1.1 Background

This report is a part of our Management Information System (MIS-405). The topic of the report is “Electronic Commerce [e-commerce] used in the banking service of Bangladesh”. The report focuses on the private banking service in our country. We have been told to choose any one of the private banks operating in our country, irrespective of its origin. We chose the Jamuna Bank Limited for our report.

1.2 Origin

The course instructor of Management Information System (MIS-405) Ms. Ayesha Jahan orally authorized the task of writing this report to a group of five students. We proposed Jamuna Bank Limited as per the requirements of report completion. Our course instructor approved the topic of our report. Groups were independently formed about the report.

1.3 Purpose

This report has tried to fulfill the formal procedures to write a report. The purpose of the report is to show what the effect of electronic commerce is in the banking sector of Bangladesh. It is a major part of our course requirement. Learning about Management Information System practice into the contemporary business organization is one of the most important parts of our course.

1.4 Scope of the study

In our report, we briefly discussed about banking industry of Bangladesh and management information system into the banking industry. The findings of this

report includes both the current industry situation and the management information system into the Jamuna Bank. In the report, we started with the discussion of banking industry of Bangladesh and later we give our finding regarding management information system of the Jamuna Bank and some recommendation to improve to improve the mechanism of management information system into the organization to provide better customer value to its clients.

1.5 Limitations

Whenever we tried to collect any information about Management information of banking industry in Bangladesh and management information system of Jamuna Bank Limited, we faced a lot of problems. They did not give us much time about this topic. So there is some lacking in our information. One more important limitation for preparing the report was time. If we had some more time, we could have prepared the report much better than we did.

1.6 Sources and methods of collecting data

The methodology followed in this report is based on both primary & secondary sources. The required information for the introductory and descriptive part has been collected by:

- Discussing and briefing by the course instructor

- Discussing with the employees of the company

- Searching web-sites

2.0 Banking Industry Overview:

The Jews in Jerusalem introduced a kind of banking in the form of money lending before the birth of Christ. The word ‘bank’ was probably derived from the word ‘bench’ as during ancient time Jews used to do money –lending business sitting on long benches. First modern banking was introduced in 1668 in Stockholm as ‘Svingss Pis Bank’, which opened up a new era of banking activities throughout the European Mainland. In the South Asian region, the Afgan traders popularly known as Kabuliwallas introduced early banking system. Muslim businessmen from Kabul, Afghanistan came to India and started money-lending business in exchange of interest sometime in 1312 A.D. They were known as ‘Kabuliawallas’.

The number of banks in all now stands at 49 in Bangladesh. Out of the 49 banks, four are Nationalised Commercial Banks (NCBs), 28 local private commercial banks, 12 foreign banks and the rest five are Development Financial Institutions (DFIs).

Sonali Bank is the largest among the NCBs while Pubali is leading in the private ones. Among the 12 foreign banks, Standard Chartered has become the largest in the country. Besides the scheduled banks, Samabai (Cooperative) Bank, Ansar-VDP Bank, Karmasansthan (Employment) Bank and Grameen bank are functioning in the financial sector.The number of total branches of all scheduled banks is 6,038 as of June 2000. Of the branches, 39.95 per cent (2,412) are located in the urban areas and 60.05 per cent (3,626) in the rural areas. Of the branches NCBs hold 3,616, private commercial banks 1,214, foreign banks 31 and specialised banks 1,177.

Bangladesh Bank (BB) regulates and supervises the activities of all banks. The BB is now carrying out a reform programme to ensure quality services by the banks.

- · BB

- · NCBs

- · PCBs

- · Specialized Banks

3.0 Jamuna Bank Limited

Jamuna Bank Limited (JBL) is a Banking Company registered under the Companies Act, 1994 with its Head Office at Chini Shilpa Bhaban, 3, Dilkusha C/A, Dhaka-1000. The Bank started its operation from 3rd June 2001.

Jamuna Bank Limited is a highly capitalized new generation Bank with an Authorized Capital and Paid-up Capital of Tk.1600.00 million and Tk.390.00 million respectively. The Paid-up Capital has been raised to 429.00 million and the total equity of the bank stands at 725.00 million as on June 30, 2005. Currently the Bank has 35 (Thirty Five) branches: 14 in Dhaka, 6 in Chittagong, 2 in Gazipur, 3 in Sylhet, 1 in Bogra, 2 in Naogaon, 1 in Munshigang, 1 in Shirajganj, 1 in Rajshahi and 1 in Narayanganj (including Nine Rural Branches).

The Bank undertakes all types of banking transactions to support the development of trade and commerce of the country. JBL’s services are also available for the entrepreneurs to set up new ventures and BMRE of industrial units.

Jamuna Bank Ltd., the only Bengali named new generation private commercial bank was established by a group of winning local entrepreneurs conceiving an idea of creating a model banking institution with different outlook to offer the valued customers, a comprehensive range of financial services and innovative products for sustainable mutual growth and prosperity. The sponsors are reputed personalities in the filed of trade, commerce and industries.

The Bank is being managed and operated by a group of highly educated and professional team with diversified experience in finance and banking. The Management of the bank constantly focuses on understanding and anticipating customers’ needs. The scenario of banking business is changing day by day, so the bank’s responsibility is to device strategy and new products to cope with the changing environment. Jamuna Bank Ltd. has already achieved tremendous progress within only Seven years. The bank has already ranked at top of the quality service providers & is known for its reputation.

Jamuna Bank offers different types of Corporate and Personal Banking Services involving all segments of the society within the purview of rules and regulations laid down by the Central Bank and other regulatory authorities.

The operation hour of the Bank is 9:00 A.M. To 5:00 P.M. from Sunday to Thursday with transaction hour from 9:00 A.M. to 3:00 P.M. The Bank remains closed at Friday and Saturday including government holidays.

3.1 STRATEGIES

| • | To manage and operate the Bank in the most efficient manner to enhance financial performance and to control cost of fund |

| • | To strive for customer satisfaction through quality control and delivery of timely services |

| • | To identify customers’ credit and other banking needs and monitor their perception towards our performance in meeting those requirements.

|

| • | To review and update policies, procedures and practices to enhance the ability to extend better service to customers. |

| • | To train and develop all employees and provide them adequate resources so that customers’ needs can be reasonably addressed. |

| • | To promote organizational effectiveness by openly communicating company plans, policies, practices and procedures to employees in a timely fashion |

| • | To cultivate a working environment that fosters positive motivation for improved performance |

| • | To diversify portfolio both in the retail and wholesale market |

| • | To increase direct contact with customers in order to cultivate a closer relationship between the bank and its customers. |

3.2 VISION:

To become a leading banking institution and to play a pivotal role in the development of the country.

3.2 MISSION:

The Bank is committed to satisfying diverse needs of its customers through an array of products at a competitive price by using appropriate technology and providing timely service so that a sustainable growth, reasonable return and contribution to the development of the country can be ensured with a motivated and professional work-force.

3.3 OBJECTIVES

| • | To earn and maintain CAMEL Rating ‘Strong’ |

| • | To establish relationship banking and improve service quality through development of Strategic Marketing Plans. |

| • | To remain one of the best banks in Bangladesh in terms of profitability and assets quality. |

| • | To introduce fully automated systems through integration of information technology. |

| • | To ensure an adequate rate of return on investment. |

| • | To keep risk position at an acceptable range (including any off balance sheet risk). |

| • | To maintain adequate liquidity to meet maturing obligations and commitments. |

| • | To maintain a healthy growth of business with desired image. |

| • | To maintain adequate control systems and transparency in procedures. |

| • | To develop and retain a quality work force through an effective human Resources Management System. |

| • | To ensure optimum utilization of all available resources. |

| • | To pursue an effective system of management by ensuring compliance to ethical norms, transparency and accountability at all levels. |

3.4 The Management

| Managing Director Mr. Mohammed Lakiotullah Additional Managing Director Mr. Motior Rahman Deputy Managing Director Mr. Abdus Salam Mr. Md. Alauddin Al-Azad Senior Executive Vice President Mr.Md. Rafiqul Islam Mr. A.K.M. Rasshiduzzaman Executive Vice President Mr.Md. Yunus Ali Senior Vice President Mr. Shahedul Alam Khan Mr. Mirza Elias Uddin Ahmed Mr. A. K. M. Saifuddin Ahamed Ms. Nur-E-Jannat Begum; Mr. Mahbubul Huq Choudhry Vice President Mr.Md. Nazmul Hossain Mr. Khorshed Ahmed Nayeem Mr.Md. Zobaidul Islam Mr.Md. Elias Ali Akanda Mr. Manzurul Ahasan Chowdhury Mr. Fazlul Jalal Mr. Mahboob Alam Choudhury Mr. Mokhlesur Rahman Senior Assistant Vice President Mr. Amir Uddin Chowdhury Mr.Md. Belal Hossain Mr. Ahmed Nawaz Mr. Khandaker Zia Hassan Mr. Monsur-Uz-Zaman Mr. Zashim Uddin Mr.Md. Mostafizur Rahman Mr.Md. Abdur Rahim Mr. Abdul Hamid Chowdhury Mr. A.K.M. Shah Alam Mr.Md. Nazrul Islam Mr. Manjurul Hasan Mr.Md. Mohtasinul Hoque |

3.5 BranchNetwork

Motijheel Branch, Dhaka

Mohakhali Branch, Dhaka

Sonargaon Road Branch, Dhaka

Moulvibazar Branch, Dhaka

Dhoalikhal Branch, Dhaka

Banani Branch, Dhaka

Ashulia Branch, Dhaka

Goala Bazar Branch, Sylhet

Agrabad Branch, Chittagong

Dilkusha Branch, Dhaka

Beani Bazar Branch, Sylhet

Sylhet Branch, Sylhet

Shantinagar Branch, Dhaka

Gulshan Branch, Dhaka

Dhanmondi Branch, Dhaka

Nayabazar Branch (Islamic Banking), Dhaka

Mohadebpur Branch, Naogaon

Naogaon Branch, Naogaon

Khatunganh Branch, Chittagong

Konabari Branch, Gazipur

Bhatiyari Branch, Chittagong

Foreign Exchange Branch, Dhaka

Jubilee Road Branch (Islamic Banking), Chittagong

Chistia Market Branch, Dhaka

Baligaon Branch, Munshiganj

Bashurhat Branch, Noakhali

Rajshahi Branch, Rajshahi

Shirajganj Branch, Shirajganj

Bahddar Hat Branch, Chittagong

Mawna Branch, Gazipur

Kadamtali Branch, Chittagong

Kushtia Branch, Kushtia

Dinajpur Branch, Dinajpur

3.6.1 Corporate Banking:

The motto of JBL’s Corporate Banking services is to provide personalized solutions to our customers. The Bank distinguishes and identifies corporate customers’ need and designs tailored solutions accordingly.

Jamuna Bank Ltd. offers a complete range of advisory, financing and operational services to its corporate client groups combining trade, treasury, investment and transactional banking activities in one package. Whether it is project finance, term loan, import or export deal, a working capital requirement or a forward cover for a foreign currency transaction, our Corporate Banking Managers will offer you the accurate solution. Our corporate Banking specialists will render high-class service for speedy approvals and efficient processing to satisfy customer needs.

Corporate Banking business envelops a broad range of businesses and industries. You can leverage on our know-how in the following sectors mainly:

- Agro processing industry

- Industry (Import Substitute / Export oriented)

– Textile Spinning Dying and printing

– Export Oriented Garments, Sweater.

– Food & Allied

– Paper & Paper Products

– Engineering, Steel Mills

– Chemical and chemical products etc.

- Telecommunications.

- Information Technology

- Real Estate & Construction ·

- Wholesale trade

- Transport · Hotels, Restaurants ·

- Non Bank Financial Institutions

- Loan Syndication ·

- Project Finance · Investment Banking

- Lease Finance · Hire Purchase · International Banking ·

- Export Finance

- Import Finance

3.6.2. Personal Banking:

Personal Banking of Jamuna Bank offers wide-ranging products and services matching the requirement of every customer. Transactional accounts, savings schemes or loan facilities from Jamuna Bank Ltd. make available you a unique mixture of easy and consummate service quality.

We make every endeavor to ensure our clients’ satisfaction. Our cooperative & friendly professionals working in the branches will make your visit an enjoyable experience.

Deposit Accounts

Q-Cash Round the Clock

Jamuna Bank Q-Cash ATM Card enables you to withdraw cash and do a variety of banking transactions 24 hours a day. Q-Cash ATMs are conveniently located covering major shopping centres, business and residential areas in Dhaka and Chittagong. ATMs in Sylhet, Khulna and other cities will soon start be introduced. The network will expand to cover the whole country within a short span of time.

With your Jamuna Bank Q-Cash ATM card you can:

- Cash withdrawal Round The Clock from any Q-Cash logo marked ATM booths.

- POS transaction (shopping malls, restaurants, jewellaries etc)

- Enjoy overdraft facilities on the card (if approved)

- Utility Bill Payment facilities

- Cash transaction facilities for selective branches nationwide

- ATM service available in Dhaka and Chittagong Withdrawal allowed from ATM’s of Jamuna Bank Ltd., AB Bank, The City Bank, Janata Bank, IFIC Bank, Mercantile Bank, Pubali Bank, Eastern Bank Ltd. respectively

- And more to come Is Q-Cash

Is Q-cash Secure?

Yes, Q-Cash is fully secure. Q-Cash cardholders can only carry out transactions on Q-Cash ATMs with Personal Identification Numbers (PIN). The PIN is a unique 4-digit number that allows you to access your account. You can change your PIN anytime from ATM machine. In case you have lost your card, transactions cannot be done without the PIN.

Jamuna Bank Limited has installed its first Q-cash ATM at Dhanmondi Branch, Dhaka.

Jamuna Bank is going to issue VISA card soon.

In line with the issuance of Q-cash products JBL is going to introduce VISA card very soon.

3.6.3 International Trade Finance:

International Trade forms the major business activity undertaken by Jamuna Bank Ltd. The Bank with its worldwide correspondent network and close relationships with key financial institutions provides an extensive trade services network to handle your transactions efficiently. Personnel experienced in International Trade Finance staff our key branches in Dhaka, Chittagong, Sylhet and Naogaon. These offices are the focal point for processing import and Export transactions for both small and large corporate customers. We offer a complete range of Trade Finance services. Our professionals will work with you to develop solutions tailored to meet your requirements, through mobilizing our full range of trade services locally, and drawing on our global resources. We can offer you professional advice on all aspects of International Trade requirements, namely:

- Issuing, advising and confirming of Documentary Credits.

- Pre-shipment and post-shipment finance.

- Negotiation and purchase of Export Bills.

- Discounting of Bills of Exchange.

- Collection of Bills. Assist customers to insure all risks.

- Foreign Currency Dealing etc.

List of Foreign Correspondents

To provide International Trade related services we have established Correspondent Banking relationship with 336 locations of 106 world reputed Banks in more than 100 countries.

Main Correspondent Banks are:

Citi Bank N.A., Standard Chartered, American Express Bank, Bank of New York, Bank of Nova Scotia, Duetche Bank, Dresdner Bank AG, Habib American Bank, Habib Bank AG Zurich, Bayerische Hypo Vareins Bank, Mashreq Bank PSC, Nordea Bank AB, Royal Bank of Canada, UBS AG, Union De Banques Arabes ET, Francaises, Wachovia Bank NA, Forties Bank S.A/NV, Svenska Handlesbanken, Bank of Ceylon, Banca Toscana, ABN Amro Bank, Commonwealth Bank of Australia, Danske Bank A/S. Absa Bank Ltd., Agricultural Bank of Chaina, Banca Intesa SPA, Banca Italo Albanese, Banca Popolare Commercio E Industria SPA, Bank Austria Credittanstal AG, Bank Commonwealth, Bank Madiri (Europe), Bank of Cyprus, Bank of Bahrain and Kuwait, Bank of Jordan Ltd., Bank Sadarat Iran, Blue Nile Bank, Commercial Bank of Kuwait, Commercial Bank of Qatar Ltd., Development Bank of the Philippines, Dexia Bank SA, EON Bank Berhad, First International Merchant Bank PLC., Foreign Trade Bank of North Korea, Foreign Trade Bank of Vietnam, Hiroshima bank, HVB, Hungary RT, ICICI Bank Canada. Industrial and Commercial Bank of China, ING Bank NV, Islamic Bank of Yemen and for Finance & Investment, Korea Exchange Bank, National Commercial Bank, Shinhan Bank, State Bank of India (Canada) UFJ Bank Ltd., United Bank of India, Bank of Bhutan, Allied Bank Philippines.

3.6.4 Foreign Remittance:

Jamuna Bank Ltd. has a network of 19 branches in Bangladesh and 4 more branches are going to be added to network soon.

Remittance services are available at all branches and foreign remittances may be sent to any branch by the remitters favoring their beneficiaries.

Remittances are credited to the account of beneficiaries instantly through Electronic Fund Transfer (EFT) mechanism or within shortest possible time.

Jamuna Bank Ltd. has correspondent banking relationship with all major banks located in almost all the countries/cities. Expatriate Bangladeshis may send their hard earned foreign currencies through those banks or may contact any renowned banks nearby (where they reside/work) to send their money to their dear ones in Bangladesh.

To facilitate sending money in Bangladeshi Taka directly, Jamuna Bank Ltd. has Taka Drawing Arrangement with many banks/exchange companies in different countries. The expatriate Bangladeshis may send their money in BDT through the branches/subsidiaries of Jamuna Bank Ltd.

3.6.5 Credit Facilities:

Interest Rates of Loans & Advances

|

3.6.6 Shop Finance Scheme

Objectives:

01. To enable the small business community to run the business smoothly

02. Facilitating expansion of the existing businesses

03. To improve the banking habit of self employed persons

04. To diversify bank’s lending to Small & Medium Enterprises (SME) which are considered as less risky and help community developments. It may be noted down that the government is also encouraging investment in SME sector.

Categories of eligible business:

i) Grocery/departmental/whole sale store

ii) Confectionary/bakery (owned by the bakers)

iii) Stationary shops

iv) Cloth materials & small local garment traders

v) Shoe makers/shops

vi) PVC & plastic product traders/small manufacturers

vii) Tiles/sanitary items retailers

viii) Computer/Photostat/Cyber Café.

ix) Electrical & electronic items retailers

x) Pharmacy

xi) Gift shop/cosmetics shops

xii) Restaurant/fast food joints

xiii) Hardwire shops

xiv) Glass/ceramic retail outlets

xv) Sports kit retailers

xvi) Photo studio

xvii) Rod, Cement & C.I. Sheet (Tin) Shop

xviii) Engineering Workshop

xix) Fertilizer & Pesticide shop

Maximum Loan Amount:

1) Up to a maximum of 10.00 lac in single case or 60% of possession value (distress value to be considered) whichever is lower. However, loan size will depend on creditworthiness of the borrower and the decision of the sanctioning authority.

2) Branch Manager must verify the amount of possession money actually paid before recommending such proposal.

Tenure of the loan limit:

Minimum 01 year – Maximum 03 years from the date of disbursement of the loan

Eligibility criteria:

The applicant must fulfill the following criteria to be eligible for loans and advances under the scheme:

i) Shop owner must run the establishment himself, having at least three years of successful business experience

ii) Valid lease deed for a minimum period of 03 years up to 05 years

iii) Satisfactory conducted deposit account with JBL for minimum 03 months.

iv) To deposit the daily sales proceeds in the account maintained with JBL

v) Agree to abide by credit rules & regulations of JBL

vi) Furnishing net-worth of the applicant/client.

vii) Clean CIB

viii) The bank reserves the right to accept or reject any application without assigning any reason whatsoever.

ix) The intending borrower /loanee shall apply through the letter head of the business firm or through a plain paper requesting the branch manager for sanction of loan under the Shop Finance Scheme

Security:

i) Simple deposit of valid lease deed of agreement of the shop.

ii) A tripartite agreement to be signed in between leaseholder/shop owner/Bank- to the effect that the leaseholder cannot rent out or transfer the leased property without the written consent of the Bank.

iii) The lease deed between the landlord and the borrower must be duly executed & the original lease deed should be kept in the Bank as part of document.

iv) Lease must contain provisions enabling the landlord to forfeit the lease and enable the bank to enforce a right to sell the possession of the shop to liquidate the default debt (if any).

v) Letter of disclaimer by the landlord to facilitate the bank to liquidate the default loan (if any)

vi) Equal numbers of post dated cheques covering amount of each loan installment

Insurance

All borrowing customers’ inventory i.e. Stock-in-trade will be insured against Fire, Rsd & other risks with the Bank’s mortgage clause cost of which will be borne by the shop owner/client/borrower.

Repayment Schedule:

Repayment schedule should be as under:

i) In case of 01 year, 10 monthly installments for the loan limit up to Tk. 3.00 lac with 02 month grace period from the date of disbursement

ii) In case of 02 year, 22 monthly installments for the loan limit up to Tk.6.00 lac with 02-month grace period from the date of disbursement

iii) In case of 03 year, 34 monthly installments for the loan limit above Tk.6.00 lac with 02-month grace period from the date of disbursement

3.6.7 Lease Finance

Lease means a contractual relationship between the owner of the asset and its user for a specified period against mutually agreed upon rent. The owner is called the Lessor and the user is called the Lessee.

Lease finance is one of the most convenient source of financing of assets viz machinery, equipment vehicle, etc. The user of the assets i.e. Lessee is benefited through tax advantages, conserving working capital and preserving debt capacity. Moreover, Lease is an off-balance sheet item i.e lease amount is not shown in the balance sheet of the lessee and does not affect borrowing capacity.

Leasing enables the lessee to avail the services of a plant or equipment without making the investment or incurring debt obligation. The Lessee can use the asset by paying a series of periodic amounts called “lease payment” or “lease rentals” to the owner of the asset at the predetermined rates and generally in advance. The payments may be made monthly or quarterly.

Jamuna Bank Ltd., the highly capitalized private Commercial Bank in Bangladesh has introduced lease finance to facilitate funding requirement of valued customers & growth of their business houses.

Lease Items

· Vehicles like luxury bus, Mini bus, Taxi cabs cars, Pick-up, CNG three wheeler etc.

· Factory equipment.

· Medical equipment

· Machinery for Agro Based Industry

· Construction equipment

· Office equipment

· Generators, Lift & Elevators for commercial place.

· Sea or River Transport.

Computer for IT EducationCenter.

3.6.8 Trading of Government Treasury bond & Other Govt. Securities

Jamuna Bank Limited has been nominated as a Primary Dealer by the Bangladesh Bank for trading 5 years & 10 Years Treasury Bonds and other Government Securities.

Eligibility criteria:

(i) Individuals and institutions resident in Bangladesh, including provident funds, pension funds, bank and corporate bodies shall be eligible to purchase the BGTBs.

(ii) Individuals and institutions not resident in Bangladesh shall also be eligible to purchase the BGTBs, with coupon payment and resale/redemption proceeds transferable abroad in foreign currency subject to fulfillment of conditions as mentioned in the Bangladesh Govt. Treasury Bond Rules-2003.

2. Loan facility:

JBL offers loan upto 95% of the present value of the bond/other securities against lien of the above instrument for their customers.

4.0 E-commerce in Jamuna Bank Limited:

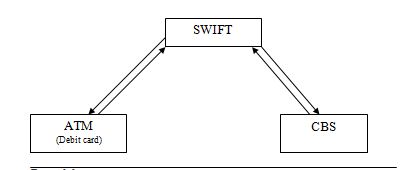

How ATM systems work?

N.B: CBS refers to ‘core banking systems’.

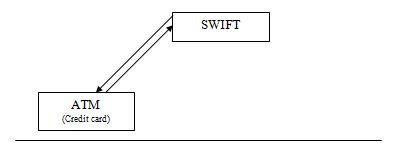

This diagram shows us how Debit card works. When any customer insert ATM card into machine, the system will connect with SWIFT and SWIFT send the information to the CBS [Core Banking System]. Again CBS send the return information to SWIFT and swift confirm it to ATM machine. Finally, customer can withdraw the money. The credit card does the same function except the SWIFT doesn’t make any query to CBS. Rather, the function works between ATM and SWIFT, since the credit limit is fixed before into the SWIFT server by the authority. This function is well illustrated by the following diagram:

JBL customer can access their VISA card into 8 authorized Banks booth. They are:

- TRUST BANK

- IFIC

- JANATA BANK

- MERCANTILE BANK

- AB BANK

- EBL

- NATIONAL BANK

- PUBILI BANK

They do not start true Internet banking yet. But they have tested this system through return dent server. They did it successfully. They will apply it very soon. Through this facility customer can view their balance and the particular transaction by particular banks website. But there is some limitation, such as government rules (for instance: Money laundering act) to initiate this.

They will introduce SMS banking very soon.

4.1 Phone banking

Jamuna Bank has phone-banking facility. They give a secret password to their client. Through this code customer can quarry their balance.

4.2 SME Banking

Jamuna Bank has SMS banking facility. They give a secret password to their client. Through this code customer can quarry their balance form a particular cell phone that is given by the customer.

4.3 SWIFT:

Jamuna Bank Limited is the member of SWIFT (Society for Worldwide Inter-bank Financial Telecommunication). SWIFT is a member owned co-operative, which provides a fast and accurate communication network for financial transactions such as Letters of Credit, Fund transfer etc. By becoming a member of SWIFT, the bank has opened up possibilities for uninterrupted connectivity with over 5,700 user institutions in 150 countries around the world.

SWIFT No.: JAMUBDDH

4.4 Q-Cash Round the Clock:

Jamuna Bank Q-Cash ATM Card enables you to withdraw cash and do a variety of banking transactions 24 hours a day. Q-Cash ATMs are conveniently located covering major shopping centres, business and residential areas in Dhaka and Chittagong. ATMs in Sylhet, Khulna and other cities will soon start be introduced. The network will expand to cover the whole country within a short span of time.

With your Jamuna Bank Q-Cash ATM card you can:

- Cash withdrawal Round The Clock from any Q-Cash logo marked ATM booths.

- POS transaction (shopping malls, restaurants, jewellaries etc)

- Enjoy overdraft facilities on the card (if approved)

- Utility Bill Payment facilities

- Cash transaction facilities for selective branches nationwide

- ATM service available in Dhaka and Chittagong Withdrawal allowed from ATM’s of Jamuna Bank Ltd., AB Bank, The City Bank, Janata Bank, IFIC Bank, Mercantile Bank, Pubali Bank, Eastern Bank Ltd. respectively

- And more to come Is Q-Cash

Is Q-cash Secure?

Yes, Q-Cash is fully secure. Q-Cash cardholders can only carry out transactions on Q-Cash ATMs with Personal Identification Numbers (PIN). The PIN is a unique 4-digit number that allows you to access your account. You can change your PIN anytime from ATM machine. In case you have lost your card, transactions cannot be done without the PIN. Jamuna Bank Limited has installed its first Q-cash ATM at Dhanmondi Branch, Dhaka. Jamuna Bank is going to issue VISA card soon.In line with the issuance of Q-cash products JBL is going to introduce VISA card very soon.

4.5 Online Banking:

Jamuna Bank Limited has introduced real-time any branch banking on April 05, 2005. Now, customers can withdraw and deposit money from any of its 35 branches located at Dhaka, Chittagong, Sylhet, Gazipur, Bogra, Naogaon, Narayanganj, Dinajpur, Kushtia,Rajshahi, Bashurhat, Sirajganj and Munshigonj. Our valued customers can also enjoy 24 hours banking service through ATM card from any of Q-cash ATMs located at Dhaka, Chittagong, Khulna, Sylhet and Bogra.

All the existing customers of Jamuna Bank Limited will enjoy this service by default.

Key features:

- Centralized Database

- Platform Independent

- Real time any branch banking

- Internet Banking Interface

- ATM Interface

- Corporate MIS facility

Delivery Channels:

- Branch Network

- ATM Network

- POS (Point of Sales) Network

- Internet Banking Network

Jamuna Bank Limited, for its online banking activities support use software provided by the company Flora Limited. The name of the software is ‘flora online banking software’. If any one want to use online banking they will provide his provided some charges due to access online banking is applicable to the clients shore and that is 50 tk per lakh. (Both for withdrawn and deposit of money.). The Q –cash facility of the bank give opportunity to its clients to use total of 253 booths. The bank offering credit card facilities and the credit card limit to its holder is upon the status and financial capability of the credit card holder. Recently, the bank is offering dual currency VISA card. Its issuing changes are $50 and the system will charge $1.5 for per transaction. There are some limitations that the company personnel delivered to the interviewer that are as follows for using the ATM services:

- Machine hang,

- Take time to solve this problem (Approximately).

- Linking network down,

- Electricity problem, without electricity it is not usable for service.

5.0 Problems

Jamuna Bank Limited is ready to implement Internet banking facilities. But due to following things are considered to be obstacles to implement these concerns:

a) Rules and regulation of Bangladesh Bank to implement Internet Banking facility like (Money laundering act)

b) User security concern.

c) Lack of skilled employee.

d) Customer and client’s awareness and skill to implement Internet banking system and its facilities.

5.1 Prospects:

Since the world is moving toward electronic based facilities to achieve economic advantages, Internet banking system is the term to be greatly concerned by the authority of the bank. Albeit, there exist some problems mentioned above, but it is clear if it is successfully launched, both the clients and the organization will be equally benefited from using the Internet facility into the banking service system.

| Online Banking Launching Ceremony held at Hotel Sheraton on April 2005 |

| Opening of Online Banking Services of Jamuna Bank Limited |

6.0 Conclusion:

Jamuna Bank Limited is a bank that is trying to implement Internet banking service truly, where other banks claim Internet banking facilities but virtually providing only narrow focused service to their clients undermining the concept of e-commerce usage in the Internet based banking system to add more customer value to its clients. Very soon, Jamuna Bank Limited is going to provide Internet banking facilities where clients by sitting into his convenient place do any banking transaction using internet banking that others cannot support efficiently. Wish the bank all success to proof its efficiency to ensure greater customer value to its clients through Internet banking using e-commerce concept that will turns to its competitive advantage in the arena of banking service in Bangladesh. The bank will be concerned to this issue because,

“NO ONE IS IMMUNE FROM ATTACK

IT IS A QUESTION OF TIMING”

Recommendations:

Security system for individual clients for banking services and transactions should be well concerned.

Inform the clients to anchor into the Internet banking facilities to gain his customer value than others.

Educate the clients regarding how to get better service through e-commerce banking services.

Training facilities among internal employees to ensure better services to be delivered to clients by them.

Generosity of management to adopt and adapt any aspect of modern banking facilities.