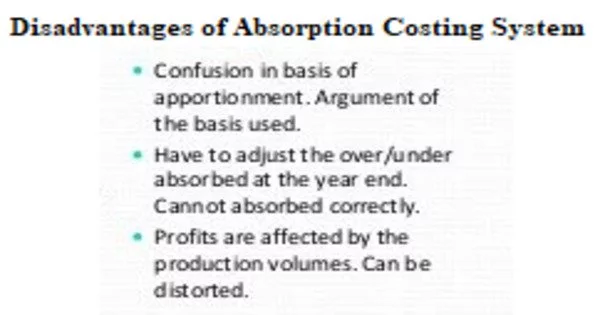

Absorption costing can provide invaluable insight into the total cost of manufacturing a single product. Though absorption costing is extremely useful, there are some drawbacks to this costing method. Absorption costing is not useful for product decision-making because it includes allocating fixed manufacturing overhead to the product cost. Absorption costing provides an inaccurate estimate of the true cost of manufacturing a product. As a result, variable costing is used to assist management in making product decisions.

The main disadvantages of absorption costing are given below:

- Over-assigning overhead costs

Even overhead costs that cannot be directly traced back to the product are assigned to each unit with absorption costing.

Absorption Costing, unlike Marginal Costing, cannot be used as an effective monitoring tool to evaluate a company’s profitability. This is because absorption costing includes fixed costs in the cost of the product, which will remain constant regardless of output or production, whereas marginal costing is based on contributions earned per unit, which includes only the variable costs of the product.

- Overproduction to cut costs

This pricing method allows for increased profitability by overproducing a product. This is because the fixed overhead is assigned to the total number of produced units, lowering the cost for each additional unit produced. When units are not sold, the fixed overhead costs are not transferred to expense reports, increasing profitability.

Because the cost of the product is based on both fixed and variable costs, this method cannot be used for management decision-making or planning subsequent actions such as forecasting, budgeting, and so on.

- Incomplete data

Fixed overhead is included in the data gathered for determining a product’s cost through absorption costing. This can inflate the actual cost of manufacturing and lead to insufficient data for a thorough analysis.

Absorption costing can improve the appearance of a company’s performance. This is because fixed costs are directly included in product costs and are not deducted from revenues until the sale is realized and the products are actually sold. As a result, this procedure can be used to manipulate a company’s profitability status and increase the likelihood of ‘creative accounting,’ which could ultimately mislead stakeholders’ economic decisions, particularly potential investors.

- Uninformed profitability

Absorption costing can provide an incomplete picture of a company’s profit levels because fixed costs cannot be deducted from revenue until the units are sold. This can result in costs that go unaccounted for on an income statement, temporarily increasing a company’s apparent profitability on the balance sheet.

Absorption costing makes cost volume profit (CVP) analysis difficult because the addition of fixed costs makes determining variations in the variable cost of the product difficult. It makes assessing the efficiency and effectiveness of the company’s operations difficult for management.

Profits for a period must be adjusted for under/over absorption of fixed costs. This situation arises because the fixed overheads absorbed into product costs are estimated, whereas original overheads are realized when actual fixed costs are incurred. This can make profit calculation complicated and difficult, especially when a company has a large number of products.