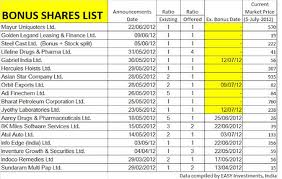

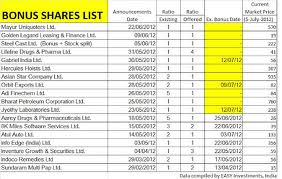

What are bonus shares?

Bonus shares are shares allotted to the existing members of the company pro rata with the shares they already hold and the shares are paid for by the company out of its accumulated profits. In other words, instead of paying out the profit as dividends, the money is used to pay for additional shares given to each shareholder.

Why are bonus shares issued?

The reasons for doing are various but can include:

- making the balance sheet look stronger by increasing the share capital

- making individual share values more realistic

- increasing the number of shares so that some may be given away or sold

- increasing the number of shares held by the existing shareholders so that the company may issue other shares to outside investors.

Procedures for issuing bonus shares

Issuing bonus shares will involve a share allotment and must be recommended by the directors and approved by the shareholders.

If the company has an authorised share capital, the articles may need to be updated to remove the limitation on the number of shares that may be allotted. There can be complications where the company has different classes of shares, in which case there must be careful review of the terms attached to the different classes.

Our service

The Company Law Solutions service for allotting bonus shares provides all required:

- guidance as to the applicable procedures

- notices of directors’ meetings

- minutes of directors’ meetings

- notices of shareholders’ resolutions

- shareholders’ consents to resolutions

- notices for Companies House

- completed official forms for Companies House

- our straightforward, step by step guide to completing the procedures

- checking by us when the documents are completed (if required)

- dispatch by us to Companies House of the completed and checked documents (if required)

- guidance on completion of share certificates

- guidance on completion of statutory registers

If we required, we can supply share certificates and/or statutory registers as an additional service.

If the company is a single person company, with just one director/shareholder, appropriate alternative documentation is provided.

Prices

Most bonus issues will fall within the benchmark price. Increased charges may apply if the articles need to be updated to remove the authorised share capital or there are complications with multiple share classes.

Steps involved in Issue of Bonus Shares

A company issuing bonus shares should ensure that the issue is in conformity with the guidelines for bonus issue laid down under Chapter IX of SEBI (Disclosures and Investor Protection) Guidelines, 2000.

The procedure for issue of bonus shares by a listed company is enumerated below:

1. Ensure that bonus issue has been made out of free reserves built out of the genuine profits or securities premium collected in cash only.

2. Ensure that reserves created by revaluation of fixed assets are not capitalised.

3. Ensure that the company has not defaulted in payment of interest or principal in respect of fixed deposits and interest on existing debentures or principal on redemption thereof or in respect of the payment of statutory dues of the employees such as contribution to provident fund, gratuity, bonus etc.

4. Ensure that the bonus issue is not made in lieu of dividend.

5. There should be a provision in the articles of association of the company permitting issue of bonus shares; if not, steps should be taken to alter the articles suitably.

6. The share capital as increased by the proposed bonus issue should be well within the authorised capital of the company; if not, necessary steps have to be taken to increase the authorised capital.

7. Fix the date for the Board Meeting for considering the following matters:

— To approve the bonus issue;

— To approve the resolution to be passed at a general meeting;

— To approve requisite resolution for increase of the capital and consequential alteration of the memorandum and the articles (if necessary)

— To decide (or authorise managing director/secretary or some other officer of the company to decide) the dates for fixing a record date.

8. If there are any partly paid-up shares, ensure that these are made fully paidup before the bonus issue is recommended by the Board of directors.

9. The date of the Board Meeting at which the proposal for bonus issue is proposed to be considered should be notified to the Stock Exchange(s) where the company’s shares are listed.

10. Hold the Board Meeting and get the proposal approved by the Board.

11. Intimate the decision taken at the board meeting to the Stock Exchange(s)

12. A company which announces bonus issue after the approval of board of directors and does not require shareholders’ approval for capitalisation of profits or reserves for making bonus issue as per the Articles of Association, shall implement bonus issue within fifteen days from the date of approval of the issue by the board of directors of the company and shall not have the option of changing the decision

However, where the company is required to seek shareholders’ approval for capitalisation of profits or reserves for making bonus issue as per the Articles of Association, the bonus issue shall be implemented within two months from the date of the meeting of the board of directors wherein the decision to announce bonus was taken subject to shareholders’ approval.

13. Arrangements for convening the general meeting should then be made keeping in view the requirements of the Companies Act, with regard to length of notice, explanatory statement etc. Also three copies of the notice should be sent to the Stock Exchange(s) concerned.

14. Approvals of banks, financial institutions, debenture trustees, etc, if required under the related agreements, shall be obtained before the general meeting.

15. Hold the general meeting and get the resolution for issue of bonus shares passed by the members. A copy of the proceedings of the meeting is to be forwarded to the concerned Stock Exchange(s).

16. Within 30 days of the date of the general meeting, file the necessary returns in the prescribed forms e.g. e-Form Nos. 5, 23 to the Registrar of Companies

17. Fix the date for closure of register of members or record date and get the same approved by the Board of directors. Issue a general notice under Section 154 of Companies Act in respect of the fixation of the record date in two newspapers one in English language and other in the language of the region in which the Registered Office of the company is situated.

18. Give 30 days notice to the Stock Exchange(s) concerned before the date of book closure/record date.

19. After the record date process the transfers received and prepare a list of members entitled to bonus shares on the basis of the register of members as updated. This list of allottees is to be approved by the Board or any Committee thereof.

20. File return of allotment with the Registrar of Companies within 30 days of allotment (Section 75 of the Companies Act). Also intimate Stock Exchange(s) concerned regarding the allotments made.

21. Get the share certificates printed, prepared and issued to the allottees as per the provisions of Companies (Issue of Share Certificates) Rules, 1960.

22. Submit an application to the Stock Exchange(s) concerned for listing the bonus shares allotted.