Executive Summary

Prime Bank Limited is one of the leading commercial bank in our country with huge growth in almost every sphere. It was incorporated under the Companies Act 1994, started its operation on April 17, 1995 with a target to play the vital role on the socio-economic development of the country and with the motto “Bank with difference”. It availed its registration as a banking company under the Banking Company Act 1993 from the Bangladesh Bank dated February 12, 1995. Currently the bank has 52 branches and lately introduced the ATM services to the people. Mr. Imam Anwar Hossain is the Chairman and Mr. M. Shajahan Bhuiyan is the Managing Director.

The equity capital and total assets are Tk. 38555.41 million and Tk. 608976.21 million at the end of the 2006. The deposit of PBL stood at Tk. 547240.80 million. Moreover the default rate is only 1.52% and the credit disbursed at the end of 2006 is 450102.18 million. The return on asset and equity for the last two year were 1.36%& 1.72% and 20.23%&, 27.25% which indicate the efficient management of the bank.

The failure of the commercial bank is mainly occurs due to bad loans, which occurs due to inefficient management of the loan and advance portfolio. Actually the credit portfolio is not only constituted the banks asset structure but also a vital factor of the bank’s success. PBL has a credit policy and guideline with operational manual under which the bank will operate. The bank provide loan in almost all mode like; Overdraft, Loan (general), PAD, LIM, LTR, IBP, FDBP, Packing Credit Loan, lease finance, and CCS etc. While sanctioning of credit undergoes some steps-like collecting of related documents and information with dully filed-up credit application form, scrutinizing, investigation (appraisal), preparation of proposal, sanctioning, pre-disbursement compliance, disbursement, supervision monitoring. Credit management deals with all this process. The loan policy has established the lending limit for all loan officers and combination of officers and loan committee. In general like any other bank in PBL secured loans will carry higher limit than the unsecured loans for comparable purpose, seasonal working capital loans, might carry higher limit than term loan. The bank has 26% payable on demand loan.

Effective Credit Administration can ensure good recovery of loan and advance and good yield. When the credit proposal are approved the credit officer must have to be ensured that the disbursement of the credit facilities must comply with the directions written in the credit policy and circular made by time to time. Moreover the credit officer has to collect NOC from other bank where the client is enjoying the credit facility and the CIB report. Maintenance of the credit file is another issue that is urgent because “Credit file” must provide all the pertinent information relating to that particular credit on the spot monitoring if required. Loan policy of the Prime Bank Limited has prescribed uniform credit files maintenance and documentation procedures.

Supervision is another vital part in the credit management procedure. The objective of supervision is to make sure that the repayment is as per condition and the loan account is not having any “EXCESS OVER LIMIT”. To ensure that they check the entire loan accounts, communicate with the borrower reminding him, performance analysis of the client’s business,

The loan review process is a crucial tool in reducing losses and in monitoring loan quality. Loan review consists of a periodic audit of the ongoing performance of some or all of the active loans in a bank’s loan portfolio. To ensure that the loan policy is consistent with the bank and BB requirements, the official has to carry out this function and also to know the overall status of the loan portfolio. While classifying the loans PBL categorizes the loans in to four: Continuous loan, Demand Loan, fixed term loan, and Agriculture and Micro credit. On both objective and qualitative basis the loans are classified. If any loan remains outstanding more than 6 months, 9 months and 12 months will be classified as substandard, doubtful, and bad and loss. (Demand, continuous). In dealing with the problem loan, PBL offer revised loan agreement, interest discount and if not recovered – filed legal suit. The accounting policy for the classified loans is different.

Proper credit appraisal is the vital factor to reduce the default culture in the banking industry. If the borrowers are assessed properly, possibility of default will reduce. Depending on the amount of the loan the appraisal procedures varies. After collecting all the documents the credit officer scrutinize the documents and then start investigation. For credibility appraisal PBL collect information from other banks, business community, suppliers etc. Management’s ability, risk-taking attitudes are appraised though evaluating the business background and investment in business. Then the products are appraised in terms of demand and user. But the problem is that the competitive position analysis is ignored in most of the cases. After the investigation, a proposal is made for loan sanctioning. Before sanctioning any credit, the committees consider the factors-Remunerative, Recovery.

The appraisal system need be improved in-terms of risk measurement-mitigation, perfect market analysis-competitive position analysis (Five force model- where competitor, supplier, new entry, buyers, potential substitute products will be highlighted and briefly discussed.) product comparisons in terms price, quality, packaging etc. For efficient management of the loan accounts the assignment system (a credit officer is assigned some number of loan account and overall managing of the can be followed for tighter monitoring, and supervision. Beside this the importance to set up Research and Development department must be realized by the top management to reduce the data unavailability and continuous monitoring of the costs and finding out new ways reduce costs. The job description of the credit departments should be specific or defined to improve the quality of work and motivation.

1. INTRODUCTION

ORIGIN OF THE REPORT

As part of the Internship Program of Bachelor of Business Administration course requirement, I was assigned for doing my internship in The Prime Bank Limited for the period of 12 weeks starting from April 2007 to June 2007 as an intern. In PBL I am working in the Credit department of the Motijheel Branch and my organizational supervisor is Md. Abdullah- Al-Masud, VP. My project was Credit Appraisal System and Credit Management in Prime Bank Limited, which was assigned by my faculty supervisor Dr. Mosharaf Hossain, Professor of Department of Finance, University of Dhaka, also approved the project and authorized me to prepare this report as part of the fulfillment of internship requirement.

OBJECTIVES

Part A: Organization Part

- Features of the PBL

- Performance analysis

Part B:

Credit Appraisal System and Credit management of Prime Bank Limited

- Finding out the credit appraisal and credit management practice by Prime Bank.

- Analysis and comparison of credit appraisal and management with that of standard.

- SWOT Analysis of Prime Bank Limited.

- Trend Analysis of Loans and Advances particularly of Syndication Finance and Consumer Credit Scheme.

- Finding out the major and minor problems associated with that of Prime Bank Limited and recommendations thereagainst.

Beside the organization’s objective, my objective is to have a clear-cut knowledge of credit appraisal and management practice by a prominent bank and to know the effectiveness of credit appraisal system in the process of credit approval system and the portfolio of loan and advances and how they manage it.

SCOPE OF THE REPORT

The study would focus on the following areas of Prime Bank Limited.

- Credit appraisal system of Prime Bank Limited.

- Procedure for different getting credit facilities.

- Portfolio (of Loan or advances) management of Prime Bank Limited.

Each of the above areas would be critically analyzed in order to determine the efficiency of PBL’s Credit appraisal and Management system.

SOURCES OF INFORMATION

Information collected to furnish this report is both from primary and secondary sources.

The primary sources are:

- Practical desk work

- Face to face conversation with the officers

- Face to face conversation with the clients

- Relevant file study as provided by the concerned officer

The secondary sources are:

- Different Circulars issued by the Head Office and Bangladesh Bank

- Different ‘Procedure Manual’, published by PBL

- Annual Reports (2002, 2003 and 2004) of PBL

- Publications obtained from different libraries and from internet

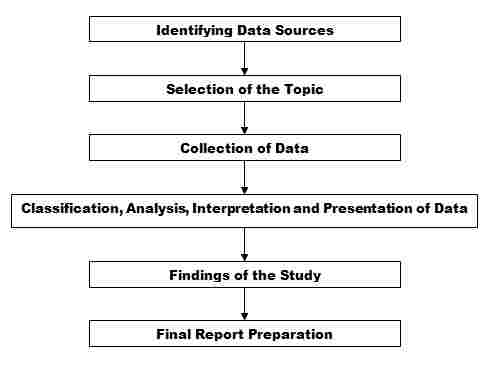

METHODOLOGY

The study requires a systematic procedure from selection of the topic to final report preparation. To perform the study data sources are to be identified and collected, they are to be classified, analyzed, interpreted and presented in a systematic manner and key points are to be found out. This overall process of methodology is given in the following page in the form of flowchart that has been followed in the study.

Figure: Flow chart of methodology

- Selection of the topic: The topic selected for the study was assigned by my supervisor Professor Dr. Mosharaf Hossain Before assigning the job it was discussed with me so that I can prepare a well-organized internship report.

- Identifying data sources: Essential data sources both primary and secondary are identified which will be needed to complete and workout the study. To meet up the need of data primary data are used and the study also requires interviewing the officials and staffs where necessary.

- Collection of data: Primary data are collected through 100% physical inspection as there is no provision and scope for using sampling technique.

- Classification, analysis, interpretation and presentation of data: To classify, analyze, interpret and presentation of data I used some arithmetic and graphical tools to understand them clearly.

- Findings of the study: After scrutinizing the data problems of the study are pointed out and they are shown under concerned heads. Recommendations are suggested thereafter to overcome the problems.

- Final report preparation: On the basis of the suggestions of our honorable course teacher some deductions and additions are made and final report is prepared thereafter.

LIMITATIONS

Though I tried my level best to produce a comprehensive and well-organized report on the Credit Appraisal System and Credit Management of Prime Bank Ltd., some limitations were yet present there:

- A period of twelve week was not sufficient to collect and understand the insights of credit appraisal and management.

- Banks policy did not permit to disclose various data and information related to Credit Portfolio.

2.AN OVERVIEW OF PRIME BANK LTD.

BACKGROUND:

Prime Bank being Banking Company has been registered under the companies Act 1993 as a Public Limited Company on February 12, 1995 with its registered office at 5, Rajuk Avenue, Motijheel Commercial Area, Dhaka-1000, Bangladesh. Later, the office had been shifted to Adamjee Court (annex building), Motijheel Commercial Area. It started operation from April 17, 1995 with a commitment to play some social role in addition to normal banking. Its slogan is “Prime Bank Ltd. – a bank with a difference”. From the very beginning, the bank has adopted the policy of diversifying its business. To achieve this objective, the bank started Consumer Credit Scheme, Lease Financing, Hire Purchase, loans in general, Secured Overdrafts etc. Under the dynamic leadership of the Chief Executive Officer, the bank earned profit within December 1995 and raised its reserve. The bank started operation its business through four branches. Now its branches stood at fifty two and by this year another two new branches will start their operation.

Prime Bank has an authorized capital of Taka 4,000 million and paid up capital of Taka 1,750 million. It is a full licensed scheduled commercial bank set up in the private sector by a group of highly successful entrepreneurs in pursuance of the government to liberalize banking and financial services. The former Governor of Bangladesh Bank Mr. Lutfar Rahman Sarker was the first Managing Director of this bank. At present, Managing Director is Mr. M Shahjahan Bhuiyan, who has a long experience in domestic and international banking. Highly professional people having wide experience in domestic and international banking are managing the bank. The bank has made a significant progress within a very short time due to its very competent board of directors, dynamic management and introduction of various customer friendly deposit and loan products. At present bank has 13 Directors, including the Chairman. The bank holds the first position in the CAMEL rating, published by Bangladesh Bank for the last consecutive four years.

VISION OF THE BANK

“A Bank with a difference”is the motto of Prime Bank Limited. So the motto itself is self-explanatory to deliver the vision of the bank. Prime Bank Limited is prepared to meet the challenge of the 21st century well ahead of time. To cope with the challenge of the new millennium it hired experienced and well-reputed banker of the country from the inception. The bank has efficient and dedicated professional and equipped with modern technology to provide the best service in the need of the people and thus to realize its vision. So the Bank is defined:

Vision

- To be the best Private Commercial Bank in Bangladesh in terms of efficiency, capital adequacy, asset quality, sound management and profitability having strong liquidity.

Mission

- To build Prime Bank Limited into an efficient, market driven, customer focused institution with good corporate governance structure.

- Continuous improvement in our business policies, procedure and efficiency through integration of technology at all levels.

Efforts focused

- On delivery of quality service in all areas of banking activities with the aim to add increased value to shareholders’ investment and offer highest possible benefits to our customers.

Strategic Priorities

- To have sustained growth, broaden and improve range of products and services.

OBJECTIVES OF THE BANK

The objectives of the Prime Bank Limited are specific and targeted to its vision and to position itself in the mindset of the people as a bank with difference. The objectives of the Prime Bank Limited are as follows:

- To mobilize the savings and channeling it out as loan or advance as the company approve

- To establish, maintain, carry on, transact and undertake all kinds of investment and financial business including underwriting, managing and distributing the issue of stocks, debentures, and other securities

- To finance the international trade both in Import and Export

- To carry on the Foreign Exchange Business, including buying and selling of foreign currency, traveler’s cheque issuing, international credit card issuance etc.

- To develop the standard of living of the limited income group by providing Consumer Credit

- To finance the industry, trade and commerce in both the conventional way and by offering customer friendly credit service

- To encourage the new entrepreneurs for investment and thus to develop the country’s industry sector and contribute to the economic development

MANAGEMENT OF THE BANK

Board of Directors are the sole authority to take decision about the affairs of the business. Now there are 13 directors in the management of the bank. All the directors have good academic background and have huge experience in business. Mr. Imam Anwar Hossain is the Chairman of the bank. The board of directors holds meetings on a regular basis.

Executive Committee: The Executive Committee consists of the members of the Board of Directors. This committee exercises the power as delegated by the Board from time to time and approves all matters beyond the delegation of Management.

Management Committee: The Management Committee consists of the Managing Directors and Head Office Executives. They discuss about the progress on portfolio functions. Different ideas and decisions, guidelines regarding deposits, lending and management of Human and Material resources are the main concern of this committee.

1. Managing Director |

2. Deputy Managing Director |

3. Senior Executive Vice President |

4. Executive Vice president |

5. Senior Vice President |

6. Vice President |

7. Senior Assistant Vice President |

8. Assistant Vice president |

9. First Assistant Vice president |

10. Senior Executive Officer |

11. Executive Officer |

12. Principal Officer |

13. Senior Officer |

14. Management Trainee Officer |

15. Junior Officer |

All these committees meet on a regular basis for discussing various issues and proposals submitted for decisions.

Management hierarchy of Prime Bank Limited:

DEPARTMENTS OF PBL

If the jobs are not organized considering their interrelationship and are not allocated in a particular department, it would be very difficult to control the system effectively. If the departmentalization is not fitted for the particular works there would be haphazard situation and the performance of a particular department would not be measured. Prime Bank Limited has done this work very well.

Logistic & Support Services Division (L&SSD)

This Division was formerly known as General Services Division (GSD). Its main functions relate to procurements and supply of all tangible goods and services to the Branches as well as Head Office of Prime Bank Limited. These include:

- Every tangible functions of Branch opening such as making lease agreement, interior decoration etc.

- Print all security papers and Bank Stationeries

- Distribution of these stationeries to the Branch

iv. Purchase and distribute all kinds of bank’s furniture and fixtures

- Receives demand of cars, vehicles, telephones etc. from branches and different divisions in Head Office and arrange, purchase and delivery of it to the concerned person / Branch

vi. Install & maintain different facilities in the Branches

Financial Administration Division (FAD)

Financials Administration Division mainly deals with the account side of the Bank. It deals with all the Head Office transactions with bank and its Branches and all there are controlled under the following heads:

- Income, Expenditure Posting: income and expenditures are maintained and posted under these heads.

- Cash Section: Cash section generally handles cash expenditure for office operations and miscellaneous payments.

- Bills Sections: this section is responsible for inland bills only.

- Salary & Wages of the Employee: Salary and wages of the Head Office executives, officers and employees are given in this department.

- Maintenance of Employee Provident Fund: Employee provident fund accounts are maintained here.

Consolidation of Branch’s Accounts: All Branches periodically (especially monthly) sends their income and expenditure i.e. profit and loss accounts and Head Office made the consolidation statement of income and expenditure of the bank. Here branch Statements arte reviewed. This division also prepares different monthly, quarterly, half-yearly statements and submits to Bangladesh bank. It also analyzes and interprets financial statements for the management and Board of director.

Credit Division

The main function of this division is to maintain the Bank’s Credit Portfolio. A well reputed and hard working group of executives & officers run the functions of this division. These functions are as follows:

- Receiving proposals

- Proposing and appraising

- Getting approval

- Communicating and sanctioning

- Monitoring and follow-up

- Setting price for credit and ensuring effectiveness of it

- Preparing various statements for onward submission to Bangladesh Bank

International Division:

The objective of this division is to assist management to make international dealing decisions and after decision is made, guide Branches in their implementation. Its functional areas are as follows:

- Maintaining correspondence relationship

- Monitoring foreign rate and exchange dealings

- Maintaining Nostro A/Cs and reconciliation

- Authorizing of signing and test key

- Monitoring foreign exchange returns & statements

- Sending updated exchange rates to the concerned Branches

Computer Division:

Prime Banks operates and keeps records of its assets and liabilities in computers by using integrated software to maintain client Ledger and general Ledger. The main function of this division is to provide required Hardware and Software. The functions of this division are:

- Designing software to support the accounting operation

- Updating software, if there is any lagging

- Improvising software to get best possible output from them.

- Hardware and Software trouble shooting

- Maintaining connectivity through LAN, Intranet & Internet

- Providing updated CD’s of online accounts to the Branches

- Routine Checking-up of computers of different Branches

Public Relations Division

It has to perform certain functions related to all types of communication. The broad routine functions can be enumerated as follows:

- Receiving and Sanctioning of all advertisement application

- Keeping good relation with different newspaper offices

- Inviting concerned ones for any occasion

- Keeping good relation with different officers of electronic media

Marketing Division

Marketing Division is involved in two types of marketing:

Asset Marketing: Marketing of assets refers to marketing of various kinds of loans and advances. In-order to perform this job, they often visit dome large organizations and attract then to borrow from the Bank to finance profitable ventures.

Liability Marketing: The process of Liability marketing is more of less same as Asset marketing. In this case different organizations having excess funds are solicited to deposit their excess fund to the Bank. If the amount of money to be deposited is large, the Banks sometimes offer a bit higher price than the prevailing market rate.

Human Resources Division

HRD performs all kind of administrative and personnel related matters. The broad functions of the division are as follows:

- Selection & Recruitment of new personnel

- Preparation for all formalities regarding appointment and joining of the successful candidates

- Placement of manpower

- Dealing with the transfer, promotion and leave of the employees

- Training & Development

- Termination and retrenchment of the employees

- Keeping records and personal file of every employee of the Ban

- Employee welfare fund running

- Arranges workshops & trainings for employee & executives

Inspection & Audit Division

Inspection and Audit division works as internal audit division of the company. The officers of this division randomly go to different Branches, examine the necessary documents regarding each single account. If there is any discrepancy, they inform the authority concerned to take care of that/those discrepancies. They help the bank to comply with the rules and regulation imposed by the Bangladesh Bank. They inform the Bangladesh Bank about the Current position of the rules and regulation followed by the Bank.

Credit Card Division

Prime Bank obtained the principal membership of Master Card International in the month of May, 1999. A separate Division is assigned to look after this card. The Marketing Team of this division goes to the potential customers to sell the card. Currently Prime Bank Ltd. offers four types of cards-

1. Local Silver Card

2. International Silver Card

3. Local Gold Card

4. International Gold Card

Recently Prime Bank has obtained the membership of VISA credit Card and soon they will start marketing of it.

Merchant Banking and Investment Division

This division concentrates its operation in the area of under writing of initial public offer (IPO) and advance against shares. This division deals with the shares of the Company. They also look after the security Portfolio owned by the Bank. The Bank has a large amount of investment in shares and securities of different corporations as well as government treasury bills and prize bond.

HUMAN RESOURCES MANAGEMENT OF PBL

The core competencies in banking sector can be created with the help of its personnel. The main thing in banking business is that a bank or financial institution has to avail the trust of the depositor, client for improving its performance. Availing the trust of the general people is not an easy task. Not only the directors attitude and efficiency but also that of the employees are important for achieving the trust of the general people and thus for better performance of the bank. In the face of the today’s global competition, it is not only essential to assemble the best people to work for the company but also to equip the workforce with the latest skill and technologies and retain the high achievers to compete effectively and efficiently.

To cope with the consumers’ need Prime Bank’s human resources policy emphasize on providing job satisfaction, growth opportunities, and due recognition of superior performance. A good working environment reflects and promotes a high level of loyalty and commitment from the employees. Realizing this Prime Bank Limited has placed the utmost importance on continuous development of its human resources, identify the strength and weakness of the employee to assess the individual training needs, they are sent for training for self development. To orient, enhance the banking knowledge of the employees PBL organize both in-house and external training.