The labor rate variation is the difference between the actual and standard cost of direct labor. The gap between the actual amount paid and the standard rate per hour while production time remains constant.

The variation might be both positive and negative. When the actual labor cost per hour is less than the standard rate, this is advantageous. It signifies that the direct labor cost is lower than anticipated. Unfavorable, on the other hand, is that the actual labor cost is more than planned.

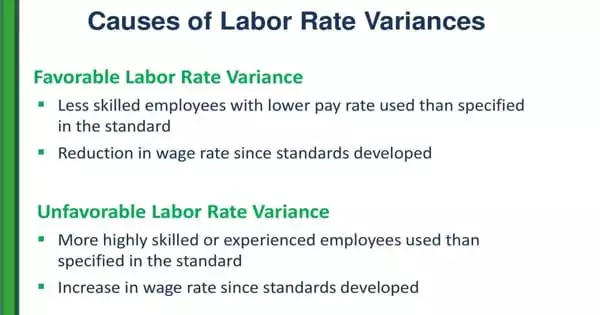

Causes of a Labor Rate Variance

There are a number of possible causes of a labor rate variance. For example:

- Incorrect standards

The labor standard may be out of date in terms of employee pay rates. The standard, for example, may not reflect the changes imposed by a new union contract. If the labor supply exceeds the demand, the labor rate falls. There may be a labor shortage at times, but workers are demanding more pay. The utilization of unskilled labor at lower wages may have resulted in decreased wage payments.

- Pay premiums

Employment of a more efficient and skilled labor force demanding a higher compensation rate. Extra payments for shift differentials or overtime may be included in the total amount paid. If there is a labor shortage, existing or new workers may demand a higher wage. A rush order, for example, may necessitate the payment of overtime in order to achieve a tight deadline. There may be more labor available, and wages may be paid at a lower rate.

- Staffing variances

A labor standard may anticipate that a specific job classification will execute a specific task whereas, in fact, the work may be performed by a different position with a different pay rate. A business hires unskilled workers at a lesser wage. This would also cause a difference. For example, the only person available to complete the work may be highly competent and hence highly compensated, even if the underlying norm anticipates that the work should be done by a lower-level worker (at a lower pay rate). As a result, this difficulty is the result of a scheduling issue.

- Component tradeoffs

The engineering team may have decided to change the components of a product that requires manual processing, hence changing the amount of work required in the manufacturing process. For example, rather than assembling many components in-house, a company may employ a subassembly given by a supplier. There may also be a difference if the mechanism of wage payment changes. Any change in worker grade may also result in a variation. Any new government legislation or agreement with a labor union for wage increases may also result in a variation.

Benefits changes

If the cost of labor includes benefits and the cost of benefits has changed, the variance is affected. Overtime work by employees may also result in variance. This is due to the fact that overtime wages are often higher than regular wages. When a corporation hires outside labor, such as temporary workers, the labor rate variance can be beneficial because the company is presumably not paying their benefits. Workers who receive an additional shift allowance or a larger bonus may also see a variation. If workers receive greater compensation (incentive) for high-quality output, this may result in a variation.

In general, the pay rate is controlled by the labor market’s demand and supply factors. As a result, labor rate variation is unmanageable. If workers are selected incorrectly, or if low grade or high grade labors are used in place of high grade or low grade labors, respectively, the production foreman will be held accountable.