A material quantity variation is the difference between the actual amount of materials used in the manufacturing process and the amount projected to be utilized. The measurement is used to determine the efficiency of a manufacturing process in transforming raw materials into final goods.

A Material Quantity Variance, also known as a Material Usage Variance, arises when a corporation uses a different amount of material for manufacturing than the standard quantity that should have been utilized for production.

If the actual quantity utilized is smaller than the standard quantity, the Material Quantity Variance will be beneficial. In contrast, if the actual quantity utilized exceeds the standard quantity, the Material Quantity Variance will be negative. A corporation may have a Material Quantity Variance for a variety of reasons. It could be due to theft, waste, or material quality discrepancies, among other things.

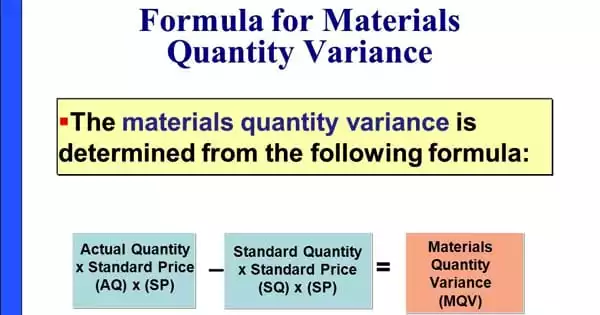

Formula for Material Quantity Variance

The formula for Material Quantity Variance is:

(SQ – AQ) x SP = Material Quantity Variance

Now, let’s do an example to show how to compute Material Quantity Variance.

MUV = (75lbs. – 50 lbs.) x $7 = $175 (F)

The Material Quantity Variance in this example is favorable because the standard quantity is greater than the actual quantity that the company used.

The result would have been adverse had the actual quantity used been greater than the standard quantity.

The material amount variance can produce unexpected results because it is based on a standard unit quantity that may not be even close to actual usage. The engineering department normally determines the material quantity, which is based on the amount of material that should theoretically be used in the manufacturing process, plus a suitable amount of scrap. If the standard is overly lenient, there will be a long run of favorable material quantity deviations, even if the manufacturing team is not doing a particularly outstanding job. A parsimonious standard, on the other hand, leaves minimal space for mistake, increasing the likelihood of a large number of negative variances over time. Thus, the standard used to derive the variance is more likely to cause a favorable or unfavorable variance than any actions taken by the production staff.

Variances can, of course, be produced by production blunders, such as an excessive amount of scrap while setting up a production run, or by damage caused by mistreatment. It can even be caused by the purchasing department ordering materials of abnormally low quality, resulting in more material being scrapped during the manufacturing process.

Example

ABC International expects to use 100 pounds of plastic resin to make a batch of plastic cups, but instead uses 120 pounds. The standard cost of the resin is $5 per pound. Therefore, the material quantity variance is:

(120 pounds actual usage – 100 pounds standard usage) x $5 per pound

= $100 Material quantity variance

Note: In rare circumstances, material quantity variance can be used to measure marketing material usage during sales campaigns, when actual usage is compared to the projected total amount of utilization. This is frequently the case when the expense of marketing materials is relatively expensive.