Literature review

Morris (1986) reported that :

Management Strategy and Employee relations

The research is focused on the response of the Bank to changes in the financial sector which has been experiencing deregulation, increasing competition, technological innovation and an increasingly discriminating public. It examines both changing business and employee relations strategies and the links between the two. As greater diversity begins to exist amongst the retail banks the study explores the Banks attempt to find itself a niche or adopt a focus strategy. This paper is primarily concerned with Human Resource issues. Changes in the nature of banking clearly have a knock-on effect on employee relations as banks move towards being more market driven organizations with a culture consistent with that, and with staff being regarded more as a resource than a cost

Historically, it has been the case that employee relations have been regarded as a “second order” strategy, purely facilitative and not fully integrated into overall business strategy. Hence, there was little consideration of unrest was such that labor was seen as a problem, as for instance in the car industry. Although there has been a gradual rise in the number of personnel professionals at Board level, these are still a minority. Lack of serious consideration of employee relations has also been said to owe something to the dominance of financial control at this level and the lack of union influence. Certainly many would argue that while senior, management do think about human resource issues, the degree of unpredictability in this area pushes it fairly well downstream in corporate planning. However, there are dangers of looking at HR issues in this way. The importance of ensuring the active co-operations of employees in industry has been emphasized control to one of commitment and this can be even more significant for the service sector. Thus in retail banking, the banks do not yet provide significantly different products and hence consumer choice is heavily influenced by convenience and image, the latter partly created by contract with quality of service and staff quality. Yet, in banking traditionally staff have not been recruited or developed for customer contract skills but for technical and administrative ability.

Torrington (1994) says that:

The recent emphasis on the human resource management, Torrington suggests that not only is the management of labor being given more attention, but that the issues discussed are broader and more strategic as well as tactical define strategic human resource management as “those decisions and actions which concern the management of employees at all level in the business and which are related to the implementation of strategies directed towards creating and sustaining competitive advantage. Thus, unlike the traditional peripheral function of many personnel managers, the newer style of human resource managers attempts to:

“Relate personnel practices to beliefs, to link each and every process of the recruitment, induction, training, appraisal rewarding of individuals to an overall set of articulated beliefs of organization”

Human resource management is seen as part of the movement away from concentration on unions and collective bargaining, to an emphasis on staff as individuals. Behind all is a belief that it will release greater commitment from employees although one has to be careful to examine the extent tonew equal partnership between employers and employed, or are then really offering a convert from of employee manipulation dressed up as mutuality.

One must be wary of evaluating HRM simply by the range of activity being undertaken. HRM is about both new processes new outcomes. The existence of the former does not guarantee the latter. Many initiatives may be no more than ‘flavor of the month’ changes; other may be opportunistic rather than strategic, taking advantage of slack labor markets; in many uses the gap between the rhetoric and the reality may be wide.

Batstone (1984) reported that:

The banking sector has been characterized by apparently harmonious industrial relations and has not suffered from the “British diseases” of industrial action and demarcation issues associated with parts of manufacturing industry. Banks have promoted unitary encouraging an ethos of teamwork, shared interest and loyalty, wanting commitment beyond

the cash nexus. While banks are generally seen as having a passive approach

to employee relations, paternalism did underpin the system and particularly important was the system of internal promotion supported by an unwritten.

agreement between the major UK banks on no poaching. The internal labor market created two categories of employees; career and non-career which equated to a male/female divide.

Retail banking is a highly labour intensive retail banking is a highly industry labour costs forming 70% of total operting expenditure and “involment in funds transmission meant that majority of clerical staff have not been used as a means of marketing the banks’ products nor directly for increasing business but to process existing accounts. They have accordingly been regarded as an overhead rather than a resource”(Morris,1986,p.22). until the 1980s competition between banks has been limited,banks operating as an oligopoly and government’s concern with maintaining economic stability with limits to lending, to the management of staff as national wage bargaining minimized competition for labour. However ,deregulation led to the collapse of the national system and a questioning of old employment practices.

Background:

The co-operative Bank is a wholly owned subsidiary of the co-operative Whole sale Society (CWS).the bank has a network of 90 branches and some 4,000 in-store banking points in co-operative stores. it has seen itself as an alternative force in uk banking and has a reputation for innovation. In banking products. While the history of the bank shows development away from the CWS(25years ago 90%of deposit came from movement and 10 % from other sources: the reverse is now the case) it remains the banker to the co-operative movement and as it’s chief Executive stated in the 1986 Annual Report,” our co-operative philosophy dictates that we approach the bank market in a fundamentally different way”.(see Wilkinson,1991).

The development of the bank’s policy on the management of people illustrates the move from the narrower re.

structure of the study:

The research divided in chapter as follow:

1st chapter includes:

Introduction

Objective of the study

Significant of the study

Methodology of the study

Literature review

Structure of the study

2nd chapter includes:

Conceptual frame work

Introduction

Human Resources management

3rd chapter includes

An overview of Pubali bank

4th chapter includes

Findings & Analysis

5th chapter includes

Recommendation and conclusion

6th chapter includes

References

7th chapter includes

Appendix

Chapter 2

Conceptual frame work

Introduction:

In formulating the Human resource management, HR managers must address three basic challenges; the need support corporate productivity and performance improvement efforts; the fact that employees play an expanded role in the employer’s performance improvement efforts; and the fact that HR must be more involved in designing not just executing the company’s strategic plan.

There are six basic steps in the strategic management process ; Define the business and its mission perform an external and internal audits translate the mission into strategic goals; formulate a strategy to achieve the strategic goals; implement the strategy and evaluate the performance.

A strategy is a course of action. It shows how the enterprise will move from the business it is in now to the business it wants to be in, given its opportunities and threats and its internal strengths and weaknesses.

Strategic human resources management means formulating and executing HR systems that produce the employees competencies and behaviors the company requires to achieve its strategic aims

The high performance work system is designed to maximize the overall quality of human capital throughout the organization, and provides a set of benchmarks against which today’s HR manager can compare the structure, content, and efficiency and effectiveness of his or her HR system.

Human Resources Management:

Human Resources (HR):

Human resources (HR) are the people who are ready, willing, and able to contribute to an organizations success.

Human resources (HR): Hiring activities, including recruitment, interviewing, training, layoff planning, including out placement, and counseling.

Human resources (HR) segment contains the full set of capabilities needed to manager, schedule. Pay, and hire the people who make a company run. It includes payroll, benefits and administration, applicant data administration, personal development planning, workforce planning, schedule and shift planning, time management, and travel expense accounting.

Human Resources Management:

Human resources management is concerned with the people dimension in management. Every organization is made up of people acquiring their services developing their skills motivating them to high levels of performance and ensuring right people right time and right place.

Definition of Human Resource management:

(Randall s. schuter):

Different terms are used to describe the people who work in an organization employees, associates (Wal-Mart, for instance), personnel, human resources (HR).The term HR has gained widespread acceptance over the last decade because it expresses the belief that workers are a valuable and irreplaceable resources/asset

In simple term, Human Resource Management is about managing people in organizations.

Wright and McMahan says (1999)

“The pattern of planned human resource activities intended to enable an organization to achieve its goals”

Again, Miles and Snow says (1984)

“A human resource system that is tailored to the demands of the business strategy”

.So, Human resource management is the process of acquiring, training, appraising, and compensating employees, and attending to their labor relations, health and safety, and fairness concerns.

A set of activities directed at an organization’s resources with the aim of achieving organizational goals in efficient and effective manner.

Functions of Human resource:

Human Resource Management is a process consisting of four functions, these are Staffing, Training & Development, Motivation, Maintenance .For a HR manager for maintaining an effective workforce it is necessary to know these functions.

Staffing: concerned with sourcing & hiring qualified employees.

The key areas of staffing are:

- Strategic Human Resource Planning: HRP help the organization to achieve the corporate goals by adopting and adjusting with changing situations for example rapid technological change

- Recruiting: The process of discovering potential job candidates by external & internal sources.

- Selection: Choosing the best incumbent for the organization.

Training & Development: concerned with assisting employees to develop up-to- date skills, knowledge & ability.

The major area of Training & Development is:

- Orientation: The activities involved in introducing new employees to the organization & their work units.

- Effective Training

- Employee Development: Future oriented training focusing on the personal growth of the employees.

- Carrier Development: The sequence of positions that a person has held over his/her life.

Motivation: Helping employees exert high energy level.

Some important factors of Motivation are:

- Motivational Theory & job Design.

- Performance Appraisal

- Rewards & Compensation

- Employee Benefits

- Discipline

Maintenance: maintaining employee’s commitment & loyalty to the organization.

Maintenance consist of

- Safety & Health

- Employee/Labor Relations

- Communication

Feature of the HRM:

The activities that a company dopes to manage their human resources include—

Understanding the Environment internal environment; structure, size, business, strategy, technologies etc.

The Environment: External, Specific and General Environment

External environment-Outside institutions or forces that potentially affect an organization performance. It has two components- Specific and general

Enduring advantage will come from making better used people.

Specific environment- includes those external forces that have a direct and immediate impact on manager decisions and actions and directly relevant to the achievement of organizational goals. The main ones are customers, suppliers, competitors and pressure groups (like environmentalists, green parties, students unions etc.)

Managing Organizational and Human Resource changes: Such changes may include bending the culture of two newly merged companies, or successfully managing downsizing efforts

Staffing the organization: Staffing activities may include- analyzing the job, recruiting job candidates, selecting, selecting the most appropriate one.

Workforce Diversity: (varied backgrounds of employees) : managing people was considerably simpler fifty-years before because workforce was more or less homogenous (within as well as outside the national boundary). After 1960s minority and female workers started to rise in USA and accommodating their demands and needs have become vital responsibilities for managers. Until very recently, organizations took a melting-pot approach to differences in organizations. It was assumed that people who were different would somehow automatically want to assimilate. But today’s manager have found that employees do not set aside their cultural values and lifestyle preferences when they come to work. The challenge for the managers therefore, is to make concerted efforts to attract and maintain a diversified workforce, not only in USA but all over the world.

Evidence involves four factors:

- The person belong to a protected class

- The person applied for, and was qualified for, a job the employer was trying to fill

- The person was rejected despite being qualified

- The position remained open and the employer continued to seek applicants as qualified as the person rejected

More clearly, disparate impact occurs when the standard is applied to all applicants or employees, but that standard affects a protected class more negatively.

CHAPTER 3

An overview of Pubali bank

Bank Profile:

History of Pubali Bank Limited:

After liberation the Eastern mercantile bank was converted into Pubali Bank and was taken under the government management because the government policy was nationalized of all financial institutions. The objective was strengthening the rural economy. The result of the policy was a mixed one. In late 70s when the government wanted to establish a market oriented economy with less public sector role. As pert of the privatization and liberalization process this bank was denationalized in the year 1983. it started function as a public limited company Limited and registered as Pubali Bank Limited. All liabilities and asset of the bank is transferred to the limited company.

The bank was incorporated under the Companies Act (Act VII) of 1913 as a limited company having its Head Office in Dhaka. The Bank started functioning with the approval of Bangladesh Bank under the guidelines, rules and regulations given for scheduled commercial banks in Bangladesh.

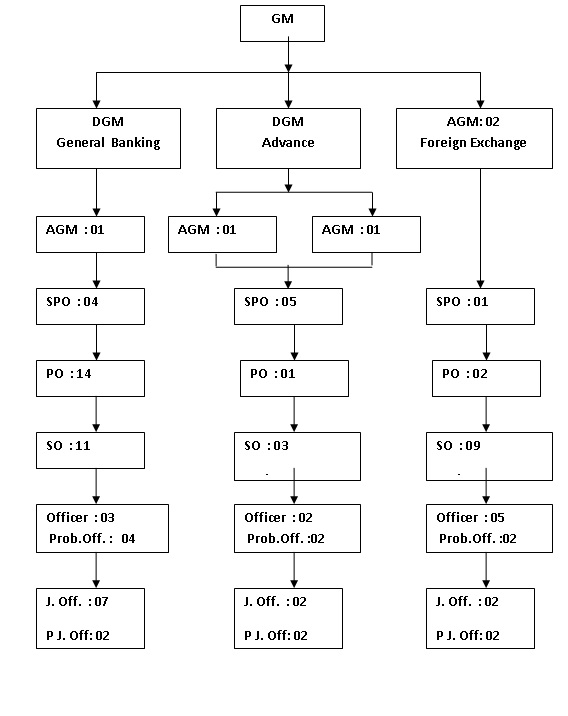

Organization Structure of PBL:

Pubali Bank Ltd expanded as a largest commercial bank in the country. Its operational networks cover almost every part of the country including the major cities, rural townships, which are prospective business centers in Bangladesh.

The bank was established primarily as private bank. After liberation it was nationalized and it remained so for quite a long period. Though it has been denationalized again and has gone back to its private norm it could not get rid of all the rules and norms of nationalized bank. The bank is run by an excellent management team under the direct supervision of a competent board of directors. The board of directors comprises total fourteen members headed by the chairman. Mr.E.A.Chaudhury is the present chairman of the board. The Managing Director (MD) heads management team. Under him a General Manager (GM) heads each department of the bank. Mr. Khondkar Ibrahim Khaled is the present MD of PBL. There are total twelve divisions in the Head Office of PBL. List of various divisions of PBL is given below:

Boards of Directors:

Mr. E. A. Chaudhury

Mr. Moniruddin Ahmed

Mr. Sk. Wahidur Rahman

Mr. Monzurur Rahman

Mr. Giashuddin Ahamed

Mr. M. A. Raquib

Mr. Syed Moazzem Hussain

Mr. Ahmed Shafi Chowdhury

Mr. Fahim Ahmed Faruk Chowdhury

Mr. Habibur Rahman

Mr. Manir Ahmed

Mr. Mohammed Yaqub

Mr. Muhammad Faizur Rahman

Divisions of Head Office:

| Sl# | Division | Functions |

| 1. | Board & MD’s Secretariat Division | Deals with Shares |

| 2. | Human Resource Division | Recruitment, promotion, training, Disciplinary action, dismiss, discharge, retirement, pay and allowances, career plan, trade union etc. |

| 3. | Establishment division | Engineering, transport, telephone, telex, fax, security system, real estate etc. |

| 4. | Credit Division | All sorts of credit, its allocation, estimation, sanction, etc. |

| 5. | Credit Monitor and recovery Division | Monitoring of credit, classification, evaluation and recovery of credit etc. |

| 6. | International Division | All types of works with foreign banks or organizations. |

| 7. | Central Accounts Division | Correct accounts, financial evaluation and forecast of future financial events of the bank. |

| 8. | Branch Operation Division | Management of branches, control, monitoring and evaluation of performance of branches of the bank. |

| 9. | General Services & Develop Division | Looks for improvement services, sets strategy for business promotion and development of the bank. |

| 10. | Audit Division | Conduct internal audits of the branches. |

| 11. | Information Technology Division | Mainly looks after the computer system, provides necessary support to the branches in regards to computer and electronic equipments. |

| 12. | Lease Financing & Law Division | Deal with the lease financing and help the bank to move with its legal aspects. |

Registered Head Office:

Pubali Bank Bhaban

26, Dilkusha Commercial Area

Dhaka – 1000, Bangladesh

Post Box No. 853

Cable: pubalipeak, Dhaka.

Telex: 675844 Pub BJ/632240 UCBL- H- O- BJ

Fax: 880-2-9564009

PABX: 9551614

Email: pubali@bdmail.net

Website: www.pubalibangla.com

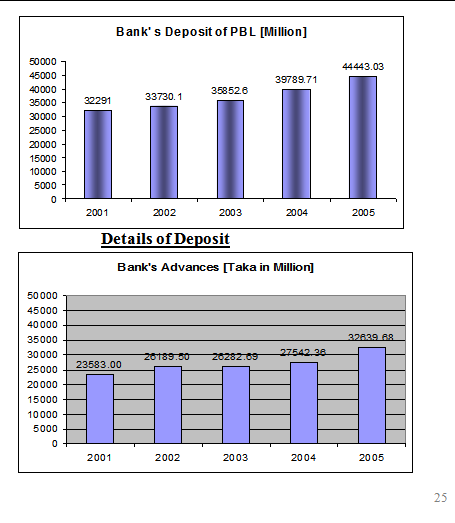

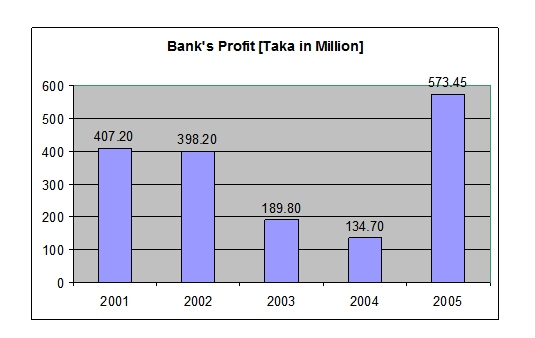

Financial Analysis of Information:

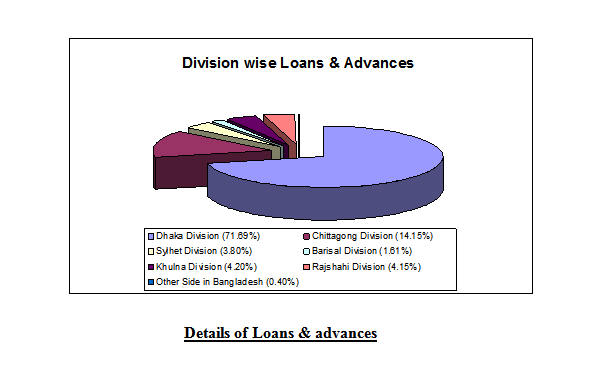

Details of advance:

Details of HR:

Branch Profile:

Location of Principal Branch :

Principal Branch of Pubali Bank is situated in the ground floor of Pubali Bank Bhaban, 26 , Dilkusha C/A , Dhaka-1000, Bangladesh.. The office is highly decorated and it is the most important and busy branch maintaining all types of banking transactions. There 96 employees are working in this branch.

Distribution of Employees:

| DESIGNATION | NO |

| General Manager | 01 |

| Deputy General Manager (DGM) | 02 |

| Assistant General Manger (AGM) | 05 |

| Senior Principal Officer (SPO) | 10 |

| Principal Officer (PO) | 17 |

| Senior Officer (SO) | 23 |

| Officer | 10 |

| Junior Officer | 11 |

| Prob. Senior Officer | 04 |

| Prob. Officer | 08 |

| Prob. Junior Officer | 06 |

Organ pgram of the Employees in PBL:

Branch Financial Position as on Date 27th October, 2008:

PARTICULARS | AMOUNT IN TK. |

| Cash & Bank Balance | 337,30,85,825.99 |

| Loans and Advances | 850,51,24,720.18 |

| Deposit | 254,59,07,560.17 |

| Bills Payable | 4,59,40,870.48 |

| Bills Discounted & Purchase | 5,78,44,600.50 |

| Fixed Asset | 2,19,30,264.90 |

| Other Asset | 14,12,02,956.30 |

| Income | 82,89,01,879.59 |

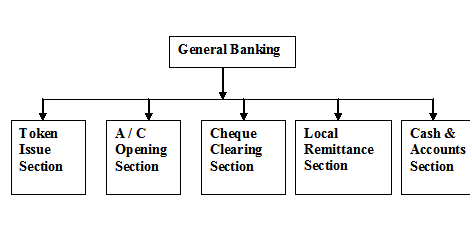

General Banking of PBL:

Introduction:

General banking is the starting point of all the banking operations. It is the department, which provides day-to-day services to the customers. Everyday it receives deposits from the customers and meets their demand for cash by honoring cheques. It opens new accounts, remit funds, issues bank drafts and pay orders etc. Since bank is confined to provide the services everyday, general banking is also known as ‘retail banking’.

According to World Bank, the general people understand the depositing and withdrawal of money and credit financing. But Bank performs numerous types of services. To deal these services bank has to maintain many register/ ledger and documents. Some different jobs that waive the General banking has shown in the following diagram

Token Issue:

The token issue department uses a register book and different types of tokens decorated with different letters for different types of accounts. There are two types of tokens. One is for savings A/C and another is current / other accounts.

Procedure:

The client will encash money from his account will show his cheque to the respective officer of the desk. The officer will give him a token with particular number after being sure of his two signatures on the back of the cheque. The officer will give him a token with a particular number on the back of the cheque. The client will then proceed on for encashment. The officer then gives an entry about the token number, account name and the amount in the column of the register book.

The token will be checked by the responsible officer for maintaining at the end of each business day. Tokens are then handed over to the supervising official concern to keep them in a locked box. Tokens are checked once a month by the supervising officer in charge wheather tokens is ok or not. When a token is lost it is informed to the head office for a matter of precaution.

Maintenance of the subsidiary register for receipt of cheques, drafts :

At the counter every cheque, demand draft and other credit instrument tender for the credit of the customers account will be delivered. Deposits received by post will sent by the receiving officer to the bills department against acknowledgment of the dealing officer. The dealing officer is concerned here about four types entries. They are

- Local Clearing

- IBC (Inter Branch Collection )

- SC (Short Collection )

- BT (Bank Transfer)

In case of local clearing one bank sends money by cheque or DD which will be collected in the name of the account holder of this branch. This cheque or DD will be taken to the clearing house where agents of all banks exchange these instruments. Important thing is that the paying Bank must be in the local area (Dhaka). In case of IBC the branches must be of the same banks for short collection, the paying banker is in the area other than Dhaka whereas bank transfer will be between two accounts of the same branch.

The dealing officer of this desk should be aware of the following things about instruments:

© Name of the account is very clearly written on the deposit slip.

© Full particulars of the deposit instruments such as cheque numbers, name of bank, etc are properly recorded on the paying slip as required.

© The pay in slip has been signed by the depositor.

© Full particulars of the railway receipts and instruments of title goods, bills of exchange, invoice etc. associated with an inland documentary bill received from the depositors direct at the counter or by post from other branches/ banks endorsement thereon.

© All cheques, bills and other instruments are crossed with crossing seal .

After categorizing all the instruments and checked out the preliminary mandatory things, the dealing officer gives entries in the appropriate column of subsidiary ledger for crediting the accounts.

Account Opening Section:

When a customer want to open a deposit account in bank, he/she will have to go the A/C opening section to know the rules and regulations for opening account and to have the set of documents required. Since PBL is an authorized dealer it can open deposit A/Cs denominated both in Taka and approved foreign currencies.

Deposits are like raw materials out of which credits are created. Deposit accounts are one of the important sources of funds. In order to attract customers the banks offer different facilities to various types of account holders. Competition in accepting deposits takes two forms:

(a) Improvement in customer service

(b) Offer a higher rate of interest.

In our country PCBs and foreign banks are appreciated to attract deposit because of their superior customer services. PBL principal office branch with its traditions customer service approaches faces difficulties to draw attention of new customers.

Main functions of account opening are given below:

- To give answers to the queries regarding account opening

- To supply the appropriate type of account opening form

- To put a/c number from a computerized sheet on advice of new account

- To input date into computer from a/c opening form.

- To maintain and update the a/c opening file for different types of accounts.

- To maintain a register for cash type of recording details of a/c opening

- To supply deposit slip books and cheque book on requisition

- To act on request for closing and transferring of deposit a/c

- To act on request for closing and transferring of deposit a/c

Classification of Customer:

a) Individual (personal)

b) Proprietorship (Sole traders)

c) Partnership firms (Register or Unregistered)

d) Joint Stock Companies ( Private Limited and Public Limited )

e) Municipalities/Municipal Corporations/Local Bodies etc.

f) Clubs / Societies / Associations /School / Colleges / Universities etc.

g) Executors /Administrators

h) Trustees

i) Illiterate persons

j) Constituted Attorney

k) Wage Earners

Different types of A/C of PBL Principal Office:

- Current A/C : Interest free and generously withdraw able.

- Saving Bank A/C: Interest bearing and checkable with some restriction

- Short Term deposit: Usually interest bearing and with draw able on short notice.

- Fixed deposit: Interest bearing and definite period like one year or six month.

- Non Resident foreign currency deposit: All non residents of Bangladesh can open this interest bearing account in the form of term deposit with a minimum amount of $1000 or equivalent.

- Private Foreign Currency A/C: Bangladeshi National residing abroad or foreign nationals may open this a/c with deposit mode from inward.

- Convertible Take Amount: A type of non-interest bearing current a/c designed specially for foreigners living here.

- Private foreign Currency A/C: Bangladeshi nationals residing abroad or foreign nationals may open this a/c with deposit mode from inward.

Documents required for opening new account:

- Documents Common for all types of Account & Customers

- Advise of New Account

- Specimen signature cards

- Account Opening Agreement Form

- Photographs of Account Holder

- Deposit Slips Book

- Cheque book Requisition slips

- Letter of mandate is required where necessary.

Account opening procedure:

- Applying in a printed application in a certain stipulated form printed by the bank itself.

- Supply a set of printed forms required for opening the account which will normally include

i) Advise of new Account

ii) Specimen Signature Cards

iii) Account Agreement

iv) Deposit slip Book

v) Cheque Book Requisition slip

- The account should properly introduced by any one of the following

i) An existing Current Account holder of the bank

ii) Officials of the Bank not below the rank of an Assistant officer

iii) A respectable person of the locality well known to the Manager or Sub- Manger of the Branch concerned.

- A number of photographs which must be duly attested by the introducer in front of the manager or responsible officer. The signature of the introducer must be attested. After being scrutinize the application and the manager or authorized officer may give his consent to open the account.

- A package with deposit book, cheque book with a unique A/C No. given to the Customer maintaining the A/C opening register book.

Precautionary Measures of A/C Opening:

- Soon after the opening of a new Account a letter of Thanks should be sent to the introducer.

- A letter of thanks as per prescribed should also be sent to the account holder immediately upon opening the account, under registered post with a/c for verification of postal address as well as genuineness of the Account holder.

- In case of a new account is opened a proprietorship / partnership firm, having local business address, a responsible officer of the branch will inform the firm to obtain the confidential report on the firm.

Formalities for opening Current A/C and STD A/C:

These accounts are meant for business firms and corporate bodies. Initial deposit requirement is Tk 5000 in addition to common documents required to open a saving a/c following additional documents will be required for depending upon the nature of the organization.

Joint Account of two or more persons:

Mandate for Operation of Account: A clear authority by all the joint A/C holders containing instructions as to who will operate the account and how the account is to be operated should be obtained. The mandate should mention the name of the persons authorized to draw check. In case of death, insanity, insolvency of one or more of the joint a/c holders, the authority will cease to operate:

For sole traders:

i) Trade license

ii) A certificate with tax identification number from income tax authority

iii) Seal

iv) In case of current account an agreement to accept all responsibilities for all over draws, interest cost and expenditures

For Partnership firms:

i) Trade license

ii) Notarized deed of partnership

iii) A mended in agreement form regarding operation of the account signed by the entire partnership firm

iv) Sale/ Stump of the firms

v) 2 copy photo of all partners

For Private and Public Limited Companies:

i) Memorandum and Articles of association

ii) Certificate of incorporation

iii) Certificate of commencement of business if it’s Public limited

iv) Copy of board resolution to open a/c certificate by the chairman and secretary

v) Power of attorney to operate a/c in favor of any one or more of directors.

vi) Balance sheet and income statement

vii) List of Directors and their address and chairman certificate.

Formalities for opening Private foreign currency A/C:

Foreign Currency account may be opened in US dollar, Pound Sterling, Douche Mark and Japanese Yen. Credit may be made to this A/C against inward remittance from abroad. Usually this a/c operated like a current a/c but no checkbook are issued against his a/c. Withdrawals may be made through withdrawals slips. Interest may be paid on this a/c if it is maintained in the form of term deposit for a minimum of 90 Day’s Bangladeshis’ living abroad can open even without initial deposit. A nominee can be appointed.

Documents required: When an eligible person is interested to open an F/C account his passport is to be checked and signature verified. When he is staying abroad his signature is to be verified and attested by –

i) Bangladeshi embassy on that country

ii) His banker in this country

iii) Notary public of that country

Following documents are needed to:

i) Photocopy of 1st 4 pages of passport

ii) Photocopy of visa and work permit

iii) Nominees photo and account no.

iv) Declaration of source of income

Issue of Duplicate cheque book:

Duplicate cheque book in lieu of lost one should be issued only when A/C holder personally approaches the bank with an application. Fresh Cheque Book in lieu of lost one should be issued after verification of the signature of the Account holder from the Specimen signature card and on realization of required excise duty only with prior approval of manager of the branch. Cheque series number of the new cheque book should be recorded in ledger card signature card as usual. Series number of lost cheque book should be recorded in the stop payment register and caution should be exercised to guard against fraudulent payment.

Closing of Account:

Upon the request a customer an account can be closed. After received an application from the customer to close an Account, the following procedure are followed by a Banker.

The customer should be asked to draw the final cheque for amount standing to the credit of his a/c by deducting the amount of closing and other incidental charges.

In case of joint a/c the application for closing the a/c should be signed by all the joint holder.

Interest rate on deposit:

Interest rate different types of deposit as prescribed by PBL head office from time to time irrespective of size of deposit

Type of Deposits | Interest rates |

| a. Saving deposit | 8.00% |

| b. Special notice deposit | 6.50% |

| c. Fixed Deposit | |

| 3 Months | 7.50% |

| 6 months | 8.00% |

| 1year | 8.5% |

| 2 or 3 year | 9.% |

Clearing Section:

The Cheque Clearing Section of PBL principal office branch sends Inter Branch Debit Advice (IBDA) to the Head office on the receiving day of the instruments. The main Branch takes those instruments to the Clearing House on the following day. If the instrument is dishonored, Head office of PBL, sends IBDA to the PBL, Principal Office branch. The total procedure takes three days if everything goes orderly.

The Cheque Clearing Section of PBL, Principal Office branch sends Outward Bills for Collection (OBC) to the concerned Paying Bank to get Inter Branch Credit Advice (IBCA) from the paying Bank. If the instruments are dishonored by the Paying Bank, the Paying Bank returns it to the PBL, Local Officer Branch describing why the instruments are dishonored. The procedure takes around a week.

The Cheque Clearing Section of PBL, Principal office branch sends Outward Bills for Collection (OBC) to the concerned paying Branch to get Inter Branch Credit Advice (IBCA) from the paying returns it to the PBL, Local Office branch describing why the instrument is dishonored.

Local Remittance Section:

Local Remittance is used to transfer of funds denominated in Bangladesh Taka between banks within the country. It is an order from the Issuing branch to the Drawee Bank/ Branch for payment of a certain sum of money to the beneficiary. The payment instruction is sent by Telex / Telegram and funds are paid to the beneficiary through his account maintained with the Drawee branch or through a pay order if no a/c is maintained with the drawee branch. The cash department does remittance of cash. Instruments of local remittances at PBL branches are follows

Local Remittance

Telegraphic transfer TT | Demand Draft DD | Pay Order | |||

Pay Order:

- Pay order issue process

For issuing a pay order the client is to submit an Application to the Remittance Department in the prescribed form (in triplicate) properly filled up and duly signed by application. The processing of the pay order Application form, despot of cash/cheque at the Teller’s country and finally issuing a order etc, are similar to those of processing of L.D Application.

As in case of L.D each branch should use a running control serial number of their own for issuance of a pay order. This control serial number should be introduced at the beginning of each year which will continue till the end of the year. A fresh number should be introduced at the beginning of the next calendar year and so on.

- Charges

For issuing each pay Order commission at the rate prescribed by Head Office is realized from the client and credited to Income A/c as usual.

- Entries

Dr. Teller’s Cash/client’s a/c

Cr pays Order a/c

Cr commission a/c

- P.O issue Register

The remittance Department will issue the pay Order’s duly crossed “A/c payee” and will enter the particulars of the P.O Issued in the prescribed P.O Register duly authenticated.

- Payment of pay orders

As the P. Os crossed A/c payee, the same are presented to the Issuing branch for payment either through clearing of for credit to the client’s A/c. Os when presented for payment are processed in the Remittance Department. On making payment, the relative entry in the P.O Register is marked of by entering the date of payment in the P.O Register duly authenticated. The paid instrument is treated as Debit Ticket.

- Refund of Pay Order

The following procedure should be followed for refund of pay order by cancellation

- The purchase should submit a written request for refund of pay order by cancellation attaching therewith the original pay order

- The signature of the purchaser will have to be verified from the original application form on record.

- Manager/Sub-manager’s prior permission is to be obtained before refunding the amount of pay order cancellation.

- Prescribed cancellation charge is to be recovered from the application and only the amount of the pay order less cancellation charge should be refunded.

- The pay order should be affixed with a stamps “ cancelled” under should also be canceled with RED ink but in no case should be torn. The canceled pay order should be kept with the relevant Ticket.

- The original entries are to be reversed with proper narrations.

- Cancellation of the pay Order should also be recorded in the pay order Issue register #Issue and payment of Pay-order:

Strictly speaking pay-order is not meant for remittance. Because it is payable by the issuing branch. A order is issued to facilitate fund transfer within a clearing area.

Dr. tellers cash/Client A/c

Cr. Manages cheque

Cr. Commission

Up to Tk.1000 Tk. 10

Tk.1001-100000 Tk. 25

Tk.100, 001-500000 Tk. 50

Above Tk.500000 Tk. 100

When paying against pay-order following entries are passed

Dr. Manager’s cheque

Cr Cash/Client A/c

Loans and Advances:

Introduction:

Major source of income of a bank is the earning from credit. Borrower selection is the main and prime task of this department. Advancing loans is the primary function of the commercial banks. Without loans country’s industrial and commercial development is not possible. Therefore, smooth loan system in banking sector is a catalyst for economic development of a country.

Manager’s Concern:

In the process of loan Manager has to ensure three things:

1) How to locate purpose

2) How to locate security

3) How to locate borrower

How to locate purpose:

Manger has to ensure that the loan will generate adequate cash. For that matter the loan should be engaged in productive activities. Such an employment will increase economic activities, promote trade and commerce, create employment avenues and increase movement of goods and flow of cash. This flow of cash is known in the banking concept as cash generation. If there is enough cash generation, funds will automatically flow into the borrowers accounts with the bank and will show a satisfactory turnover in accounts which the lending bank always demands. This is why the manager’s speculation should be making the highest cash through the employment of the advances.

How to locate security:

As soon as the evaluation of purpose is done manager will examine and evaluate in the following manner the securities offered by the prospective borrower:

a) Security is the source of information on the prospective borrower. If offered are valuable properties like land, building, shares of stocks or pledged goods, these will offer adequate information about the borrower as to his financial position.

b) If securities are hypothecated stocks of raw materials for production, these will offer adequate information about the borrower as to his ability or capacity to utilities

c) Securities (tangible or intangible) offer a yardstick for measuring the extent of involvement of the borrower himself. The lending bank’s investment of funds is a joint venture of the banker and the borrower. The securities offered are the borrower’s portion of involvement i.e. his equity or capital. Thus the greater is his involvement, the better for the banks. The borrower in that case will think twice that if the business goes wrong, it is who will suffer most. Thus it will be in his own interest that he will avail and utilize the loan as per agreed stipulations. Thus the best way to safeguard the lending banks interest is, as far as possible to maximize the banks commitment.

d) The branch Manager’s responsibility as to security is also to see how much control he will be in a position to exercise on the entire stocks of the borrower.

How to locate borrower:

In appraising a loan process, the selection of the prospective borrower is the most vital point. The borrower is the real actor and must be in position to achieve the purpose for which the loan has been requested. In selecting ideal borrower, the branch manager thus assumes the greatest responsibility. Capital is another point to indicate the borrower’s position. He should be given loan in proportion to this own investment as working capital. As a general rule a bank should not sanction loan more than the investment of the borrower.

Then the consideration of borrower’s capacity – whether the borrower can utilize the funds or not.

Of all the qualifications of a prospective borrower, character is undoubtedly the greatest. While the capacity and capital are the factors upon which depends his ability to repay the money advanced, the character of the borrower indicates his intention to repay the loan.

To select the ideal borrower the following points have to consider:

a) Branch records: The manager may have first hand information on a prospective borrower by a reference to his records, if the banks with him. The turnover of his financial dealings is reflected in the ledger folios of his branch.

b) Borrower’s Record: The prospective borrower may be advised to submit his books of accounts balance sheet etc. for examination by the manager. These financial tools reflect the position of his assets and liabilities and a fair idea about the capital and capacity of the borrower.

c) Personal Enquires: As an individual the borrower must be a desirable person in the society. He must have integrity. There are some factors such as the sobriety, the promptness of payment goods habits personality, the ability and the willingness to carry a project

Advance Secured and Unsecured:

- Secured Advance: Secured advance are those advance which are secured by tangible securities of adequate value over which the bank has either absolute or constructive control in addition to the personal guarantee of the customer.

- Unsecured Advance: The advances which are granted to a constituent of undoubted standing and reliability and only in exceptional circumstances and for short period without any tangible security are called unsecured advances.

Types of Loan:

Pubali Bank Principal Branch has the following loan schemes

- Continuous Loan

- Demand Loan

- Term Loan

- Cash Credit (CC)

- Overdraft (OD)

- Bank Guarantee

- Staff Loan(PBL)

Continuous Loan: The limited loans with expiry date of loan payment, which can be transacted without any particular payment schedule, are termed as continuous loan. Following are the various categories :

- Small Enterprise Financing (SEF)

- Consumer Financing (CF)

- Other than SEF and CF

Demand Loan:

The loans, which become eligible for payment when demanded by the bank, are termed as demand loan. If contingent or any other debt becomes forced loan, then those are also termed as demand loan.

Following are the various categories :

- Small Enterprise Financing (SEF)

- Consumer Financing (CF)

- Other than SEF and CF

Term Loan:

The loans which are to be paid within limited term with a particular payment schedule are known as term loan.

Following are the various categories :

(a) Term loans up to 5 years

- Small Enterprise Financing (SEF)

2. Consumer Financing (Other than HF & LP)

3. Housing Finance (HF)

4. Loans for Professionals to setup business. (LP)

5. Others

(b) Term loan over 5 years

- Small Enterprise Financing (SEF)

2. Consumer Financing (Other than HF & LP)

3. Housing Finance (HF)

4. Loans for Professionals to setup business. (LP)

5. Others

Short term Agri and Micro Credit: The short-term loans which are listed in yearly loan disbursement schedule served by the loan department of Bangladesh Bank, are termed as short-term agricultural loan and micro-credit. The loan given to the agricultural sector for less than 12 months is also included in this category. By short-term loan we mean the loan below Tk 10,000 to be paid within 12 months.

Loan classification and provision of 2006 as on date 30th September.

Cash Credit (CC):

| |

CC (hypothecation) | CC (pledge) |

| |

Over Draft (OD):

| |

| Secured Overdraft – SOD | Loan General – LG |

| |

OD and CC amount as on 27th October, 2006

- Over Draft 141,77,69,177.12

- Cash Credit 47,24,41,768.59

Bank Guarantee:

| |

| Bid Bond | Generally issued while dropping tender for work. |

| Performance Bond | It is issued when customer gets a specific work-order. Here bank guarantees that his customer is willing and able to complete the required work, and bank takes the responsibility of completing the contracted work. |

Staff Loan

Staff House Building Loan – SHBL:

- 120 times of the basic salary is provided as SHB

- Bank Rate + 1%, interest is charged to the employee

- Repayment is adjusted from their monthly salary

- Repayment is made at equal monthly installment

Staff Loan Against Provident Fund – SPF:

a. 10% of basic is contributed by employee in every month

- b. 10% of basic is also contributed to the PF by the Bank

- c. Repayment is adjusted from their monthly salary

- d. Maximum Sanction from PF

Process of Loan:

| Heads | Characteristics |

| Application | Applicant applies for the loan in the prescribed form of the bank describing the types and purpose of loan. |

| Sanction |

|

| Documentation |

|

State of Classification and Provision for 5 Years of PBL:

With the passage of time the bank is expanding day by day. Due to expansion the bank is offering more loans to its clients. That is what we see that the amount of loan is increasing gradually from year 2001 to 2005. Bangladesh Bank is promulgating improved and renewed rules to check the loan default and enhance recovery. Accordingly Pubali bank is also enacting newer policies. Here

The amount of classified loan is decreasing and that is nearer to 32%. As the offering of loan is increasing day by day, so it is quite encouraging that the amount of classified loan should checked and it is becoming less than half.

Figure 11: Recovery of Classified Loan:

Again from the figures and graphs above we see that, recovery of classified loan was on an average 10% to 15%, which is not at all satisfactory. Though the amount of classified loan is controlled the amount of recovery has not been increased as it is expected. It seems that there is a lack in either rules of recovery or lack in incentives for the officers and employees to recover the classified loan. Even then it is quite encouraging to see that recovery rate of last year was 20%.

Classification of loans and advances:

Loans may be classified in three categories

1) Substandard

2) Doubtful

3) Bad and loss

After six month loan become Substandard, after 12 month loan becomes doubtful, after 24 month loan becomes bad and loss

Criteria for Classification

1) Over due period

2) Required payment

3) Legal action

4) Limit over drawn

5) Qualitative judgment

1) Over due period:

If the gap between expiry date and reference date is over 5 month then the mode of classification will e substandard, if over 11 month then it will be doubtful, if over 23 month then mode will bad and loss

2) Required payment

Either the time period 6 month or the gap between reference date and Expiry date the closest one is chosen. The credit summation for a certain time period (say 3 month) is worked out and is converted into one year time period. If this worked outbalance is higher the Highest debit balance then the loans unclassified and if it is lower than the highest debit balance then the loan is said to be classified.

Legal action

The classified is considered on the basis of illegal transaction

3) Limited over drawn:

When the borrower with draws money from his loan A/C and the withdrawn amount exceeds the actual sum granted, then loan becomes classified. In this case 45 days are considered for repayment and after 45 days. The loan becomes classified.

4) Qualitative judgment:

The classification decision is taken on the basis of the qualitative nature of the loan.

Foreign Exchange:

Introduction:

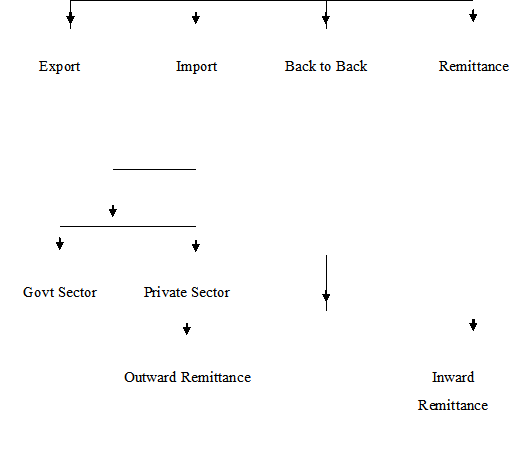

Banks play a very important role in foreign exchange transaction of a country. Mainly transactions with overseas counties are respect of imports, exports and foreign remittance come under this. Banks are the vital sectors of Foreign exchange transactions. Central Bank record all sorts of Foreign Exchange transaction which is to be reported regularly (e.g. daily, fortnightly, monthly quarterly, yearly etc.) to Bangladesh Bank. This part of the report consists of the following areas

1) International Trade : Import & Export

2) Foreign Exchange related banking terms & rules

3) Foreign Exchange rate & foreign Remittance.

Foreign exchange transaction is classified according to there activities.

Foreign Exchange

International Trade:

International trade is the trade between countries with the rest of the World. Now we live in a global economy. In the age of globalization each country has free access to the market of other with quality goods and services.

International Trade has two components – as following Import & Export.

To handle of International transaction in a sound and efficient manner there must have a written contract between the buyer & seller. For international trading purpose a Bank or Banks may involve in this contract and then the contract renamed into a letter of credit. It is the media under which the international trades are concluded.

Function of Foreign Exchange Department:

- L/C Opening

- L/C Amendment

- Sanctioning PAD, LIM, LATR.

- T.C issuing

- Foreign Bill Purchase(FBP)

- Local Bill Purchase(LBP)

- Foreign Remittance

- FC A/C maintaining

- Foreign Currency remitting

Foreign Exchange Mechanism:

01) L/C Opening

02) Issue the L/C by issuing Bank and send to advising bank

03) Advised and or confirm the L/C by Advising and Add confirming Bank

04) Submit the documents to Negotiating Bank by export

05) The Negotiating Bank makes payment

06) The Negotiating Bank forward/sends documents to issue bank

07) Issuing Bank makes payment to negotiating bank

08) A issuing bank instructs to pay or reimburse the paying bank and paying bank makes payment or reimburse to the negotiating bank

09) Issuing bank sends documents to the import

10) The import makes payment

Types of L/C Offered:

Letter of Credit (L/C) can be defined as a ‘Credit Contract’ whereby the buyer’s bank is committed (on behalf of the buyer) to place an agreed amount of money at the seller’s disposal under some agreed conditions. It is also known as documentary letter of credit. It may be either:

(i) Revocable: A revocable credit is a credit which can be amended or cancelled by the issuing bank at any time without prior notice to the seller.

(ii) Irrevocable: It constitutes a definite undertaking of the issuing bank(since it can’t be cancelled or amended without the agreement of all parties thereto), provided that the stipulated documents are presented & the terms and conditions are satisfied by the seller.

Special documentary Credit:

- Revolving Credit: It is the credit which provides for restoring the credit to the original amount after it has been utilized.

- Transferable Credit: It can be transferred by the original beneficiary in full or in part to one or more subsequent beneficiaries.

- Back to Back Credit: It is a new credit opened on the basis of an original credit in favor of another beneficiary.

- Anticipatory Credit: The anticipatory credit makes provision for pre-shipment payment, to the beneficiary in anticipation of his effecting the shipment as per L/C conditions.

- Red Clause Credit: A red clause credit is a credit with a special condition incorporate into it that authorizes the confirming Bank or any other Nominated Bank to make advances to the beneficiary before presentation of the documents.

- Green Clause Credit

Parties Involved in L/C:

There are number of parties involved in a letter of credit and the right and obligation of the different involved parties will differ from each other. The involved parties to a letter of credit are named below:

01) The applicant/The importer/The buyer

02) Opening bank/Issuing bank

03) The beneficiary/The Exporter/The seller

04) The Advising Bank/The transmitting Bank/The notifying bank

05) The Confirming Bank

06) The Negotiating Bank

07) The Reimbursing Bank/Paying Bank

Characteristics of the importer who wants to open a letter of credit:

- Must have an A/C in the branch

- Must be a member of the Chamber of Commerce

- Must be a TIN holder

- Must have IRC(Import Registration Certificate)

- VAT(Value Added Tax certificate)

Chapter 4

Findings & Analysis:

Major findings of the study:

- The organization has a human resource management.

- The organization has a prescribed salary structure.

- The organization has provided provident fund & gratuity facilities.

- The accounts department has professional accountant.

- The training department has needs more trainers.

- They have to recruit technologically sound people for their future project.

- The organization has to motivate the different personnel & provide different facilities to get best effort from them.

- Technical support department must be more conscious about customer care.

- Management will have to concern about the satisfaction of the employee.

- Leave & working hour are not maintained.

- Last two years the turnover rate of employee is getting higher.

Analysis of this report are as follows:

Recruitment & Selection:

Training Facilities:

Job Design:

Compensation:

Bank Safety and security:

Recruitment involves assessing the nature of a post and advertising for suitable candidate.

“Recruitment is the process of finding and attracting capable applicants for employment. The process begins when new recruits are sought and ends when their applications are submitted. The result is a pool of applicants from which new employs are selected.”

The process of defining the recruitment should stunt with an analysis of the job. This is called Job analysis.

Job analysis has three components:

1. Job descriptions: a written statement of the job holder does, how it is done and why it is done.

2. Job specifications: statements indicating the minimal acceptations qualifications incumbents must posses to successfully perform the essential elements of their jobs.

3. Job Evaluation: specifies the relative value of each job in the organizations

In light of Pubali Bank’s job analysis practice:

1. Job description: management generally offer for the post of probationary officer each year, they also offer higher post like executives, Senior vice president , Senior asst. vice president, Managing director, Deputy managing director.

2. Job specification: In this job specification section. Required qualification differs by the nature of the job.

The Job specification table of PBL is given below:

Job Description | Educational Qualification | Experience | Age Limit |

Probationary Officer | MBA/MBM/MA from any reputed university. At least Two first division in the entire education life.(No third division) | N/A | 30Years(Maximum) |

Executive | MBA/MBM/MA from any reputed university. | At least five years of banking experience. | 40 years(Maximum) |

Senior assistant vice president | MBA/MBM/MA from any reputed university. | At least eight years of banking experience. | 45years(Maximum) |

Senior vice president | MBA/MBM/MA from any reputed university. | At least ten years of banking experience. | 48years(Maximum) |

| Managing Director | PhD in Finance/Management/ Accounting | At least fourteen years of banking experience. | 55years(Maximum) |

Deputy Managing Director | PhD in Finance/Management/ Accounting | At least fourteen years of banking experience. | 52years(Maximum) |

Classification of staff of Pubali Bank Limited:

There are four types of PBL staff. Those are as:

Regular Staff:

There are levels of Employee. The employee will work one year as a trainee before being permanent. After being permanent the staff may be come under the shade of provident fund. Assistant Officer, Junior Officer, Probationary Officer, Executive, vice president, senior assistant vice president, senior vice president, Executive senior vice president all are regular staff. The total number of regular staff is five hundred thirty two.

Project Staff:

During a running project; the staff is appointed on the basis of project duration. Posting from the appointed project is not possible. Project staff will get benefit and opportunity on the basis of rules and regulation of the project and terms and condition of appointment letter. Managing director, Deputy Managing director, Secretary is the project staffs.

Service Staff:

Service Staffs are graded staff. Period of probation is not applicable for the service staff. Service staff can be the member of provident fund after they join in the job. Office assistant, Guard, Cleaner is treated as service staff. There is seventy five service staff in PBL.

Contract Staff:

The duration of employment depends on the contracted time -limit. Job benefit and opportunity will determine by contract. The time-lime of contract can be renovated. Period of probation is not applicable for the contract staff. Contract staff will not get the benefit of provident fund, gratuity for service and festival allowance. Example-Chartered accounts.

Recruitment Process Of Pubali Bank Limited.

There are various methods which a company can select the right people for the right post .How ever Pubali Bank Ltd. do not apply all the methods that exist in the books of Management. The sources of man power have a great influence on the method of selection.

PBL recruit its employees from both internal & external sources.

Staff Recruitment Board:

The representative authorized by the human resource division and nominated by the program will take the viva of the applicants. To ensure the quality and subject oriented staff recruitment, the orientation of board member may be held if it is necessary.

If any relative applicant applies then it should avoid from being the board member.

At least one member of board should come from the human resource division.

Deployment of New Staff:

Regular staffs have to agree to work any place where Standard Bank Limited operates their operation in Bangladesh.

Joining of New Staff:

The staff will join on his/her specific joining date specified by the Pubali Bank Limited. In case of head office or branch office, each staff should have joined his/her work before 9.00 am. Staff can join on his work within seven days of his/her joining date and local authority can accept the joining report. After seven days it is not possible to join without the permission of human resource division. The new staff will submit the following papers or documents when he/she joins:

Interview Card: Issued by the HRD. Joining related all information are given in the interview card.

Bond of Security: Before joining the new staff has to sign the bond of security. Rules of this paper are if he/she leaves the job before three years then she/he must return 30% of his total salary.

Identity Card (Certificate issued by Chairman): name, residence-address, organization’s name, designation, blood group are given in the card.

Blood test report: The new employee should have to place his blood group, HIV& Hepatitis test report to the authority two days before joining.

Time Table of work:

The working day of Standard Bank Limited head office & in AD branches is Saturday to Thursday. The Friday is the weekend holiday. But in non AD branches, working day is from Sunday to Thursday.

Record of Attendance:

All staff should have to sign in the attendance register in attendance book which kept in workplace to record his attendance. Every employee has to sign in the attendance register before starting work.

Every one should attend in office timely. If any staff attends after 15 minute of scheduled time then he/she will consider as late. If any employee comes lately 3 times in a month then it will consider as his 1-day casual leave. If any staff comes lately seven times in a month then the manager of the branch will give him a warning notice. One copy of that warning notice will send in human resource division.

If any employee gets continuous 3 warning notice then the staff may be terminated. If any employee is on leave then it should have a clear description of his leave and types of leave in the register book.

Recommendation and conclution:

Recommendations:

Pubali Bank is the largest bank in the private sector of our country. Increment in the net profit of the banking sector was on an average 10% last year. Though it is observed that credit management of the bank is quite satisfactory, the following recommendations can be taken into consideration to make it more effective.

Bangladesh Bank should monitor more closely the lending activities of Pubali Bank.

- As once upon a time it was a nationalized bank, various rules regulations, office norms and working environment still exist like other nationalized banks of our country. Pubali bank has to come out from that footing and be organized like some reputed private sector banks, which are doing very well.

- There exist various rules and also prescribed format for offering loans and advances to the customers. In maximum of the case these are not followed properly. Lending Risk Analysis (LRA) is not done regularly and properly.

- Application forms of the customers remain erroneous and full of wrong information. It has been observed that the information given by the customer regarding business, property holding, inventory, bio data of entrepreneur do not tally on ground. Even after that the banker provides these customers with loans after doing necessary correction in the customer’s application by the banker. Close monitoring and supervision has to be ensured by the bank authority in this respect.

- After assessing 3-4 years record it is found that near about half of the loans and advances have become classified. Moreover 4-5% of that classified loans are substandard or doubtful. Almost all the amount of classified loan is bad/loss percentage of which is 95%. Carrying forward of this loans have made the figure of the net profit of the bank an inflated one which is also misleading. Some bad/loss loan with long outstanding duration has to be written off.

Assessing the five years credit statement of the bank, it is found that recovery rate of classified loan is only 10% to 15% which is very much alarming. Though it slightly increased last year, a coordinated effort has to be undertaken by the bank to increase the recovery rate.

More incentive program needs to be undertaken for the officers and employees of the bank to improve the recovery rate. Here the incentive scheme taken by Bangladesh Krishi Bank named “MIRACLE” can be mentioned which has given fruitful result.

Credit information bureau (CIB) should act more efficiently. All the necessary information of a prospective borrower should be available to the bank authority also. Here the bank should use upgraded computer software for this purpose.

- The bank itself should be much more cautious before sanctioning loan. The bank authority should strictly follow the loan appraisal procedure, and also ensure that all the information provided by the clients is correct.

- All the officers and employees working specially in the recovery section should be more sincere to their respective job.

- Long outstanding cases filed in the insolvency court should be resolved as early as possible with greater priority. For its own interest bank should employ well-reputed lawyers to settle all the outstanding cases.

- More emphasis should be given on foreign exchange transactions. Timely collection of export proceeds has to be ensured. The bank should strictly follow all the means and ways to check the fraudulent activities in case of foreign exchange trade.

- Opening an L/C involves lot of paper works and also time consuming. Officers and employees are not also very thorough and well conversant with the rules and policies of foreign exchange. They need to be trained on these and the whole system has to be made computerized so that it takes less time to open an L/C.

- Due to non-availability of affiliation, negotiation becomes difficult with some of the foreign banks. For this some prospective exporter and importer are discouraged to do their business with all those particular countries. To expand the business activities, Pubali bank should make an endeavor to increase the affiliation with more number of foreign banks.

Normally in our country most of the report does not see the light, they remain in pen and paper. Even if it is published, the recommendations are not implemented. It is nice to observe that Government has already promulgated some rules basing on those recommendations. So the recommendations should be implemented despite of any hindrance for the betterment of banking sector.

During the seven weeks practical orientation at Corporate Branch, almost all the desks have been observed more or less. It has been arranged for gaining knowledge of practical banking and to compare this practical knowledge with theoretical knowledge. Comparing practical knowledge with theoretical involves identification of weakness in the branch activities and making recommendations for solving the weakness identified. Though all departments and sections are covered, it is not possible to go to the depth of each activities of branch because of time limitation. However, highest effort has been given to achieve the objectives the practical orientation.

Conclution:

With a view to analyzing the status of Pubali Bank Limited applied in indeed very much consistent and relevant to develop the rural areas. Human resource management is the process of acquiring, training, appraising, and compensating employees, and attending to their labor relations, health and safety, and fairness concerns. It’s true that any individual who works in Human Resources must be a “people person.” Since anyone in this department deals with a number of employees, as well as outside individuals, on any given day, a pleasant demeanor is a must.

In the light of above information we find that This Organization has excellent competitive advantage than its measure competitors. It is also positive considerable performance of the organization merging internationally, besides this Organization is giving efforts to introduce different types of problem. On the other hand to make Organization’s business position strong. Human resources management is very much important for every business organization. Human Resources may be the most misunderstood of all corporate departments, but it’s also the most necessary. Those who work in Human Resources are not only responsible for hiring and firing; they also handle contacting job references and administering employee benefits. Actually these departments do that work.

This department of the organization works with the employee and the staff and worker. This department deals with their job planning and design, recruitment, selection, measure their job performance and target their compensation.

Chapter 6

Referrences:

Morris.(1986),Innovations in Banking, Beckenham, Coon Helm. Peters, T. and Waterman, R. (1982), In Search of Exellence, New York, Harper and Row.

Torrington, D. and Tan Chee Huat (1994), Human Resourse Management for South East Asia, Simon & Schuster, Singapore.

Wilkinson A. (1991), The Changing Fortunes of the Corporate Bank, Journal of Co-operative Studies, No 71 June P5-10.

Bastone, E. (1984). Working Order, Oxford, Basil Blackwell.

Human Resource Management

Tenth edition, Gary Dessler

Annul Report-2007

Pubali Bank Limited.

Decenzo,. DavidA. & Robbins, Stephen P. Human Resource Management. Sixth Edition, John Willey&Sons, Singapore. 2003.

Baird, Marian & Compton, Robert & Nankervis, Alan Strategic Human Resource Management. Fourth Edition, South-Western Publishing Co. 2002.

Griiffin, Principles of Management. Fifth Edition, McGrew-Hill. 1996.

Robins, Stephen P. Organizeational Behaviour. Fourth Edition, McGrew-Hill. 1996.

Randall S.Schuter

Wright and Mcmahum (1999)

Websites:

www.pubalibank.com

Chapter 7

Appendix:

Recruitment Process:

1. In which methodology man power is recruited?

(a) written test& viva voce

(b) Without written test& viva voce

2. Is any circular published in news paper in recruiting process?

(a) Yes

(b) No

3. Who supervise the whole recruiting process?

(a) Managing director

(b) Director

(c) Administrative office

(d) HRM officer

4. What educational criteria asked for appointment of staffs? Is any prior working experience is needed?

(a) Minimum graduate.

(b) Minimum diploma on engineering.

(c) Minimum masters.

5. Is any written examination been held for appointment?

Is any practical test of the cleaned criteria been held?

(a) i- Yes

(a) ii-No

(b) i-Yes

(b) ii- No

Training facility

- Is there any scope for training of the employees?

(a) On the job training 1-3 months.

(b) Of the job training 3-4 months.

B. Who does give the training? What criteria do they held?

(a) Manager

(b) External trainer

C. Is the training compulsory for all?

(a) Yes

(b) No

D. Is any training been given to the staffs of lower ranks?

(a) Yes

(b) No

Compensation

- How the amount of compensation is specified for each staff?

(a) Policy determination and market definition.

(b) Conduct pay surveys and draw policy line.

(c) Competitive pay levels and structure

(d) All the above.

- In what basis the compensation of the staffs is increased?

(a) performance

(b) Seniority

(c) Working experience

(d) All the above.

- Is any reward been given for better performance?

(a) Yes

(b) No

- Are any employee benefits offered?

(a) Yes.

(b) No.

D (i ) If yes what are they ?

(a) Life insurance

(b) Pension

(c) Workers compensation

(d) All the above.

Job design

- Is the skill variety demanded from the individual workers?

(a) yes

(b) No

- Is there any task identity for the staffs?

(a) Yes

(b) No

- Is the autonomy been given to the staff?

(a)Yes

(b)No.

- Is there any scope for flex time?

(a) Yes

(b) No.

A newspaper advertisement of PBL for the post of probationary officer:

Pubali Bank Limited

Head Office:

Recruitment of “Probationary Officer”

Pubali Bank Limited a third generation progressive private commercial bank with steady growth in it’s business expansion program desires to recruit 5th batch of PROBITIONARY OFFICERS to strengthen the team with potential candidates who are challenge striving, forward looking, proactive, self-motivated with positive attitude & pleasing personality & possessing consistent high grade academic track record.

Candidates from Bangladeshi citizen with MBA/MBM/Masters

in Accounting/Banking/Finance/Marketing/Economics/

Political Science/ Sociology/Physics/ Mathematics / history/English/

Psychology / Public.Admin./ International Relations/Agriculture having at least two 1st class, no “Third division”, during their entire academic courses with age bar of 30 years (maximum)as on 31.12.2007 may apply with confidence furnishing their detailed “Resume”, with two copies of recent passport size photograph, authenticated copies of all academic certificates along –with Draft/Pay-order for taka.300/-(Taka Three Hundred) only (non-refundable)in favor of Pubali Bank Limited, addressed to the Managing Director, Pubali Bank limited, Head Office, 26 Dilkusha Motijheel C/A,Dhaka-1000 to reach latest by 10th September,2009.

Candidates possessing requisite qualification shall have to sit for the written test to complete the selection process.

Selected candidates will be appointed on Probation for a period of 1(one) year with a monthly consolidated pay of Tk.18, 000/- (Taka eighteen Thousand) only. On successful completion of Probation period they will be absorbed as “Officer” under the regular pay packages as admissible in the grade. Any kind of persuasion shall be as disqualification of the candidates.

The specimen of Pubali Bank Limited Performance Appraisal:

Pubali Bank Limited

Performance Appraisal Form

(For Asst. Officer to above)

Reporting Period

From :

To :

To be Filled in by the concern employee

PART – I

Section – ‘A’

a) Name :

b) Present Designation :

c) Date of Birth :

d) Educational Qualification :

e) Professional Qualification :

f) Date of Joining in PBL :

Along with status

g) Present status with date of :

Promotion

i) Past Banking Experience :

1. Non officer’s Grade :

2. Officer’s Grade : :

3. Executive’s Grade :

j) Non – Banking Experience :

(if any ) Other than Bank

j) Division Dept. Branch :

Presently attached to

To be Filled in by the concern employee

Section – ‘B’

a) Job specification:

b) Business Performance :

(Applicable for Branch-In-Charge)

Target for Achieved up to 31.12.200… %of Target achieved

1)Deposit :

2)Advance :

3)Profit :

4)Exports :

5)Imports :

6)Remittance :

Income

7)Profit/Loss :

c) Business Performance for the current 12months :

(Applicable for Officer’s & Executives other than Branch-In-charge)

Sl. No. | Description of Performance | Target | Achievement | Name of the Branch where booked |

1. | Deposit | |||

2. | Recovery of stuck-up classified advance | |||

3. | Other Business |

N.B : Attach details on separate sheet duly signed by Branch In-charge.(if necessary)

INSTRUCTION FOR REPORTING OFFICER:

PART-II

GUIDELINE FOR PERFORMANCE RATING:

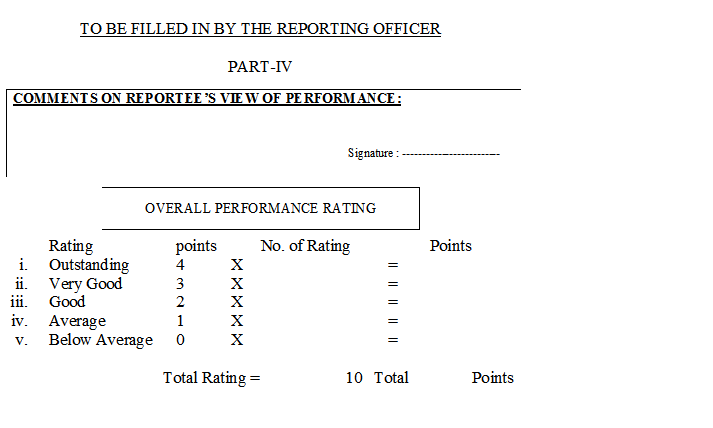

- Be an immaculate judge of fairness. The employee should be apprised on each of the factors in relation to his present job position. Total marks awarded should be entered in overall performance rating column in Part-04.Remember; correctness of this appraisal depends upon the care, impartiality & judgment used by the Appraiser. General comments should be avoided each comment should be specific.

- SPECIAL INSTRUCTION: FOR RATING OF “OUTSTANDING” & “BELOW AVERAGE” SPECIAL JUSTIFICATION IS NECESSARY UNDER ‘OVERALL PERFORMANCE RATING”IN PART -04.

- Points can be allowed on the basis of Management executive consensus : 10

- Maximum points can be obtained for Appraisal Report (10 criteria’) : 40

……………..Total points(c+d) : 5 0

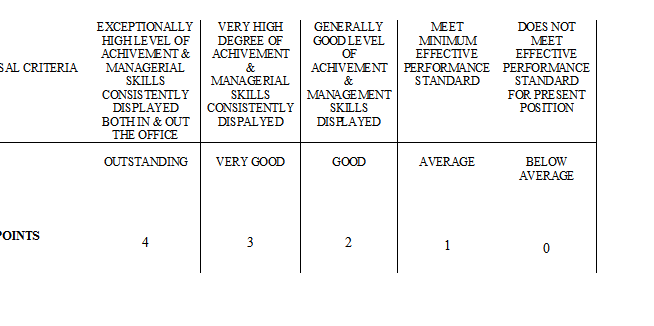

2. APPRAISAL CRITERIA: Rating Point

a) Exceptionally high level of achievement and Managerial skills : Outstanding = 4

Consistently displayed both in & out of the office.

b)Very high degree of achievement & Managerial skills : Very Good = 3

Consistently displayed.

c) Generally good level of achievement & Managerial : Good = 2

Skills constantly displayed.

d) Meet minimum effective performance standard : Average = 1

e) Does not meet minimum effective performance : Below Average = 0

standard for that position.

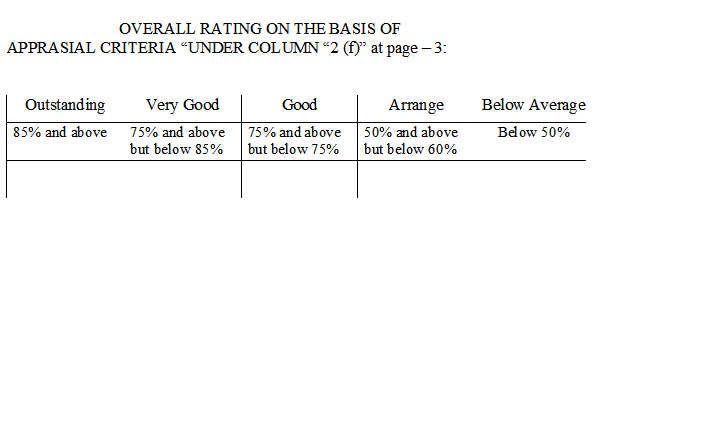

f) Overall performance rating as per criteria below:

- i. Outstanding : 85% & above.

- ii. Very Good : 75% & above but below 85%

- iii. Good : 60% & above but below 75%

- iv. Average : 50% & above but below 60%

- v. Below : Below 50%

PLEASE INITIAL AGAINST THE RATING AS YOU FEEL APPROPRIATE:

TO BE FILLED IN BY THE REPORTING OFFICER

PART-III

(DETAIL OF PERFORMANCE RATING)