Fund | 65.00 | 32.00 | 103.13 |

| ICB AMCL First Mutual Fund | 50.00 | 35.00 | 42.86 |

| ICB AMCL Unit Fund | 30.00 | 25.00 | 20.00 |

| ICB AMCL Islamic Mutual Fund | 35.00 | 25.00 | 40.00 |

| ICB AMCL Pension Holders’ Unit Fund | 28.00 | 24.00 | 16.67 |

| ICB AMCL First NRB Mutual Fund | 35.00 | 24.00 | 45.83 |

| ICB AMCL Second NRB Mutual Fund | 22.00 | 12.50 | 76.00 |

| Prime Finance First Mutual Fund | 1.25 | – | – |

| ICB AMCL Second Mutual | 14.00 | – | – |

| ICB Employees Provident Mutual Fund One: Scheme One | 1.15 | – | – |

| Prime Bank First ICB AMCL Mutual Fund | 1.00 | – | – |

FINANCIAL RESULTS:

Total Income:

In 2009-10 ICB earned a total income of Tk.527.62 crore as compared to Tk.364.21 crore earned in 2008-09 showing an increase by 44.87 per cent. The major heads of income of ICB were interest income, capital gain, dividend income and income from fees and commissions. During 2009-10 income from all heads excepting interest income went up substantially compared to those of the previous year. Of the total income of Tk.527.62 crore, the highest income being the capital gain of Tk.262.9 crore (49.83 %) followed by interest income of Tk.194.85crore (36.93 %),dividend and interest income on securities of Tk.36.55 crore (6.93%), fees and commissions of

Tk.30.27 crore (5.74 %) and Tk.3.05 crore (0.57 %) as income from other sources. Due to efficient management of the portfolio and favorable market condition income from capital gain stood at Tk.262.9 crore in 2009-10, which was 123.63 % higher than the capital gain of Tk.117.56 crore of the previous year. Divided income increased due to satisfactory dividend performance of maximum companies.

Total expenditure:

During 2009-10, the total expenditure amounted to Tk. 314.57 crore as compared to Tk. 252.58 crore in 2008-09 showing a decrease of 24.54% over the previous year. The major heads of expenditure were: interest expense of Tk. 157.71 crore which was Tk. 172.85 crore in the previous year, showing a decrease by 8.72 %. Other operating expense was Tk. 29.78 crore compared to Tk. 21.32 crore in 2008-09, registering an increase by 39.68%. Through the other operating expense was 39.68% higher than that of the previous year, it was 19.43% lower than the budgeted amount of Tk.36.96 crore as a result of various measures undertaken by the management to contain costs. During the year, provision of Tk.2.02 crore was provided against loans and advances. In addition, Tk.100.0 crore has been set aside against future diminution in the value of marketable securities held in the own portfolio, possible fluctuation of stock market indices and present booming market condition.

Gross Profit:

The gross profit before provision and tax was Tk.340.07 crore in 2009-10 compared to Tk/170.04 crore in 2008-09, showing an increase of 99.99% over last year

Net profit:During 2009-10, ICB’s net profit after tax increased to Tk. 213.05 crore from Tk. 111.63 crore in 2008-09, showing an increase of 90.85 percent.

Dividend:The Board of directors of ICB recommended cash dividend as the rate of Tk. 15.00 per share and 1:4 stock dividend for 2009-2010. Cash dividend of Tk. 5.00 per share and 1:1 stock dividends were paid in the previous year.

Appropriation of Profit:

The Board of Directors of ICB recommended appropriation of Tk. 222.25 crore which includes net profit of Tk. 213.05 crore of 2009-10 and retained profit of Tk. 9.2 crore of the previous year and others in the manner:

Figure: Appropriation of profit of 2009-10 (crore)

Statement of Financial Results and some key financial ratios:

| Particulars | ICB | Increase/decrease (percentage) | |

| 2009-10 | 2008-09 | ||

| Financial Results: | |||

| Total income ( tk. In crore) | 527.62 | 364.21 | 44.87 |

| Total expenses (tk. In crore) | 314.57 | 252.58 | 24.54 |

| Profit before provision (tk. In crore) | 340.07 | 170.04 | 99.99 |

| Provision made (tk. In crore) | 127.02 | 58.41 | 117.46 |

| Net profit (tk. In crore) | 213.05 | 111.63 | 90.85 |

| Financial ratios: | |||

| Net profit to total income( percentage) | 40.38 | 30.65 | 31.75 |

| Return on total investment( percentage) | 34.69 | 26.76 | 30.02 |

| Return of equity( percentage) | 35.58 | 28.43 | 25.15 |

| Earning per share (Tk.) | 106.52 | 111.62 | -4.58 |

| Book value per share (Tk.) | 302.50 | 397.29 | -23.86 |

| Dividend yield (percentage) | 0.80 | 4.24 | -81.13 |

| Dividend Payout ratio (percentage) | 37.55 | 94.06 | -66.08 |

| Price earning ratio(times0 | 46.86 | 22.20 | 66.04 |

| Current ratio | 1.22 | 1.07 | – |

| Debt equity ratio | 3:97 | 6:94 | – |

| Capital Adequacy Ratio(%) | 37.25 | 28.20 | 32.09 |

ICB’S ROLE IN THE SECURITIES MARKET:

ICB has been one of the architects of the capital market, particularly the securities market in Bangladesh. ICB undertakes diverse activities with the objectives of quickening the pace of industrialization on the one hand and on the other hand, bolster the capital market. ICB and its three subsidiary companies play impressive roles in maintaining a buoyant and sustainable capital market in the country. In this regard ICB participates both in primary and secondary markets. As on 30 June 2010, the number of ICB assisted securities was 139 out of 279 listed securities (excluding 171 Govt. treasury bonds) of Dhaka Stock Exchange Ltd. Out of 232 listed securities of Chittagong Stock Exchange were 100.

In the reporting year, through the purchase and sale of securities for ICB’s investment portfolio, unit fund and mutual funds portfolios and on behalf of investment account holders ICB made significant contribution In maintaining depth, stability, reliability and liquidity of the stock market. During 2009-10 the total trading of ICB and its subsidiary companies in both the bourses was Tk. 12435.32 crore which was 129.24 percent higher than the previous year. In the reporting year, ICB and its subsidiary companies contribution to total turnover of Tk. 277870.91 crore of both the bourses was 4.48 percent which was 5.32 percent in the preceding year. As the rate of contribution of ICB and its subsidiary companies to total turnover of both the bourses has increased, simultaneously the transaction volume has increased significantly during the year.

The activities pertaining to merchant banking, mutual fund operations and stock brokerage functions by the three subsidiary companies of ICB, namely ICB Capital Management Ltd.ICB Asset Management Company Ltd. and ICB Securities Trading Company Ltd. has been remarkable during the year. During the year, all the mutual funds and unit funds managed by ICB Asset management Company Ltd. a subsidiary of ICB declared much higher dividend over 2008-09. ICB motivates companies to float bonds in the securities market. Up to 30 June 2010, 11 bonds of 8 companies of Tk.1007.95 crore have been floated of which one is a listed corporate bond. Ten out of these eleven bonds were floated under trusteeship of ICB.

ICB has taken steps to float two sectoral mutual funds of Tk. 500.0 crore each mainly to develop the power sector of the country. The decision was taken in a Board meeting held on 13 April 2010.

MILESTONES OF ICB:

Particulars | Date of Establishment |

| ICB | 1 October 1976 |

| Investors’ Scheme | 13 June 1977 |

| ICB Chittagong Branch | 1 April 1980 |

| First ICB Mutual Fund | 25 April 1980 |

| ICB Unit Fund | 10 April 1981 |

| ICB Rajshahi Branch | 9 February 1984 |

| Second ICB Mutual Fund | 17 June 1984 |

| Third ICB Mutual Fund | 19 May 1985 |

| ICB Khulna Branch | 10 September 1985 |

| ICB Sylhet Branch | 15 December 1985 |

| Fourth ICB Mutual Fund | 6 June 1986 |

| Fifth ICB Mutual Fund | 8 June 1987 |

| Sixth ICB Mutual Fund | 16 May 1988 |

| ICB Barisal Branch | 31 May 1988 |

| Nomination as the Country’s Nodal DFI in SADF | 7 May 1992 |

| Seventh ICB Mutual Fund | 30 June 1995 |

| Eighth ICB Mutual Fund | 23 July 1996 |

| ICB Bogra Branch | 6 October 1996 |

| ICB Local Office,Dhaka | 15 April 1997 |

| Purchase of Own Land & Building (Rajarbag) | 11 December 1997 |

| Participation in equity of SARF | 16 January 1998 |

| Advance against ICB Unit Certificates Scheme | 12 October 1998 |

| Lease Financing Scheme | 22 April 1999 |

| “The Investment Corporation of Bangladesh (Amendment) Act, 2000” | 6 July 2000 |

Commencement of operations of the Subsidiary Companies:

| Formation & Registration of Three Subsidiary Companies | 5 December 2000 |

| ICB Capital Management Ltd. | 1 July 2002 |

| ICB Asset Management Company Ltd. | 1 July 2002 |

| ICB Securities Trading Company Ltd. | 13 August 2002 |

| Registration as a Trustee with SEC | 20 August 2002 |

| Registration as a Custodian with SEC | 20 August 2002 |

| Bank Guarantee Scheme | 21 June 2003 |

| Advance Against ICB Mutual Fund /ICB AMCL Unit Certificates Scheme | 21 June 2003 |

| Consumer Credit Scheme | 15 February 2004 |

| Venture Capital Financing Scheme | 26 April 2007 |

| Purchase of own Land (Agargoan) | 3 March 2008 |

| Equity and Entrepreneurship Fund (EEF) | 1 June 2009 |

PRODUCTS OF ICB:

Private Placements:

ICB is authorized to act as an agent of the issuers and investors for private placements of securities. Under this arrangement, ICB places securities to individuals/institutions on behalf of the issuers for which it charges fees. ICB also acquires shares/securities for its own portfolio.

Trustee, Custodian and Issue Manager:

ICB is acting as trustee to the issue of debenture and securitized bonds. Up to 30 June 2009 ICB acted as trustee to the debenture issues of 17 companies involving taka 184.15 crore and issues of 7 bonds of 5 companies involving taka 624.36 crore. ICB also under took the responsibilities of trustee to 8 mutual funds involving taka 230.00 crore.

To act as the custodian to the public issue of open-end &closed-end mutual funds, ICB provides professional services. It also acts as banker to the issues and provides similar services through the network of its branches. Fees in this regard are negotiable. However, ICB has, under restructuring programme, discontinued issue management function since 2003.

Lease Financing:ICB extends lease finance mainly for machinery, equipment and transport. ICB has the capacity to provide professional advice and financial assistance to the prospective clients. The period of lease, rentals, charges and other terms and conditions are determined on the basis of type of assets and the extent of assistance required by the applicants. Since introduction of this scheme in 1999 good response has been received from the intending lessees.

Advances against ICB Mutual Fund Certificates Scheme:

Advance against ICB Mutual Fund Certificates Scheme was introduced in 2003, designed for the ICB mutual fund certificate holders to meet their emergency fund requirements. One can borrow maximum of 50 percent value of last one year’s weighted average market price of certificates at time of borrowing by depositing his/her certificates under lien arrangement from any of the ICB offices. The rate of interest on the loan is reasonable and also competitive.

Advances against Unit Certificates Scheme:

Advance against ICB Unit Certificates Scheme was introduced in 1998, especially designed for the ICB unit- holders to meet their emergency fund requirements. One can borrow maximum Tk. 85 per unit by depositing his/her unit certificates under lien arrangement from any of the ICB offices where from such unit certificates were issued. The rate of interest on the loan is reasonable and competitive.

Consumer Credit Scheme:

As part of business diversification program, ICB has introduced “Consumers Credit Scheme” in 2003-04 considering at the need of various household commodities of different employees of govt., semi-govt., autonomous bodies and some established private sector organizations. Under this scheme one can enjoy minimum Tk 1.0 lac but maximum 5 lac credit facilities. The rate of interest on the loan is reasonable and competitive which is fixed by the board of directors of ICB considering the bank rate and with the guidelines of Bangladesh Bank. Under this scheme the cumulative amount of loan disbursed up to 30 June 2010 was Tk. 10.95 crore. No amount has been disbursed during 2009-10

Venture Capital Financing:

With a view to encourage rapid industrialization of high risk but potential industries of the country ICB as part of business diversification has launched venture capital financing scheme. Up to 30 June 2010 ICB has received 5 applications for financing of Tk. 76.62 crore.

Equity and Entrepreneurship Fund (EEF):

The Government of Bangladesh (GOB) had set up an Equity Development Fund (EDF) in the budget 200-01 known as Equity and Entrepreneurship Fund (EEF) with a view to encouraging the investors to invest in the rather risky but promising two sectors, namely, software industry and food-processing/agro-based industry. Initially the management of the fund was vested to Bangladesh Bank. Subsequently a sub-agency agreement was signed between ICB and Bangladesh Bank on 1st June 2009. According to this agreement, the management of the fund has been devolved on ICB.

ICB Mutual Fund:Mutual Funds are also known as close ended Mutual Funds. The issued capital of a Mutual Fund is limited, that is, a Mutual Fund offers a limited number of certificates for sale to the public. The amount of capital and the number of certificates of each Mutual Fund remains unchanged. ICB Mutual Funds are independent of one another. A Mutual Fund being listed is traded on the Stock Exchanges. Price of Mutual Fund certificates after IPO is determined on the Stock Exchanges through interaction of supply and demand. The market price of a Mutual Fund certificates is available in Stock exchange quotations and in newspapers.

ICB Unit Fund:ICB Unit Fund was established on April 10, 1981. Its main objective is to mobilize savings through sale of its units to small investors and invest these funds in marketable securities. The schemes provides a potential source of equity and debt to industrial and commercial concerns and thus contribute to the industrial development of the country. Unit fund is an open ended Mutual Fund. It provides an opportunity to the unit holders to invest their funds in a well managed and diversified portfolio with a high degree of security of capital and reasonable yearly returns.

Investors’ Scheme:The Investors’ Scheme was introduced in 1977 with the objective of broadening the base of equity investment through mobilizing savings of small and medium size savers for investment in the securities market. In addition to Head Office, Investment Accounts are also operated at the 7 branch offices of ICB located at Dhaka, Chittagong , Rajshahi, Khulna , Barisal , Sylhet, and Bogra. However in view of strategic changes in policy reform, from 01 July 2002 ‘ICB Capital Management Ltd.’ started opening and managing investment accounts. ICB will continue to provide services to its existing accounts only.

Further steps were undertaken to enhance the quality and speedy service under the scheme like computerization of all activities and installation of merchandizing operation management software. This enables the management to offer better and

quick service to the investors including instant supply of the financial statement, portfolio, balance of the accounts, etc. Installation of telephone banking system in Investors’ Account enabling investors to collect information and operate their account over telephone was at the final stage of operations. Besides, installation of Electronic display system of DSE online trading on the floor of ICB was in progress.

Bank Guarantee Scheme:

ICB introduced Bank Guarantee scheme in 2002-03. ICB provides

- Bid Bond for enabling the business people to participate in any tender or bidding;

- Performance Bond for helping the business community to continue their business smoothly by fulfilling their obligations promised by them to their clients; and

- Customs Guarantee for solving different disagreements between the customs authority and the business classes at the initial stage. The maximum limit of guarantee is Tk. 2.00 crore and would be issued against at least 20% cash and 80% easily encashable securities or against 100% cash margin. Re-guarantee from other financial institution is required for guarantee against the amount exceeding Tk. 2.00 crore.

Managers and Acquisitions:

Companies willing to expand their business through mergers or acquisitions or to Disinvestment projects that no longer viable into present capacity of operation can contact the Corporation. ICB provides professional services & advices in respect of shaping up the cost and financial structures to ensure best possible operational results. Besides, in case of divestment, the corporation, through network and established business relationship, bring buyers and sellers together, help them to negotiate final agreement and advice on the emerging corporate structure.

Corporate Financial Advice:Government enterprises and Companies intending to go public issue often seek professional & financial advice on corporate restructuring & reengineering. ICB through its expertise provide such services through its expertise.

ICB’S ORGANIZATIONAL STRUCTURE AND MANAGEMENT:

Institutional Framework of ICB:

Investment Corporation of Bangladesh is a corporate body as per section 3 of Investment Corporation of Bangladesh Ordinance, 1976 and deemed to be a banking company within the meaning of the Banking Companies Ordinance, 1962 (L VII of 1962). The shares of corporation are listed with the stock exchange. ICB is an authorized broker of DSE.

Regulatory Framework of ICB:

As the mentioned earlier the regulatory framework of ICB is the, Investment Corporation Bangladesh Ordinance, 1976. This ordinance and regulations laid under the authority of the ordinance is the source of all power and authority of ICB. Through the recent enactment of “The Investment corporation of Bangladesh (Amendment) Act, 200” (XXIV) of 2000, scope of ICB’s activities through the formation of subsidiaries have been expanded. In addition to these, to resume its duties and functions, it has to compel by Companies Act 1994, Trust Act 1882, Insurance Act 1983, Security and exchange commission Act 1993, banking companies Act 1993, Foreign exchange regulation 1974, Income Tax act etc.

It is to note that no provision of law relating to the winding up of companies or bank shall apply to the corporation and the corporation shall not be wound up save by order of the government and in such manner as it may direct.

Management of ICB:

The head office of the corporation as per the requirement of the ordinance of ICB is located at Dhaka. The general direction and superintendence of the corporation is created in a board of directors, which consist of 12 persons including the chairman and managing director of ICB. The board of directors consists of the following directors:

The chairman to be appointed by the government.

The directors to be appointed by the government from among persons serving under the government.

One director to be nominated by the Bangladesh Bank.

Four other directors to be elected by the share holders other than the government, BB, BSB, & BSRS.

The managing directors of ICB to be appointed by the government. The board in discharging its functions acts on commercial consider rations with due regard to the interests of industry and commerce, investment climate, capital market, depositors, investors and to the public interest generally and is guided in question policy by the institutions, if any, given to by government which shall be sole judged as to whether a question is a question of policy or not.The managing director is the chief executive of the corporation. The corporation has an executive comprised of 5 people including managing director.

Administration & Human Resource:

Investment Corporation of Bangladesh (ICB) is providing different category of financial and banking services. Nature of the different division departments vary, such that Economic and Business Research (EBR) department requires teamwork, Lone Appraisal division requires professional work. Funds divisions need chain work. Managing director is entrusted with authority to transact the regular business of the organization; he may delegate some authority to officials of the Corporations. However, most of the policy decisions are taken by the different committee with the approval of managing director and where required of the board. it is the discretionary authority of the board to constitute the execute committee and to maintain its Chairman to assist the board in the discharging of the function stated under the ordinance. The board may appoint such other committee (s) as it thinks fit to assist it in the efficient discharge of its function. So far, board has appointed two such committees. Economic and Business Research (EBR) committee and Loan Appraisal committee is headed by General Manager.

Organization Manpower:

During 2009-10, 10 officers and 20 supporting staff joined services of the Corporation at different levels. Moreover, recruitment of 60 officers was under process. On the other hand 5 officers resigned and 1 supporting staff retired from the services of the Corporation. During the period, 9 employees including 2 supporting staff retired from the services of the Corporation and 1 employee died. As per direction of the government, the retirement age of the freedom fighters has extended by 2 years to 59 years. According to this direction retirement date of 5 employees of the Corporation has been extended. The total work force as on 30 June 2010 was 478 which was 464 on the same date of the previous year. Out of 478 employees, 290 were officers and 188 were supporting staff. The total number of female employees was 72 including 44 officers representing 15.06 per cent of the total manpower. During the year, 6 officers and 7 supporting staff of the Corporation were promoted at different levels

DEPARTMENT OF ICB:

Personal department:

The main functions of this department are:

- For making a well trained administration must me selected the rules and regulation.

- Appoints the manpower in the corporation.

- Transfer, selects the salary, pension vacation, promotion, confirm the job, etc are the personnel related works.

- Processing the promotion, time scale, vacation related works.

- Processing the retirement.

- Personnel’s give the facilities when they are going on retirement such as–gratuity, pension, provident fund are processed and control the attendance.

- To maintain the national salary scale, select the salary, pension, increasing the annual salary etc.

- The function which are related with the annual secret reports of the personnel’s.

- Function of personnel discipline.

- Take short term and long term development planning for the executive of a corporation.

- Maintained the relation with the ministry.

- Functions which are all related with the officers union.

- According to need, others functions which are given by administration.

Human Resources department:

The main functions of this department are:

- To give and complete the different steps of training for the officers/personnel’s in the corporation.

- Inventing the foreign training and organize the training in the foreign countries.

- To organize the internal training for personnel.

- To organize the training for new appointed personnel.

- To maintain the official training center.

- To organize the seminar/workshop, symposium, if needed take specialist.

- To collect the training tools and give facilities of the trainee.

- To select the officer/personnel for attending the different type of important meeting, seminar and workshop.

- According to need, others function given by administration.

Establishment department:

This department deal with purchases of office supplies, office equipment etc, also maintain the utility services like telephone bill electricity bill etc. The cost of this department is divided into two categories revenue cost and fixed cost. For fixed cost, depreciation is charged at straight-line method basis.

There are two purchase committees to accomplish the purchase. There remains a quality control committee to examine the quality of the product purchased. For the purchase of the product, this department gives tender notice to the listed supplies. Quality control committee is formed with two Deputy General Manager (DGM), one Assistant General Manager (AGM) and members from the Establishment Department. In case of selling of scraps and wastage the tender offer in same way.

Secretary’s department:

The main functions of this department are:

Arrange meetings of the Board of Directors, Executive Committee and other Committee.

Communicate with the directors of the Corporation.

Call board meeting.

Prepare work schedule of directors meeting and collect signature of the Chairman.

Send work schedule to Govt. and board of directors.

Send decisions of the meetings for implementation of concerned department.

Maintain attendance registers of directors.

Preserve the registration of shareowners.

Share transfer, transmission, split, issue duplicate share and dividend warrant.

Call Annual General Meeting.

Select directors.

Send work schedule of AGM to Govt. and other directors of corporation.

Distribution of dividend to the shareowners.

Communicate with shareowners.

Public Relations department:

The main functions of this department are:

Maintain close liaisons with the Ministry of Finance and other concerned officers.

Help publish all types of official advertisements.

Furnish management with the relevant newspaper cuttings.

Help focusing ICB through mass media.

Meet all adverse comments about the Corporation published in Different newspapers and periodicals.

Publish internal newsletter or journal.

Appraise the management of its overall relation to public.

Any other matters as may be assigned by the management.

Shares department:

The department, subject to act as, a custodian of ICB portfolio and investors accounts. It maintains IPO shares, right shares, bonus shares and secondary shares. When sales order placed to the concern department, it needs to justify the physical existence maintain by four volts. As by rule, shares must be delivering within three days of transaction, but in some case fluctuation may be seen because of share’s transfer registration.

Securities Reconciliation department:

This department is involved in reconciliation of the securities if any discrepancy rises among the settle number of securities and the balance of the ledger. In case of sale concern department go through by the help of shares department for the conformation of physical existence of shares.

Dematerialization department:

The main functions of this department are:

Paper share converted to electronic share.

70-75 Companies share has completed to dematerialization.

Investor’s department:

The main task of Investors Department is to accumulate the investment of small and new investors of the capital market by helping them open an investment account in the concern department. This department deals with ‘Investors scheme’. The following are the main functions of this department:

Open and maintain Investment Accounts.

Sanction loans against deposits in Investment Accounts.

Buy and sale shares on behalf of the investors.

Counsel investors in respect of building up their portfolios.

Withdraw funds and shares from Investment Accounts.

Issue income tax certificates, portfolio statement, accounts statement etc.

Provide service to Investment Accounts Holder.

Keep financial records of all Investment Accounts.

Processing of withdrawal of funds.

Confirm fund position of individual accounts and

Posting of all transactions.

System Analysis department:

The main functions of this department are:

System administration of the entire network setup.

Performing system analysis wherever ICB feels the need for periodic change in computerization setup.

Performing miscellaneous small hardware and software related servicing tasks on the many workstations, network system, sever and other components and provide training to staff of other departments about computer usage.

Any other assignment given by the management.

Programming department:

The following are the main functions of this department are:

Developing new software for ICB.

Customizing the software developed in the present computerization phase according to the changes of the requirements of the ICB with time.

Provide active assistance to the staff of system analysis department for training of the staff of other department about computer usage.

Data Management department:

The following are the functions of this department are:

Handling peak load of data entry and data processing work for all other department of ICB.

Any other assignment given by the management.

Planning, Research & Business development department:

This department has a basic decision making function for the organization. The major functions of this department are:

To make the portfolio management decision in favor of the organization as well as small investors.

Conduct meeting of the securities purchase and sales committee.

Convey securities sales or purchase decision to the merchandising division.

Perform all activities related to South Asian Development Fund (SADF).

Management Information Systems department:

This department basically helps the organization in decision making by providing information. The main works of this department are:

Prepare and distribute Annual Report of ICB, Mutual Funds and Unit Funds.

Make arrangement for off loading of government portion of shares in different companies and state owned institutions.

Manage the business development cell, which is established to explore the possibility of business diversification.

Maintain liaison with ministry of finance, Bangladesh Bank and provide ICB related information to interested parties.

Securities Analysis department:

This department basically analysis the securities in the market and upcoming securities into the market. The basic task of this department is as follows:

Collect information about DSE, CSE, Public issue and half yearly accounts of the listed company.

Prepare 5 years performance appraisal reports of the listed companies.

Prepare board memo regarding declaration of divisions on ICB’s own portfolio, Unit and Mutual funds.

Central Accounts department:

All kinds of receipts and payments of ICB are done by the Central Accounts department. The bill of all departments end destination is account department. Account department holds and maintain all separately. For this reason adjustment and rectification of any transaction of all departments become easier to this department. The functions of this department are to:

Prepare income tax return and matters relating to accounts.

Prepare bills including projects accounts and maintenance of project accounts.

Prepare salary statement, overtime statements etc.

Prepare final accounts.

Keep accounts for Government loan and debentures.

Keep accounts of Unit and Mutual Funds.

Make correspondence with the Government, financial institutions, branches etc.

Maintain liaison with external audit and commercial audit.

Maintenance of investor’s accounts and portfolio ledgers.

Calculation of quarterly interests.

Posting and balancing of ledgers.

Furnishing of information to other departments related to Investor’s Scheme.

Determine sources of fund, rising of fund ensure proper utilization of fund.

Prepare fund flow statement of the corporation.

Ensure proper budgetary and cost control.

Take measure for controlling of expenditure.

Prepare annual budget of the corporation.

Fund management department:

The main works of this department are:

Manage overall fund of the corporation.

Different organization provided FDR

Different organization taken TDR

Projects Loan Account department:

This department presents up to date information about the project of the given loan from the organization. The functions of this department are:

Issue check to the projects after getting disbursement order from the Project Finance Committee.

Maintenance of registers for interest penal interest due and over dues.

Calculation of interest and preparation of periodical bills.

Preparation and dispatch of statement of accounts.

Furnishing of various information regarding disbursements, dues over-dues etc. relating to project loan.

Any other assignment given by the management.

Law department:

Law department is a specialized department; handle any kind of legal affairs of ICB. ICB takes the resource of legal actions against the defaulting borrowers who did not come forward to repay loans despite repeated persuasion and reminders. The functions of this department are as follows:

Prepare legal documents, advances agreement, share agreement, demand promissory notes, Memorandum and deposit of title deed etc.

Arrange exception of underwriting-cum-advance agreement, underwriting agreement and supplementary etc.

Process litigation cases, prepare legal notices and refer cases to legal advisor in the court.

Prepare necessary Board Memos for placement in the board meeting relating to litigation and legal affairs.

Handle the legal issues related to employee’s loan facilities and other issues related to law.

Punishment of staffs.

Documentation department:

The following are the main functions of this department are:

All important documents are kept.

Debenture finance.

Lease finance.

Asset securitization.

Equity/ Preferential share finance.

Audit and Methods department:

Department under Audit & Method department are showing in the following:

- Audit & Method head Office.

- Audit & Method Branches.

The main functions of this department are:

- Checking out that all rules are properly maintained or not i.e. circulars given by the ICB Board, Government and the method approved by the Board are correctly implemented or not.

- Advising of new method of ICB.

- This department finds out the fault done by other department.

Unit Repurchase department:

ICB unit is an open end Mutual Fund through which the small and medium savers get opportunity to invest their savings in a balanced and relatively low risk portfolio. It ensures a continuous and regularly flows of incomes for the holders and is easily cashable. Units are sold through ICB offices and other authorized bank branches. ICB stopped selling of Unit Certificates from 1st day of July after the business operation starts of ICB Asset Management Company Limited.

The main functions of this department are to sale, repurchase and transfer of Unit Certificate:

- Act as manager of Unit Fund.

- Promote sales of Unit Certificates.

- Sell and issue Unit Certificates to the applicants.

- Repurchase Unit Certificates.

- Issue new Unit certificates in lieu of mutilated, lost or defaced Unit Certificates.

- Reconcile the amount received and Unit Certificates send to the agents.

- Transfer the units if applied for the prescribed from.

- Split the units if applied for.

- Transmission of units in case of death of unit holder.

- Issue and distribution of Cumulative investment Plan (CIP) Certificates.

- Making of lien of units, if necessary.

Unit Registration & Procurement department:

The following are the functions of this department:

- Registration and transfer Unit Certificates.

- Maintain a separate register of unit holder under Cumulative investment Plan (CIP).

- Verify signature of transfer deed.

- Issue dividend warrants and CIP certificates to the holders.

- Procure Unit Certificates of various denominations from the printing press.

- Issue Unit Certificates to ICB sale officers/branches as well as appointed bank branches.

- Co-ordinate all activities relating to procurement and issue of Unit Certificates.

Mutual Fund department:

Investment Corporation of Bangladesh (ICB) has so far floated eight close and Mutual Funds. The first Mutual Fund was floated on 25th April 1980 while the eight ICB Mutual Fund was floated in 10th August 1996.

Broadly the functions of Mutual Funds department consist of:

- Act as manager of all Mutual Funds.

- Maintenance of ledger with the name, address and number of certificates along with distinct folio number for each Mutual Fund separately.

- Verify the signature of the holder in the 117 forms.

- Preparation of dividend list from the ledger position.

- Issue dividend warrants to the holders of the certificates.

- Distribution of final dividend warrants to the certificate holders after completing necessary formations.

- In case of change of ownership of Mutual Funds certificate holder facilities the transfer process.

- Make arrangement for re-issue or duplicate copy of certificate in case of loss or damages of certificates.

- Receiving application for the change of address, correction of names and forwarding the same to the computer department.

- Arrange for splitting the share scraps as and when necessary in accordance with the Stock Exchange Rules.

- Arrange for revalidating the date of payment of dividend on Dividend Warrants.

Project Implementation & and follow-up department:

The following are the tasks of this department:

Placement of IPO.

Justify the projects terms and conditions.

Help implementation of sanctioned projects.

Review progress of implementation of projects and recommend disbursement of funds.

Submit progress reports to the management regarding implementation.

Process the case for cancellation of sanctioned projects.

Inspect the site and books of accounts of projects

Make recommendations for additional loans in appropriate cases and refer them to LDA.

Provide counseling for solution of any disputes and problems.

Inspire the project to go for public as far as possible after commercial operator.

Contract with the consortium member/main financer regarding implementation of the projects.

Take necessary steps to re-arrange the consortium commitment during implementation period if necessary.

Recovery Department:

Loan recovery and follow-up department is the key operation as it ensures the recovery of funds provided as credit. There remains two ‘Task forces’ and the ‘Review & Monitoring Committee’ for giving necessary guidelines for accelerate process of recovery.

The main functions of this department are:

To provide and reconcile statements of dues /over dues periodically.

To visit projects for evaluating operational performances.

To hold meeting with sponsors of ICB financed projects in connection with recovery of dues.

To furnish status reports on the sponsors of ICB assisted projects to different institutions.

To ensure recovery of dues /over dues from sponsors.

To recommend for making necessary provisions for bad and doubtful debts in the Annual Accounts of the Corporation.

To prepare memorandum for consideration of the Board of Directors for granting financial relief to projects facing various problems.

Analyze the problem of sick projects and put forward suggesting for salvation of the same.

Assist the Law Department of the Corporation to take legal actions against defaulting projects.

To furnish information to different departments of ICB regarding recovery of loans.

Trustee department:

The main functions of loan appraisal departments are:

One of the most important works is to save the self-keeping of the investor, bond holder, Debenture holder.

To reserve the resources of the trustee.

To maintain the account of trustee.

To give the monthly report in the SEC which are related to the trust maintaining

The savings money of the trustee is invested for short term.

Public Issue department:

The public issue department is a vital department in the ICB as the ultimate objective of sanction loan is to help the project to go for public issue. The department is engaged in:

Visit and collect audited financial statement from the sponsors.

Analyzing the financial statement of ongoing projects.

Advice and pursue sponsors of ongoing projects.

Assists in preparing prospectus for issuing shares and debentures.

Examines the prospectus submitted by the sponsors and help getting approval.

Advise companies in issuing allotment letters and warrants.

Make necessary adjustments of bridge loan of the concerned company.

Make liaison with the recovery and follow-up department regarding realization of dues and overdue.

Help the company in securing approval from relevant institution.

Other functions assigned by the management.

Venture Capital Department:

With a view to encourage rapid industrialization of high risk but potential industries of the country ICB as part of business diversification has launched venture capital financing scheme. Up to 30 June 2010 ICB has received 5 applications for financing of Tk. 76.62 crore.

Equity and Entrepreneurship Fund (EEF) Department:

The Government of Bangladesh (GOB) had set up an Equity Development Fund (EDF) in the budget 200-01 known as Equity and Entrepreneurship Fund (EEF) with a view to encouraging the investors to invest in the rather risky but promising two sectors, namely, software industry and food-processing/agro-based industry. Initially the management of the fund was vested to Bangladesh Bank. Subsequently a sub-agency agreement was signed between ICB and Bangladesh Bank on 1st June 2009. According to this agreement, the management of the fund has been devolved on ICB.

Branch Affairs Department:

Organizations and Methods Department:

The main functions of this department are given bellow:

To prepare organizational manual of corporation.

To prepare systematic manual of corporation.

To prepare operation manual of corporation.

To maintain and coordinate of the directions and information’s regarding corporations policy decisions.

To reform, correct and extension of corporate existing manuals of different sections.

To select the system of administration of corporate different schemes.

To take permission and to inform the authority regarding the correction, extension and changing the list of instruments and the organization chart.

Any other assignment given by the management.

Appraisal Department:

Basic main function of the Appraisal Department- Issues Pre-IPO placement different companies securities, advanced against equity, invest to debenture, buy preference share, invest to bond and trustee of the debenture and bond issue, trustee of the mutual fund and custodian, arrange the share and debenture issue, bank guarantee etc.

Lien and Consumers Credit Department:

As part of business diversification programme ICB has introduce Consumer Credit Scheme in 2003-04 to meet the needs of various household appliances of different professionals of govt., semi-govt., autonomous bodies and some established private sector organizations. Under this scheme one can enjoy minimum of Tk. 10 lac but maximum of Tk. 5 lac credit facilities. The rate of interest on the loan is reasonable and competitive.

Leasing Department:

ICB extends lease finance mainly for machinery, equipment and transport. ICB has the capacity to provide professional advice and financial assistance to the prospective clients. The period of lease, rentals, charges and other terms and conditions are determined on the basis of types of assets and the extent of assistance required by the applicants. Since introduction of this scheme in 1999 good response has been received from the intending lessees.

Custodian Department:

To ace as the custodian to the public issue of open-end & closed-end mutual funds, ICB provides professional services. It also acts as banker to the issues and provides similar services through the network of its branches. Fees in this regard are negotiable.

Loan Appraisal Department:

ICB provide credit facilities to the public limited companies to meet heir equity gap. There are two modes by which ICB provides credit facilities to the public limited companies through:

- Direct underwriting for BMRE

- Underwriting through bridge financing.

The main functions of loan appraisal departments are:

Received investment proposal from sponsors.

Place appraisal reports the board.

Apprise management on technical aspect of the projects.

Prepare appraisal reports on project appraisal committee.

Issue sanctions letters to the projects.

Conduct meeting of the project appraisal committee.

Maintains liaison with commercial banks or financial institutions or Ministry or agency.

To develop capital market.

Placement of share and debenture.

Participating in bond financing.

Act as trustee on debenture on behalf of the bondholder.

Subsidiary Affairs Department:

ICB Capital Management Limited (ICML):

ICB Capital Management Limited started its journey as a subsidiary company of ICB on July 1, 2002. the authorized and paid-up capital of ICML as on 30 June 2010 stood at Tk. 100.0 crore and Tk. 58.5 crore respectively.

ICML has been playing an important role in the development of capital market by carrying out the functions of underwriting public issue of securities, portfolio management, issue management and management of investment accounts with the objectives to help mobilize savings and encourage and broaden the base of investment. The Company has emerged as one of the fastest growing merchant bank in the country.

Up to 30 June 2010, the amount of deposits received and net investments made against 27975 investor’s operated by the Company stood at Tk. 788.80 crore and Tk. 6382.98 crore respectively. The company underwrote the issues of shares and debentures of Tk. 396.11 crore fo 82 companies and assumed the responsibilities of issue manager to 54 companies involving Tk, 3079.53 crore.

ICB Asset Management Company Ltd. (ICBAMCL):

ICB Asset Management Company Ltd. a subsidiary company of ICB was registered under the companies Act 1994 as a public company limited by shares on 5 December 2000. The company started its functions for management of mutual funds from July 1, 2001. The company can manage the asset of any trust or fund of any type and/or character and hold, acquire, sell or deal in such asset or any trust or fund. It can organize various schemes of different types for trust funds, take part in the management of any mutual fund operation, conduct, accomplish and establish services for industrial trading and commercial activities, invest funds in shares and securities, carry on business, and act as financial and monetary agent and merchandise shares and securities.

The activities of this company have bolstered the mutual fund industry. The company has already gained widespread reputation as one of the best asset management companies in the country. Up to 30 June 2010, the company floated 10 closed-end mutual funds and 2 open-end mutual funds of which 5 closed-end mutual funds was floated at the end of 2009-10. The company has planned to float various regular and special types of mutual funds including IFIL Islamic Mutual Fund-1, ICB AMCL Growth Mutual Fund One, ICB Employees Superannuation Mutual Fund One:

Scheme One, ICB Bank First Mutual Fund, First Agrani Bank Mutual Fund, Sonali Bank Mutual Fund, Janata Bank Employees Provident Mutual Fund: Scheme One etc. recently.

ICB Securities Trading Company Ltd. (ISTCL):

During the year, the company has expanded its activities significantly to become one of the most active brokers of both DSE and CSE as in the previous years. Among many other functions the company primarily provides brokerage service for buying and selling securities listed with stock exchanges and provides brokerage service for buying and selling securities over the counter markets by the company itself and by appointing sub-brokers, sub-agents, bond brokers, specialists and odd-lot-dealers. Furthermore, the company also works as a full service Depository Participant in the CDBL.

The company has been undertaking trading activities of securities for general investors alongside the institutional investors. With a view to tempting more investors in the securities market, ISTCL has adopted an upgraded trading system namely Wide Area Networking(WAN) Connectivity through which it installed Radio Link/ VSAT/Dial-up connection in its geographically dispersed branch offices and performing direct trading.

CHAPTER -3

An evaluation of ICB Mutual Funds

It is a recognized principle that diversification of investment reduces risk. An individual may not have the time, expertise and resources to undertake such diversification. Here arises the advantage of a Mutual Fund. Mutual Funds pool the savings of a great number of investors and make investments in a wide array of securities. In Bangladesh ICB has pioneered Mutual Funds for the sake of investors and of the capital market. Country’s first Mutual Fund the “First ICB Mutual Fund “was floated on 25th April 1980. Since then ICB has, over the years, floated 8 Mutual Funds with the total capital of Tk. 17.50 crore. ICB Mutual Funds continued to command the confidence and attraction of investors as lucrative and rewarding investment in terms of steady dividend performance.

DEFINITION OF MUTUAL FUND:

Mutual Funds are also known as close ended Mutual Funds. The issued capital of a Mutual Fund is limited, that is, a Mutual Fund offers a limited number of certificates for sale to the public. The amount of capital and the number of certificates of each Mutual Fund remains unchanged. ICB Mutual Funds are independent of one another. A Mutual Fund being listed is traded on the Stock Exchanges. Price of Mutual Fund certificates after IPO is determined on the Stock Exchanges through interaction of supply and demand. The market price of a Mutual Fund certificates is available in Stock exchange quotations and in newspapers. .

TYPES OF MUTUAL FUND:

Any Mutual Fund could be of either of the following two kinds. Such as-

Open-end Mutual Fund:

Open-end investment company is a fund that continues to sale and repurchases their shares after their initial public offering. They stand ready to sell additional number of shares and thus keep going larger. The open-end fund company can by or sale their own shares.

Close-end Mutual Fund:

A close-end investment company operates like any other public firm. Their stock is traded on regular secondary market and the market price of its shares is determined by the supply and demand. It has a definite target amount for the found and cannot sell more shares after its initial offering. Its growths in terms of number of shares are issued like any other company’s new issues listed and quoted it stock exchange.

OBJECTIVE OF MUTUAL FUND:

The objective of any fund would fit into one of three broad categories.

Income: The emphasis is on producing a steady flow of dividend payment.

Capital gain: The manager concentrates on increasing the value of principal through appreciation of the stocks held.

Income and capital gain: Some combination of the first two approaches.

ADVANTAGES OF MUTUAL FUND:

- Mutual Fund substantially minimizes the investment risk of small investors through diversification in which funds are spread out into various sectors, companies, securities as well as entirely different market.

- Mutual Fund mobilizes the savings of small investor and channels them into lucrative investment opportunities. As a result, Mutual Fund adds liquidity to the market.

- Mutual Fund provides the small investors access to the whole market that at an individual level, would be difficult if not impossible to achieve.

- Because funds are professionally managed, investors are relieved from the emotional strain associated with the day to day management of the fund.

- The investors save a great deal in transaction costs given that s/he has access to a large number of securities by purchasing a single share of a Mutual Fund.

- Mutual Fund is the only vehicle which operates simultaneously both at the demand as well as the supply side of the market. On the supply side, the Mutual Fund being itself security at the SEC introduces a good and reliable instrument in the capital market for the small but astute investor.

- Mutual Fund is one of the most strictly regulated investment vehicles. The laws governing Mutual Fund require exhaustive disclosure to the SEC as well as the general public. The laws also entail continuous regulations of fund operations by the Trustee.

LAUNCHING OF ICB’S MUTUAL FUNDS:

ICB pioneered the Mutual Fund industry in Bangladesh. The country’s first Mutual Fund, the “First ICB Mutual Fund” was launched on 25 April 1980. Since then ICB had floated eight Mutual Funds of total capital of Tk.17.5 crore up to 1996.All ICB Mutual Funds are close-end Mutual Funds. Investors now perceive ICB Mutual Funds as a rewarding and relatively safe investment vehicle because of its strong and steady performance in terms dividend and portfolio management.

ICB launches eight Mutual Funds in different period with different paid up capital.

| Mutual Fund | Date of Floatation | Paid up capital (Tk. In lack) |

| First ICB Mutual Fund | 25 April,1980 | 50.00 |

| Second ICB Mutual Fund | 17 June,1984 | 50.00 |

| Third ICB Mutual Fund | 19 May,1985 | 100.00 |

| Fourth ICB Mutual Fund | 6 June, 1985 | 100.00 |

| Fifth ICB Mutual Fund | 8 June, 1987 | 150.00 |

| Sixth ICB Mutual Fund | 16 May,1988 | 500.00 |

| Seven ICB Mutual Fund | 30 June,1995 | 300.00 |

| Eighth ICB Mutual Fund | 23 July,1996 | 500.00 |

| Total 1750.00 | ||

Figure: Paid-up capital of eight ICB Mutual Fund

Here we see that 6th & 8th ICB Mutual Fund is the highest paid-up capital (Tk. 500.00 lac)

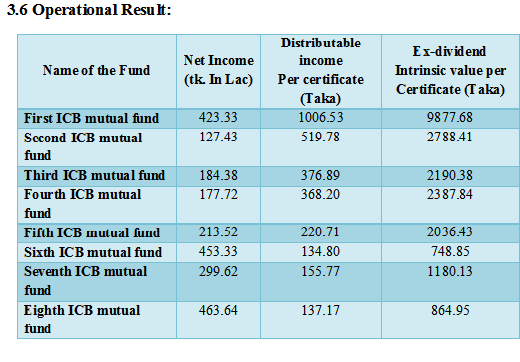

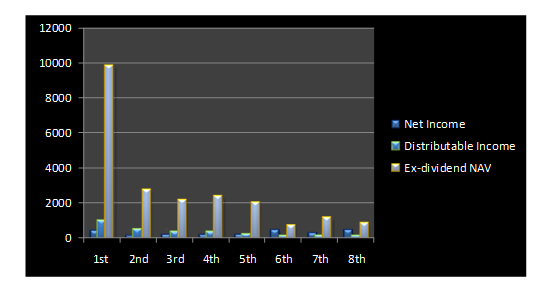

Operational Result:

Here we see that, maximum Net Income comes from 8th ICB Mutual Fund 463.64; maximum Distribute Income per certificates comes from 1st ICM Mutual Fund 1006.53; and Ex-dividend intrinsic value per certificate comes from 1st ICB Mutual Fund 9877.68

CONSOLIDATED PORTFOLIO STATEMENT:

As on 30 June 2010 cost price and market price of eight Mutual Funds were Tk. 8006.72 lac and Tk 32058.21 lac respectively. A consolidated statement of the portfolio of the Funds is given in the following table:

Consolidated position of portfolios of ICB Mutual Funds as on June 2010

| Sl.no. | Particulars | 1st Mutual Fund | 2nd Mutual Fund | 3rd Mutual Fund | 4th Mutual Fund | 5th Mutual Fund | 6th Mutual Fund | 7th Mutual Fund | 8th Mutual Fund |

| 1 | No. of Companies | 122 | 120 | 140 | 139 | 153 | 187 | 181 | 172 |

| 2 | No. of Securities | 124 | 123 | 141 | 141 | 155 | 189 | 182 | 177 |

| 3 | Total investment at cost (Tk. In Lac) | 887.70 | 612.98 | 698.25 | 748.52 | 952.61 | 1225.85 | 1341.95 | 1538.86 |

| 4 | Market Value | 7791.87 | 1782.44 | 2547.87 | 2784.04 | 3662.00 | 4162.39 | 4324.86 | 5002.74 |

Portfolio Position, Market Price per Certificate and Number of Certificate Holders: (as on 30 June 2010)

Name of the Fund | Cost of portfolio (Tk. In Lac) | Market Value of the portfolio (Tk. In Lac) | Market price per certificate (Taka) | No. of Certificate-holders |

| First ICB mutual fund | 887.70 | 7791.87 | 8701.00 | 1105 |

| Second ICB mutual fund | 312.98 | 1782.44 | 2578.75 | 1093 |

| Third ICB mutual fund | 698.25 | 2547.87 | 1972.50 | 1502 |

| Fourth ICB mutual fund | 748.52 | 2784.04 | 2139.75 | 1253 |

| Fifth ICB mutual fund | 952.61 | 3662.00 | 1763.00 | 2560 |

| Sixth ICB mutual fund | 1225.85 | 4162.39 | 647.75 | 6385 |

| Seventh ICB mutual fund | 1341.95 | 4324.86 | 1063.00 | 2383 |

| Eighth ICB mutual fund | 1538.86 | 5002.74 | 755.50 | 6735 |

| Total | 8006.72 | 32058.21 |

| 23016 |

PRICE MOVEMENT AND TRANSACTIONS:

During the year under review, certificates of eight Mutual Funds were actively traded on the floor of the Dhaka Stock Exchange Ltd and Chittagong Stock Exchange Ltd. The highest and lowest price of the eight Mutual Funds certificates on Dhaka Stock Exchange Ltd and position of total transaction during 2009-10 are shown in the following table:

Market prices of ICB Mutual Funds and Transactions during 2009-10

| Sl. No | Mutual Funds | Highest market price (Taka) | Lowest market price (Taka) | Closing Market Price (Tk as on 30 June 2010 |

| 1 | First ICB Mutual Fund | 9450.00 | 5790.00 | 8701.00 |

| 2 | Second ICB Mutual Fund | 1100 | 721 | 2578.75 |

| 3 | Third ICB Mutual Fund | 690 | 460.50 | 1972.50 |

| 4 | Fourth ICB Mutual Fund | 700 | 458 | 2139.75 |

| 5 | Fifth ICB Mutual Fund | 465 | 200 | 1763.00 |

| 6 | Sixth ICB Mutual Fund | 350 | 175 | 647.75 |

| 7 | Seven ICB Mutual Fund | 320 | 165.25 | 1063.00 |

| 8 | Eight ICB Mutual Fund | 316 | 162 | 755.50 |

Here we see that, 1st ICB Mutual Fund’s rate was highest price in the capital market and the amount is Tk. 9450, lowest market price in year of 2009-10 is 8th ICB Mutual Fund and the amount is Tk. 162. Maximum closing price Tk. 8701 (1st ICB Mutual Fund) and minimum closing price is Tk. 647.75 (6th ICB Mutual Fund).

FUNCTIONS OF ICB MUTUAL FUNDS DEPARTMENT:

Mutual portfolio formation and floating decision taken by ICB with the approval of the management EBR department decides holding category considering capital, portfolio risk, income trend, and risk diversified uniform income and growth. After all these decision security to be held are collected from IPO, Debenture issue, Secondary market etc. ICB helps sometime giving security at discount rate or at face value. Then the Fund is registered with SEC and listed with DSE and CSE. However after public issue, the fund portfolio is handed over to funds division for management operation. For purpose the Mutual Fund department has to perform the following activities mainly:

- Renunciation and issue of certificate.

- Maintain the register of the certificate holders.

- Transfer certificate if applied for after verifying transferee signature.

- Register the name of the transferee after getting approval from competent authority.

- Prepare dividend list and issue and mail dividend warrant as decided by the board.

- Record/ correct changes of address if applied.

- Reissue certificate after confirming loss and mark transfer restriction of the lost certificate, if applied for and also inform DSE & CSE on revision of the following document submitted by the loser.

REGULATORY SET-UP OF ICB’S MUTUAL FUNDS:

When ICB took the initiative of floating mutual fund in Bangladesh, there was no organized and recognized regulatory set-up for managing of mutual funds in Bangladesh. ICB had to formulate the necessary regulatory set-up and rules for the management of mutual funds. The regulatory set-up for ICB mutual funds is explicitly explained in the ICB Regulation-1977. The main features of this regulatory set-up are mentioned below:

- The Corporation may from constitute of ICB mutual funds of such denominations and securities in such each case as the board may determine.

- ICB mutual fund certificates will be listed and quoted in the stock exchange in Bangladesh and the board may determine subject to the permission of the stock exchange.

- ICB mutual funds certificate shall be movable property and freely transferable.

- ICB Mutual Fund certificate will be sold or offered for subscription with the prior consent of the government.

MANAGEMENT OF THE FUNDS:

There is a decision making board in order to manage different Mutual Funds. As per board’s decision securities are bought under different Mutual Funds. At the same way securities are sold. In case of new Mutual Fund subscribes for public issue.

ICB authority is made portfolio earlier by its own finance and given it name. After that it is published on any newspaper as prospectus. By studying this prospectus public response whether they will buy the Mutual Fund or not.

FLOATATION OF NEW MUTUAL FUNDS:

When ICB floats a new mutual fund, it is announced through publication of prospectus in two widely circulated newspapers. An investor has to apply for the shares of new mutual fund by filling in prescribed application form that can be collected from ICB officers and other attorney banks. Sometimes allotment is done by lottery draw.10% of any new mutual fund is served for non-Bangladeshi. Any Bangladeshi living abroad can collect from Bangladesh mission abroad or from authorized bank branches or from web site.

HOW TO BUY EXISTING MUTUAL FUNDS:

An investor can purchase any of the existing eight ICB Mutual Funds certificates through the Stock Exchanges at the prevailing Market Price. However, if an investor buys Mutual Fund certificates through the Stock Exchanges he/she must be careful to submit the certificates along with duly filled-in transfer deed at ICB Head Office to ensure that the certificates are registered in his/her name.

ADVANCES AGAINST MUTUAL FUND CERTIFICATES SCHEME:

Advance against ICB Mutual Fund certificates Scheme was introduced in 2003, designed for the ICB Mutual Fund Certificate holders to meet their emergency fund requirement. One can borrow maximum of 50% value of last one year’s weighted average market price of certificates at time of borrowing by depositing his/her certificates under lien arrangement from any of the ICB offices. The rate of interest on the loan is reasonable and also competitive.

MANAGEMENT FEE, CHARGE ETC:At present management fee @ 1% on the paid up capital of the Fund is charged annually. No amount is charged on account of custodial and trust services. Part of operating expenses are charged to the respective Mutual Funds on pro rata basis

ASSETS OF ICB MUTUAL FUNDS:

ICB Mutual Funds Certificates holders shall have unfettered ownership in the assets of the Fund to which they are related. In case of winding up of the Corporation the assets belonging to any ICB Mutual Fund shall not be treated as the assets of the Corporation.

TAX CONCESSIONS:

- Ø Investment in Certificates provides the same tax exemptions as an investment qualifying under Section 44 of the Income Tax Ordinance, 1984.

- Ø Capital gains received on investment in the Fund Certificates shall not be included in the total income of a Certificate holder within the limits specified in the Income Tax Ordinance, 1984.

- Ø Dividends received on investment in the Fund will be treated as dividend income under Income Tax Act, and will be exempted from tax with the limits specified in the Act.

- Ø The Fund incomes are to be exempted from all taxes as granted by the Government as per SRO No 80-L/80 dated April, 1980.

DECLARATION OF DIVIDEND:

The net income received on investments of Funds on account of dividend, bonus, interest, capital gain etc. are distributed amongst the Certificate holders as per decision of the Board of Directors of ICB. Board declares such income in the form of dividend at the end of July each year. Dividends declared by ICB in the past on the Mutual Funds were very attractive. The year-wise per certificate dividend performance of the Funds is given below.

Rate of the Dividend per Certificate (Taka)

| Year | Eight Mutual Funds | |||||||

| 1 st | 2 nd | 3 rd | 4 th | 5 th | 6 th | 7 th | 8 th | |

| 1980-81 | 20 | |||||||

| 1981-82 | 20 | |||||||

| 1982-83 | 20 | |||||||

| 1983-84 | 25 | |||||||

| 1984-85 | 35 | 21 | ||||||

| 1985-86 | 38 | 23 | 21 | |||||

| 1986-87 | 41 | 25.5 | 22.5 | 21.5 | ||||

| 1987-88 | 48 | 28 | 25.5 | 23 | 20 | |||

| 1988-89 | 49 | 29 | 26 | 23.5 | 20.5 | 15.5 | ||

| 1989-90 | 49 | 29 | 26 | 23 | 20.5 | 13.25 | ||

| 1990-91 | 35 | 22 | 19 | 17 | 10 | 6 | ||

| 1991-92 | 31 | 22 | 19 | 18 | 11 | 6 | ||

| 1992-93 | 31 | 21 | 18 | 17 | 12 | – | ||

| 1993-94 | 45 | 27 | 22 | 40 | 25 | 16 | ||

| 1994-95 | 50 | 40 | 27 | 41 | 28 | 18 | ||

| 1995-96 | 60 | 42 | 28 | 41 | 30 | 20 | 18 | |

| 1996-97 | 70 | 45 | 38 | 45 | 35 | 24 | 21 | 18 |

| 1997-98 | 70 | 30 | 35 | 32 | 22 | 18 | 14 | 12 |

| 1998-99 | 100 | 32 | 38 | 35 | 20 | 15 | 13 | 12 |

| 1999-2000 | 125 | 35 | 40 | 36 | 21 | 16 | 13.5 | 12.5 |

| 2000-2001 | 170 | 40 | 45 | 38 | 23 | 17 | 14 | 13 |

| 2001-2002 | 175 | 42 | 50 | 40 | 24 | 17.50 | 14.50 | 13.50 |

| 2002-2003 | 180 | 45 | 50 | 40 | 24 | 17.50 | 14.50 | 13.50 |

| 2003-2004 | 200 | 50 | 50 | 45 | 24 | 17.50 | 15 | 14 |

| 2004-2005 | 210 | 55 | 52 | 48 | 27 | 18.50 | 16 | 15 |

| 2005-2006 | 210 | 55 | 52 | 48 | 27 | 18.50 | 16 | 15 |