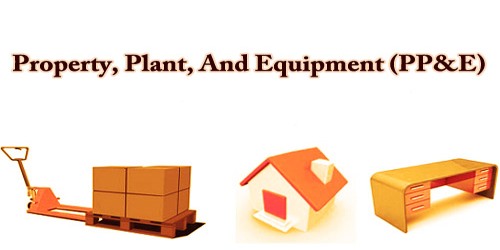

Property, Plant, and Equipment (PP&E) is a non-current, measurable capital asset shown on a company’s balance sheet and used to produce sales and profits; these are of a physical nature or may be affected. PP&E’s total value can vary from very low to extremely high when compared to total assets. It plays a key part in the financial planning and analysis of a company’s operations and future expenditures, especially with regards to capital expenditures.

Property, plant, and equipment assets are usually listed at their expense, followed by a deduction for the cumulative depreciation that applies to all of these assets except land; which is not depreciated. Purchases of PP&E are proof that management has faith within the long-term outlook and profitability of its company. The PP&E account is commonly denoted as net of accumulated depreciation; this implies that if a company or an organization doesn’t purchase additional new equipment (therefore, its capital expenditures are zero), then Net PP&E should slowly decrease in value every year due to depreciation.

Property, plant and equipment (PP&E) are also called fixed assets, which means they are tangible assets that cannot be easily liquidated or sold by a corporation. This is a measurable object on a fixed-asset portfolio and is normally very illiquid. A business may sell its equipment, but it does not sell its inventory or assets such as bonds or stock shares as easily or quickly as possible. The value of PP&E between companies varies substantially according to the nature of its business. Examples of property, plant, and equipment include the following:

- Machinery

- Computers

- Vehicles

- Furniture

- Buildings

- Land

PP&E’s importance depends on its age and cost of originality. All fixed assets are recorded at their purchase price and are recorded at their historical cost on the balance sheet. As time goes on, each period of the assets is depreciated slowly decreasing their reported book value. PP&E assets are tangible, identifiable, and expected to come up with an economic return for the corporate for quite one year or one operating cycle (whichever is longer). Investment in PP&E is additionally called a capital investment; Industries or businesses that need an outsized number of fixed assets like PP&E are described as capital intensive.

Property, Plant, and Equipment (PP&E) Formula:

Net PP&E = Gross PP&E + Capital Expenditures – Accumulated Depreciation

To measure PP&E add to capital expenditure the amount of gross property, plant, and equipment specified on the balance sheet. First, deduct from the impact of cumulative depreciation. In most cases, when reporting financial results, companies will list their net PP&E on their balance sheet, so that the calculation has already been done.

If a company or an organization produces machinery (for sale), that machinery doesn’t classify as property, plant, and equipment. The machinery wont to produce the machinery for sales is PP&E, but the machinery manufactured purchasable is classed as inventory. The same is true of real estate companies that own buildings and land under their control. Their office buildings and land are PP&E but they are inventory of the houses they rent.

Property, plant, and equipment (PP&E) are vital to many businesses’ long-term success but are capital-intensive. When the corporate spend money investing in either (1) updating existing equipment, or (2) purchasing new additional equipment, this adds to the entire PP&E balance on the record. Companies or organizations sell a portion of their assets often to collect cash and increase their profit or net profits. As a result, tracking the investments a company makes in PP&E and any sales of its fixed assets is significant.

Information Sources: