INTRODUCTION

Lavela Textile Ltd. is a 100% export-oriented Basic Sweater manufacturing unit at Kutoria, Ashulia, Savar, Dhaka. At present the management of the Company has decided to go for manufacturing production capacity by adding modern Pre-fabricating building & modern machinery. The plant will be equipped with most modern and sophisticated Machinery and equipment to be imported from reputed manufactures/suppliers at competitive price, which will be run by highly trained and skilled manpower. The factory will be self-sufficient, continuous trouble free operation and timely delivery.

The Chairman and the Managing Director of the Company have dynamic leadership in business sector and have sufficient means and wealth in the country to provide equity of the proposed project. So, the proposal for sanctioning loan from Bank may be accepted to all concerned authorities with great pleasure.

01. | Name of the Project | : | LAVELA TEX LTD. |

02. | Address of Factory & Head Office | : | Kutoria, Ashulia, Savar, Dhaka. |

: | 55, Suhrawardi Avenue, GrandPlaza, (3rd Floor), Apt # E-3, Baridhara, Dhaka-1212. | ||

03. | Managing Director | : | Mr. A.K.M. Sanaul Haque |

04. | Total Fixed Cost of the Project | : | Tk. 314.49 Lac |

05. | Term Loan | : | Tk. 204.42 Lac |

06. | Equity | : | Tk. 110.07 Lac |

07. | Proposed Working Capital | : | Tk. 30.00 Lac |

07. | Debt Equity Ratio for BMRE | : | 35 : 65 |

08. | Production Capacity (Annual at 100% Capacity) | : | |

Item |

| Quantity (After BMRE) | |

| Basic Sweater |

| 25,000 Doz. |

09. Financial Projection :

| Expected Capacity Utilization | 60% at 1st year | 70% at 2nd year | 75% at 3rd year |

| Sales Revenue | 89812 | 104781 | 112266 |

| Gross Profit | 21615 | 26839 | 29088 |

| Operating Profit | 14503 | 18729 | 29088 |

| Net Profit Before investment | 8659 | 11827 | 12633 |

| Debt Service Coverage Ratio (in times) | 3.57 | 3.36 | 3.57 |

| Internal Rate of Return (IRR) | 32% (aprox.) | ||

| BEP Analysis SalesSales Capacity Utilization | Tk. 412.68 Lac 28% | ||

| Employment Generation | 500 Persons | ||

| Fixed Cost Employed per job creation | Tk. 101450 | ||

Management and Organization

1.01 The proposed project envisages setting up of a 100% export oriented Basic Sweater manufacturing unit at Kutoria, Ashulia, Savar, Dhaka. A profile of this effect has been prepared about the project design covering in details of its probable cost, profitability and other relevant aspects. The sponsors have gathered sufficient experience in this line of products and they are qualified. Besides this, qualified and experience personnel will be recruited for production managerial & administrative purpose and thus it will be helpful for management of the project.

1.02 BOARD OF DIRECTORS:

The following 03 (Three) persons are the first director of the Company;

Sl. No. | Name & Address of the Director | Status in the Management | Share Holding |

1. | A.K.M. Sanaul HaqueS/O, MD. Shamsul Haque Mother- Late Zebunnesa Begum House # 38, Rod # 104, Apt # B-2, Gulshan-2, Dhaka.

| Chairman & Managing Director | 24,000 |

2. | Mohiuddin AhmedS/O, Late Mujubuddin Ahmed Mother-Fatema Ahmed 211/B, Khilgaon Chowdhury Para, Dhaka-1219

| Director | 3,000 |

3. | Kazi Abu JafarS/O, Kazi Abdul Halim Mother-Mrs. Amirunnessa 211/B, Khilgaon Chowdhury Para, Dhaka-1219.

| Director | 3,000 |

Among the above Mr. A.K.M. Sanaul Haque is the Chiarman & Managing Director of the Company and will hold this post five years after incorporation of the Company. The Managing Director is entitled to such remuneration as may be determined by the Board of Directors in the general meeting for any extra services.

1.03 CORPORATE SET UP:

The sponsors already formed a private limited Company that is registered with registrar of Joint Stock Companies & Firms. The authorized capital of the Company is Tk. 1.00 Crore and paid up capital is Tk. 30.00 Lac.

1.04 MANAGEMENT OF THE COMPANY:

The overall management of the Company will be vested with the Board of Directors of the Company. The Board will formulate Company’s Policies and provide guidelines for its day to day business operation. The Managing Director is the Chief executive to look after the business affairs and other logistic support of the Company. The Managing Director will be assisted by the other Directors as well as by the Managerial and Technical Staff at different levels. The Organization Chart of the proposed Company is given below;

2.01 PROJECT PURPOSE AND DESIGN:

The proposed project envisages setting up of a 100% export-oriented Basic Sweater manufacturing unit at Kutoria, Ashulia, Savar, Dhaka. The building will be made by pre-fabricated steel and imported modern machinery. The technology involved in manufacturing Basic Sweater is not so complicated. The implementation of the project is expected to completed & go into commercial operation after sanctioning of loan & completion of the steel building.

2.02 PRODUCT-MIX & PRODUCTION CAPACITY:

The annual rated capacity of the project based on single shift operation of 8 (eight) hours per day and 300 working days in a year will be as under. The estimated attainable capacity of the project will be 60% in the 1st year, 70% on the 2nd year, 75% in the 3rd year and onward respectively.

| Item | Quantity at 100% Capacity (After BMRE) |

| Basic Sweaters | 25,000 Dozens |

The product mix is flexible and it will be determined as per profitability and market demand. The unit will have capacity to produce a few amount of total demand of the world.

2.03 RAW MATERIALS:

The required raw Materials to produce above product will be imported under back to back L/C using bonded warehouse facilities against irrevocable and confirmed export L/C to be opened by required raw materials.

2.04 TECHNOLOGY AND MANUFACTURING PROCESS:

The technology involved manufacturing basic sweater already available in the country. Besides arrangement will be made for training of operation under highly skilled technical personnel which will be available.

2.05 LAND & LOCATION:

The project has been proposed to be set up at Kutoria, Ashulia, Savar, Dhaka at rental premises. The project will cover and area of 1.35 Bigha developed land with all infrastructure facilities like power, gas, water and man-power. The selected land is suitable sufficient for the project.

2.06 BUILDING AND CIVIL CONSTRUCTION:

The proposed industry will be constructed out of prefabricated structure from local source and covered area of 20,000 sft.

The proposed building comprises factory building raw material & finished goods godown, administrative office, toilet, safety tank, overhead tank, sanitation, electrification, surface drain, compound wall, main gate and internal road etc. For this a cost has initially be assumed at Tk. 314.49 Lacs.

2.07 MACHINERY AND EQUIPMENTS:

A) Imported :

The project will be equipped with Brand New, most modern & sophisticated, complete and balanced machinery together with all auxiliaries and equipment. The main machinery for the project will be imported from the reputed manufacture of Japan/China/Taiwan/ U.K. and U.S.A.

For the selection of proposed machinery quotation form different local indenters have been procured on the basis of performance considering versatility, durability, cost benefit and improved operational performance of machinery. Total C & F cost of imported machinery, spares and accessories stand at US $ 11291. Details of imported machinery are attached with this profile.

2.08 ERECTION & INSTALLATION OF BUILDING:

Erection & Installation of main machinery will be done by Foreign technical personnel under the direct supervision of experts/Engineers form Supplier of foreign machinery. Agreements will be made by the sponsors with suppliers in this regard. Local machinery will be installed by local technical expert with joint collaboration of Foreign expert. The loading, fooding, local transportation, pocket money, two way air ticket for foreign technical personnel will provide by the buyer. Cost for the purpose has been estimated at Tk. 3.00 Lacs only.

2.09 UTILITIES:

Power:

The connected load of the project will be 60 KW and the maximum demand will be around 50 KW. The power will be available from local PDB/REB source. An amount of Tk. 1,00,000/- has been estimated for required security deposit for power.

The annual cost for electricity consumption stand at Tk. 50X8X300X3.10X10%=Tk. 4.09 Lac.

It is mention that the projects will have 01 Nos. of Diesel generating set of 150 KVA for smooth and trouble free operation of the project.

b. Water:

Water will be required for processing of sweater and domestic. The daily requirement of Water has been estimated at about 2000 gallon. The required water will be available from overhead water tank, Underground water reservoir and Deep-Tube-Well.

c. Stores and Spares:

Store and spares for the 1st year will be supplied during procurement of machinery. The cost of 2nd and 3rd year of operation & onward has been considered at the rate of 1% and 1.5% cost of the machinery.

d. Repair & Maintenance

For machinery this cost has been considered @ 1%, 1.5% and 2% for 1st, 2nd and 3rd and onward respectively.

Erection, Installation, Commissioning, Trial and commercial production will be carried out by the Erectors deputed by the supplier of foreign machinery at their own cost. Production and quality control will be supervised by them.

f. Man Power:

The requirement of technical, managerial personnel and labor with their salaries wages is given below. The following personnel have to be recruited for single shift operation of 8 hours each per day.

Administration:

Sl. No. | Name of the Post | No. of Post | Monthly Salary | Total Tk. In “000” |

1 | General Manager | 01 | 25,000/- | 300 |

2 | Manager (Admin) | 01 | 15,000/- | 180 |

3 | Accounts Officer | 01 | 15,000/- | 180 |

4 | Asstt. Accountant | 02 | 6,000/- | 144 |

5 | Senior Executive | 03 | 6,000/- | 216 |

6 | Clerk/Typist/Computer Operator | 03 | 4,000/- | 144 |

7 | Driver | 01 | 6,000/- | 72 |

8 | Security Officer | 01 | 6,000/- | 72 |

9 | Peon/Guard | 11 | 3,000/- | 396 |

10 | Cleaner | 03 | 3,000/- | 108 |

| Total | 27 |

| 1812 |

Technical:

Sl. No. | Name of the Post | No. of Post | Monthly Salary | Total Tk. In “000” |

| Factory Manager | 01 | 25,000/- | 300 | |

| Asstt. Factory Manager | 02 | 15,000/- | 360 | |

| Supervisor | 10 | 15,000/- | 1800 | |

| Skilled Worker | 320 | 6,000/- | 23040 | |

| Semi-skilled worker | 70 | 6,000/- | 5040 | |

| Un-skilled Worker | 70 | 4,000/- | 3360 | |

| Total | 473 |

| 33,900 |

Above personnel will be allowed annual increment @5% on basic pay and equivalent 2 months basic pay as bonus. High incentive may be allowed for stillness of the workers.

2.10 OTHER FIXED COST:

Furniture:

The project will require internal decoration furniture & fixture, computer, photocopier, fax, printer etc. For which an amount of Tk. 13,82,000.00 has been estimated.

Safety Provision:

The plant will be adequately equipped, with safety provision like fire fighting equipments, first aid medical etc. cost has been estimated at Tk. 3,00,000/- for the purpose.

Preliminary & Pre-operating Expenses:

An amount of Tk. 1,50,000/- has been estimated for Company formation, registration, appraisal, design, drawing, consultancy, traveling expenses for machinery selection and Tk. 1,50,000/- for pre-operating expenses. Test run Expenses estimated for Tk. 2.00 lacs.

Transportation:

The project will required a Reconditioned Micro Bus for carrying of Raw Materials and Finished goods. Cost of Tk. 16.00 lacs have been estimated for the purpose.

2.11 Pollution and Disposal:

The project will not pose any pollution and waste disposal problem. Necessary permission should be obtained from the environment pollution bureau before commercial production of the project.

2.12 Construction Schedule:

It is expected that the project will go into normal operation within 03 months from the date of opening L/C for imported machinery. The sponsors of the project has got sufficient practical experience in export business and they earned good reputation in international market. The project will be set up with Brand New Most Modern and sophisticated machinery and equipment manufactured by developed countries. The project will have own power generator for meeting continuous demand of power. So, proper and timely shipment will be possible for the unit.

2.13 THE PROJECT IMPLEMENTATION SCHEDULE

It is expected that the proposed project will completed and go in to commercial operation within a four month the date of placement of order of imported machinery.

THE PROJECT IMPLEMENTATION SCHEDULE

Month | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

| Loan Sanction | X | |||||||||||

| Documentation | X | |||||||||||

| Civil works started | X | |||||||||||

| L/C opening for Machinery | X | X | ||||||||||

| Civil Works Completed | X | |||||||||||

| Machinery received | X | |||||||||||

| Installation | X | |||||||||||

| Trial Production | X | |||||||||||

| Trial Production | X | |||||||||||

| Commercial Production | X |

DEMAND ANALYSIS:

3.1 The demand of exportable ready-made sweater of Bangladesh is dependent on the World market demand. It is quite difficult to estimate the world market demand for basic sweater, which is increasing for diversifying with chances of fashion and choice of users. However, ready-made garments now emerge as the number one sector of export earning of Bangladesh. During 1990-91 its contribution was US$ 431 million to the total export earning of US$ 1,718 million. Today Bangladesh exports more than 100 categories of garments to about 50 countries, of which 10 countries namely U.S.A, Germany, France, U.K., Italy, Netherlands, Canada, Sweden, Belgium and Norway together account for about 98% of destination.

3.2 Starting from 198 with a small number of unit technical collaboration of South Korea, the number of apparel manufacturing units increased manifold with Ina decade. Bangladesh has now become an established source of apparels supplier to most of the developed nations supported by over 2300 manufacturing units. Over the years, Bangladesh has emerged as major supplier of ready-made garments to 3 very important markets and on quantity basis, she has been the 8th largest exporter to U.S.A., 9th to Canada and 10th to EEC. The U.S.A. customs report of March 31, 1992 reveals that Bangladesh were the 4th largest exporters to U.S.A. in that particular month. The rapid growth in the sector within this shortest span of time has been possible mainly due to the dynamism of the entrepreneurs and significant diversification of the product base and markets which in recent years, resulted in penetration Bangladesh into European market in a substantial way. As part of further market diversification, efforts are underway to market Bangladeshi garments to Japan, Australia, Middle East and the newly created commonwealth of Independent states (Former USSR).

REASONS FOR INCREASING DEMAND:

3.3 The demand for Bangladesh-origin ready-made garments/Sweater are increasing mainly due to following facts:

a) Cheaper source of labor;

b) Cheaper infra-structural facilities;

c) Generalized system of preference (GSP) availed by Bangladesh exporters for export to Australia, EEC and other countries and as such tax remission in enjoyed by the importers of such countries; and

d) Development of appropriates Sweater technology to caster the international market demand.

3.4 The following fiscal measures of the Government of Bangladesh have also encouraged local and foreign investors in establishing more export-oriented ready-made garments industries in the country.

a) Confessional rate of duty in import of capital machinery @ 2.5% on C&F cost, for setting up new export-oriented industries.

b) Introduction of back to back L/C facility and bonded warehouse system towards reducing the cost of working capital;

c)Tax holiday benefit of 10 years for newly set-up export-oriented industries;

d) Confessional rate of interest on the packing credit/export credit; and

e)Export performance benefit (XPB) to the exporters or ready-made garments (of course, the facility does not significantly help the exporter any more as the little difference between bank and outside dollar rate has made such benefit of no physical gain in recent month.

QUOTA SYSTEM:

3.5 All typse and varieties of ready-made garments do not have free entry to every importing country. U.S.A. and Canada have imposed quota systems on export of the items of ready-made garments from Bangladesh.

3.6 The product of the proposed is a non-quota item for EECX and other major importing countries except U.S.A., which has imposed quota only on Acrylic wool knitted sweaters. However, a quick market survey indicates that Bangladesh with it’s current limited production capacity can not meet quota allocated to her implying scope for further expansion of this specialized item. Generalized Systems of preference (GSP) can be availed by Bangladeshi sweater exporters for EEC countries and as such entry the importers of such countries enjoy tax remission.

PROJECTION OF SUPPLY GAP:

3.7 It is difficult to project the supply gap of individual item, particularly basic knitted sweater, in the international market. However, a projection of export earning from the ready-made garments sector can be made on the basis of actual earnings sector can be made on the basis of actual earnings during the past years. The table shows the export earning during 1987 to 1995 period.

EXPORT EARNING DURING 1987-95

Financial Year | Export Earnings Value in Million Taka | % Increase/Decrease |

1987-88 | 12,881 | — |

1988-89 | 13,780 | 7 |

1989-90 | 19,492 | 41 |

1990-91 | 28,120 | 44 |

1991-92 | 34,590 | 23 |

1992-93 | 42,546 | 23 |

1993-94 | 52,331 | 18 |

1994-95 | 64,337 | 23 |

Source: Export Promotion Bureau of Bangladesh.

EXPORT POTENTIALLY OF KNITTED SWEATER:

3.8 For more than 10 years Bangladesh is exporting different types and ready-made garments to European, Canadian and U.S.A. markets. The quantity is increasing every year sweater is a specialized item which may be considered as a diversification approach to traditional garments line. Major quantity of orders for knitted sweater in Bangladesh come from UK, Germany, France, Norway, Sweden and USA. The other European countries who also buy considerable quantity are Holland, Belgium and Italy. But to rise in cost of labor and other infrastructural facilities in other South Asian countries like South Korea, Hong Kong, Taiwan etc. the demand for Bangladesh origin ready-made garments is increasing further. As such, more industries are being set-up in this sector which will increase earning of valuable foreign exchange of the country.

3.9 Different types and varieties of knitted Acrylic yarn/woolen sweaters are being exported to the world market for quite sometime by Bangladesh exporters. Like other garments items, the demand for sweaters is increasing every year and as such, the small number of existing units remains booked throughout the year. Most of the existing units are advance booked by continuous inflow of orders.

3.10 The local built-up capacities are greatly inadequate to meet the increased quantum of orders that keep on pouting in this particular category of knitted Acrylic yarn (woolen) products. This trend obviously indicates the underlying potentiality and prospect for establishment of more number of units in this specialized sub sector of the country.

3.11 Performance of Existing Units:

Although there are more than 2200 export-oriented ready-made garments industries in the country. Most of these units are recently established, running at full capacity and all of them are fully booked up to 2000-2001. For the last few years, they have been supplying knitted sweaters to USA, UK, Canada, Holland, Belgium, Denmark, Norway, Sweden and France with full satisfaction.

EXPORT EARNING FROM SWEATER INDUSTRY DURING 1995-1999

YEAR | EXPORT EARNING VALUE IN MILLION US$ |

2000-2001 | 403.92 |

2001-2002 | 393.93 |

2002-2003 | 446.58 |

2003-2004 | 534.60 |

Source: Bangladesh Garments Manufacturers and Exporters Association (BGMEA)

MARKETING AND SELLING ARRANGEMENT

3.12 The sponsors will arrange direct orders from foreign buyers or their representative at Dhaka. Besides, attempts would be made to produce export orders through different Buying Houses operating in Bangladesh. The number of Buying House presently operating in Bangladesh is about 300.

3.13 The sponsor of the project has got sufficient experience in export business and they earned good reputation in international market. The project will be set up with Brand New, Most Modern and Sophisticated Machinery and Equipment manufactured by developed countries. The project will have own Power Generator set for meeting continuous demand of power. So, proper and timely shipment will be possible for the unit.

4.01 Project Cost:

The estimated cost of the project and total cost of the project and means of finance as stated below;

COST OF THE PROJECT:

(Tk. In “000”)

SL. No. | Particulars | Cost to Incur | ||

F/C | L/C | Total | ||

1 | Land | – | – | – |

2 | Building & Civil Works | – | 14,692 | 14,692 |

3 | Machinery & Equipments | 8,711 | – | 8,711 |

4 | Clearing & Forwarding, L/C Commission, Port Charge, Duty & Surcharge and Internal Freight @ 9% on M/C | – | 784 | 784 |

5 | Local Machinery | – | 1,556 | 1,556 |

6 | Erection & Installation | – | 300 | 300 |

7 | Contingency | – | 800 | 800 |

8 | Furniture & Fixture | – | 1,382 | 1,382 |

9 | Vehicles | – | 1,600 | 1,600 |

10 | Preliminary & Pre-operating expenses | – | 500 | 500 |

11 | Interest During Construction period | – | 1,124 | 1,124 |

| Total Cost of the Project | 8,711 | 22,738 | 31,449 |

The total cost of the project has been estimated at Tk. 314.49 Lac. The details of the cost estimated showing break-up under different heads have been seen at annexure 1 to 15 enclosed. The summarized project is presented above.

4.02 Means of Finance

The above estimated cost of the project is proposed to be financed as under;

(Tk. in “000”)

Means of Finance ( Fixed Cost) | Amount (Tk.) |

| Term Loan | 204.42 |

| Equity: | |

| Sponsors own contribution | 110.07 |

| Total | 314.49 |

4.03 Debt Equity Ratio for Term Loan is 35:65 (Based on Fixed Cost).

4.04 The implementations of the project will involve a capital outlay of Tk. 314.49 Lac that the promoter’s participation in equity has been estimated of Tk. 110.07.

4.05 Financial Evaluation:

Cost of production and profitability:

a) Profitability potential of the project has been computed for 3 (three) projected years of operation to assess the financial viability of the project. Statement showing the forecast of earning which inter-alia includes sales estimates, cost of goods sold, general, administrative and selling expenses and financial expenses are presented in Annexure enclosed.

b) Period of Term Loan has been considered for 12 (seven) years that includes grace period of 12 months.

c) Repayment of Term Loan has been considered by 44 quarterly installments.

Assumptions underlying the earning forecast:

The main assumptions for the financial projection are as under;

i) The project will operate for 300 working days in a year on single shift operation basis of 8 hours per day.

ii) Capacity build-up has been assumed at 60%, 70% and 75% in the 1st, 2nd an 3rd years and onwards respectively.

iii) Constant prices have been used for both input and out put for the entire projection period. This has been done on the assumption that any increase/decrease in input prices will be offset by a corresponding increase/decrease in output prices.

iv) Depreciation/amortization has been charged on straight line method at the following rates:

Building @5%

- Machinery @10%

- Other Assets@20%

v) Economic life of the project has been assumed to be 10 years without any major BMRE.

4.06 Break Even Analysis:

The break even analysis has been carried out on the basis of cost and sales date of 3rd year of operation and is shown in Annexure-11. The project is expected to break even (Sales) at 28% at a sales value of Tk. 1122.49 Lac.

4.07 Internal Rate of Return:

The Internal Rate of Return computed following discounted cash flow technique works out to 32%.

4.08 Cash Flow Statement:

The Cash Flow Statement based on profitability estimate has been worked out. The project is expected to have comfortable cash position that will enable the unit to repay the bank dues in time. Details are shown in Annexure-13.

4.09 Balance Sheet:

Balance Sheet is prepared to show the financial position of the project. Details are shown in Annexure-15.

4.10 Conclusion :

The total cost after setting up of the project is estimated at Tk. 314.49 Lac The project will create job opportunities for 500 persons.

It reveals from the financial analysis that the project will be a profitable concern. The profitability ratios are satisfactory and the project will be sufficiently liquid to pay all its liabilities. The break-even analysis shows sound position and survivability of the project in sensitive market situation. The project if capable to afford a maximum cost of capital of 32% as indicated by Internal Rate of Return (IRR). The project will be contributive to National Economy. In view of the above facts it is found that the project is Technically sound, Financially and Economically Viable. So, investment from Bank/Financial Institutions may be recommended.

Annexure-1

COST FINANCING PATTERN:

Tk. In “000”)

SL. No. | Particulars | Cost to Incur | ||

F/C | L/C | Total | ||

1 | Land | – | – | – |

2 | Building & Civil Works | 5,142 | 9,550 | 14,692 |

3 | Machinery & Equipments | 2,878 | 5,833 | 8,711 |

4 | Clearing & Forwarding, L/C Commission, Port Charge, Duty & Surcharge and Internal Freight @ 9% on M/C | – | 784 | 784 |

5 | Local Machinery | 545 | 1,011 | 1,556 |

6 | Erection & Installation | – | 300 | 300 |

7 | Contingency | – | 800 | 800 |

8 | Furniture & Fixture | 1,382 | – | 1,382 |

9 | Vehicles | 560 | 1,040 | 1,600 |

10 | Preliminary & Pre-operating expenses | 500 | – | 500 |

11 | Interest During Construction period | – | 1,124 | 1,124 |

| Total Cost of the Project | 11,007 | 20,442 | 31,449 |

Debt Equity Ratio for proposed Term Loan = 35: 65 (Based on Fixed Cost).

Annexure-2

WORKING CAPITAL ESTIMATION

(Tk. In ‘000’)

Item | Tied up period | Amount |

| Imported raw materials | 90 days | Back to Back |

| Local cost of raw materials | 2 months | 794 |

| Labor wages | 2 months | 5952 |

| Other cash | L.S. | 142 |

Total | 6888 |

Bank Loan 70 % | Tk. 4,822 | |

Equity 30 % | Tk. 2,066 | |

Total | Tk. 6888 |

Annexure-3

PROJECTED INCOME STATEMENTS

(Tk. in ‘000’)

| DESCRIPTION | 1ST YEAR | 2ND YEAR | 3RD YEAR |

| Capacity Utilization | 60% | 70% | 75% |

| Sales Revenue | 89812 | 104781 | 112266 |

| Cost of Goods Sold | 68197 | 77942 | 83178 |

| Gross Profit | 21615 | 26839 | 29088 |

| General, Admin. & Selling Expenses | 7112 | 8110 | 8638 |

| Operating Profit | 14503 | 18729 | 20450 |

| Financial Expenses: | 2133 | 2606 | 2402 |

| Net Profit before Tax | 12370 | 16125 | 18048 |

| Investment in Govt. Bond (30%) | 3711 | 7838 | 5415 |

| Tax | Tax | Holiday |

|

| Net Profit after Investment in Govt. Bond | 8659 | 11287 | 12633 |

| Rations (%): | |||

| Gross profit to Sales | 24% | 25% | 25% |

| Operating Profit to Sales | 16% | 17% | 18% |

| Net Profit to Sales | 9% | 10% | 11% |

| Net Profit to Total Fixed Cost | 24% | 32% | 36% |

Annexure – 4

SALES ESTIMATION

(Tk. In ‘000’)

Item | Quantity | Unit Price | Amount |

| Basic Sweater | 35,000 (Dozen) | USD 62.53 Per Dozen | 149688 |

1 USD = BDT 68.40

Sales Estimate:

Year | Capacity Utilization | Total |

1st Year | 60% | 89812 |

2nd Year | 70% | 104781 |

3rd Year | 75% | 112266 |

Assumption:

1. Operation Time : Three shift per day of 8 (eight) hours per shift.

2. Operation Period : 300 working days in a year.

3. Assumed capacity utilization : 60%, 70% & 75% in the 1st, 2nd & 3rd year of projected operation.

Annexure-5 | |||||||

SENSITIVE ANALYSIS | |||||||

BASED ON 5% DECREASE IN SALES PRICE | |||||||

EARNING FORECAST | |||||||

| (Tk. in “000”) | |||||||

DESCRIPTION | 1ST YEAR | 2ND YEAR | 3RD YEAR | ||||

| Capacity Utilization | 60% | 70% | 75% | ||||

| Sales Revenue | 85,321 | 99,542 | 106,653 | ||||

| Cost of goods sold | 68,197 | 77,942 | 83,178 | ||||

| Gross profit | 17,124 | 21,600 | 23,475 | ||||

| General, Admin, & Selling Expenses | 7,112 | 8,110 | 8,638 | ||||

| Operating profit | 10,012 | 13,490 | 14,837 | ||||

| Financial Expenses | 2,133 | 2,606 | 2,402 | ||||

| Net profit before Investment | 7,879 | 10,884 | 12,435 | ||||

Annexure-6 | |||||||

SENSITIVE ANALYSIS | |||||||

BASED ON 5% INCREASE IN RAW MATERIALS COST | |||||||

EARNING FORECAST | |||||||

| (Tk. in “000”) | |||||||

DESCRIPTION | 1ST YEAR | 2ND YEAR | 3RD YEAR | ||||

| Capacity Utilization | 60% | 70% | 75% | ||||

| Sales Revenue | 89,812 | 104,781 | 112,266 | ||||

| Cost of goods sold | 71,607 | 81,839 | 87,337 | ||||

| Gross profit | 18,205 | 22,942 | 24,929 | ||||

| General, Admin, & Selling Expenses | 7,112 | 8,110 | 8,638 | ||||

| Operating profit | 11,093 | 14,832 | 16,291 | ||||

| Financial Expenses | 2,133 | 2,606 | 2,402 | ||||

| Net profit before Investment | 8,960 | 12,226 | 13,889 | ||||

Annexure-7

COST OF GOODS SOLD

(Tk. in ‘000’)

| DESCRIPTION | 1ST YEAR | 2ND YEAR | 3RD YEAR |

| Capacity Utilization | 60% | 70% | 75% |

| Raw materials | 53090 | 61940 | 66360 |

| Factory Wages & Salaries | 10580 | 11112 | 11640 |

| Store & Spares | 210 | 315 | 420 |

| Repair & Maintenance | 297 | 402 | 507 |

| Water, Power, Fuel & Gas | 821 | 958 | 1026 |

| Depreciation | 2610 | 2610 | 2610 |

| Rent, Tax & Insurance | 385 | 385 | 385 |

| Other Mfg. expenses | 200 | 220 | 230 |

| Total Expenses | 68197 | 77942 | 83178 |

Annexure-8

ASSUMPTION UNDERLYING COST OF GOODS SOLD

Raw Materials requirement at 100% capacity

SL. No. | Item | Qnty. | Price Tk. | Value | Source |

1 | Mixed Wool | 210000 Lbs | 143.00 ($2.6) | 30030 | Import |

2 | Lambs Wool | 126000 Lbs | 233.75 ($4.25) | 29452 | Do |

3 | 100 % Rayon Viscot | 84000 Lbs | 247.50 ($4.5) | 20790 | Do |

4 | Accessories for manufacturing & Packaging | 35000 Doz. | 120/- kg | 80272 | |

5 | Local Currency cost for import of yarn | @5% on C&F Value | 4200 | ||

Total | 88486 |

| |||

Therefore raw materials requirement

at 60% Capacity 53090

at 70% Capacity 61940

at 75% Capacity 66360

2. Factory Wages / Salaries:

1st Year | 2nd Year | 3rd year | |

| Wages | 9072 | 9072 | 9072 |

| Increment @ 5% | – | 453 | 906 |

| Bonus (2 months) | 1512 | 1587 | 1662 |

| Total | 10584 | 11112 | 11640 |

3. WATER POWER & FUEL:

A. Water : Available with Deep-Tube well cost included with the Local Machinery.

4. Stores and Spares:

On M/C cost @ 1% 210 315 420

1.5%, 2% on ward

5. Repair and Maintenance

On M/C cost @ 5%, 1% & 1.5% onward 105 210 315

On Building cost @ 2% 192 192 192

270 402 507

6. Rent, Tax, Insurance:

1% of fixed 385 385 385

FUEL & LUBRICANT

Item | Quantity | Rate per Unit | Amount (Tk.) |

| Lubricant | 200 Ltr. | 200/Liter | 40000 |

| Fuel | 24000 Ltr. | 215 Liter | 600000 |

| Grease | 200 Lbs | 100/Lbs | 20000 |

| Total |

|

| 660000 |

TOTAL COST OF WATER POWER FUEL & LUBRICANT

100% | 1st Year | 2nd Year | 3rd Year | |

Power | 409 | |||

Fuel & Lubricant | 960 | |||

1369 | 821 | 958 | 1026 |

5. DEPRECIATION:

| A) | Depreciation on machinery has been assumed @ 10% per year (Value 21360) | 2130 | 2130 | 2130 |

| Depreciation on Building has been assumed @5% per year | 480 | 480 | 480 | |

2610 | 2610 | 2610 |

Annexure-9

GENERAL, ADMINISTRATION AND SELLING EXPENSE

Taka in (000)

| Particulars | 1st Year | 2nd Year | 3rd Year |

| Directors Remuneration | 300 | 300 | 300 |

| Salaries of administrative | 1079 | 1133 | 1187 |

| Postage, Telegram & Telephone | 128 | 140 | 155 |

| Printing & Stationery | 100 | 130 | 145 |

| Traveling & Conveyance | 150 | 170 | 185 |

| Depreciation & Write-off | 464 | 464 | 464 |

| Audit Fees | 20 | 20 | 20 |

| Selling Expenses | 4724 | 5473 | 5847 |

| Advertisement | 50 | 100 | 150 |

| Misc. Expenses | 100 | 170 | 185 |

| Total | 7112 | 8110 | 8638 |

SALARIES:

| Particulars | 1st Year | 2nd Year | 3rd Year |

| Salaries | 996 | 996 | 996 |

| Increment @ 5% | – | 50 | 100 |

| Bonus ( 1 month) | 83 | 87 | 91 |

| Total | 1079 | 1133 | 1189 |

| 2 | Depreciation: | |

| a) Furniture & Vehicle @ 2% | 264 | |

| Preli. & Security Expenses | 200 | |

| Total | 464 |

3. Selling Expenses: Assumed to be 5% on net Sales.

Annexure-7

BREAK EVEN ANALYSIS

TERM LOAN

(Tk. in ‘000’)

Operating Year : 2nd year

Capacity Utilization : 7%

Sales Revenue : 88646

Expenditure | Total Cost | Fixed Cost | Variable Cost |

| Raw materials | |||

| Wages & Salaries | |||

| Storage & Spares | |||

| Repair & Maintenance | |||

| Water Power & Fuel | |||

| Depreciation & Write off | |||

| Rent, Tax & Insurance | |||

| Other Mfg. Expense | |||

| Directors Remuneration | |||

| Administrative Salaries | |||

| Postage, Telephone etc. | |||

| Traveling & Conveyance | |||

| Printing & Stationery | |||

| Audit Fees | |||

| Misc. Expense | |||

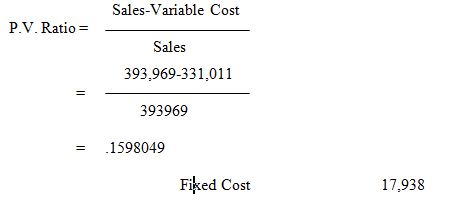

Total | 348,948 | 17,938 | 331,011 |

BEP in capacity utilization = 28%

Annexure-12

INTERNAL RATE OF RETURN (IRR)

(Tk. in ‘000’)

| Year | Investment | Cash Inflow | Net Cash Inflow | NPV at 30 % discounting factor | NPV at 40 % discounting factor |

| 0 | |||||

| 1 | |||||

| 2 | |||||

| 3 | |||||

| 4-7 | |||||

| 8 |

IRR = 32%

Salvage Value:

1) Land @ 100% = 16000

2) Building @ 10% = 2600

3) Machinery @ 5% = 1777

20377

Assumptions:

1) The recovery value of money is not considered.

2) The cash flow contents operating profit plus non-cash expenses.

3) The economic life of the project is 12 years.

Annexure-13

PROJECTED FUND FLOW STATEMENT

(Tk. in ‘000’)

| A) Sources of Fund: | Construction Period | 1st Year | 2nd Year | 3rd Year |

| Equity- Existing |

|

|

|

|

| Equity-Proposed for BMRE |

|

|

|

|

| Existing Term Loan |

|

|

|

|

| BMRE Term Loan |

|

|

|

|

| Working Capital Loan ( CC & PC) |

|

|

|

|

| Operating Profit |

|

|

|

|

| Return on Govt. Bond |

|

|

|

|

| Depreciation & Write off |

|

|

|

|

| Total |

|

|

|

|

| B) Application of Fund: |

|

|

|

|

| Investment in Fixed Assets |

|

|

|

|

| Increase in current assets |

|

|

|

|

| Investment in Govt. Bond |

|

|

|

|

| Payment: |

|

|

|

|

| Principal (Term Loan) |

|

|

|

|

| Interest (Do) |

|

|

|

|

| Intt. on Working Capital |

|

|

|

|

| Total |

|

|

|

|

| Surplus (A-B) |

|

|

|

|

| Opening Cash balance |

|

|

|

|

| Closing Cash balance |

|

|

|

|

Annexure-14

DEBT SERVICE COVERAGE RATIO (DSCR)

(Tk. in ‘000’)

| Income | 1st Year | 2nd Year | 3rd Year |

| Net profit before investment |

|

|

|

| Depreciation & write off |

|

|

|

| Interest of Term Loan |

|

|

|

| Income available for meeting liabilities |

|

|

|

| Liabilities |

|

|

|

| Installment of Term Loan |

|

|

|

| Total liabilities |

|

|

|

D.S.C.R. (Times) |

|

|

|

Annexure-15

PROJECTED BALANCE SHEET

(Tk. in ‘000’)

| Assets | Const. Period | 1st Year | 2nd Year | 3rd Year |

| Cash Balance |

|

|

|

|

| Current Assets |

|

|

|

|

| Investment in Govt. Bond |

|

|

|

|

| Fixed Assets |

|

|

|

|

| Total |

|

|

|

|

| Liabilities |

|

|

|

|

| Existing Term Loan |

|

|

|

|

| BMRE Term Loan |

|

|

|

|

| Working Capital Loan |

|

|

|

|

| Intt. During construction period |

|

|

|

|

| Equity (Existing + BMRE) |

|

|

|

|

| Retained Earning |

|

|

|

|

| Total |

|

|

|

|

ECONOMIC ASPECTS

1. EMPLOYMENT OPPORTUNITY:

The project will create direct and full time employment for 1200 persons. The cost of employment creation per persons comes to around Tk. 1.01 Lac.

At 85 % capacity utilization the project is expected to contribute Tk. 921.57 Lac per annum to the country’s GDP. The detailed calculation is shown below;

Tk. in “000”)

Items |

| Taka |

| A. Sales : (3rd years operation) | : | |

| B. Less inter firm transactions: | ||

| 1. Raw and Packing Materials | : | |

| 2. Repair & Maintenance | : | |

| 3. Water, Power, Lubricants etc. | : | |

| 4. Insurance/Rent/Tax | : | |

| 5. Stores & Spares | : | |

| 6. Office Supplies, Postage etc. | : | |

| 7. Traveling & Transportation | : | |

| 8. Selling Expenses | : | |

| 9. Miscellaneous Expenses | : | |

Total | ||

| Total Contribution to GDP ( A-B) |