The main objective of the study is to make an overview of the marketing strategies of” Premier Genius Account of ‘The Premier Bank’.

The Premier Bank Limited is incorporated in Bangladesh as banking company on June 10, 1999 under Companies Act.1994. Bangladesh Bank, the central bank of Bangladesh, issued banking license on June 17, 1999 under Banking Companies Act.1991. The Head Office of The Premier Bank Limited is located at Banani, one of the fast growing commercial and business areas of Dhaka city.

It was 1999,The world was approaching Y2K.the stage was set for anew millennium heralding an age of global governance with advance mechanism.the immediacy of global change was felt across the broder.Such perception in our local background Paved the way for the formation of third generation bank incorporated as ,The Premier Bank Limited” under Bank Companies Act 1991.The Bank Started Its Journey from October 26,1999 with a clear vision of corporate ex cellence together with a popular motto of ‘Service first’ under the auspices of 13 succesful entrepreneurs,well-known at their respective fields of business and industry.form the very beginning the bank set forth a dream to create a financial institution that would stand out the crowd and meet the demand of 21 century.

* TPBL Means =The Premier Bank Limited:

Foreign Trade (Import):

| Item No. | Type of Services | Nature of Charges/Commission | Revised Charges/ Commission w.e.f. 01.04.2009 |

| 1.

| Letter of Credit L/C Opening Commission Under Cash

| 1st QuarterFor each subsequent quarter or part thereof. Minimum

| @ 0.50%@ 0.30%

Tk. 1000/-

|

|

| L/C Opening Commission Under AID/Loan/ Credit/Barter | 1st QuarterFor each subsequent quarter or part thereof.Minimum

| @ 0.50%@ 0.30%

Tk. 1000/-

|

|

| L/C Opening Commission Under Deferred Payment

L/C Opening Commission for Back to Back L/C on A/C of export oriented Garments or specialized Textiles Industry

| 1st QuarterFor subsequent quarter or part thereof Minimum

| @ 0.60%@ 0.40%

Tk. 1000/-

@ 0.80% covering 180 days from L/C opening date to acceptance maturity date.

|

|

| L/C Opening Commission for Back to Back L/C other than export oriented Garments or specialized Textiles Industry | For each subsequent quarter or part thereof.Minimum | @ 0.50%@ 0.30% Tk. 500/-

|

|

| L/C Amendment Charge L/C Opening Commissions where 100% margin is received

| If amendment of L/C is transmitted by SWIFT1st QuarterFor each subsequent quarter or part thereof.

| At actual min Tk. 1000/- 0.25% per quarter Maximum

|

| Item. No. | Type of Services | Nature of Charges/Commission | Revised Charges/Commission w.e.f. 01.04.2009 |

| Acceptance Commission under Differed Payment L/Cs(except BTB) | 1st QuarterFor each subsequent quarter or part thereofMinimum

| @ 0.40%@ 0.40% Tk. 1000/-

| |

|

| If L/C’s are Transmitted by MailBy Courier, By Post

| Charge(This shall cover cost of registered mail of L/C to Advising Bank & copy to Reimbursing Bank) | At actual |

| If L/C’s Transmitted by SWIFT | Charge | At actual, Minimum Tk. 2500/- | |

| If L/C’s Transmitted in Short and Non-Operative SWIFT | Charge | At actual, Minimum Tk. 1000/- | |

| If Amendment of L/C is Transmitted by Mail, By Courier, By Post | Charge | At actual | |

| If Amendment of L/C is Transmitted by SWIFT | Charge | At actual, Minimum Tk. 1000/- | |

|

| Add Confirmation by Foreign Bank -Local Confirmation Charge

For our arranging Add Confirmation charge from Third Bank

| ChargeCharge

Charge

| At actual@ 0.25% (Flat)

@ 0.25% (Flat)

|

| ItemNo. | Type of Services | Nature of Charges | Revised Charges /Commissionw.e.f. 01.04.2009

|

| Foreign Correspondents charges (FCC) for all types of L/C’s | Charge | At actual as per Schedule of Charges of Foreign Bank’s Claim plus Swift Charge | |

| L/C Handling | Charge | Tk. 1500/-(To be realized at the time of opening of L/C) | |

| Foreign Correspondents charges for amendments of L/C’s | Charge | At actual as per schedule of charges of foreign correspondents (to be realized at the time of amendment)Minimum Tk. 800/- | |

| Certification of copyDocuments for assessment of Customs Duty | Charge | FREE. | |

|

| L/C Cancellation or Expired Unutilized charges | By Cable /SwiftBy Air Mail

| FREE |

| 2. | Collection of Credit Report on the Beneficiary by Swift /Dun & Bradstreet | Charge | At actual as per schedule of charges of Foreign Correspondents plus Tk. 750/- for each report. |

Foreign Trade (Export):

Item No.

Type of Services

Nature of Charges

Revised Charges/Commission

w.e.f. 01.04.2009

1.Export:

Negotiation Commission for Export Bills in Foreign Currency

Commission

No Charges for Negotiation, Interest

on overdue period will be applied as per lending rate

Negotiation Commission for Export Bills in Local Currency

Commission@ 0.25 % flat. Minimum Tk. 1000/-

Advising of Foreign Bank L/C’s to the local beneficiary

Charge Tk. 1000/-Per instance for our client.Tk. 2000/- for other than Bank’s client.

Advising of Local L/C’s

BTB & Inland

Charge Tk. 500/- for our customers

Tk. 1000/- for other than Bank’s client.

L/C Amendment Advising Charge Tk. 500/- per instance for our client.Tk. 1000/- per instance for other Bank’s client Transfer of L/Cs Charge.

Amendment Charge

Tk. 1000/- per instance for our client

Tk. 1500/- per instance for other Bank’s client

Tk. 300/- for our client

Tk. 1000/- for other Bank’s client

Foreign Bank’s Guarantee Commission against discrepant bills

Commission At Actual

Collecting Bank’s charges abroad

Charge

At Actual Processing of documents under collection in Foreign currency

Charge

FREE

Processing of documents under collection in Local currency

Charge

@ 0.15 % Minimum Tk. 500/- plus Swift/Telex/Mail Charges

Item No.

Type of Services

Nature of Charges

Revised Charges/ Commission w.e.f 01.04.2009

Mailing of Export Documents

By Courier

By Post

At Actual, Minimum Tk. 1600/-

For SAARC countries- at actual

Minimum Tk. 1000/-

At actual, Minimum Tk. 500/-

SWIFT Charge for sending payment instruction of reimbursement

Charge

At actual, Minimum Tk. 500/-

Adding of Confirmation

Commission

@ 0.25 % Minimum Tk. 1000/-

if payable by foreign correspondent / beneficiary

Handling Charge against Packing Credit Facility Charge@ 1.5 %

Foreign Trade

(Export)ChargeWhen any Packing Credit facility becomes overdue then it will be charged @ 15.00% P.a for the overdue period till the time of adjustment.

2.Foreign Bank Guarantee

Advising of Guarantees to the beneficiary in original without any engagement on our part

Commission Tk. 1000/- (Flat)

Advising of Guarantees in original by adding our confirmation

Commission

@ 0.40 % per quarter or part thereof

Minimum Tk. 2000/-

Advising of Guarantee in our own format or on the format supplied by the issuing/ opening bank with our full engagement

Commission

@ 0.50 % per quarter or part thereof

Minimum Tk. 1000/-

Indemnity for Shipping Guarantee in absence of original document provided full value of document is deposited by client.

Charge

Tk. 1000/-

3.Export Transaction

Issuance of Export Performance Certificate (EXP)

Charge

Tk. 200/- each

Item. No.

Type of Services

Nature of Charges

Revised Charges/Commission w.e.f 01.04.2009

4.Stationery

Charge Tk. 50/-

5.Issuance of Proceeds Realization Certificate

(PRC)

Charge.Tk. 500/-

6. Issuance of Back to Back L/C Certificate

ChargeTk.500/-

Foreign Trade (Miscellaneous):

Item No

Type of Services

Nature of Charges

Revised Charges /Commission w.e.f 01.04.2009

1.Forwarding application regarding Import Registration Certificate etc. (IRC)

Charge Tk. 350/- per instance

2.Handling Charges for License of Indenting & Money Changer etc.

Charge Tk. 350/-

3.Handling Charges for Settlement of Cash Incentive & DEDO

Charge Tk. 1000/-

4.Inland L/C Advising and Reimbursement Charge

ChargeTk. 500/-

5.Correspondence against Customer’s Queries / Investigation

Charge At actual Minimum Tk. 300/-

Foreign Remittance:

Item No.

Type of Services

Nature of Charge

Revised Charges/Commission w.e.f. 01.04.2009

1.Foreign Remittances

Purchase of Foreign Bank Drafts drawn abroad

Charge a) @ 0.20 % per US$

b) @ 0.30 % per GBP

Payment of any Foreign Taka Drafts which are drawn on our Bank

Charge

FREE

Encashment of any Foreign TT in Taka at our Counter

Charge

FREE

Encashment Certificate Charge

a) Tk. 100/- within 1 month

b) Tk. 150/- within 3 months

c) Tk. 300/- over 3 months

2. a) Opening / Renewal of Student File for Education Purpose

b) Remittance Fees

Charge

a) Tk. 4000/- + VAT 15 % per Student File

b) Other Charges as per Schedule of Charges.

3.Issuance of F.C. Demand Draft drawn on Bangladesh Bank

Charge Tk. 300/- or US $5/-

4.Clearing of FC Drafts drawn on Bangladesh Bank

Charge

FREE

5.Disposal of Remitted Fund on A/C of Home Remittance

Charge

FREE

Item No.

Type of Services

Nature of Charges

Revised Charges/Commission w.e.f. 01.04.2009

6.Collection (Inward)

For Collection of Clean Item (Inward) from local bank Charge @ 0.15 % Minimum Tk. 200/-

For Documentary Collection Bills (under all types of L/Cs)

Charge@ 0.15 % Minimum TK. 500/-

For Documentary Bill under Grant (without L/Cs)

Charge 0.20%

Minimum TK. 500/-

All other charges including SWIFT etc. for above transaction

Charge At actual as per Schedule of Charge

Collection of Foreign Currency Draft from Abroad

Charge At actual cost plus SWIFT Charge

Minimum Tk. 500/-

Encashment of any Foreign Currency Draft at our counter

Charge

Tk. 300/- (flat)

Plus SWIFT charges (if any).

Issuance of TC/ Endorsement in Passport

Fee & Commission

Endorsement Fee = Tk. 200/- (Fixed)

Issuance of TC = 1 %, Min. Tk. 100/-

Issuance of Cash (FC) Endorsement in Passport

Fee & Commission

Endorsement Fee = Tk. 200/- (Fixed)

Transactions by Nominee/ Account Holder in FC A/Cs

Charge

NO Charge

Issuance of FC Drafts on Foreign Correspondents

Charge TK. 500/- plus SWIFT Charge.

Remittance by T.T. (F.C) through Foreign Correspondents (Out going)

Charge TK. 500/- plus SWIFT Charge Cancellation of Drafts in Foreign Currencies

Charge At actual cost Min. Tk. 500/- plus SWIFT Charge.

On Line Charges for Any Branch Banking Services

| Transaction Type | Limits | Revised Charges w.e.f 01.04.2009 |

Cash Deposit & WithdrawalAny amount within Dhaka or Chittagong Clearing House AreaFREEUp to Tk. 1.00 lac, Outside Dhaka or ChittagongCityTk. 50/-

Above Tk. 1.00 lac to Tk. 10.00 lac, Outside Dhaka or ChittagongCityTk. 100/-Above Tk. 10.00 lac to Tk. 25.00 lac, Outside Dhaka or ChittagongCityTk. 200/-Above Tk. 25.00 lac, Outside Dhaka or ChittagongCity

Tk. 300/-

* Vat is applicable as per Government Rules*

Special Note:

- Above Charges/Commissions/Rates are Exclusive Govt. Duty/Tax/VAT, if any, shall be recovered from the Customers in addition where applicable.

Place: The Premier Bank has thirty two branches all over the Bangladesh. And many other palaces in Bangladesh is prospected to set up the branches in Bangladesh.

List of Branches :At present they have 30branches and 8 proposed branches (Sorted Alphabetically)

| Ashugonj Branch |

Station Road, Ashugonj, Brahmanbaria.

Tel: 08528-448

Mobile: 01711826048

Banani Branch

Ground and 2nd Floor, Iqbal Center,

42, Kemal Ataturk Avenue, Banani, Dhaka – 1213

Tel: 9887581-84, Ext. – 301, 306

Fax: 880-2-8815393

Telex: 642542 PRBHO BJ

S.W.I.F.T. : PRMRBDDH

Bangshal Branch

1st Floor, 70, Shahid Syed Nazrul Islam Sarani

(North-South Road), Bangshal, Dhaka

Tel : 880-2-9565684, 880-2-9565738

Fax: 880-2-9565807

Barishal Branch

54, Sadar Road, Barisal

Tel : 0431-63102-4

Mobile : 0173450651, 0171465788

Fax : 0431-63104

Bhairab Bazar Branch

129 (Old), 172 (New) East Kalibari Rd, Bhairab Bazar, Kishoregonj

Tel : 09424-71122, 71133; Mobile : 01713144282 (Open: 16-11-2006)

Fax: 71133

Dhanmondi Branch

House # 84, Road # 7/A, Dhanmondi, Dhaka –1209

Tel : 9145186, 9143081, 8124746

Mobile : 01711- 595720

Fax : 9112395

Telex : 642552 PRBDB BJ S.W.I.F.T. : PRMRBDDHDHN

Dilkusha Branch

44, Dilkusha C/A, Dhaka – 1000

Tel: 880-2-9552303, 880-2-9569180, 880-2-9552328

Fax: 880-2-9552801

Telex: 642552 PRBDB BJ S.W.I.F.T.: PRMRBDDHDIL

Elephant Road Branch

1st floor, 248, New Elephant Road, Dhaka

Tel : 880-2-8616803, 8617992, 8618003 (Direct)

Mobile : 01713-001815 (Manager)

Gulshan Branch

140, Gulshan Avenue, Gulshan Circle 2, Dhaka-1212

Tel: 880-2-8815268, 880-2-9882781, 880-2-9890391

Fax: 880-2-8818338

Telex: 642541 PRBGL BJ S.W.I.F.T.: PRMRBDDHGUL

Imamgonj Branch

75, Mitford Road, Imamgonj, Dhaka

Tel : 7313199, 7317752

Mobile : 01199805334 (Manager)

Fax : 7313199

Telex : 642556 PRBIM BJ

Joydebpur Branch

Ground Floor, Dilan Complex, Dhaka Road

Chandana Chowrasta, Joydebopur, Gazipur-1702

Tel : 9257551, 9257552

Mobile : 01713-039774

Kawran Bazar Branch

Pragati Rhone Poulenc Centre, RAJUK Plot No. 20 / 21

Kawran Bazar C/A, Tejgaon, Dhaka

Tel: 880-2-9121485, 9139657

Fax: 880-2-9133645

Khatungonj Branch

Nabi Super Market (1st floor), 232, Khatungonj, Chittagong

Tel: 639521 (Direct), 639523, 618259

Fax: 639468, Mobile: 01711- 723119

Kakrail Branch

46/A (2nd floor), VIP Road, Kakrail, Dhaka-1000 (Opening: 24 Dec 06)

Tel: 9344628, 9344438, 9353963, 9359116

Mobile: 01199885888, 01711584401, 01815447980 (Manager)

Fax: 9344438Khulna Branch

Ist floor, 141 Sir Iqbal Road, Khulna

Tel : 880-41-810253-4

Mobile : 01711-218373 (Manager)

Meghnaghat Branch

New Town Commercial Complex (1st Floor)

Meghnaghat, Sonargaon, Narayangonj.

Tel: 0607-8210111, 0189-249836

Mohakhali Branch (Islami Banking Branch)

99 Mohakhali C/A, Dhaka

Tel : 8853503, 8859223, 8858118(Direct)

Mobile : 01713-007659 (Manager)

Moulvi Bazar Branch

855/6 Sayed Mujtoba Ali Road, Moulvi Bazar, Sylhet (Opening: 28 Dec 06)

Tel : 62880, 62881

Mobile : 01715397399 (Manager)

Motijheel Branch

81, Motijheel C/A Dhaka – 1000

Tel: 880-2-957113-4,9557656,9555340(D)

Fax: 880-2-9557317

Telex : 642552 PRBDB BJ

Narayangonj Branch

2nd Floor, Rahat Complex, Old-56, New 53/3

SM Maleh Road, Tanbazar, Narayangonj

Tel: 9750102-3; Mobile : 01713031878 (Manager)

Fax: 9752493 (Opening: 15 Feb 2004)

O. R. Nizam Road Branch

Hotel Harbour View Building (1st Floor), 721 CDA Avenue,

O.R.Nizam Road, Chittagong (Open: 23-11-2006)

Tel : 031-2852437, 2852434, 2852438, 2852436

Mobile : 01713124422, 0189310526 Fax: 2852438

Rajshahi Branch

M.M.Plaza, 1st Floor, 222, Kumarpara, Old Nator Road, Saheb Bazar, Boalia, Rajshahi.

Tel : 880-2-0721-773408

Rokeya Saroni Branch

Oriental Arabian Tower, Ground & 1st Floor, 849/3, Shawrapara, Begum Rokeya Sarani, Kafrul, Dhaka.

Tel : 880-2-03772820045

Savar Branch

Hashem Plaza, DEPZ Gate, Ganakbari, Savar

Tel : 880-2-7702108-9, Fax:7702108

Mobile : 01199808332 (Manager)

Savar Bazar Stand Branch

Savar New Market, Ground Floor, 03, Savar Bazar Bus Stand, Savar, Dhaka.

Tel : 880-2-7743753

Fax: 880-2-7743754

Sylhet Branch (Islamic Banking)

Plot # 177, Laldighirpar, Sylhet

Tel : 0821-813050-2

Mobile : 01713-010346, 01713-302002

Tongi Branch

175 Kazi Market (1st Floor), Mymensingh Road, Tongi.

Tel : 9815756-7; Mobile : 01711538758 (Manager)

Fax: 9815758

Uttara Branch

Ground floor, House # 39, Road # 7

Sector 4, Uttara, Dhaka

Tel : 880-2-8956430, 8953945

Mobile : 01199812862 (Manager)

Zinzira Branch

Haji Nannu Bepari Mansion(1st Floor),2nd Buriganga Bridge Road,

Zinzira, Keranigonj, Dhaka

Mobile : 01730000466(Manager)

Promotion: the Premier Bank limited Using Brushier, Leaflets, Billboards, TV advertisement, Radio advertisement as promotional activities of them. The premier Bank Ltd also decorates their branches by the leaflets of their branches when a new product launches. Premier Bank Ltd also engaged in some charitable or sponsored in many sports events as the part of their promotions such as premier Bank divisional cricate league.

Departments of The Premier Bank Ltd.

As far as The Premier Bank Ltd is concerned, it is one of the top in all-domestic commercial banks in Bangladesh. The rapid increase in branch network shows the Bank’s performance within seven years, which is worth considerable.

However, this branch works with mostly all banking operations, which are normally performed by every commercial bank. It has basically following departments under which it operates all functions of bank diligently. These are mainly:

- Account opening department:

- Remittances department:

- Clearing department:

- Accounts department:

- Cash department:

- Credit department :

- Credit card department:

- General service division:

- FDR Section:

SOWT analysis of The Premier Bank Ltd:in SOWT analysis we find that though the premier bank limited is a pivate local bank but it have a good strength in the market and the opportunity to expand its operation is vast, on the other hand as it also have some weakness and threats too. the SOWT of The Premier Bank Ltd is explaining in below.

Strength: Strength means the power of protection own from any destruction or the power of compete with others. In this view point I can say that the premier bank has enough strength to compete in the present market situation as it present total asset and liabilities shows that pre premier bank have enough asset and standard level of liabilities (in respect to Bangladesh Bank )that helps premier bank Ltd to compete in the banking sector.

Opportunities: As the number of people of Bangladesh at present there are more that 16 corer people lives in Bangladesh .in which there are more than four corer people are employed and most of the people dot using any banking services so it a great opportunities to engage them with banking sectors on the other hand the premier bank have only thirty two branches in Bangladesh so it have a great opportunities to involve new clients by expanding their branches.

Weakness: As an organization The Premier Bank Ltd also have some problem or weakness to , as I know the premier bank is set up by some political people so it have a negative impression on the market.

Threats: The premier bank limited is a local private bank as at present it don’t have any threats but it could be because it is an financial organization and it lend money to other though it give money after gathering enough information about the clients but sometimes it could default. And as our country economy is venerable so any organization can fall in a bad situation in any time.

Details about Premier Genius Account:

The Executive committee/ board of directors of The Premier bank Ltd in its 662nd meting held on March 172008 have approved a new product named “Premier Genius Account\’-a saving account for the student s of our country.

Premier Bank Ltd offers a banking pack for the students if you are a student, you will appreciate their new premier genius account with a number of extra benefits specially a higher rate of interest with some other benefits designed for the students of Bangladesh.

What are the:

1. 7.5% p.a simple interest on daily closing balance. Effective rate will be 7.645however in case of Islamic Banking Branch, they will determine provisional profit rate, in the light of changes made, by themselves.

2. Interest is payable on half yearly.

3. Daily interest paid on daily closing balance.

4. Withdraw a maximum amount of tk.10000/-per day from any of our ATMs.

5. Free online banking for any amount in between of Dhaka clearing house area and Chittagong clearing area only

6. Free of charge standing instruction to transfer fund

7. free-pay order service (for self job application, admission and education purpose only)

8. Aftercompletion of the education, premier Genius Account will be converted in to regular savings account

9. VISA debit card for ATM users named Premier Genius Card”. Free for the 1st year.50% discount on annual free for rest of the years.

10. Premier Genius A/C holder will get priority service /discount for opening student. File for abroad.

Benefits of the parents:

Parents can transfer fund from their bank account to Childs premier Genius account free of charge. So that his or her collage fees,tution, living expenses etc. are taken care of it.

If you have a premier bank VISA credit card, you can give your son /daughter a supplementary card specify a pre determined spending limit.

Who are eligible?

- 18 years old or above

- Bangladeshi by national

- Enrolled in a full time program at under graduate/Post Graduate

Level or equivalent in a recognized university or educational instution

Documentation needed to open this account:

The applicant must provide the following documents:

1. Two copies of photograph

2. Acceptable Identity proof of the applicant such as an identity card, library card, pay slip, passport, if any, and a letter of conforming admission to the university or educational institution.

3. Photocopy of SSC or equivalent

4. A letter of introduction from the university/institutions where the course particulars including end date of the course to be mentioned.

Completed Account Opening from with a nominee From, KYC From 7 Photograph of nominee attested by applicant.

5. Details of parents/Gardians-name,address ,phone numbers,nationality,residential status.

Interest calculation:

Interest will be calculated @7.00%p.s on Daily closing balance.

Suppose an account holder maintained balance TK.2000/-from the 1ST November to 9th November, TK .00/- from 10th November and tk-5000/- from 16th November, the interest on that account for the month November will be calculated as follows:

- TK2000.00 X 9 days={(TK.2000X0.07)/360}X 9 days=TK.3.5

- TK 00.00 X 6 days={(TK0.00X0.07)/360}X 6 days=TK.0.0

- TK5000.00 X 15 days={(TK.5000X0.07)/360}X15 days=TK.14.58

So total interest on the above account for the month April will be TK3.50+TK0.0+TK14.58 = TK.18.08

Therefore to maximize the benefit of Interest from the account, student will be encouraged to maintain at least minimum balance of take 00/- in their Genius Account at all the times.

Fees and charges of the Premier Genius Account:

| Account Closing charge | TK-200/- |

| Standing Instruction | Free |

| Issuance of Solvency Certificate | Free |

| Supply of Regular Statement of Account | Free of Charge |

| Supply of Duplicate Statement of Account | Free |

| Stop payment Instruction | TK.50/-per instruction |

| Issuance of cheque book | Issuing 10 leaves=TK.25/- |

Issuing 25 leaves=TK.50/-

Issuing 50 leaves=TK.100/-

Account Reactivation charge(if the minimum balance go below TK500/- at any time Account will be inactiveTK100/-ATM fee for the Premier Genius Card(Free for 1st year only)50%discoun for the rest years.Pin replacement FeeAt ActualCash withdrawal Fee(ATM)Nil(Premier Bank ATM)Other ATM at actualReplacement Card FeeAt ActualPayment Order (self job application, admission& educational Purpose only)Free of ChargeOnline Transfer Charge For any amount in between Branches of Dhaka Clearing house area onlyFree of ChargeOnline Transfer Charge For any amount in between Branches of Chittagong Clearing house area onlyFree of ChargeOnline Transfer up to TK. One lac charge outside Dhaka and Chittagong cityTK.50/-Online Transfer Above TK. One lac to 10 lac charge outside Dhaka and Chittagong cityTK.100/-Online Transfer Above TK. 10 lac to 25 lac charge outside Dhaka and Chittagong cityTK.200/-Online Transfer Above TK. 25 lac charge outside Dhaka and Chittagong cityTK.300/-Service ChargeFree

Frequently Asked Questions:

How do I approach Premier Genius Account?

Any one can just walk into any of our branch with your supporting papers as stated.

How much amount required opening this account?

Any one can open this account by deposit of TK 2000/- only

What is the minimum balance required to be maintained for a premier Genius Account?

The minimum balance required to be maintained is TK 500/- only to keep the account active.

At what frequency will the interest be paid to me?

Interest earned on your premier Genius account balance shall be credited to your account on half yearly basis.

Do I need an introduction from an existing premier bank account holder?

The Bank needs no introduction from an existing premier bank account holder if you are submitting satisfactory proof of identity with address as prescribed.

Can this account to be opened jointly? Whom can I joint Applicant?

Nobody can’t open this account jointly, but can nominate someone

Can this account opened in the name of any organization or firm?

No this is a personal account for the regular student which can be opened individually

What is premier genius card?

Premier Genius card is a regular Premier VISA Debit card issued by the Premier bank Ltd which is only for the Premier Genius Account Holder.

v What is the difference Between a Premier Student Account and other Savings Account offered by Premier Bank ltd.

- Premier Savings Account:

Anyone Can Competent Person

Daily interest amount TK10000/-

Interest rate6.5% p.a

Service charge, online transfer fee is free with condition

- Premier genius Account:

Only a regular student at a minimum the age of 18 years old

Daily interest on any amount

Interest rate is 7.50 pay

No Service Charge, online Transfer Fee is Free with conditions

As my topic of Internship “Marketing strategies of the Premier Bank Limited “A special focus on the Prospect of Premier Genius Account”.

Marketing Strategy means: Marketing strategy is a method of focusing an organization’s energies and resources on a course of action which can lead to increased sales and dominance of a targeted market niche. A marketing strategy combines product development, promotion, distribution, pricing, relationship management and other elements; identifies the firm’s marketing goals, and explains how they will be achieved, ideally within a stated timeframe. Marketing strategy determines the choice of target market segments, positioning, marketing mix, and allocation of resources. It is most effective when it is an integral component of overall firm strategy, defining how the organization will successfully engage customers, prospects, and competitors in the market arena. Corporate strategies, corporate missions, and corporate goals. As the customer constitutes the source of a company’s revenue, marketing strategy is closely linked with sales.

The marketing concept of building an organization around the profitable satisfaction of customer needs has helped firms to achieve success in high-growth, moderately competitive markets. However, to be successful in markets in which economic growth has leveled and in which there exist many competitors who follow the marketing concept, a well-developed marketing strategy is required. Such a strategy considers a portfolio of products and takes into account the anticipated moves of competitors in the market.

(McGrath, Michael E., Product Strategy for High Technology Companies):

Service Quality

Service quality is a concept that has aroused considerable interest and debate in the research literature because of the difficulties in both defining it and measuring it with no overall consensus emerging on either (Wisniewski, 2001). There are a number of different “definitions” as to what is meant by service quality. One that is commonly used defines service quality as the extent to which a service meets customers’ needs or expectations (Lewis and Mitchell, 1990; Dotchin and Oakland, 1994a;

Asubonteng et al ., 1996; Wisniewski and Donnelly, 1996).

Service quality can thus be defined as the difference between customer expectations of service and perceived service. If expectations are greater than performance, then perceived quality is less than satisfactory and hence customer dissatisfaction occurs (Parasuraman et al ., 1985; Lewis and Mitchell, 1990).

Always there exists an important question: why should service quality be measured? Measurement allows for comparison before and after changes, for the location of quality related problems and for the establishment of clear standards for service delivery. Edvardsen et al. (1994) state that, in their experience, the starting point in developing quality in services is analysis and measurement. The

SERVQUAL approach, which is studied in this paper is the most common method for measuring service quality.

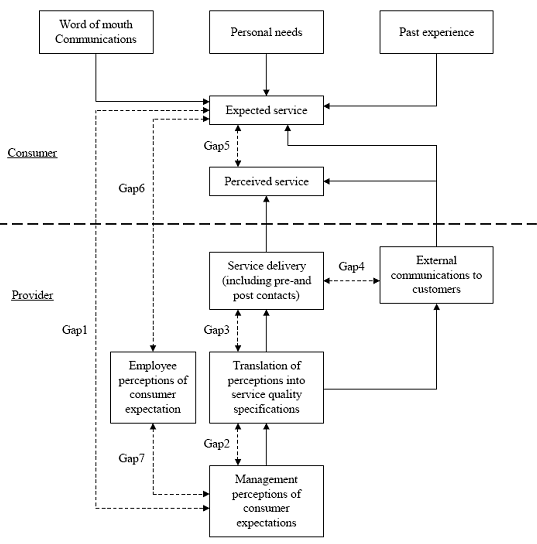

Model of Service Quality Gaps:

There are seven major gaps in the service quality concept, which are shown in Figure 1. The model is an extention of Parasuraman et al. (1985). According to the following explanation (ASI Quality

Systems, 1992; Curry, 1999; Luk and Layton, 2002), the three important gaps, which are more associated with the external customers are Gap1, Gap5 and Gap6; since they have a direct relationship with customers.· Gap1: Customers’ expectations versus management perceptions: as a result of the lack of a marketing research orientation, inadequate upward communication and too many layers of management.· Gap2: Management perceptions versus service specifications: as a result of inadequate commitment to service quality, a perception of unfeasibility, inadequate task standardization and an absence of goal setting.· Gap3: Service specifications versus service delivery: as a result of role ambiguity and conflict, poor employee-job fit and poor technology-job fit, inappropriate supervisory control systems, lack of perceived control and lack of teamwork.· Gap4: Service delivery versus external communication: as a result of inadequate horizontal communications and propensity to over-promise.· Gap5: The discrepancy between customer expectations and their perceptions of the service delivered: as a result of the influences exerted from the customer side and the shortfalls (gaps) on the part of the service provider. In this case, customer expectations are influenced by the extent of personal needs, word of mouth recommendation and past service experiences.· Gap6: The discrepancy between customer expectations and employees’ perceptions: as a result of the differences in the understanding of customer expectations by front-line service providers.

Gap7: The discrepancy between employee’s perceptions and management perceptions: as a result of the differences in the understanding of customer expectations between managers and service providers.

According to Brown and Bond (1995), “the gap model is one of the best received and most heuristically valuable contributions to the services literature”. The model identifies seven key discrepancies or gaps relating to managerial perceptions of service quality, and tasks associated with service delivery to customers. The first six gaps (Gap 1, Gap 2, Gap 3, Gap 4, Gap 6 and Gap 7) are identified as functions of the way in which service is delivered, whereas Gap 5 pertains to the customer and as such is considered to be the true measure of service quality. The Gap on which the SERVQUAL methodology has influence is Gap 5. In the following, the SERVQUAL approach is demonstrated.

SERVQUAL methodology:

Clearly, from a Best Value perspective the measurement of service quality in the service sector should take into account customer expectations of service as well as perceptions of service. However, as

Robinson (1999) concludes: “It is apparent that there is little consensus of opinion and much disagreement about how to measure service quality”. One service quality measurement model that has been extensively applied is the SERVQUAL model developed by Parasuraman et al . (1985, 1986,

1988, 1991, 1993, 1994; Zeithaml et al. , 1990). SERVQUAL as the most often used approach for measuring service quality has been to compare customers’ expectations before a service encounter and their perceptions of the actual service delivered (Gronroos, 1982; Lewis and Booms, 1983;

Parasuraman et al. , 1985). The SERVQUAL instrument has been the predominant method used to measure consumers’ perceptions of service quality. It has five generic dimensions or factors and are stated as follows (van Iwaarden et al. , 2003):

(1) Tangibles . Physical facilities, equipment and appearance of personnel.

(2) Reliability. Ability to perform the promised service dependably and accurately.

(3) Responsiveness . Willingness to help customers and provide prompt service.

(4) Assurance (including competence, courtesy, credibility and security). Knowledge and courtesy of employees and their ability to inspire trust and confidence.

(5) Empathy (including access, communication, understanding the customer). Caring and individualized attention that the firm provides to its customers.

In the SERVQUAL instrument, 22 statements (Appendix I) measure the performance across these five dimensions, using a seven point likert scale measuring both customer expectations and perceptions (Gabbie and O’neill, 1996). It is important to note that without adequate information on both the quality of services expected and perceptions of services received then feedback from customer surveys can be highly misleading from both a policy and an operational perspective. In the following, the application of SERVQUAL approach is more specified with an example in a catering company.

Findings of the Study:

Prospect: Naturally prospect means something expected; a possibility.Chances. Financial expectations,

Especially of success.

A potential customer, client, or purchaser.

The Premier genius account is a saving account for the student in our country and the prospect of Premier genius Account is very high.

In 2009, a total of 10,63,484 students appeared in the examination। Of them, 8.01 lakh students sat for the S.S.C. examinations under eight general education boards, 1.86 lakh students of under Madrasa Education Board and 75,057 students for the S.S.C. (vocational) exams under the Technical Education Board. Average 70.89% examinees of them have passed this year. (Source: Bangladesh national web).

In 2008 a total of 726,563 out of 10, 06,569 candidates under the nine education boards passed the SSC examination, held from March 23 to April 27 this yea(source: Bangladesh Education Board).

In 2007 As many as 10,24,537 students 5,51,255 boys and 4,73,282 girls appeared in this years SSC exams under nine educational boards and 5,97,955 of them 3,35,443 boys and 2,62,512 girls passed. (Source: Bangladesh Education Board)

In 2006 As many as 789669 students, of 203030 in science, 346723 Humanities and 239916 in business Studies appeared in this years SSC exams under nine educational boards .(source: Bangladesh Education Board)

And al the above data shows that in some recent years there are more than thirty lacs student have passed in their S.S.C exam an if we hope that 75%of them continuing their studies then there is a great opportunity to involve them in Premier genius Account.

Analytical Data and calculation result of User perception and Nonuser Expectation:

In the finding part I find that the clients of the premier bank are satisfied with the bank services. Here I tried to find out the market potentiality perception and the satisfaction level of the users of the bank services and the expectation level of the nonusers of bank services .To find out that I use the SPSS software for the calculation

The user perception of the premier bank limited are describing in below

Part A:

Overall Satisfaction:

Variale1

Bank service meets my expectation

Mean | Std. Deviation | |

| Bank service meet my expectation | 4.00 | .926 |

| Valid N (listwise) |

The table and the figure shows that the mean value is 4 which means most of the people are agree with this variable that Bank service meet my expectation

Variale2

I am satisfied to openining premier Genius Account in this bank

Frequency | Percent |

8 | 100.0 |

The table and the figure shows that 100% of the people or the clients of this bank are strongly agreewith this variable that I am satisfied to openining premier Genius Account in this bank

Variale3

Mean | Std. Deviation | |

| I will recomend this bank to my freinds and or associates | 4.50 | .535 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.5nd it can be take as approximate 5. Which shows that most of the clients are strongly agree with the variables that I will recommend this bank to my friends and or associates

Variale4

Mean | Std. Deviation | |

| I am willing to continue transactation with this bank | 4.38 | .518 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.38nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that I am willing to continue transactation with this

Variale5

I experienced problem with this bank

Frequency | Valid Percent | Cumulative Percent | ||

| Valid | Yes | 3 | 37.5 | 37.5 |

| No | 5 | 62.5 | 100.0 | |

| Total | 8 | 100.0 | ||

The Figure and the table shows that there are only 37%of people are agree with this variable that- I experienced problem with this bank abd 62.5 %of people don’t faces any problem

Variale6

My problem resolved satisfactory

Percent | Valid Percent | Cumulative Percent |

87.5 | 87.5 | 87.5 |

12.5 | 12.5 | 100.0 |

100.0 | 100.0 |

The figure says that there are 87.5 %people says that when they fall in a problem then the bank resolved the problem in satisfactory level

For more elaboration of the user perception there are 25 variables and their descriptive analytical result are given in below

Users Perception

Variable 1

Mean | Std. Deviation | |

| Bank should have modern looking equipment | 3.88 | .835 |

| Valid N (listwise) |

Figure 1

The descriptive analytical data shows that the mean value is 3.88 and it can take as approximate 4. Which shows that most of the clients are agree with the variables that the bank have the modern looking equipment.

Variable 2

Mean | Std. Deviation | |

| The Physical Faciliies at excellent bank should be visually appearing | 3.88 | .835 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.88 and it can take as approximate 4. Which shows that most of the clients are agree with the variables that The Physical Facilities at excellent bank should be visually appearing

Variable 3

Mean | Std. Deviation | |

| Personnel at excellent bank should be neat in appearence | 3.75 | 1.165 |

| Valid N (listwise) |

Here we can see that most of the clients are agree with the variables of Personnel at excellent bank should be neat in appearance because the mean value if near about the agree perception.

Variable 4

Mean | Std. Deviation | |

| Materials associated with the service should be visually appearing | 3.38 | 1.188 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.38 and it cant be take as approximate 4. Which shows that most of the clients are neutral with the variables that “Materials associated with the service should be visually appearing”

Variable 5

Mean | Std. Deviation | |

| When bank promise to do so somthing by a certain time they should do so | 3.75 | 1.488 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that “When bank promise to do so something by a certain time they should do so”

Variable 6

Mean | Std. Deviation | |

| When client has a problem bank should show a sincere interest in solving it | 4.00 | 1.309 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4. Which shows that most of the clients are agree with the variables that “When client has a problem bank should show a sincere interest in solving it”

Variable 7

Mean | Std. Deviation | |

| Excellent bank should provide their service at the time they promise to do so | 3.50 | 1.069 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.5and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that “Excellent bank should provide their service at the time they promise to do so”

Variable 8

Mean | Std. Deviation | |

| Excellent bank should insist on error free records. | 4.00 | 1.069 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4. Which shows that all the clients are agree with the variables that Excellent bank should insist on error free records.

Variable 9

Mean | Std. Deviation | |

| Personnel in excellent bank should tell clients exactly when services will be performed. | 4.13 | 1.126 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.13and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank should tell clients exactly when services will be performed.

Variable 10

Mean | Std. Deviation | |

| Personnel in excellent bank should give promt service to client | 4.25 | 1.035 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.25and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank should give promt service to client

Variable 11

Mean | Std. Deviation | |

| Personnel in excellent bank should always be willing to help client. | 4.50 | .535 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.50and it can be take as approximate 5. Which shows that most of the clients are stongly agree with the variables that Personnel in excellent bank should always be willing to help client. Variable 12

Mean | Std. Deviation | |

| The behavior of personnel in excellent bankshould install confidence in client | 3.88 | .991 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.88and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that the behavior of personnel in excellent bank should install confidence in client

Variable 13

Mean | Std. Deviation | |

| Personnel in excellent bank should consistently courtious with clients | 4.13 | .991 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.13and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank should consistently courtious with clients

Variable 14

Mean | Std. Deviation | |

| Excellent bank should give client individual attention | 4.38 | 1.061 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.38and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank should give client individual attention

Variable 15

Mean | Std. Deviation | |

| Excellent bank should have operating hours convenient to all their clients | 3.75 | 1.282 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank should have operating hours convenient to all their clients

Variable 16

Mean | Std. Deviation | |

| Excellent bank should have staff who give clients personal attention | 3.75 | 1.488 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that excellent bank should have staffs who give clients personal attention

Variable 17

Mean | Std. Deviation | |

| Excellent bank shouldhave the clients best interest at hart | 3.63 | 1.408 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.63and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank should have the clients best interest at hart

Variable 18

Mean | Std. Deviation | |

| The personnel of excellent bank should understand the specific needs of their clients | 4.13 | .991 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.13and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that The personnel of excellent bank should understand the specific needs of their clients.

Variable 19

Mean | Std. Deviation | |

| Personnel in excellent bank should never too busy to respond to clients requests | 4.00 | .926 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank should never too busy to respond to clients requests

Variable 20

Mean | Std. Deviation | |

| Personnel in excellent bank should have knowledge to answer clients questions | 4.50 | .756 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.5and it can be take as approximate 5. Which shows that most of the clients are strongly agree with the variables that Personnel in excellent bank should have knowledge to answer clients questions

Variable 21

Mean | Std. Deviation | |

| Bank should deduct less service charge | 3.63 | 1.302 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.6nd it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that Bank should deduct less service charge

Variable 22

Mean | Std. Deviation | |

| Bank should give more interest rate to their clients | 4.50 | .535 |

| Valid N (listwise) |

The data shows that the mean value is 4.5nd it can be take as approximate 5. Which shows that most of the clients are strongly agree with the variables that Bank should give more interest rate to their clients

Variable 23

Mean | Std. Deviation | |

| Bank should charge less penalty to their clients | 3.50 | 1.195 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.5nd it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that Bank should charge less penalty to their clients

Variable 24

Mean | Std. Deviation | |

| Bank should provide less waiting time to their clients | 4.75 | .463 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.75nd it can be take as approximate 5. Which shows that most of the clients are strongly agree with the variables that Bank should provide less waiting time to their clients

Variable 25

Mean | Std. Deviation | |

| Bank should extent the time of payment installment | 4.13 | .641 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.13nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Bank should extent the time of payment installment

Nonuser Expectation:

Variable 1

Mean | Std. Deviation | |

| Bank will have modern looking equipment | 4.19 | 1.109 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.19nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Bank will have modern looking equipment

Variable 2

Mean | Std. Deviation | |

| The Physical Faciliies at excellent bank should be visually appearing | 3.69 | .793 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.69nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that The Physical Facilities at excellent bank should be visually appearing

Variable 3

Mean | Std. Deviation | |

| Personnel at excellent bank will be neat in appearence | 3.75 | 1.238 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel at excellent bank will be neat in appearence

Variable 4

Mean | Std. Deviation | |

| Materials associated with the service will be visually appearing | 4.06 | 1.063 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.06nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Materials associated with the service will be visually appearing

Variable 5

Mean | Std. Deviation | |

| When bank promise to do so somthing by a certain time they will do so | 3.25 | 1.183 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.25nd it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that When bank promise to do so somthing by a certain time they will do so

Variable 6

Mean | Std. Deviation | |

| When client has a problem bank will show a sincere interest in solving it | 4.38 | .719 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.38 and it can be take as approximate 4. Which shows that most of the clients are agree with the variables that When client has a problem bank will show a sincere interest in solving it

Variable 7

Mean | Std. Deviation | |

| Excellent bank will provide their service at the time they promise to do so | 4.13 | .806 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.13nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank will provide their service at the time they promise to do so

Variable 8

Mean | Std. Deviation | |

| Excellent bank will insist on error free records. | 3.19 | 1.167 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.19nd it can be take as approximate3. Which shows that most of the clients are neutral with the variables that Excellent bank will insist on error free records.

Variable 9

Mean | Std. Deviation | |

| personnel in excellent bank will tell clients exactly when services will be performed. | 3.75 | 1.000 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that personnel in excellent bank will tell clients exactly when services will be performed.

Variable 10

Mean | Std. Deviation | |

| Personnel in excellent bank will give promt service to client | 3.94 | .998 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.94nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank will give promt service to client

Variable 11

Mean | Std. Deviation | |

| Personnel in excellent bank will always be willing to help client. | 4.00 | 1.317 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank will always be willing to help client.

Variable 12

Mean | Std. Deviation | |

| The behavior of personnel in excellent bank will install confidence in client | 3.69 | .793 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.69nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that the behavior of personnel in excellent bank will install confidence in client

Variable 13

Mean | Std. Deviation | |

| Personnel in excellent bank will consistently courtious with clients | 3.75 | 1.000 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.75nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank will consistently courtious with clients

Variable 14

Mean | Std. Deviation | |

| Excellent bank willl give client individual attention | 3.56 | 1.153 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.565nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank willl give client individual attention

Variable 15

Mean | Std. Deviation | |

| Excellent bank will have operating hours convenient to all their clients | 3.19 | 1.047 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.19nd it can be take as approximate 9. Which shows that most of the clients are neutral with the variables that Excellent bank will have operating hours convenient to all their clients

Variable 16

Mean | Std. Deviation | |

| Excellent bank will have staff who give clients personal attention | 3.13 | 1.258 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.13nd it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that Excellent bank will have staff who give clients personal attention

Variable 17

Mean | Std. Deviation | |

| Excellent bank will have the clients best interest at hart | 3.69 | .946 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.69nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Excellent bank will have the clients best interest at hart

Variable 18

Mean | Std. Deviation | |

| the personnel of excellent bank will understand the specific needs o their clients | 3.88 | 1.088 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.88nd it can be take as approximate 3 Which shows that most of the clients are neutral with the variables that the personnel of excellent bank will understand the specific needs o their clients

Variable 19

Mean | Std. Deviation | |

| Personnel in excellent bank will never too busy to respond to clients requests | 3.50 | 1.033 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.5nd it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that Personnel in excellent bank will never too busy to respond to clients requests

Variable 20

Mean | Std. Deviation | |

| Personnel in excellent bank will have knowledge to answer clients questions | 3.88 | .885 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.88nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Personnel in excellent bank will have knowledge to answer clients questions

Variable21

Mean | Std. Deviation | |

| bank will deduct less service charge | 3.19 | 1.223 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.19nd it can be take as approximate 4. Which shows that most of the clients are neutral with the variables that bank will deduct less service charge

Variable 22

Mean | Std. Deviation | |

| Bank will give more interest rate to their clients | 3.69 | 1.250 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.69nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Bank will give more interest rate to their clients

Variable 23

Mean | Std. Deviation | |

| Bank will charge less penalty to their clients | 4.00 | .816 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4. Which shows that most of the clients are agree with the variables that Bank will charge less penalty to their clients

Variable 24

Mean | Std. Deviation | |

| Bank will provide less waiting time to their clients | 3.44 | .964 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 3.44 and it can be take as approximate 3. Which shows that most of the clients are neutral with the variables that Bank will provide less waiting time to their clients

Variable 25

Mean | Std. Deviation | |

| Bank will extent the time of payment installment | 4.06 | .929 |

| Valid N (listwise) |

The descriptive analytical data shows that the mean value is 4.06nd it can be take as approximate 4. Which shows that most of the clients are agree with the variables that Bank will extent the time of payment installment

Part B:

Respondent Identity of the user group:

What is your gender?

Percent | Valid Percent | Cumulative Percent |

37.5 | 37.5 | 37.5 |

62.5 | 62.5 | 100.0 |

100.0 | 100.0 |

In all the respondent there was 62.5%of respondent was male and 32.5%was female

What is your age

Frequency | Percent | ||

| 16-20 | 1 | 12.5 | |

| 21-25 | 4 | 50.0 | |

| 26-30 | 3 | 37.5 | |

| Total | 8 | 100.0 | |

The figure shows that there was most of the respondent was 21-25 of agesome of themwere 26-30 years of age and rest of them were 31-35years of age

What is your educational qualification

Frequency | Percent | |||

| Undergraduate | 4 | 50.0 | ||

| Graduate | 3 | 37.5 | ||

| Postgraduate | 1 | 12.5 | ||

| Total | 8 | 100.0 | ||

The figure shos that there was 50%of respondents were undergraduate and 37%were graduate and rest of them were post graduate

Respondent Identity Nonuser group:

Variable:1

What is your gender

Percent | Valid Percent | Cumulative Percent | ||||

| Female | 12.5 | 12.5 | 12.5 | |||

| Male | 87.5 | 87.5 | 100.0 | |||

| Total | 100.0 | 100.0 | ||||

Interactive Graph

The table and the figure shows that there were only 12% of the respondent were female an rest of them were male

Variable:2

What is your age

Frequency | Percent | ||

| Valid | 16-20 | 1 | 12.5 |

| 21-25 | 4 | 50.0 | |

| 26-30 | 3 | 37.5 | |

| Total | 8 | 100.0 | |

Statistic:

Here we can see that from all the respondent there were 12.5% were 16-20 years of age50%were 21-25 years of age and rest of them were 26to 30 years of age

Variable: 3

What is your educational qualificati

Percent | ||

| Valid | H.S.C | 6.3 |

| Undergraduate | 75.0 | |

| Graduate | 6.3 | |

| Postgraduate | 12.5 | |

| Total | 100.0 | |

The table shows that the 75%of respondent were undergraduate 6.3%were graduate and 12.5 %were post graduate respondent.

Conclusion and Recommendation:

At the end of all the regular part of internship program after complete all the necessary can say that Premier Bank Ltd is one of the best quality private local bank in Bangladesh and it have enough strength to capture the market in competition with other banks. and its promotional activities are weaker them other bank and it don’t give enough effort for their marketing campaigns there re some recommendation for premier bank given in below:

- Ø Go private universities and offer the students there suitable products and services

- Ø Increase media exposure by giving more promotional ads

- Ø Participate in any nationwide program, sports or event

- Ø Try to remove bad political impression the banks have

- Ø By giving better services try to create the clients loyal

Some are parts:

Internship Report on Marketing Strategies of the Premier Bank Limited(Part 1)

Internship Report on Marketing Strategies of the Premier Bank Limited(part 2)