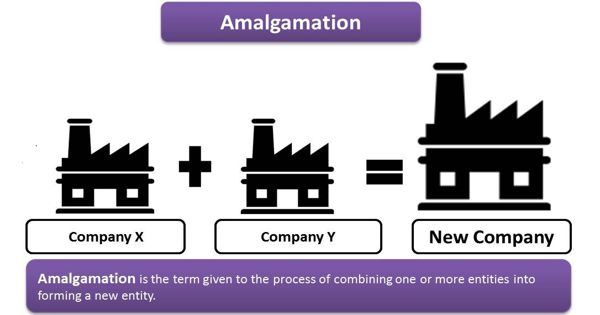

Conversion of Partnership Company to Limited Company

Often, a partnership firm converts itself into a joint-stock limited company or sells its business to an existing one. Chiefly with the objective of limiting the personal liabilities of the partners, an existing partnership firm may sell its entire business to an existing limited company or may convert itself into a limited company. Whatever the company pays as consideration will be credited to the Realisation Account. The former is the case of absorption of a partnership firm by the joint-stock company whereas, the latter is the case of the flotation of a new joint-stock company so as to take over the business of the partnership firm. If expenses are incurred by the firm, the amount will be debited to the Realisation Account.

In both of these cases, the existing partnership firm is dissolved and all the books of accounts are closed. Thus when a partnership firm is sold or converted into a company, the same accounting procedure is followed as for the simple dissolution of a firm.

The purchase consideration (price) in between the vendor (dissolving) firm and the purchasing company is fixed as mutually agreed upon. It may or may not be specified in a lump sum figure. When it is not specified in a lump sum figure, the difference of agreed values of acquired assets over the agreed amount of liabilities is undertaken.

The purchase price is discharged by the purchasing company either in the form of cash or shares (equity or preference) or debentures or a combination of two or more of these. The shares or debentures may be issued by the purchasing company, at par, at a premium or at a discount.

In the absence of any agreement, the shares received from the purchasing company are distributed among partners in the ratio of their final claim i.e. in the ratio of their capital standing after all the adjustments.

Information Source: