Acknowledgement:

I would like to convey my sincere thanks to ALLAH because he has given me the opportunity to complete my internship .The Almighty for whom we are living in this beautiful world and able to conduct our works. Off course, I acknowledge the support & assistance given by a number of people. I am grateful to many individuals for the completion of the report successfully. Stamford University Bangladesh & Islami Bank Bangladesh limited both provided enormous support & guidance for my internship program.

I would like to acknowledge my honorable assistant lecturer “Mostofa Mahmud Hasan”. He sincerely helped me and has given necessary suggestions in preparing my internship report .I like to express my gratitude to my honorable course co-coordinator Mahmuda Sultana, for all of her guidance & co-operation throughout my internship program.

I am thankful to Md. Mosiur Rahman, Assistant officer Md. Mamunur Rashid. Probationary officer for all their continuous co-operation in every step from beginning to end of preparing this report.

I would also like to take this opportunity to express my whole hearted gratitude to my fellow friends near and dear ones who faired encouragement, information, inspiration and assistance during the course of constructing this internship report.

Executive Summary:

This report will give a clear idea about total activities and its performance. Especially this report focuses on the “Analysis of Different Modes of Investment of Islami Bank Bangladesh Limited IBBL”. After reading this report it will be easy to get idea about establishment of Islami Bank Bangladesh Limited (IBBL). This report also focuses on performance evaluation of IBBL .This report also explains the general banking, Investment and Foreign Trade of IBBL .This report also contains findings, recommendation and conclusion.

IBBL is an Islamic Bank based on “Islamic Shariah”. It follows the alternative concept of Islamic Banking which represents unique human approach to credit and banking based on profit-oriented economy avoid of interest (RIBA). In this regard IBBL has introduced a number of income generating programs for the millions of urban and rural people. With that objective in view IBBL has formulated a profitable investment option for the rich and poor to earn and live in a better society with security and peace.

In this report there is discussion on topics of over all activities and the performance of IBBL. This report also discuss about deposit collection, investment policy, various type of deposit account and their characteristics.

This report also give clear idea about general banking, account opening procedures and the different department of general banking. Also some other basic functions like- maintaining cash or vault, keeping proper record of necessary papers and documents, handling evening banking and so on.

In this report we also provide some important and valuable information about general & other functions which we closely observed and done during working in Local Office of IBBL.

Chapter 1: Introduction of Report :

| 1.1 Background of the Study |

| 1.2 Rationale of the Study |

| 1.3 Objectives of the report |

| 1.4 Scope of the report |

| 1.5 Limitations of the study |

| 1.6 Methodology |

Background of the Study:

The people of this country are deeply committed to Islamic way of life. Naturally, it remains a deep cry in their hearts to fashion and design their economic lives in accordance with the precepts of Islam. The establishment of Islami Bank Bangladesh Limited it is committed to conduct all banking and investment activities on the basis of interest-free profit-loss sharing system. People working abroad are remitting money into Bangladesh .But the general public along with others most likely to get involved in Foreign Exchange & Inward Transaction does not have a clear understanding there of Exposing foreign exchange & Inward Transaction practice is the pursuit of this report.

Rationale of the Study:

In our economy, there are mainly three types of schedule commercial banks are in operation. They are nationalized commercial banks, local private commercial banks and foreign private commercial banks. Islami Bank has discovered a new horizon in the field of banking area, which offers different General Banking, Investments and Foreign Exchange banking system. So, I have decided to study on the title “Analysis of Different Modes of Investment of Islami Bank Bangladesh Limited (IBBL)”.Because the internship program of the university is an integral part of the BBA program. This also provides an opportunity to the students to minimize the gap between theoretical and practical knowledge.

Objectives of the report:

The first objective of the report is to fulfill the partial requirement of the BBA program. Secondly, to give an overview of Islami Bank Bangladesh Limited (IBBL) in general based on our work experience. The objectives of the report are:

- To understand Islamic view in banking sector and to find out the superiority of Islamic banking over conventional banking.

- To analyze Islami banking practice of Islami Bank Bangladesh Limited.

- To understand the various functions of Islami Bank Bangladesh Limited like general banking, Investment and Foreign exchange.

- To find out the problem and how to improve the performance of the IBBL.

- To make recommendation to eliminate the problems faced by Islami Bank Bangladesh Limited on it’s over all activities.

Scope of the report:

The scope of this report is confined to foreign exchange & Inward Transaction practice in Islami Bank Bangladesh Limited (IBBL). It should only cove how the bank manages import-export process as well as foreign exchange & foreign remittance.

Limitations of the study:

- Shortage of time period

- Busy working environment

- Insufficient Data

- Secrecy of Management.

The study requires a systematic procedure from selection of the topic to prepare the report. To prepare the report data sources are to be identified and collected, data to be classified, analyzed, interpreted and presented in a systematic way and it is must to find out the key points. This overall process of methodology is given in the below which has been follow to prepare the report.

- Topic selection: After an intensive fifteen (15) days training from IBTRA. With the discussion with our course coordinator we decide to make our report on “A study on Over all activities & performance of IBBL”

- Identifying data Sources: The report is prepared by using both primary and secondary data. But secondary data is mostly use to prepare this report.

Primary sources: Some required & important information came from primary sources. These sources are:

- Interviews and conversations with officers and executives of the bank from different divisions and departments.

- official records of Islami Bank Bangladesh Limited (IBBL)

- Observations of the work done by the different department.

Secondary sources: Most of the parts of the report and conceptual part have been collected from different secondary sources. Some of these secondary sources are:

- Annual Report of IBBL

- Different circulars issued by the IBBL

- Class notes of IBTRA.

- Different journals and articles.

Chapter 2 (Background of the organization):

| 2.1 An overview of the organization |

| 2.2 Mission, vision, strategy statement |

| 2.3 Corporate Information |

| 2.4 Composition of the board |

| 2.5 Capital and reserves |

| 2.6 Milestones in the development of the organization |

| 2.7 Corporate Information |

| 2.8 Risk management |

| 2.9 HRD |

| 2.10 District-wise Branch distribution |

| 2.11 Profit and loss account (Income Statement) |

| 2.12 Balance Sheet |

| 2.13 Cash flow statement |

An overview of the organization:

Establishment of Islamic Development Bank (IDB) by the OIC member states in the year 1975 has been proved to be a breakthrough in the expansion of Islamic Shariah based finance and specially banking throughout the world. As a founder member of IDB, the Government of Bangladesh also had the commitment to establish Islamic banks which was reflected in different steps taken by the governments of the country. The OIC members consented to the proposals to introduce Islamic economy and banking in their respective countries held in the foreign ministers’ conferences in 1978 and 1980 in Dakar and Islamabad respectively. In the year 1981, OIC in its 3rd summit held in Makkah approved the proposition submitted by Bangladesh to introduce separate banking system following Islamic ideology. As per decision, the GOB sent representatives to the Middle Eastern countries to learn the existing banking systems in those countries.

Mission, vision, strategy statement:

Mission of IBBL:

- To Establish Islamic Banking through the introduction of welfare oriented banking system and also ensure equity and justice in the field of all economic activities, achieve balanced growth and equitable development through diversified investment operations particularly in the priority sectors and less developed areas of the country.

- To encourage socio-economic uplift and financial services to the low-income community particularly in the rural areas.

Vision of IBBL:

The Vision of IBBL is to always strive to achieve superior financial performance, be considered a leading Islamic Bank by reputation and performance.

- IBBL goal is to establish and maintain the modern banking techniques, to ensure the soundness and development of the financial system based on Islamic principles and to become the strong and efficient organization with highly motivated professionals, working for the benefit of people, based upon accountability, transparency and integrity in order to ensure stability of financial systems.

- IBBL will try to encourage savings in the form of direct investment.

- Also try to encourage investment particularly in projects which are more likely to lead to higher employment.

Strategy Statement:

2011 Year of welfare & green banking.

Corporate Information:

(As On 31 December, 2010)

| Date of Incorporation | 13th March, 1983 |

| Inauguration of 1st Branch (Local office, Dhaka) | 30th March, 1983 |

| Formal Inauguration | 12th August, 1983 |

| Share of Capital | |

| Local Shareholders | 41.77% |

| Foreign Shareholders | 58.23% |

| Authorized Capital | Tk.20,000 Million |

| Paid-up Capital | Tk. 7,413.12 Million |

| Deposits | Tk. 291,347.00 million |

| Investment (including Investment in Shares) | Tk. 292084.00 million |

| Foreign Exchange Business | |

| Import | Tk. 246,281.00 million |

| Export | Tk.148,421.00 million |

| Remittance | Tk. 214,629.00 million |

| Branches | |

| Total number of Branches | 251 |

| Number of AD Branches | 43 |

| Number of Shareholders | 52164 |

| Manpower | 10068 |

Composition of the board:

The board of direction consists of 15 non-executive members .The number of board members is within the maximum limit set by the central bank .The board is composed of experienced members with diverse professional experiences .The board members are independent who express their views & opinions free from any influence. The directors are also independent from management, business/other relationship of the bank that could materials interfere the activities of the bank. The decision making process and practices are based on free exchange of views to make effective directors for the management which is one of the key responsibilities of the board.

Capital and reserves:

The Authorized Capital of the Bank is Taka 10,000.00 million and Paid-up capital is Taka 7,413.00 million in October, 2010. The Paid-up Capital was Taka 67.50 million in 1983.

The Reserve Fund of the Bank has been increasing steadily. on 31st December 1983, it was Taka 0.36 million and stood at Taka 13,927.96 million as on 31st December 2009 .

Milestones in the development of the organization:

The principles and working procedures of Islamic Banks are completely new and different from the conventional banks. There is an inevitable need for training of the employees of the banks to orient and attune them to the new system of Islami banking. To cater to this need, Islami Bank training and Research Academy (IBTRA) was established in 1984, soon after the inception of the Bank.

The activity of IBTRA covers both training and research on various aspects of Islamic banking. The Academy developed a rich library of its own with a treasure of valuable books on different subjects including Islamic economics, banking, comparative philosophies and journals of home and abroad and research articles and documents. Employees of the Bank, learners and researchers have been taking full advantage of the library.

The Academy edited books on “Readings in Islamic Banking” and “Investment Operations”. It also edited and published a brochure on “Investment and Trade Opportunities in Bangladesh.”

Keeping in view the existing and future training requirement of the Bank and also to generally cater such needs of different Islamic banking & financial institutions of the region, the management of Islami Bank Training and Research Academy has been placed at the disposal of an Academic Council consisting of 3 Directors of the Board, Management Executives of the Bank, Shariah scholar, renowned academicians and representatives of reputed institutions engaged in the training of bank officials of the country.

The Academy conducts training courses, and workshops. The courses include Islamic Banking, Banking Law and Practice, Investment Operations and Management, Foreign Trade and Foreign Exchange, Shariah Based Audit and Inspection.

Besides, orientation, induction, foundation and motivation courses on different subjects are also conducted round the year. In addition to conducting regular training courses, it arranges seminar on Islamic economics and banking and such other related topics of current interest.

Apart from this, an “Executive Development Programme” has been introduced at the Head Office of the Bank in Dhaka since 1988 for enriching knowledge and thought

process and developing professional skill of the Executives. This programme has proved to be effective and now being extended outside Dhaka. The Academy conducts internship courses for the students of different Departments of various Universities of the country. The Bank introduced annual award for the best three students of the Department of Banking and Finance of Dhaka University who secure 1st class 1st, 2nd and 3rd with ‘Islami Banking’ as special subject from the year1994.

The Bank is also providing financial assistance for publication of a textbook on ‘Islamic economics and banking’ for the university students.

Besides, a motivational programme has been introduced since 1987 for the clients of the Bank. Client-orientation programme are arranged at different branches for disseminating the concept of Islamic economics and banking and to acquaint the clients with the operations of Islamic banking system.

The Bank, in 1993, co-sponsored a 3-day International Seminar on ‘Islamic Common Market’ in which scholars, economists, bankers, industrialists and representatives of trade bodies of 15 countries participated. The Bank, with the collaboration of International Association of Islamic Banks (IAIB), organised an International Seminar on Islamic Banking in1985 and another International Seminar on Islamic Banking and Insurance in 1989.

Risk management:

The management of Islami Bank limited acknowledges that risk is an integral part of business and attaches the importance to various risk involved in the banking business .The board of the bank has also endorsed the view of the management and instructed to implement the same in line with the directives of Bangladesh Bank .The bank has also taken initiatives to structure the banking activities in line with Bangladesh Bank’s risk management at guidelines.

The bank management of the bank cover a wide spectrum of risk issues and the 6(six) core risk areas of banking, investment risk, asset liability management risk,

internal control & compliance risk, money laundering risk & information technology risk, foreign exchange risk gave already been implemented by IBBL.

Now skilled and senior professionals man the risk areas. Accordingly, the Board of directors of IBBL has approved 6(six) risk management polices guidelines on the above . The management shall pay special attention to reduce the risk to an acceptable level apart from prudent controls over the banks assets.

HRD:

| Human Resources DivisionIn-charge: Abdus Sadeque Bhuiyan, Executive Vice President |

| Division / Department | In-charge | Designation |

| Administration and Personnel Planning DepartmentDiscipline and Appeal Deptt.Staff Welfare and Training Department | O N M Abdul HannanAbdus Sabur Khan1. Nazimuddin Ahmed Khan (Staff Welfare) 2. Mohammad Jalaluddin (Training) | Vice PresidentAsstt. Vice PresidentAsstt. Vice President Vice President |

| Board Secretariat Division | Md. Shouquat Ali | Executive Vice President |

| Research, Planning & Development Division | Md. Shah Jahan | Executive Vice President |

| Rural Development Division | Md. Obaidul Haque | Senior Vice President |

| Share Department | Md. Abdur Rahman Banerjee | Senior Vice President |

District-wise Branch distribution:

1. Dhaka Division

2. Chittagong Division

3. Khulna Division

4. Rajshahi Division

5. Barisal Division

6. Sylhet Division

| Category | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

| Total Branch | 169 | 176 | 186 | 196 | 224 | 251 |

| 3.1 General banking |

| 3.1.1 Account opening section |

| 3.1.2 Documents for opening some special account |

| 3.1.3 Limited company |

| 3.1.4 Club society |

| 3.1.5 Savings account individual or joint |

| 3.1.6 Other products and services |

| 3.2 Remittance in Bangladesh |

| 3.3 Local Remittance |

| 3.3.1 Pay order issue |

| 3.3.2 Demand draft issue |

| 3.3.3 Telegraphic transfer |

| 3.3.4 Mail transfer |

| 3.4 Clearing section |

| 3.5 Cash section |

| 3.6 Dishonor of cheques |

| 3.7 Deposit section |

| 3.8 Closing accounts |

| 3.9 Accounts section |

| 3.10 Credit & Risk Management (CRM) |

| 3.10 .1 Loans and Investment |

| 3.10.2 Foreign exchange |

| 3.10.3 Foreign exchange market and Bangladesh |

| 3.10.4 Foreign exchange products in Bangladesh |

| 3.10.5 Different foreign exchange rate in Bangladesh |

| 3.10.6 History of exchange rate system in Bangladesh |

| 3.10.7 Inter bank transaction in foreign exchange |

| 3.10.8 Movement of monthly averages of USD/BDT exchange rate |

| 3.10.9 Category wise position of inter bank FX transaction |

| 3.10.10 Foreign exchange department |

| 3.10.11 Import |

| 3.10.12 Export |

Chapter 3 (General activities of the organization):

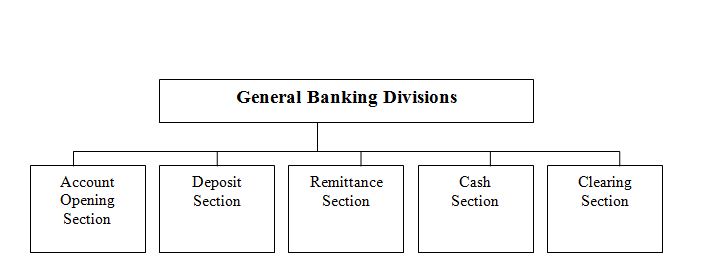

General banking:

Account opening section:

Account Opening is the gateway for clients to enter into business with bank. It is the foundation of banker customer relationship. This is one of the most important sections of a branch, because by opening accounts bank mobilizes funds for investment. Various rules and regulations are maintained and various documents are taken while opening an account.

Who can open an account?

- Person over 18 (Eighteen) years.

- Account of club

- Account of associations

- Account of agent

- Govt. & Semi govt. organization

- Liquidators

- minors

- Married Women

- Illiterate

- Firms

- Co-operative

- Non-resident and so on.

Documents for opening some special account:

One who want to open an account, He/She has to fill up an account opening form. This form is a legal contract between the bank and prospective customers. The rules and regulations for opening of an account vary from customer to customer, if he wants to open different types of accounts. to open different types of account of the people who can introduces of the following requirements which are mentioned below:

- Bank provides account opening form to the prospective customer or applicant.

- Applicant fills up the form.

- An applicant submits the form dully signed by an introducer.

- The authorized officer scrutinizes the application form.

- If they are satisfied, they will open the account.

- They issue deposit slip and deposit must be made it.

- After deposition one cheque book is issued.

- Bank preserves the specimen signature card to verify the signature of the client.

- Account is opened.

Limited company :

- Copies of Memorandum and Articles of Association duly certified by the Register of JSC with up to date amendment & list of director.

- Duly attested copy of Certificate of Incorporation issued by the RJSC.

- Certificate of Commencement of Business (in case of public Ltd. Co.) .

- Resolution of Board of directors authorize the person / persons / to open & operate the A/C.

- Common seal of the company mentioning status of operator(s) should be affixed where necessary.

Club society:

- Constitution/Buy-Laws etc. under which such Clubs & Societies have been established.

- Resolution of the Board/Management Committee for opening & operation of the account under official seal & signature to be obtained.

- List of Executive Committee/Managing Committee.

- Seal of the organization mentioning official status of the officer bearer authorized to operate the account should be affixed.

Savings account individual or joint:

Individual Accounts:

- Genuine and acceptable introduction

- Attested photographs of the applicant

- Certificates from the chairman / commissioners or any responsible person

- Photocopy of National ID card

- Certificate of incorporation.

- Certified copy of resolution of the board of directors regarding opening of account.

- List of directors under the signature of the chairman

- Copied of latest financial statement / transaction profile.

Joint Accounts:

Accounts are allowed to be opened in two or more (individual). Documents required are similar to those applicable to Individual Accounts. In case of Joint Accounts special instruction for opening the accounts must be mentioned in the A/C opening form, like either or survivor, any one can operate Jointly etc.

Other products and services:

- Mudaraba Savings Account (MSA)

- Mudaraba Short Notice Deposit Account (MSND)

- Mudaraba Monthly Profit Deposit Scheme (MMPDS)

- Mudaraba Savings Bond scheme (MSBS)

- Mudaraba Muhor Savings deposit Scheme (MMSDS)

- Mudaraba Special Savings (pension) Scheme (MSS)

- Mudaraba Hajj Savings

- Mudaraba Waqf Cash Deposit Account

- Mudaraba Foreign Currency Deposit Scheme

Remittance in Bangladesh:

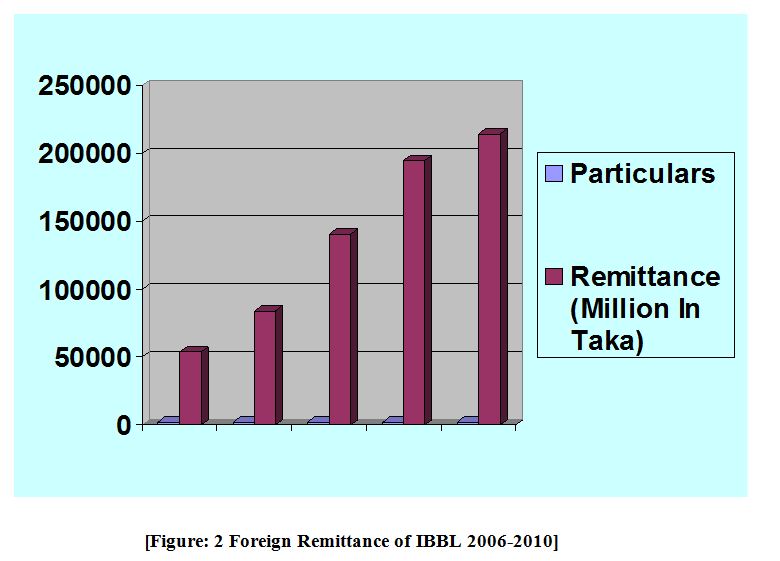

Transmission/transfer of money from one place to another is called remittance. Local remittance represents remittance that takes place within the territory of a country. In spite of global financial crisis and return of our expatriates to a good number, the foreign remittance position was outstanding in 2010. IBBL with its sophisticated software, motivated and efficient employees has consolidated its position as the market leader in foreign remittance with 10% growth in 2010 as against 39% growth in 2009. IBBL handled 27.66% of foreign remittance of the country in 2010 as against 11.61% handled by the next competitor Sonali Bank Ltd.

The total remittance business of the bank during the year stood at Tk.214, 629 million which was Tk.19, 913 million higher than the total remittance of Tk.194, 716 million received in 2009.

Table – 1: Remittance in IBBL

| Particulars | 2006 | 2007 | 2008 | 2009 | 2010 |

| Remittance(Million In Taka) | 53,819 | 84,143 | 140,404 | 194,716 | 214,629 |

IBBL has got 919 correspondent banking networks in 117 countries for smooth handling of its foreign trade and remittance business.

Remittance mainly two types:

- Inward Remittance

- Outward Remittance

Local Remittance:

Banks has a wide network of branches all over the country and offers various types of remittance facilities to the public. They serve as best media for remittance of funds from one place to another. This service is available to both customers as well as non-customers of the bank. The followings are some of the important modes of transferring funds from one to another through banks.

Remittances have been growing rapidly in the past few years and now represent the largest source of foreign income for our country.

The official data on the inflow of remittances into Bangladesh refers to the transfer of funds made by migrant workers through the banking channel is called inward remittance. Inward remittance mainly transfers in IBBL through some modes. Such as-

- Telegraphic Transfer

- Demand Draft

- Spot cash

- Foreign Demand Draft

- Foreign Currency Account etc.

Pay order issue:

Pay order is and instrument that is used to remit money within a city through banking channel the instruments are generally safe as most of them are crossed.

Charges for Issuing pay order:

| Tk. 1 to 10,000 | Tk. 18/- |

| Tk. 10,001 to 1, 00,000 | Tk. 23/- |

| Tk. 1, 00,001 to 5, 00,000 | Tk. 35/- |

| Tk. 5, 00,001 to 10, 00,000 | Tk. 46/- |

| Tk. 10,00,001 and Above | Tk. 58/- |

Vat: 15% of principle amount

Demand draft issue:

Demand Draft is very much popular instrument for remitting money from one corners of a country another. The instrument is basically used for transfer and payment. Difference between pay order and demand draft is in terms of place only payment order is used for remitting money within the city whereas demand draft is used for within the country demand draft too constitutes current liability on the part of a bank. At IBBL demand draft is not sold to people other than its customer.

Charges for issuing Demand Draft:

| Tk. 1 to 10,000 | Tk. 23/- |

| Tk. 10,001 to Above | Tk. 1 for every 1,000 |

Vat: 15% of principle amount.

Telegraphic transfer:

Telegraphic Transfer (T.T)

Telegraphic transfer is one of the fastest means of transferring money from one branch to another or from one to another. The T.T issuing bank instructs its counterpart by tested telex message regarding remittance of money. No instrument is given for T.T unless both parties have account, as money is transferred.

Charges for issuing T.T

| Tk. 1 to 10,000 | Tk. 20/- |

| Tk. 10,001 to Above | Tk. 1 for every 1,000 |

| Telephone Charge | Tk. 30/- |

Cash Section:

Cash section demonstrates liquidity strength of a bank. It also sensitive as it deals with liquid money. Maximum concentration is given while wording on this section. As far as safety is concerned special precaution is also taken. Tense situation prevails if there is any imbalance in the case account. Operation cash sections are:

- Cash receipt

- Cash Payment

- Issuance of Cheque book

- Passing Cancellation & Payment of Cheque.

Mail transfer :

IBBL has operating its service with 215 branches .Online service is now available for all customers both cash deposit & withdrawals cheque deposits & transfer.

Clearing section:

Clearing Section:

The main function of clearing section is to operate with safety and security of financial transaction of financial instrument like Demand Draft, Pay order, Cheque etc. on behalf of the customer through Bangladesh bank clearing House, outside bank clearing, inter branch clearing. This section examines in the following ways:

- Whether the paying bank within the Dhaka city

- Whether the payment is in their own branch. This cheque can be cleared by Local Bill of Collection (LBC).

- Whether the paying bank outside the Dhaka city then that cheque can be cleared by OBC (outward bills for collection).

- Clearing

Clearing is a system by which a bank can collect customers fund from one bank to another through clearing house.

- Clearing house

Clearing house is a place where the representatives of different banks get together to receive and deliver cheque with another banks.

Normally, Bangladesh Bank performs the clearing house in Dhaka, Chittagong and Khulna & Bogura .Where there is no branch of Bangladesh Bank, Sonali Bank arranges this function.

Member of clearing house:

Islami Bank Bangladesh Ltd. is a scheduled bank. According to the article 37(2) of Bangladesh bank order, 1972, the banks, which are the member of the clearing house, are called as scheduled banks. The scheduled banks clear the cheque drawn upon one another through the clearing house.

Inward Clearing:

When the cheques of its customers are received for collection from other banks, the following should be checked very carefully:

- The cheque must be crossed.

- The collecting bank must check whether endorsement is done properly or not.

- The cheque should not carry a date older than the receiving date for more than 6 months.

- The amount both in words and figures in deposit slip should be same and also it should be conformity with the amount mentioned in words and figures in the cheques.

- Entry in the IBG register & also IBC number is given.

Outward Clearing:

When the financial instruments like Payment Order ,Demand Draft, Cheques collected by specific branch within the Dhaka city and not of their own branch then the outward clearing will be functioned. The procedures of outward clearing are followed:

- The instruments with schedules to the Local branch of Islami Bank Bangladesh Ltd. with issuing an IBDA (Inter Branch Debit Advice).

- Clearing stamps are affixed on the instruments.

- Checked for any apparent discrepancy.

- The authorized signature endorses instruments.

- Endorsement gives payees account will be credited on realization.

- Particulars of the instruments and vouchers are recorded in the outward clearing register and OBC number is also given on the forwarding letter.

Responsibility of the concerned officer for the clearing cheque:

1) Crossing of the cheque

2) Computer posting of the cheque

3) Clearing seal & proper endorsement of the cheque

4) Separation of the cheque from deposit slip

5) Sorting of cheque 1st bank wise and then on branch wise.

6) Computer print 1st branch wise & then bank wise.

7) Preparation of 1st clearing house computer validation sheet.

8) Examine computer validation sheet with the deposit slip to justify the computer posting.

9) Copy of computer posting in to the store.

Cash section:

Cash section demonstrates liquidity strength of a bank. It also sensitive as it deals with liquid money. Maximum concentration is given while wording on this section. As far as safety is concerned special precaution is also taken. Tense situation prevails if there is any imbalance in the case account. Operation cash sections are:

- Cash receipt

- Cash Payment

- Issuance of Cheque book

- Passing Cancellation & Payment of Cheque .

Cash Receipt:

- Cash receipt functions are directly handled by receiving cash.

- Clients have to fill up the pay slip clearly. Any discrepancies like cutting, erasing, overwriting should not be acceptable.

- It might be acceptable only it the depositor entrust his / her error by giving a signature beside that error which was done unwillingly.

- After revising all the information needed for receiving cash ( Amount in figure, wording of that amount, date, signature, full name, A/C no etc) carefully, the authorized officer receive the cash.

- Carefully count down the amount received and match that amount with the amount mentioned in the payment slip.

- Officer has to maintain a register book for the documentation of cash receipt.

- The registrar book contain the following heads i.e. serial no, account no, amount received, signature of the depositor (verification of A/C holder’s signature is not too much mandatory) and officer’s signature.

- Then the officer writes down serial number and paste the seal on both the side of that slip.

- The officer then sign on the posted seal and upon the head “Officer”.

- Last of all cut down the right of that slip and preserve it for posting or crediting client’s A/C after the transaction period (10.00 am to 4.00 pm).

Cash Payment:

Cash payment function may be very much complicated because there is scope for making fraudulent activities. Both the client and the bank’s officers should always active about payment slip or cheque slip. Clients are always advised to keep cheque book in safe guard and it should always be filled just before withdrawal of cash. If cheque book is lost or stolen, clients should immediately order bank to stop payment against that account. Without any prior notice to stop payment, bank will not be liable for any kind of discrepancies. Payment of cash is done through three sequences. They are as in below:

Cutting Token:

- A register book is maintained for cutting token.

- Respective date should be marked first.

- Serial number should be posted previously to lessen the time because it’s a very busy segment of banking.

- Validity of the cheque should be carefully verified (validity of date- within 6 months, amount in figure and word, banks and branch name etc.)

- Whether “yourself” is written on the face of the cheque leaf or not.

- Account holders have to sign on required place as well as back side of the leaf (mandatory if bearer receives cash).

- If the account holder sends the bearer to receive cash, the leaf must be signed by the account holder and bearer name should be clearly written on the leaf at the required place. Both the bearer and account holder should sign on the leaf. Bearer will sign back to the leaf.

- Whether the leaf is “open” or “crossed”. If it is crossed, the bearer cannot withdraw cash.

- Now if the above things are ok, token can be cut down.

Checking payee’s Account through computer:

- Clients have to resubmit their leaf (other than token) in the computer counter.

- Authorized officer enter the account number into eIBS (specialized software for IBBL).

- If the account balance agree with the withdrawal of the amount of money (remaining the minimum balance), authorized officer debits the party’s account and credits the same to IBG account.

- If the operation is done by successfully, computer automatically gives an transaction ID.

- It should be written on the leaf with authorized signature.

- Then the authorized officer will pass it to another officer to verify the signature (scanned copy of card carry the picture & signature of the clients).

- After verification is done, it is then sent to the respective officer (with the seal “signature verified” and authorized signature) to pay the cash amount.

Payment of cash:

- Cash payment functions are directly handled by the paying cash counter.

- Respective officer call upon clients according to the token number. He maintains a register book also. It contains serial number, account number, account holder signature and authorized signature.

- After justifying the amount of withdrawal, payment will be made and cash payment seal will be posted with authorized signature & serial number.

Dishonor of cheques:

IBBL bankers can dishonor a cheque in the following situations:

- Insufficient Fund

- Amount in figure and word differs

- Cheque out of date / post dated.

- Drawer’s signature differs

- Payment stopped by Account holder

- Crossed cheque to be presented through a bank

- Payee’s endorsement required / Irregular / Illegible.

- Effects not cleared. May be presented again.

- Alternations in date / figure / words required drawer’s full signature.

- Clearing stamp required / requires cancellation / endorsement of the bank.

- Cheque crossed “Account payee only”.

- Collecting bank’s discharge irregular / require.

- Not drawn on us.

Deposit section:

Principles of Deposit Collection:

Deposit is the life blood of a bank. From the history and origin of the banking system we know that deposit collection is the main function of a bank. IBBL collect deposit based on the following principles

Al-Wadia Principles:

As per Shariah “Amanat” means to keep something to any reliable person / institution for safe and secured preservation of the same keeping its ownership unchanged and which will be returned to the owner of the fund on demand as its primary shape. In case of Amanat bank or any other person / institution can not use investment and amalgamate the fund of Amanat with the banks with any prior permission of the owner of the Amanat. But Al-Wadia principle indicates to some extend addition of the concept of Amanat, in which there is, a provision to obtain prior permission from the owner of the fund to use, invest, and amalgamate the said fund with their other funds and return the same within banking hour on demand. Bank is here muaddah and depositor is muaddi.

Mudaraba Principles:

Mudaraba is a form of partnership where one of the contracting parties called the ‘Shahib-Al-Mal”, who provides a specified amount of capital and acts like a sleeping or dormant partner while the other party, called ‘Mudarib’ (Entrepreneur) who provides the entrepreneurship and management for carrying on any venture, trade, industry or service with the objective of earning profit. Under this arrangement profit is distribute under ratio and loss (if any) will be borne by “Sahib-Al-Mal’.

Principles of Distribution of profit to Mudaraba Depositors:

The principles of calculation and distribution of profit to Mudaraba depositors generally followed by Islami Bank Bangladesh Limited are as under:

Mudaraba depositors share income derived from investment activities i.e. from the use of fund.

Mudaraba depositors do not share any income derived from miscellaneous banking services where the use of fund is not involved, such as communication, exchange, service charge and other fees realized by the bank in connection with sale and purchase of Demand Drafts, Telegraphic Transfers and Mail Transfer etc.

Mudaraba deposits get priority in the matters of investment over bank’s equity and other cost free funds.

Mudaraba depositors do not share any income derived from investing bank’s equity and other cost free funds.

The amount of statutory cash reserve and liquidity reserve which are required to be maintained with Bangladesh Bank is deducted from the aggregate balance of Mudaraba deposits to arrive at the net balance of profit sharing deposit.

The gross income derived from investment during the accounting year is. at first allocated to Mudaraba deposits and cost free funds according to their proportion in the total investment.

Minimum 65% is distributed to Mudaraba depositors applying the rates of weight- age shone below. Mudaraba depositor’s share of 65% of gross investment income might further be raised by the bank’s management at its discretion to rationalize the rates of profit to Mudaraba depositors but it would not be reduced during any accounting year without giving prior declaration.

Successfully mobilized Tk.291, 283 million deposits from 49,39,502 depositors.

Table – 2: Deposit of IBBL

| Particulars | 2006 | 2007 | 2008 | 2009 | 2010 |

| Deposit(Million In Taka) | 132,814 | 166,812 | 200,725 | 244,292 | 291,283 |

[Figure: 3 Deposit Mobilization of IBBL 2006-2010]

The rest of gross investment income is retained by the bank as management fee for managing the investment and for making reserve for bad and doubtful investment

Closing accounts:

| During 2011 | |||

| Closing : | Tk. 800.50 | Closing : | Tk. 804.00 |

| Highest : | Tk. 879.00 | Highest : | Tk. 900.00 |

| Lowest : | Tk. 430.00 | Lowest : | Tk. 380.00 |

Accounts section:

Types of Accounts with Terms & Conditions

(a) Al-Wadiah Current Account :

AWCA accounts are unproductive in nature as far as banks loan able investment fund is concerned sufficient fund has to be kept in liquid form, as current deposit are demand liabilities. Thus huge portion of fund becomes no performing. For this reason banks do not pay any of AWCA account holder. Businessmen and companies are the main customer of this product.

Terms & condition:

The depositors can deposit any amount in this account.

Minimum opening deposits of Tk.1000/- is required

Depositors can withdraw any amount by cheque.

No profit is allowed in this account as it is on performing

The depositors will also not bear any loss

Cheque, bills etc are collected in this account against commission

Incidental charge Tk.50/- half yearly basis is deducted from the account where minimum balance is not maintained. Closing charge Tk.300/- will be realized while closing the account.

Objectives:

To lessen the risk of holding big amount of cash

To make easier business transaction