Executive Summary:

The report represents the three months working experiences on the HSBC Limited. I have assigned to the Head Office : AnchorTower, 1/1-B, Sonargaon Road, Dhaka-1205. This report will present a study of the overall performance of HSBC and the study of credit policy practiced in HSBC. The focal point of the study is to overview the whole banking activities of HSBC, to identify their strength and weakness, to analyze their performance based on the available data and gathered the knowledge particularly on the credit operation structure and polices of the Credit Administration Department where I was intern.

This report divided into ten chapters. The first chapter of the report describes the background of the project, its scope, and objectives, methodology along with the limitation encountered. The Second Chapter deals with the overview of HSBC in the global perspective., historical background of their improvement all over world and so on. The third Chapter deals with the overview of HSBC in Bangladesh.

The fourth chapter deals with introducing the management functions, the operational functions of the Bank, and the department wise management structure. This part gives a brief look at structural and managerial overview of the Bank. Next the fifth chapter is the SWOT analysis of the Bank for the purpose of identifying their strength, weakness, opportunity and threats. Then in the sixth Chapter the performance of the Bank is evaluated both in social and economic perspective.

From the Chapter Seven, the second part of my internship report is started. This chapter helps to get the brief idea about the Credit Administration department of HSBC and their major job responsibilities. The Eight and most crucial chapter deals with the credit facilities and credit policies practiced in HSBC. This chapter describes different types of loan & advances provided by HSBC, credit sanctioning procedure, classification of loan, credit risk management and so on. The Chapter Nine analyses the performances regarding the advances & facilities.

The Final chapter deals with the findings of the report and identifies some problems faced by the Bank in sanctioning and managing the loan and advances. This chapter draws the conclusion of the report along with my personal experiences in HSBC during my internship period and some general guidelines are given which if the Bank further study or follows may gain benefit from it.

Origin of the Report:

This report is an outcome of Three month’s Internship Program(01 August 2006-01 October 2006) prepared as the partial requirement of BBA program of Department of Management & Information System, American International University-Bangladesh.

The focus of the report is “Overview of HSBC ” & “Credit Operation System of the HSBC”. Actually this is a feedback which department accepts from the students who join in an organization after the completion of theoretical part of the BBA program. My department Manager Mr. Shafiul Alam (Manager, Credit Administration Department, HSBC) assigned me the project of the report & my supervisor Mr. Shariar khan of AmericanInternationalUniversity duly approved it. The report will definitely increase the knowledge of students to know the corporate world and will teach to apply theoretical knowledge in the practical life.

Objective of the report:

General Objective:

- The research was conducted for a two-fold purpose. First to analyze the consumer banking industry of Bangladesh and second to have a practical knowledge of the professional life and to relate the four year theoretical learning to business. More importantly, it was required for the partial fulfillment of the BBA program.

Specific Objectives:

- Presentation of an introduction to the HSBC Group

- Provide information of HSBC Bangladesh

- To analyze overall banking industry of Bangladesh

- To analyze consumer banking industry of Bangladesh

- To make a comparative analysis of the asset items of PFS like home loan, car loan, personal secured loan, personal secured credit, personal installment loan with the similar products of other banks.

- To make a comparative analysis of the liability items of PFS like Current account, savings account, Bangladesh International with the similar products of other banks.

Scope:

The presentation of the organizational structure and policy of HSBC Bangladesh and investigating the strategies applied by it, provide the scope of this report. An infrastructure of the organization has been detailed, accompanied by a global perspective and look into the future. The scope of this report is limited to the overall description of the company, it’s services, and it’s position in the industry and its financial performance analysis. The scope of the study is limited to organizational setup, functions, and performances.

Methodology:

Type of research:

In this study, exploratory research was undertaken to gain insights and understanding of the overall banking industry and also to determine some of the attributes of service quality in Banks. After, that a more comprehensive conclusive research was undertaken to fulfill the main purpose of the study.

Target group:

Exploratory Research:

- Managers, Executives, customers of various banks in Bangladesh.

Conclusive Research:

- Individual customers of HSBC.

Sources of Information:

Primary data:

I have collected primary information by interviewing employees, managers by the process assigned by HSBC, observing various organizational procedures, structures, directly communicating with the customers. Primary data were mostly derived from the discussion with the employees & through surveys on customers of the organization. Primary information is under consideration in the following manner:

Secondary data:

I have elaborated different types of secondary data in my research. Sources of secondary information can be defined as follows:

Internal Sources

Bank’s Annual Report

Group Business Principal manual

Group Instruction Manual & Business Instruction Manual

Prior research report

Any information regarding the Banking sector

External Sources

Different books and periodicals related to the banking sector

Bangladesh Bank Report

Newspapers

Data collecting instruments:

In-depth interview: During the exploratory research, in-depth interviews were conducted with various managers, employees & customers of HSBC & other Banks in Dhaka.

Limitations of the Report:

Time frame for the research was very limited. The actual survey was done within a month.

Large-scale research was not possible due to constraints and restrictions posed by the organization.

The research only covers the customers of Dhaka city. Due to cost and infrastructure limitations Chittagong arena was not covered.

Part of organizational culture was written from individual’s perception and may vary from person to person.

In many cases, up to date information is not published.

To protect the organizational loss in regard of maintaining confidentiality, some parts of the report are not in depth.

Getting Relevant papers and documents were strictly prohibited.

Many procedural matters were conducted directly in the operations by the top management level, which may also gave some sort of restrictions.

Overview of HSBC:

Headquartered in London, HSBC Holdings plc is one of the largest banking and financial services organizations in the world. It began operations in Hong Kong more than 130 years ago. The HSBC Group’s international network comprises some 7,000 offices in 80 countries and territories in Europe, the Asia-Pacific region, the Americas, the Middle East and Africa.

With listings on the London, Hong Kong, New York and Paris stock exchanges, around 190,000 shareholders in some 100 countries and territories hold shares in HSBC Holdings plc. The shares are traded on the New York Stock Exchange in the form of American Depositary Receipts.

Through a global network linked by advanced technology, including a rapidly growing e-commerce capability, HSBC provides a comprehensive range of financial services: personal, commercial, corporate, investment and private banking; trade services; cash management; treasury and capital markets services; insurance; consumer and business finance; pension and investment fund management; trustee services; and securities and custody services.

HSBC Group at a glance

Assets US $ 746,335 million at 30 June 2002.

ofit (pre-tax) US $ 5067 million in 2002

Staff Some 170,000 employees in 81 countries and territories.

Share listings HSBC Holdings is listed on the London, Hong Kong, New York, and Paris stock exchanges. Trading of the company’s shares on the stock exchanges is conducted in London, Hong Kong and Paris in the US$ 0.50 ordinary shares, and in New York in the form of American Depository Shares, each of which represents five ordinary shares.

Technology : HSBC maintains one of the world’s largest private data communication networks and is reconfiguring its business for the e-age. Its rapidly growing e-commerce capability includes the use of the Internet, PC banking

over a private network, interactive TV, and fixed and mobile telephones.

Product range: Personal, commercial, corporate, investment and private banking; trade services; cash management; treasury and capital market services; insurance; consumer and business finance; pension and investment fund management; trustee services; and securities and custody services.

Key events :The HSBC Group evolved from the Hong Kong and Shanghai Banking Corporation Limited, which was founded in 1865 in Hong Kong with offices in Shanghai and London and an agency in San Francisco. The Group expanded primarily through offices established in the bank’s name until the mid-1950s when it began to create or acquire subsidiaries. This strategy culminated in 1992 with one of the largest bank acquisitions in history when HSBC Holdings acquired Midland Bank plc (now called HSBC Bank plc), which was founded in UK in 1836.

Foundation and growth of HSBC:

The HSBC Group is named after its founding member, The Hong Kong and Shanghai Banking Corporation Limited (HSBC), which was established in 1865 in Hong Kong and Shanghai to finance the growing trade between China and Europe. The inspiration behind the founding of the bank was Thomas Sutherland, a Scot who was then working as the Hong Kong Superintendent of the Peninsular and Oriental Steam Navigation Company. He realized that there was considerable demand for local banking facilities both in Hong Kong and along the China coast and he helped to establish the bank in March 1865. Then, as now, the bank’s headquarters were at 1 Queen’s Road Central in Hong Kong and a branch was opened one month later in Shanghai.

Throughout the late nineteenth and the early twentieth centuries, the bank established a network of agencies and branches based mainly in China and South East Asia but also with representation in the Indian sub-continent, Japan, Europe and North America. In many of its branches the bank was the pioneer of modern banking practices. From the outset, trade finance was a strong feature of the bank’s business with bullion, exchange and merchant banking also playing an important part. Additionally, the bank issued notes in many countries throughout the Far East.

During the Second World War the bank was forced to close many branches and its head office was temporarily moved to London. However, after the war the bank played a key role in the reconstruction of the Hong Kong economy and began to further diversify the geographical spread of the bank. The group expanded primarily through offices established in the banks name until the mid 1950s when it began to create or acquire subsidiaries. This strategy culminated in 1992 with one of the largest bank acquisitions in history when HSBC holdings acquired Midland Bank plc, which was founded in UK in 1836. The following are some key developments in the group since 1955:

1955 The Hong Kong and Shanghai Banking Corporation of California was founded.

1959 The Hong Kong and Shanghai Banking Corporation acquires The British Bank of the Middle East (formerly the Imperial Bank of Persia, now called HSBC Bank Middle East) and The Mercantile Bank (originally the Chartered Mercantile Bank of India, London & China).

1960 Wayfoong Finance Limited, a Hong Kong hire-purchase and personal finance subsidiary, is established.

1965 The Hong Kong and Shanghai Banking Corporation acquires a majority shareholding in Hang Seng Bank Limited, now the second-largest bank incorporated in Hong Kong.

1967 Midland Bank purchases a one-third share in the parent of London Merchant bank Samuel Montagu & Co. Limited (soon to be renamed HSBC Republic Bank (UK) Limited).

1971 The Cyprus Popular Bank Limited (now Laiki Bank) becomes an associated company of the Group.

1972 The Hong Kong and Shanghai Banking Corporation forms merchant banking subsidiary, Wardley Limited (now called HSBC Investment Bank Asia Limited). Midland Bank acquires a shareholding in UBAF Bank Limited (now known as British Arab Commercial Bank Limitd).

1974 Samuel Montagu becomes a wholly owned subsidiary of Midland.

1978 The Saudi British Bank is established under local control to take over The British Bank of the Middle East’s branches in Saudi Arabia.

1980 The Hongkong and Shanghai Banking Corporation acquires 51% of New York State’s Marine Midland Bank, N.A. (now called HSBC Bank USA), with a controlling interest in Concord Leasing. UK-based merchant bank Antony Gibbs becomes a wholly owned subsidiary. Midland acquires a controlling interest in leading German private bank Trinkaus & Burkhardt KgaA (now HSBC Trinkaus & Burkhardt KgaA).

1981 Hongkong Bank of Canada (Now HSBC Bank Canada) is established in Vancouver. The Group acquires a controlling interest in Equator Holdings Limited.

1982 Egyptian British Bank S.A.E. is formed, with the Group holding a 40% interest.

1983 Marine Midland Bank acquires Carroll McEntee & McGinley (now HSBC Securities (USA) Inc.), a New York based primary dealer in US government securities.

1985 New Head office building opened at Hong Kong.

1986 The Hong Kong and Shanghai Banking Corporation establishes Hong Kong Bank of Australia Limited (now HSBC Bank Australia Limited) and acquires James Capel & Co. Limited, a leading London-based international securities company.

1987 The Hong Kong and Shanghai Banking Corporation acquires the remaining shares of Marine Midland and a 14.9% equity interest in Midland Bank.

1989 A strategic alliance is entered into between The Hong Kong and Shanghai Banking Corporation and California-based Wells Fargo Bank. Midland Bank Launches First Direct, the UK’s first 24-hour telephone banking service.

1991 HSBC Holdings is established; its shares are traded on the London and Hong Kong stock exchanges.

1992 HSBC Holdings purchases the remaining equity in Midland Bank. HSBC Investment Bank plc is formed.

1993 The HSBC Group’s Head Office moves to London. Forward Trust Group Limited (now HSBC Asset Finance (UK) Limited), a Midland subsidiary, acquires Swan National Leasing, establishing the UK’s third largest vehicle contract hire company.

1994 The Hong Kong and Shanghai Banking Corporation is the first foreign bank to incorporate locally in Malaysia, forming Hong Kong Bank Malaysia Berhad (now HSBC Bank Malaysia Berhad).

1995 Wells Fargo & Co. and HSBC Holdings establish Wells Fargo HSBC Trade Bank, N.A. in California to provide customers of both companies with trade finance and international banking services.

1996 HSBC Holdings and Wachovia Corporation of the United States form a non-equity alliance to market corporate financial services worldwide. Forward Trust acquires Eversholt (now HSBC Rail (UK) Limited), a rail rolling-stock leasing company and the largest owner of electric trains operating on the UK mainline network. Marine Midland Bank acquires First Federal Savings and Loan Association of Rochester in New York. In Latin America, the Group establishes a new subsidiary in Brazil, Banco HSBC

Bamerindus S.A. and completes the acquisition of Roberts 01S.A. de Inversiones in Argentina (now HSBC Argentina Holdings S.A.).

1999 Shares in HSBC Holdings begin trading on a third stock exchange, New York. HSBC Holdings acquires Republic New York Corporation (now integreted with HSBC USA Inc.) and its sister company Safra Republic Holdings S.A. (now HSBC Republic Holdings (Luxembourg) S.A.). Midland Bank acquires a 70.03% interest in Mid-Med Bank p.l.c. (Now called HSBC Bank Malta p.l.c.), Malta’s largest commercial bank.

2000 HSBC and Merrill Lynch form a joint venture to launch the first international online banking and investment services company. HSBC reaches an agreement in principle to acquire 75% of the issued shares of Bangkok Metropolitan Bank, the eighth largest bank in Thailand. HSBC acquires Credit Commercial de France (CCF), a major French banking group. Shares in HSBC Holdings are listed on a fourth stock exchange, in Paris.

2001 Agreement is reached for HSBC to acquire Barclays Bank’s branches and fund Management Company in Greece. New 44-floor Headquarter building at London’s Canary Wharf is due to be ready for occupation.

HSBC International Network:

The HSBC Group’s international network comprises of some 7,000 offices in 80 countries. A brief list is presented below:

Country Classifications:

To ensure that key resources (management time, capital, Human resources and information technology) are correctly allocated and that the exchange of best practice is accelerated between entities, the group has classified the countries where it operates into 3 categories: the large, the major and the international.

These classifications are a function of sustainable, attributable earnings, the number of retail clients, balance sheet and size of operation. A brief presentation of this classification is shown below:

HSBC Principal Business Entities:

The group is represent by different business entities in over 80 countries and territories around the world. It would be difficult to list them all individually so the name of the major entities are shown on the following page along with their region and volume of operation.

HSBC Group Vision:

- Become the world’s leading financial services company.

- Balance Group earnings between OECD and Emerging Markets.

HSBC Group Values:

- Long term ethical client service;

- High productivity through team work;

- Confident and ambitious sense of excellence;

- International character, conservative orientation;

- Capable of creativity and strong marketing

HSBC Governing Objective:

We will beat the mean Total Shareholder Return performance of a peer group of financial institutions over a three year rolling average; and target to double shareholder returns in five years.

HSBC’s Business Principal and Values

The HSBC Group is committed to five Business Principles:

- Outstanding customer service;

- Effective and efficient operations;

- Strong capital liquidity;

- Conservative lending policy;

- Strict expense discipline;

HSBC also operates according to certain Key Business Values:

- The highest personal standards of integrity at all levels;

- Commitment to truth and fair dealing;

- Hand-on management at all levels;

- Openly esteemed commitment to quality and competence;

- A minimum of bureaucracy;

- Fast decisions and implementation;

- Putting the Group’s interests ahead of the individual’s;

- The appropriate delegation of authority with accountability;

- Fair and objective employer;

- A merit approach to recruitment/selection/promotion;

- A commitment to complying with the spirit and letter of all laws and regulations;

- The promotion of good environmental practice and sustainable development and commitment to the welfare and development of each local community.

HSBC Brand & Corporate Identity:

The Hexagon logo of HSBC derives from HSBC’s traditionally flag, a white rectangle divided diagonally. Like many other Hong Kong company flags in the last century, the design of the flag was based on the cross of ST.Andrew, The Patron Saint of Scotland.HSBC brand & corporate identity represents what HSBC wants its brand to mean to its customer. It is derived from the groups:

Corporate Character:

HSBC is a prudent, cost conscious, ethically grounded, conservative, trustworthy international builder of long-term customer relationships.

Basic Drives:

Higher productivity, Team Orientation, Creative Organization & Customer Orientation.

Vision:

To be the world’s leading financial company.

The essence of HSBC brand is integrity, trust and excellent customer service. It gives confidence to customers, value to investors & comfort to colleagues.

HSBC in Bangladesh:

The HSBC Asia Pacific group represents HSBC in Bangladesh. HSBC opened it’s first branch in Dhaka in 17th December, 1996 to provide personal banking services, trade and corporate services, and custody services. The Bank was awarded ISO9002 accreditation for its personal and business banking services, which cover trade services, securities and safe custody, corporate banking, Hexagon and all personal banking. This ISO9002 designation is the first of its kind for a bank in Bangladesh. The Hong Kong and Shanghai Banking Corporation Bangladesh Ltd. primarily limited its operations to help garments industry and to commercial banking. Latter, it is extended to pharmaceuticals, jute and consumer products. Other services include cash management, treasury, securities, and custodial service.

Realizing the huge potential and growth in person banking industry in Bangladesh, HSBC extended it’s operation to the personal banking sector in Bangladesh and within a very short span of time it was able to build up a huge client base. Extending its operation further, HSBC opened a branch at Chittagong, two branch offices at Dhaka (Gulshan and Mothijheel) and an offshore banking unit on November’1998. Another branch has been opened at Dhanmondi on 1st of March, 2003. At 28th February 2003, the number of employees of this bank in Bangladesh was 175.

HSBC Bangladesh is under the strict of supervision of HSBC Asia Pacific Group, Hong Kong. The Chief Executive Officer of HSBC Bangladesh manages the whole banking operation of HSBC in Bangladesh. Under the CEO there are heads of departments who manage specific banking functions e.g. Personal banking, corporate banking, etc.

Currently HSBC Bangladesh is providing a wide range of services both two individual and corporate level customers. In 2000 the bank launched a wide array of personal banking products designed for all kinds of (middle and higher middle income) individual customers. Some such products were Personal loans, car loans, etc. Recently the bank launched three of its personal banking products – Tax loan, Personal secured loan & Automated Tele Banking (ATB) service. These products are designed to meet the diverse customer needs more completely.

HSBC in Bangladesh also specializes in self-service banking through providing 24-hour ATM services. Recently it opened two new ATM’s at Shantinagar & Banani to better satisfy those geographic segments. In total the branch currently has 9 ATM’s (5 on-site & 4 offsite) located at various geographical areas of Dhaka & Chittagong.

HSBC Bangladesh Overview:

Name of the Organization: The Hong Kong Shanghai Banking Corporation Bangladesh LTD

Year of Establishment: 1996

Head Office: AnchorTower, 1/1-B Sonargaon Road

Dhaka 1205, Bangladesh

Nature of the organization: Multinational company with subsidiary group in Bangladesh.

Capital: Asset: TK 4380 million

Deposit – Tk 3985 million

Advance – Tk 2755 million

Shareholders: HSBC group shareholders

Products: Savings & deposit services.

Loan products.

Corporate and Institutional services.

Trade services

Hexagon

Management: Mr. David C. Griffith

Chief Executive Officer

Mr. Mamoon Mahmood Shah

Head of Personal Financial Services

Mr. Adil Islam

Head of Corporate Banking

Mr. Syed Akhtar Hossain Uddin

Human Resource Manager

Mr. Munir Hussain

Marketing Manager

Mr. Wasim Adnan Wahed Chief Operating Officer

Number of Offices: 5 (Dhaka, Motijheel, Gulshan, Dhanmondi & Chittagong)

Number of ATM’s: 10

Number of employees: 195

Technology: Offers full online banking from branch to branch and also from Dhaka to Chittagong.

Service Coverage & Customers: Serves individual and corporate customers within Dhaka & Chittagong.

HSBC Bangladesh currently provides services from two of its full service branches one in Dhaka and the other one in Chittagong. Besides these offices there are two personal banking Booth offices located at Gulshan & Motijheel. There are currently 8 ATM’s operating in Dhaka and 1 in Chittagong. The list of these offices are shown below along with there their addresses:

Branches & Booths:

- Dhaka Main Office (Full service branch with two ATM’s)

AnchorTower, Sonargaon Road – Dhaka

- Gulshan Office (Personal Banking Booth with one ATM)

Gulshan Avenue, Dhaka

- Motijheel Office (Personal Banking & Remittance office with 1 ATM)

Rajuk Avenue, Motijheel- Dhaka

- Chittagong office (Full service branch with one ATM)

Osman Court, Agrabad – Chittagong

- Dhanmondi Office (Full service branch with one ATM)

Rd. 27 Dhanmondi Dhaka

Functional Areas of HSBC Bangladesh

Management of HSBC Bangladesh:

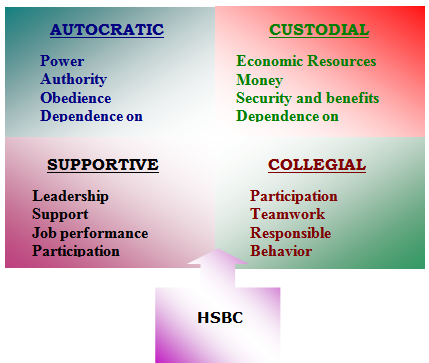

HSBC, Bangladesh is one such company that has to over come a lot of hurdles to reach the position it now holds. At present, Mr. Steve Banner is the CEO; Mr. Adil Islam is the chief of Corporate Banking; Mr. Adnan Wahed is COO, Mr. Mamoon Mahmud Shah is the Chief of Personal Banking, and Mr. Syed Akhtar Hossain is the Human Resource Manager at HSBC Bangladesh.These five men at the top carried out their management roles exhaustively. They equally contributed to HSBC’s superior leadership, by carrying out their unique roles. They worked well together, respecting each other’s abilities, & arguing openly & without any rancor when they disagreed.To maintain a close touch with the organization each man works in separate area of HSBC’s complex. Their offices are indistinguishable from all other cubicles where HSBC’s junior executives & secretaries work in. There are no office walls in HSBC and all the staff starting from the CEO to the lower operating level employee share the same premises under one roof. There are no Specialized cabins for top management and executives and also no executive dining rooms. This has created a management team that is unified, cohesive & energetic.

Each and every employee of HSBC takes pride of being an employee at HSBC and his or her pride comes from the freedom of direct communication with the top management. The management of HSBC is supportive in the sense that the top management deliberately supports the suggestions, values, ideas, innovation and hard work of the employees and officer. Again high amount of employee participation is encountered in the management process. There are also systems for awards, incentives, and status for innovative ideas and hard works. Again the management style can also be termed as Collegial as high amounts of team work and participation exists between the top and bottom parts of HSBC. Thus according to my perspective of management style at HSBC Bangladesh falls somewhere between supportive and collegial. A graphical presentation is shown below:

HSBC follows a 4 layer management philosophy in Bangladesh. These are Managers, Executives, officers & Assistant officers. The CEO is the top most authority of all the levels. Managers are the departmental heads who are responsible for the activities of their departments. They are the heads of the department and formulate strategies for that department. e.g. Human Resources Manger. Executives have the authority next to managers. They are basically responsible for certain activities & organizational functions. e.g. Admin Executive. These two layers represent the management level of HSBC Bangladesh.

Officers are the next persons to stand in the hierarchy list. They are the typical mid-level employees of HSBC organizational hierarchy. The operating level employees of HSBC who are ranked as Assistant Officer fill the last layer of this hierarchy. They perform they day-to-day operational activities of HSBC. An organizational hierarchy chart is shown below:

Chief Executive Committee:

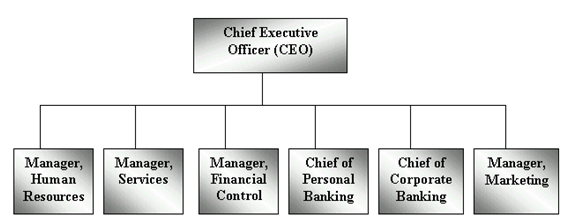

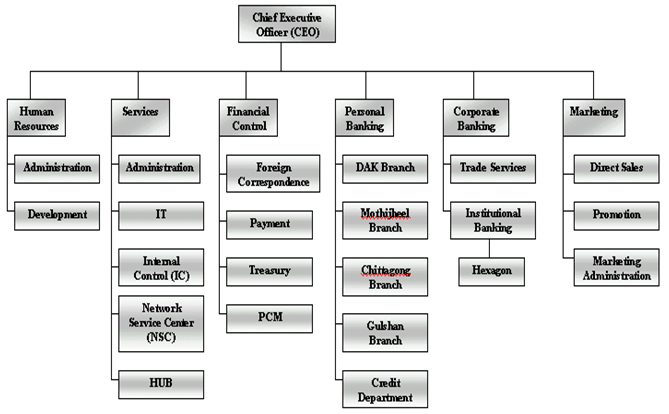

The organizational structure of HSBC Bangladesh is designed according to the various service and functional departments. The Chief Executive Officer (CEO) heads the chief executive committee, which decides on all the strategic aspect of HSBC. The CEO is the person who supervises the heads of all the departments and also is the ultimate authority of HSBC Bangladesh. He is responsible for the all the activities of HSBC Bangladesh and all its consequences. He administers all the functional departments and communicates with the department heads for smooth functioning of the organization. The HSBC Chief Executive Committee is formed with the heads of all departments along with the CEO. The structure of this top-most authority is shown in the following figure. Besides the CEO the CEC is staffed with 6 more managers: Manager of Human Resources, Manager of Services, Manager of Financial Control Department, Chief of Personal Banking, Chief of Corporate Banking and Manager of Marketing.

Functional Departments of HSBC:

Human Resource Department:

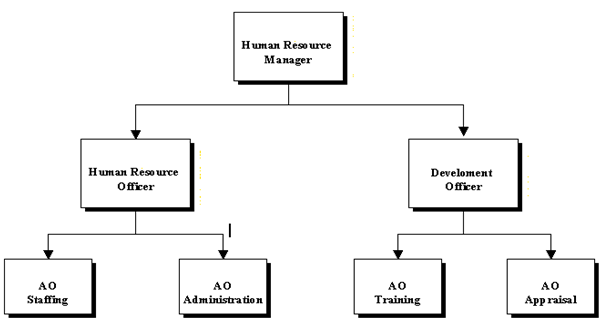

The Human resource Manager currently heads this department. The major functions of this department are Recruitment, Training and developments, Personnel Services and Security. The HR department is very are very much concerned with the discipline that is set up by the HSBC group. HSBC group has got strict rules and regulations for each and every aspect of banking, even for non-banking purposes; i.e. The Dress Code. All these major personnel functions are integrated in the best possible way at HSBC, which results in its higher productivity. The Human resource officer monitors the employee staffing and administration activities. The Training officer supervises Training, development & rotation activities. The structure of the HR department is shown below:

Structure of Human Resource Department:

Recruitment, Training and Development:

HSBC Bangladesh limited follows a standard procedure for recruitment and selection. However there is no set time period when this recruitment and selection takes place. Each Departmental head places the requisition for recruitment to the Human resource officer, if any vacancy is created due to (1) Retirement, (2) Resignation (3) Death, or (4) Extra work load.

The process for the recruitment of personnel for managerial and non-managerial level differs slightly but the basic steps are same in both the cases. The steps are-

Step- I Initial Screening:

Step- II Screening by Departmental Heads:

Step- III Filling of the HSBC Job Application Form (HJAF)

Step- IV Screening on the basis of SAF:

Step- V Initial Interviewed:

Step –VI Selection for written test

Step- VII Written test

Step –VIII Evaluation of test papers

Step –IX Selection of Final interviewees

Step –X Final interview

Step- XI Documentation Check

Step – XII Medical Examination

Step – XIII Probationary Appointment:

Step- XIV confirmation

In order to enhance the efficiency of the employees, HSBC gives emphasis on the both theoretical and practical training for its personnel. All the training and development programs are aimed at two basic reasons – (1) skill development (2) motivation through counseling and persuasion to change value system. For the top management or senior Managers there is provision for overseeing training arranged by HSBC group. For the mid-level manager or other managerial level there is provision for regional training courses.

Performance Appraisal:

The company follows both rating and descriptive systems for the performance appraisal. Although the appraisal system is non-participative but the employees are annually assessed with a joint consultation with their immediate supervisor and departmental head.

Rating is mainly done on the following factors-

i) Knowledge of work

ii) Accuracy and Reliability

iii) Speed

iv) General intelligence

v) Sense of responsibility and duty

vi) Diligence

vii) Initiative and self confidence

viii) Readiness to work for and with others.

Welfare Activities:

HSBC has many well-structured welfare policies for its employees. These include well-structured wage & salary policy, medical facility, sports & cultural facilities, provision for loans, free uniform etc. These welfare policies aim at strengthening the relationship of the employees to the organizations and make them more responsible in their respective positions. The brief description of the major welfare policies are stated below:

Wages and Salary Administration:

HSBC follows a well-defined wage structure and fringe benefits for its employees. The wage structure is updated periodically (Two years terms) by the management. The major deciding factors are-

a) Profitability of the company

b) Average cost of living in the country due to year to year basis inflationary trend

c) Status of wage earners in similar organization

d) Restrictive conditions given by the government from time to time

e) Financial benefits status in the company

Components of existing wage structure:

Base basic structure

Home rent

Conveyance allowance

Allowances & Benefits:

Besides the regular wage and salary HSBC provides other financial benefits to the employees. These includes-

- Gratuity: 30days basic wage for each completed year of service.

- Provident fund

- Group Insurance Scheme

- Core Leave facilities (27 days annually)

- Core Leave allowance

- Medical allowance (up to 20,000 annually)

- Hospitalization allowances (up to 25,000 annually)

- Marriage Leave

- Maternity leave

- Bonus: (Festival bonus, 13month bonus)

- Lower rate employee loans.

Operations of HSBC Bangladesh:

HSBC activities are performed through functional departmentalization. So, the departments are separated according to the functions they perform. Within the major departments there are some other subsidiary departments that allow smooth operation of their own major departmental function.

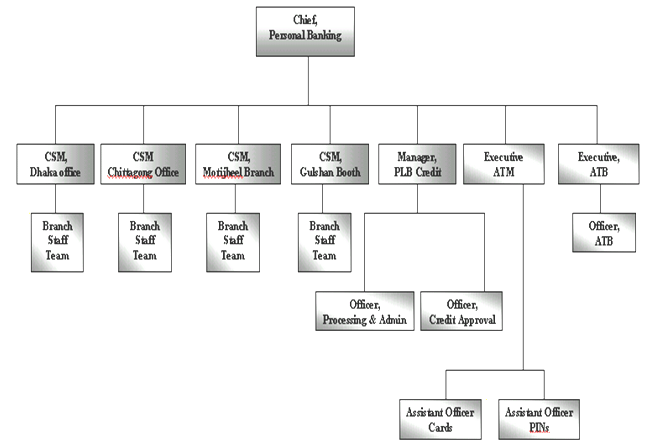

Personal Banking Division (PLB):

PLB is the most flourishing department of HSBC Bangladesh. This department basically deals with the management of products and services offered to the in individual consumers. Within a span of only five year HSBC PLB has grown tremendously and is still growing with its innovative products and service offerings. Chief of PLB, JOE B. Bennett a British national, manages this department. He is the person behind the astounding growth of PLB department in HSBC Bangladesh. Chief of PLB manages and supervises the Personal Banking activities of the branch network of HSBC Bangladesh. The 4 branches of HSBC basically deal with the personal banking activities and provide various accounts services to individual customers. The departments under PLB credit is shown in the following diagram:

Branch network:

There are four branches of HSBC, 3 situated at different Dhaka and 1 at Chittagong. Only the Dhaka office (head office) branch & Chittagong branch deals with both corporate and personal banking. There functions are to provide various financial services to the consumers. These include customer services, sale of various PLB products, opening new accounts, providing cash, remittance and other teller services, etc. the branches are quite decentralized for better delivery of services to customer and have their own premises and facilities.

Credit Department:

The personal banking credit department deals with the consumer credit schemes such as the Personal loan, Car loan. Education loan, tax loan, personal secured loan, etc. which are tailored to meet the demand of individual customers. The manager of PLB credit who approves and administers all the activities heads this department. He is staffed with one loan approval officer, one loan processing officer, two assistant officers and one MIS clerk. The approval officer mainly rejects or approves the credit requests. After being checked by the approval officer, the credit requests go to the processing officer for further processing of the application.

ATMCenter:

The ATM center ensures smooth operation of the ATM machines that are located at Dhaka and Chittagong. The ATM center is responsible for regular replenishment of the off-site ATM’s and servicing of all the ATMs. Currently a total 8 ATMs are in operation. The ATM center also deals with issuance, termination and servicing of the ATM cards. On an whole, the ATM center is the department that is solely responsible for all the activities related to ATM and is the facilitating department that enables customers 24 hour banking support.

ATB centre:

ATB refers to Automated Tele Banking. This department deals with the back office servicing of the HSBC phone banking services provided to customers. This department is basically responsible for the activation of ATB, ATB pin generation, and ATB security management, ATB blocking and troubleshooting of all ATB problems. This department is fairly new and was constructed on January’2001.

Some Other Individual Loan Facilities provided by Personal Financial Services Department(PFS) of HSBC

Personal Installment Loan :

HSBC offers a low cost Personal Installment Loan solution to meet your lifestyle and professional needs backed by local knowledge and global expertise. You can now get your mind at ease by making HSBC a part of your life

Personal Installment loan is any purpose loan. For the customers’ convenience, it is categorized by:

- Professional Loan : to meet the professional needs.

- Lifestyle Loan : to add comfort to your personal life.

- Wedding Loan : to fulfill the dream of a perfect wedding and a good beginning of a new life.

- Festival Loan : to maximize the purchasing power during various festivals.

The following loans with different benefits are also available under personal installment loan :

- Travel Loan : to fulfill the dreams to take an overseas vacation or travel to an exotic place of one’s choice.

- Motorbike Loan : With a motorbike loan from HSBC, overcome all the obstacles and realize the dream.

- Student Loan : to secure the future or getting the Graduate or Post Graduate degree or completing the professional degrees while you are still working.

Car Loan : Every people have a dream to buy a car for a long time. Now with car loan from HSBC, any one can realize that dream.

Home Loan : The decision to buy or renovate a home is probably the most important investment decision any body will ever make. HSBC put together a loan facility to assist in purchasing new apartment or to help you during renovation of home.

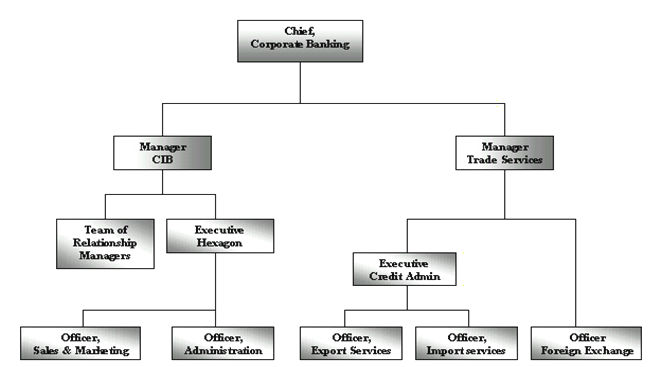

Corporate Banking Division :

This division if HSBC provides financial services to organizational clients. HSBC is a worldwide leader in banking and financial services whose success is based on its relationships with its corporate clients. Whether it is locally or around the world, HSBC offers a comprehensive range of services that can be tailored to the individual needs of the company. The Head of this department is the Chief of Corporate Banking. He is also the Vice-CEO of HSBC Bangladesh. The chief of CB manages the activities of corporate banking of HSBC Bangladesh. Corporate Banking of HSBC Bangladesh includes Corporate Institutional Banking (CIB) Trade Service (HTV), and Hexagon. These sub-divisions are discussed briefly in the following sections along with a structure chart of Corporate Banking division of HSBC Bangladesh.

Corporate Institutional Banking (CIB):

As their major customers operate internationally, HSBC services them internationally. Operating through the major centers and in close liaison with HSBC Investment Bank, Corporate and Institutional Banking provides the full range of the Group’s capabilities at local and global levels, with a particular focus on payments and cash management, trade and securities custody. HSBC also offers local financial institutions and banks access to wide range of financial services available on an international basis. The services are tailored to suit the needs of the companies. CIB has two separate wings: Relationship management department and Hexagon. These are discussed below:

Relationship Management Department:

The RM department consists of various relationship managers who are assigned to different corporate client to better satisfy their needs. These RM’s communicate with the clients and are solely responsible for the companies they deal in. Any information regarding a corporate client must be communicated through the respective RM assigned to that corporate client. A relationship manager may be assigned more than one company and this decision depends on the chief of Corporate Banking.

Hexagon:

The Hexagon department deals with all aspects related to HSBC’s unique banking software product – Hexagon. It is the global Electronic Banking system of HSBC, which offers the customers more convenient and efficient banking than ever before. It is an innovative desktop banking system developed by the HSBC group, which operates via the group’s proprietary worldwide communications network.

HSBC Trade Services (HTV)

Trade service is known by various names in other banks, e.g. Trade Finance Foreign Exchange, Foreign Trade etc. However, the functions are the same. As the name suggests, this department is involved in facilitating trade, both international & within Bangladesh. HSBC is the leading provider of trade finance and related services to importers and exporters in Asia. Trade is considered a core business of the group. The group’s presence in 81 countries of the world gives a good opportunity to control both ends of a trade transaction and keep the business within the Group. The various awards it has won from the leading publications of the world acknowledge HSBC’s excellence in trade.

- Export Services:

To benefit from HSBC’s export services, you do not need to have special facilities, or even an account with us. Simply request your buyers to advise your documentary credits through us and benefit immediately from our international network.

Pre-shipment Finance

Post-shipment Finance

Documentary Credit Advising

- Import Services :

With over 130 years of experience supporting importers globally, HSBC is well positioned to fulfill your trading needs. A full range of import services handled by experienced staff is available, ensuring that your import documents are processed without delay.

Simply apply to us for import facilities, and we can begin handling your imports immediately.

Documentary Credits

Import Collections

Import Finance

Shipping Guarantee

- Import Collections

Collections offer a cost-effective but secure means of trading internationally. Using these instruments, the importer only effects payment in exchange for the documents of title for the goods shipped. If these are found to be unacceptable, payment can be refused, giving the buyer peace of mind.

However, the above is subject to Central Bank rules, therefore should consult with the Bank before considering import collections.

- Import Finance

Whether the client import using documentary credits or collections, HSBC are prepared to consider providing import finance for the client.

HSBC can offer the customers Import Loan or a Trust Receipt, both loans granted to an importer for payment of import bills.

- Shipping Guarantee

In certain situations your goods may arrive in port before the shipping documents have been processed through the banking system. In these circumstances, HSBC can issue a shipping guarantee, allowing you to take control of the goods from the shipping company without the bill of lading. The advantages of using HSBC for this are as follows:

Rapid Issuance

Shipping guarantees are only of value if they are issued immediately. HSBC can issue shipping guarantees as soon as the application is made, meaning you can release your goods from the carrier immediately.

Financial Strength

HSBC issued shipping guarantees are universally accepted by shipping companies. This means you can always be assured that you will get your goods on time.

- Trade Express:

Trade Express is an umbrella service, which combines traditional trade products, document delivery services, reinforced by HSBC’s proprietary state of the art e-banking (Hexagon and Electronic DC Advising), designed to provide tailored solutions for our priority customers from the convenience of their own office remote banking.

With this product you can now execute all your trade transactions faster, cheaper, and with more accuracy than ever before and most importantly, from the convenience of your own office

The trade service department has two separate subsidiaries: Credit Administration & Foreign Exchange Division.

Credit Administration department basically deals with all the documentation, processing, administration and disbursement of the import-export services provided to corporate clients. This department is known to be the heart of HSBC trade services that administers and manages all the trade tools and facilities provided by HSBC Corporate Banking. Some important aspects of this department are LC advising, documentation, OD facilities, guarantees, etc.

The For-ex division of trade services is solely concerned with the management of Foreign exchange inflow and outflow. The For-ex division of trade service in relation with NSC and FCD manages the foreign currency traffic of HSBC that originates from Corporate Banking and trade services.

Finance Department of HSBC Bangladesh:

This is considered as the most powerful department of HSBC. It keeps tracks of each and every transaction made within HSBC Bangladesh. It is headed by Manager of FCD who ensures that all the transactions are made according to rules and regulation of HSBC group. Violation of such rules can bring serious consequences for the lawbreaker. The functions of FCD are briefly discussed below along with an organ gram of the department:

Foreign Correspondence (FC):

FC keeps records of all the accounts of HSBC. All the vouchers, notes, advices and transaction reports of the branches are sent to FC for record keeping purposes. FC also prepares the financial statements for the banks and decided upon banks assets and liabilities. It also deals with the returns that are submitted to the Central Bank on regular interval.

Treasury:

This department works under FCD. Their main job is to take decisions regarding purchase and sell of foreign Currency. The purpose of Treasury’s operations is to utilize the funds effectively and arrange funds at a lowest possible rate of interest, through maintaining effective relationship with other banks and following the Government rules and foreign exchange regulations.

Payment and cash Management (PCM):

PCM deals with the inter-bank payment. PCM strategies are designed to ensure efficiency, profitably and comprehensive support.

Country wide Payments:

Most corporate treasurers cannot afford to spend time worrying about routine payments. HSBC in Bangladesh has the technology to put you in better control of routine operations and has been successfully handling payment requirements throughout the nation for its corporate clients. We provide you with benefits, which include:

- Reduction in payment time.

- Availability of payment details through Hexagon.

- Easy reconciliation of payments/receipts through Hexagon statement.

- Centralization of control of payments.

- Network coverage of almost 200 locations nation-wide.

Country wide collection:

As receivable management is crucial to your financial cycle, we have developed products for you to efficiently manage your requirements and reduce cost. The services and benefits include:

- Cost reduction through efficient fund management.

- Detailed MIS on cash collection, resulting in better management.

- Account reconciliation done through Hexagon.

- Centralization of control of all your cash and instruments.

- Network coverage of almost 200 locations nation-wide.

- Quicker cash collection into a central account, resulting in greater earnings.

Hexagon offers comprehensive cash management services in an easy-to-use and highly secure system. This provides you timely and accurate account information and gives you total control over your finances.

You can pay to third parties at ease and can effect instant fund transfer between your own accounts. This will take effect instantly. So no more signature and fax hassle for an instruction.

Marketing Department:

The sixth major department of HSBC is the marketing department. The marketing department of HSBC play a vital role in fostering the continuos growth HSBC in Bangladesh. A manager is assigned to this department who looks after the overall marketing operation of HSBC in Bangladesh. This department is basically concerned about marketing the company’s products, services and building a strong corporate image. The marketing department of HSBC has three subdivisions: Direct Sales, Promotion & Marketing Administration. This division are discussed below:

Direct Sales (DS):

An executive is assigned to this part of the marketing department. The Direct Sales division coordinate & manages the sales activities of all the Mobile Sales Officers (MSO) of HSBC Bangladesh. The MSO’s basically makes sales of the company various Personal Banking products such as, savings accounts, consumer loan, etc outside the banking premises. There are a total of more than 50 mobile sales officers (MSO) employed in the cities of Dhaka and Chittagong. A MSO’s are assigned to specific branches for making sales activities more smoothly. The DS executive sets sales strategies & targets for the Sales officers and manages the whole team of MSO’s

in Bangladesh. The direct sales department also decides upon the commission and remuneration of the mobile sales officers as their salary structure is based on sales performances. Thus this part of the marketing division is very important for the overall growth of the Personal Banking Division.

Promotion:

This part of the marketing department deals with all the promotional activities of HSBC Bangladesh. Prime responsibilities of this department are: Maintaining strong public relations with various media intermediaries, Advertising the companies products and services, building a strong corporate image of HSBC in Bangladesh.

Public Relations:

The promotion department organizes various environmental and social activities in order to build a strong corporate image of HSBC in the minds of customers as well as in the media. Maintaining strong relationship with news media is another major duty of this department.

Advertising:

The promotion also coordinates all the advertising of HSBC products within Bangladesh. Some of the advertising tools that are frequently used by the company are as follows:

a) Newspapers Advertising: Regular advertisements of various products and services of HSBC are given in some of the countries most renowned daily newspapers.

b) Billboards: Huge colourful billboards with HSBC logo are found in various major areas of Dhaka and Chittagong. These billboards emphasize on the needs of customers and shows HSBC logo as solution to their needs.

c) Road Side Signposts: Medium sized multi colour signposts focusing on various products of HSBC are found on the roadsides of various posh areas such as, Gulshan, Dhanmondi, Baridhara, Motijheel, etc.

d) Mailers: various product updates and new product information are regularly sent to existing customers of HSBC.

e) Broachers: Various colourful broachers featuring specific products of HSBC are being displayed and distributed to existing and potential customers via branch offices and Mobile sales officers.

Marketing Administration:

This department formulates & executes various marketing strategies of HSBC Bangladesh. This department also administers various marketing research activities on the existing and potential customers of HSBC. Some such research activities are: mystery shopping, critical incident surveys, customer suggestion surveys, etc. The results of these surveys are integrated while formulating various marketing strategies. This department also deals with the billing and invoicing of various marketing & advertising costs of HSBC Bangladesh.

In these are the major departments of HSBC Bangladesh. Except the branches all other departments are situated at HSBC Bangladesh head offices located at AnchorTower, Kawran Bazar. Most of HSBC’s operation and activities are operated centrally from the head office. But to deal with customers more completely, the branches are given considerable authority and they operate in a more decentralized manner but subject to verification of the respective departments.

Services Department of HSBC:

This is an integral and vital part of the bank. The services department ensures smooth operation and functioning within and between all the departments of HSBC. It also provides continuous support to the core banking activities of HSBC. The Manager of Services heads this department who formulates and manages various critical issues of the services function of HSBC. He is followed by a group of executives who are the heads of various subsidiary divisions that operate within the services department. The services department is considered as the backbone of all other departments. The various subsidiary division within this department are Administration, IT, Internal Control (IC), Network Services Center (NSC), and HUB. A structure of the services department is presented below followed by a briefing of the subsidiary divisions:

Administration:

Like that of any other organizations, the Admin department of HSBC makes sure that the organizations moves on with all its departments and staffs operating according to all the rules and regulations of the company. It also prevents any bottlenecks within the work process and ensures smooth functioning. The admin department has two divisions – general administration and Business support services.

The general admin division is pretty much similar to the admin departments of other companies that ensure discipline and regulatory concerns. The business support services provide supports to the departments during employee leaves and sudden terminations so that the department can function without problems.

IT:

This department gives the software and hardware supports to different departments of the bank. As HSBC is engaged in online banking, the role of IT is very crucial for the bank. This department is the most active department of HSBC where employees always stand by to solve any problems in the system. The managers and executives of IT division work continuously to develop the total IT system of HSBC so that it can be operated with ease, accuracy and speed.

Internal Control:

HSBC has internal auditors who visit on regular basis and submit the report to the higher authority for audit purposes. This gives different departments the chance to know their mistakes and take necessary corrective actions. Again, the Bank annually administers a company wide audit program to evaluate the overall performance of the bank in Bangladesh.

HSBC universal banking (HUB):

The HSBC banking system is called HUB. HSBC does the online banking and it is HUB, which sets up the parameter for that. This HUB is linked with the HSBC group via satellite and each and every transaction made by HSBC within Bangladesh is being recorded at the HSBC Asia-pacific headquarters at Hong Kong via HUB. Thus the HUB is the most powerful and important equipment of HSBC Bangladesh that monitors and tracks any fraud and faults made with HSBC Bangladesh.

Network Services Centre (NSC):

This department can be described as the ‘Power House of HSBC Bangladesh. NSC does the back office job for the bank. The main four jobs that are performed by NSC are Clearing, Scanning of signature cards, issuing checkbooks and sending & receiving Remittances. NSC looks after the clearing process of HSBC and makes necessary contact with the central bank for maintaining account flows. All the customer signatures are scanned in this department and are entered into the system. NSC also issues checkbook for new and old accounts based on requisition from various branches. ‘Remittance’ is a banking term, which means ‘Transfer of funds through banks’. When a bank remits on behalf of its customers, it is termed as outward remittance. On the other hand, when the bank receives the remittance on behalf of the bank, it is inward remittance. The following are the methods that NSC used to remit money for customers: Telegraphic Transfer (TT), Demand Draft (DD) & Cashier’s Order.

SWOT Analysis of HSBC

SWOT Analysis:

In order to develop marketing strategy SWOT analysis is very vital. In the process of making a SWOT marketer identifies the strength and weakness of the company and also the opportunities and threat to the company. The SWOT analysis of HSBC has given below.

Strength

| Weakness

|

Opportunity

| Threat

|

SWOT ANALYSIS:

Strengths

Strong corporate identity:

- HSBC is the leading provider of financial services Identity worldwide. With its strong corporate image and identity it can better position in the mind’s of customers. This image has helped HSBC grab the personal banking sector of Bangladesh very rapidly.

Distinct operating Procedure:

- HSBC in known worldwide for its distinct operating Procedures procedure. The company’s Managing for Value strategy satisfy customers needs better and also keeps the firm profitable.

Distinct schedule:

- Everyone in HSBC from the appraiser to the top management has to work to the same schedule towards a different aspect of the same goal, interfacing simultaneously at all level over quite a long period of time.

Strong employee bonding and belongings:

- HSBC employees are one of the major assets of the company. The employees of HSBC have a strong sense of commitment towards organization and also feel proud and a sense of belonging towards HSBC. The strong organizational culture of HSBC is the main reason behind this strength.

Efficient Performance:

- HSBC provides hassle free customer service to its client base comparing to the other financial institutions of Bangladesh. Personalized approach to the needs of customers is its motto.

Young enthusiastic Workforce:

- The selection & recruitment of HSBC emphasizes on having the skilled graduates & postgraduates who have little or no previous work experience. The

logic behind is that HSBC wants to avoid the problem of ‘garbage in & garbage out’. & this type young & fresh workforce stimulates the whole working environment of HSBC.

Empowered Work force:

- The human resource of HSBC is extremely well thought & perfectly managed. As from the very first, the top management believed in empowered employees, where they refused to put their finger in every part of the pie. This empowered environment makes HSBC a better place for the employees. The employees are not suffocated with authority but are able to grow as the organization matures.

Companionable Environment:

- All office walls in HSBC are only shoulder high partitions & there is no executive dining room. Any of the executives is likely to plop down at a table in its cafeteria & join in a lunch chat with whoever is there. One of the employees has said, “Its exciting to know you may see & talk to the top management at any time. You feel a real part of things”.

Equalization:

- At HSBC workshops are conducted periodically. On the workshops, all people participate as equals, with new members free to openly challenge top managers.

MBO

- HSBC also has Management by Objectives (MBO) everywhere. Each person has multiple objectives. All the employees must have to get the approval of their bosses on what they are going to do. Later they review as how well they have performed their job with their management as well as the peer group.

One-to-one” meeting

- The MBO makes the review a communication device among various groups. The key to the system is a “one-to-one” meeting between a supervisor & a subordinate. In the meeting, the problems in dealing with customers are put forward first & everyone dug it to solve them.

Modern equipment & technology:

- HSBC owns the best banking and information technology in Bangladesh. It ultra modern banking systems starting from terminal pc’s to HUB’s are based on the international HSBC group standards and are the latest. The Hexagon product is one of the best examples in this context.

Visually appealing facilities:

- HSBC has some of the best visually appealing branches and office premises in Dhaka & Chittagong that highly attracts customers attentions and customers also feel the international environment while banking with HSBC.

Weaknesses

Narrow operating span:

- HSBC has a very narrow operating span in Bangladesh. It has only 2 full service branches in Bangladesh situated only at Dhaka and Chittagong. Various geographic segments are currently not availing the services of HSBC due to inconvenient branch location or absence of neighborhood branches.

Absence of strong Marketing Activities:

- HSBC currently don’t have any strong marketing activities through mass media e.g. Television. TV ads playa vital role in awareness building. HSBC has no such TV ad campaign.

More Innovative products must be offered:

- In order to be more competitive in the market HSBC should come up with more new attractive products. This one of the weakness that HSBC is currently passing through.

Lack of customer confidence:

- AS HSBC is fairly new to the banking industry of Bangladesh average customers lack the confidence in HSBC and judge the bank as an average new bank.

Too many contract workers:

- HSBC has contract workers who lack the commitment with superior quality service and also are pretty dissatisfied as being a contract worker. This hampers the bank’s service quality as a whole.

Low remuneration Package:

- The remuneration package for the entry level officers are considerable low. Since other foreign and local banks offer a more lucrative salary package, it will be difficult for HSBC to attract MBA ‘ s in future with its current salary package.

Diversification:

- HSBC can peruse a diversification strategy in expanding its current line of business. The management can consider options of starting merchant banking or diversify in to leasing and insurance. As HSBC is one of the leading provider of all financial services, in Bangladesh it can also offer these services.

International Credit Cards:

- This is one of the most popular and emerging product in Bangladesh which offers customers total financial mobility. Various other banks and institutions are currently offering this product. HSBC can also take advantage of this product and grab the market share.

High Cost for Maintaining Account:

- The account maintenance cost for HSBC is comparatively high. This is very often highlighted by other banks. In the long run this might turn out to be a negative issue for HSBC.

Opportunities

Acquisition:

- HSBC is one of the experts in acquiring various firms and organizations. In Bangladesh it can also diversify quickly by acquiring various local established banks and increase it’s total operation within Bangladesh rapidly.

Distinct operating procedures:

- Repayment capacity as assessed by HSBC of individual client helps to decide how much one can borrow. As the whole lending process is based on a client’s repayment capacity, the recovery rate of HSBC is close to 100%. This provides

HSBC financial stability & gears up HSBC to be remaining in the business for the long run.

Country wide network:

- The ultimate goal of HSBC is to .expand its operations to whole Bangladesh. Nurturing this type of vision & mission & to act as required, will not only increase HSBC’s profitability but also will secure its existence in the log run.

Experienced Managers:

- One of the key opportunities for HSBC is its efficient managers. HSBC has employed experienced managers to facilitate its operation. These managers have already triggered the business for HSBC as being new in the market.

Huge Population:

- Bangladesh is a developing country, to satisfy the needs of the huge population, a large amount of investment is required. On the other hand building EPZ areas and some Govt. policies easing foreign investment in our country made it attractive to the foreigners to invest in our country. So, HSBC has a large opportunity here.

Weak marketing massage by local & foreign banks:

- The basic assumption of trade business is that customer will come to the bank and ask for service that is why local & foreign banks are not that much enthusiastic about letting know their service features. This an opportunity for HSBC to develop massages regarding their services.

Threats

Upcoming Banks:

- The upcoming private local & multinational banks posses a serious threat to the existing banking network of HSBC: it is expected that in the next few years more commercial banks will emerge. If that happens the intensity of competition will rise further and banks will have to develop strategies to compete against and win the battle of banks.

Similar Products are offered by other Banks:

- Now day’s different foreign and private banks are also offering similar type of product with an almost similar profit margin. So, if all competitors fight with the same weapon, the natural result is declining profit.

Default Culture:

- This is a major problem in Bangladesh. As HSBC is a very new organization the problem of non-performing loans or default loans is very minimum or insignificant. However, as the bank becomes older this problem will arise enormously and the bank may find itself in a more threatening environment. Thus HSBC has to remain vigilant about this problem so that proactive strategies are taken to minimize this problem.

Industrial downward trend due to recession, inflation & Unemployment:

- Bangladesh is economically unstable country. Flood, draught, cyclone, and newly added terrorism have become an identity of our country. Along with inflation, unemployment also creates industry wide recession. These caused downward pressure on the capital demand for investment.

Chapter 6 : Performance Analysis of HSBC

1. Performance of HSBC in the Community:

Each year, employees select charities to focus fundraising and donation activities. HSBC further supports employees and their chosen charities by making corporate donations. Some of the charities that the Bank are involved in this year include:

2004

Charity Concert

Warm clothes to the poor

Chittagong Lions Foundation

The Children Leukaemia and Support Services

The Friendship

The Seid Trust charity

2003

Charity Golf Tournament

Warm clothes to the poor

International Federation of Red Cross and Red Crescent Societies (IFRC)

Shishu Polli Plus

Blood donation drive with Sandhani and Red Crescent Society

SAARC Women’s Association

Out of Focus

2002

Charity Golf Tournament

Acid Survivors Foundation

Centre for the Rehabilitation of the Paralysed (CRP)

Others

HSBC believes that support for primary and secondary education, in particular for the underprivileged, is crucial to the future development and prosperity of every country. School of Hope is an example of this support.

2004

School of Hope

2003

School Environment Fair 2003 in Gazipur

School of Hope

HSBC is deeply conscious of its responsibilities to the environment, believing that the needs of today’s society should not be fulfilled at the expense of future generations, and that sustainability is paramount.

2004

World Environment Day photography competition

2003

World Environment Day photography competition

2002

Investing in Nature

2.. Economic Performance of HSBC :

HSBC is continuing their business all over the world. By analysis their financial statement of their Annual Report it is seen that the Bank is going to be profitable and dynamic financial institutions day by day by expanding their business and providing the improved services to the customers. The performance of HSBC is mentioned below:

| The Hongkong and Shanghai Banking Corporation Limited | ||||

2003 | 2002 | 2001 | 2000 | |

| For the year | HKDm | HKDm | HKDm | HKDm |

| Profit on ordinary activities before tax | 34,797 | 33,661 | 34,635 | 34,636 |

| Profit attributable to shareholders | 25,797 | 25,167* | 26,237 | 25,965 |

| ||||

| At year-end | ||||

| Shareholder’s funds | 110,012 | 91,134* | 83,129 | 90,812 |

| Total capital | 138,858 | 126,486* | 109,171 | 108,244 |

| Current, savings and other deposit accounts | 1,669,704 | 1,473,539 | 1,378,119 | 1,395,702 |

| Total assets | 2,148,741 | 1,868,700* | 1,742,741 | 1,761,970 |

| Risk-weighted assets | 1,008,824 | 895,496 | 836,946 | 817,967 |

| Ratios | % | % | % | % |

| Return on average shareholders’ funds | 27.4 | 29.2* | 32.2 | 31.8 |

| Post-tax return on average total assets | 1.46 | 1.61* | 1.73 | 1.77 |

| Cost : income ratio | 39.1 | 38.6 | 38.2 | 37.2 |

| Net interest margin | 2.24 | 2.54 | 2.57 | 2.55 |

| Capital adequacy ratios | ||||

| total capital | 12.1 | 12.7 | 13.0 | 13.2 |

| tier 1 capital | 10.3 | 9.8 | 9.5 | 9.4 |

| * Figures for 2002 have been restated to reflect the adoption of Hong Kong Statement of Standard Accounting Practice 12 (revised) on ‘Income taxes’. | ||||

Principal Activities:

The Hongkong and Shanghai Banking Corporation Limited (“the Bank”) and its subsidiary and associated companies (“the group”) provide a comprehensive range of domestic and international banking and related financial services, principally in the Asia-Pacific region.

Reserves:

Profits attributable to shareholders, before dividends, of HK$25,797 million have been transferred to reserves. During the year, a deficit of HK$1,397 million, net of the related deferred taxation effect, arising from professional valuations of premises and investment properties held by the Bank and the group was debited to reserves. Details of the movements in reserves, including appropriations there from, are set out in note 31 to the financial statements. The Directors do not recommend the payment of a final dividend.

(In HK$ million)

Group Bank Associated Companies

Total Reserves at December 2003 49,959 145,911 822

Total Reserves at December 2002 42,694 115,198 781

(Source: Annual Report 2003)

Share Capital

The authorised ordinary share capital of the Bank at 31 December 2003 is HK$30,000 million divided into 12,000 million ordinary shares of HK$2.50 each (2002: HK$18,000 million divided into 7,200 million ordinary shares of HK$2.50 each). The authorised preference share capital of the Bank at 31 December 2003 is US$7,500,500,000 comprising 500,000 cumulative redeemable preference shares of US$1 each and 7,500 million non-cumulative irredeemable preference shares of US$1 each (2002: US$4,174,500,000 comprising 500,000 cumulative redeemable preference shares of US$1 each and 4,174 million non-cumulative irredeemable preference shares of US$1 each).

Issued and fully paid Bank and Group

2003 2002

HK$m HK$m

Ordinary share capital 16,254 16,254

Preference share capital 35,349 28,686

51,603 44,940

Group Profit & Economic Profit of HSBC:

The group’s internal performance measures include economic profit, a measure which compares the return on the amount of capital invested in the group by its immediate holding company with the cost of that capital. Economic profit is used by management as one of the measures to decide where to allocate resources so that they will be most productive.

Attributable profit for 2003 reported by The Hongkong and Shanghai Banking Corporation Limited (‘the Bank’) and its subsidiary and associated companies (‘the group’) increased by HK$630 million, or 2.5 per cent, to HK$25,797 million in 2003. Profit on ordinary activities before taxation increased by HK$1,136 million or 3.4 per cent, to HK$34,797 million.

Some are parts:

Internship Report on Hongkong and Shanghai Banking Corporation Limited(Part 1)

Internship Report on Hongkong and Shanghai Banking Corporation Limited(Part 2)