Procedure of Credit Rating:

A Study on WASO Credit Rating Company BD

WASO Credit Rating Company (BD) Ltd. (“WCRCL”) was incorporated as a public limited company under the Office of the Registrar of Joint Stock Companies and Firms in July of 2009. With the license from the Securities & Exchange Commission (SEC) of Bangladesh to operate as a credit rating company, WCRCL has officially started its journey on 15th February, 2012. It has also been recognized as an External Credit Assessment Institution (ECAI) by Central Bank of Bangladesh in October of 2012.

WCRCL is independent and transparent in its operations and eligible to rate Banks and FIs, PSEs, Insurance, Corporate and Debt Instruments. The WCRCL team is formed with experienced professionals and specialists from different disciplines with the highest levels of ethics and integrity.

WASO Credit Rating Company (BD) Ltd. has executed an agreement for foreign partnership with Financial Intelligence Services Ltd (FISL). Through this partnership with FISL, WCRCL has created bondage with the global resources hub, thus being able to provide the best judged opinion through rating services to the nation.

Financial Intelligence Services Ltd. (FISL) is a Hong Kong based rating wing of World Vest Base (WVB), USA. FISL also operates as a holding company with offices in 16 countries. Since its inception in 1985 in Chicago, USA, World Vest Base (WVB) has become the world‟s leading global provider of financial fundamentals serving the research and analytic needs of thousands of top companies in the financial services, media and corporate markets. The WVB global database is the financial industry‟s premier source of detailed and transparent financial statement data on public companies.

The database universe spans over 50,000 public companies encompassing130 countries from Asia, Africa, Australia, Europe, Latin America and North America. Additionally, WVB provides databases with Insider & Major Shareholders Transactions, specialized End-of-Day pricing for emerging markets, worldwide credit risk and business risk scoring.

WCRCL Services

WASO Credit Rating Company provides many services beside the generic service as a credit rating agency. Some services are

- WCRCL RATINGS

- WCRCL ADVISORY

- WCRCL RESEARCH

WCRCL Ratings:

WCRCL provides different sort of rating services. Some of them are;

- Corporate Ratings

- Bank & FI Ratings

- Structured Finance Ratings

- Insurance Ratings

- State Owned Entities Ratings

- Micro Finance Institution Ratings

- Small & Medium Enterprise Ratings

- Other Organization/s Rating.

WCRCL Advisory:

WCRCL provides different sort of advisory services. Some of them are;

- IRB Implementation

- Enterprise Risk Management

WCRCL Research:

WCRCL provides different sort of research related services. Some of them are;

- Economic Research

- Industry Research

- Specific Research

Objectives of the Study:

The report is going to serve three particular objectives, which are-

- Describe Credit Rating in Bangladesh

- Describe different Rules and Regulations associated with Credit Rating in Bangladesh.

- Describe the procedure and importance of Credit Rating Services in Bangladesh.

Data Sources:

Primary Data:

Primary data were being obtained from different field visits and interviewing different office employees and through working on official documents.

Secondary data:

Secondary data were being obtained from visiting different websites, books, journal, brochures etc.

Literature Review

Credit ratings aim to measure the creditworthiness of an entity, e.g. a corporation, or issue. They represent an opinion of a rating agency that evaluates the fundamental credit strength of an issuer and his ability to fully and punctually meet his debt obligations (Gonzalez, et al., 2004). Credit ratings are produced by professional rating agencies and in most of the countries it requires establishment of regulatory guidelines that permits and monitors the credit rating agencies. For example, in the USA, agencies must be approved as Nationally Recognized Statistical Rating Organizations (NRSRO) by the Securities and Exchange Commission (SEC) (Hill, 2004). In Bangladesh, credit rating agencies has to be approved by Bangladesh Securities and Exchange Commission (BSEC). Subsequently, for the CRAs to rate issues and issuers under the BASEL II guideline has to be approved by Bangladesh Bank (BB) as External Credit Assessment Institution (ECAI). In an economic sense, rating agencies function as financial intermediaries, the existence of which would not be justifiable under the hypothesis of efficient markets (Ramakrishnan & Thakor, 1984).

Ratings are placed on a discrete ordinal scale, where for example under the S&P scale an AAA (the so called `triple A’) rating is the highest credit rating assigned to issuers with the highest credit-quality and a D rating is the lowest rating assigned to bonds or firms in default. Moreover, CRAs stress that ratings are just opinions. These opinions, which stem from fundamental credit analysis, are used to classify credit risk. In keeping with their status as opinions, ratings are determined by a rating committee. As such, ratings do not constitute a recommendation to buy, sell or hold a particular security, and do not address the suitability of an investment for a particular investor (Hilderman, 1999).

Empirical studies on credit ratings can be roughly divided into three lines of research (Blume, Lim, & MacKinlay, 1998). The first two measure the information content of credit ratings in different ways. The first line analyses whether credit ratings measure what they claim to measure, i.e. an issuer‟s creditworthiness. More specifically, the relationship of ratings and corporate default is measured (Zhou, 2001). The second line measures the information content of ratings on capital markets. Here, capital market reactions around rating changes are analyzed to see if ratings contain additional information (Gonzalez, et al., 2004). The third line of research investigates the determinants of credit ratings. Here ratings as independent variables are modeled on a number of financial data (Ederington, 1985), corporate governance characteristics (Bhojraj & Sengupta, 2003), and macroeconomic factors (Amato & Furfine, 2004). These studies show that ratings can be replicated to a certain degree solely using publicly available data. Further studies in this context analyze the stability of credit ratings with respect to their ‘through-thecycle’ approach and the determining factors of rating changes and transition probabilities.

Several academic studies have examined the behavior of credit ratings over time, for instance through the analysis of credit upgrades and downgrades. Altman and Kao (1992) for example analyze the stability of newly issued S&P ratings for two sub-periods (1970 to 1979 and 1980 to 1988). They show that for every rating and time horizon (one to five years) newly-rated issues from the earlier period exhibit greater stability.

Credit Rating in Bangladesh

Credit rating industry in Bangladesh started its journey with the mandatory requirement of having credit rating for all public debt type instruments, right offer issues and shares issued at a premium before the same were offered to the public. In the year of 2002, Credit Rating Information & Service Limited (CRISL) started its operation as the first registered credit rating agency of Bangladesh. The second rating agency, Credit Rating Agency of Bangladesh Limited (CRAB) went to operation on 2004.

Credit Risk Grading Manual of Bangladesh Bank was circulated by Bangladesh Bank vide BRPD Circular No. 18 dated December 11, 2005 on Implementation of Credit Risk Grading Manual which is primarily in use for assessing the credit risk grading before a bank lend to its borrowing clients. By that time CRISL rating reports were appearing to be very useful for the users; specially CRISL rating report on the then Al Baraka Bank convinced the Bangladesh Bank of the need of credit rating and it took the initiative to make mandatory for all banks to have credit rating before it goes for public offering. The banking regulator further decided to make it mandatory for all banks to submit credit rating reports to the regulator within six months after the finalization of accounts.

Following the example of the central bank, the insurance regulator also came up with the requirement to make rating mandatory for all general insurance companies every year and for the life insurance companies bi-annually. The Dhaka Stock Exchange, while issuing the direct listing regulations, made the credit rating mandatory before a company apply for direct listing. The above regulations created an enabling environment for credit rating in the country‟s capital and financial markets. The concept of client rating by the rating agencies to support capital adequacy of the banks came up in view of the need for implementation of Basel II capital adequacy framework by Bangladesh Bank.

Bangladesh Security and Exchange Commission (BSEC) allow only a mere 2% default rate of the credit rating agencies. There are certain penalties in case default rate of more than 2% including cancellation of license of the defaulter rating agency as the highest penalty by BSEC.

Other credit rating companies namely National Credit Ratings Ltd and Emerging Credit Rating Ltd started their journey on 2010. Lastly, new four credit rating companies have come to operation on 2012, which are ARGUS Credit Rating Services Ltd., Alpha Credit Rating Limited,

The Bangladesh Rating Agency Limited and WASO Credit Rating Company (BD) Limited. A list of credit rating companies operating in Bangladesh can be found in the following table. According to Association of Credit Rating Agencies of Asia, Bangladesh has the highest number of credit rating companies. India, one of the largest economies of Asia has only two credit rating companies. On the other hand China, another largest economy is continuing its economic growth with a single credit rating company.

Below are the Names and Dates of issuance of Registration Certificates of CRAs‟ in Bangladesh

Table: List of CRAs

Overview of Credit Rating Agencies in Bangladesh

CRISL

Credit Rating Information and Services Limited is a company that started its journey to implement a Concept in Bangladesh – “Credit Rating”. Before CRISL, “Credit Rating” was text paper words for the teachers and students of Bangladesh. The voyage of how CRISL conceptualized this idea in 1995 and implemented it in Bangladesh and finally achieved its operating license in 2002 – after almost eight years of struggle – has a long, interesting, exciting and also painful history. CRISL is now the national flagship company representing the profession at home and abroad.

CRAB

Credit Rating Agency of Bangladesh Ltd. (CRAB) was incorporated as a public limited company under the Registrar of Joint Stock Companies in August 2003 and received its certificate for commencement of business in November 2003. It has been granted license by the Securities & Exchange Commission (SEC) of Bangladesh for operating as a credit rating company in February 2004. The formal launching of the company was held on 5 April 2004.

NCRL

National Credit Ratings Limited (NCR) is a full service rating company that offers a wide range of services. Incorporated as a public company, NCR started its business with a paid up capital of TK 10.00 million. The Securities and Exchange Commission granted the license to NCR in June 2010 under the Credit Rating Companies Rules 1996.The Company is recognized by the Bangladesh Bank as an External Credit Assessment Institution (ECAI).

ECRL

The ISLQ International Star for Leadership in Quality Award acknowledges the strong commitment to quality and excellence. Mr. Ahsan Parvez (Managing Director& CEO) & Mr. Noor-e-Khoda Abdul Mobin (Deputy Managing Director & COO) received the award in the Concorde La Fayette Hotel in Paris on June 25, 2012, from the president of B.I.D., Mr. Jose E. Prieto. Emerging Credit Rating Ltd. is made up of a team oriented towards the continuous improvement of processes, striving for an important role in the leadership of the business world.

ACRSL

ARGUS Credit Rating Services Ltd. (ACRSL) is the next-generation Credit Rating Agency of Bangladesh. Founded as a joint-venture between global experts in credit & equity research and local sponsors with strong capital markets track record, ACRSL received its license from the BSEC in 2011. ACRSL is partnered with DP Information Group (“DP”), the premier credit rating agency of Singapore for over 30 years. Having pioneered credit rating in Singapore, DP has played an influential role in the development of the credit rating sector in China, Indonesia, and Philippines. Further, DP‟s parent company, the UK based Experian Group is one of the world‟s top credit reference agencies.

WCRCL

WASO Credit Rating Company (BD) Ltd. (“WCRCL”) was incorporated as a public limited company under the Office of the Registrar of Joint Stock Companies and Firms in July of 2009. With the license from the Bangladesh Securities & Exchange Commission (BSEC) of Bangladesh to operate as a credit rating company, WCRCL has officially started its journey on 15th February, 2012. It has also been recognized as an External Credit Assessment Institution (ECAI) by Central Bank of Bangladesh in October of 2012.

ALPHA

Alpha Rating was incorporated on the 24th of February 2011. a result of the initiative of a few distinguished and renowned professionals of Bangladesh and the with support and organizational assistance from SATCOM IT Ltd., Axis Resources Ltd., Equity Care Bangladesh Ltd., and TAN Equity and Investment Ltd. Date of Issuance of Registration Certificate is 20th February 2012.

BDRAL

The Bangladesh Rating Agency Ltd (BDRAL), a subsidiary of Dun & Bradstreet South Asia Middle East Ltd., is the pioneer in rating the SME sectors in Bangladesh. BDRAL has launched its SME ratings in Bangladesh following a successful pilot phase carried out in the year 2009.Date of Issuance of Registration Certificate is 7th March 2012.

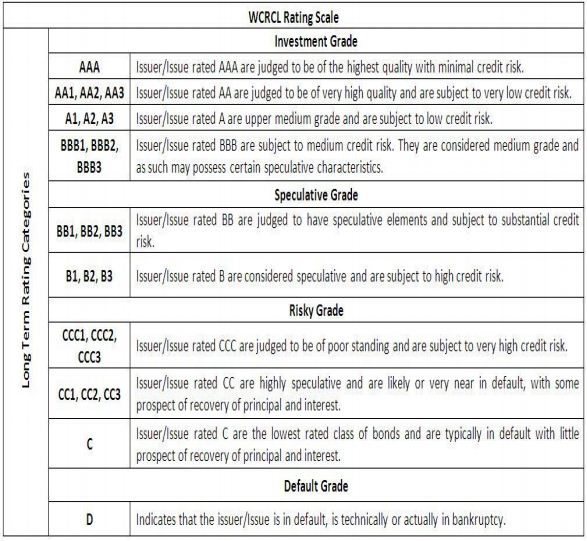

WASO Rating Scales and Definitions

Rating Symbol:

WASO credit rating is an opinion of credit quality of an individual obligation or of issuer‟s general creditworthiness. To express the opinion, WASO uses generic rating symbol to describe the status of the respective issue or issuer profile. Additionally, it also uses some auxiliary signal about credit risk through the use of Rating Outlook and Rating watch list designation.

Unless otherwise indicated within the definition, all rating systems are monitored through surveillance. Rating may also be withdrawn for various reasons. The Rating Committee is in full discretion to assign any rating.

Scope of Rating Definitions:

The definitions in this handbook are not intended to provide a detailed view of how ratings are determined. WASO publishes rating methodology for the respective sector and these are designed to describe the factors underpinning the WASO‟s rating opinion. We encourage reader to review the respective rating methodology.

General Credit Rating Symbol and Definitions:

Issuer Ratings:

Issuer Ratings are opinions of the abilities of entities to honor senior unsecured financial obligations and contacts. WASO expresses issuer ratings on its General short term and long term scales.

Issuer Rating: Long Term

Other Rating Symbols

- Provisional Ratings (P)

WASO will assign a provisional rating when the assignment of a final rating is subject to the fulfillment of contingencies but it is highly likely that the rating will become definitive after all documents are received or an obligation is issued in the market. A provisional rating is denoted by placing a (P) in front of the rating. Such ratings are typically assigned to transaction based structures like bond, debentures that require investor education before investment decision.

When a transaction uses a well established structure and transaction‟s structure and terms are not expected to change prior to sale in a manner that would affect the rating. A definitive rating may be assigned directly.

- Withdrawn (WR).

When WASO no longer rates an obligation on which it previously maintained a rating.

- Not Rated

NR is assigned to an unrated issuer or issue.

WASO Rating Framework

The factors considered by WASO Ratings are divided into six categories:

Promoters

- Industry house

- Group companies (market price)

- Group companies (EPS)

- Existing company (market price)

- Group companies(EPS)

- Auditors qualifications

- Experience

- Qualifications

- AGE

Project

- Product technology

- Collaboration

- Gestation

- Location

- Utilities

- Labor

- Cost of project

- Cost of finance

- Institutional appraisal

- Other similar project

Prospects

- Consumer

- Present market size

- Future market size

- Competitors

- Marketing arrangements

- Technology obsolescence

- Future projects

Government Policy

- Price control/subsidy import

- Taxation Government attitude

- Import (OGL, etc.)

- Government Attitude

Security Characteristics

- CCI consent

- Secured/unsecured

- Interest

- Capital appreciation

- Dividend

- Premium

- Size of issue

- Tax benefits

- Liquidity

Miscellaneous

WASO Ratings assigns a maximum of 100 points, distributed among the characteristics mentioned above. Since there are about 40 sub criteria, the total of 100 points is divided among the sub- criteria at about 2.5 points per sub criterion. As a result no sub criteria are given undue weight. Though all the criteria used for evaluation are spelt out, the way in which the criteria are weighted and combined to form a final score is not explicitly specified.

Importance of Credit Rating in Bangladesh

The motives act behind the entities‟ paying fees to secure a credit rating depends on the surrounding regulatory environment and form of financial market. There are several reasons of getting a rating. The reasons are different in different markets and economies. The motives of getting a rating in Bangladesh are not identical as USA or UK. As same, the motives of

American entities are not same as those of European or Australian entities. However, there are some common reasons for which the entities all over the world are spending money to get rating from the rating agencies. The identical reasons are enumerated here within the context of Bangladesh:

To Build up Market Reputation

New companies that seek to build a reputation in the international financial markets demand credit ratings to increase the exposure of their brand name. This brand exposure is important when companies for example initiate foreign direct investments. An entity with a higher rating is considered as a reputable organization. Recently, Delta BRAC Housing (DBH) has been awarded as an “AAA” rated company of the country, which excels the company‟s reputation that was reflected through the share price the company at DSE and CSE.

For Lower Cost of Funding

A less known company can lower their cost of borrowing if they obtain a higher investment grade rating. Banks or financial institutions consider rating as an indication of an entity‟s performance measurement yardstick. Entities with a higher rating are sanctioned loan at a lower interest rate whereas a lower graded entity is charged at a higher interest rate. So, it is going to be a common practice of the country to require an entity to be rated itself before applying for a loan to the banks or financial institutions.

Better Market Access

Any company that wishes to enter capital markets and issue debt in capital market is obliged to obtain a credit rating. Rating conveys the entity‟s ability and willingness to the market participants regarding repayment of its borrowed money or equity capital. In Bangladesh, as per Credit Rating Companies Rules 1996, all the companies are required to be rated before issuing its debt or floating its equity share at premium in the market.

To Comply with Regulatory Requirement

All over the world entities are rated for the regulatory bindings by the Securities and Exchange Commission and other authorities. In Bangladesh, BSEC, Bangladesh Bank and Department of

Insurance are the three regulators who issued regulations, circulars and notifications for the entities for rating. Our banks and insurances are now rated once in a year for these requirements of the regulatory authorities.

Limitations of Credit Rating

The biggest limitation of rating agencies across the world has often been accused of not being able to predict future problems. In part, the problem lies in the rating process itself, which relies heavily on past numerical data and standard ratios with relatively lower usage of judgment and understanding of the underlying business or the country economics. Data does not always capture all aspects of the situation especially in the complex financial world of today. An excellent example of it is the meaningless over reliance on numbers in the poor country rating given to Bangladesh.

In general, rating is a very good estimate of the actual creditworthiness of the company; however, it is not able to predict extreme situation, which are unlikely to have been predicted by most investors in any cases, investors should realize that a credit rating is not sacrosanct and that one has to do one‟s own due diligence and investigation before investing in any instrument.

They should use the rating as a reference and a base point for their own effort. One good way of doing this is examine the behavior of the stock price in case the stock is listed. As a collective, the market is far smarter at predicting problems than any credit rating agency. Witness the sharp erosion in stock price of companies much before their credit ratings were downgraded.

SWOT Analysis of WCRCL

Strengths of WCRCL

WCRCL has many points of strengths which they should capitalize on. Some of them are

- They have a great Board of Directors.

- Renowned Rating Committee members.

- Excellent analyst team comprising experienced and youth professionals.

- Great partnership with a few banks.

- It holds an image that, WCRCL provides nothing but fair grades.

Weaknesses of WCRCL

WCRCL has many points of weaknesses which they need to work on. Some of them are

- Very high turnover rate in marketing and administration department.

- Lack of proper facilities within the office for employees.

- Human Resource Department is highly inexperienced and often selects wrong individual for different positions.

- Often they are unable to clear employee dues timely which impact in decreasing performance of the concerned employees.

Opportunities of WCRCL

WCRCL has many scopes or opportunities in Bangladeshi Market, which they can capitalize on. Some of them are;

- Market is growing

- People are more aware of Credit Rating and the rate in increasing

- It is becoming a tool to differentiate a company from others in the similar sector.

Threats of WCRCL

WCRCL has a few threats they should be prepared for. Some of them are

- This sector has already turned into a red sea with 8 companies.

- Politically issued licenses can be terminated by regulators if government changes.

Recommendations:

Based on above discussions, I would like to suggest the following to and for WASO Credit Rating Company (BD) Ltd.

- WCRCL should try and establish branches outside Dhaka to increase market size.

- WCRCL should increase employee training and other monetary facilities.

- WCRCL should pressurize to establish a separate body for monitoring credit rating agencies.

- Government should provide clear and written “Code of Conduct” for the credit rating agencies.

- WCRCL should try to reattempt to form an association to stop unfair pricing.

- WCRCL can buy out or form joint venture with any other CRA who is/are facing a hard time.

Conclusion:

Our beautiful Bangladesh is not a very good example on how a Credit Rating Agency/s should operate. We have now 8 agencies where two largest countries of the world India and China has 3 combined. This definitely has increased price war and reduced quality in consequence. Still among the new generation of Credit Rating Agencies, WASO Credit Rating Company (BD) Ltd is still fighting hard with dignity. Hopefully it would be able to convince the regulators to take necessary actions so that the agencies can operate with integrity and honesty.

At this moment, Bangladeshi financial sector is facing a very tough time. CRAs‟ are also sufferers of it. As the government has issued licenses, it should be their responsibility to safeguard these companies at tough times and in return these companies should operate for the sake of the common people of Bangladesh.