Cost control is an extension of cost reduction. Cost reduction encompasses a much broader concept than cost control. In terms of objectives and standards, cost control is essentially a short-term program. However, cost-cutting initiatives could be both short-term and long-term.

Cost reduction is the process of identifying and eliminating unnecessary costs in order to improve a company’s profitability.

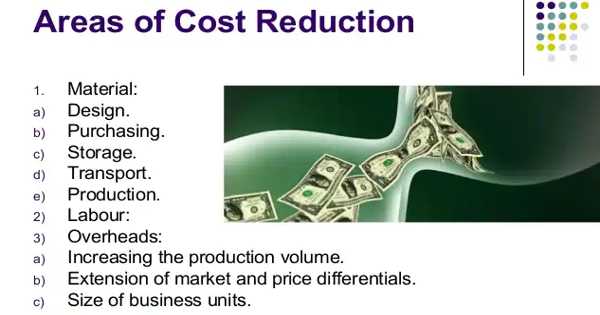

Following are the main Common Areas of Cost Reduction:

- Focus

Cost control focuses on waste reduction rather than cost reduction. Cost reduction focuses on lowering costs through new manufacturing processes, improved plant layout, scientific material handling, and so on.

- Design

Product design has the most potential for cost savings because a manufactured article must be functionally useful while also satisfying the customer. When introducing a new design, designers and cost estimators must work closely together to consider the impact of design on material cost, labor cost, direct expenses, cost savings, and so on.

The design of the product should encourage the discovery of cheaper raw materials as a substitute, maximum production, less quantity, and so on. Product design may reduce operating time, after-sales service costs, minimum tolerance, and so on.

- Marketing

Marketing cost-cutting measures include representation, advertising, market research, sales office and administration, after-sales service, packing, transportation, and warehousing. The collection and appropriate analysis of these services may result in the introduction of the most cost-effective services in accordance with the current business activities.

- Basis of Application

Continuous cost control is routinely implemented. When a cost-cutting opportunity is identified, it is used to gain a competitive advantage for a longer period of time.

A proper study of unused utilization of material, manpower, and machines should be conducted; maximum utilization of all of the above may effectively reduce the cost of any product.

- Use of Accounting Techniques

Accounting techniques are heavily used in cost control. Accounting techniques may not be used to reduce costs.

Employees should be encouraged to participate in cost-cutting initiatives. There should be no room for doubts or frictions; there should be no communication gap between any department or level of management, and there should be a proper delegation of responsibilities with defined areas of an organization’s functions.

- Finance

Cost reduction in the field of finance is an important aspect because capital may be tied up in fixed on current assets associated with risks of obsolescence, bad debts, bank charges, loss of discount, and so on due to slight negligence on the part of management. The return on capital employed must be monitored on a regular basis, as a suitable cost-cutting program will ensure the highest possible return.

- Utility services

Labor, steam, air conditioning, water, and other services are examples of utility services. Utility service costs may rise dramatically as a result of underutilization. As a result, extreme caution is required to ensure that utility services are used efficiently.