Syndication means joint financing by more than one bank to the same borrower against a common terms and conditions governed by a common document.

In this report present syndicated loan, practiced by Bangladesh commercial Banks in Bangladesh and possible potentiality of it’s in Bangladesh explored. Techniques & Documentation Syndicate Loan in Bangladesh. The syndicated credit market in our country is developing rapidly due to imposition of regulatory limit by Central Bank, diversification of risks and in depth analysis of the project by more than one analyst etc. Many local banks and financial institutions are coming ahead to take part in Syndication Market as lead arranger and also doing agency function, which is the core function of any syndication loan process.

Prime Bank also provided Syndicated Loan in 1999-2010. Prime Bank Limited (PBL) is becoming a local giant in the syndication market by competing with the foreign banks. Annual Report-2010 Syndicated Loan in Prime Bank.

Bangladesh Bank, 18 April, 2010 “Decade of Loan Syndications”. There should be specific guide lines from Bangladesh Bank to operate Syndication Finance in Bangladesh. Banks. Bangladesh Perspectives of syndicated Loan. Syndicated Loan in Recommendations & Conclusion with Reference.

Background of the study

Most successful small companies that have developed to the point where they are damaging at the boundaries of that “small” designation have always dealt with one or a few individual banks negotiating individual loans and lines of credit separately with each institution. The next financing step, however, may be to consolidate banking activity through one syndicated facility. Corporate Cash flow Magazines Thomas Bunn noted that while business owners and executives sometimes dislike running the risk of alienating banks with which they have long done business the simple reality is that “Companies can outgrow their traditional banks and need new capabilities or an expanded bank group to fund their continued growth. (Bunn, Thomas, (1995))

Syndicated lending is a form of lending in which a group of lenders collectively extend a loan to a single borrower. The group of lenders is called a syndicate. The loan is called a syndicated loan, in contrast to a bilateral loan, which is a loan made by a single lender to a single borrower Syndicated loans are routinely made to corporations, sovereigns or other government bodies. They are also used in project finance and to fund leveraged buyouts.

Problem Statement

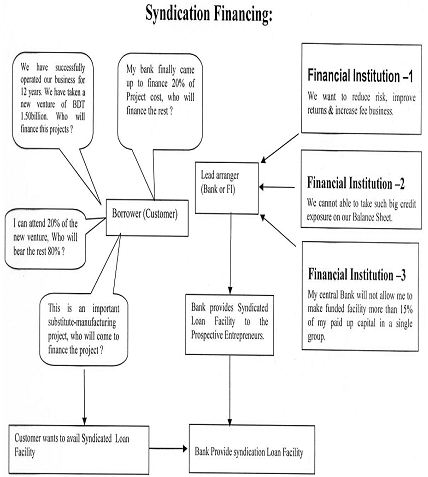

For a developing country like Bangladesh a huge amount of capital investment is very much needed both in private and public sectors. In order to get maximum benefits from such capital investment project financing is very important factor. But for many reasons project financing faces many problems, such as regulatory constraint, lack of expertise in project evaluation, scarcity of fund etc. Syndicated loan as an innovative product alleviate most of the problems in large amount of project financing.

Objectives of the study

The objectives of the study include the following :

- To Build a sound concept on syndicated lending.

- To gather knowledge about global and local practice on Syndicated lending.

- To know the techniques applied in Syndication Loan in Bangladesh.

- To know the status and performance of Syndication Loan in Bangladesh.

- To assess the prospect of Syndication loan in Bangladesh.

Methodology of the Study

Type of research

This study examined the operational mechanism and performance of Syndication Loan of Commercial Banks in Bangladesh. Descriptive research has been made in this study.

Sources of data

The data are collected from both the primary and secondary data.

Primary Information:

Primary information has been collected by personal observation the concerned resource persons. Such as Senior Vice President, Assistant Vice President, Senior Principal Officer, and Principal Officer of Prime Bank Limited, Dhaka Bank Limited .All these people have first-hand experience on the process of syndicated loan.

Secondary Information

Sources of secondary information included internal reports of syndicated loan unit of three private commercial banks, articles, and website of periodicals, website of Bangladesh Bank, other related articles presented in conferences, seminars, workshops and newspapers, books, journals, reports, internet, etc.

Data Collection Method

This paper is descriptive type of research focuses on the operational mechanism and performance Syndication loan of Commercial Banks in Bangladesh. Personal observation and group discussion has been conducted.

Limitations of the Report

Collection of required information limited time period hampered the data collection and analysis. Besides secondary information in the relevant area acted as major constraint to the report preparation. Moreover syndicated loan market is very competitive in Bangladesh now. For this reason local banks maintain so much confidentiality for their syndicated loan information. In addition, there is no aggregate record in Bangladesh Bank too. However, I tried my best effort to manage with the limitations and to successfully finish the report writing.

Literature Review

A number of available research papers have been studied to the backdoor of doing this study. The main findings of those researches have been summarized in this part of study.

Loan syndication in Bangladesh is getting popular among financial institutions because of its structure. But lack of expertise about the product is one of the major problems faced by the loan syndication practice in our country. Syndicated facilities bring businesses the best prices in aggregate and spare companies the time and effort of negotiating individually with each bank. Syndicated credit requires more approval stages than bilateral loan agreements, which makes it more transparent. And it leads to a sound credit approval. Less default rate in syndicated loan compare to stand-alone credit facility in Bangladesh. If default rate in stand-alone loan is 100%, default rate in syndicated loan is 1-2%. Easy and more acceptable documentation procedure for participating financial institutions and borrower. Sometimes transfer of loan to secondary market cannot done by lead arranger because of lack of adequate information of borrower, negative mentality of participating financial institutions. Regulatory constraint of providing loan more than 15% sometimes increases the number of financial institutions in syndicate

A syndicated loan is a single facility financed by a group of lenders under the same contractual conditions. Although the contract is the same for all banks in the lending syndicate1, they do not necessarily receive the same return on their loans. Besides periodical interest payments, banks also receive up-front fees at the time the contract is signed. These upfront fees can differ across banks. In our sample of sovereign syndicated loans, the average difference between the top and bottom upfront fees is 16 basis points. This up-front fees differential is substantial seen that the average lifetime of sovereign syndicated loans is typically quite short. In fact, the “annualized” up-front fee differential is on average 10 basis points, i.e. just over 10 percent of the interest spread. This means in a typical bank syndicate, some banks earn on average 10 percent more than some others, while the loan conditions are the same. (Rhodes, T., (2004)),

Traditionally, loan syndication was practiced in Europe. Euro syndicated loan is usually a floating rate loan with fixed maturity, a fixed draw down period and a specified repayment schedule. One, two or even three banks may act as lead managers and distribute the loan among themselves and other participating banks. One of the lead banks acts as the agent bank and administers the loan after execution, disbursing funds to the borrower, collecting and distributing interest payments and principal repayments among lead banks, etc. A typical Euro credit would have maturity between 5 to 10 years, amortization in semi-annual installments, and interest rate reset every three or six months with reference to LIBOR. Syndicated loans can be structured to incorporate various options, e.g., a drop lock feature converts the floating rate loan into a fixed rate loan if the benchmark index hits a specified floor. A multi-currency option allows the borrower to switch the currency of denomination on a roll-over date. Security in the form of government guarantee or mortgage on assets is required for borrowers in developing countries like India. ( Subrata Kumar Bhowmick FCA And Ratna Dutta ACA).

The mandated arrangers of a syndicate usually provide or under write a larger fraction of the loan facility and can be considered to build stronger relationships with the borrower than the low-tier members that merely are invited for risk sharing purposes. Additionally, only the mandated arrangers are engaged in information production on the borrower, which increases their knowledge of firm (Yasuda, 2005)

What is Syndicated Loan?

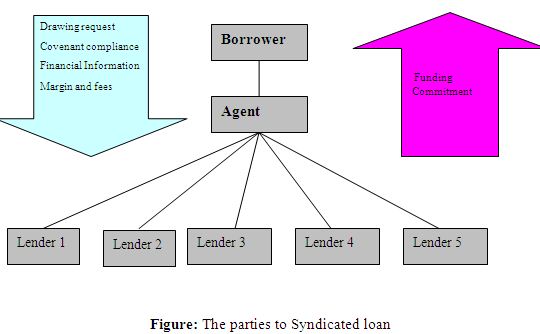

A syndicated loan is one in which two or more banks (the syndicate of lenders) contract with a borrower to provide loan on common terms and conditions governed by a common document or set of documents. Interest on syndicated loans accrues at a variable rate rather than a fixed rate, which is more usually found in the securities markets. This variable, or floating, rate of interest is reset periodically, the periods most frequently used are one, two, three and six months, and are usually selected by the borrower. The borrower usually mandates one or more banks to act a arranger and one member of the bank group is normally appointed to act as the agent bank for the syndicate. It is the role of this bank to coordinate all negotiations, payments and administration between the parties once the contract has been executed. The mandated arrangers prepare information material, invite other banks to provide capital, and communicate with the borrower on behalf of all the participating capital providers. Additionally, the mandated arrangers usually provide a larger amount of capital than the other banks. One of the participating banks, most likely a mandated arranger, will act as the facility agent of the transaction with the responsibility to manage the loan during its lifetime (Armstrong, 2003). Mandated arrangers are often referred to as top-tier banks and their title in loan transactions is currently Mandated Lead Arranger (MLA).

The broad definition of a syndicated loan embodies the principal features of the product. It is a multi-bank transaction with each bank acting on a several basis – each bank acts as underwriter and/or lender, on its own without responsibility for the other banks in the syndicate. If a bank fails to honor its obligations as a member of a bank syndicate, the other syndicate banks have no legal duty to satisfy these obligations on that behalf. The agent bank will usually consult with the borrower in such circumstances and attempt to find a wiling replacement bank or banks – although it is not obliged to do so.

Syndication means joint financing by more than one bank to the same borrower against a common terms and conditions governed by a common document. (Toudihul Alam Khan)

As per Encyclopedia of Banking and Finance (EBF), “Syndication” means a temporary association of parties for financing and execution of some specific business purpose.

EBF also defines “Syndicated Loan ”as loans extended by multiple banks where the overall credit involved exceeds an individual lender’s legal lending or other limits.

Syndicated loan is made available by a group of FIs in predefined proportions under the same credit facility following common loan documentation formalities. (project Finance and Loan Syndication).

Parties to Syndicated loan

Loan syndication is different from club financing (where many banks finance a single borrower and Agent) in terms of deal origination, mechanism, documentation, disbursement, monitoring, management, etc. Essential Characteristics: (i)single borrower, (ii)more than one lender, (iii)common loan & security documentation.

General Features

The provision of debt for these projects have been through syndications/club financing

- Equity components ranged between 20% and 35%

- Participants in large syndications average 13 banks

- Tenure tends to be 5 to 7 years

- Interest rates tend to be between 12% and 14% ( i.e. base of around 8% + margin)

- All loans have been denominated in local currency (Bangladesh taka)

- There were no GoB Guarantees or Multilater

Formation of Syndicated Loan

A borrower’s ability to secure a syndicated loan, though, is predicated on its ability to spur the creation of a syndicate in the first place. “No two syndications are identical,” wrote Bunn. Syndicated loan involves many banks, each member bank holds different titles: lead bank, arranging bank, underwriting bank, allied bank ,senior manager bank, manager bank or participating bank. Syndicated loan includes three types of member banks from functional perspective:

1. Lead Bank

Upon customer’s entrustment ,it plans and organizes syndicate, arranges banks to underwrite the loan. Lead Bank only guarantees the underwriting of the loan amount they commit. Lead Bank can be one bank or joined by many banks.

2. Participating Bank

With the invitation of lead bank. it participates in loan syndicate and provides loan according to the agreed share.

3. Correspondent Bank

It is responsible for lending and management after the legal documents are signed. Correspondent Bank is usually the lead bank or its branch institution, it can also be determined through discussion between member banks.

Documents in syndicated loan

• Facility Agreement

• Pari Passu security sharing Agreement

• Escrow account agreement

• Agreement for Assignment of Insurance

• Agreement for Assignment of contract

• Projects funds and share retention Agreement

• Subordination Agreement

• Deed of Mortgage

• Letter of Hypothecation (machinery to be purchased)

• Letter of Hypothecation (existing machinery)

• Letter of Hypothecation (Balance on the account of

Escrow Account)

• Power of Attorney to sell the hypothecated machinery

• Letter of Undertaking of all the Shareholders

• Personal Guarantee of the sister concerns

• Corporate Guarantee of the sister concerns

• Letter of continuation

• Demand promissory Note

• Letter of Comfort. (Source: Syndication Loan Subrata Kumar Bhowmick FCA and Ratna Dutta ACA)

Advantages of Syndicated Loans

Syndication in financial markets goes back in time for over a century. First used in insurance and security underwriting, syndication became increasingly important in venture capital, the hedge fund industry and, more recently, in the corporate loan market. It has some advantages, they are exploring here

Main Advantages

In addition, economists and syndicate executives contend that there are other, less obvious advantages to going with a syndicated loan. These benefits include :(Bunn (1995))

- Syndicated loan facilities can increase competition for business, prompting other banks to increase their efforts to put market information in front of borrower in hopes of being recognized.

- Flexibility in structure and pricing. Borrowers have a variety of options in shaping their syndicated loan, including multicurrency options, risk management techniques, and prepayment rights without penalty

- Syndicated facilities bring businesses the best prices in aggregate and spare companies the time and effort of negotiating individually with each bank.

- Loan terms can be abbreviated

- Increased feedback. Syndicate banks sometimes are willing to share perspectives on business issues with the agent that they would be reluctant to share with the borrowing business

- Syndicated loans bring the borrower greater visibility in the open market. Bunn (1995) noted that “For commercial paper issuers, rating agencies view a multi-year syndicated facility as stronger support than several bilateral one-year lines of credit.”

Other Advantages

Besides Bunn (1995) mention, A syndicated transaction offers a number of clear-cut advantages over bilateral credit arrangements. Among them

- Less Documentation : It would not need separate negotiations and separate documents for each lender. One set of documents will govern the credit facility, regardless of how large it is or how many banks participate.

- Market Sponsorship : Agent will help to coordinate or underwrite future financings and serve as a strong leader in the marketplace.

- Competitive Rates : It will bring the best deal available in the market for businesses given situation. Agent bank will bid aggressively for that role, and the other banks in the transaction will ensure that the agent delivers a competitive financing package

- Relaxed Banks : Syndicate bank group will take comfort in the syndicate structure knowing they will be treated as equals, getting the same terms and prices as the other lenders

- Greater Flexibility : Changing a syndicated credit is easier, not harder, than changing bilateral loan agreements, which require 100% approval. Most amendments to syndicated transactions require only a majority vote.

Parties of Syndication Loan

Lead Arranger: Captain of Loan Syndication Boat

- The borrower nominates lead Bank. It is very important factor for a borrower to nominate Lead Bank/Arranger in the light of maintaining long term relationship. It leads to a Lead Bank being an Agent Bank of syndication, which is common practice. For this reason, it should be an organization with which the borrower is likely to feel comfortable over the whole loan period

- After analyzing all the relevant aspects of risks, Lead Bank will help the borrower by taking proper steps and will set a plan to raise the fund from the Banks/FIs to set up the proposed project. A Time Schedule to be prepared by the Lead Arranger to close the syndication deal (Format is enclosed in annexure).

- A Good professional arranger will always be able to add something to a borrower’s own deliberations. It should be able to suggest amendments and enhancements, which will make it easier for a syndicate to take up the loan without compromising its essential elements

- It is very important that the lead bank has an in-depth knowledge of the individual borrower. This applies not only to the particular company but also to the wider environment in which it works, the economic pressures, the competitive environment and so on.

- As part of the process of selecting a potential syndicate leader it will be necessary to decide whether it can sell this deal to the sort of syndicate that is desired. If a high-quality group is the aim, then a high level of past performance in similar transactions will be required in order to encourage other experienced banks into the syndicate.

- Credibility can be equally important when dealing with less heavyweight players, who will rely to a much greater extent on the senior members of the syndicate.

- The Lead Bank/Arranger has the responsibility for much of the selling of the loan to participants.

- The Lead Bank will be the first port of call for questions and needs to be able to answer them authoritatively in order to head off problems and sensitivities before they arise. This role will be particularly important with respect to syndicate members who do not know the borrower particularly well

- Arranger earns at a rate of 0.50% – 1.50% of the total loan amount as the arrangement fee from the borrower if the transaction approved. This rate should be undisclosed to the other participants of the syndicate

- Agent:

- Agent will preserve all security documents and will do all the administrative & monitoring activities tenure of the loan.

- The agent bank’s role is to act as the agent for the banks (not for the borrower) and to co- ordinate and administer all aspects of the credit facility once relevant documentation has been executed.

- The activities of agent bank include the disbursement of monies from the syndicate to the borrower, after satisfaction of relevant conditions precedent, and will also cover collection of monies, essentially commitment fees, front-end fees, interest and repayments of principal, from the borrower on behalf of the participating banks.

- The agent will also be responsible for transmitting any post-closing waivers or amendments requested by the borrower and negotiating them with the syndicate banks The responsibilities and role of the agent in cases an event of default has occurred

- Inform the participating banks regarding progress of the project time to time as per clause of facility agreement

- The Agent will send the audited financial statements regularly as per clause of facility agreement.

- The Agent will call a review meeting time to time where the borrowers and the representatives of the participating banks will be present.

- Participating Banks/Financial Institutions (FIs):

A group of Banks/FIs committing to some extent for participation in the syndication under lead arranger.

- Joint Arranger/Co-Arranger

A group of mandated banks who will act jointly to raise the fund from the syndicated market for the borrower.

- Lead Manager

A senior underwriter or a Bank/FI committing to the highest level of participation.

- Manager:

A second tier underwriter or a bank committing to the second level of participation.

- Co-Manager:

A Bank committing to a third level of participation.

- Borrower:

An institution or individual that arises funds in return for contracting into an obligation to repay those funds, together with payment of interest at determinable periods over the life of a facility to the agent. (Touhidul Alam khan, (2003))

Loan Syndication process

1) Pre-Signing Stage

A) Pre-Mandate Phase

- Selection/Identification of Borrower for Syndication

- Build-up continuous relationship with the Borrower

- Round Table discussion with the borrower in Loan Syndication Unit of the Bank and articulation/structuring of the borrower’s need from the syndication credit market

- Preparation of Term Sheet by Loan syndication unit based on discussion with the borrower (Term sheet is a document, which is not generally intended to be legally binding until it forms part of a formal offer, setting out the main agreed terms and conditions to a transaction between the borrower and arranger

- Discussion with the top management of the Bank for finalization of Term Sheet for obtaining letter of Mandate from the borrower. A meeting can be arranged in the Head Office of Lead Bank with the borrower and top management of the Bank on this issue followed by special entertainment and gift

(Mandate is the authority to act in the marketplace on behalf of a Borrower to the market is based upon terms and conditions, which have been agreed between the Arranger and Borrower.)

B) Post-Mandate Phase

1. Obtaining letter of Mandate from the Borrower along with loan processing fee. Contents of Term Sheet/Letter of Mandate:

a) Name of Lead Arranger

b) Name of Borrower

c) Nature of Facility;

d) Currency;

e) Total Project Cost;

f) Syndicated Amount

g) Minimum Participation Amount

h) Period;

i) Purpose;

j) Repayment;

k) IDCP (Interest During Construction Period);

l) Debt-equity Ratio;

m) Pricing/Interest rate

n) Loan Processing Fee (Flat) : A lump-sum amount to be paid to the Lead Arranger for processing the loan in the syndicated credit market. A loan-processing fee is non refundable.

- Syndication Fee/Arrangement Fee (Flat): Fee to be paid on syndicated amount before signing of the agreement to the mandated bank/Lead Arranger or group of banks for arranging a transaction (This fee will not be shared to the participating banks);

p) Agency Fee (Flat): Fee payable on syndicated loan amount to the Agent for preserving all security documents and for administrative & monitoring activities as agent tenure of the loan.

q) Participation Fee (Flat): Fee to be paid on syndicated loan amount to the Lead Arranger before signing of the agreement which will be shared among the participants on pro-rata basis.

r) Management Fee (Annual): Fee on outstanding amount of the facility after end of every loan year during loan period to be shared by all the participating banks on pro- rata basis.

s) Commitment Fee (Quarterly): An annual percentage fee payable to the Lead Bank on the undrawn portion of a facility made available by it to a borrower. This fee is typically payable quarterly in arrears and to be shared on pro-rata among the participants.

t) L/C Commission: L/C will be opened (for import of capital machinery and equipment for the proposed project) by the Front Bank (Lead Arranger or L/C opening Bank) and some percentage of commission to be realized by the Front Bank. L/C opening Bank (Front Bank or Lead Arranger) may retain some percentage as skim of L/C commission and the rest will be shared on pro-rata basis and the rest will be shared on pro-rata basis.

u) Escrow Account: Escrow Account is opened pursuant to the Escrow Account Agreement into which all funds accrued in all accounts of the borrower permitted under this Agreement shall be paid into and in respect of which the borrower shall give irrevocable instructions to the bankers of such accounts to transfer the proceeds thereof to Escrow Account in accordance to the terms of this Agreement

v) Supplier’s Guarantee: Guarantee from the suppliers for due performance of the machinery/commercial production will be obtained before payment to the suppliers. The suppliers will provide a Guarantee from a reputed Bank for minimum 10% of the invoice value of machinery ensuring the quality of machinery, production capacity and commercial production.

w) Availability period: The period in which the facility to be availed by the borrower after the date of signing of the facility agreement.

x) Security Packages: Against the syndicated facility will be sanctioned includes pari passu charge by way of registered mortgage of project land and building, pari-pasu charge on machinery and equipment of the project, personal guarantee of the directors & their spouses, corporate guarantee of sister concerns etc.

y) Legal Expenses: All legal costs relating to prepare the documents by the Lead Arranger to be borne by the borrower. But vetting of the documents by the participating banks to be borne by the participating banks.

z) Syndication (Best effort Basis): Placement in syndication market where loan facility has not been fully underwritten, the arranger will agree to use its best efforts to attract sufficient lenders to complete the syndication deal in the amount required by the borrower.

- Obtaining Feasibility Report on the Project from the borrower.

- Collecting CIB Inquiry Form on the customer for obtaining CIB report from Bangladesh Bank on the Borrower.

- Obtaining Board’s Approval/Consent for raising fund under lead management of the Bank and determining Lead Bank’s stake.

- Officials of Syndication Unit of the Lead Bank may visit the supplier’s country to observe the supplier’s (of machinery and equipment) performance and the project where the supplier supplied the same machinery. If it is not possible to visit before opening of L/C, the visit program may be arranged before shipment of machinery & equipment of the project.

- Offer Letter may be issued to the prospective participating Banks/FIs (before sending IM) for obtaining ‘Soft Commitment’ which may touch about the project, sponsors, pricing and period.

- Preparation of Information Memorandum (IM) after studying all relevant aspect of the project for viability of the same (if necessary, expert opinion of technical expert, market survey to be done by the lead arranger to strengthen the IM). Contents of Information Memorandum (IM) given below :

2) Post-Signing Stage

- Issue Sanction Letter to the Borrower from the Agent.

- Completion of all the documentation/mortgage formalities as per sanction terms and conditions and Facility Agreement and other syndication agreements.

- Send a copy of the set of all documents to the borrower and the participating banks attested by the authorized signatory (person) of syndication unit of agent bank.

- Opening of L/C for import of capital machinery and equipment by Front Bank/Lead Arranger/Agent.

- Distribution of participation fee to all the participating banks by the lead arranger/agent on pro-rata basis

- Distribution of L/C commission to all the participating banks by the lead arranger/agent.

- Prepare draw down schedule and send draw down notice to the participating banks/FIs as per Facility Agreement and collection of fund;

- Send the Audited Financial Statement of the company to the participating banks as per facility agreement;

- Send the progress report on the project to the participating banks describing the details works of the project completed and the contribution of the equity of the borrower

- Preparation of Investment Schedule of the project

- Preparation of Repayment Schedule

- Arrange Site Visit Program time to time before starting Trial Production and Commercial Production by the Lead Arranger/agent

- Obtain NOC from the participating banks/FIs, if there is any change in Means of Finance/Project Cost or any change of terms & conditions of the Facility Agreement or other syndicated documents

- Arrange review meeting with the borrower, participating banks and the Lead Arranger time to time for exchanging views with each other regarding progress of the project and to enhance the relationship with the Lenders and the Borrower. Minutes of the meeting to be distributed to the borrower and participating banks/FIs in time

- Distribution of installment of syndicated loan to the participating banks/Fs as per repayment schedule;

- Proper monitoring of the syndicated loan by the Lead Arranger/agent and provide any information about progress or any other issue of the project;

- Reconcile the outstanding amount with all the participating banks along with principal and interest;

Closing the syndication deal by the Lead Arranger/Agent in real sense by payment of last installment to the participating banks and reconciling all the calculation of the syndication deal. (Touhidul Alam khan, (2003))

Bangladesh Bank Perspective

Borrowing needs of large new industrial and infrastructure projects coming up in Bangladesh now typically run into billions of taka. Sharing of the credit risk burden of large loans to large projects by syndication has enabled fast expansion of industrial term lending, particularly since the late nineteen nineties (table 1, chart 1). (Source: Bangladesh Bank, 18 April, 2010 “Decade of Loan Syndications”)

Annual movement of Industrial term loans Arrange by Syndicated in Bangladesh (Disbursement & Recovery)

(Tk. in crore)

| Year | Disbursement | Recovery |

| 1994-1995 | 1281.20 | 481.11 |

| 1995-1996 | 1230.44 | 519.69 |

| 1996-1997 | 1200.00 | 887.19 |

| 1997-1998 | 1120.34 | 859.43 |

| 1998-1999 | 1330.10 | 1093.31 |

| 1999-2000 | 1627.26 | 1653.34 |

| 2000-2001 | 3057.07 | 2795.10 |

| 2001-2002 | 3505.15 | 3212.97 |

| 2002-2003 | 3961.99 | 3835.12 |

| 2003-2004 | 6675.99 | 4963.44 |

| 2004-2005 | 8704.52 | 8546.98 |

| 2005-2006 | 9650.02 | 6759.52 |

| 2006-2007 | 12394.78 | 9068.45 |

| 2007-2008 | 20150.82 | 13624.20 |

| 2008-2009 | 19972.69 | 16302.48 |

Source: SME & Special Programmes Department, Bangladesh Bank.

Types of Facility Through Syndication in Bangladesh

The syndicated credit market uses many instruments and has developed a stream of new products to meet borrower needs and to take advantage of changes in the markets. Out of many Instruments SYNDICATED TERM LOAN is most popular in our country. At present, many non-funded facilities are being provided through syndication.

Duration of Syndication Loan in Bangladesh

A syndication loan is usually of medium-term maturity, i.e., 3 (three) to 10 (ten) years, although transaction can be arranged with a maturity as short as six months or as long as 25 (twenty-five) years.

Bangladesh Perspective

Bangladesh’s syndicated loan market is growing fast, as more private local banks in a group have come forward to lend different organizations because of the less risk in such banking product, according to bankers. The 2008 data from major market playing banks show a 60% rise in such lending over the last year. The total syndicated loan this year stands around Tk.2,500 crore, while it was Tk.1,500 crore in 2007.

The Performance of Syndicated Loan in Prime Bank Limited (1999-2010)

Prime Bank Limited (PBL) is becoming a local giant in the syndication market by competing with the foreign banks. Earlier, Lead Arranger for any syndication deal denotes only Foreign Banks. Now, the local Banks are coming with this biggest noble task of arranger for smooth industrialization of Bangladesh. Among the local banks, Prime Bank’s role is pioneer in syndication market. Prime Bank Limited has successfully concluded 20 (twenty) syndicated deals by raising Tk 1141 crore (approx.) as Lead Arranger and Agent till date through Syndications and Structured Finance Unit (SSFU) of the Bank as under:

| Sl. No. | Deal Name | Taka Lac | Year | Facility | No. of FIs | |

| KDS Textile Mills Ltd. | 900.00 | 1999 | Term Loan | 4 | ||

| Rahmat Textiles Ltd. | 1300.00 | 2000 | Term Loan | 4 | ||

| CMC | 11300.00 | 2001 | Bank Guarantee | 3 | ||

| Mir Ceramics Limited (Phase-I) | 2805.00 | 2002 | Term Loan | 7 | ||

| H.P. Chemicals Limited | 3578.00 | 2003 | Term Loan | 4 | ||

| Nasir Glass Industries Ltd. | 10000.00 | 2003 | Term Loan | 14 | ||

| Confidence Salt Limited | 3200.00 | 2003 | Term Loan | 8 | ||

| Popular Pharmaceuticals Ltd. (Phase-I) | 3900.00 | 2004 | Term Loan | 5 | ||

| ColorMaster Limited | 2300.00 | 2004 | Term Loan | 2 | ||

| Mir Ceramics Limited (Phase-II) | 2400.00 | 2005 | Term Loan | 7 | ||

| Popular Pharmaceuticals Ltd. (Phase-II) | 5000.00 | 2005 | Term Loan | 9 | ||

| BRAC | 20000.00 | 2005 | Term Loan | 17 | ||

| Virgo Pharmaceuticals Ltd. | 2300.00 | 2006 | HPSM | 3 | ||

| Khulna Power Company Ltd. | 14500.00 | 2006 | Pref. Share | 6 | ||

| Ananta Denim Technology Ltd. | 6500.00 | 2007 | Term Loan | 7 | ||

| Tania Cotton Mills Ltd. | 6500.00 | 2007 | Term Loan | 10 | ||

| Olympic Spinning Mills Ltd. | 5150.00 | 2008 | Term Loan | 7 | ||

| Configure Engineers & Construction Co. Ltd. | 3000.00 | 2008 | Term Loan | 3 | ||

| M&H Telecom Ltd. | 5280.00 | 2009 | Term Loan | 6 | ||

| X-Ceramics Ltd. | 4133.90 | 2009 | Term Loan | 6 | ||

| Sea Peal Beach Resort & Spa Ltd | 8500.00 | 2010 | Term Loan | 9 | ||

Table : Year-wise Fund raising position as Lead Arranger of Prime Bank Limited

Total exposure handling by SSFU:

At present, PBL is also working as agent for 16 (sixteen) number of syndicated deals and handling total credit portfolio of Tk 170433.00 lac of more than 35 (thirty five) syndicated customers, where Prime Bank’s exposure is Tk 93411.00 lac (funded 76591.00 lac and non-funded Tk 16820.00 lac) (approx.) (Source: Bangladesh Bank,18 April, 2010 “Decade of Loan Syndications”

Significant events of Syndications

• Celebrating Decade of Loan Syndications

PBL pioneered loan syndications initiatives in March 1999 through launching the Syndications and Structured Finance Unit (SSFU). Its success story till close of business includes putting in place over BDT 1,150 million for 22 projects as a lead arranger. To mark a decade of loan syndications journey, the bank organized a gala celebration event on April-2011 that witnessed:

• Governor, Bangladesh Bank to attend the ceremony as the Chief Guest;

• Chairman and members of the Board of Directors of the bank being present; and

• Key persons representing the borrowing companies under the syndicated transactions, and the participating banks joining to mark the event. (Annual Report 2010)

Prime Bank Arranges Tk 2Bln syndicate Term Loan for BRAC

A syndicated term loan agreement for Tk 2 billion (Tk 200 crore) favouring BRAC was signed recently at a city hotel under the lead arrangement of Prime Bank Limited. Presided over by Prime Bank Managing Director M Shahjahan Bhuiyan, the ceremony was attended by Prime Bank Limited Board of Directors Executive Committee Chairman Imam Anwar Hossain as the chief guest and BRAC Executive Director Abdul Muyeed Chowdhury as the guest of honour.

The syndicated term loan has been sanctioned for the micro-credit lending programme of BRAC, which is one of the world’s largest non-government organisations (NGOs) operating in the country. By arranging this syndicated term loan facility, Prime Bank Limited has created an opportunity for local and foreign commercial banks to demonstrate their shared commitment to meet the challenge of the International Year of Microcredit, 2005.

Prime Bank Limited deputy managing directors Nasiruddin Ahmed, Mahbubul Alam and Kazi Masihur Rahman along with other executives and officials of BRAC and the participating banks were also present in the ceremony.

Prospects of Syndicated Loan in Bangladesh

Term loans provided by the financial system in Bangladesh amount to only about US$250-300 million per year, equivalent to about 1.5 percent of Gross Domestic Product (GDP), while private and public investment amounts to about 16 percent of GDP. A major constraint to the provision of term loans is the lack of a well developed long-term savings market. Nationalized Commercial Banks (NCBs) fund their term loans mainly with their deposits creating a maturity mismatch.

Proper Syndication Loan Procedure examines the needs of both borrowers and lenders involved in the design, origination, arrangement, distribution and management of syndicated loans and link the process of executing a successful deal to the optimal design of a syndication unit. For the following reason financial institutions can go syndicated loan market.

- The entry of financial institutions into the corporate loan market has helped improve the transparency and liquidity of the secondary loan market, at the expense of increased overall loan borrowing costs.

- As the large investment is increasing day to day, borrower needs fund without minimum transaction hassle with minimum funding cost. Government also restricted the funding limit of the financial institutions. In this situation loan syndication seems a better solution for both the borrower and loan provider.

- Most important issue is the risk associated with big projects. These types of risks can be minimized by evaluating properly and monitoring regularly the projects and with the borrowers.

- Most prospective and large investment sectors in Bangladesh are Power, Telecom Textile Industries, Steel Mills, Cement, Sugar Mills, Private Container Terminal, Gas Evaporation Project, Infrastructure Development Projects, School & Hospital through foreign joint venture, Information & Communication Technology etc.

- After phasing out of Multi Fiber Agreement (MFA) our country is realizing more intensely the importance of backward linkage industry to support and sustain our garments sector in the face of emerging harsh competition because through this phase out garments industry will loose their protected market to other competitors of the region. Garments sector contributes 36 % of the total export-earnings of the country.

- Investment banks are relatively new entrants into the commercial lending business and lend to less profitable, more leveraged firms than do commercial banks.

- The presence of a dual market maker is found to increase liquidity in the secondary market for syndicated bank loans. (Jahan, A. and Akter, B., (2006))

Local Banks of syndicated Loan

Local commercial banks are largely limited to making loans with a maximum tenor of 5-7 years and generally require equity of 25 % – 35% of total project cost. Loan amounts are typically small with limits imposed by Bangladesh Bank on single party exposure. Syndications and club financing are the favoured means to increase pooled finance, but it has been estimated that projects in excess of $70 – 100 million are difficult to finance locally (largest syndication to date has been $57 million). As such, local banks are unlikely to provide significant amounts of long-term financing for large projects. Inexperience with large scale new infrastructure projects requiring consortium lending – on a non-recourse basis – pose difficulties which local banks are unlikely to overcome in the short-term. Currently, interest rates are high and stand at about 12.5% (base rates of around 8% + margin of 4.5%). Importantly, beyond supply side issues, demand side factors – the impact on investor returns of competitively bid projects, suggest that sponsors have an advantage in opting for international finance sources at lower interest cost and longer tenors.

Challenges of syndicated Loan in Prime Bank Perspective

A syndicated loan is one that is provided by a group of lenders and is structured, arranged and administered by one or several commercial or investment Banks known as arrangers. Arrangers may appoint co-arrangers as and when required for stronger knitting of the loan syndication. Starting with the large leveraged buyout loans of the mid 1980’s, the syndicated market has become the dominant way to top banks and other institutional capital providers for such loans.

A syndicated loan may be compared with a ship moored with several anchors, which disseminate threats in an idiosyncratic rhythm and therefore make the loan portfolio more secure and hence more performing than a conventional loan. The mammoth loans required now a day towards large infrastructure or industrial projects including heavily capitalized power plants, commercial purposes and etc, need to be syndicated since no single bank would be prudent to risk such loan alone.

Bangladesh is fast marching forward to become a mid economy country due to achievement of about 6% GDP growth during last decade through rapid industrialization, almost self sufficiency in food and fantastic earnings from exports and overseas workers remittances. Bangladeshi entrepreneurs therefore are in dire need for syndicated loans from financial institutions to keep pace with this race of development.

Prime Bank’s professional syndication team will always take this challenge shoulder to shoulder with different discipline of entrepreneurs. All the members of Prime Bank Limited for their accomplishments and am eagerly looking forward to achieving more success, bringing in more innovations and leaving stronger impact in country’s economic growth and prosperity. (Source: Bangladesh Bank,18 April, 2010 “Decade of Loan Syndications”

Prospects of syndicated Loan Prime Bank Perspective

Bangladesh is now poised to achieve rapid industrialization, economic growth and respectable GDP growth. We believe that loan syndication has a great role to play in supporting initiatives in this respect. The extensive use and reliance on syndicated loan market will surely help generate financial innovations and provide large projects with more convenient, professional and custom-made services. Syndicated loan business, based on the mechanism of sharing both risk and return, and pooling of resources and expertise, add depth and breadth to financial markets in various ways.

Prime Bank has worked to the satisfaction of its co-lenders in all the projects it has taken the lead. Syndications efforts put forth by the Bank have been painstaking and proved instrumental in adding buoyancy in most of the important sectors of the economy covering microfinance, glass and ceramics, minerals mining (salt), textiles, chemicals, pharmaceuticals, telecommunications, physical infrastructure (inland container depot), tourism & hospitality, etc. Our syndication initiatives accommodated financing for many groundbreaking projects, some of which are import substitutes, have created huge employment opportunities, and are saving as well as earning scarce foreign currency through exporting project outputs.

The Bank’s presence has also led to product development in syndicated loan market. The Bank, for a record, had arranged the first ever Sharia’h based syndicated investment facility in 2006 that was widely acclaimed regionally. It has maintained its efforts to place second such transaction lately. The syndication team has also imparted training on syndication techniques and practices for central bank officials. The Bank will continue to offer this value added service and in coming days will place more and more emphasis upon loan syndication to support the country achieving her development goals.

On this important occasion,

Prime Bank Limited (PBL), one of the leading private commercial banks in Bangladesh is operating for last 15 years since inception on 17th April 1995. Its mission is, to be the best private commercial bank in terms of efficiency, capital adequacy, asset quality, sound management and profitability having strong liquidity.

The Bank is providing full-fledged, cost-effective, and customer-friendly conventional and Islamic Sharia’h based banking solutions to its customer via a network of eighty-four (84) branches all over the country including five (5) Islamic Banking branches, five (5) SME service centers, one (3) off-shore banking unit, one (1) exchange company based in Singapore, one (1) merchant banking unit, and around seven-hundred owned and shared ATM booths.

Prime Bank started its journey in loan syndication market by successfully concluding its first syndication deal as the Lead Arranger in 1999. By this time, the Bank has deepened and added breadth to the loan syndications market by raising around BDT 11,500 million for 21 milestone projects as the Lead Arranger and providing agency functions as the Agent. (Source: Bangladesh Bank,18 April, 2010 “Decade of Loan Syndications”)

Prime Bank arranges tk 150m syndicated loan for ceccl

Dhaka, Bangladesh (BBN)- Prime Bank Limited (PBL) has successfully concluded a BDT 150 million syndicated loan agreement as lead arranger with two other private commercial banks for Configure Engineering and Construction Company Limited (CECCL) for setting up a five-star hotel in Cox’s Bazar.

The two other banks are the Pubali Bank Limited and the Mutual Trust Bank Limited.

A signing ceremony was held at a local hotel on Thursday where the managing directors and chief executives of the participating banks and the sponsors of the project were present.

Managing Director of Prime Bank Limited M Ehsanul Haque, Managing Director of Pubali Bank Limited Helal Ahmed Chowdhury, Deputy Managing Director of Mutual Trust Bank Limited Quamrul Islam Chowdhury, Chairman of CECCL Habibur Rahman and Managing Director of CECCL Khurshid Alam Opu signed the agreement on behalf of their respective organisations.

The PBL, a leading private commercial bank, has been working in the syndication market by successfully concluding the first syndication deal as lead arranger since 1999 and now the bank is a dominant player in the area.

Keeping their role as pathfinder in syndication market the PBL has established a strong position in banking arena as lead arranger and agent by arranging a good number of deals through raising fund for large as well as medium size industries, the bank said.

Prime Bank to hike investment Syndicated loan in telecom, power projects

Prime Bank has planned to scale up financing in infrastructures including the capital-intensive power and telecom sectors as part of its efforts to boost industrialisation in the country, its chief executive officer (CEO) said Monday.

Risk-averse Bangladeshi private banks usually stay clear of funding big projects, forcing many local investors to seek loans abroad or at a costly term from foreign financial giants operating in the country.

Prime Bank Limited CEO Ehsanul Haque said the PBL – the leading private bank in the country — wants to be an exception as it has planned to bankroll key energy and telecom projects in the coming months through its ‘hugely successful’ syndication lending arrangements.

“The risk sharing nature of the syndicated loan model makes it ideal for investing in mid and large scale infrastructure projects and over the years we have seen that such lending works perfectly well in the country,” Haque told newsmen at a briefing. to mark the occasion of “Decade of Loan Syndications: As Lead Arranger” in celebration of its ongoing journey for expanding partnership and building economy.

Haque said Bangladeshi economy needs massive investments in infrastructure and his bank “sees ample opportunities to provide large scale financing in power, telecommunications, renewable energy, tourism and communication related projects.”

“These are the sectors which are likely to grow enormously in the coming years and would require huge volume of large and mid scale financing which can better be served through syndicated loan schemes”, he added.

The 15-year-old private bank, over the last decade raised around Tk. 11.5 billion through syndicated financing as lead arranger while providing funds worth of another Tk. 4.5 billion either as participating banks.

This year, the bank has already arranged Tk. 850 million under such scheme for Sea Pearl Beach Resort and Spa Limited in Cox’s Bazar, which is set to be the first five star resort in Bangladesh promoting international time sharing.

Earlier, the bank also played a pioneering role in raising syndication loan for the country’s first vacuum evaporated salt re-crystallization plant, the first hydrogen peroxide project and the first ever float glass manufacturing plant.

In 2006, the bank arranged the first ever Sharia’h based syndicated investment facility and at the same time, it has imparted training on syndication techniques and practices for central bank officials, officials said.

“Years ago, only the multinational banks used to take the leading role in syndicated financing but lately the local private banks have come forward to dominate the scene”, Ehsanul Haque said.

Terming the syndicated loan scheme as the future in the banking sector, he said, “The greater opportunity for risk sharing in syndicated financing would enable the local banks to finance a greater number of up and coming infrastructure projects requiring sizable investments”.

Haque called for quicker initiation of the government’s Public Private Partnership (PPP) projects, underlining these large-scale infrastructures would require joint financing by the government and private sector to take off.

“Until now, the local private banks have largely opted out of financing large-scale power sector projects as they usually involve long term investment and pose greater risk

Recommendations

Syndication or club financing is a growing concept in Banking Arena of Bangladesh. Syndicated finance diversifies the risk of one bank on a single borrower and increases the quality of loan through consensus or cumulative judgment and monitoring of different banks / financial institutions.

- There should be specific guide lines from Bangladesh Bank to operate Syndication Finance in Bangladesh.

- Establishment of separate Syndication Unit in all Banks.

- Banks should narrow lead time of approval process in case of Syndication Finance though giving more delegation to the Management.

- Review pricing process including alternative instruments, relative value and secondary loan market.

- There should be specific code of conduct among agent banks in Bangladesh that they resolve any dispute regarding syndication advance among themselves.

- Sending the officials of the syndication unit in the training program on Loan Syndication (domestic & foreign).

- Understanding the nature of work of syndication unit by the top management of Lead Bank and the participating bank regarding time frame for completion a syndication deal successfully.

Conclusion

The advantages of syndicated loans for banks and borrowers show that they provide an important financing vehicle for emerging markets and thus for their economic development as they contribute to enhance the sources of external finance in these countries. Moreover, if syndicated loans reduce the cost of borrowed funds, they also contribute to favor the financing of companies. The expansion of syndicated loans increases the diversification possibilities for banks in terms of risk and income, which decreases the likelihood of bank failures. As a consequence, the expansion of syndicated loans contributes to financial stability, which is a fundamental issue for emerging economies. Bangladesh is also emerging economy who can benefit from syndicated lending based project financing

While these benefits are especially important for emerging markets finance, the agency problems related to syndications can have severe consequences for the financial stability of these markets A crucial input to mitigate these problems is the structure of the syndicates that, if adapted, can reduce agency costs related to the syndication process.

Overall, the structures of syndicates are adapted to enhance monitoring of the borrower and to increase the efficiency of re-contracting process in case of borrower’s distress. Main syndication motives, such as loans portfolio diversification, regulatory pressure and management costs reduction, also influence syndicate structure in emerging markets.

Euro area banks seem to have expanded. In the last several years the popularity of this type of loan has exploded. By 2000, the total annual volume of syndicated loan issuance had risen to $1.2 trillion, a $100 billion increase over the year before. The businesses that are choosing this option to finance their growth have expanded beyond the Fortune 500 companies that were its first users. Initially developed to address the needs of huge, acquisition-hungry companies, they have now become a flexible funding source for both mid-sized companies and smaller companies that are on the cusp of moving into mid-sized status. In fact, syndicated loans for as little as $10 million have become commonplace. A syndicated loan is a much larger and more complicated version of a participation loan.