Cash earnings per share (cash EPS), more generally referred to as operating cash flow, is a profitability ratio that compares the cash flow of a company to the outstanding number of shares. It is exceptional from the more broadly utilized net benefit metric, earning per share (EPS), which just considers overall gain per share. Money EPS is not the same as customary earning per share (EPS), which takes the organization’s total compensation and partitions it by the quantity of offers extraordinary. As such, EPS gauges the amount of the organization’s benefit that can be distributed to each portion of the stock, while Cash EPS quantifies how much income can be designated to each portion of the stock. Cash EPS can prove a more accurate measure of financial and operational health, free of non-cash components, such as depreciation used in profit-based EPS measures.

An organization with higher cash earnings per share is considered to show better monetary execution and have a superior capacity to produce income. Cash EPS can be utilized to look at the organization against its friends or against its own previous outcomes. Cash EPS doesn’t consider any non-money components. For instance, depreciation, which is part of profit-based earnings per share estimates, is not included. Because of this, CEPS can be a more precise measurement of the financial and operational states of a company. The larger the CEPS of a firm, the better it is assumed that its success is over for the specific time considered.

Example of Cash Earnings Per Share

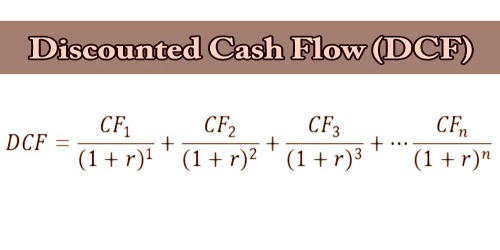

When comparing trends within a business and trends among different companies in similar industries, the CEPS ratio is useful. By integrating non-cash transactions such as amortization, depreciation, and deferred tax back into Net Income to find operating cash flow, we calculate Cash EPS. Then this is separated by the number of shares.

Cash EPS = Operating Cash Flow / Diluted Shares Outstanding

where:

EPS = earnings per share

All the information expected to compute money EPS can be found in the fiscal reports and notes to accounts. For the most precise CEPS figuring, it is pivotal to decide the entirety of the non-money components in the pay explanation. A non-cash transaction is one that is documented in the revenue statement of the business but does not include real cash flow during the recorded period. Depreciation cost, for instance, is deducted from net profits but does not necessarily require any cash outflow. Therefore, to eliminate the accounting effect, this must be added back to net profits.

Operating cash flow, which is reported in the cash flow statement of a company, is essentially EBITDA with the inclusion of a working capital change and all other non-cash changes. The amount of outstanding shares can be simple or diluted and can be found in the notes to the accounts and all the remaining shares are included in the statement of income. While investigating an organization, a standard monetary examination compares cash flow from operations (CEPS) to revealed total compensation. At the point when an organization has a high money income, it might demonstrate that they are performing well overall. Typically, analysts consider the ratio’s average growth rate for a period of years. As a consequence, this means that a positive indicator is a strong growth rate over time.

When operating cash flow begins to substantially lag behind recorded net income, a common warning sign for aggressive revenue recognition frequently emerges. It could be a red flag for acknowledging revenue too quickly when this happens. It is also possible to equate the CEPS of one company with those of other companies within the same sector and with similar varieties of goods. This is one key advantage offered by CEPS over ordinary EPS. Since CEPS might be adapted to all non-money things, generally drawn from the board gauges, it empowers experts to think about the qualities for a few organizations.

Convertible securities apply to the outstanding warrants of a company, stock options, convertible debentures, and preferred shares convertible. The diluted EPS of the business would often be lower than the cash EPS. Simple EPS can be an inaccurate indicator of success as it is very vulnerable to accounting manipulation. Accordingly, while assessing likely speculation, financial specialists, for example, Warren Buffet lean toward money-based measures to manage their investigation. Another significant part of the CEPS is the enormous disparity between typical EPS and CEPS. In the event that the hole is at any rate half or more, this is viewed as enormous. It may be an indication that clever accounting strategies were used by the management to mask the actual results of the company. But this distance must also be discussed from a realistic perspective.

Cash earnings per share show the capacity of the organization to create income that can be utilized for some, things, including overhauling its obligations, delivering investors’ profits, and undertaking different exchanges. In order to better understand the financial state of the organization, analysts must go deeper to see what is actually causing the decline or rise. In certain situations, a company can buy back from the open market, if the price is reasonable, to offset the dilution of stock options. All the more as of late, stock buybacks, as opposed to stock profits, have been a mind-boggling famous strategy to restore benefits to investors. It is possible to make a case that this helps boost EPS by reducing outstanding shares, thus helping corporate executives game earnings per share growth to juice performance-based compensation plans.

Information Sources: