Difference between Consignment and Sales

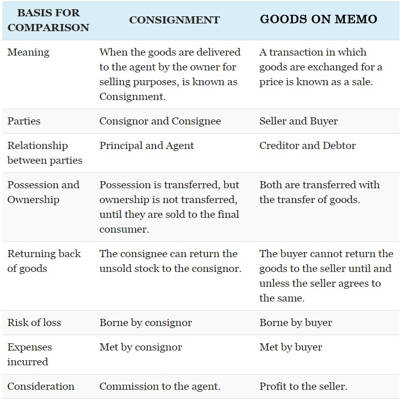

Consignment can not be treated as sales of goods. When the goods are delivered to the agent by the owner for selling purposes, it is known as Consignment. It is different from sales. A transaction in which goods are exchanged for a price is known as a sale. The difference between consignment and sales are as follows:

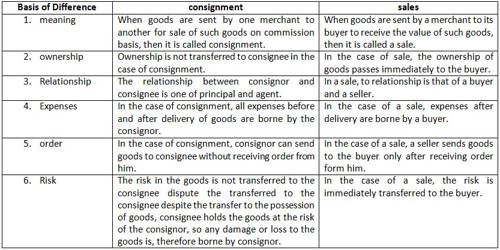

(1) Ownership

- Consignment: The ownership of the goods remains with the consignor until sales is effected by the consignee. Possession is transferred, but ownership is not transferred until it is sold to the final consumer. Legal ownership is not passed on to the agent but is within the consignor.

- Sales: The ownership of the goods immediately transferred to the buyer when the sale is effected. Sale refers to the transfer of property from the seller to the buyer. Legal ownership of the goods is passed on to the buyer.

(2) Relationship

- Consignment: The relationship between the consignor and consignee are of principal and agent. Their relationship are continued until terminated. The reason is that the consignee sells goods on behalf of the consignor.

- Sales: The relationship between the two parties is that of seller and buyer and they terminated as soon as payment is made and goods are delivered. The relationship between the seller and the buyer is that of creditors and debtors.

(3) Expenses

- Consignment: The expenses incurred by the consignee to execute sale and the expenses incurred by the consignor to send the goods to the consignee, both are borne by the consignor. All the expenses on the goods are to be borne by the consignor.

- Sales: Any expenses incurred after the sale is not borne by the seller. All the expenses on the goods are to be borne by the buyer unless agreed.

(4) Risk

- Consignment: The risk of goods under consignment is always with the consignor.

- Sales: When the sale is made the risk is transferred to the buyer. The risk of the goods is transferred to the buyer as the sale made.

(5) Return of Goods

- Consignment: Consignee can return goods to the consignor since those are properties of the consignor.

- Sales: A buyer can not return goods unless the goods are found defective or damaged or the seller agrees to.

(6) Statement

- Consignment: Forgiving details about the goods sold and expenses incurred by him, the consignee sends the account sales to a consignor.

- Sales: The buyer need not submit any account sales to the seller.

(7) Stock

- Consignment: The unsold stock with the consignee will be treated as a stock of the consignor.

- Sales: In the case of a sale, the buyer’s unsold stock does not attract the seller.

(8) Commission

- Consignment: Commission is the main consideration of consignment. The consignee performs the selling activity only for commission.

- Sales: Profit is the main consideration of sales.

There are many forms of sale and consignment is one of the forms of sale. In the case of the sale, the possession, as well as ownership of the goods, is immediately transferred to the buyer.

Information Source: