In economics, the debt-to-GDP ratio is the ratio of a country’s government debt (measured in currency units) to its gross domestic product (GDP) (measured in units of currency per year). The debt-to-GDP ratio is a reliable indicator of a country’s ability to repay its debts since it compares what it owes to what it generates. In other terms, the debt-to-GDP ratio compares a country’s annual economic production to its public debt. A low debt-to-GDP ratio shows that an economy’s ability to produce and sell goods and services is sufficient to repay loans without accumulating new debt.

Regularly communicated as a rate, this ratio can likewise be deciphered as the quantity of years expected to take care of obligation, in case GDP is committed completely to obligation reimbursement. International and monetary contemplations including financing costs, war, downturns, and different factors impact the acquiring practices of a country and the decision to bring about additional obligation. The greater the debt-to-GDP ratio, the less likely the country is to repay its debt and the greater the chance of default, which might generate financial panic in domestic and international markets.

The debt-to-GDP ratio measures the strength of a country’s economy and its likelihood of repaying its debt. It’s used to evaluate debt levels between countries and determine whether a country is on the verge of economic collapse. It should not be mistaken with the deficit-to-GDP ratio, which quantifies a country’s annual net fiscal loss (total expenditures minus total revenue, or the net change in debt per year) as a percentage of GDP for nations with budget deficits; for countries running budget surpluses, a surplus-to-GDP ratio measures a country’s annual net fiscal gain as a share of that country’s GDP.

The formula for calculating the ratio is as follows:

Debt-to-GDP Ratio = Debt / Gross Domestic Product

Where:

Debt is the cumulative amount of a country’s government debt

Gross Domestic Product is the total value of goods produced and services produced over a given year

A country with a high debt-to-GDP ratio typically has trouble paying off external debts (also called “public debts”), which are any balances owed to outside lenders. A ratio is a useful tool for investors, leaders, and economists. It allows them to gauge a country’s ability to pay off its debt. In such scenarios, creditors are apt to seek higher interest rates when lending. Extravagantly high debt-to-GDP ratios may deter creditors from lending money altogether.

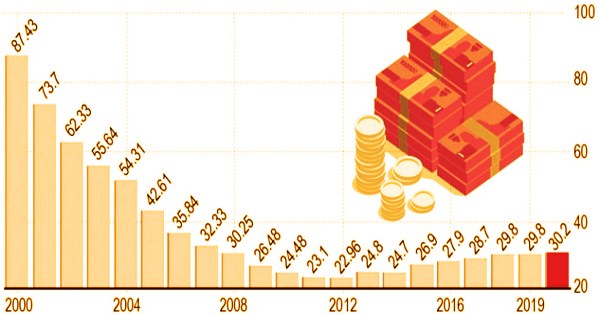

At the end of the 1st quarter of 2021, the United States public debt-to-GDP ratio was 127.5%. According to the IMF World Economic Outlook Database (April 2021), the level of Gross Government debt-to-GDP ratio in Canada was 116.3%, in China 66.8%, in Germany 70.3%, in France 115.2% and in the United States 132.8%. A high ratio means a country isn’t producing enough to pay off its debt. A low ratio means there is plenty of economic output to make the payments. If a country were a household, GDP is like its income.

Although governments strive to lower their debt-to-GDP ratios, this can be difficult to achieve during periods of unrest, such as wartime, or economic recession. In a study conducted by the World Bank, a ratio that exceeds 77% for an extended period of time may result in an adverse impact on economic growth. It was indicated that each additional percentage point of debt above that level reduced annual real growth by 1.7%. In such challenging climates, governments tend to increase borrowing in an effort to stimulate growth and boost aggregate demand. This macroeconomic strategy is a chief ideal in Keynesian economics.

The debt-to-GDP ratio is commonly misunderstood, as many think that a ratio exceeding 100% indicates a bankrupt or insolvent country. The change in debt-to-GDP is approximately “net change in debt as a percentage of GDP”; for government debt, this is a deficit or (surplus) as a percentage of GDP. Economists who adhere to modern monetary theory (MMT) argue that sovereign nations capable of printing their own money cannot ever go bankrupt, because they can simply produce more fiat currency to service debts.

Subsequently, the ratio doesn’t offer solid bits of knowledge into a country’s probability of default. Financial backers will be glad to assume a nation’s obligation in the event that it has a moderately more significant level of monetary yield. Investors who are concerned about repayment will perceive a higher danger of default, resulting in a higher demand for a higher interest rate return on their investment. This raises the country’s debt service costs. Debt costs can easily spiral out of control, resulting in a debt crisis.

At the end of World War II, in 1946, the United States had the largest debt-to-GDP ratio in the world, at 106 percent. 4 Debt levels rapidly declined from their post-World War II highs, plateauing at 31 and 40 percent in the 1970s before falling to a historic low of 23 percent in 1974. In any case, within the sight of critical expansion, or especially excessive inflation, GDP may increment quickly in ostensible terms; assuming obligation is ostensible, its proportion to GDP will diminish quickly. A time of collapse would have the contrary impact.

External debt is seen to have negative consequences for a country’s economy. Goal 17 of the United Nations Sustainable Development Agenda, which is an integral aspect of the 2030 Agenda, aims to alleviate debt distress by addressing the foreign debt of highly indebted poor nations. A high ratio is acceptable, however, provided a country can pay interest on its debt without refinancing or negatively impacting its economic growth.

Japan’s debt-to-GDP ratio, for example, was 253 percent in 2017 (higher than Greece’s 177% in 2017). Despite the fact that Japan’s debt-to-GDP ratio is substantially larger than that of other countries, economists believe the country’s danger of default is extremely low. Due to the fact that the majority of Japanese government bonds are held by the country’s residents, which results in extraordinarily cheap interest rates, Japan is able to sustain and remain afloat despite a staggering ratio.

As a country’s obligation to-GDP ratio rises, it frequently flags that a downturn is in progress. A country’s GDP diminishes in a downturn. There is a contrast between outside obligation named in homegrown money and outer obligation named in unfamiliar cash. In an optimal situation, financial improvement spending is effective, and the downturn lifts. The stimulus boosts economic activity, which raises taxes and federal revenue, allowing the debt-to-GDP ratio to be brought back into balance. Tax revenues can be used to service external debt denominated in local currency, but to service foreign currency debt, tax revenues must be converted to foreign currency in the foreign exchange market, putting downward pressure on the value of the country’s currency.

Information Sources: