EXECUTIVE SUMMERY:

As a part of Internship program for Business Graduate students, each of the students needs an organizational attachment. Being attached with Mercantile Bank Limited, this study has been undertaken to fulfill the internship purpose. During a specified period of internship, the students are required to prepare a report on the organization from where he has completed his internship.

Mercantile Bank Limited is a private commercial bank, which is operating its business last 9 years. The bank has achieved a tremendous success during this short span of time and established itself as a progressive and dynamic financial institution in the country. The bank is widely acclaimed by the business community, starting from small businessmen/entrepreneurs to the big traders/industrial group, including the top rated corporate clients who hold pragmatic outlook and financial solution.

The objective of the report is to meet the compulsory requirement of submitting a report that is an essential part of the internship program and to have a practical knowledge in professional life. The objective is to discuss with the “Product Management of Mercantile Bank Limited, Khatungonj Branch”.

Both primary and secondary data have been used in this research. Conducting a servey through questionnaire collected primary data. The main source of secondary data were Bank’s previous research materials, published documents, annual report etc.

Some times it happens that the researcher did not collect whole information from the customers. As a result some of the questionnaire of those have been missed out which effects the findings of the research.

Apparently, this report has been prepared on “Product Management of Mercantile Bank Limitrd, Khatungonj Branch”. And I tried to gather some knowledge through the contact with the customers through the questionnaire. By the research I found that somr customers are satisfied with corresponding with the bank and some are dissatisfied with the bank.

During my work, I have faced various obstacles. By the Grace of God and by the help of some related person, I have successfully overcome those problems.

Table of Contents:

Introduction of the Study:

This report has been prepared as a practical requirement of MBA Program. After completing the academic courses a student has to complete a 3-month organizational attachment. So, after completion of 3-month organizational attachment at Mercantile Bank Limited, this report has been prepared.

This report on “Product Management” on Mercantile Bank Limited, Khatungonj Branch, was initiated as a part of Internship Program, which is a MBA degree requirement of the Business Administration of Premier University Chittagong. This ort is being submitted to Prof. Dr. Milon Kumar Bhatecharjee, Dean, Department of Business Administration, Premier University, Chittagong.

Since the MBA Program is an integrated, practical, theoretical method of learning, the student of this program are required to have practical exposure in any kind of business organization.

Intention of the Study:

The intention to prepare this report are stated below:

- Briefly observe the banking environment of Bangladesh and look at Mercantile Bank Limited as an Organization at some length.

- To know about the overall banking activity.

- To know about the management style and organizational structure of Mercantile Bank Limited.

- To identify the problems and weakness of the banking systems of Mercantile Bank Limited.

- Market scenario of banking sector and the current position of Mercantile Bank Limited.

- To know the product and services of Mercantile Bank Limited.

- To identify the major strength of the bank’s customer service division.

- To provide probable suggestions for the improvement of the customer service quality and the overall development of the bank.

Methodology:

In the organization part, much information has been collected from different published articles, brochures, web site and previous internship report. All the information incorporated in this report has been collected from the following sources:

- Observation from the total internship period.

- Operational process.

- Discussion with the officials.

- Data from company documents and bank’s computerized information system.

- Statement of Affaires of the Bank.

- Periodic bulletins published by the bank.

- Bank’s other published documents.

- Some textbooks.

- Internet.

Scope:

The scope of the repor5t is limited to the overall description of the bank,, its services, its position in the industry and its competitive advantages. The scope is also defined by the organizational set-up, functions and performances. Here, Mercantile Bank Limited is compared with the different foreign and local banks as well.

Limitations:

The limitations, in preparing this repost, are given below:

- I had no pervious experience to direct a survey program that’s why this report might not bring the same result what the authority expect.

- There was a limited scope for me to deal with the banking activities directly.

- The people, to whom I made my survey, most of them were not cordial to give their recommendation.

- Within the short period of time, it is not possible for me to study every thing about the Mercantile Bank Limited.

- The management people and the responsible officers of the bank are passing very busy time. So that, they could not give me enough time for collection information.

“Mercantile Bank Limited” – at a Glance. 4

“Mercantile Bank Limited” – at a Glance

Mercantile Bank limited emerged as a new commercial bank to provide efficient banking services and to contribute socio-economic development of the country. Mercantile Bank Limited is a scheduled Bank under the private sector in Bangladesh formed with the bank company act 1991, the rules and regulation issued by the Bangladesh Bank, the company Act1994, the securities and exchange rules 1987 and other applicable laws and regulations in 1999. The Bank commenced its operation on June 2, 1999. The first branch was opened at 61, Dilkusha Commercial Area in Dhaka on the inauguration day of the Bank. The number of branches of the bank stood at 35 at the end of 2006 of which 27 branches are located at major trade centers of the country while remaining 8 branches are at the rural areas of the country with more than 700 employees. During this short span of time, the Bank has been successful in positioning itself as a progressive and dynamic institution in our country.

The authorized capital of the bank was BDT 1,200.00 million of 12,000,000 ordinary share of BDT 100 each as of June 2006. The shares of the bank have been listed both in Dhaka Stoke Exchange and Chittagong Stoke Exchange and being treated at price higher than the book value.

As per guideline of Bangladesh Bank, the Bank adopted BIS (Bank for International Settlement) risk adjusted capital standards of measure capital adequacy. The Bank’s capital adequacy ratio stood at 10.39% 2005 as against 10.24% in 2004.

The bank has acquired 150000 shares of International Development and Leasing Company of Bangladesh Limited (IDLC) from International Finance Corporation (IFC), sponsor of IDLC. This shareholding represents 10% of IDLC’s share capital, The Bank acquired each share at BDT 863.00 against the face value of BDT 100.00, Market price per share of IDLC stood at BDT 1007.25 as of December 2005.

The Bank provides a board range of financial services to its customers and corporate clients. About 30 famous and renowned Industrialists came forward to establish this bank. The Board of Directors consists of eminent personalities from the realm of commerce and industries of the country.

The Bank is manned and managed by qualified and efficient professionals. Md. Abdul Jalil selected, as a Chairman of the board of directors and Mr. Shah Md. Nurul Alam

is the Managing Director and CEO of the bank. He brings with him a wealth of experience of managing private sector banks in the country. The board of directors consists of 13 members.

The Bank purchased a land measuring 1 bigha 2 chattaks located at Gulshan, Plot 3, Block CEN (C), Gulshan Avenue, Gulshan, Dhaka 1212, Municipality Holding 105, Gulshan Avenue, Gulshan during the year 2005 for Bank’s own use. The land is under litigation and possession of the land is yet to be taken. In this connection a provision has been made as per Bangladesh Bank’s instruction. 6

Vision:

“Would make finest corporate citizen”.

Mission:

Will become most caring, focused for equitable growth based on diversified development of resources and nevertheless would remain health and gainfully profitable Bank.

Objective

Strategic objective:

- To achieve positive Economic Value Added (EVA) each year.

- To be market leader in product innovation.

- To be one of the top three Financial Institution in Bangladesh in terms of cost efficiency.

- To be one of the top three Financial Institution in Bangladesh in terms of market share in all significant market segments we serve.

Financial objectives:

- To achieve a return on shareholders’ equity of 20% or more, on average.

Core Values:

For the customers:

- Providing with caring service by being innovative in the development of new banking product and services.

For the shareholders:

- Maximize wealth of the bank.

For the employees:

- Respecting worth and dignity of individual employees devoting their energies for the progress of the bank.

For the community:

- Strengthening the corporate values and taking environment and social risks and reward into account.

Registered Office:

The registered office the Mercantile Bank Limited is its Head Office that is-

Mercantile Bank Limited

61, Dilkusha Commercial Area,

Dhaka-1000, Bangladesh.

PABX: +880-2-9559333, 9553892, 9561140..

Fax: +880-2-9561213.

Telex: 642509 MBL ID BJ.

E-mail: mbl@bol-online.com

Website: www.mblbd.com

Timeline of the company:

| December 28, 2006. | Opening of 35th branch at Sapahar (Naogaon). |

December 28, 2005.Opening of 28th branch.

May 15, 2005.Retirement of 5 sponsors Director of the bank after 6 consecutive years.

December 29, 2004.Opening of 25th branch.

February 26, 2004.Listed in Chittagong Stock Exchange.

February 16, 2004.Listed in Dhaka Stock Exchange.

December 24, 2003.Opening of 20th branch.

October 21-22, 2003.Subscription of Share.

June 30, 2003.Publication of Prospectus for IPO.

June 03, 2002.Opening of 15th branch.

March 27, 2001.Get permission to start business at Khatungonj.

October 29, 2000.Opening of 10th branch.

June 02, 1999.Commencement of Business.

May 20, 1999.Incorporation of the Bank.

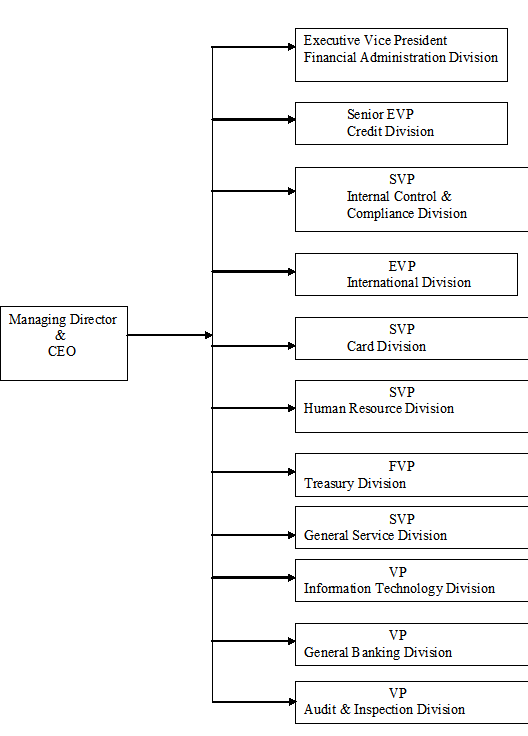

Organ gram:

The organ gram of the bank are shown in below:

Management Team:

The management of the mercantile Bank Limited is vested on a board of Directors, for overall supervision and directions on policy matters. The power of general supervision and control of the affairs of the bank is exercise by the president and the CEO of the bank who is also the Managing Director of the board.

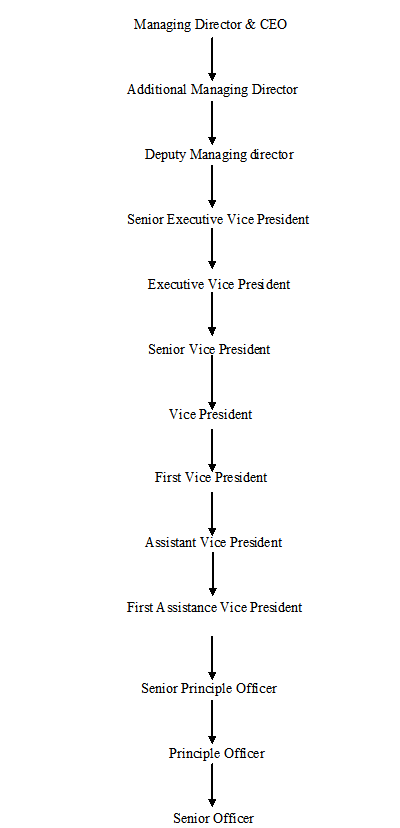

The hierarchy of The Mercantile Bank Limited is as Follows:

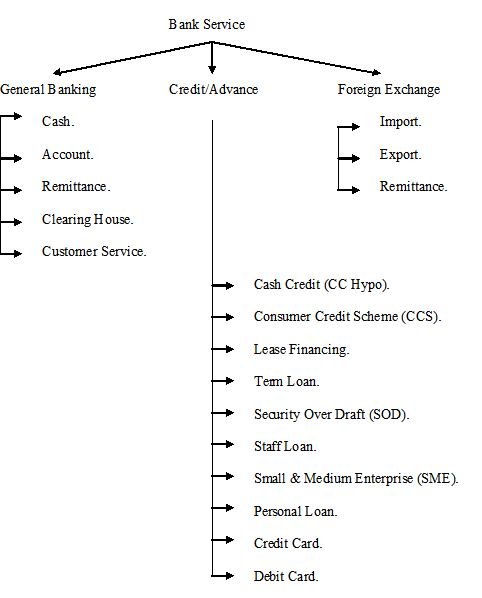

2.10. Structure of the Banking service:

Major financial product

Monthly Savings Scheme:

The prime objective of this scheme is to encourage people to build up a habit of saving. Under this scheme, one can save a fixed amount of money every month and get a lucrative amount of money after five, eight or ten years.

Family Maintenance Deposit:

Under this scheme, one can deposit certain amount of money for five years and in return he will receive benefits on monthly basis. Benefits start right from the first month of opening an account under the scheme and continue up to five years.

Double Benefit Deposit scheme:

Under this scheme, depositor’s money will be doubled in a 6-year period.

Special Savings Scheme:

Under this scheme, depositor’s money will be tripled in a 15-year period.

Pension and Family Support Deposit:

Pension and Family Support Deposit has been evolved especially for old age. Under this scheme one can get life long benefit if he deposits specific amount per month for a period of 10 or 15 years. The scheme can also be opened in the name of minors.

Consumers’ Credit Scheme:

Consumers’ Credit is relatively new field of collateral-free finance of the bank. People with limited income can avail of this credit facility to buy household goods including computer and other consumer durables.

Small Loan Scheme:

This scheme has been evolved especially for small shopkeepers who need credit facility for their business and cannot provide tangible securities. 13

Lease Finance:

This scheme has been designed to assist and encourage the genuine and capable entrepreneurs and professionals for acquiring capital machineries, medical equipments, computers and other items. Terms and conditions of this scheme have been made easier in order to help the potential entrepreneurs to acquire equipments of production and services and repay gradually from earnings on the basis of ‘Pay as you earn’.

Doctors’ Credit Scheme:

Doctors’ Credit scheme is designed to facilitate financing to fresh medical graduates and established physicians to acquire medical equipments and set up clinics and hospitals.

Rural Development Scheme:

Rural Development Scheme has been evolved for the rural people of the country to make them self-employed through financing various income-generating projects. This scheme is operated on group basis.

Women Entrepreneurs Development Scheme:

Women Entrepreneurs Development Scheme has been introduced to encourage women in doing business. Under this scheme, the bank finances the small and cottage industry projects sponsored by women.

SME Financing Scheme:

Small and Medium Enterprise (SME) Financing Scheme has been introduced to assist new or experienced entrepreneurs to invest in small and medium scale industries.

Personal Loan Scheme:Personal Loan Scheme has been introduced to extend credit facilities to cater to the credit needs of low and middle-income group for any purpose. Government and semi-government officials, employees of autonomous bodies, banks and other financial organizations, multinational companies, reputed private organizations and teachers of recognized public and private schools, colleges and universities are eligible for the loan facilities.

Car Loan Scheme:

Car Loan Scheme has been introduced to enable middle-income people to purchase Cars/SUVs/Jeeps. Government and semi-government officials, employees of autonomous bodies, banks and other financial organizations, multinational companies, reputed private organizations, teachers of recognized public and private universities and business men are eligible for the loan facilities.

Key financial information:

(BDT in million)

| 1999 | 2001 | 2003 | 2005 | |

| Authorized Capital | 800.00 | 1200.00 | 1200.00 | 1200.00 |

| Paid-up Capital | 245.00 | 276.85 | 639.53 | 999.27 |

| Total Capital | 261.06 | 596.44 | 1235.23 | 2045.85 |

| Deposit | 3104.63 | 12234.70 | 16285.19 | 25727.43 |

| Loans & Advances | 871.46 | 6707.42 | 10775.95 | 21857.05 |

| Investment | 70.18 | 882.47 | 2107.26 | 3517.68 |

| Fixed Assets | 17.97 | 67.76 | 81.50 | 366.80 |

| Total Assets | 3411.45 | 13085.86 | 18324.73 | 28890.48 |

| Import | 2096.20 | 12268.00 | 20380.80 | 33271.90 |

| Export | 1011.00 | 13085.86 | 18324.73 | 24108.57 |

| Remittance | 42.60 | 308.40 | 474.00 | 679.10 |

More information

Funding Structure:

(BDT in million)

| Components | Amount | % Of Total |

| Deposits | 25727.43 | 89.05 |

| Paid-up Capital | 999.27 | 3.46 |

| Reserves | 1046.58 | 3.62 |

| Others | 1117.20 | 3.87 |

| Total | 28890.48 | 100.00 |

Total Income:

(BDT in million)

| Components | Amount | % Of Total |

| Interest Income | 2720.38 | 78.34 |

| Commission | 300.61 | 8.66 |

| Exchange Gains | 259.20 | 7.46 |

| Other Income | 192.32 | 5.54 |

| Total | 3472.51 | 100.00 |

Total Expenses:(BDT in million)

| Components | Amount | % Of Total |

| Interest Expenses | 1987.16 | 79.32 |

| Salaries & Allowances | 282.88 | 11.29 |

| Rent, Rates, Taxes etc. | 69.65 | 2.78 |

| Stationeries, Printing & Advertisements | 33.37 | 1.33 |

| Depreciation & Repairs | 30.33 | 1.21 |

| Postage, Stamps & Telecommunication | 16.22 | 0.65 |

| Other Expenses | 85.67 | 3.42 |

| Total | 2505.28 | 100.00 |

Asset Portfolio: (BDT in million)

| Components | Amount | % Of Total |

| Loans & Advance | 21857.05 | 75.65 |

| Investment | 35517.68 | 12.18 |

| Cash | 1878.41 | 6.50 |

| Money at Call & Short Notice | 625.00 | 2.16 |

| Balance with other Bank | 118.19 | 0.41 |

| Other Assets | 894.15 | 3.10 |

| Total | 28890.48 | 100.00 |

SWOT Analysis:

Strengths

| Weaknesses

|

Opportunities

| Threats

|

“Mercantile Bank Limited” – Khatungonj Branch:

Mercantile Bank Limited – Khatungonj Branch is the 12th branch of the bank. It got permission to start its business on 27th march, 2001. The then Commerce Minister of The Government of Bangladesh and the Chairman of the Bank inaugurated the Branch on 3rd June, 2001. Now the Branch is Headed by the First Vice President Mr. Md. Jamal Uddin. The Branch consists of 18 officers. It is one of the important Branch in Chittagong as well as whole Bangladesh. The Bank provides all the banking services of their customers and clients at their best. Some financial information of Mercantile Bank Limited – Khatungonj Branch are given as below:

As on: 30/12/2007.

No. | Particulars | Amount (BDT)

|

1. | Total Assets | 236,29,73,652.45 |

2. | Total Deposit | 98,43,05,781.53 |

3. | Total Advance | 153,24,39,259.51 |

4. | Demand Deposit | 3,84,28,053.81 |

5. | Time Deposit | 91,29,57,271.39 |

6. | Total Liabilities | 346,81,30,366.24 |

7. | Letter of Credit (General) | 35,25,75,000.00 |

The hierarchy of the Branch is:

First Vice President

&

Head of Branch

Staff Officer

&

Manager Operation

Senior Executive Officer

Executive Officer

Officer

Assistant Officer

Trainee Assistant Officer

Activities of the Bank. 21

Activities of the Bank:

| 4.1. General Banking Division: |

4.1.1. Customer Service:

Mercantile Bank Limited provides their best service to their clients. They are improving their service day by day to their customer. They provide the following services to their customers:

- Account Opening.

- Customer Inquiries.

- Account Transfer.

- Account Close.

- Cheque Book Issue.

- Issuing of – Demand draft (DD).

Pay Order (PO).

Security Deposit Receipt (SDR).

Pay Slip (PS).

Account Opening:

Like all the Bank Mercantile Bank Limited has also two types of deposit e.g. two types of accounts. These are:

a) Demand Deposit.

b) Time Deposit.

a) Demand Deposit:

Demand Deposit are general types of deposit or account which is operate through cheque, accounts holder can deposit his or her money in his account and also he can withdraw money from his account. The Demand Deposit accounts are –

- Savings Account (SB),

- Current Account (CD),

- Short Term Deposit (STD) and

- Foreign Currency Account in Dollar (FCAD). 22

b) Time Deposit:

It is the special scheme account for the customer. In such account customer deposit money for a certain period to gain some profit. The time Deposit Accounts are –

- Fixed Deposit Receipt (FDR),

- Masik Sanchaya Scheme (MSS),

- Double Benefit Deposit Scheme (DBDS),

- Monthly Benefit Scheme (MBS).

The number of accounts of the customers maintain by the Mercantile Bank Limited are as follows:

(As on 31.12.2007)

Types Of Account |

No of Customers

Current Account (Customer)

355

Savings Account (Customer)

780

Savings Account (Stuff)

41

Short Term Deposit

52

Time Deposit

578

Scheme Deposit

7867

Loans

469

Others

62

Total

10204

Checklist for Accounts Opening:

Before providing the documents, a customer(s) must fill up the prescribed account opening form provide by the Mercantile Bank Limited. A complete account opening form include:

- Client Information.

- Specimen Signature Card.

- Cheque Requisition Form.

- Nomination Form.

- Transaction Profile.

- Declaration.

- KYC (Know Your Customer).

Most important point of a new account holder(s) is that s/he must have an introducer who has an account in the Mercantile Bank Limited. There is a part for introducer in the account opening form and the account holder(s) photograph must be abstract by the introducer. The account holder(s), along with the form, should submit following documents:

Savings Account:

a) Photo – 2 copies of account holder(s).

b) Nationality Certificate or valid Passport or Voter ID card of account holder.

c) Photo – 1 copy of nominee(s).

Current Account:

For Proprietorship Business:

a) Photo – 2 copies of account holder.

b) Nationality Certificate or valid Passport or Voter ID card of account holder.

c) Photo – 1 copy of nominee(s).

d) Trade License.

e) TIN Certificate of Proprietor.

For Partnership Business:

a) Photo – 2 copies of all partners.

b) Nationality Certificate or valid Passport or Voter ID card of account holder.

c) Photo – 1 copy of nominee(s).

d) Partnership deed (Notary Public).

e) Partnership registration certificate.

f) Letter of partnership (Printed form, MF – 06, MF – 07).

g) Resolution.

h) Trade License.

i) TIN Certificate of Partners.

24

For Private Limited Company:

a) Photo – 2 copies of all Directors.

b) Nationality Certificate or valid Passport or Voter ID card of account holder.

c) Photo – 1 copy of nominee(s).

d) Articles of Association.

e) Memorandum of association.

f) Certificate of incorporation.

g) Resolution of Board of Directors (With all Directors Signature).

h) Trade License.

i) TIN Certificate of Directors.

For Public Limited Company:

a) Photo – 2 copies of all Directors.

b) Nationality Certificate or valid Passport or Voter ID card of account holder.

c) Photo – 1 copy of nominee(s).

d) Articles of Association.

e) Memorandum of association.

f) Certificate of incorporation.

g) Resolution of Board of Directors (With all Directors Signature).

h) Trade License.

i) TIN Certificate of Directors.

j) Certificate of Commencement.

Importance of KYC:

KYC means “Know Your Customer”. KYC is become an important part in today’s critical structure. It become safeguards for bank collect client information and helps to formulate a customer acceptance on bank’s police(s). KYC provide a particular relevance to the safety and security of the financial institutions. A KYC transaction profile include:

- Occupation or nature of customer’s business.

- Net worth / sales turnover of the customer.

- Reasons for opening the account.

- Nature of transaction.

- Expected value of monthly transactions.

- Expected number of monthly transactions.

- Expected value of monthly cash transactions.

- Expected number of monthly cash transactions. 25

Customer Inquiries:

The respective officers of the Department are always ready to provide all kinds of information to their customers. Customers can make their quires easily about their desired information.

Account Transfer:

Some times customer change their place due to some unavoidable reason. At that situation customer had to transfer their account to their convenient place. All the process of account transfer is happen through the General Banking Division.

Account Close:

Very few times, customers are facing problem to not to continue their accounts. At that situation the Mercantile Bank Limited are complied to close their client’s account. Most of the time this is happen in the case of Masik Sanchaya Scheme (MSS). At the closing of MSS, clients are asking to bring all the deposit books along with an application. The procedures of closing are varies from account to account.

Cheque Book Issue:

In the accounts opening form, there is a page for chequebook requisition, which is signed by the accounts holder. The chequebook does not issue immediately after opening the account. When the authorized officer verifies the accounts holder demand for the chequebook, then his or her signature. And after the signature verification a chequebook is issue for the account holder. There are chequebooks for all types of accounts from 10 leaves to 50 leaves.

Issuing of:

Demand Draft (DD): Demand Draft is issue for the customer of the client who pay their payment to other bank, which are out of clearing house.

Pay Order (PO): Pay Order has been issued for the client for to make the client’s payment instead of cash. It has been issued to pay with the range of clearinghouse. To issue a Pay Order, bank charges commission and VAT from their client.

Security Deposit Receipt: It is the similar type of pay Order. But it issue when the amount of cash or cheque is more then Tk. 1,00,000.00. All the function of SDR is as like as Pay Order.

Pay Slip: Pay Slip, Pay Order, SDR, the function of these three instruments is all most same. The basic difference of Pay Slip with the other two instruments is, it is issue just for Bank’s own expenses. To issue a Pay Slip, bank does not charge any commission and VAT. 26

Clearing House:

Mercantile Bank Limited is a Scheduled Bank. According to the Article 37(2) of Bangladesh Bank Order, 1972, the banks, which are the member of the clearinghouse, are called as Scheduled Banks. The Scheduled banks clear the cheque with other banks through the clearinghouse. The clearing cheque means the client of the bank deposit the cheques of other bank to their account. When the bank receives such cheque then the bank put a seal “received for Collection” on the voucher and also put a seal on the cheque on the left corner is called Crossing. These cheques are placed in the clearing house for pass or return. This is an arrangement by the central bank where everyday the representative of the member banks gathers to clear the cheque. The place where the banks meet and settle their dues is called the Clearing-House. The Clearing-House sits for two times in a working day. The morning shift is called 1st House and evening shift is called 2nd House.

Cash Department:

One of the main parts of a bank is Cash Department. Customers and clients deposit and withdraw their money from cash counter. Receiving of cash and payment of cheque is the main task of the cash department.

Account holder has to write a deposit slip to deposit the money in the bank. He should write his bearing account number, name and the amount, he wants to deposit in the bank, carefully. After receiving the cash, the cash officer put his signature and marked “Cash Received” seal on the deposit slip. If the account holder makes any mistake to write his name or account number then the amount is deposited in a special account, which is called “Sundry” and had been informed immediately.

Account holder can place cheque to withdraw cash from his account. He should write the cheque first, which should not be overwrite and sign properly. After submitting the cheque his signature will be verified by an authorized officer and check his account whether the cheque amount is available or not. If the amount is available in the account then the officer cancel the cheque and the cash officer will make payment to the customer and marked “Cash Paid” seal on the cheque.

| 4.2. Credit Division/Advance: |

This is also one of the important divisions of a banking system. The major task of this department is to provide loan/advance facilities to the client. There are difference between loan and advance. Loan means when an advance is made in a lump sum repayable either in fixed monthly installment or in lump sum and no subsequent debit is ordinarily allowed except by way of interest, incidental charges etc. it is called loan. And when a lump sum amount is sanctioned to a customer for a specific period of time or for a long period is known as advance.

Mercantile Bank Limited makes loan & advance to reputed clients and encourages them in lending to socially desirable, national important and financially viable sector. Mercantile Bank extends its credit facilities to the area, which the branch is located and the ability of its stuff to supervise and monitor the same also considered. The Bank complies with all the laws and act of the country including central banks instruction relating to banks. The credit division tries to actively participate in the growth and expansion of our national economy by providing credit to viable borrowers.

Credit Approval Authority:

The Senior Management of Mercantile Bank Limited delegates authority to individual credit analyst and credit manager. Loan Administration Division also retains copies of all Delegation of Lending Authorities.

Approval Process:

Credit approval should be centralized within the credit function. Regional credit centers may be established, however, the Head of Credit Division, Head Office, Dhaka must approve all large loans. Any credit proposal that does not comply with Lending Guidelines, regardless of amount, should be referred to Head Office for approval.

Credit Administration:

After approval, Credit Team will send/forward application along with the security and other documents to the Credit Administration Division under Operation Unit for processing. The Credit Administration function is critical in ensuring that proper documentation and approvals are in place prior to the disbursement of loan facilities. Under Credit Administration there may be two-sub unit, Documentation & QC and Loan Administration department who will process the document and disburse the loan.

Credit Documentation:

Credit Documentation Department is responsible for:

- To ensure that all security documents complies with the terms of approval.

- To control loan disbursements only after all terms and condition are approval have been met and all security documents as per the checklist are in place.

- To maintain control over all security documentation.

- To monitor borrower’s compliance with agreed terms and conditions, and general monitoring of account conduct/performance.

Loan Disbursement:

Credit administration Department will disburse the loan amount under the loan facilities only when all security documents are in place. CIB (Credit Information Bauer) report is obtained, as appropriate and clean.

Custodial Duties:

Loan disbursement and the preparation and storage of security documents should be centralized in the regional credit center. Security documents is held under strict dual control, in locked fireproof storage.

Risk Management:

The credit division is full of risk. The Credit & Collection Unit (CCU) manages the risk. The following elements contribute to the management of credit risks:

Third Party Risk.

Fraud Risk.

Liquidity and Funding Risk.

Political and Economic Risk.

Operational Risk.

Maintenance of Documentations and Securities.

Internal Audit.

Collection & Remedial Management:

Collection of loans and advance are done through the following process:

Monitoring: A banks loan portfolio should be subject to a continuous process of monitoring. This will be achieved by generation of over limit and over due reports, showing where facilities are being exceeded and where payment of interest and payment of principle are late. There should be formal procedures and a system in place to identify potential credit losses and remedial action has to be taken to prevent the losses.

Recovery: The collection process for loans will start when the borrower has failed to meet one or more contractual payment (Installment). It therefore, becomes the duty of the Collection Department to minimize the outstanding delinquent receivable and credit losses.

Collection Objective: The collector’s responsibility will commence from the time an account becomes delinquent until it is regularized by means of payment or close with full payment amount collected.

Collection/Monitoring Steps: To identify and manage arrears, the following again classification is adopted:

Days Past Due (DPD)

| Collection Action |

| 1-14 |

Letter, Follow up & Persuasion over phone.

15-29

1st Reminder letter & Follow up & Persuasion over phone.

45-5932. 3rd Reminder letter.

Group visit by team member.

Follow up over phone.

Letter to Guarantor, Employer & Others.

Warning on legal action by next 15 days.60-89

- Call up Loan.

- Final Reminder & Serve legal notice.

- Legal proceedings begin.

- Repossession starts.

90 and above

- Telephone calls/Legal proceedings continue.

- Collection effort continuous by Officer and Agent.

- Letter to different Banks/Associations.

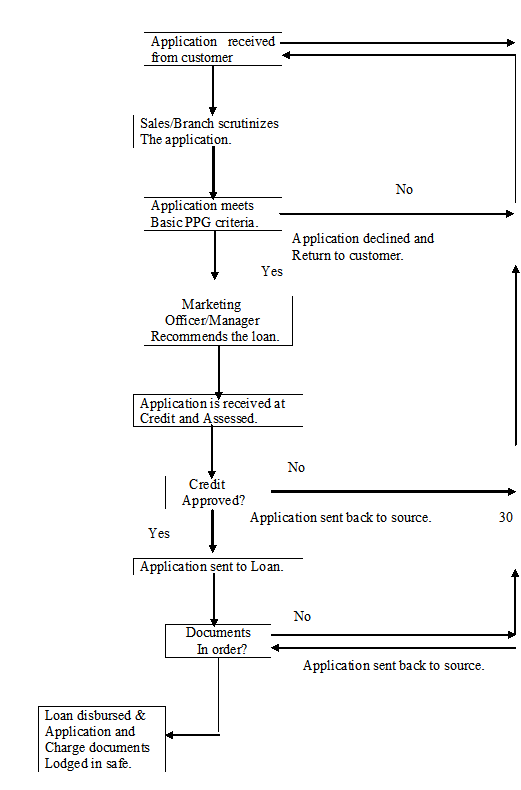

Process Flow Chart of Loan processing:

A Process Flow Chart of Loan and Advance are shown here:

4.2.10. Loans and Advances:

Mercantile Bank Limited, Credit Division provide the following loans and advance facilities to their clients:

- Secured Over Draft (SOD).

- Lease Finance.

- Payment Against Documents (PAD) Cash.

- Cash Credit (CC Hypo).

- Personal Loan.

- Loan Secured.

- Small Loan Scheme.

- Consumer Credit Scheme (CCS).

- Car Loan.

- House Building Loan.

- Loan Against Trust Receipt (LTR)

- Small & Medium Enterprise (SME) Loan.

To enjoy the above loans and advance facilities clients has to provide some documents to the bank according to their purpose. Cause different loans have different documents requirement charge documents. A list of charge documents of some popular loans and advances, provided by the bank, are given below:

Secured Over Draft (SOD):

- Demand Promissory Note.

- Letter of Arrangement.

- Letter of Authority.

- Letter of Undertaking.

- Letter of lien for Advance Against Fixed Deposit/Special Deposit Receipt.

- Memorandum of deposit of securities.

- Letter of Continuity.

- Letter of Authority for encashment of DBDS/ MBDS/ SSS/ MSS/ FDR.

- Balance Confirmation Slip. 31

Cash Credit (CC Hypo):

- Demand Promissory Note.

- Letter of Arrangement.

- Letter of Authority.

- Letter of Undertaking.

- Letter of Hypothecation.

- Supplementary Agreement for Letter of Hypothecation.

- Letter of Continuity.

- Letter of Revival.

- Letter of Guarantee.

- Balance Confirmation Slip.

Composite Credit Limited:

- Demand Promissory Note.

- Letter of Arrangement.

- Letter of Authority.

- Letter of Undertaking.

- Letter of Hypothecation.

- Supplementary Agreement for Letter of Hypothecation.

- Letter of Continuity.

- Letter of Revival.

- Letter of Guarantee.

- Letter of Trust Receipt.

- Letter of Indemnity.

Some other information:

Loans and advances of MBL for the year of 2006 & 2007

No. | Types of Loan | Amount in 31.12.2006 (Tk) | % of total loans & advances | Amount in 31.12.2007 (Tk) | % of total loans & advances |

1. | Unclassified | 131,65,24,777.00 | 99.95% | 131,69,03,517.00 | 99.95% |

2. | Classified: | ||||

a. | SMA | NIL | NIL | ||

b. | Substandard | 3,19,065.31 | 0.05% | 3,25,056.53 | 0.05% |

c. | Doubtful | NIL | NIL | ||

d. | Bad & Loss | NIL | NIL | ||

3. | Total Loans & Advances | 131,68,43,842.69 | 100% | 131,71,13,431.18 | 100% |

The condition of Loans and Advances of MBL in 2006 & 2007 are shown below:

Particulars | 2006 | 2007 |

| Total Amount Loans & Advances | 131,68,43,842.69 | 131,71,13,431.18 |

| % Of classified Loans & Advances | 0.05% | 0.05% |

| Credit Deposit Ratio (in %) | 66.46% | 66.45% |

| Amount of Classified Loans & Advances during the year | 3,19,065.31 | 3,11,745.23 |

Sanction of Loans & Advances (in %) are given below:

No. | Particulars | % Of total in 2006 | % Of total in 2007 |

1. | SOD Against Accept Bill | 5.39% | 5.39% |

2. | SOD Against FDR | 0.88% | 0.88% |

3. | SOD Against Special Scheme | 0.51% | 0.51% |

4. | SOD General | 6.43% | 6.43% |

5. | Lease Finance | 0.52% | 0.52% |

6. | Payment against Document (PAD) Cash | 1.91% | 1.91% |

7. | Cash Credit (CC Hypo) | 4.45% | 4.45% |

8. | Loan Secured | 8.54% | 8.54% |

9. | Personal Loan | 0.29% | 0.29% |

10. | Small Loan | 0.09% | 0.09% |

11. | Consumer Credit Scheme (CCS) | 0.21% | 0.21% |

12. | Loan Against Trust Receipt (LTR) | 70.22% | 70.22% |

13. | Car Loan | 0.17% | 0.17% |

14. | Doctors Credit Scheme | 0.02% | 0.02% |

15. | House Building Loan | 0.50% | 0.50% |

| Total | 100% | 100% |

| 4.3. Foreign Exchange: |

What is it?

Foreign Exchange means exchange of foreign currency between two countries. If we consider “Foreign Exchange” as a subject, then it means all kinds of transaction related to foreign currency. In other words, foreign exchange deals with foreign financial transaction. Thus foreign exchange means foreign currency and includes: all deposits, credits and balance payable in any foreign currency and any drafts, travelers cheques, letter of credit and bills of exchange expressed or drawn in local currency but payable in foreign currency and any instrument payable at the option of drawee or holder there of or any other party there to, either in local currency or in foreign currency or partly in one and partly in the other.

Fundamentals of foreign exchange:

There are three (3) fundamental aspect of the general mechanism of foreign exchange:

- Every country has its own currency-legal tender/distinctive unit of account.

- The conversion of one currency into another is effected by banks by book keeping entry carried out in the two centers concerned.

- These exchange is effected by means of credit instrument i.e. Draft, Mail Transfer, Tele Graphic Transfer etc.

Administration of Foreign Exchange in Bangladesh:

The statute for administration of foreign currency in Bangladesh is the Foreign Exchange Regulation Act 1947 as adopted in Bangladesh. Under the act, the Government with the Bangladesh Bank, Central Bank of the country vests the responsibility and authority of administration of foreign exchange. Any person who deals with foreign exchange has to abide the direction given by the Bangladesh Bank in that behalf.

In exercise of the powers conferred by the Foreign Exchange Regulation Act 1947 on certain schedule banks, who are authorized to deal in foreign exchange by Bangladesh Bank, the selected branches of the bank can transact such business. They are known as “Authorized Dealer”. Bangladesh Bank does not deal directly with the public; “Authorized Dealer” does the transaction in accordance with the guidelines given by the Bangladesh Bank.

Credit Instruments:

The foreign exchange operations of banks consist primarily purchase and sales of credit instruments. There are many types of credit instruments used in making foreign remittance. They differ chiefly in the speed with which the creditor at the other end can receive money after it has been paid in by the debitor at his end. The credit instruments are:

- Bills of Exchange.

- Letter of Credit.

- Banker’s Draft.

- Telegraphic Transfer.

- Mail Transfer.

- Stock Draft.

- Personal Cheque/ Dividend Warrant.

- Society for Worldwide Inter bank Financial Telecommunication (SWIFT).

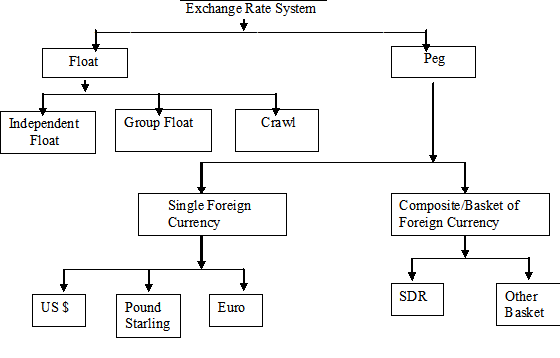

Exchange Rate System:

The rate at which the conversion of one currency into another is effected or the rate at which one currency is exchanged with another is known as Rate of Exchange (ROE). All the dealings of foreign exchange market are carried out at specified rate of exchange. The choice of exchange rate system is given in the following:

Letter of Credit (L/C):

The main and the most important task of the foreign exchange department are to deals with the letter of credit (L/C). L/C can be defined as a ‘Credit Contract’ whereby the buyer’s bank is committed (on behalf of the buyer) to place an agreed amount of money of seller’s disposal under some agreed conditions. Since the agreed conditions include, amongst other things, the presentation of some specified documents, this letter is called Documentary Letter of Credit. The Uniform Customs & Practice for Documentary Credit (UCPDC) published by the International Chamber of Commerce (1993) revision, Publication No 500 maintain the rules and regulation of Documentary Letter of Credit. Now UCPDC 600 has been published which will be affected from July 2007. There are different types of Letter of Credits. These are:

- Revocable Credit.

- Irrevocable Credit.

- Revolving Credit.

- Transferable Credit.

- Back-to-Back Credit.

A short description of these types are given below:

Revocable Credit:

This type of credit can be cancelled or amended at any time by the issuing bank without prior notice to the seller. In the present time, it is not in use. 35

Irrevocable Credit:

This type of credit can’t be cancelled or amended by the issuing bank without the arrangement of parties concerned thereto. The entire credit instruments issued in our country are of irrevocable nature.

Revolving Credit:

This provides for restoring the credit to the original amount after it has been utilized.

Transferable Credit:

If the word “transferable” incorporate in an L/C, then the L/C is transferable. The first beneficiary can transfer “Transferable L/C” to the second beneficiary. But second beneficiary cannot transfer it further to another beneficiary.

Back-to-Back Credit:

The Back-to-Back is a new credit opened on the base of an original credit in favor of other beneficiary, under this concept the first credit offers it as security to the advising bank for the assurance of second credit. The beneficiary of the Back-to-Back credit may be located inside or outside the original beneficiary’s country.

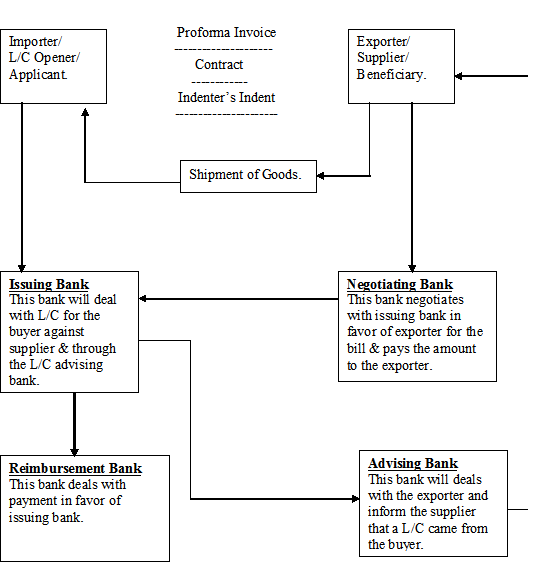

Parties related to L/C:

The following parties are related with a Documentary Letter of Credit:

Importer/Buyer.

Opening/Issuing Bank.

Exporter/Seller Beneficiary.

Advising/Notifying Bank.

Confirming Bank.

Negotiating Bank.

Paying/Reimbursing Bank.

Documents needed to open a L/C:

To open a L/C, an Importer must have an account in the respective bank. Then he needs the following documents. These are:

- Import Registration Certificate (IRC).

- Membership Certificate.

- Insurance Cover Note and Receipt of Premium Payment.

- TIN Certificate.

- Trade License.

- VAT Certificate.

Accept these, Importer has to full fill some papers provided by the bank. These are:

- L/C form

- LCA form means Letter of Authorization Application form.

- Import Permission. 36

- Deed.

- Charge Documents.

- Guaranty form.

Some financial information:

(Amount in Million)

Particulars | July-November 2006 | % During the year | July-November 2007 | % During the year |

Board Money | Tk. 1,17,795.00 | 6.50% | Tk. 1,45,529.00 | 7.27% |

Domestic Credit | Tk. 1,25,997.00 | 7.09% | Tk. 1,32,155.00 | 8.25% |

Import Payment | $ 6,818.30 | 20.71% | $ 7,514.20 | 22.11% |

Export Exhibit | $ 5,045.72 | 25.81% | $ 6,019.28 | 26.14% |

Foreign Remittance | $ 2,178.87 | 31.38% | $ 2,297.57 | 32.31% |

In the backdrop of changing national and global economics, the bank did well in 2007. In the period review a substantial growth has been achieved in the areas of business and revenues. Gross revenues grew by 33.37% to reach at BDT 4631.41 million in 2007. Interest income increased by 28.61% to reach at BDT 3498.67 million during the period under review. Interest expenses grew by 33.99% to reach at BDT 2662.58 million in the year. As a result net interest income stood at BDT 836.09 million in 2007, registering a growth of 14.03% over the previous year. Fee income grew by 50.60% in 2007 over the previous year resulting a net addition of BDT 342.67 million in 2007 in the operating revenue of the bank. Due to excellent growth in net interest income and fee income, the bank posted operating revenue of BDT 1178.76 million in 2007 registering a growth of 21.87% over the previous year.

Comparative Analysis of Export Import Business of Mercantile Bank Limited, Khatungonj Branch:

IMPORT

(BDT in Crore)

No. | Name of L/C | 2007 | 2006 | 2005 |

No. Amount Of L/C | No. Amount Of L/C | No. Amount Of L/C | ||

1. | Cash (Foreign) | 245 124.08 | 174 109.48 | 114 95.13 |

2. | Back-To-Back (Foreign) | 6 0.52 | NIL NIL | 4 0.30 |

3. | Back-To-Back (Local) | 27 1.29 | NIL NIL | 20 1.13 |

Total | 278 125.89 | 174 109.48 | 138 96.56 |

EXPORT

(BDT in Crore)

2007 | 2006 | 2005 |

No. of L/C Amount | No. of L/C Amount | No. of L/C. Amount |

259 3.81 | 25 3.00 | 23 3.91 |

FOREIGN REMITTANCE

(BDT in Crore)

| 2006 | 2005 | 2004 |

| Inward Outward | Inward Outward | Inward Outward |

| 0.05 NIL | 0.04 NIL | 0.01 0.01 |

Operational Procedure of L/C in Export & Import Business:

Product Management of Mercantile Bank Limited, Khatungonj Branch.

What is it?

‘A product is anything that is potentially valued by a target market for the benefits or satisfactions it provides, including objects, service, organizations, places, people and ideas’ (Cravens, 1987). As the above definition clearly mentioned that services are the products, we consider all banking services of “Mercantile Bank Limited” as the products. Cravens (2000) identified that product management includes three major activities, which are: market orientation, customer value & satisfaction and continuous learning about market.

In our study, first attempt has been taken to know whether there is any product management system at branch level. In the primary discussion with branch management it is found that some of the product management activities have been done at branch level and some others have been performed at corporate level. In absence of any precise product management system at branch level, data have been collected to know the present conditions of product management activities in “Mercantile Bank Limited” at branch level. In this regard, a questionnaire has been developed to collect market related information. Internal management information has been collected through face-to-face interview and personal observation.

Base of Analysis:

The following variables are considered in analyzing the product management of “Mercantile Bank Limited”:

Market Related Factors | Organizational Factors |

| 1. Market Orientation a. Product acceptability b. Competitor analysis

| 1. Team approach |

| 2. Customer Value and Satisfaction a. Waiting time for service b. Response to specialized service c. Perceived ranking of bank by customers

| 2. Relationship strategies |

| 3. Continuous learning about market |

a. Customers expected product

b. Reasons of choosing the bank

Inter-organizational relationship:

Based on the above model of product the study on product management has been conducted in “Mercantile Bank Limited” and the findings are summarized in the following under the three areas of product management.

Market Orientation:

In today’s competitive financial market setting a company cannot survive without proper market orientation. Appropriate market orientation will help the company to target the suitable segment. Market orientation is essential for proper marketing mix strategy for positioning the company’s product in the target market. In the study it is found that more than thirty eight percent of the customers are taking the benefits of more than five products. Around the seventeen percent of the customers are using two or four products while the rest of the customers are taking the benefits of one, three or five products.

No. Of Account | Percentage of Customers holding the accounts |

1 | 5.56% |

2 | 16.67% |

3 | 11.11% |

4 | 16.67% |

5 | 11.11% |

5+ | 38.89% |

Loyalty of the Customers:

The success of a bank in today’s business world depends on to provide the total solution of financial problems. But the study shows that only eleven percent customers are loyal to the company, which reveals that about ninety percent customers are not getting their entire necessary product needs from the bank. That is why; they are choosing some other banks. The following table shows the Customers Loyalty to Mercantile Bank Limited:

Loyal to Mercantile Bank Limited | Percentage of Respondent |

Not Loyal | 88.89% |

Loyal | 11.11% |

Key Competitors:

In the study it is found that the major competitors of Bank are Standard Chartered Bank & Sonali Bank. The study discloses that among the following competitors two banks become close competitors to the bank. The following table presents the Customers of Mercantile Bank Limited using the products of their Competitors:

Competitors Bank | % of existing customers using competitors bank |

Standard Chartered Bank | 31.25% |

Sonali Bank Limited | 31.25% |

Janata Bank Limited | 12.50% |

Prime Bank Limited | 6.25% |

Standard Bank Limited | 12.50% |

EXIM Bank Limited | 6.25% |

List of the Products:

Application Type | Particulars | No. of Accounts |

| Current Account (Customer) | 355 |

Savings Account (Customer) | 780 | |

Savings Account (Stuff) | 41 | |

Demand Deposit | Short Term Deposit (Customer) | 52 |

FCAD (Exp) | 1 | |

FC Held Against B/B LC-$ | 3 | |

Sub Total | 1,232 | |

| Fixed Deposit 01 Month – Customer | 24 |

Fixed Deposit 03 Month – Customer | 36 | |

Fixed Deposit 06 Month – Customer | 25 | |

Time Deposit | Fixed Deposit 12 Month – Customer | 486 |

Fixed Deposit 24 Month – Customer | 5 | |

Fixed Deposit 36 Month – Customer | 8 | |

Sub Total | 584 | |

| Monthly Savings Scheme (MSS) – 05 Yrs | 1,351 |

Monthly Savings Scheme (MSS) – 08 Yrs | 249 | |

Monthly Savings Scheme (MSS) – 10 Yrs | 5,213 | |

Double Benefit Deposit Scheme – 06 Yrs | 672 | |

Double Benefit Deposit Scheme – 07 Yrs | 212 | |

Double Benefit Deposit Scheme – 08 Yrs | 14 | |

Double Benefit Deposit Scheme – 09 Yrs | 3 | |

Double Benefit Deposit Scheme – 10 Yrs | 10 | |

Schemes Deposit | Special Savings Scheme – 10 Yrs | 45 |

Special Savings Scheme – 11 Yrs | 10 | |

Special Savings Scheme – 12 Yrs | 3 | |

Family Maintain D @ 50 Thu | 194 | |

Family Maintain D @ 57 Thu | 21 | |

Family Maintain D @ 75 Thu | 7 | |

Family Maintain D @ 425 Thu | 6 | |

Pension & Family SD | 24 | |

Sub Total | 8,034 | |

| Secured Over Draft (SOD) – General | 8 |

SOD Against Accept Bill | 122 | |

SOD Against FDR | 48 | |

SOD Against Special Scheme | 97 | |

Lease Finance | 8 | |

Loans & Advance | CC Hypothecation | 23 |

Loan Secured | 3 | |

Small Loan | 9 | |

Personal Loan | 49 | |

Small & Medium Enterprise (SME) Loan | 3 | |

LTR | 84 | |

Others | 47 | |

Sub Total | 501 | |

Total No. Of Accounts | 10,351 | |

From the above table it is found that scheme products of Mercantile Bank Limited are popular. The company has four product lines and about 40 brands. Among them, DPS are the most popular account of the Bank. Also Current A/C, Savings A/C, Fixed Deposits are very popular.

Customer Value and Satisfaction:

Successful product management requires to provide the expected benefits and to satisfy the customers. There are three kind of companies based on customer satisfaction. These are:

1) Companies those who are trying to satisfy customers by providing necessary values and ensure customers satisfaction.

2) Companies those who are trying to provide all expected desire, so that customers feel fulfillment.

3) And companies those who provides values that the customers have yet thought, which make customers fulfilled.

In our study it is found that Mercantile Bank Limited still trying to satisfy customers as a number one type of companies. The table stated below shows the Mean Customers Satisfactions of the Bank:

| Factors Evaluated | Customers Responses |

| Waiting time for service | 4.92 |

| Response to specialized services | 5.28 |

| Perceived ranking of Bank by customers | 4.65 |

| Service charge | 4.13 |

| Bank statements | 3.75 |

| Mean Score | 4.55 |

The study identify that the mean customer satisfaction score is 4.55 which indicates that customers are merely satisfied where the score 5.00 is identical to customer satisfaction in a five point scale. Among the five evaluated factors for Customer satisfaction, customers have shown their dissatisfaction on specialized services of banks and waiting time for service, whereas customers have shown satisfaction for regularly receiving of bank statements, for perceived ranking of bank and service charge. The study also identified the reasons of customer dissatisfactions. The next paragraph deals with identifications of customer dissatisfaction.

Causes of Customer Dissatisfaction at Mercantile Bank Limited:

There are different kinds of problems identified by the customers that caused their dissatisfactions. These are procedural problem, timing problem and space problems etc. The following table shows the problems that causes dissatisfaction:

| Problem mention by the respondents | Percent of respondents identified the problem |

Facing procedural problem11.11%

Facing time problem

22.22%Space problem

16.67%No problem at all

66.67%

In the study it is found that the most sever problem that causes the majority of the dissatisfaction is time problem. Almost twenty two percent of the customers identified that they are facing time problem in banking operation. The second severe problem is space problem while dealings with the banker’s and around eleven percent customers identified that they are unhappy with procedural problems to receive the services. On the other hand, a significant rate of customers is happy with the bank’s product management. More than sixty six percent of the customers are found happy with the present product management in Mercantile Bank Limited.

Continuous Learning about the Market:

A continuous flow of information helps companies to learn about market. It is an essential part of product management. In the survey it is found that customer of Khatungonj Branch of Mercantile Bank Limited is highly intended to get the proper on-line facilities, though the company has already introduced it to their customer but the bank charge fees to their customer to transfer amount out of the city. This finding proves that the bank has understanding about the market expectation. In the study, it is found that some people want the bank should increase the rate of FDR and should introduced new schemes.

Unlike physical product, majority of the people are using the products of the bank because of the better service of the bank, not only the likeness to the products. About twenty two percent of customers are using the bank for the nearness of their business or service. And the rest of the customers are using the bank for better understanding, local banker’s or other reasons. The table stated below present the reasons for choosing the Bank:

Selection mention by the responder | Percent respond to the reason |

Nearness to business/service | 22.22% |

Better service for bank | 44.44% |

Reason to local bankers | 11.11% |

Better understanding with Mercantile Bank Limited | 11.11% |

Others | 11.11% |

The above findings indicate that the bank should give more effort to learn the market so that it can meet customer’s needs and demand. A regular and cognitive based information system can help the company to develop its system in the organization.

Concluding Part. 46

Concluding Part

Recommendation:

Mercantile Bank Limited is one of the prominent banks in the country. But the system followed by the bank for marketing their product is not moderate. Their marketing activities are also not satisfactory. Form the study; I tried to recommend some probable solution to the bank.

- The Bank has to go through the proper online banking for better service to the customer.

- The Bank should try to follow modern marketing system.

- The Bank should promote their product by advertisement.

- The Bank should introduce new and attractive product to their customer.

- The Bank should emphasize on training its employee on a frequent basis.

Conclusion:

Mercantile Bank Limited is one of the most renowned private banks in the country. Within this short Internship Period, it was not possible for me to learn every thing of a banking system. But I tried my level best to learn some thing within this short period. In spite of shortcomings, I tried to find out problems, give possible solution, which is not up to the expectation of the authority. I apologize for making errors in the report.