Credit Rating Method of

Credit Rating Agency of Bangladesh (CRAB)

Credit stands for being monetary liable and rating stands for symbolic result of evaluation. But the combination of these two words defines more than their meaning; it is the process of evaluation to rate to someone’s creditworthiness. This concept got popularity after the financial crisis started over the globe. Usually banks and financial institutions are popular in case of lending or giving credit money which are deposited to them by depositors. And when a depositor fails to repay back both the bank/FI and creditor suffers. Continuity of these sufferings turns them to bankrupt. Eventually a country becomes bankrupt as the most influential sector in economics (banking sector) of the country defaults. From this point of view, some companies named Moody’s, Flitch and Standard & Poor had developed and remained practicing the concept of credit rating from more than 200 years back. Increase in occurrence of financial recession, the practice of credit rating was spreading over the world as countries’ were becoming financially insolvent. Credit Rating is two types; International credit rating (rating of a country) and national credit rating (rating of an institution/person).

Many more organizations and associations like ICRA, ACRAA also emerged with the intention to regulate, control, formulate rules and to integrate this credit rating practice. At first its application was mandatory on Bank, FIs and NBFIs. Bit by bit, it turned out to be applicable on corporate business and SMEs too. Country’s credit rating is also compulsory for public finance and foreign aid sanction. Eventually, credit rating practice started in Bangladesh in 2002 with holding the hand of CRISL. Bangladesh Bank has also administrated BASEL accord and amended the credit rating act 1996. CRAB was the first mover of the industry which incorporated at 2004. Chain of command from top to bottom approach is maintained in Credit Rating process of CRAB. At first CRAB does an initial meeting with its client and takes information. Then a detail analysis is done on clients’ business model, financial condition, industry risk, operation risk, management, background, and credit facility. After that a group of credit rate debates and decides an appropriate rating maintain all the codes of conduct for the credit worthiness of the company. An award letter and credit rating report have to be submitted mentioning the rating to its client. In this report I’ve discussed about credit rating, credit rating in Bangladesh, requirements of rating in Bangladesh, about CRAB, details discussion on the credit rating process at CRAB, brief discussion on the financial ratios, grading. In my internship report I have done an analysis on ABC Ltd. And it was rated A3 which defines it has strong capacity to meet financial commitments.

Over all, there are some recommendations on CRAB and its rating process. It can be said that importance of credit rating is increasing day by day. Proper rating can save a country to get bankrupt.

Objectives of the report:

- To know about the credit rating process thoroughly

- To know about the current market situation of credit rating companies like CRAB and their customer services as well.

- To know about the regulations of the sector.

Methodology of the Report:

The type of methods used in this report is mainly of a descriptive nature. Both primary and secondary data analysis were selected as the basic research method.

Primary Data Collection:

- The primary data has been collected from:

- Interviewing the key persons of the company.

- Face to face conversation with officers and staffs;

- Related files, books study provided by the officers concerned;

- Sharing practical knowledge of officials.

Secondary Data Collection:

Certain data for this report has been extracted from secondary sources, since the descriptive nature of the study to prepare this report calls for existing facts and information compilation. The websites used in case of data collections are mentioned in Reference.

Credit Rating

Credit Rating Definition

The Credit Rating (CR) is a collective definition based on the pre-specified scale and reflects the underlying credit-risk for a given exposure. It deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure. Credit Risk Rating is the basic module for developing a Credit Risk Management system.

Credit rating evaluates the credit worthiness of a debtor, especially a business (company) or a government. It is an evaluation made by a credit rating agency to find out the debtor’s ability to pay back the debt and the likelihood of default. Credit ratings are determined by credit ratings agencies. The credit rating represents the credit rating agency’s evaluation of qualitative and quantitative information for a company or government; including non-public information obtained by the credit rating agencies analysts. Credit ratings are not based on mathematical formulas. Instead, credit rating agencies use their judgment and experience in determining what public and private information should be considered in giving a rating to a particular company or government. The credit rating is used by individuals and entities that purchase the bonds issued by companies and governments to determine the likelihood that the government will pay its bond obligations. A poor credit rating indicates a credit rating agency’s opinion that the company or government has a high risk of defaulting, based on the agency’s analysis of the entity’s history and analysis of long term economic prospects. Credit ratings for borrowers are based on substantial due diligence conducted by the rating agencies.

While a borrower will strive to have the highest possible credit rating since it has a major impact on interest rates charged by lenders, the rating agencies must take a balanced and objective view of the borrower’s financial situation and capacity to repay the debt. The credit rating has an inverse relationship with the possibility of debt default. From the opinion of the rating agency, a high credit rating indicates that the borrower has a low probability of defaulting on the debt; conversely, a low credit rating suggests a high probability of default.

Credit rating agencies typically assign letter grades to indicate ratings. Standard & Poor’s, for instance, has a credit rating scale ranging from AAA (excellent) and AA+ all the way and D.

A debt instrument with a rating below BBB- is considered to be speculative grade or a junk bond. Credit rating changes can have a significant impact on financial markets. For individuals, the credit rating is conveyed by means of a numerical credit score that is maintained by Equifax, Experian and other credit-reporting agencies. A high credit score indicates a stronger credit profile and will generally result in lower interest rates charged by lenders.

Types of Credit Ratings

(a) International Ratings:

Issuer Credit Ratings (for governments, financial institutions and corporate institutions) summarize an entity’s overall creditworthiness and its ability and willingness to meet its financial obligations as they come due across international borders. Sectors and the types of ratings that may be assigned are given below.

i) Sovereign credit ratings:

A sovereign credit rating is the credit rating of a sovereign entity, i.e., a national government. The sovereign credit rating indicates the risk level of the investing environment of a country and is used by investors looking to invest abroad. It takes political risk into account.

ii) Banks and other Financial Institutions:

- Long and short term local currency ratings

- Long and short term foreign currency ratings

- Financial strength ratings (an opinion of stand-alone financial health)

- Support ratings (an assessment of the likelihood that a bank would receive external support in case of financial difficulties)

iii) Corporate:

- Long- and short-term local currency ratings

- Long- and short-term foreign currency ratings

iv) Issue Credit Ratings:

Bonds, Sukuk and other financial obligations are opinion of an entity’s ability and willingness to honor its financial obligations with respect to a specific bond or other debt instrument. The ratings assigned to the debt issues of financial institutions and corporate can be either shortterm or long-term, depending on the tenor of the financial obligation. A short-term rating is assigned to debt instruments with an original maturity of up to one year.

(b) National Ratings:

National Ratings measure the creditworthiness of issuers or issues relative to all other issuers or issues within the same country, and unlike CI’s other ratings are not intended to be comparable across countries. National Ratings are used in countries whose sovereign credit ratings are some way below ‘AAA’ on CI’s international ratings scales, and where there is sufficient demand from capital market participants for such ratings. National Ratings enable the ratings of obligation in a given country to be distributed across a full rating scale (from ‘AAA’ to ‘D’), thereby allowing greater credit differentiation than may be possible under internationally comparable rating scales.

Profile of top two Credit Rating Agencies

The two renowned rating companies of today’s world are Moody’s Investors Service and Standard & Poor (S&P). The history of credit rating is similar to the history of forming and adopting credit rating services by these companies.

Moody’s Investors Service

John Moody and Company first published “Moody’s Manual” in1900. The manual published basic statistics and general information about stocks and bonds of various industries. From 1903 until the stock market crash of 1907, “Moody’s Manual” was a national publication. In 1909 Moody began publishing “Moody’s Analyses of Railroad Investments”, which added analytical information about the value of securities. Expanding this idea led to the 1914 creation of Moody’s Investors Service, this, in the following 10 years, would provide ratings for nearly all of the government bond markets at the time. By the 1970s Moody’s began rating commercial paper and bank deposits, becoming the full-scale rating agency that it is today.

Standard & Poor’s

Henry Varnum Poor first published the “History of Railroads and Canalsin the United States” in 1860, the forerunner of securities analysis and reporting to be developed over the next century. Standard Statistics formed in 1906, which published corporate bond, sovereign debt and municipal bond ratings. Standard Statistics merged with Poor’s Publishing in 1941 to form Standard and Poor’s Corporation, which was acquired by The McGraw-Hill Companies, Inc. in 1966. Standard and Poor’s has become best known by indexes such as the S&P 500.

Credit Rating in Bangladesh

Bangladesh credit rating industry started its journey with the mandatory requirement of having credit rating for all public debt instruments, right offer issues and shares issued at a premium before the same were offered to the public. In the year of 2002, Credit Rating Information & Service Limited (CRISL) started its operation as the first registered credit rating agency of Bangladesh. The second rating agency, Credit Rating Agency of Bangladesh Limited (CRAB) went to its operation on 2004, thus, making the sustainability more difficult for two rating agencies.

Credit Risk Grading Manual of Bangladesh Bank was circulated by Bangladesh Bank vide BRPD Circular No. 18 dated December 11, 2005 on Implementation of Credit Risk Grading Manual which is primarily in use for assessing the credit risk grading before a bank lend to its borrowing clients. By that time CRISL rating reports were appearing to be very useful for the users; specially CRISL rating report on the then Al Baraka Bank convinced the Bangladesh Bank of the need of credit rating and it took the initiative to make mandatory for all banks to have credit rating before it goes for public offering. The banking regulator further decided to make it mandatory for all banks to submit credit rating reports to the regulator within six months after the finalization of accounts.

Following the example of the central bank, the insurance regulator also came up with the requirement to make rating mandatory for all general insurance companies every year and for the life insurance companies bi-annually. The Dhaka Stock Exchange, while issuing the direct listing regulations, made the credit rating mandatory before a company apply for direct listing.

The above regulations created an enabling environment for credit rating in the country’s capital and financial markets.

The concept of client rating by the rating agencies to support capital adequacy of the banks came up in view of the need for implementation of Basel II capital adequacy framework by Bangladesh Bank. According to Basel II framework, BB adopted a standardized approach for credit risk in which the services of rating agencies were required under certain strict terms and conditions. Bank client rating is a very sensitive issue in view of the fact that most of the private sector companies, enjoying banking facilities, are not maintaining standard financials for appropriate evaluation. Unless and until all the above factors are properly evaluated through sector wise studies, the ratings are bound to give wrong signals. Security and Exchange Commission of Bangladesh (SECB) allows 2% default rate of the credit rating agencies. There are certain penalties in case default rate of more than 2% including cancellation of license of the defaulter rating agency as the highest penalty by SECB.

Other credit rating companies National Credit Ratings Ltd and Emerging Credit Rating Ltd started their journey on 2010. ARGUS Credit Rating Services Ltd. is on operation since2011. Lastly, new four credit rating companies have come to operation on 2012 which are WASO Credit Rating Company (BD) Limited, Alpha Credit Rating Limited, The Bangladesh Rating Agency Limited and WASO Credit Rating Company (BD) Limited. A list of credit rating companies operating in Bangladesh is attached with the report as Appendix.

According to Association of Credit Rating Agencies of Asia, Bangladesh has the highest number of credit rating companies. India; one of the largest economy of Asia has only two credit rating companies. On the other hand China, another largest economy is continuing its economic growth with a single credit rating company.

The rating industry In Bangladesh is now considered to be a parentless industry. The behavior of the regulators towards nourishing this industry does not appear to be rational. The rating agencies are still defined by the SEC rules as an investment advisory company. This has not changed over a long time. The paid-up capital still remains at Tk. 5.0 million (50 lakh), to start a rating agency by any group of sponsors.

Requirement for Rating in Bangladesh

(1) The Credit Rating Agencies Rules 1996 issued by the Securities & Exchange Commission requires that the following instruments be rated prior to making issuance and that the information on rating be incorporated in the prospectus of offer documents:

- Public offering of all debt instruments: bond, debenture, commercial paper, structured finance (asset/mortgage backed securities) and preference shares.

- Public issue of shares at a premium.

(2) Securities & Exchange Commission through its Securities and Exchange (Rights Issue) Rules, 2006 requires rating of the followings:

- All rights issue at premium

(3) The SEC rules 2004 (asset backed security issue) requires the credit rating of an asset pools to be securitized with optional requirements of credit rating of the originator.

(4) Bangladesh Bank through its circulars requires mandatory credit rating for the followings:

- All scheduled Banks on an annual basis

- All financial institutes in case of IPO

- Bank exposures

(5) Chief Controller of Insurance requires mandatory credit rating for the followings:

- All general insurance companies on an annual basis

- All life insurance companies on biennial basis

Overview of CRAB

About CRAB

Credit Rating Agency of Bangladesh Ltd. (CRAB) is the leading credit rating agency of Bangladesh, providing rating, grading, advisory and information services. The Company was incorporated as a public limited company under the Registrar of Joint Stock Companies in August 2003 and it received certificate for commencement of business in November 2003. CRAB was granted license by the Securities & Exchange Commission (SEC) of Bangladesh for operating as a credit rating company in February 2004. The formal launching of the company was held on 5 April 2004. CRAB has been accredited as an External Credit

Assessment Institution (ECAI) by Bangladesh Bank in 2009, which status gives it the eligibility to provide rating of bank credit exposures for risk weighted capital adequacy calculation.

CRAB is an independent and professional company established in technical collaboration with ICRA Ltd of India. CRAB is a leading provider of investment information and credit rating services in Bangladesh. CRAB’s shareholders include individuals and institutions including Investment Corporation of Bangladesh (ICB) and IDLC.

ECAI Status

Bangladesh Bank accredited CRAB as an External Credit Assessment Institution (ECAI) in April 2009. Under the standardized approach for calculating risk weighted assets against credit risk, the credit rating is to be determined on the basis of risk profile assessed by the ECAIs. Banks will use the ratings of the ECAIs and corresponding risk weight for calculating RWA for credit risk under the standardized approach.

Mission

CRAB’s mission is to effect significant contribution towards qualitative development of the money and capital markets and enhancement of transparency of financial information and credibility of the corporate sector in Bangladesh for helping in the growth of investment.

Code of Conduct

CRAB complies with the Code of Conduct as prescribed under the Credit Rating Agencies Rules of Securities & Exchange Commission. The Code of Conduct focuses on the following:

- Responsibility & Trust

- Integrity & Competence

- Quality of Rating

- Confidentiality

- Independence

- Avoidance of Conflict of Interest

- Transparency and Timeliness of Rating Disclosure

Grading Service

CRAB is equipped to offer specialized evaluation methodologies addressing exclusive and area specific requirements under the umbrella of Grading services. The services are meant for evaluation of different activities and entities belonging to multi-faceted industries. CRAB’s grading service is designed to provide an objective, credible and independent opinion on the quality of entities being examined with specific reference to parameters and issues unique to the sector/sub-sector. Construction and real-estate development activities, hospitals and diagnostic services, are examples of such sector/sub-sectors. CRAB intends to establish strategic association with reputable and specialized bodies associated with the sector/subsector to develop and offer specialized grading products.

The following grading methodologies will illustrate the scope:

Real Estate Developers Grading:

It is designed to make the investors (end user/buyer of property) aware of the risks involved in the developer’s ability to deliver as per specified terms and quality parameters and transfer of ownership on time. Also facilitates the overall growth of the real estate sector by providing the developers with guidance and incentives to conform to legal requirements and fair trade practices.

Health Care Institutions Grading:

It evaluates capability of the diagnostic and treatment providers to deliver quality care from the user’s (patient’s) perspective. Grading is designed to evaluate the two most important dimensions of care, viz. technical and interpersonal care, reflecting both infrastructure facilities and processes.

Other Grading Services:

CRAB is working in developing more grading services to other related areas and is equipped to design new services upon requirements of the clients.

Advisory & Consultancy Services

The Advisory & Consultancy Services will offer wide ranging management advisory services which include strategic counseling, restructuring solutions, financial feasibility, financial structuring/modeling, client specific need-based studies in the banking and financial services, corporate and other core sectors. CRAB is prepared to extend sophisticated Credit Risk Management services for banks and other lenders. CRAB advisory services are also available for project preparation, evaluation and execution.

CRAB is also ready to offer advisory/consulting services to clients who are seeking to be more competitive in their operating spheres. Such advisory services will be useful for a variety of clients – corporate entities, regulatory authorities, banks/financial service organizations, industry associations, local governments, government organizations, and multi-lateral agencies, through selective tie-ups with reputed organizations having expertise in specific sectors.

- Banking & Insurance:

Risk Management through to designing and implementing risk models in areas of Credit, Portfolio, Derivatives, Asset Liability Matching etc.

- NPL management

- Strategy Development

- Process & Organizational Restructuring

- Corporate:

- Financing structures & modeling

- Financial feasibility of expansions or restructuring

- Need based assignments

- Projects:

- Project Feasibility Studies which include technical and financial feasibility, demand studies, regulatory compliance, risk identification & mitigations etc.

- Financial structure of project financing

- Power Sector:

- Price & tariff setting, evaluation of contracts, business policy & plan formulation, service costing, capacity building.

- Project Feasibility Study with Technical & Financial Viability, Risk assessment, Due diligence, Counter-party risk assessment, Market assessment, growth strategies, improving profitability and competitiveness

- Financial Structuring & Arrangement of Funds

- Infrastructure:

Project Feasibility studies, structuring private sector participation options, risk assessment, assessing commercial viability of projects, designing concession agreements, Financial Structuring & Arrangement of Funds.

- Transport:

Project identification, technical and financial feasibility/modeling, demand/traffic studies, traffic and transport planning.

Information Service

CRAB provides information service in the form of database, financial analysis, market analysis, market survey etc. The service is customized to specific need of the clients.

Credit Rating Process of CRAB

Implementation of Basel II

Basel II is recommendatory framework for banking supervision, issued by the Basel Committee on Banking Supervision in June 2004. The objective of Basel II is to bring about international convergence of capital measurement and standards in the banking system. The Basel Committee members who finalized the provisions are primarily representatives from the G10 countries, but several countries that are not represented on the committee have also stated their intent to adopt this framework.

In December 2008, Bangladesh Bank issued guidelines on the New Capital Adequacy Framework (BRPD Circular 09, dated 31.12.08) to banks operating in Bangladesh, based on the Basel II framework. These guidelines inform that BB suggests implementation of Basel II with the following approaches:

i) Standardized approach for calculating RWA against credit risk;

ii) Standardized approach for calculating RWA against Market Risk; and

iii) Basic indicator approach for calculating RWA against Operational Risk.

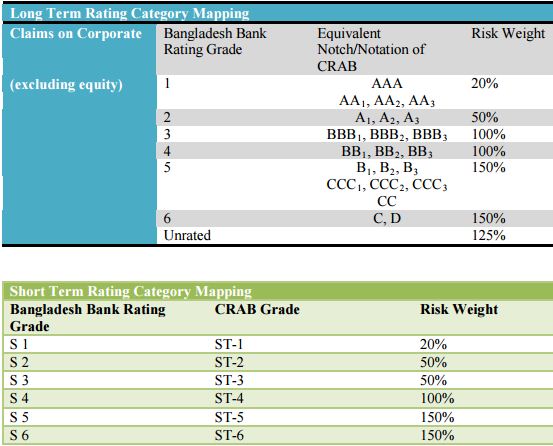

Under the standardized approach for measuring credit risks, the risk grades are determined on the basis of ratings assigned by the ECAIs.

Mapping of BB Rating Grade with ECAI Rating

Rating Process of CRAB

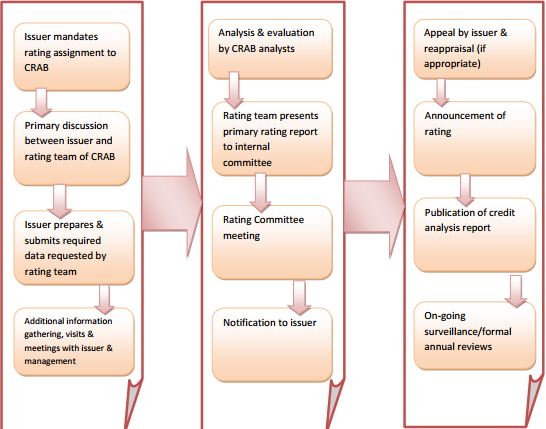

Figure: Credit Rating Process of CRAB

CRAB’s Rating process is initiated on receipt of a formal request (or mandate) from the Client. A Rating team consisting of Financial Analysts is engaged for conducting Rating assignment. Analysts collect information from the client through documents, data, meeting, site visits etc. CRAB also relies on secondary sources of information, including its own research division. After completing the analysis, Analysts prepare a Draft Rating Report, which is discussed in the Internal Committee. A draft report is provided to the client also to ensure that there is no factual mistake or misrepresentation in the report. After that the report is presented to the CRAB Rating Committee. The Rating Committee is the final authority for assigning Ratings. The assigned Rating, along with the key issues, is communicated to the issuer’s top management for acceptance. If the client does not find the Rating acceptable, it has a right to appeal for a review. Such reviews are usually taken up only if the issuer provides certain fresh inputs. During a review, the issuer’s response will be presented in the Rating Committee. If the inputs and/or fresh clarifications are warrant, the Rating Committee would revise the initial Rating decision. As part of a mandatory surveillance process, CRAB monitors the accepted Ratings over the tenure of the contract period. The Ratings generally reviewed once every year, unless the circumstances of the case warrant an earlier review. The Rating outstanding may be retained or revised (that is, upgraded or downgraded) on surveillance. Rating is an interactive process with a prospective approach. It involves a series of steps. The main steps are described as follows:

A) Rating Request:

Ratings in CRAB are usually initiated on formal request (or Mandate) from the prospective Issuer. An undertaking is also obtained on a Taka 150 non-judicial Stamp Paper before commencement of a Rating assignment; which spells out the terms and conditions of the engagement of credit rating agency.

B) Team:

The Rating team usually comprises two members. The composition of the team is based on the expertise and skills required for evaluating the business of the Issuer. The team is usually led by the lead analyst with adequate knowledge of the relevant instrument to be Rated.

C) Role of the Lead Analyst:

The lead analyst shall arrange to finalize the Rating report and send the same to the Rating Committee members. The lead analyst shall arrange to make a presentation before the Rating Committee. The lead analyst will make sure that all the relevant and material issues that may have an impact on the credit quality of the issuer (including, but not limited to those which are related to the program being Rated) are presented before the Rating Committee for discussion. The lead analyst will ensure communication of the Rating decision to the Issuer and initiate all the necessary actions consequent to the reaction of the issuer depending on the circumstances.

D) Information Requirements:

Issuers are provided with a list of information requirements and broad framework for discussions. These requirements are derived from the experience of the Issuers business and broadly conform to all the aspects, which have a bearing on the rating.

E) Secondary Information:

CRAB draws on the secondary sources of information including its own in-house research and information obtained through meetings with the Issuers’ bankers, auditors, customers and suppliers among many other relevant market participants. CRAB also has a panel of industry experts who provide guidance on specific issues to the Rating team.

F) Management Meetings and plant visits:

Rating involves assessment of number of qualitative factors with a view to estimate the future earnings prospects of the Issuer. This requires intensive interactions with the Issuers’ management specifically with a view to understanding the business plans, future competitive position and funding policies, etc.

G) Other Meetings:

The CRAB analyst team may also decide to meet the auditors (accounting policies followed, quality of internal controls, standard of disclosures, etc.), bankers / lenders (relationship, reputation, dealings in the past in respect of timeliness of servicing obligations) lawyers (if there are major litigations pending which may have serious impact on credit quality), trade union leaders (if industrial relations is a sensitive issue), key functional executives as well as a few investors, customers and suppliers, depending upon the circumstances to get a direct feedback from different stakeholder.

H) Meeting with the Issuers’ CEO /CFO:

This would be a very important meeting (usually, the last meeting) when the Rating team would discuss all the critical issues / findings that may impact the Rating decision with the CEO / CFO of the Issuer (in the absence of CEO / CFO, with a senior executive nominated by the Issuer for this purpose).

I) Internal Review Committee Meeting:

Once the draft report is prepared by the Analysts team, it is placed before the Internal Review Committee Meeting. The committee comprise of senior analysts. The committee reviews the draft rating report and analysis made by the analysts. Committee also reviews the due diligence, documents, meetings, site visits etc.

J) Rating Committee Meeting:

The authority for assigning Ratings is vested in the Rating Committee of CRAB. The Rating reports are sent by the analyst team in advance to the Rating Committee members. A presentation about the Issuers business and the management is made by the Rating team to the Rating Committee at the meeting. All the key issues are identified and discussed at length during the meetings and all relevant issues, which influence the Rating, are considered. The differences if any arise during the discussion are taken note of. Finally, a Rating is assigned either by a consensus or by majority votes.

K) Surveillance:

It is obligatory on the part of CRAB to monitor Accepted Ratings (including the Ratings treated as Deemed Acceptance) over the tenure of the Rated instrument or till any amount is outstanding under the program(s) Rated. The Issuer is bound by the agreement to provide information to CRAB to facilitate such monitoring. In case the Issuer do not co-operate by way of providing information, etc. for the purpose of surveillance, CRAB may on its own carry out the surveillance on best efforts basis based on the available information and possible interactions after giving the Issuer adequate notice requesting him to co-operate. The Ratings are generally reviewed every year, unless the circumstances of the case warrant an earlier review due to changes in circumstances or major developments that were not anticipated / factored in the Rating decision. The Ratings may be upgraded, Downgraded or retained after the surveillance. The CEO, at his sole discretion, may give one opportunity to the Issuer to represent his case if he is not satisfied with the Rating decision after the surveillance process. However, the Issuer would not have any option of not accepting the Rating after the surveillance.

Time Line

About one week after getting information; and could be longer depending on the adequacy of the discussions with the management and the information provided by the client.

Rating Methodology of CRAB’s Corporate Unit

In the Corporate rating division of CRAB, it does the rating procedure of different corporate entities including group of company and SME. The Corporate enteritis could be from any industry except from Banking and Insurance industry. In the term of rating different corporate entities CRAB follows following rating methodology-

- Operation/ Business Risk Analysis

- Industry /Market Risk Analysis

- Management Risk Analysis

- Credit Facility and Collateral Risk Analysis

- Financial Risk Analysis

Operation/ Business Risk Analysis:

In this section Analyst’s work is basically analyzing the company’s operation and risk related with Operation. By analyzing operating risk CRAB finds out existence of any Company’s strength which comes from the operation of the company. Factors which are considered here are listed below-

- Production or trading scale

- List of top five Customers

- Raw material quality

- Pricing

- Product diversity

- Raw material procurement strategy

- Relationship with customer

- List of top five Suppliers

- Cost Efficiency

- Adequacy of Resources

- Technological advancement

- Total value of existing machineries of the Company

- List of machineries; brand names and country origin of those machineries

- Quality commitment and quality policy

- Quality of imported raw material

- Quality of products produced

- Business Model

- Investment in renovation

- Investment in branding and marketing

- Utility supply, specially electricity, gas supply, gas based generator(s) to ensure continuous power supply, generators’ brand name and capacity, pump for supplying necessary water for the factory

Industry to industry these factors may vary in terms of analyzing a company’s business performance.

Industry Risk Analysis:

CRAB’s industry risk analysis focuses on the strength of industry prospects, as well as the competitive factors affecting that industry.The reason behind this consideration is to compare the current performance of selected company with the industry to oversee whether the company is running properly or not. Factors which are considered here are given below-

- Industry prospects for growth, stability or decline

- The pattern of business cycle

- Investment plans of the major players in the industry

- Demand and supply of product

- Price trends

- Change in technology

- International/domestic factors

- Regulation, entry barriers

- Capital intensity

- Corruption

- Existence or potential for heavy taxation

Management Risk Analysis:

This section identifies if there is any deviation in the management team which might affect the company in their daily run of business. Several factors observed here are shown below-

- Shareholders’ position and percentage of share

- Type of Management Hierarchy

- Number of Employees

- Process of Reporting

- Degree and Qualification of employee

- Employees’ safety measures

- Corporate governance

- Types of Strategy taken and description

- Foreign Promoters

Credit Facility and Collateral Risk Analysis:

CRAB puts more emphasis on security analysis in case of rating of instrument. In case of rating loan obligation focus is more one cash flow compared to collateral. Collateral risk means risk associated with the collateral which has been given to the Bank or any financial institution for any debt taken by the company. Several Factors have been considered here which are shown below-

- Types of collateral; Short term or long term

- If the Collateral is long term like land then full description of the land is to be given

- Available security and collateral

- Quality of collateral

- Adequacy of collateral

- Additional credit enhancement i.e. in the form of guarantee, insurance

- Legal risk of the collateral

Relation Risk Analysis:

In order to assess the creditworthiness of a company, it is inevitable to assess the banking relationship of the rated entities. Rating reflects the willingness as well as ability of the corporate to service its obligations on time. CRAB prefers to collect “Banker’s Confidentiality Report” from all the bankers of the corporate. In order for that CRAB developed a standard format of the report which includes:

- How long has the subject been your customer? Are the dealings with the subject and its sister companies satisfactory?

- Has the interest and principal payment from the subject been timely? Have there been any defaults by the subject or its sister companies? If yes, please give the details during one year.

- A brief profile of the subject’s financial relationships with its suppliers and customers (any dishonoring of cheque due to insufficient fund) during last one year.

- Loan particulars funded, non-funded and others, amount sanctioned/limit, amount disbursed and Overdrawn (if any) as of current date.

Findings

- Despite of the fact that CRAB try to analyze all of its clients’ financial condition as ethically and accurately in details as possible even then some clients are dropping gradually due to “Rating Shopping”. There are many credit rating agencies in Bangladesh who does rating of companies unethically. These rating agencies make a contract with clients to award them a high rating than they actually deserve at a lower fee. This is termed as “Rating Shopping”. They do not conduct detail analysis of the annual reports nor do they go to factory visits or site visits. Other rating agencies charges a lower fee to attract clients, which at times goes lower than the benchmark fixed. Some clients show unwillingness to continue rating service after one or two years with CRAB whereas a contract of 4 years (Initial year + 3 years of Surveillance) is signed. The fact that CRAB goes to factory visits and performs a detail analysis increases the cost so CRAB charges comparatively higher rating fees from clients to meet up for the cost. Because of this “Rating Shopping” and price war CRAB clients are becoming reluctant which is gradually pulling back revenue growth.

- One of the reasons why rating agencies are not being able to prosper in Bangladesh is because these are not many financial products in Bangladesh.

- Availability and disclosure of information: in some cases clients does not record all the information, while some clients have information but not well organized. In other circumstances, a company is big enough for maintaining Management Information System (MIS) but does not implant one, or even if a client has MISeven then they are not willing to disclose confidential information to Rating Agency. Clients sometimes think the confidentiality would be broken but they do not understand that all sorts of detail information are required for analyzing the firm and award them a rating, and that the confidentiality is maintained of the information provided. This is due to lack of knowledge about the credit rating process as a whole.

- Unavailability of market or industry information.

Recommendations

- More regulations from the regulatory bodies, Bangladesh Bank and (Securities and Exchange Commission) SEC. The regulatory bodies must rigidly monitor all the Credit Rating Agencies in Bangladesh. In 2014 all the registered credit rating agencies, Bangladesh Bank and SEC have created an association, Association of Credit Rating Agencies of Bangladesh, ACRAB, to regulate the credit rating agencies. ACRAB must closely monitor the activities of all eight agencies in Bangladesh; how ethical they are working, what fees they are charging, whether they are charging fees below the benchmark or not. They must come forward in reducing the “Price war” and “Rating Shopping”. Banks must also be strict about the authenticity of the report before accepting it. Some of the renowned banks and Bangladesh Bank only accept the credit rating report only from CRAB. But all other banks should be cautious.

- More financial products should be introduced in Bangladesh for Credit Rating Agency to flourish. The more financial products (like bond market, mutual fund) will increase in Bangladesh the more demanding, wealthy and attractive credit rating agencies would become. A bond rating fee could be charged around Taka Fifty Lac, in addition mutual fund rating could be charged around Taka One Crore. If financial products increase then the revenue would climb drastically.

- Mass people should be educated about credit rating services through seminars, by including it in the educational studies.

- CRAB’s administrative expenses should be reduced. Some clients unfortunately become reluctant before the end of the contract as CRAB charges high rating fees. This is because in order to maintain a standard CRAB pays high salary to its Officers and Financial Analysts. Also the Analysts gather detail information, thoroughly analyze them, and make factory visits almost to all of the clients every time surveillance is done and in the initial rating. These incur lots of costs, which in turn increases the fee structure. Moreover, since CRAB analyzes ethically so often the rating comes low. But other credit rating agencies act significantly unethically and come to a contract with a client to increase the rating. Also other credit rating agencies take the advantage of the existing price war between the credit rating agencies by offering comparatively low fee. As clients get better rating at a lower fee which is extremely beneficial for clients in getting loan from banks so they sometimes switch to other credit rating agencies. In addition, in some circumstances, company’s performance extremely deteriorates which ultimately makes them defaulter. So they automatically stop rating.

- There is no database in Bangladesh that is publically available of a particular industry or market situation. The rating agencies works on hundreds of organizations of the same industry. CRAB itself has worked on almost five hundred to six hundred organizations of the same industry of more or less all industry sectors. With the information CRAB has it is enough to analyze the current industry situation, industry trend and market trend and current market scenario. They should plan to create a database of each industry through which they can perform trend analysis of particular industries and market. CRAB needs to hire industry experts who can help them in this work and also in the analysis.

- Individual Financial Analyst should continue to maintain ethics and moral norms.

Conclusion

This is a brief analysis on rating procedure of Credit Rating Agency of Bangladesh (CRAB) and credit rating methods followed in successful company like ABC Company. The main purpose of this analysis is to understand the current credit rating procedure of CRAB. This report also includes a detail idea about credit rating, its history, different rating company and Credit Rating Agency of Bangladesh Limited (CRAB). I have successfully done my internship in CRAB. It was really a great experience of working with financial analysts of CRAB. My major duties and responsibilities were collecting information, assisting financial analysts, learning corporate culture, learning rating process, analyzing financial statements, preparing credit rating reports etc. During Internship program a student undergoes practical learning process in an organization. It is a good blend of theoretical and practical knowledge.