1.1 Methodology

In the organization Chapter, much information has been collected from the secondary sources such as from annual report, different published articles, journals, brochures, web sites etc. Some information has been collected directly from organization. All the data collected for reporting purpose are systematically.

1.2 Limitation

Past and present information that are confidential could not be accurately obtained. Alike all other banking institutions, BRAC Bank is also very conservative and strict in providing managerial information. In such cases, we have relied upon certain assumptions, which are only amateur estimates. As many of the analysis on the obtained data are based on our sole interpretation, there may be some biases, as lack of knowledge and depth of understanding might have hindered our ability to produce an absolutely authentic and meaningful report.

2.1 Banking Industry of Bangladesh

The gradual improvement in the overall policy environment has enabled Bangladesh to improve its economic performance in recent years. Successive governments in Bangladesh have been confronted with the problem of stimulating the economic growth rate in a country where a substantial segment of the population lives below the subsistence level. Economic policies are still guided by five year plans. Nevertheless, some progress has been made over the years, such as self -sufficiency in food grain production, reducing the population growth rate, poverty alleviation and boosting export income. The GDP growth has been about 6.5% in 2007, lower than 6.7% in 2006.

The Banking Industry in Bangladesh is one characterized by strict regulations and monitoring from the central governing body, the Bangladesh Bank. The chief concern is that currently there are far too many banks for the market to sustain. As a result, the market will only accommodate only those banks that can transpire as the most competitive and profitable ones in the future.

Currently, the major financial institutions under the banking system includes:-

Bangladesh Bank

Commercial Banks

Islamic Banks

Leasing Companies

Finance Companies

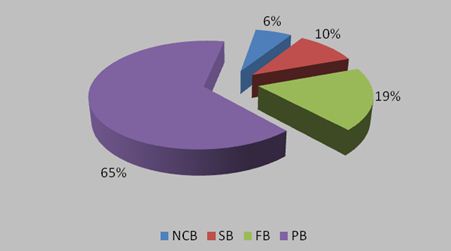

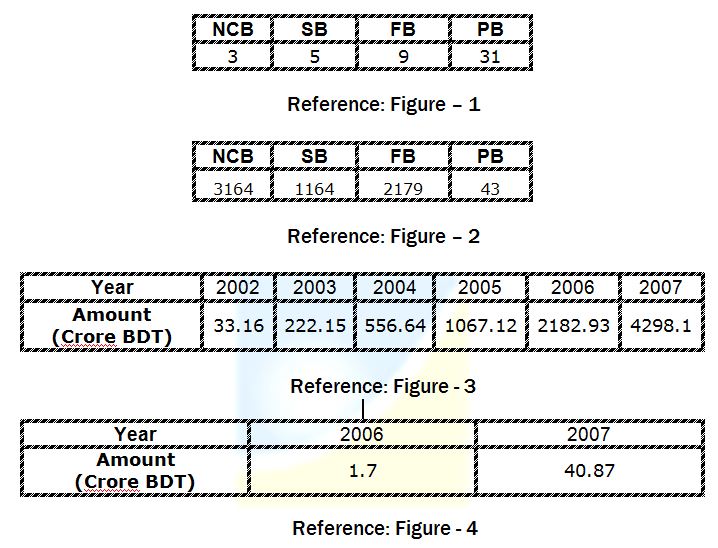

Of these, there are 3 nationalized commercial banks (NCB), 5 specialized banks (SB), 9 foreign banks (FB), 31 domestic private banks (PB) currently operating in Bangladesh.

Figure – 01: Schedule Banks of Bangladesh

All local banks must maintain 5% Cash Reserve Rate (CRR), which is non-interest bearing and a 20% Statutory Liquidity Rate (SLR). With the liberalization of markets, competition among the banking products and financial services seems to be growing more intense each day. In addition, the banking products offered in Bangladesh are fairly homogeneous in nature due to the tight regulations imposed by the central bank.

The Banking Industry of Bangladesh at present is in the growth stage. Almost every year new private banks are coming up, new branches are opening within two to three months, and new customers are coming to open an account in different banks. As a result, according to December 31, 2007 there are 3 nationalized commercial banks, 5 specialized banks, 31 local private commercial banks and 9 foreign commercial banks operating in this country.

Market size of an industry can be measured by many ways, such as Total Revenue, Volume of production number of customers and so on. However, in case of the Banking sector the measurement of market size is quite peculiar as both the total amount of deposits and advances are taken into consideration.

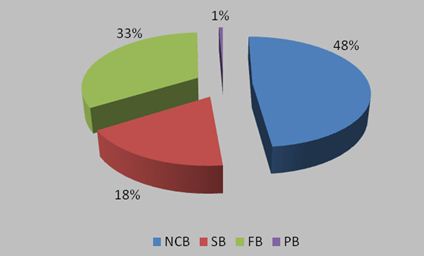

The following figure shows that the percentage of total branches of all the banks in the year 2004:

Figure – 02: Total Branches of All Banks

Table 01: Schedule Banks in Bangladesh

Name of Bank | Number of Branches | |

Inland | Abroad | |

| A. Nationalized Commercial Banks | ||

| 1. Agrani Bank | 978 | — |

| 2. Janata Bank | 848 | 4 |

| 3. Sonali Bank | 1320 | 14 |

| B. Specialized Banks | ||

| 1. Bangladesh Krishi Bank | 836 | — |

| 2.Bangladesh Shilpa Bank (Industrial) | 15 | — |

| 3. Bangladesh Shilpa Rin Sangstha | 5 | — |

| 4. BASIC Bank ( Bank of Small Industries and Cottage) | 8 | 1 |

| 5. Rajshahi Krishi Unnayan Bank | 300 | — |

| C. Private Commercial Banks | ||

| 1. Al-Arafa Islami Bank Ltd. | 20 | — |

| 2. Arab Bangladesh Bank Ltd. | 58 | 2 |

| 3. Bangladesh Commerce Bank Limited | 25 | — |

| 4. Bank Asia Limited | 27 | — |

| 5. BRAC Bank Limited | 36 | — |

| 6. Dhaka Bank Ltd. | 9 | — |

| 7. Dutch Bangla Bank Limited | 40 | — |

| 8. Eastern Bank Ltd. | 21 | — |

| 9. Exim Bank Limited | 30 | — |

| 10. First Security Bank Limited | 13 | — |

| 11. International Finance & Investment& Commerce Bank Ltd. (IFIC) | 55 | — |

| 12. Islami Bank Bangladesh Ltd. | 100 | 1 |

| 13. Jamuna Bank Limited | 29 | — |

| 14. Mercantile Bank Limited | 36 | — |

| 15. Mutual Trust Bank Limited | 25 | — |

| 16. National Bank Ltd. | 66 | — |

| 17. National Credit and Commerce Bank Limited | 50 | — |

| 18. One Bank Limited | 29 | — |

| 19. Oriental Bank Limited | 17 | — |

| 20. Premier Bank Limited | 20 | — |

| 21. Prime Bank Ltd. | 16 | — |

| 22. Pubali Bank Ltd. | 356 | — |

| 23. Rupali Bank | 493 | — |

| 24. Shajalal Islami Bank Limited | 22 | — |

| 25. Social Investment Bank Ltd. | 5 | — |

| 26. South East Bank Ltd. | 10 | — |

| 27. Standard Bank Limited | 05 | — |

| 28. The City Bank Ltd. | 80 | — |

| 29. The Trust Bank Limited | 16 | — |

| 30. United Commercial Bank Ltd. | 79 | — |

| 31. Uttara Bank Ltd. | 198 | 1 |

| D. Foreign Commercial Banks | ||

| 1. Bank Al Falah | 3 | — |

| 2. Citi Bank NA | 1 | — |

| 3. Commercial Bank of Ceylon Limited | 2 | — |

| 4. Habib Bank Ltd. | 2 | — |

| 5. Hong-Kong & Shanghai BankingCorporation ( HSBC ) | 9 | — |

| 6. National Bank of Pakistan | 2 | — |

| 7. State Bank of India | 1 | — |

| 8. The Standard Chartered Bank Limited | 22 | — |

| 9. Woori Bank | 1 | — |

| Total Number of Branches | 6339 | 23 |

2.2 Profile

BRAC Bank Limited, with institutional shareholdings by BRAC, International Finance Corporation (IFC) and Shorecap International, has been the fastest growing Bank in 2004 and 2005. The Bank operates under a “double bottom line” agenda where profit and social responsibility go hand in hand as it strives towards a poverty-free, enlightened Bangladesh.

A fully operational Commercial Bank, Brac Bank focuses on unexplored market in the SME business segment, which hitherto remained largely untapped within the country. The bank is also actively involved in retail banking and broad range of consumer loans ranging from to personal loan to auto loans to Debit & Credit cards. Furthermore the bank has gained a strong market share in the global money transfer market or remittance through significant tie-up with the most major transfer agencies. In the last five years of operation, the Bank has disbursed over BDT 1500 crore in loans to nearly 50,000 small and medium entrepreneurs. The management of the Bank believes that this sector of the economy can contribute the most to the rapid generation of employment in Bangladesh. Since inception in April 2008, the Bank’s footprint has grown to 36 branches, 392 SME unit offices and 67 ATM sites across the country, and the customer base has expanded to 200,000 deposit and 45,000 advance accounts through 2006.

Today Brac Bank is considered as on of the fastest growing banks extending full range of banking by providing efficient, friendly and modern fully automated on-line service. Since its inception, it has introduced fully integrated online banking service to provide all kinds of banking facilities from its conveniently located branches.

2.3 Corporate Vision

“Building a profitable and socially responsible financial institution focused on Markets and Business with growth potential, thereby assisting BRAC and stakeholders build a “just, enlightened, healthy, democratic and poverty free Bangladesh”.

2.4 Corporate Mission

Sustained growth in ‘Small & Medium Enterprise’ sector

Continuous low-cost deposit growth with controlled growth in Retail assets

Corporate assets to be funded through self-liability mobilization. Growth in Assets through syndication and Investment in faster growing sectors.

Continuous endeavor to increase fee based income

Keep our debt charges at 2% to maintain a steady profitable growth

Achieve efficient synergies between the bank’s branches. SME unit offices & Brac field officers for delivery of Remittance & Bank’s other products & services

Manage various lines of business in fully controlled environment with no compromise on service quality

Keep a diverse, far flung team fully motivated and driven towards materializing the Bank’s vision into reality

2.5 Corporate Values

our strength emanates from our owner – BRAC. That means we will hold the following values and be guided by them as we do our jobs.

Value the fact that we are a member of the BRAC Family.

Creating an honest, open and enabling environment

Have a strong customer focus and build relationships on integrity, superior service and mutual benefit

Strive for profit and sound growth

Work as a team to serve the best interest of our owners

Relentless in pursuit of business innovation and improvement

Value and respect people and make decisions based on merit

Base recognition and reward on performance

Responsibility, trustworthy and law-abiding in all that we do

2.6 Corporate Chronicle and Information

Inauguration of Banking operation : 4th July, 2001

First SME unit office : 1st January, 2002

Signing with Shore Cap as investor : 29th December, 2003

Signing with IFC as investor : 08 may, 2004

First ATM installed : 3rd April, 2005

Preferential share issued : 31st January, 2006

Signing with Infosys and 3i InfoTech for changing Bank’s IT platform : 1st august, 2006

24×7 Phone Banking opening : 9th September, 2006

Listing with CSE : 24th January, 2007

Listing with DSE : 28th January, 2007

Commencement of share trading in DSE and CSE : 31st January, 2007

Credit Card Launching : 06th February, 2007

Introduced Probashi Banking : 14th April, 2007

Launching of Travel related services (TRS) : 01st November, 2007

Launching of Omnibus with 12 member banks : 20th November, 2007

Company Registration Number : C-37782 (2082) of 1999

Auditor

KPMG, Rahman Rahman Huq

Chartered Accountants, 9 Mohakhali C/A, (11th & 12th Floor), Dhaka- 1212

Legal Advisor

Law Valley

Shajan Tower, Commercial Block, Suit # 202 (1st Floor)

4, Segunbagicha, Dhaka – 1000

Tax Advisor

Khandaker & Associates

73, Kakrail, Dhaka – 1000

2.7 Board of Directors

The number of directors in the board of the bank is 8 which are within the maximum limit as imposed by BRPD circular # 12 dated April 26, 2003 of Bangladesh Bank and notification – SEC/CMRRCD/2006-158/Admin/02-08 dated February 20, 2006 of Securities and Exchange Commission.

The names of the Board of Directors are given below:

Chairman : Mr. Fazle Hasan Abed

Directors : Mr. Syed Humayun Kabir

Mr. Md. Aminul Islam

Mr. Muhammad A. (Rumee) Ali

Mr. Quazi Md. Shariful Ala

Mr. Mark A. Coffey

Ms. Nahid Kabir

Managing Director : Mr. Kaiser Tamiz Amin

2.8 Credit Rating of the Bank

Pursuant to the Bangladesh Bank’s BPRD Circular no. – 06 dated July 05, 2006 and in order to safeguard the interest of investors, depositors, creditors, shareholders we have completed credit rating by Credit Rating Agency of Bangladesh Limited (CRAB) for the year ended 31 December, 2007.

Credit Rating Agency of Bangladesh Limited assigned “AA2” (pronounced double A two) rating to Brac Bank Limited in the Long Term and “ST-2” rating in the Short Term. Commercial Banks rated in this category is adjudged to be very strong banks, Characterized by very good financials, healthy and sustainable franchises and a first rate-operating environment. Rating in this category is characterized with commendable position in terms of liquidity, internal fund generation access to alternative sources of fund.

2.9 Corporate Governance

BRAC Bank Limited places the grater emphasis to maintain high standard of Corporate Governance. As the trustee on behalf of the shareholders of the company, the Bank’s board is fully aware of responsibilities and therefore, endeavors to safeguard the interest of all concerned.

The Board of Directors is the highest level of authority in the organization structure of BRAC Bank Limited. The board is responsible for overall direction and is ultimately accountable to the shareholders for the activities, strategies and performance of the company. In terms of the Corporate Governance principles set out by the Securities and Exchange Commission our Board of Directors has appointed an Independent Director. The prime concern of the Board is to ensure that the overall activities of the business are conducted responsibly and with focus on long-terms value creation. The Board meets periodically to transact matters placed them that require Board’s approval and directions. Board reviews the overall business and where necessary strategic guidelines one givens for onward implementation.

The Management Committee of BRAC Bank Limited is engaged to implement the decisions of Board of Directors and supervisions of day-to-day business affairs of the company. The committee is also responsible for achieving the business plan. The Committee consists of functional heads of different operating/business segments and is headed by Managing Director and CEO. In conformity with the Corporate Governance principles set out by the Securities and Exchange Commission, the Board of Directors constituted an Audit Committee.

2.10 Registered / Head Office and Branches

BRAC Bank Limited

1, Gulshan Avenue, Gulshan – 1

Dhaka – 1212, Bangladesh

Telephone : 01819230000, 01819260000

Website : www.bracbank.com

There are 36 Branches of BRAC Bank including the registered branch around in Bangladesh. In these, 12 branches are in Dhaka city and other 24 are outside Dhaka city.

2.11 Reach of the company

392 SME Unit Offices

36 Branches

67 ATMS

14 Cash Deposit Machines

700 POS Terminal

1900 Remittance Delivery Points

2.12 Regulatory & Legal Compliance

The bank complied with the requirements of following regulatory and legal authorities:

The Bank Companies Act, 1991

The Companies Act, 1994

Rules and Regulations issued by Bangladesh Bank

The Securities and Exchange Rules, 1987

The Securities and Exchange Ordinance, 1969

The Securities and Exchange Commission Act, 1993

The Securities and Exchange Commission (Public Issue) rules, 2006

The Income Tax Ordinance, 1984

The Vat Act, 1991

BRAC Bank has a strong and active management department. The department is divided in 19 divisions which have sub-divisions and many more features. Each of the divisions is now discussed briefly below.

3.1 Small Medium Enterprise ( SME ) Banking Division

SME Banking division of Brac Bank Limited has ascertained with the specter to establish itself as the market leader in SME financing and to assist country’s economic development, serving different productive and contributing sectors in a focused way by mobilizing fund from urban to rural areas. In line with BRAC Bank’s vision, the SME Banking division’s objective is to achieve a two folded bottom line i.e. to build a profitable organization by contributing to the society as well as the economy through creation of an entrepreneur class in the society eventually eliminating poverty from the country. The deposit collected through the branches of BRAC Bank, which are mostly located in urban Bangladesh, are distributed nation wide to small & medium entrepreneurs through our dedicated SME unit offices located across the country.

Lifting the country’s banking practices to a newer dimension, BBL has introduced a challenging platform wherefrom, it serves a customer base, which, previously was not acquainted with banking products & services along with the micro finance graduates who were in dilemma with regard to the access of credit towards enhancement of their business activities further. BRAC Bank Limited is the first bank to address the needs of “missing middle” in a focused way. BBL attempts not only to provide financial products and services to this segment but also help them to be educated & get aware, so that it can be easier for them to acclimatize themselves with the ever changing business world. BRAC Bank has brought a momentous change in the lifestyle of their clients and has significant economic and social contribution in poverty alleviation by upgrading the standard of living by generating employment. According to a research, BRAC Bank has contributed in generating more than 6,00,000 jobs over the last five years.

SME Banking division has so far covered 113,00 customers mark and is fully dedicated to boost the customer base by reaching the doorsteps of small and medium enterprises involved in different business sectors and located in different parts in 64 districts of the country . Brac Bank has long been serving the fund requirements of traders, manufactures, importers, traders, suppliers and distributers, women entrepreneurs and other service providers like medical institution & educational institutions in a focused way. SME Banking division has also introduced a unique way of reaching the clients, spread throughout the country with 2000 efficient & dedicated people deployed in 392 unit offices.

SME Banking division’s core competency is a combination of providing loans that are collateral free and offering a service that is quick, prompt and without any hassle. By doing this, the SME Banking division has helped to create a social revolution in the banking industry and also has served those who were not bankable to other banks. At present The SME Banking division of BRAC Bank Ltd. Offers collateral free loans up to BDT 10 Lacs or US$ 14,000. As of 2007, the SME loan portfolio stands at BDT 1,908 crore or US$ 272.57 million out of which approximately 95% is collateral free. SME Banking division is actively involved in providing facilities to the sectors that were mostly underserved by the banking sector and has enabled these borrowers to enjoy banking facilities instead of borrowing money from local moneylenders at extremely high rates.

In 2007, BRAC Bank has excelled in SME Banking operation in almost the same volume that it has achieved from 2002 to 2006. The exceptional growth has been possible for continuous support of the stakeholders.

Brac Bank’s SME Banking is continuing its journey of serving the MSE’s as can be observed from the tremendous growth in client base by 88% from 2006 to 2007. The strength of BRAC Bank’s SME Banking division behind the success of growth is as follows:

Dynamic Human Resource

Countrywide distribution network & coverage

Continuous development in creating innovative products

Unique loan approval process & monitoring

Robust risk management system

Till 2006 the bank was a SME lender, but from 2007 onwards BRAC Bank Limited took a deliberate strategic approach to be the SME banker. Hence, The bank has participated in countrywide road shows and has entered into strategic alliance with national & international chamber bodies to build awareness and opted to provide with both deposit & loan products along with various other Banking services coupled with state of art & technology.

Now that the Bank has expanded its businesses across the country, the need has arisen for a segment-oriented approach to SME Banking. The different niches within the same market need to be approached individually. Therefore, SME Banking division of BRAC Bank has well equipped itself with market focus units, with exclusive products & new strategies to serve varying banking requirement of the diverse Small & Medium Enterprises across the country specially the funding part.

3.1.1 Women Entrepreneur Cell (WEC)

Women Entrepreneur Cell (WEC), one of its kinds in the banking industry of Bangladesh, was launched in 2006 under SME Banking division with an objective to offer access to formal finance along with training and technical assistance to the women entrepreneurs across the country. Women entrepreneurs were overlooked by the traditional banking sector, although they are sincere to repay, makes proper utilization of credit facilities and portray better repayment behavior as has already been proved in Micro Credit Programs. BRAC Bank is the pioneer to understand the need and credit requirement of this underserved sector, which has long been deprived of funding in a focused manner and thus instigated this business unit with “PROTHOMA RIN”, a customized loan product.

In the small span of operation, WEC has already satisfied the financial need of 1,343 women entrepreneurs throughout the country. Women Entrepreneurs Cell (WEC) has excelled incredible in BRAC Bank is the pioneer in the banking industry of Bangladesh to conduct a need based training for women entrepreneurs through its Central Training Department as was committed by the WEC. In addition, WEC has organized training programs in collaboration with other trade bodies and institutions like Dhaka Chamber of Commerce and Industries (DCCI), Junior Chamber International Bangladesh (JCI) etc.

3.1.2 Manufacturing Business Unit (MBU)

As a nation matures from an under-developed to a developing country, the needs to satisfy its demand with available resources also increase. Thus a manufacturing sector develops gradually and the nation turns from a trading-based economy to a manufacturing-based economy.

The Bank has identified Manufacturing Enterprises as a potential niche and launched the Manufacturing Business Unit in August 2007 under SME Banking division. The objective of launching this unit is to better serve the manufacturing sector by providing sector-focused loan & other services with regard to financial needs as well as addressing any other needs of this sector such as training facilities & advisory services.

3.1.3 Commercial Credit Unit (CCU)

The Commercial Credit Unit (CCU) was launched in October2007 with the sole objective of providing financial services in the Trade Finance sector. As many existing clients of SME Banking are importers and have taken SME loans from the bank, the objective of CCU is to provide them with a one-stop banking service along with providing them with pre & post import facilities.

All these products are part & parcel of a composite facility known as “Trade Plus”, a specially designed product for the import oriented business for import & incurring day to day expenses.

3.1.4 Supplier & Distributer Finance (SDF)

The significance of linkage industry is inevitable for proper functioning of trading & manufacturing concerns. Linkage industry extensively contributes in manpower creation, economic development & financial acceleration. Creating a fresh financial market for this sub-sector is simply a diversification of the banking product. Due to this reason, BRAC Bank has moved into this area from September, 2007 as a part of new business development.

Supplier & Distributer Finance unit was launched by introducing “Super Supply Loan”, a customized & composite facility of both overdraft & revolving limit for small & medium sized suppliers. BRAC Bank Limited proved its success in global SME financing sector by becoming one of the four most profitable and sustainable SME banks in the world, rated by Council of Microfinance Equity Funds (CMEF), USA following a global research. The other three renowned banks are Bank Rakyat Indonesia (BRI), Bank Compartamos (Mexico) and Equity Bank (Kenia). The success of SME Banking division extensively depends on the customer’s success in achieving goal with the required & timely assistance.

SME Banking division is confident enough to continue it’s over increasing growth to take the bank ahead of its imagination and to erect newer and startling milestones in banking industry.

SME Network Coverage of BRAC Bank

3.2 Retail Banking Division

“Retail Banking Unit” has further strengthened its position as a major channel of business by stretching its horizon with its unique offer of personal banking across the country. This unit takes foremost funding responsibility of the bank and is committed to offer multifarious services to entire customer base of the bank through Branch’s Alternative delivery channels, Premier banking services and literally Retail banking products to doorsteps through Direct Sales force.

The year 2007 marked as a series of exciting events and achievements for retail banking unit. At the very onset, the year started with the challenge of establishing a new core banking software platform and Retail team played a very vital role to make the ‘FINACLE’ implementation a big success in all branch networks across the country.

3.2.1 Retail Distribution

“Retail Distribution” unit takes care of all branch activities, this unit ensured a seamless operation in all b ranches throughout the year and also organized inauguration of 10 new Branch’s ; 2 in Dhaka, 1 in Chittagong and rest 7 in Barishal, Bogra, Dohar, Monohordi. Tongi, Potiya & Cox’s Bazar. Out of these 10 new branch’s 6 branch’s started operation in urban areas in different divisions / districts and 4 branch’s in different rural areas. This thoughtful placement of branch’s helped Retail Distribution team to offer a total banking solutions and services through its facilities to customers of these new regions. BRAC bank now has a total of 36 branch network in the country.

Ensuring convenience for our valued customers always had been a priority to the management and in 2007, 3 major branch’s were relocated to convenient locations. These are Gulshan branch in Dhaka, Agrabad branch in Chittagong and Sylhet Milleneum branch in Sylhet. The new premises are quite spacious with extended facilities which ensure comfort to our valued clients.

“Retail Distribution” also initiated evening banking facilities in three more branchs last year. Mirpur & Uttara in Dhaka and Moulovibazar in Sylhet. Response from respective neighborhood was observed to be overwhelming.

3.2.2 National Sales’ Initiative

“National Sales” under Retail drives entire direct sales force for bringing in new business for the bank. This unit took a number of initiatives to create opportunities for people from all sectors to bank with BRAC Bank Limited. Some of the initiatives are briefed below :

Door to Door campaign in Monohordi, Potiya, Tongi, Halishahar neighborhood

Tie up with ‘Global Brand (Pvt) Limited’ to offer consumer loans at discounts for purchase of personal computer, laptop

Arranged road shows at different corporate bodies

Tie up with car showrooms for joint promotion

A phenomenal growth in terms of new customers was registered by Retail team and a graphical comparison of last 3 years is given below:

3.2.3 New Products

Some new products and special business offers were also designed from Retail National Sales unit, these are:

ECO – a special package for salaried individuals working in multinational and local corporate bodies

“Quick Loan” was another brainchild from National Sale’s unit, this product was designed for businessman to meet their immediate needs

“Medical Loan” was launched to arrange loans for people going abroad for treatment.

3.2.4 Non Funded Business & TRS

Non Funded Business (NFB) unit under “Retail” concentrates on fee income for the bank. This unit runs a student centre where from all student files are processed for onward remittances for the purpose of studying abroad. This unit a MOU with VFS and IOM and through this agreement, all visa processing fees of a number of foreign embassies are being collected by this team in Dhaka, Chittagong and Sylhet. Its worth to be mentioned here that BRAC Bank is the only nominated bank in Bangladesh which may receive UK visa fees.

Travel Related Services (TRS) is a new venture which was introduced as a wing under Non Funded Business of Retail Banking.TRS is launched with the aim to provide a one stop travel solutions and to cater to the needs of the traveling class of the country, with a parallel objective to improve the sales of FCY / TC of the bank. Strategic partnerships were made with top travel agencies of the country and through them, a fast, hustle-free service to our clients being ensured. TRS team, in partnership with leading travel operators, is equipped with online air and hotel reservation system, experienced travel guides and visa processing counselors for our clients convenience. “Travel Loan” specially designed for travelers has also been relaunched which can be availed up to BDT 3 Lacs at a very affordable rate. The services provided through TRS centers are :

Travel Loan

Visa Processing / Expediting

Air Ticketing

FYC / TC endorsement

Hotel reservations

Tourism package

3.2.5 Premium Banking

“Premium Banking” unit ensures service excellence to highnetworth (HNW) customers of the bank through a team of dedicated Relationship Managers. This unit is committed to offer personalized services to HNW customers and arranges home delivery services at customer doorstep. Relationship Managers suggest appropriate investment opportunities to Premium customers and ensures a mutual benefit.

3.2.6 Alternative Delivery Channel

“Alternative Delivery Channel” has been created to facilitate 24 hours cash transactions and other enquiry services throughout the year customers. This unit offer options for customers to use self operated electronic channels – ATM (Automated Teller Machine) and CDM (Cash Deposit Machine) of the bank to do cash deposits and withdrawals at any hour of the day. Alternative Delivery Channels drives operations of all ATM’s and CDM’s, Phone banking, SMS banking and Internet banking. In 2007, a large number of ATM’s and CDM’s were added to BRAC Bank’s network and the numbers are as below:

Number of ATM’s in 2006 – 22

Number of CDM’s in 2006 – 05

New ATM’s in 2007 – 32

Mew CDM’s in 2007 – 09

Total Number of ATM’s in 2007 – 54

Total Number of CDM’s in 2007 – 14

Total volume of cash dispensed through ATM’s in 2007 – 953.70 crore

Average volume of dispensed per ATM (@ 54 ATM’s) – 17.66 crore

Average volume of cash dispensed through ATM’s per day in 2007 – 2.61 crore

Total volume of cash received through CDM’s – 71.70 crore

Average volume of cash received per CDM (@ 14 CDM’s) – 5.12 crore

Average volume of cash received through CDM’s per day in 2007 – 19.64 crore

3.2.7 Phone Banking

Phone Banking is another important unit under Alternative Delivery Channel (ADC) which became n essential part of account relationship immediate after opening of personal accounts. Major services that are being offered through Phone Banking are :

Activation of cheque book and ATM card

Account balance

Last few transactions

Cheque book requests

Stop payment of cheque and ATM / Debit cards etc.

3.2.8 SME Banking

This is a unique facility for customers to enquire their account balance, last few transactions etc through their cell phone. Customers also receive SMS information’s on following occasions:

Any transaction exceeding 1 lac

On maturity of fixed deposit

3.2.9 Service Quality

Of many deliverables, “Retail” concentrates mostly to ensure ‘Service Excellence’ across all points of services, initiates regular research works through “Service Quality Unit” and tailors superior service propositions for valued customers. Some remarkable initiatives of Service Quality Unit are briefed below for perusal:

Campaign “Say Yes” among branch teams helped to create a very positive and pro active attitude in handling customer queries in branch’s

“World Class Customer Service Training” helped to increase service skills of branch officials

“Service Quality Unit” designed dress code for front line officers working in branch’s

Apart from the above-mentioned initiatives, service quality department is involved in solving customer complaints, customer queries and regular performance evaluation of front line employees through Score Card and Co-coordinating Mystery Shopping survey al the year round.

3.3 Corporate Banking Division

Being a major business unit of the bank, Corporate Banking division has been playing a significant role to achieve the overall objectives of the bank. Since the starting, the division is continuously striving to provide more customer focused products for its valued corporate clients. In this process, the division has segmented itself into various units which cater the associated customer segment. The year 2007 will be marked as a milestone for the Corporate Banking division as it has financed several large projects in this year. Last year, Corporate has been the lead arranger of several big syndicated financed loans and also it has attained significant expertise in Cash Management and Corporate Liabilities. Corporate Banking helps its customer to fulfill their objectives by carefully listening and analyzing their ideas, providing necessary expertise and composite products. The business unit operates through the following five major wings:

Structured Finance

Local Corporate Unit

Leasing & Instruction Unit

Medium Enterprise unit

Cash Management & Corporate Liabilities

3.3.1 Structured Finance

BRAC Bank is equipped with technical expertise to provide one stop solution for Large Scale Project finance. Its aim is to provide the right partnership for successful project implementation. This section arrange fund from banks / financial institutions through syndication. As Lead Arranger, the bank provides service for documentation. Execution and administration of the syndicated finance. Besides, Structure Finance unit provides the following services to its clients:

Corporate Advisory Service

Debt Raising

Quasi Equity Instruments

Equity Participation

Project Counseling

3.3.2 Local Corporate Unit

Local Corporate Unit focuses on end-to-end services as per large corporate clients, mid-sized companies, and international trade finance businesses and institutional customers and government entitles / agencies demand. It offer a wide range of products and services, technologies to leverage them anytime, anywhere and the expertise to customize them to client-specific requirements.

Our dedicated Team of Relationship Managers along with wholesale Operation unit, Extensive Line of Corresponding Banking Network support client’s local and international business by meeting Working Capital / Team Loan requirements as well as export and import financing. The bank emphasize on providing full-length services and products covering from suppliers to the ultimate consumers of our Corporate Clients.

3.3.3 Leasing and Institutions Unit

The Leasing and Institutions Unit furnishes financial solutions for all institutions and provides lease financing facilities for all corporate bodies. Its products offerings are suited to fast and timely availability of credit facilities to serve purposes of acquiring capital machineries, equipments and vehicles among others. Despite the apparent rigorousness of lease financing its product portfolio caters to customers funding for institutions. In view of the fact that not all of its target customer institutions are slowly aimed towards profit maximization but has significant impact on the development of the economy. Its target market segments including NGOs and other development organization, health service, industry, Non banking financial institutions, Micro finance institutions and educational institutions along with other corporate bodies that require support for building their business infrastructure. It believes in building long lasting relationship with its clients by collaborating in the journey to their growth and not just overseeing it.

3.3.4 Medium enterprise Unit

Medium Enterprise Unit serves medium enterprises having facility requirements alike large corporate in nature, but in smaller volumes. In order to reach specific market segments the unit has designed products like CommerZ loan, Supplier Finance, MFI Receivables Finance, Light Engineering Finance etc. Its clientele can be proprietorship concerns, private limited companies suppliers of corporate houses, chain super shops, educational institutions as well as NGOs.

Facilities may include fund based like overdraft, short term loan, revolving loan, term loan, lease finance, LATR, bill discounting etc or non fund based like letter of credit (L/C) and letter of guarantee as well as composite credit facility that includes various corporate products. At present, Medium Enterprise Unit has a solid clientele base with a portfolio mix of about 100 crore funded facilities and 25 crore non-funded facilities.

3.3.5 Cash Management & Corporate Liabilities

Cash Management & Corporate Liabilities unit under corporate Banking division provides corporate fund management solutions along with a number of investment opportunities to large corporate clients. It offer tailored cash management solutions like NCS (Nationwide Collection Solution), PTS (Payment Transfer Solution), Mobile Banking Services, Cash Pick Up Services and bill collection solutions through its own and correspondent branch network and through different alternative delivery channels as per clients requirement and specification. Within a very short span of time, its cash management unit has established themselves in the market by providing cash solution to large FMCGs, Telecommunications companies, NGOs and different Governmental Organizations. In addition to Cash Management solutions, its liability has also introduced different long and short run investment products for large and medium business enterprises.

3.4 Probashi Banking Division

2007 has been an eventful year for SRS. Remittance Services in 2007 has turned out to be one of the core business area of the bank. The year remained as a rewarding and successful one in terms of new tie-ups and partnerships with a focus on pursuing unexplored and niche markets around the globe. 4 new partnerships have been added to the list of SRS affiliated Exchange Companies in this year. Association with international renowned banks like ICICI bank and Bank of Ceylon are also major accomplishment of the year 2007.

With a goal to provide fast and expeditious services to deliver remittances even in the most remote corner of Bangladesh, the network of electronically connected field officers have been expanded more than 1200 BDP outlets across the country for remittance payment.

An array of products and services have been introduced targeting the non-resident Bangladeshis living in different parts of the world, a milestone for BRAC Bank as to becoming the pioneer in such operation. The official launching of Probashi Shubidah Account took place on 16 January, 2007 with a perspective to catering the beneficiaries of NRB customers with their different banking needs. SRS had also launched TT arrangements through Sonali Bank in Bangladesh, which has added to our options in making the fastest remittance in Bangladesh.

In March 2007, an open-air concert was organized jointly by BRAC Bank and Western Union Money Transfer to endorse the remittance facility in Singapore. A road show was organized along with Western Union all over the country from the month of May 2007 to September 2007 as a promotional campaign to promote the newly added BRAC BDP locations as part of the wide coverage of BRAC Bank for processing Western Union transactions. This year, BRAC Bank has been also chosen as a western Union distribution network in Bangladesh. Secure remittance service of BRAC Bank, made strategic alliances with two other private banks – Dhaka bank on 13 may, 2007 and First Security bank on 17 September, 2007 as its subagents of processing Western Union transactions.

SRS counter branding at the departure lounge of ZIA International Airport had been done this year. This unique branding had yield huge visibility at this key national installation and lifted the corporate image immensely. This branding at ZIA has been the biggest branding effort of BRAC Bank so far as it is estimated that annually 3 million (approx.) travelers are using ZIA International Airport for traveling.

Overseas deployment of two employees from SRS team of BRAC Bank had been initiated in this year. One of them was deployed to Singapore on March, 2007 and other was to Italy on August, 2007 to promote BRAC Bank – Western Union remittance tie-up in the respective countries.

Brac Bank had been considered as the market leader in terms of Western Union payouts with approximately 50,000 transactions in the month of December, 2007 among 13 agents and subagents in Bangladesh. This has honored BRAC Bank as one of the three largest WU agents in South Asia. In the end of the year2007, SRS participated in first ever NRB conference held in Bangladesh and was the main sponsor of the Painting Exhibition during the event.

3.5 Card Division

February 6th, 2007 marks the beginning of BRAC Bank’s Credit cards Business. Being the latest entrant into the cards market, the card division’s greatest challenge was to publish itself in an already demanding marketplace and create its own niche. In a space of a year, BRAC Bank today has become the fastest growing issuers of credit cards in Bangladesh.

Staying true to our motto of being the bank of the masses it has successfully managed to penetrate and enlist a large segment of the middle class society who has adopted the plastic card as part of their everyday life.

With an aim to becoming the credit card of choice, regular product innovations and value added services round the year ensured acquisition of new users and also aided in retention of existing clients. Aggressive promotional and brand building campaigns have created a niche that serves to distinguish Brac bank Credit Card from the competition,

Dedicated and well defined organizational verticals allow efficient and quick turnaround of all internal and external challenges. Acquiring, Sales, portfolio, Product development, Customer Services and Collection wings forms an effective cards team to create a positive and lasting impact in the Credit Card market of Bangladesh.

3.6 Treasury & Financial Division

Treasury department is vested with the responsibility to measure and minimize the risk associated with bank’s liquidity, foreign exchange exposure and asset liability management. Treasury continuously monitors price movements of foreign exchange and uses various hedging techniques to manage its open position in such a way that minimizes risk and maximizes return.

The Asset Liability Management (ALM) desk provides country economic analysis, balance sheet gaps, ALM ratios and many other findings before the ALCO.

The Financial Institutions (FI) wings works as the trigger point of establishing new relationship with correspondent banks as well as to maintain the existing relationship to provide a smooth funding channel for all business units.

3.6.1 Summary of performance of Business Division – Treasury & FI

Brac Bank’s treasury is well equipped with modern telecommunication infrastructure facilities like SWIFT, Reuters, Bloomberg, Internet, Voice Recorder etc. recently it successfully implemented Kastle, a treasury software which is one of the top ranked software for treasury functions from 3i InfoTech. Bank’s independent Dealing Room is committed to provide best rate / price to its customers. A centralized operation with on-line connectivity facilities its customer to avail fast and efficient service. BRAC Bank is a very active player in inter-bank call money and fx. market. It is one of the major suppliers of foreign currency in the inter-bank fx. market. Money market maintains the portfolio of Call & Term, Govt. & Private Securities, equity Investment, Repo & reverse Repo bank’s account while maintaining CRR & SLR. Fx. dealers quote very competitive cross currency spot, forward and swap rates to its customers while complying with Bangladesh Bank’s Foreign Exchange Risk Management Guidelines. BRAC Bank Has clearly demarcated Front Office, mid office and Back office having separate reporting lines, as per international best practice of treasury management and core risk management guidelines of Bangladesh Bank. The Front office involves in dealing activities, Mid office monitor rate appropriateness and any breach of limit while the Back office is responsible for all related process, support and settlement functions.

BRAC Bank has a dedicated team for Asset Liability Management. Recently they implemented Kastle, ALM software from 3i InfoTech for their rigorous analysis and forecasting the market behavior and to provide useful information before the ALCO. The ALM team monitor and present before ALCO the country’s overall economic position, Bank’s Liquidity position, ALM ratios, Interest Rate Risk, Capital Adequacy, deposit Advance growth, Cost of deposit & Yield on Assets e.g. Gap, Market Interest Rate and deposit and lending pricing strategy. The ALM team is also responsible for complying all regulatory requirements related with asset liability management. BRAC Bank has a strong worldwide correspondent network with the world’s leading 20 banks to facilitate trade, remittance & other services to its client efficiently and profitably. BRAC Bank also maintains about 477 accounts with 13 local banks to support its Small & Medium Enterprise (SME), Probashi Banking Services (PBS) & Cash Management business throughout the country.

3.7 Central Operations Division

Central Operations is the warden of all kinds of loan securities of the valued customers of BRAC bank. It is a single point of contact of all loan documents and securities. Central Operations supports business and other operational units through its following arms:

Loan Archive

Reconciliation

Data Control

Regional Operating centre

There are some major endeavors of Central Operations. They are as followed :

Reconciliation of Financial Transactions

Post Disbursement Monitoring

Safe Keeping of loan files after due checking

Performing of clearing activities

Data validation and monitoring

Release of securities on demand

3.8 Financial Administration Division

Financial Administration Department Has the responsibility of doing financial planning and management, chart of A/C and control, budgeting, planning, cost management and ensures financial control across the bank. It also generates and disseminates all forms of internal and external financial reporting, regulatory reporting and all business MIS.

3.9 General Infrastructure Division

General Infrastructure services (GIS) plays the pivotal role to ensure all kind of infrastructure support services for the bank. This department consists of six functional units namely Infrastructure Development, Infrastructure Management, Operations, procurement, Logistics and Small & Medium Enterprise administration Unit. With the combined roles and responsibilities of all these units, GIS is actually the execution point for all administrative related activities including the development of infrastructure setups for new Head Office Premises, Branch, ATM Booths, and Sales Center for BRAC Bank Limited all over the country.

3.10 Credit Division

In order to minimize credit risk, BBL has formulated a comprehensive credit policy according to Bangladesh Bank Core Risk Management guidelines. Credit policy of the bank provided for the separation of the credit approval function from business / marketing and loan administration function. Credit policy of BBL recommended thorough credit assessment and risk grading of all clients at the time of approval and portfolio review. Credit policy also provides thee guidelines of required information for credit assessments, marketing strategy, approval process, loan monitoring, early alert process, credit recovery, NPL account monitoring, NPL provisioning and write off policy etc. The board of directors reviews the credit policy of the bank annually.

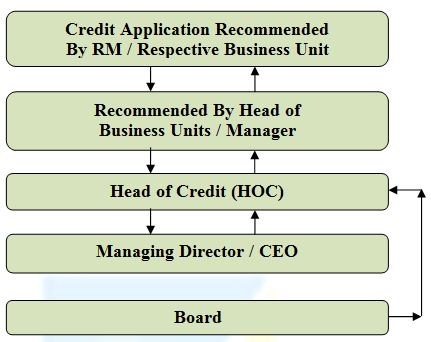

3.10.1 Approval Process

Previously in the approval process, the bank had a Credit Committee consisting of four members, Managing Director & CEO, Deputy Managing Director & COO, Head of Corporate Banking & Head of Credit for approval of credit proposals. Later on, as per Bangladesh Bank credit Risk management (CRM) observations it has dissolved the Credit Committee and set the delegation of authority at individual level, duly approved by the board. Under BBL approval process, the activity of credit has been segregated as follows:

1. Relationship Manager (RM) / Direct Sales Executives / Customer relationship Officer prepares the loan proposals and submits for recommendation from Head of Business Units / Respective managers.

2. Head of Business Units / Managers place it to credit division for their approval / recommendation.

3. After proper assessment of loan proposal by credit division, Managing Director Approves / recommends as per delegated authority by the board.

4. Managing Director presents the proposal before board.

5. Board advises the decision.

The following diagram illustrates the existing approval process:

3.10.2 Sanctioning

Due to increase in business volume and for ease of operations, the bank has delegated approval Authority to individual underwriters (by name) within Credit Division for Retail, SME , Cards and Corporate Credit.

3.10.3 Processing

1. For smooth operations & reduction turn around time of approval process, the bank has initiated a web based (software) approval system parallel with its existing one. Through this approval system, BBL also wants to ensure the CRM guidelines on segregation of duties and responsibilities of business units from approval authority to maintain quality of portfolio. This will take over the existing paper based system immediately.

2. The bank has introduced a Central Verification Unit to support the verifications of data provided in the loan applications especially for Retail Credit & Credit Card.

3. Pre-approval visit by independent officer of Risk Management Department is mandatory for each proposal under SME unit. Approver only approves after receiving the visit report. This report has come into effect from the beginning of 2007 which verifies the authenticity of SME borrowers’ loan application individually.

3.10.4 Monitoring

A guideline namely “manual of Monitoring process for Managing Corporate and Medium Enterprise Portfolio” for core risk areas of BBL has been developed for continuous monitoring of corporate and medium enterprise borrowers. It helps continuous watch over of the loan including borrower’s compliance with approval terms, account performance of the client, identifying early signs of irregularities. The monitoring phase has been divided in to three broader categories i.e. Pre-disbursement phase, Disbursement Phase, Post-disbursement Phase. The following tools & techniques have been developed for managing credit portfolio of the bank:

1. Portfolio Review: In the time of portfolio review (2 times in a yr), factory / business visit & physical verification of stock should be conducted. Portfolio review should be conducted with updated information on the borrower’s financial & business conditions including review of – account performance, utilization of limit, financial stability, deviation from terms & conditions & security lapses, credit grading, CIB status etc. In the event of any deterioration the ratings are immediately revised as recommended by credit division.

2. Early Alert Report: Early alert process is an effective tool & technique that will help the bank in detecting any deterioration in clients account and trigger out problem accounts at early stage so that proper attention can be given to avoid any losses.

3. As part of monitoring, continuous monitoring of utilization of fund, timely repayment, monthly stock report verification, weekly reporting of status of cheque placement (cheque dishonored) of the clients, frequent client visits, visiting mortgaged properties at least once in a six-monthly period.

4. A robust technical support has been developed to monitor the Retail and SME credit to reduce the overdue by generating automated reminder litter. BBL also formed an MIS team to support monitoring by providing a vast MIS reports.

5. Review large exposures to a single client / group and portion of it being non-performing are conducted regularly.

6. Review sector-wise exposure, ensure portfolio diversification, identify sectors having high rate of NPL and provide special attention during the review.

7. Risk Management Department conducts audits of all credit files, security documents and provides an independent assessment of the quality of the asset portfolio.

8. Rating Review: As part of portfolio monitoring, review has been done on credit exposure on the basis of risk grade by credit division. Adequate trend and migration analysis also conducted to identify any deterioration in credit quality.

3.10.5 Recovery

The conducted RM / CRO / Ro / Officers of CCU are responsible to monitor and recover irregular loans. The concerned RM / CRO / Ro / Officers of CCU supported by Credit Division directly monitor the accounts with sustained deterioration. Bank may identify and subsequently transfer EXIT accounts graded 4-5 for efficient exit based on recommendation of credit and respective business unit. Whenever an account is downgraded, the primary functions for credit division with respective business unit are:

Determine Account Action Plan / Recovery Strategy

Pursue all options to maximize recovery

Ensure adequate loan loss provisions are made based on actual & expected losses

Regular review of grade 6 or worse accounts

Impaired Asset management (IAM) has been established to take care of Non-Performing Loans (NPL) of Corporate, SME & Retail with their approved policy guidelines, which deals legal matters & recovery process. Accounts Downgraded to 6 and above should be assigned to “Impaired Asset management (IAM)” for initiating legal action with recommendation from Credit Division and respective business unit and approved by Managing Director, who is responsible for coordinating and administrating the action plan / recovery of the account and should serve as the primary customer contact after the account the account is downgraded to substandard. However, to expedite the recovery, some NPL account of SME & retail have also been given to outsource agency in fully commissioned basis.

3.10.6 Pricing

Loan pricing on various lending categories will depend on the level of risk and type of security offered. During product pricing exercise, rate of interest is determined only after assessing the risk. The higher the risk, the higher the interest rate is. Interest rate may be reviewed at least once in 6 months and more often whenever is appropriate. Fixed interest rate should be discouraged. Generally interest rates vary with fluctuation of cost of funds based on a spread for profit. All pricing of loans however has relevance with the market condition and determined by Asset Liability Management Committee (ALCO) from time to time. However, for each corporate loan proposal, there should be a separate and unique pricing on the basis of risk grading and other relevant factors with proper justification.

3.11 Consumer Service Delivery (CSD)

Consumer Service Delivery (CSD), an integral part of the bank’s business, complement the ever-flourishing retail business through account opening, customer statement generation, inter-banking cheque clearing, ATM & credit card production, cheque book production and processing government bonds. CSD continually aspire from retail business growth which saw the department expand significantly over 2007 in line with the growth attained by retail business in terms of personnel and activities. The year highlighted 8, 50,000 inter-bank clearing cheque processing, 1, 32,000 new account opening and more than 7, 16,000 account statement generation. In addition, CSD also produced 32,000 cards. There has been an overall expansion of 24% in the department in terms of activities than that of 2006. The new technology platform FINACLE introduced in 2007 has enabled centralized Consumer Service Delivery with on-line connectivity provide fast and efficient services. In its endeavor to facilitate business, the department initiated the processing and servicing of term-deposits as centralized function for all businesses that would support retail banking achieve its goal of breaking the barriers. To supplement the business target of 2008 and consolidate as fastest growing bank in the industry, CSD initiated the outsourcing of its major non-core functions such as data entry, cheque book personalizing & MICR coding and account statement generation. Keeping with the vision of the bank, CSD is entering the New Year by incorporating all retail operations and services including loan processing under a singular umbrella and announcing itself as Retail banking Operations.

3.12 Enterprise Risk Management (ERM)

Enterprise Risk Management (ERM) is a new dimension for BRAC Bank Ltd. ERM will set risk management strategy across the enterprise, designed to identify potential events that may affect the organization and manage risk to be within its risk appetite to provide reasonable assurance regarding the achievement of organizational objectives.

The management committee approved the ERMC policy, which contains the guidelines for reporting to Risk Management Committee. The ERMC has twelve members:

Head of Risk Management

Managing Director & COO

Head of Retail

Head of SME

Head of Credit

Head of Treasury

Head of Financial Administration

Head of HR

Head of Corporate Banking

Head of SRS

Head of External Affairs

Head of Impaired assets Management

Head of Risk Management chairs the committee.

The ERMC meet on 15th of every month. The committee discusses about the various issues raised relating to previous month and updates the same provided by units reported to Risk management department in the prescribed formats by 7th of the current month. The units qualify the specific risk according to the matrix provided by Bangladesh Bank. The meeting minutes are reviewed by the Board Audit Committee on quarterly basis.

As corporate governance BRAC Bank Limited, the fastest growing bank in Bangladesh, is apprehended regarding risky areas, which are being identified by the Risk Management department. The Management under the guidance of the Board of Directors has developed an Enterprise Risk management Department separately to manage bank’s overall risk.

3.13 ALCO

BRAC Bank formed Asset Liability Management Committee (ALCO) headed by the Managing Director & CEO. All the business heads along with Head of ERM, Head of Credit & Head of Regulatory & Internal Control are member of this committee. The committee evaluates the economy and market situation, money market & fund position, capital adequacy, deposit-advance position, deposit mix of the bank, different ALM ratios, interest rate risk, foreign currency maturity gap, forecasted fund position, cost of deposits & yield on advances, deposit-lending pricing strategy etc. ALCO generally meets once in a month however, special ALCO meeting can be held if deemed necessary.

3.14 Regulatory & Internal Control Division

Operating in a Banking industry BRAC Bank is exposed to many sectors of the economy. Since the very beginning the bank has adopted a policy to manage and mitigate its risk factors. BRAC Bank ahs adopted Core Risk Management guideline provided by the Bangladesh Bank as per BRPD Circular no. 17 of 7 October, 2003 and best practices in the global banking industry. In current centralized environment of operation, entire control mechanism of the bank wrapped around various departments and their sub wings. Thus the control mechanism in BRAC Bank is much stronger and reengineering the process faster than any other decentralized bank. The main objective of our Regulatory & Internal Control function to put the bank in a balanced position of Risk & Return, and no Risk should be unidentified and non-calculative.

The objective of managing and mitigating risk factors derives the bank to adapt new ideas and technology. Recently the ban had moved to a new structure, where activities of managing risk are further broken down. Regulatory & Internal Control department has been restructured to focus more on regulatory issues and internal mechanism.

Regulatory & Internal Control functions ensures subject related to regulatory bodies are handled correctly. Being in the middle of Regulatory bodies and internal departments; it serves as a connection between Regulatory and the bank. All correspondent, reports, returns are sent to the regulatory bodies through this department. An Internal Control and Compliance unit under Regulatory & Internal Control department has been formed to ensure that controls are in place at every operational level of the bank. The Internal Control & Compliance and Monitoring Department undertakes periodic and special review of the branches and departments of the corporate office for identifying and correcting operational lapses. The audit committee of the board also reviews the audit and inspection reports of the Internal Control & Compliance unit. The bank introduced risk based internal audit and audit ratings for its branches. A comprehensive audit manual has been prepared by Regulatory & Internal Control department, which has been approved by the board and has already circulated to the branches for meticulous compliance. Other than regular control activities, Fraud and forgeries are also investigated through department. Identified loopholes are immediately closed. Simultaneously, the bank set up a policy to manage its Core Risk factors. Such as:

Credit Risk

Asset Liability Risk

Foreign Exchange Risk

Internal Control & Compliance Risk

Money Laundering Risk

Information technology (IT) Risk

Minimization and Mitigation measures of all core risk factors are adopted by the concerned department of the bank. Among the core highlighted risks Regulatory & Internal Control function checks the following Risks:

3.14.1 Internal Control & Compliance Risk

Internal Control function ensures the bank manages its Internal Control & Compliance risk in accordance to the guidelines of Regulatory bodies and bank’s it self’s. These risks are defined as unexpected loss, consequential loss derived from human error, loop holes in the operational procedure, fraud and forgeries and technology failure. These risks are inherent in all activities of the bank. The Internal Control system of the bank enforces checks in all possible ways to minimize risk exposure towards internal factors. This system ensures all the departmental process and procedure are as per guideline provided and also maintains ethical standards, accounting rules. And efficiency in business process and safeguarding of assets are ensured.

Internal Control & Compliance function consist of an audit and inspection process. The bank has placed audit procedure in its day to day activities. All departments and branches are audited periodically and instant recommendations are provided to concerned department and branch. These audit reports are submitted to the Board Audit Committee and Board of Directors. Moreover all our SME loans are audited prior disbursement. All SME loans are distributed on the conformity of the auditor upon verification of the validity of data provided in account and loan documentation.

3.14.2 Money Laundering Risk

Money Laundering can be defined as breach of the regulation and being negligent in the prevention on money laundering. As per guidelines of Bangladesh Bank, Head of regulatory & Internal Control has been nominated as the Chief Anti Money Laundering Compliance Officer (CAMLCO); Branch Managers are as Branch Anti Money Laundering Compliance Officer (BAMLCO). BAMLCO’s throughout all its branches monitors all accounts and transactions with an established procedure of Know Your Customer (KYC), Transaction Profile (TP), Cash Transaction Report (CTR), Suspicious Transaction Report (ATR) and so on. KYC update process for its legacy accounts is in place. All branch personnel of the bank are trained on Prevention of Money Laundering procedure and process. In line with the objective the bank towards prevention of money laundering all the relevant departments are instructed to be vigilant and prevent such activities. The bank also conducts training programs and regular workshops for developing awareness regarding ANTI MONEY LAUNDERING.

3.15 Company Secretariat

One of the significant developments in the corporate sector throughout the country is the Company Secretariat department of the company. Company Secretariat works as the bridge between policy and implementation. The duties of Company Secretariat are related with some legal, mandatory and ministerial responsibilities bound by the statue and managerial and administrative responsibilities.

Company Secretariat is the flow line of all information to and from the Board of Directors. In the age of free economy, Company Secretariat maintains a clear and distinct relation and liaison among investor, financiers, bankers, donors. Correspondent and many others of the market economy.

The Company Secretariat of the BRAC Bank Limited is engaged to perform with a vital role in the management. There are two wings of Company Secretariat:

1. Board Secretariat: Board Secretariat is the vital wing of Company Secretariat. One of the main tasks of the Board Secretariat is to convene, conduct and conclude meeting of the Directors and Shareholders. Company Secretariat of BRAC Bank Limited also maintains public relationship with specialized bodies like the Stock Exchange, Securities and Exchange Commission, Investment Corporation of Bangladesh, different banks, Register of Joint Stock Companies & Firm, Bangladesh bank etc.

2. Share Division: Share Division is directed under the Board Secretariat. The activities of Share Division are involved with Share Management of the BRAC Bank Limited. The Share Division maintains all statutory registers related shareholder. It also maintains relationship with the ordinary shareholders answers their quarries and assists them.

3.16 Impaired Assets Management Division

Impaired Assets Management is a new concept in the banking arena. Impaired Assets Management (IAM) department of BBL is playing a pivotal role in managing Non Performing Loan (NPL) and Written Off Loan Portfolio of BRAC Bank and maintaining its Portfolio At Risk (PAR) at a low level.

Basically IAM department takes legal steps against classified loan defaulters of the bank. IAM reduces NPLs through deploying third party recovery agencies and lawyers, amicable settlements with defaulters, arrangements for auctions of mortgaged properties etc. separate segments of IAM department are engaged to monitor and follow-up NPLs of different business unit. These legal and recovery processes are done under BRAC Bank IAM policy and Bangladesh Bank guidelines.

3.17 Information Technology Division

For BRAC Bank, technology is the silent strength behind its wide array of products and its 24/7 service delivery capabilities. In 2007, BRAC Bank embraced a number of best-in-class technology platforms that will ensure seamless behind the scenes support for its rapid growth. BRAC Bank’s technology partners are some of the most renowned companies in the world.

BARC Bank follows the guideline dated in BRPD Circular no. 14, dated 23 October 2005 regarding “Guideline on Information and Communication Technology for Scheduled Banks”. IT operation management covers the dynamics of technology operation management including change management, asset management and operating environment procedures management. The objectives are to achieve the highest levels of technology service quality by minimum operational risk.

In order to ensure that information assets are protected against risk, there are controls over:

Password

User Id maintenance

Input

Network Secuÿÿty

Data Encryption

Virus Protection

Internet & e-mail

The Business Continuity Plan (BCP) is formulated to cover operational risks and taking into account the potential for wide area disasters, data center disasters and the recovery plan. The BCP takes into account the backup and recovery process.

The BRAC Bank technology infrastructure now supports real time, online transactions between 36 branches for over 4,57,126 customers throughout Bangladesh. Steps are also underway to automate the 392 SME unit offices of the country to bring about further efficiencies and economies of scale.

As it’s unique to truly broad-based and participatory electronic banking system in Bangladesh, BRAC Bank has sponsored OMNIBUS – a shared ATM network that covers 141 ATMs locations for customers of 15 banks.

BRAC Bank’s Eldorado initiative, a proposed private sector nationwide remittance and payment system, was awarded a grant under the Remittances and Payments Challenge Fund (RPCF), an initiative jointly supported by Bangladesh Bank and the department.

3.18 PSRM Division

Project Strategy & Review Management (PSRM) is a new concept that deals with project administration and plays a pivotal role in coordinating and forecasting BRAC Bank driven projects. Assuring service quality as well as determining segment wise operational Risk exposure is another endeavors of this department generating Operational MIS to track and supervise operational as well as organizational growth also encircles the functions of PSRM.

3.19 Human Resources Division

Human Resources Division plays a very important role in BRAC Bank. Managing almost 44oo employees is a challenging task and HRD is trying their best to do it in an efficient manner. Besides day-today operational works, HRD arranges two large recruitments each year for their Customer Relations Manager & Management Trainee Officer programs. Maintaining co-ordination among unit offices and branches all over Bangladesh is a big issue of HRD. HRD is trying to move towards automation for all HR processes. Two new models for E-Learning & E-Attendance have been introduced in the year 2007. Reward & Recognition Program, Employee Satisfaction Survey and other programs all around the year help to generate motivation and feedback from the employees.

3.19.1 Human Capital

The biggest asset of BRAC Bank is its human resource. To support the fastest growing bank in the country, HRD always striving to employ the right candidate. The bank employs permanent as well contractual staffs and trains them all around the year through in-house, local and foreign training to prepare them to face and deliver their job efficiently and effectively. In the year 2007 HRD trained 2091 employees through 156 training programs. Almost 82% of the regular employees have been trained when they join the bank which is later followed by need based training. It also organizes specialized and advanced training programs as well as foreign trainings for the potential employees and future leaders of the bank. The manpower of BRAC Bank is as follows:

Particulars 2006 2005 2007 2004

Numbers of Employees 3047 1650 4428 1216

HRD is also acting as a strategic business partner constantly with the business units in order to achieve the projected growth of bank and in order to peruse the vision with the right blending of ethical commitments; we have created some core internal value which is called CRYSTAL all together. CRYSTAL is for:

C = Creative

R = Reliable

Y = Young

S = Stable

T = Transparent

A = Accountable

L = Loyal

3.20 Marketing & Corporate Affairs

Marketing & Corporate Affairs takes care of all forms of marketing and corporate communication, brand management, promotional activities, public relations and CSR activities. Brac banc aims to be the most preferred brand in its category and the Marketing and Corporate Affairs department works towards realizing that ambition.

BRAC bank is a socially responsible organization with an obligation to consider the interests of customers, employees, shareholders, communities and ecological considerations in all aspects of its operations. This obligation is seen to extend beyond its statutory obligation to comply with legislation. In line with vision of BRAC Bank, CSR is closely linked with the principles of sustainable development, which argues that it should make decisions based not only on financial factors such as profits or dividends, but also based on the immediate and long-term social and environmental consequences of its activities.

As a part of its Corporate Social responsibility BRAC Bank donated $38,252 to ICDDR, B for the renovation of a temporary shed that was thronged with diarrhea patients soon after the recession of flood water of last year. A Co-Branded Credit Card was also introduced to maintain an ongoing support for ICDDR, B.

BRAC Bank employees have made a contribution of TK 1.35 million equivalents to their one-day’s salary to BRAC for its countrywide flood relief and rehabilitation activities in August, 2007

BRAC Bank has sponsored the 2nd National Women Entrepreneur Conference 2008, where women entrepreneurs from all over Bangladesh have participated to attend in the workshops and knowledge sharing activities undertaken by SME Foundation of Bangladesh.

To assist Bangla Academy with their publication and research and development initiatives, BRAC bank has lent their support to carry forward their projects. Also BRAC bank has supported in stall preparation and beautification of ‘Amor Ekushey Boi Mela 2008’, this initiative was taken to make the fair enjoyable for participations as well as the visitors.

To conserve nature and alleviate the illegal slay of immigrant birds, BRAC Bank has sponsored ‘Pakhi Mela 2008’ organized by Jahangirnagar University.

Six new immigration counter of Zia International Airport is established for outgoing passengers by BRAC bank with proper branding and computer assistant to mitigate the time of passengers. A Probashi information counter has been installed for the wage earners who can gather information about sending foreign remittance to Bangladesh.

BRAC bank took an initiative to stand by the SIDR affected people of Barishal & Khulna with relief. A number of employees distributed dry food, water, clothes, medicine etc. among the SME borrowers.

A donation of TK. 1 million was made to an art exhibition of ‘Shako’ – a 12 women artist organization. The total money collected by selling the paintings was donated to ‘Apon Drug Rehabilitation Center’.

To encourage and create awareness on SME development of Bangladesh, BRAC Bank has sponsored AMDIB forum organized by Institute of business Administration (IBA). This forum has helped the participants to share views, get key insight and discussed about the ways to alleviate problems faced by SME entrepreneurs, while seeking financial support.

BRAC bank has also supported annual fund raising program of SAARC Women’s Association Dhaka to support and assist Islamia Eye Hospital and Dhaka Shishu Hospital for operation and treatment.

To support the humanitarian endeavors of Rotary International like polio plus program, cancer detection unit, drug abuse and HIV/AIDS advocacy, Brac Bank has sponsored a conference organized by Rotary International.

As a part of its corporate policy BRAC bank does not provide any financial support to any environmentally hazardous or child labor exploited company.

3.21 Audit Committee

The Audit Committee of BRAC bank Limited was formed by the Board of Directors of the Bank in associated with the BRPD Circular # 12 , dated December 23, 2002 of Bangladesh Bank and the notification of Securities & exchange Commission Notification No. – SEC/CMRRD/2006-158/ADMIN/02-08, dated February 20, 2006.

The Audit Committee of BRAC bank Limited is compromised of two members of the Board of Directors, Managing Director and the Company Secretary. The audit committee sits once in every two months. The composition of present Audit Committee is as under:

Mr. Muhammad A. (Rumee) Ali : Chairman

Mr. Md. Aminul Islam : Member

Mr. Kaiser Tamiz Amin : Member

Mr. Rais Uddin Ahmed : Observer

The purpose of the audit committee is to ensure and to improve the adequacy of internal control system of the company’s operations and to assist the board in discharging its responsibilities towards the shareholders of the company.

The Audit Committee evaluates the adequacy and effectiveness of the internal control system based on the existing policies. This committee ensures a sound financial reporting system and provides the updated information to the Board of Directors. The committee is empowered to examine the matter relating to the financial and other affairs of the company. The objectives of the Audit Committee are to assist the Board of Directors mainly in the following areas:

To ensure compliance with all applicable legal and regulatory rules and regulations imposed by the Regulatory bodies

To review on the Statutory and special auditor’s report and to ensure compliance and regularization of recommendations made by the external and special auditors

To inform to the board of Directors on fraud forgeries and other irregularities found and to ensure to prevent the same

To develop an adequate information technology and MIS system and to establish sufficient control system in IT operations for protecting in any adverse situation