General banking activities of Prime Bank Limited

Banks are the most important financial institutions in a modern economy. They are an integral part of modern economic activities. They help accelerate the pace of development process by securing uninterrupted supply of financial resources to people engaged in numerous economic activities. The banks act as financial intermediaries i.e. mobilization of funds from small depositors and allocate them to entrepreneurs for investments. Though initially the major function of banking was to mobilize savings and transfer them to entrepreneurs, over the time they have come to perform a number other functions as well. In addition to offering their services for safe custody of money and other valuables, they also offer demand deposits, easy transfer of money, letters of guarantees, collection of utility bills and loans for consumer durables and investments. Thus the operation of banks is vital for any economy. The Bangladeshi banking industry has been growing for the last three decades. The number of banks operating within the industry has increased by ten folds over the years. Currently there are 55 scheduled banks that are operating in Bangladesh. For a growing economy like Bangladesh, efficient operation and growth of these banks are vital.

As a bank, Prime Bank Limited (PBL) also provides the above services. It is a well-known Bank in our country and has gained firm confidence in the minds of its clients within a short period of its operation. The success is primarily attributed to prompt and bold decision-making, efficient and cordial services, economic use of resources and introduction of new financial products and technologies. The PBL has been widely acclaimed by the business community, from small entrepreneurs to large traders and industrial conglomerates, including the top rated corporate borrowers for forwarding-looking business outlook and innovative financing solutions. Thus within this very short period of time it has been able to create an image for itself and has earned significant reputation in the country‟s Banking Sector as a bank with vision.

Objectives of the study

The main objective of the report will be to provide an overview of the “General Banking Activities of Prime Bank Limited‟‟- a study on Ring Road Branch with fulfilling the requirement of BBA program. However, the objective behind this study is something broader. Objectives of the report are summarized in the following manner-

- To analyze the general banking activities of Prime Bank Limited (PBL).

- To identify problems related to general banking activities of PBL.

- To make some recommendations to solve the problems of PBL.

Rational of the study

This report is broadly organized into two broad parts. The first part is an overview of the organization itself. The second part concentrates on the assigned topic “A study on the “General Banking Activities” of Prime Bank Limited. Finally it includes the evaluation of findings, recommendation and conclusion to make understood the scope of General Banking Activities with its constrain PBL.

Historical Background of Prime Bank Ltd

The declaration of the Government’s far sighted decision to allow banks in the private sectors to play its due role in the economy of Bangladesh, have started the process of creating new and dynamic financial institutions. Prime Bank Limited is such an institution. The emergence of PBL in the private sector is an important event in the banking arena of Bangladesh. Prime Bank Ltd. entered the Bangladesh banking industry in April 1995 with the firm commitment of excellence in customer service with a difference. As a second generation bank it has been an industry pioneer in providing innovative products, superior service quality, having a strong ethical governance and professional corporate culture. Its vision remained to be the best private commercial bank in Bangladesh in terms of efficiency, capital adequacy, asset quality, profitability along with strong liquidity.

Prime Bank Ltd. has a large and well distributed network of branches in Bangladesh. It has 122 branches and 18 SME branches covering strategic financial centers. It has 3 Off-shore banking units at different EPZs in Bangladesh. It has fully owned exchange houses at Singapore and UK facilitating to serve non-resident Bangladeshi customers living in Singapore and United Kingdome. It has a fully owned finance company in Hong Kong which provides foreign trade financing services to its client. It has active presence in the country‟s capital market through Prime Bank Investment Limited and Prime Bank Securities Limited.

Prime Bank offers a wide range of financial products and services which include commercial banking through both conventional banking and Islamic banking mode, merchant and investment banking, SME & retail banking, credit card and Off-shore banking. It plays leading role in Syndicated & Structured Financing as well. It has expertise in corporate credit and trade finance and has successfully made extensive market penetration with continuous growth in corporate, commercial and trade finance sectors.

The bank has been enjoying a good streak of ratings from the country‟s two most significant rating agencies – CRISL and CRAB. As per CRISL ratings, Prime Bank has a long term rating of “AA” and short term rating of “ST-2”. In terms of CRAB ratings, the long term rating of Prime Bank Ltd. “AA2” and the short term rating is “ST-2”. The bank has earned an outlook status of „Stable‟ from CRAB.

Prime Bank Limited has been licensed by the Government of Bangladesh as a scheduled Bank in the private sector in pursuance of the policy of liberalization of banking and financial services and facilities in Bangladesh. In view of the above, the PBL has, within a period of 20 years of its operation, achieved a remarkable success and always met up capital adequacy requirement set by Bangladesh Bank.

Division of PBL (Ring Road Branch)

- General Banking & Deposit Management:

- Account opening and KYC procedures.

- Issuance of DD/TT/PO/FDR.

- Inter-bank Transaction, OBC/IBC.

- Account section.

- Clearing Section.

- It Section.

- Foreign Remittance

- Credit Department:

- Credit Proposals Processing Procedures.

- Documentation and Loan Disbursement Procedures.

- Overview on all returns.

General Banking Activities of PBL

General banking is the starting point of all the banking operations. It is the department, which provides day-to-day services to the customers. Main Functions of general banking department are the followings:

Account Opening Section

Account Opening

To build Banker and customer relationship, Account opening is the first step. Opening of an account binds the Banker and customer into contractual relationship. But selection of customer for opening an account is very crucial for a Bank.

Prime Bank Ltd. opens the following accounting

The procedure for opening a general account is provided below –

Step1: Bank provides account opening form to the prospective customer or applicant.

Step 2: Applicant fills up the form.

Step 3: Application submits the form dully signed by an introducer and along with 2 passport size photo signed by the introducer.

Step 4: The authorized officer scrutinizes the application form.

Step 5: If they are satisfied, they will open the account.

Step 6: They issue deposit slip and deposit must be made it.

Step 7: After deposition one checkbook is issued Signature card to verify the signature of the client.

Step 8: Bank preserves the specimen.

Step 9: Account is opened

Closing of an Account

An account holder can close his/her account any time he wants in order to terminate banker customer relationship. He must make an application mentioning his intention to close his/her accounts and he/she must also deposit the unused leaves of the cheque book.

After verifying the genuineness of the application bank closes the account but Tk. 50/- for savings and Tk. 100 for current account is charged as closing fees. The operation of the account might be ceased by the bank side also due to the following reasons:

- Notice given the customer himself.

- Death of customer.

- Customer insanity or insolvency.

- Order of the court / Injunction of the court.

- Garnishee Order

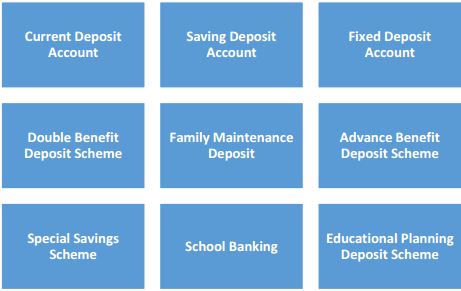

Various Types of Deposit Account

PBL offers following types of Deposit Accounts

Clearing Section

The main function of clearing section is to operate with safety and security of financial transaction of financial instrument like DD (Demand Draft), PO (Pay order), check etc. on behalf of the customers through Bangladesh Bank Clearing House, Outside Bank Clearing (OBC), Inter Branch Clearing (IBC.

Types of Clearing:

1) Outward Clearing

2) Inward Clearing.

Outward Clearing

When the Branches of our Bank receive cheques from its customers drawn on the other Banks within the local clearing zone for collection through Clearing House, it is Outward Clearing. The procedures of Outward Clearing are followed:

- The instruments are received duly signed vouchers.

- The clearing stamps are affixed on the instrument and it is endorsed with the checking of in charge.

- The particulars of the instruments and the vouchers are entered in the outward clearing register.

- The instruments with schedules received from branches and sent to the clearing house to deliver them to the respective bank.

- These sorts of things are submitted in the first houses or delivery house of Bangladesh Bank.

Inward Clearing

When the checks of its customer are received for collection from other banks, the following should be checked very carefully;

- The check must be crossed.

- The check should not carry a date older then the receiving date for more than 6 months.

- The collecting bank must check whether endorsement is done properly or not.

- The amount both in words and figures in deposit slip should be same and also it should be in conformity with the amount mentioned in words and figures in the checks.

Cheque Book

A cheque is “A bill of Exchange drawn of a specified banker and not expressed to be payable otherwise than on demand”. To facilitate withdrawals and payments to third parties by the customer, bank provides a cheque book to the customer cheque book contains 10 leaves for savings account while for current account there are 20 or 50 leaves.

Dishonor of cheque

If the cheque is dishonored, the branch sends a memorandum (cheque return memo) to the customer stating one of the following reasons:

- Refer to drawer

- Not arranged for

- Effects not cleared. May be presented again

- Exceeds arrangements

- Full cover not received

- Payment stopped by drawer

- Payee‟s endorsement irregular/ illegible/required

- Payee‟s endorsement irregular, require bank‟s confirmation

- Drawer‟s signature differs/ required

- Alterations in date/ figures/ words require drawer‟s full signature

- Cheque is postdated / out of date/ mutilated

- Amount in words and figures differs

- Crossed cheque must be presented through a bank

- clearing stamp required cancellation

- Addition to bank‟s discharge should be authenticated

- Cheque crossed “Account payee Only”

- Collecting bank‟s discharge irregular/ required.

If the cheque is dishonored due to insufficiency of funds, branch charges TK 50 as penalty

Bills Collection

If a party gives a Cheque to a branch of Prime to collect money from a branch of other bank, which is not situated in the clearinghouse then Prime collects money through OBC. In case of

OBC two ways exist to collect money from another bank.

Remittance Section

The word „Remittance‟ means sending of money from one place to another place through post and telegraph. Commercial banks expose this facility to its customers by means of receiving money from one branch of the bank and making an easier arrangement for payment to another branch within the country.

Prime remittances are safe, swift, inexpensive and simple. Different types of remittances remitted by Prime Bank are

1) Pay Order (PO)

2) Demand Draft (DD)

3) Telegraphic Transfer (TT)

Pay Order (PO)

Payment Order is a process of money transfer from payer to payee within a certain clearing area through banking channel. It’s an order of local payment on behalf of the bank or its constitution.

A customer can purchase different modes of payment Order such as pay order by cash and pay order by check.

Pay order (Issue)

Following procedure is maintained for the issuance of PO:

- Customer is supplied with PO form.

- After filling the form the customer pays the money in cash or by cheque.

- The concerned officer then issues PO on its specific block. This block has three parts, one for bank and other two for the customer. A/C Payee crossing is sealed on all pay orders issued by the bank.

- The officer then writes down the number of the PO block on the PO form.

- Two authorized officers sign the block.

- At the end customer is provided with the two parts of the block after signing on the back of the banks part.

Pay Order (Payment)

As the PO issued by the bank is crossed one it is not paid over the counter. On the contrary the amount is transferred to the payees‟ account. To transfer the amount the payee must duly stamp the PO.

- Demand Draft

This is an order to pay money, drawn by one office of a bank upon another office of the same bank for a sum of money in any place, which is outside of the clearing house area of issuing branch. It is a negotiable instrument. It can be crossed or not. For payment of DD bank checks the „Test Code‟ first mentioned on the draft. If test code agrees, then the bank makes payment. The issuing bank sends an advice about the DD to the paying branch, for further confirmation. Demand Draft is an instrument containing an order by the issuing branch upon another branch known as drawee branch, to pay a certain sum of money to the payee or to his/her order on demand.

Demand Draft Issue

- Customer is supplied width DD form.

- Customer fill up the form which includes the name of the drawer, name of the payee, amount of money to be sent, exchange, name of the drawee branch, signature and address of the drawer.

- The customer may pay in cash or by transferring the amount from his/her account (if any).

- After the money is paid and the form is sealed and signed accordingly it is given to the DD issuing desk.

- Upon receiving the form concerned officer issue a DD on a particular block.

- DD block has two parts, one for bank and another for customer.

- Bank‟s part contains issuing date, drawer‟s name, payee‟s name, sum of the money and name of the drawee branch. Customer‟s part contains issuing date, name of the payee, sum of the money and name of the drawee branch.

- After furnishing all the required information entry of the DD is given in the DD issue register and at same time bank issue a DD confirmation slip addressing the drawee branch. This confirmation slip is entered into the DD advice issue register and a number is put on the confirmation slip from the same register. Later on the bank mails this slip to the drawee branch.

At least two officer sign the DD block and the amount is sealed on the DD with a special red seal to protect it from material alteration. The number of DD is put on the DD form. Next the customer signs on the back of the DD and is supplied with his/her part of DD.

Duplicate DD issue

If the customer reports that original DD purchased by him/her is lost or stolen and produces legal documents then the bank may issue a duplicate DD.

Demand Draft Payment

When a DD is brought for payment, the branch check out the following matters:

- Whether the DD is drawn on them

- Whether it is crossed or not

- Whether it is properly signed by authorized officers of the issuing branch

- The branch then checks out whether the confirmation slip has arrived or not

- If the confirmation has not arrived, the DD is given entry in the Ex-advice register.

Stop Payment of Demand Draft

The issuing can issue instructions to the drawee bank to stop the payment of the DD issued by them only on written request of the drawer and should inform the drawee bank immediately. Once the drawee branch made the payment, no action can be taken against it.

Telegraphic Transfer (TT)

In case of TT the issuing branch sends a telegraphic message to another branch to pay a certain some of money to a named payee account. Test code is furnished on the TT message for the protection of it. Generally for such kind of transfer, payee should have account with the paying bank; otherwise it is very difficult for the paying bank to recognize the exact payee.

At customer‟s request branch transfers fund to another branch through telex and it is known as the TT, in short. TT facility is available only in that branch having telex facility. The procedure of issuing and paying TT‟s are stated below:

TT (Issue)

- Customer fills up the TT form and pays the amount along with commission in cash or by cheque.

- The respected officer issues a cost memo after receiving the TT form with payment seal, then signs it and at last give it to the customer.

- Next a TT confirmation slip is issued and its entry is given in the TT issues register.

- A test number is also put on the face of the slip. Two authorized officer signs this slip.

- Telex operator then transfers the message to the drawee branch mentioning the amount, name of the payee, and name of the issuing branch, date and test number.

- The confirmation slip is send by post.

TT (Payment)

- When a TT arrives through telex it is sent to the respected officer for the verification of the test number. If the test number is OK, the officers write down „Test Agreed‟ on it and sign it. Otherwise a message is sent back to the issuing branch for the correction of the test number.

- After agreeing the test the branch issues a debit voucher and accredit voucher – debiting the issuing branch and crediting the payees account. Branch also issues a credit advice slip addressing the payee informing him/her about the arrival of the money.

- Later, when the confirmation slip arrives the contra date, on which the payment was made, is put on it and the officer sign it.

Cash Section

Cash is the most liquid asset and it should be dealt very carefully. So this department is really handed with intensive care. This department starts the day with cash in vault. All cash receipts and payments are made through this department.

Cash section is a very sensitive organ of the branch and handle with extra care. I was not authorized to deal in this section because of its sensitivity. But I was fortunate enough to know the procedures of this section. Operation of this section begins at the start of the banking hour. Cash officer beings his/her transaction with taking money from the vault, known as the opening cash balance. Vault is kept in a much secured room. Keys to the room are kept under control of cash officer and branch in charge. The amount of opening cash balance is entered into a register.

After whole day‟s transaction, the surplus money remains in the cash counter is put back in the vault and known as the closing balance. Money is received and paid in this section.

Cash Receipt

When clients deposit cash in the bank, the bank officer on receipt of the cash and the pay in slip/credit voucher shall:

- Check and count the received cash.

- Make sure that the amount in word and number in the deposit slip are same.

- Check the account title and the number.

- Both the deposit slip is in order.

- Depositor‟s signature is in the slip.

- Receive seal in the slip is a must.

- Write the domination of the currency at the back of the pay in slip or the credit voucher and affix stamp in the slip/voucher.

- Enter particulars of in slip/credit voucher in the receiving cash officer book.

- At least, send the pay in slip/voucher to the deposit department or to the respective department.

- Deposit slip must be signed by the respective officer.

- Carbon copy of the deposit slip must be handover to the client with proper seal and signature.

Cash Payment

Cheques, demand drafts, pay orders, pay slips and debit cash vouchers etc. are received from various departments for payment of cash to customers/payees. Prior payment of cash it is the officer‟s duty to make sure that the cheque/or the instrument has been genuinely passed.

The following common precaution is thoroughly practiced before honoring a cheque:

- Check of it is an open or crossed check.

- The branch name in the cheque.

- The date in the cheque is very crucial. Cheques are normally valid six months and predated cheques are asked to present after the date given.

- Tk in words and figure of the cheque is same.

- Balance in the account is available.

- The apparent tenor of the cheque. Whether any figure, date or anything has been altered in the cheque presented. If any, then the respective officer must check whether the client is making his signature for alteration or not.

- The specimen card signature and signature in the cheque should match.

- Signature of recipient is obtained on the reverse of cheque.

- In case, where a prior arrangement has been made with the bank, a client may overdraw against a cheque.

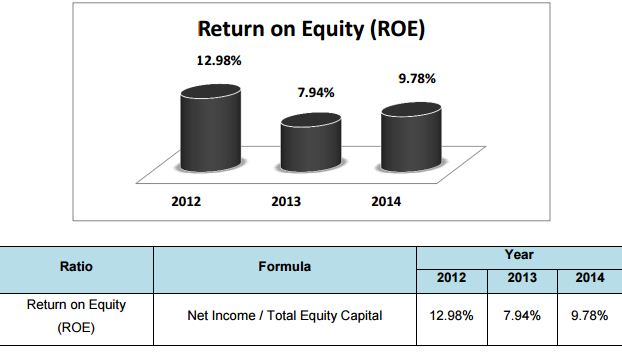

Ratio Analysis of Prime Bank Limited

Interpretation:

The return on equity ratio (ROE) measures how much the shareholders earned for their investment in the company. The higher the ratio percentage, the more efficient management is in utilizing its equity base and the better return is to investors. Over the last three years the ROE ratio of PBL has been fluctuating. In 2014, Prime Bank‟s Shareholders earned TK.9.78 for every TK.100 invested into the bank.

Interpretation:

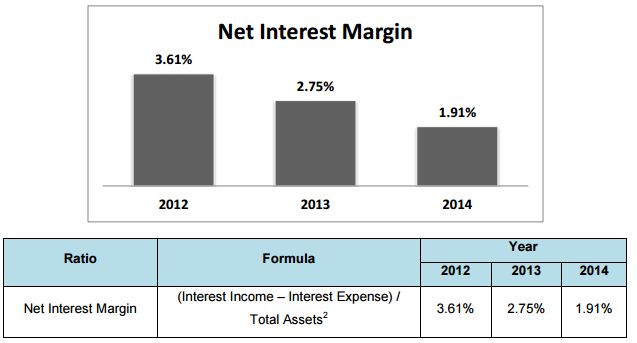

Net interest margin is a measure of how successful a firm’s investment decisions are compared to its debt situations. A negative value denotes that the firm did not make an optimal decision, because interest expenses were greater than the amount of returns generated by investments. On the other hand, Positive value refers that returns are greater than interest expenses. Over the last three years Net Interest Margin of PBL has been decreasing. In 2014,

Net Interest Margin of PBL is 1.91% which is positive that means investing strategy is successful.

Interpretation:

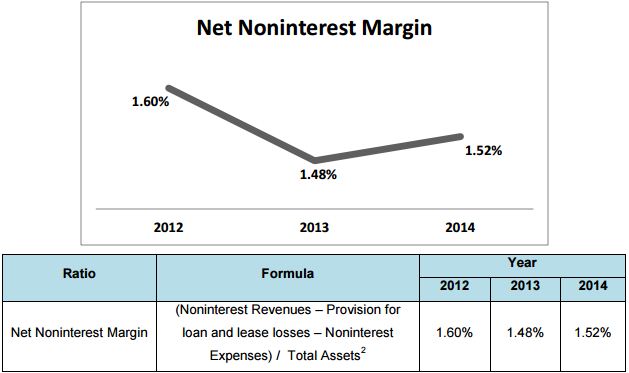

The Net Noninterest Margin measures the amount of non-interest revenues stemming from service fees the financial firm has been able to collect relative to the amount of non-interest costs incurred (including salaries and wages, repair and maintenance of facilities, and loan loss expenses). Over the last three years Net Noninterest Margin of PBL has been fluctuating. In, 2014 Net Noninterest Margin of PBL 1.52 % which is positive that means noninterest revenues are greater than non interest costs.

Recommendation

After completing my survey and informal interview with the customers of General Banking Department of Prime bank Ltd, I have recognized some problems that have been facing by the customers. These problems are given below:

- Account Opening Procedure

- Lengthy Procedure to Deposit & Withdraw

- Interest Rate

- Customer Care

- Scarcity of employees

- Lack of Trained Manpower

- Evening Service

- Process Complexity while Dealing with Big Transaction.

- Dissatisfaction with ATM Facilities and No. of ATM Booth

- Consciousness about customer opinion

- Shortage of locker service

After observing these consequences I have recommended some solutions, which are given below:

Account Opening Procedure:

During the survey and informal interviews with the customers I came to know that the introducer for Savings and Current Account is one of the major problems to them. Though now PBL has started online banking but all of its branches are not online. On the other hand the signature of the customers of other branches most of the times are not scanned so that if any customer of other branch of PBL introduces the applicant then it is impossible to verify the signature. To solve this problem the online branches should update their account holders‟ signature regularly and the process of on-line conversion of the banks must be faster.

Lengthy Procedure to Deposit & Withdraw:

Prime Bank Limited, Ring-Road branch should provide quick service of deposit and withdrawal of cash for their valuable customers. As the customers need not wait for long time so more cash counting machine and sufficient manpower should be provided in this area.

Interest Rate:

PBL should increase its interest rate of some of its products by this it can attract more customers willing to open their accounts in the bank.

Customer care:

Ring-Road Branch of Prime Bank Limited should more concern about customer service. It should provide more trained manpower to support the customer and help them to solve their enquiries.

Lack of Manpower:Trained

While doing my internship in Ring-Road Prime Bank, I have noticed that there are shortages of manpower only eleven officers are employed in Ring-Road branch. “”It has huge number of customers but to deal with these customers the manpower is not sufficient. So that there must be right number of employees in the right place and the PBL should provide behavioral training to the employees to deal with the customers more efficiently and more smartly.

Evening Service:

Now a day evening banking is well-known and warmly acceptable services from the perspective of the customer. In today‟s busy world everybody is busy with his or her activities in the whole day. It is difficult for them to find out a few times to go to the bank. So if the bank especially Ring-Road branch establish their evening banking services then it will be beneficial for the customer.

Process Complexity while Dealing with Big Transaction:

If anyone wants to withdraw a big amount of money he needs to inform the branch 7 days earlier. So if anyone needs instant money he/she cannot withdraw money at that time. So the branch needs to increase its fund capacity.

Dissatisfaction with ATM Facilities and No. of ATM Booth:

Few days ago Ring-Road Branch has started its ATM facility. It should provide ATM debit Cards to its valued customers faster so that the satisfaction level of the customers accelerated. On the other hand PBL should increase its number of ATM booth to make convenient use for its customers.

Consciousness about Customer Opinion:

Customer opinion is very important for the development of a service oriented organization. So if the branch consider the customers opinion then it will be helpful to the Bank also. They can place a customer opinion box where the customer can write down their opinion and drop that to the box. By this the banks can get important information from their client and the customers also think that they are valuable to the bank.

Shortage of Locker Service:

While doing my internship in Ring-Road Prime Bank, I have noticed that in Ring-Road Branch of PBL there is shortage of Locker. No new customer can occupy a locker in this branch so that the customers who live close to the branch have to face difficulty to go for another branch. If this branch can increase its locker facility then it will be helpful to for the customers.

Conclusion

In this competitive market Prime Bank Ltd. competes not only with the others commercial banks but also with the public Bank sector banks and has been able to throw in more positive contributing towards economic development of Bangladesh as compared to other banks. The organization is much more structured and it is relentless in pursuit of business innovation and improvement. It has a reputation as a leader in financing manufacturing sector. Client Relationships unit of Prime Bank has the major contribution to the overall revenue of the bank. This core unit of corporate banking group is with the basic job of attracting and persuading new customers as well as providing superior service value to the existing customers. Prime Bank needs to restructure its client relationships department, should concentrate more on relationship manager recruitment and development process, and should ensure more cordial working environment and more sincere efforts from the relationship managers. As client relationships performance depend on proper functioning of a group of internal departments as a team, internal co-ordination should be ensured. Moreover Client Relationships department needs to be more customer-oriented.