Introduction

Financial services firms are in the business of accepting risk. Primary aims of any financial services firm are collect and manage risks on behalf of their customers and make a profit for its shareholders. We may define ‘Risks’ as uncertainties resulting in adverse outcome, adverse in relation to planned objective or expectations. In the financial arena, enterprise risks can be broadly categorized as credit risk, operational risk, market risk and other risk. Credit risk is the oldest and important risk which banks exposure and important of credit risk and credit risk management are increasing with time because of some reasons like economic crises and stagnation, company bankruptcies, infraction of rules in company accounting and audits, growth of off-balance sheet derivatives, declining and volatile values of collateral, borrowing more easily of small firms, financial globalization and BIS risk-based capital requirements.

Credit risk can be defined as the risk of losses caused by the default of borrowers. Default occurs when a borrower can not meet his financial obligations. Credit risk can alternatively be defined as the risk that a borrower deteriorates in credit quality. This definition also includes the default of the borrower as the most extreme deterioration in credit quality. Credit risk is managed at both the transaction and portfolio levels. But, banks increasingly measure and manage the credit risk on a portfolio basis instead of on a loan-by-loan. In credit risk management banks use various methods such as credit limits, taking collateral, divers Dhaka ation, loan selling, syndicated loans, credit insurance, securitization and credit derivatives. Credit risk is considered as a critical factor that needs to be managed by the banks and financial institutions.

Credit Risk Management process permits the banks to proactively manage loan portfolios in order to minimize losses and earn a satisfactory level of return for shareholders. It includes detection, measurement, matching mitigations, supervision and control of the credit risk exposure. The purpose of credit risk management is to ensure that individuals taking the risk have full knowledge about it, the bank or financial institution is exposed to an approved risk limit, the risk related decisions are in line with the business strategies, the compensation for the risk is adequate and sufficient capital support is there to buffer the risks. Credit Risk Management process includes Credit Investigation, Financial Analysis, Credit Assessment, Credit Approval, Documentation, Monitoring ( Follow up, Supervision and Control) and Credit Recovery procedures.

Banks and Financial Institutions have high exposure to credit risk and Dhaka Bank Ltd. was initially emerged in the Banking scenario of the then East Pakistan as Eastern Mercantile Bank Limited at the initiative of some Bangle entrepreneurs in the year 1959 under Bank Companies Act 1913 . After independence of Bangladesh in 1972 this Bank was nationalized as per policy of the Government and renamed as Dhaka Bank Ltd. The bank is pledge-bound to serve the customers and the community with utmost dedication. The prime focus is on efficiency, transparency, precision, and motivation with the spirit and conviction to excel in both value and image. In this respect, Dhaka Bank Ltd. has established its own credit policy which will guide them in achieving their target of maximum value addition through an efficient and effective credit risk management.

Objectives of the study

The objectives of this study are as follows:

i) To have a sound understanding of credit risk management system and procedure followed in the Dhaka Bank Ltd.

ii) To gain knowledge about the credit related operations and maintenance in this bank.

iii) To analyze in detail the credit risk management process of the bank and to make recommendations if needed.

iv) To focus on the credit risk grading system for analyzing the credit assessment procedure of Dhaka Bank Ltd.

v) To have a general idea about the credit risk management performance of this bank.

Methodology of the study

The methodology includes the sample selection, sources of data and method of data analysis.

Sample selection

The organization to be discussed is Dhaka Bank Ltd. All the departments and functional areas will be covered with more emphasis on credit division.

Sources of data

The study is conducted on the basis of both primary and secondary data.

Primary Data

The primary data are collected from all the departments of Dhaka Bank Ltd by interviewing personnel of the respective departments. The heads of the departments or senior executives have been interviewed. However, the analysis and the explanation are the authors’ own.

Secondary Data:

The secondary data of the study are based on a review of existing brochures, documents and database of Dhaka Bank Ltd. The industry best practices are largely based on Bangladesh Bank manual, guidelines and databases. Books and published articles on this topic have also been consulted

Data analysis

The credit risk management data of Dhaka Bank Ltd will be analyzed in a descriptive manner.

Scope of the study

The scope of the study is entire Dhaka Bank Ltd. This report is a descriptive study which tries to focus on the theories and practices of credit risk management in the context of the financial institutions in Bangladesh. It will not focus on the comparable credit practices of other banks. In connection with this effort, a case study has been conducted on Dhaka Bank Ltd giving more emphasis on the credit side of the institution compared to the other sides.

Just Dhaka ation of the study

In recent days, people are becoming more aware about the management of their resources. As the banks do business by lending their depositors’ money, they have even more responsibility to manage their credit portfolio smoothly. Bank’s reputation is a critical factor for its success and therefore modern banks must follow appropriate guidelines, policies and relevant manuals regarding credit extension and recovery. The usage of banking service for any type of financial activities is increasing day by day. People are taking loans to start different types of businesses. It is now very important to know the internal processes of the banks and financial institutions to make informed decisions regarding their integrity, scope, ability and capacity.

Management of credit portfolio is one of the major operations of the banks. Therefore, as a 1st generation bank, Dhaka Bank Ltd should give much attention to this area and this study will attempt to analyze their efforts and draw a complete picture of their practices.

Limitations of the study

The limitations of the study are as follows:

i) The credit policies and manuals of DBL are of confidential nature and thus it is difficult to collect the necessary literature and documents within this short time.

ii) The bank officials though helpful in every respect do not have much time to explain the internal procedures.

iii) Many operations relating to the credit extension run simultaneously by different credit officials and it is difficult to capture the sequence of any particular credit proposal.

iv) A structured filing procedure is often neglected which also poses difficulty in understanding the sequential procedure.

v) Borrowers do not often have the time to cooperate in the information gathering process.

Credit Risk Management: A Theoretical Framework

Contemporary banking organizations are exposed to a diverse set of market and non-market risks, and the management of risk has accordingly become a core function within banks. Banks have invested in risk management for the good economic reason that their shareholders and creditors demand it. But bank supervisors, such as the Bangladesh Bank, also have an obvious interest in promoting strong risk management at banking organizations because a safe and sound banking system is critical to economic growth and to the stability of financial markets. Indeed, identifying, assessing, and promoting sound risk management practices have become central elements of good supervisory practice.

What is credit?

In banking terminology, credit refers to the loans and advances made by the bank to its customers or borrowers. Bank credit is a credit by which a person who has given the required security to a bank has liberty to draw to a certain extent agreed upon. It is an arrangement for deferred payment of a loan or purchase. (Wikipedia dictionary)

Credit means a provision of, or commitment to provide, funds or substitutes for funds, to a borrower, including off-balance sheet transactions, customers’ lines of credit, overdrafts, bills purchased and discounted, and finance leases. (Guideline on credit risk management, Bank of Mauritius)

What is credit risk?

Risk means the exposure to a chance of loss or damage. Risk is the element of uncertainty or possibility of loss that exist in any business transaction. Credit risk is the likelihood that a borrower or counter party will be unsuccessful to meet its obligation in accordance with agreed terms and conditions. (Wikipedia dictionary)

Credit risk means the risk of credit loss those results from the failure of a borrower to honor the borrower’s credit obligation to the financial institution. (Guideline on credit risk management, Bank of Mauritius). Credit risk is most simply defined as the potential that a bank borrower or counterparty will fail to meet its obligations in accordance with agreed terms (Basel Committee on Banking Supervision,2000).

Ident Dhaka ation

A bank’s risks have to be identified before they can be measured and managed.

Typically banks distinguish the following risk categories:

— Credit risk

— Market risk

— Operational risk

Measurement

The consistent assessment of the three types of risks is an essential prerequisite for successful risk management. While the development of concepts for the assessment of market risks has shown considerable progress, the methods to measure credit risks and operational risks are not as sophisticated yet due to the limited availability of historical data.

Calculation of Credit risk

Credit risk is calculated on the basis of possible losses from the credit portfolio. Potential losses in the credit business can be divided into

— expected losses and

— unexpected losses

(Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank)

Expected losses are derived from the borrower’s expected probability of default and the predicted exposure at default less the recovery rate, i.e. all expected cash flows, especially from the realization of collateral. The expected losses should be accounted for in income planning and included as standard risk costs in the credit conditions.

Unexpected losses result from deviations in losses from the expected loss. Unexpected losses are taken into account only indirectly via equity cost in the course of income planning and setting of credit conditions. They have to be secured by the risk coverage. (Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank)

Aggregation

When aggregating risks, it is important to take into account correlation effects which cause a bank’s overall risk to differ from the sum of the individual risks. This applies to risks both within a risk category as well as across different risk categories.

Planning and management

Furthermore, risk management has the function of planning the bank’s overall risk position and actively managing the risks based on these plans.

The most commonly used management tools include:

— Risk-adjusted pricing of individual loan transactions

— Setting of risk limits for individual positions or portfolios

— Use of guarantees and credit insurance

— Securitization of risks

— Buying and selling of assets

Monitoring

Risk monitoring is used to check whether the risks actually incurred lie within the prescribed limits, thus ensuring an institution’s capacity to bear these risks. In addition, the effectiveness of the measures implemented in risk controlling is measured, and new impulses are generated if necessary. (Basel Committee on Banking Supervision, 2000)

Source: (Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank)

PRISM Model of credit risk management

PRISM model is a contemporary model used in the credit risk management in modern world. It is called PRISM, an acronym for –

P = Perspective

R = Repayment

I = Intention

S = Safeguards

M = Management

Management, a PRISM component, centers on what the borrower is all about, including history and prospects. Intention or loan purpose serves as the basis for repayment. Repayment focuses on internal and external sources of cash. Internal operations and asset sales produce internal cash, whereas new debt or equity injections provide external cash sources. Internal safeguards originate from the quality and soundness of financial statements, while collateral guarantees and covenants provide external safeguards. The final component, Perspective, pulls other sections together: the deal’s risks and rewards and the operating and financing strategies that are broad enough to have a positive impact on shareholder value while enabling the borrower to repay the loan (Morton Glantz 2004).

Prerequisites for Efficient Risk Management

Methods

The methods used show how risks are captured, measured, and aggregated into a risk position for the bank as a whole. In order to choose suitable management processes, the methods should be used to determine the risk limits, measure the effect of management instruments on the bank’s risk position, and monitor the risk positions in terms of observing the defined limits and other requirements.

Processes and organizational structures

Processes and organizational structures have to make sure that risks are measured in a timely manner that risk positions are always matched with the defined limits, and that risk mitigation measures are taken in time if these limits are exceeded. Concerning the processes, it is necessary to determine how risk measurement can be combined with determining the limits, risk controlling, as well as monitoring. Furthermore, reporting processes have to be introduced. The organizational structure should ensure that those areas which cause risks are strictly separated from those areas which measure, plan, manage, and control these risks.

IT systems and an IT infrastructure

IT systems and an IT infrastructure are the basis for effective risk management.

Among other things, the IT system should allow

— The timely provision and administration of data;

— The aggregation of information to obtain values relevant to risk controlling;

— as well as an automated warning mechanism prior to reaching critical risk limits.

Why manage credit risk?

The reasons behind managing credit risks are as follows (Amitabh Bhargava,2004):

a) Increase shareholder value

— Value creation

— Value preservation

— Capital optimization

b) Instill confidence in the market place

c) Alleviate regulatory constraints and distortions thereof.

Risk Strategy

A successful, bank-wide risk management requires the definition of a risk strategy which is derived from the bank’s business policy and its risk-bearing capacity. Risk strategy is defined as

— the definition of a general framework such as principles to be followed in dealing with risks and the design of processes as well as technical-organizational structures; and

— the definition of operational indicators such as core business, risk targets, and limits.

The risk strategy in an operational sense should be prepared at least every year, with risk management and sales cooperating by balancing risk and sales strategies. The sales units contribute their perspective concerning market requirements and the possible implementation of the risk strategy. The proposal for a risk strategy thus worked out will be presented to the executive board, and following their approval, passed on to the supervisory board for their information. The risk strategy serves to establish an operational link between business orientation and risk-bearing capacity. It contains operational indicators which guide business decisions. (Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank)

Limits

The definition of limits is necessary to curb the risks associated with bank’s activities. It is intended to ensure that the risks can always be absorbed by the predefined coverage capital. When the limits are exceeded, risks must be reduced by taking such steps as reducing exposures or using financial instruments.

Methods of Defining Limits

The risk limits in the bank’s individual business units are based on the bank’s business orientation, its strategy, and the capital allocation method selected. A consistent limit management system should be installed to define, monitor, and control the limits. Such a system has to meet the following requirements:

— The parameters used to determine the risks and define the limits should be taken from existing systems. The parameters should be combined using automated interfaces. This ensures that errors due to manual entry cannot occur during the data collection process.

— The defined indicators should be used consistently throughout the bank. The data should be consistent with the indicators used in sales and risk controlling.

— Employees should be able to understand how and why the indicators are determined and interpreted. This is intended to ensure acceptance of the data and the required measures, e.g. when limits are exceeded.

— In order to guarantee effective risk management, it is essential to monitor risks continuously and to initiate clear control processes in time. Therefore, credit decision and credit portfolio management should be closely linked to limit monitoring. (Bernanke, 2006)

Limit Structure

The maximum risk limit is determined by the capital allocated to cover credit risks in the planning process. The bank’s organizational structure has a signDhaka ant impact on the way in which the limits are designed. One important success factor in the effective use of limits for risk controlling purposes is that a unit or an employee has the appropriate responsibility for an organizational unit which is assigned a limit. This is the only way to ensure that compliance with the limits is monitored and suitable measures are taken. (Bernanke, 2006)

Besides the types of limits mentioned above, there are further limit categories:

Product, business area, country, and industry limits

Product limits can be defined, among other things, for loans to retail and corporate customers, for real estate loans, as well as for project finance. Banks with an international focus can also define country limits in order to manage their risks arising from transactions in other regions. They also define industry limits in order to avoid a concentration of risks in individual industries that are subject to a degree of risk depending on the business cycle. (Bernanke, 2006)

Risk class limits

Monitoring and limiting the concentration of exposures in certain risk classes is necessary to be able to detect a deterioration of the portfolio in time, and thus to be able to avoid losses as far as possible by withdrawing from certain exposures. (Bernanke, 2006)

Limits on unsecured portions

The definition of limits for unsecured portions restricts loans that are granted without the provision of collateral or which are collateralized only partly. These limits allow banks to manage their maximum risks efficiently, as it is easy to determine and monitor unsecured portions.

Individual customer limits

Limits for individual borrowers represent the most detailed level of risk controlling. The main purpose for their application is the prevention of cluster risks in the credit portfolio. The more precisely the limits are defined; the more likely they are to yield control impulses that can be taken into account already at the time of approval of individual loans. (Bernanke, 2006)

Rigidity of Limits

In order to allow the use of limits to manage risks, it is necessary to define how strictly these limits should be applied. In practice, the rigidity of limits varies in terms of their impact on a bank’s business activities.

— Certain limits are defined rigidly and must never be exceeded, as otherwise the viability of the bank as a whole would be endangered.

— In addition, there are early warning indicators that indicate the risk of exceeding limits ahead of time.

This differentiation ensures that control signals are sent out not only after the (rigid) limits has been exceeded, but that early warning indicators point out the risk of exceeding a rigid limit in time to make sure that appropriate countermeasures can be taken immediately (Burns and Stanley, 2001)

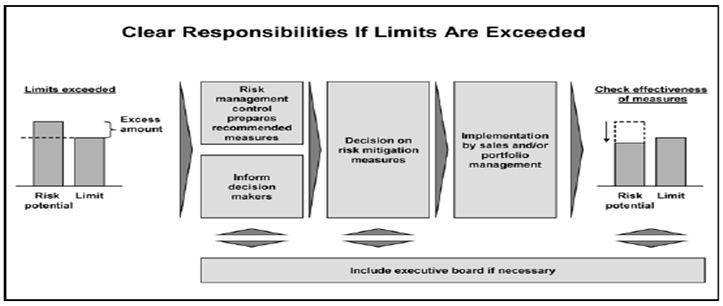

Limit Monitoring and Procedures Used When Limits Are Exceeded

The stipulated limits can have a direct impact on the credit approval. It needs to be determined if compliance with the limits should be examined before or after the credit decision is taken. In practice, this compliance is usually checked ex post, i.e. after the credit approval based on the portfolio under review, and is not a component of the individual loan decision. The credit decision is taken based on the borrower’s credit standing and any collateral, but independently of the portfolio risk. Such ex-post observation can result in a relatively high number of cases in which limits are exceeded, thus reducing the effectiveness of the limit stipulations. (Amitabh Bhargava, 2004)

Some banks check the compliance with the limits immediately during the credit approval process. Prior to the credit decision, compliance with the relevant limits is checked in case the credit is approved. Bringing limit monitoring into play at this early stage is also referred to as ex-ante monitoring. This helps prevent the defined limits from being exceeded in the course of approving new loans. Ex-ante monitoring is quite complex.

Figure Responsibilities in case of excess over limit

Source: (Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank)

The limit utilization has to be documented in the credit risk report. Processes and responsibilities concerning measures to be taken when limits are exceeded have to be defined clearly. The decision makers responsible have to be informed depending on the extent to which the limits are exceeded and the approach taken to remedy the situation.

Credit Risk Management Process

Credit risk management process should cover the entire credit cycle starting from the origination of the credit in a financial institution’s books to the point the credit is extinguished from the books (Morton Glantz, 2002). It should provide for sound practices in:

Credit Processing/Appraisal

Credit processing is the stage where all required information on credit is gathered and applications are screened. Credit application forms should be sufficiently detailed to permit gathering of all information needed for credit assessment at the outset. In this connection, financial institutions should have a checklist to ensure that all required information is, in fact, collected. Financial institutions should set out pre-qualDhaka ation screening criteria, which would act as a guide for their officers to determine the types of credit that are acceptable. For instance, the criteria may include rejecting applications from blacklisted customers. These criteria would help institutions avoid processing and screening applications that would be later rejected.

Moreover, all credits should be for legitimate purposes and adequate processes should be established to ensure that financial institutions are not used for fraudulent activities or activities that are prohibited by law or are of such nature that if permitted would contravene the provisions of law. Institutions must not expose themselves to reputational risk associated with granting credit to customers of questionable repute and integrity.

The next stage to credit screening is credit appraisal where the financial institution assesses the customer’s ability to meet his obligations. Institutions should establish well designed credit appraisal criteria to ensure that facilities are granted only to creditworthy customers who can make repayments from reasonably determinable sources of cash flow on a timely basis (Morton Glantz, 2002).

Financial institutions usually require collateral or guarantees in support of a credit in order to mitigate risk. It must be recognized that collateral and guarantees are merely instruments of risk mitigation. They are, by no means, substitutes for a customer’s ability to generate sufficient cash flows to honor his contractual repayment obligations. Collateral and guarantees cannot obviate or minimize the need for a comprehensive assessment of the customer’s ability to observe repayment schedule nor should they be allowed to compensate for insufficient information from the customer.

Care should be taken that working capital financing is not based entirely on the existence of collateral or guarantees. Such financing must be supported by a proper analysis of projected levels of sales and cost of sales, prudential working capital ratio, past experience of working capital financing, and contributions to such capital by the borrower itself.

Financial institutions must have a policy for valuing collateral, taking into account the requirements of the Bangladesh Bank guidelines dealing with the matter. Such a policy shall, among other things, provide for acceptability of various forms of collateral, their periodic valuation, process for ensuring their continuing legal enforceability and realization value (Morton Glantz, 2002).

In the case of loan syndication, a participating financial institution should have a policy to ensure that it does not place undue reliance on the credit risk analysis carried out by the lead underwriter. The institution must carry out its own due diligence, including credit risk analysis, and an assessment of the terms and conditions of the syndication. As a general rule, the appraisal criteria will focus on:

— amount and purpose of facilities and sources of repayment;

— integrity and reputation of the applicant as well as his legal capacity to assume the credit obligation;

— risk profile of the borrower and the sensitivity of the applicable industry sector to economic fluctuations;

— performance of the borrower in any credit previously granted by the financial institution, and other institutions, in which case a credit report should be sought from them;

— the borrower’s capacity to repay based on his business plan, if relevant, and projected cash flows using different scenarios;

— cumulative exposure of the borrower to different institutions;

— physical inspection of the borrower’s business premises as well as the facility that is the subject of the proposed financing;

— borrower’s business expertise;

— adequacy and enforceability of collateral or guarantees, taking into account the existence of any previous charges of other institutions on the collateral;

— current and forecast operating environment of the borrower;

— background information on shareholders, directors and beneficial owners for corporate customers; and

— management capacity of corporate customers (L.R.Chowdhury,2004).

Credit-approval/Sanction

A financial institution must have in place written guidelines on the credit approval process and the approval authorities of individuals or committees as well as the basis of those decisions. Approval authorities should be sanctioned by the board of directors. Approval authorities will cover new credit approvals, renewals of existing credits, and changes in terms and conditions of previously approved credits, particularly credit restructuring, all of which should be fully documented and recorded. Prudent credit practice requires that persons empowered with the credit approval authority should not also have the customer relationship responsibility.

Approval authorities of individuals should be commensurate to their positions within management ranks as well as their expertise. Depending on the nature and size of credit, it would be prudent to require approval of two officers on a credit application, in accordance with the Board’s policy. The approval process should be based on a system of checks and balances. Some approval authorities will be reserved for the credit committee in view of the size and complexity of the credit transaction.

Depending on the size of the financial institution, it should develop a corps of credit risk specialists who have high level expertise and experience and demonstrated judgment in assessing, approving and managing credit risk. An accountability regime should be established for the decision-making process, accompanied by a clear audit trail of decisions taken, with proper ident Dhaka ation of individuals/committees involved. All this must be properly documented.

Credit Documentation

Documentation is an essential part of the credit process and is required for each phase of the credit cycle, including credit application, credit analysis, credit approval, credit monitoring, collateral valuation, impairment recognition, foreclosure of impaired loan and realization of security. The format of credit files must be standardized and files neatly maintained with an appropriate system of cross-indexing to facilitate review and follow up.

The Bangladesh Bank will pay particular attention to the quality of files and the systems in place for their maintenance. Documentation establishes the relationship between the financial institution and the borrower and forms the basis for any legal action in a court of law. Institutions must ensure that contractual agreements with their borrowers are vetted by their legal advisers (L.R.Chowdhury,2004).

Credit applications must be documented regardless of their approval or rejection. All documentation should be available for examination by the Bangladesh Bank. Financial institutions must establish policies on information to be documented at each stage of the credit cycle. The depth and detail of information from a customer will depend on the nature of the facility and his prior performance with the institution. A separate credit file should be maintained for each customer. If a subsidiary file is created, it should be properly cross-indexed to the main credit file (L.R.Chowdhury,2004).

For security reasons, financial institutions should consider keeping only the copies of critical documents (i.e., those of legal value, facility letters, signed loan agreements) in credit files while retaining the originals in more secure custody. Credit files should also be stored in fire-proof cabinets and should not be removed from the institution’s premises.

Financial institutions should maintain a checklist that can show that all their policies and procedures ranging from receiving the credit application to the disbursement of funds have been complied with. The checklist should also include the identity of individual(s) and/or committee(s) involved in the decision-making process (Morton Glantz, 2002).

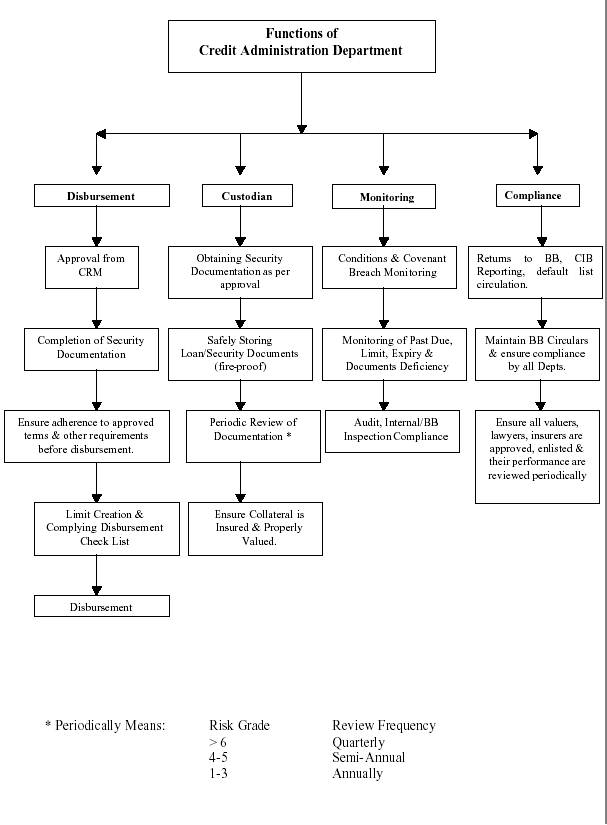

Credit Administration

Financial institutions must ensure that their credit portfolio is properly administered, that is, loan agreements are duly prepared, renewal notices are sent systematically and credit files are regularly updated. An institution may allocate its credit administration function to a separate department or to designated individuals in credit operations, depending on the size and complexity of its credit portfolio (Credit Risk Management: Industry Best Practices2005, Bangladesh Bank).

A financial institution’s credit administration function should, as a minimum, ensure that:

— credit files are neatly organized, cross-indexed, and their removal from the premises is not permitted;

— the borrower has registered the required insurance policy in favor of the bank and is regularly paying the premiums;

— the borrower is making timely repayments of lease rents in respect of charged leasehold properties;

— credit facilities are disbursed only after all the contractual terms and conditions have been met and all the required documents have been received;

— collateral value is regularly monitored;

— the borrower is making timely repayments on interest, principal and any agreed to fees and commissions;

— information provided to management is both accurate and timely;

— responsibilities within the financial institution are adequately segregated;

— funds disbursed under the credit agreement are, in fact, used for the purpose for which they were granted;

— “back office” operations are properly controlled;

— the established policies and procedures as well as relevant laws and regulations are complied with; and

— on-site inspection visits of the borrower’s business are regularly conducted and assessments documented (L.R.Chowdhury,2004)

Figure : Functions of credit administration department

Source: (Credit Risk Management: Industry Best Practices2005, Bangladesh Bank)

Disbursement

Once the credit is approved, the customer should be advised of the terms and conditions of the credit by way of a letter of offer. The duplicate of this letter should be duly signed and returned to the institution by the customer. The facility disbursement process should start only upon receipt of this letter and should involve, inter alia, the completion of formalities regarding documentation, the registration of collateral, insurance cover in the institution’s favour and the vetting of documents by a legal expert. Under no circumstances shall funds be released prior to compliance with pre-disbursement conditions and approval by the relevant authorities in the financial institution (L.R.Chowdhury,2004).

Monitoring and Control of Individual Credits

To safeguard financial institutions against potential losses, problem facilities need to be identified early. A proper credit monitoring system will provide the basis for taking prompt corrective actions when warning signs point to a deterioration in the financial health of the borrower. Examples of such warning signs include unauthorised drawings, arrears in capital and interest and a deterioration in the borrower’s operating environment (Morton Glantz, 2002). Financial institutions must have a system in place to formally review the status of the credit and the financial health of the borrower at least once a year. More frequent reviews (e.g at least quarterly) should be carried out of large credits, problem credits or when the operating environment of the customer is undergoing signDhaka ant changes.

In broad terms, the monitoring activity of the institution will ensure that:

— funds advanced are used only for the purpose stated in the customer’s credit application;

— financial condition of a borrower is regularly tracked and management advised in a timely fashion;

— borrowers are complying with contractual covenants;

— collateral coverage is regularly assessed and related to the borrower’s financial health;

— the institution’s internal risk ratings reflect the current condition of the customer;

— contractual payment delinquencies are identified and emerging problem credits are classified on a timely basis; and

— problem credits are promptly directed to management for remedial actions.

More specDhaka ally, the above monitoring will include a review of up-to-date information on the borrower, encompassing:

— opinions from other financial institutions with whom the customer deals;

— findings of site visits;

— audited financial statements and latest management accounts;

— details of customers’ business plans;

— financial budgets and cash flow projections; and

— any relevant board resolutions for corporate customers.

The borrower should be asked to explain any major variances in projections provided in support of his credit application and the actual performance, in particular variances respecting projected cash flows and sales turnover (Credit Risk Management: Industry Best Practices2005, Bangladesh Bank).

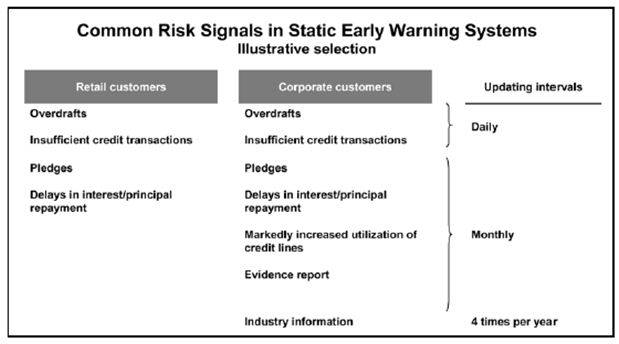

Monitoring the Overall Credit Portfolio (Stress Testing)

An important element of sound credit risk management is analyzing what could potentially go wrong with individual credits and the overall credit portfolio if conditions/environment in which borrowers operate change signDhaka antly. The results of this analysis should then be factored into the assessment of the adequacy of provisioning and capital of the institution. Such stress analysis can reveal previously undetected areas of potential credit risk exposure that could arise in times of crisis (Morton Glantz, 2002).

Possible scenarios that financial institutions should consider in carrying out stress testing include:

— SignDhaka ant economic or industry sector downturns;

— Adverse market-risk events; and

— Unfavorable liquidity conditions

Figure : Early Warning Systems

Source: (Credit Approval Process and Credit Risk Management, 2005, Oesterreichische National bank

Financial institutions should have industry profiles in respect of all industries where they have signDhaka ant exposures. Such profiles must be reviewed /updated every year. Each stress test should be followed by a contingency plan as regards recommended corrective actions. Senior management must regularly review the results of stress tests and contingency plans. The results must serve as an important input into a review of credit risk management framework and setting limits and provisioning levels (Morton Glantz, 2002).

ClassDhaka ation of credit

It is required for the board of directors of a financial institution to “establish credit risk management policy, and credit impairment recognition and measurement policy, the associated internal controls, documentation processes and information systems;”

Credit classDhaka ation process grades individual credits in terms of the expected degree of recoverability. Financial institutions must have in place the processes and controls to implement the board approved policies, which will, in turn, be in accord with the proposed guideline. They should have appropriate criteria for credit provisioning and write off. International Accounting Standard 39 requires that financial institutions shall, in addition to individual credit provisioning, assess credit impairment and ensuing provisioning on a credit portfolio basis. Financial institutions must, therefore, establish appropriate systems and processes to identify credits with similar characteristics in order to assess the degree of their recoverability on a portfolio basis.

Financial institutions should establish appropriate systems and controls to ensure that collateral continues to be legally valid and enforceable and its net realizable value is properly determined. This is particularly important for any delinquent credits, before netting off the collateral’s value against the outstanding amount of the credit for determining provision. As to any guarantees given in support of credits, financial institutions must establish procedures for verifying periodically the net worth of the guarantor.

Managing Problem Credits/Recovery

A financial institution’s credit risk policy should clearly set out how problem credits are to be managed. The positioning of this responsibility in the credit department of an institution may depend on the size and complexity of credit operations. The monitoring unit will follow all aspects of the problem credit, including rehabilitation of the borrower, restructuring of credit, monitoring the value of applicable collateral, scrutiny of legal documents, and dealing with receiver/manager until the recovery matters are finalized.

The collection process for personal loans starts when the account holder has failed to meet one or more contractual payment (Installment). It therefore becomes the duty of the Collection Department to minimize the outstanding delinquent receivable and credit losses. This procedure has been designed to enable the collection staff to systematically recover the dues and identify / prevent potential losses, while maintaining a high standard of service and retaining good relations with the customers. It is therefore essential and critical, that collection people are familiar with the computerized system, procedures and maintain effective liaison with other departments within the bank (Prudential regulations for consumer financing 2004, Bangladesh Bank).

Collection objectives

The collector’s responsibility will commence from the time an account becomes delinquent until it is regularized by means of payment or closed with full payment amount collected. The goal of the collection process is to obtain payments promptly while minimizing collection expense and write-off costs as well as maintaining the customer’s goodwill by a high standard of service. For this reason it is important that the collector should endeavor to resolve the account at the first time worked. Collection also protects the assets of the bank. This can be achieved by identifying early signals of delinquency and thus minimizing losses. The customers who do not respond to collection efforts – represent a financial risk to the institution. The Collector’s role is to collect so that the institution can keep the loan on its books and does not have to write-off / charge off.

IdentDhaka ation and allocation of accounts

When a customer fails to pay the minimum amount due or installment by the payment due date, the account is considered in arrears or delinquent. When accounts are delinquent, collection procedures are instituted to regularize the accounts without losing the customer’s goodwill whilst ensuring that the bank’s interests are protected.

Collection Steps

To identify and manage arrears, the following aging classDhaka ation is adopted:

For all products other than credit cards

Table : Credit recovery steps

| Days Past Due (DPD) | Collection Action |

| 1-14 | Letter, Follow up & Persuasion over phone (Annexure V) |

| 15-29 | 1st Reminder letter & Sl. No. 1 follows |

| 30-44 | 2nd reminder letter + Single visit |

| 45-59

|

|

| 60-89

|

|

| 90 and above

|

|

Source: (Prudential regulations for consumer financing 2004, Bangladesh Bank)

For credit cards:

Table 2.2: Credit recovery steps for credit card

| Days Past Due (DPD) | Collection Action |

| X |

|

| 30-59 |

|

| 60-89 |

|

| 90-119 |

|

| 120-149 |

|

| 150+ |

|

Source: (Prudential regulations for consumer financing 2004, Bangladesh Bank)

Legal actions could be taken on the basis of Artha Rin Adalat Ain 2003 which has been enacted to encourage speedy settlement of legal cases. It provides support for both the financial institutions and the borrower.

Dhaka Bank Ltd: Organization

Role of Banks in the modern Economy

The prosperity of a country depends upon its economic activities. Like any other sphere of modern socio-economic activities, banking is a powerful medium of bringing about socio-economic changes of a developing country. Agriculture, Commerce and Industry provide the bulk of a country’s wealth. Without adequate banking facility these three cannot flourish. For a rapid economic growth a fully developed banking system can provide the necessary boost. The whole economy of a country is linked up with its baking system.

Functions of a bank

The functions of the bank are now wide and diverse. Of all the functions of modern bank, lending is by far the most important. They provide both short-term and long-term credits. The customers come from all walks of life, from a small business to a multi-national corporation having its business activities all around the world. The banks have to satisfy requirements of different customers belonging to different social groups. The banking business has, therefore, become complex and requires specialized skills. They function as a catalytic agent for bringing about economic, industrial and agricultural growth and prosperity of the country. The banking can, therefore, be convinced “a sector of economy on the one hand and as a lubricant for the whole economy on the other”. As a result different types of banks have come into existence to suit specDhaka requirements.(L.R. Chowdhury,2004)

Company Profile of Dhaka Bank Ltd

The Bank was initially emerged in the Banking scenario of the then East Pakistan as Eastern Mercantile Bank Limited at the initiative of some Bangalee enterpreneurs in the year 1959 under Bank Companies Act 1913 . After independence of Bangladesh in 1972 this Bank was nationalised as per policy of the Government and renamed as Dhaka Bank Ltd.. Subsequently due to changed circumstances this Bank was denationalised in the year 1983 as a private bank and renamed as Dhaka Bank Ltd. The Government of the People’s Republic of Bangladesh handed over all assets and liabilities of the then Dhaka Bank Ltd. to the Dhaka Bank Ltd. Since then Dhaka Bank Ltd has been rendering all sorts of Commercial Banking services as the largest bank in private sector through its branch network all over the country.

Corporate Vision and Mission

Vision Statement

Economic Advancement in Traditional Way.

Mission Statement

- To constantly seek to better serve our Customers.

- Be pro-active in fulfilling our Social Responsibilities

- To review all business lines regularly and develop the Best Practices in the industry

- Working environment to be supportive of Teamwork, enabling the Employees to perform to the very best of their abilities.

Products & Services

Service of the Professional Personal

The officers of Dhaka Bank Ltd have to their credit, decades of banking experience with national / international banks at home and abroad. They are suitably equipped to meet customer expectations and are available at all times to provide a single-window customized and confidential service.

A State-Of-The-Art Technology Banking

The Bank will provide a state-of-the-art technology banking such as Any Branch Banking, ATM Services, Home-Banking, Tele-Banking, Mobile-Banking etc.

Retail Banking

Bank limited offers individuals the best services, including the following, to provide complete customer satisfaction:

- Deposit services.

- Current Account in both Taka and major foreign currencies.

- Convertible Taka Accounts.

- Local and foreign currency remittances.

- Various types of financing to cater to the banking requirements of multinational clients.

Institutional Banking

Dhaka Bank Ltd will offer various services to foreign missions, NGOs and voluntary organizations, consultants, airlines, shipping lines, contractors, schools, colleges and universities. The services include mainly the following:

- Deposit services.

- Current Account in both Taka and major foreign currencies.

- Convertible Taka Accounts.

- Local and foreign currency remittances.

- Various types of financing to cater to the banking requirements of multinational clients.

Corporate Banking

Dhaka Bank Ltd caters to the needs of the corporate clients and provides a comprehensive range of financial services, which include:

- Corporate Deposit Accounts.

- Project & Infrastructure Development Finance, Syndicated Finance, Linkage Finance, Investment Business Counseling, Working Capital and other finances.

- Bonds and Guarantees.

Commercial Banking

Being a commercial bank, Dhaka Bank Ltd provides comprehensive banking services to all types of commercial concerns. Some of the services are:

- Trade Finance.

- Commodity Finance.

- Issuance of Import L/Cs.

- Advising and confirming Export L/Cs. – Bonds and Guarantees.

- Investment advice.

Online Banking

Dhaka Bank Ltd offers ‘Any branch’ banking service (to limited scale) that facilitates its customers to deposit, withdraw and transfer funds through the counters of any of its branches within the country.

Merchant Banking Advisory Services

The Bank will provide Merchant Bank advisory services, offer complete packages in areas of promotion of new companies, evaluation of projects, mergers, take-over and acquisitions, liaise with the Government with regard to rules and regulations, management of new issues including underwriting support etc.

Capital Market Operation

The Bank will also introduce capital market operation which will include Portfolio Management, Investors Account, Underwriting, Mutual Fund Management, Trust Fund Management etc.

Islamic Banking Services

Dhaka Bank Ltd will open Islamic Banking Window as first initiation to serve the customers who are interested in banking based on Islamic Shariah.

Farm and Off-Farm Credits (Rural)

Out of Bank’s social commitment towards the population at the grass-root level, it will participate in farm and off-farm credit programmers in rural Bangladesh to bring in economic buoyancy in the periphery.

Seed Money for Self-Employment

The educated young people with an aptitude for organizing enterprises will be provided with the seed money primarily for self-employment and subsequently will be given advisory services as well as required fund for expansion into a fast growing productive and employment generating venture.

Credit To Women Entrepreneurs

The Bank believes in ‘Equal Opportunity Policy’ and as such has been contemplating to introduce credit programmers for willing and talented women entrepreneurs.

Consumer Credit Facility

The Bank offers a Consumer Credit Scheme, facilitating financial ease in acquiring various day to day consumer products such as usable appliances and other items.

Counter For Payment of Bills

Dedicated counters are available at Dhaka Bank Ltd’s branches to receive the payment of various utility bills.

Other Services

- Remit funds from one place to another through DD, TT and MT etc.

- Conduct all kinds of foreign exchange business including issance of L/C, Traveller’s Cheque etc

- Collect Cheques, Bills, Dividends, Interest on Securities and issue Pay Orders, etc.

- Act as referee for customers.

- Locker facility for safe keeping of valuables and documents.

Resources & Facilities

Total full time regular employee strength had increased to 300 by the year-end. Excepting for the new inductees, the remaining employees are all skilled banking professionals with varying degrees of experience and exposure, recruited from the leading local and foreign banks.

The Bank has a strong focus on imparting training towards enhancement of the skills and competencies of the employees. In the year-2007 the bank had 5,270 officers and employees. Both the Board and Management stress on developing human resources. 57 (fifty seven) courses covering different subjects were organized at the Bank’s Training Institute where 1,357 officials of different levels participated in Human Resources Development Programs. Besides these, the bank utilized the training services rendered by other training institutions like BIBM, BBTA and other national institute.

Deposits and advances

Deposits Schemes

Deposit of the Bank showed a continuous increase during the year and in 2007 stood at TK.10.16 billion. The growth over previous year was 19.15 percent. The growing customers’ confidence in Dhaka Bank Ltd. helped the necessary broadening of customer range that spanned private individuals, corporate bodies, multinational concerns and financial institutions. The Bank introduced various products/ schemes to attract the depositors. In addition to the conventional deposit forms like Current, Savings, Short-Term Deposits and Term Deposits, the Bank introduced savings schemes to attract small savers belonging to fixed low-income group. Due to affordable installment sizes and customer driven service, products are widely welcomed by small depositors.

Online banking service has been extending to cover almost the entire network of branches to enhance delivery system and provide the necessary competitive edge. The Bank continued to provide its service arms to facilitate the collection of various utility bills, which earned customer appreciation. The Bank also provides Locker Services for its depositors.

Mix of deposits improved during the year. The cost of deposit declined but was within the range of 8.50 percent. The cost of scheme deposits was higher than the conventional deposits and had reduced the net interest income during the year. However, the rate of interest on various deposits was lowered during the last quarter of the year under review.

Cash and Balances with Banks and Financial Institutions

Cash and Balances with Bangladesh Bank was TK. 6843.52 million as against Tk. 4652.40 million in 2006. The funds are maintained to meet Cash Reserve Requirement (CRR) and Statutory Liquidity Requirement (SLR) of the Bank. Due to increase in Deposits, the CRR and SLR of the bank have correspondingly increased and such requirement was properly and adequately maintained. Surplus funds after meeting the SLR and CRR were placed on short –term deposits with several commercial banks. Outstanding in such accounts in Bangladesh was TK. 1101.57 million as at 31 December 2007. The Bank maintained sufficient balances with correspondents outside Bangladesh to facilitate prompt settlement of payments under Letter of Credits commitments.

Investments

Investments of the Bank were TK. 5556.58 million showing an increase of 11.53 percent during the year under review. Investment activities centered around meeting the Bank’s SLR and were mostly in the form of Government Treasury Bills having varying dates of maturity. The average yield on the bills was 7.00% per annum.

Loans and Advances

The Bank’s total Loans and Advances stood at TK. 50,549.17 million as at December 31, 2007 showing a growth of 25.16 percent over the previous year. The portfolio was further diversified to avoid any risk of industry concentration and remained in line with the Bank’s credit norms to risk quality, yield, exposure, tenor and collateral arrangements. Bank’s clientele comprised of corporate bodies engaged in such vital economic sectors as Trade Finance, Steel-Re-Rolling, Ready Made Garments, Textiles, Ship Scrapping, Edible Oil, Cement, Transport, Construction etc. Small Business Loan Scheme was developed for providing financial assistance to small business units at urban and rural areas who cannot offer tangible securities.

Consumer Banking

The Bank continued to offer loans under Consumer Credit Scheme to the fixed income group to enable borrowers to acquire consumer products such as household appliances, office equipment, motor vehicles, mobile phone etc. With the expansion of the branch network, both in Urban and Rural areas, the Bank is now better positioned to create and deliver new services and products to its retail customers.

Foreign Exchange and Foreign Trade

Total import business handled during the year was Tk. 48.35 billion as against Tk. 37.32 billion of the previous year. The growth was 29.55 percent. Main import items were industrial raw materials, cement clinkers, yarn & fabrics for the RMG industry, vessels for scrapping, CPO & CDSO for edible oil processing and consumer items.

On the other hand, total export business handled was Tk. 19.91 billion indicating a growth of 12.46 percent. Planned and calculated thrust to finance the leading RMG units helped improve the Bank’s performance in the export sector. The satisfactory performances in Foreign Trade and Foreign Exchange sector helped the Bank to increases its fee-based income.

Treasury

The Bank’s Treasury function continued to concentrate on local money market operations which primarily include term placement of surplus fund and inter bank lending and borrowing at call. Investments for SLR purposes and participation in tenders for purchase of government treasury bills were also performed by Treasury Department. The Bank’s foreign currency dealings were supported by customer driven transactions, mainly LC payment sand negotiation of Export Bills. Special attention was given so that the Bank always remained within the open Position Limit prescribed by the Bangladesh Bank. Prudent dealing in foreign currency could improve the earnings of the Treasury Department. Hence, the Bank intends to start proper dealing operation in foreign currency as soon as possible. As a first step towards setting up a dedicated dealing room, the Treasury Department is already connected to Reuters.

Merchant Banking

Merchant Banking activity has lately gained popularity in our country. The Bank has applied for Merchant Banking License to the Securities and Exchange Commission and Intends to introduce Merchant Banking functions in 2009. At the initial stage the activities would center around issue Management, Portfolio Management and Underwriting.

Branch Network

The Bank has established a wide network of branches in urban and rural areas totaling 356. Dhaka Bank Ltd is the largest Commercial Bank in Private Sector in Bangladesh. It provides mass banking services to the customers through its branch network all over the country.

Divisional Operations in Dhaka Bank Ltd

The operations in Dhaka Bank Ltd are carried out through 5 separate departments:

- General Banking (GB)

- Cash

- Accounts

- Trade Finance

- Credit

General Banking

The General Banking division, in Dhaka Bank Ltd, generally performs the following functions:

a) Account opening

b) Cheque book issue

c) FDR issue

d) FDR encashment

e) Product issue and encashment

f) Account transfer from one branch to another branch

g) Pay order issue and encashment

h) Fund transfer from one account to other account

i) Inward Remittance

j) Outward Remittance

k) Demand Draft (DD) issue

l) Stop payment order

m) Issue of solvency certDhaka ate

n) Inward and outward clearing through the software ‘PIBS’

For every job, necessary postings are made in Micro Bank software.

Cash

Cash division is the center point of any bank. In Dhaka Bank Ltd, the cash division performs an integral part of its banking operations.

The tellers in the cash division receive cash from the clients and gives necessary postings in the PIBS (Dhaka Bank Ltd. Integrated Banking Software). At the time of receipt, ‘cash received’ and ‘posted’ seal is attached to the deposit slip. At the time of payment, the tellers first verify the signatures and then make payment. If the check is for a big amount, then it has to be authorized by the cash in charge and branch in charge. The seals used here are ‘cash paid’, ‘posted’ and ‘signature verified’.

The cash division of a branch is connected to other branches through internet and thus it can receive and pay any cheque drawn by or drawn on any other branches. In this regard, the cash division gives credit advice to other branches using Inter Branch Credit Advice (IBCA) and debit advice through Inter Branch Debit Advice (IBDA). When payment is made from other branch accounts, the payer branch issues IBCA. When payment is received for other branch, the receiver branch issues IBDA. IBDA and IBCA are treated as instruments. Related postings are made by the cash division in the MicroBank software. All the activities are also recorded in different registers.

The cash division also receives the outward clearing checks. ‘Clearing’ seal is attached for cheques inside Dhaka and ‘Collection’ seal is attached for cheques outside Dhaka. ‘Crossing’ seal is given for account pay cheques.

At the end of the day, the cash position has to be matched with the cash in hand balances. A ‘Cash Position Reserve Sheet’ is prepared and maintained by the cash in charge.

Accounts

In Punali Bank Limited, the accounts related information is fully computer generated. The central IT department generates several important statements such as the General Ledger, profit and Loss Account, Transaction journal, Overdraft and Advances Position, Full Balance position etc. These statements are disseminated in the network so that every branch can have access to its accounting information at the beginning of each working day.

The accounts division prepares the daily and weekly position of the branch in triplicate using the General Ledger. One copy is sent to the Branch Manager, one copy to the Treasury and one copy is preserved in the office record. Weekly positions of all the branches are consolidated by the central accounts department and then sent to the Bangladesh Bank. At the month end, accounts division prepares Profit Result Sheet for the month ended and Salary Sheet, charges for depreciation on fixed assets and accrued interest. It has to prepare SBS-1 (monthly) and SBS-2 (quarterly) and these statements have to be sent to Bangladesh Bank.

The accounts division performs other jobs also. It has to tally the transaction journal with each voucher. Online accounts are tallied by checking the IBDA and IBCA. Petty cash transactions and bills are also prepared and posted by the accounts division. Branch Level establishment, requisition and other personnel related activities are the responsibilities of the accounts division.

Trade Finance

Trade Finance division operates independently in the branches and it generally deals with the followings:

a) Import L/C

b) Export L/C

c) Local & foreign Bills Purchased

d) Remittance

a) Import L/C

When a client comes to open an L/C, basic queries about the IRC, VAT registration number, TIN etc, are made. Then the client presents such necessary documents as Pro-forma Invoice, Request letter to open an L/C, Application Form, IMP form for Bangladesh Bank reporting, Insurance cover note, L/C authorization form (Commercial or industrial) etc. If the bank is satisfied with all the documents, an L/C is opened and an operational entry for L/C opening is passed in MicroBank.

Customer’s Liability A/c Dr.

Bank’s Liability A/c Cr.

At this time, the bank charges for commission and other related things and pass an operational entry.

Client C/D A/c Dr.

Margin A/c Cr.

Commission A/c Cr.

SWIFT charges A/c Cr.

VAT Cr.

Stamp Charges Cr.

After shipment, the exporter submits the document to the negotiating bank. The negotiating bank sends the documents to the issuing bank. The authenticity and the content of the documents are checked and if the authority is satisfied, payment is made. At the same time, a PAD (Payment Against Document) loan is crested in the name of individual client and an operating entry is passed.

PAD Dr.

Interbranch Tk. A/c Cr.

Profit on exchange trading Cr.

Here, interbranch A/c is credited because nostro accounts are maintained by the Head Office. Another entry is passed here for reversal of liability.

Bank’s Liability Dr. Margin A/c Dr.

Customer’s Liability Cr. PAD Cr.

It is to be noted that PAD is created for only one month and if it is not adjusted within this period, a forced loan or a Loan Against Trust Receipt (LTR) is created. When the client makes payment, the bank adjusts the PAD or LTR against the client’s CD account and releases the documents. Then the bill of entry must be obtained from the client and the amount of payment must be reported to the Bangladesh Bank.

b) Export L/C

Dhaka Bank Ltd provides money to the borrowers in terms of Packing Credit and Back to Back L/C.

Packing credit is essentially a short term advance with a fixed repayment date granted by the bank to an eligible exporter for the purpose of buying, processing, manufacturing, packing and shipping of the goods meant to be exported (L.R.Chowdhury 2004). It is allowed to an exporter only when he has obtained a foreign buyer’s order. It has a certain limit and generally issued for not more than 180 days. This facility my be extended in the form of Hypothecation of goods, Pledge or Export Trust Receipt.

A Back to Back L/C is essentially a secondary credit opened by a bank on behalf of the beneficiary of the original credit, in favor of a supplier inside or outside the original beneficiary’s country.

Credit

The credit division is also an independent division in Dhaka Bank Ltd. This division basically deals with the extension of credit to the worthy clients and thus to make a profit from the interest charges. The bank invests the money of the depositors and thus the credit division has to be very cautious in terms of credit extension.

There are Relationship Managers (RM) in the branches who have the responsibility to gather valued client where the bank can invest. When a client applies for certain amount of credit, the credit officers first assess the financial and operational viability of the client and prepare a call report. A call report includes basic information about the client as well as the financial and operational position and market reputation. The credit officers often visit the business premises of the client to have an idea about his/ her business conditions. The report of these inspection visits are also enclosed in the call report. It is then sent to the Head of Credit (HOC) and Head of Marketing (HOM). If the call report passes their initial scrutiny, the branch is ordered to prepare a full fledged proposal. It is also sent to the HOC HOM and Managing Director (MD). If satisfied, they enclose their recommendations and give positive nod to the branch to prepare a credit memorandum. At this time, client is requested to present different legal documents to the loan administration division. If the board approves of disbursement and the client fulfills all the necessary legal and procedural requirements, then only the loan is sanctioned. A sanction advice is prepared and provided to the client.

The loan administration department ensures that all the guarantee and security arrangements are properly done and maintained. It keeps record of the obtained documents using security document software. After disbursement, the credit division continuously monitors the client’s business and loan repayment performance and takes necessary actions in case of non-repayment.

The credit division arranges for different types of loans and high emphasis is given on Small and Medium Enterprises (SMEs). It also issues bank guarantee in favor of the clients. Necessary postings are made through MicroBank software.

Credit Risk Management: A Case Study on Dhaka Bank Ltd

The credit risk management process followed in Dhaka Bank Ltd can be categorized in the following specDhaka segments:

Mission Statement of Punali Bank Limited

Credit Policy Guidelines

Credit Assessment

Credit Risk Grading

Credit Approval Process

Credit Risk Management

Credit Recovery

Mission Statement

To provide credit facilities to customers of DBL with care and competence and institute DBL as the ideal credit service provider in the country in terms of wide range of credit products, competitive price, adherence to credit norms, exercising due diligence and effective management of risk assets.

Credit Policy Guidelines

Credit Principles in Dhaka Bank Ltd

The credit division of Dhaka Bank Ltd is guided by 10 specDhaka credit principles. They are as follows:

i) Evaluate borrower’s nature for reliability and keenness to pay.

ii) Evaluate borrower’s loan settlement capability.

iii) Develop action plans for the likelihood of non-payment.

iv) Extension of credit in satisfactorily controllable risk areas.

v) Guarantee self-directed participation of the credit officials in the credit extension process.

vi) Perform the credit process in an ethical manner.

vii) Be proactive in recognizing, administering and conveying credit risk

viii) DBL requirements must be followed in ensuring the credit exposures and operations.

ix) Try to achieve an acceptable equilibrium between risk and reward.

x) Construct and sustain a diversified credit portfolio.

i)Evaluate borrower’s nature for reliability and keenness to pay

A borrower’s capacity and commitment to repay a loan are two important factors to a bank. In this respect, the bank has to examine the customer’s records and background in his former credit / loan related dealings. The bank should not engage itself into any commitment where there is potential threat and in these cases the bank the bank should be prepared for some exit plans.

ii) Evaluate borrower’s loan settlement capability

The loan servicing capacity of the borrower is an essential factor that has to be assessed by the bank prior to the extension of any credit facilities. For this purpose, financial techniques and procedures can be used by the bank. The bank should examine the customer’s reason for borrowing, major modes of repayment, historical and projected financial information, industry and competitive position, managerial skills, information source and systems, borrower’s operational efficiency, cyclical fluctuations in operations, supply and distribution position.

iii) Develop action plans for the likelihood of non-payment

Any kind of loan carries the possibility of default and thus it is very important for the bank to assess the secondary and tertiary modes of repayment along with the primary source. For this purpose, the bank should consider the security value, value impairment conditions, should define and document the terms and conditions of loan and ensure effective assessment.

iv)Extension of credit in satisfactorily controllable risk areas

To avoid any potential adverse situation, the bank should engage itself only in those areas where it can effectively manage and handle the transaction risk as well as the entity or business risk. In this regard, the bank has the responsibility toward developing and maintaining a productive and efficient relationship with the borrower.

v)Guarantee self-directed participation of the credit officials in the credit extension process

The independent credit participation of the credit officials is desired since it can aid in achieving the benefits of synergy and accountability. The credit personnel should utilize his or her personal skill and ability in determining the credit worthiness of the borrower and should convey all positive and negative information in time of seeking credit approval.

vi) Perform the credit process in an ethical manner

Any kind of unethical and illegal behavior, speculation, conflict of interests is prohibited in DBL. Customer related information should be kept confidential.

vii) Be proactive in recognizing, administering and conveying credit risk

The bank has to be proactive in identifying the state of the borrower’s after disbursement performance. Regular monitoring of the accounts, prompt reporting of material deterioration, utilizing Early Warning System (EWS), adjusting of lending terms and conditions are also important factors to be conformed.

viii) DBL requirements must be followed in ensuring the credit exposures and operations

Bank’s guidelines, requirements and internal directives must be complied with. The Relationship Manager must exercise his or her judgment in unforeseen circumstances.

ix)Try to achieve an acceptable equilibrium between risk and reward

The bank should be compensated for the risk it takes. Therefore, an appropriate as well as competitive pricing strategy has to be followed. Credit exposure, loan period, security, credit structure etc. should be arranged in accordance with the bank’s policies and guidelines keeping the risk return priorities in view.

x)Construct and sustain a diversified credit portfolio

Undiversified investment can expose the bank to industry specDhaka risk. Therefore, DBL has to adhere to its policy about sectoral allocation of portfolio, maintain approved ceiling for single borrower, and accurately identify risk characteristics of each exposure.

Credit portfolio mix

- Trade finance———————————— xx %

- Industry- Short term working capital ——– xx %

- Retail and SME ——————————— xx %

- Project- Finance medium and long term —– xx %

- Others ——————————————— xx %

Products offered by DBL

Table: : Products offered by DBL

| Secured Overdraft (SOD) | General purpose |

| 100% cash covered | |

| 12 months period | |

| Overdraft (OD) | General purpose |

| 12 months period | |

| Time loan | Against security or collateral |

| To finance inventory / receivables | |

| 12 months | |

| Term loan | Against fixed assets |

| Over 12 months | |

| Maximum 7 years | |

| Packing Credit | Against export LC and export order |

| 180 days |

| Payment against document (PAD) | Against sight LC |

| 21 days | |

| Loan against trust receipt (LATR) | Against import LC |

| 180 days | |

| Cash credit (Hypo) | To finance inventory |

| 12 months | |

| Local documentary bill purchased (LDBP) | To purchase discount against local usence LC |

| 180 days | |

| Foreign documentary bill purchased (FDBP) | To purchase discounted export document |

| 45 / 180 days | |

| Sight LC | For imports |

| 12 months | |

| Back to back LC & Acceptance | For import of raw materials and accessories for subsequent export |

| Maximum 180 days | |

| Letter of Guarantee | For contractual obligations |

| SpecDhaka period |

Source: DBL credit policy

Credit Assessment

Before extension of loans, a comprehensive credit risk appraisal is done and annual reviews are made. A credit memorandum (CM) is prepared by the Relationship Manager (RM) which includes the findings of such assessment. The RM used to be the owner of the customer relationship and he / she is held responsible for complying with all the policies and guidelines of Bangladesh bank, bank laws, DBL policies and guidelines etc.

The credit assessment procedure can be segregated into three segments:

Call report

Credit Memorandum

Call report

At the time inception of a relationship, the relationship manager tries to gather more and more information about the client. He / she sometimes visit the business premises to get an idea about the financial and operational condition of the prospective client. The market reputation, competitive position etc. are also duly assessed. Branch manager along with the relationship manager is also connected in this process. These initial visits or enquiries are referred to as ‘calls’.

Based on the findings of such calls, RM and the branch manager send a call report to the Head of Marketing, Head of Credit and Managing Director for initial review.

The call report contains some basic information about the client such as:

a) Client’s background

b) Business

c) Market share

d) Reliability

e) Credit exposure

f) Existing banking relationships

g) Credit requirements

h) Pricing of the proposed credit facility

Credit Memorandum (CM)

If the Head Office conveys positive sign for a call report, then only the branch RM goes for preparing a CM. The preparation of CM includes the in-depth analysis of credit risk factors, critical assessment of the client in the light of credit policy guidelines of the bank. Then it is sent to the Head of Marketing to enclose the necessary recommendations and to commence the credit approval process. The CM has to be accompanied with all the required legal documents and the financial information of the prospective client.

The CM generally contains the followings:

a) A specDhaka control number and base number for each client.

b) The credit risk grading score.

c) The authorization for the approval process.

d) The description of the proposed facility.

e) Rationale behind the loan extension.

f) Financial information of the client mainly the income statements for the past years, earnings forecasts in normal and adverse conditions.

g) Forecasted earnings from the relationship to be established.

h) Lending agreement.

i) Compliance of the policies and guidelines of Bangladesh Bank and DBL.

Most of the times CM also contains the followings:

Table 2: Credit Memorandum enclosure

| a) Facility Plan | Credit product and credit lines |

| Purpose | |

| Validity | |

| Pricing | |

| Mode of repayment | |

| b) Security Schedule | Primary and collateral security |

| Valuation by professional surveyor | |

| Valuation by the expert credit officers |

| c) Security Assistance | Personal or corporate or third party guarantee along with the detail information about the guarantor |

| Insurance | |

| Personal financial statement | |

| d) Payment | Terms and conditions for disbursement |

| Vetting of documents, security valuation, mortgage execution, deposition of fees | |

| Insurance coverage | |

| e) Lending Covenants | Financial covenants |

| Management covenants | |

| Environmental covenants | |

| Regulatory covenants | |

| f) Risks and Mitigants | Business risk |

| Financial risk | |

| Management risk | |

| Industry risk | |

| Security risk | |

| g) Visit and Inspection | Inspection report by RM, credit officer and project engineer |

| Stock inspection report | |

| h) Repayment | Repayment source |

| Repayment agenda or schedule | |

| Repayment frequency | |

| Expiry |

Source: DHAKA credit policy

The CM also contains the assessment of the following areas