Background of the work study:

Achievement of high economic growth is the basic principles of present economy policy. In achieving the objectives the banking sector places an important role. The banking sector channel resources through deposit mobilization and providing credit for different business venture. The successful running of a bank business depends upon how effective the credit management recovered the funds. NCCBL as a new commercial bank in Bangladesh responsibility bestows upon it to ensure efficient and effective operation and sound manner. The main objectives of NCCBL are

# To ensure the safety of depositor and give them different types of credit facilities, consumer credit is one of its kinds of credit facilities which help limited income people to buy any house hold effects including car, computer and other consumers durable.

# Credit management is mainly concerned with the credit disbursement and recovery in order to strength credit management and recovery position of the loans/advances by a bank it has been decided by NCCBL to follow some tools and technique for credit appraisal. With the use of such tools NCCBL credit management has shown there efficiency.

NCCBL is always ready to mention the highest quality of services by upgrading banking technology prudence in manage and by applying high standing of business ethics through its established commitment and heritage objective of a private intuition like NCCBL is to maximize profit through optimum utilization of resources by providing best customer service.

Objective of the study:

The main objective of the study is to know the overall operational performance of National Credit and Commerce Bank Ltd, through different aspects of the banking sector and its effectiveness in this regard:

The specific objectives of the study are given below:

¨ To gather comprehensive knowledge on overall banking functions of NCCBL.

¨ To trace origin of the NCCBL.

¨ To identify the weakness and problem in successful/effective credit management system.

¨ To analyze the disbursement and recovery performance of loans and advances.

¨ To understand the need and objective of credit management.

¨ To have and idea of the existing systems of loan and advances innovated and practiced by the NCCBL.

¨ To explain the meaning and concept of credit management.

¨ To acquire in depth knowledge on about NCCBL credit management.

Scope of the study

This report covers NCCBL’s organizational over view, management & organizational structure, functions performed by NCCBL. Its also covers over view of the credit Division, identification of problems regarding credit extended & sector of credit allocation of NCCBL MIRPUR BRANCH.

Origin of the report

For a student of MBA (29th Batch), StamfordUniversity, Dhanmaondi Campus,Dhaka. It is a requirement after the examination of last semester to attach with a financial institution and prepare a thesis report. To fulfill this requirement I was work as an intern in National Credit and Commerce Bank Ltd for several times. This not only fulfills the requirement of the programmed but also facilitates the dissemination of knowledge in the banking arena of Bangladesh and helps me a lot to compare theoretical knowledge with practical experience. The proposed topic is “credit management & its administration” in case study of NCCBL”. The topic is assigned by Ms. Rima Pervin, honorable course teacher StamfordUniversity, Dhanmondi campus Dhaka.

Methodology Of the report:

The study requires various types of information past and present policies, procedures and methods of credit management. Both primary and secondary data available have been used in preparing this report.

Sources of data:

- primary sources:

Discussion with officials of NCCBL.

Experts opinions comments.

- secondary sources:

Relevant books, newspapers, journals etc.

Monthly reports.

Published documents.

Office circular.

Other published papers, documents and reports.

And carefully developed, disguised queries, trend and growth rate analysis, ratio analysis, graphical presentation such as pie chart, bar, graph processed, edited for the purpose of the study.

Limitation of the study:

I have obtained whole-hearted co-operation from the employee of NCCBL mirpur branch and head in Dhaka. All the day they were extremely busy, but they gave me much time to make this report properly. I have faced the following problem which may be termed as the limitation/shortcoming of the study. These are:

- Short time period: The first obstruct is time itself. Due to the time limit, the scope and damnation of the study has been curtailed. For an analytical purpose adequate time is required. But I was no given adequate time to prepare such as in depth study.

- No availability of adequate data: To understand the facts about the study in a realistic way and more clearly the quantitative expression of information is represented by data. It was very difficult to collect data, which is very essential, because of the branch of NCCBL was newly established that’s why I could not provide necessary secondary data in all area of the study.

- Lack of records: Sufficient books, publications, fats and figures are not available. This constrict narrowed the scope of accurate analysis if this limitations were not been there, the report would have been more useful and attractive.

- Poor library facility: Most of the commercial bank have its own modern, rich and wealthy collection of huge and various types of banking related books, journals, magazines, papers, case studies, term papers, assignment etc. but the library of NCCBL is not well ornamented.

- Lesser experience: Experience makes a man efficient, I do such kind of research activity for the first time. That’s why inexperience creates obstacle to follow the systematic and logical research methodology.

Background & History:

Banking system occupies an important place in a nation’s economy. A banking institution is indispensable in a modern society. It plays a pivotal role in the economic development of a country. Against the background of liberalization of economic policies in Bangladesh, NCCBL emerged as a new commercial bank to provide efficient banking service with a view to improving the socio-economic development of a country.

National Credit and Commerce bank Ltd(NCCBL) started its operation in 25th November 1985 as a non banking financial institution under the name of National Credit Ltd(NCL).26 businessman sponsored it as a public limited company under the companies Act 1913 with an authorized capital of taka 300 million. NCC bank was incorporated as a banking company under the companies Act 1994. In end 2001 it had 30 branches all over Bangladesh. Its carries out all its banking activities through these branches among which 17 branches are authorized dealer of foreign exchange. The bank is listed in the Dhaka and Chittagong stock exchange as a private quoted company company for its general class if shares. The authorized capital of the bank is now taka 2500 million. The bank raised its paid up capital from taka 607.81 million during the year 2004 to taka 975.04 million during the year 2005 through IPO of which sponsor directors/stockholders equity stood at taka 1859 million. With the increase of paid up capital to taka 975.04 million, the capital base of the bank has become strong. NCC bank is now positioned to best suit the financial needs of its customers and make them partners of progress.

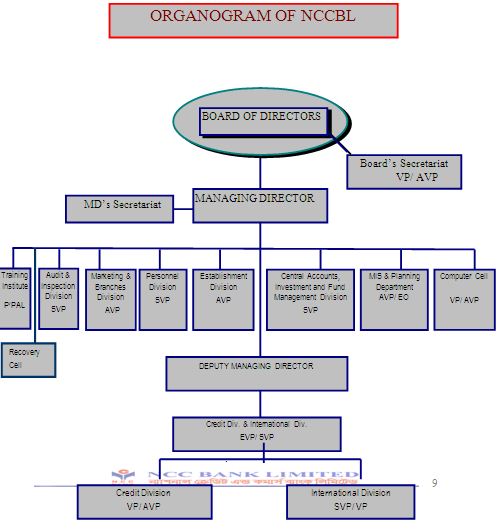

Management Structure of NCCBL:

Management of NCCBL is professional and experienced. Top management and policy formulation of the bank is vested on the board of Directors. The boars of directors consist if 26 members headed by chairman. Most of the directors are owners of the large business group having high net worth. The executives and officers of the bank execute the policies and programs formulated by the board. The managing director is the chief executive of the bank and he is assisted and supported by other qualified executives like Senior Executive vice-President, Executive vice president (EVP), Vice President (VP), senior assistant Vice president and other officers and staffs. There are nine divisions in this Bank and one training institute.

Organizational Chart of National Credit & Commerce Bank Ltd

Vision:

To be in the forefront of national development by providing all the customers inspiration strength, dependable support and the most comprehensive range of business solutions, through our team of professionals who work passionately to be outstanding in everything we do.

Mission Statement of NCCBL:

➢ To assist in bringing high quality service to their customers and to participate in the growth and expansion of our national economy.

➢ To set high standards of integrity and bring total satisfaction to their clients, shareholders and employees.

➢ To become the most sought after bank in the country, rendering technology driven innovative services by their dedicated team of professionals.

Corporate Objectives:

NCCBL’s objectives are reflected in the following areas:

➢ Highly personalized services.

➢ Customer driven focus.

➢ Total commitment to quality.

➢ Contribution in the economy .

➢ Quality of human resources.

➢ Commitment to its clients at each level.

The company believes that communication with ,and feedbacks from its clients help it achieves its goal of providing world-class product and services. NCCBL regularly conducts client satisfaction surveys and make immediate accommodations and adjustments where needed. It also constantly monitors its standards, and strives to meet clients requirements.

Strategies :

➢ To manage and operate the bank in the most efficient manner to enhance financial performance and to control cost of fund.

➢ To strive for customer satisfaction through quality and control and delivery of timely services.

➢ To identify customers credit’s and other banking needs and monitor their perceptions towards our performance in meeting these requirements.

➢ To review and update policies , procedure and practices to enhance the ability to expand better services to customers.

➢ To train and develop all employees and provide them adequate resources so that customers needs can be responsibly addressed.

➢ To promote organizational effectiveness by openly communicating company plans ,policies ,practices and procedures to all employees in a timely fashion.

➢ To cultivate a working environment that fosters motivation for improved performance.

➢ To increase direct contact with customers in order to cultivate a closure relation between the bank and its customers.

Qualitative analysis

SWOT Analysis:

SWOT analysis is an important tools for evaluation the company strengths, weaknesses, opportunities and threats. It helps the organization to identify how to evaluation which in turn would help the organization to navigate in the turbulent ocean of competition.

Strength:

a. Top Management:

The top management of the Bank is a key strength for the NCCBL contributed heavily toward the growth and development of the Bank. The top management officials have experience, skill and proficiency on banking.

b. Company Reputation:

National credit & commerce bank limited is a very creative and effective bank in the banking industry of the country chiefly among the new comes. NCCBL has already established a firm grip in the banking sector having tremendous growth in the profits and deposits within a phase often years.

c. Sponsors:

NCCBL has been founded by a group of prominent entrepreneurs of the country. The sponsors directors belongs large industrial conglomerates of the country. Md Nurul Amin is the head of the Board of Directors.

d. Modern facilities and computers:

Form the very beginning. NCCBL tries to furnish their work surroundings with modern equipment and facilities for the speedy services to the customers. The Bank has installed money-countering machine in the cash counter. The bank has computerized banning operations under the software called PC Bank. More over computer printed statements are available for internal use and occasionally for the customers. NCCBL is equipped with telex or fax facilities.

e. Stirring Branches:

From the very beginning of the NCCBL, the bank tries to furnish their branches by impressive style. These well decorated branches get the attention of the potential customers. This is one kind of promotional strategy. The Elephant Road Branch is also impressive and is comparable with the foreign banks.

f. Interactive corporate culture:

The corporate culture of NCCBL is very much interactive compare to our other local organization. This interactive environment encourages the employees to work attentively. The banking hours are very much routine work oriented and also lovely environment boosts up the capability of the employees.

g. Online Banking

Online banking system is another strength of NCCBL From the very beginning, they are using this. It saves the time for the organization and also for the clients.

Weaknesses:

a. Advertising and promotion:

Advertising and promotion are the one of the weak points of NCCBL. The bank doesn’t have any effective aggressive marketing activities. The lacking pushes the bank far behind the competitor. The directors of the bank are not so much interested to promote the bank. Now- a-days they are taking steps to overcome this.

b. Disguise employment:

Reference appointment is very much efficient in NCCBL. As a result there are many people who are looking for a good job within this organization, are becoming foolish for this. This is related to the problem of reference appointment. On the other hand there are officers who work hard but not getting values for this are leaving the Bank to the other Bank.

c. Limitation of information system:

PC bank is not comprehensive banning software. It is desirable that a more

comparative banking system should replace PC bank system.

d. Low remuneration package:

The Bank doesn’t give good payment to the entry level and mid level officers. They don’t want to see the experience of those peoples. This low pay structure doesn’t attract potential MBA and BBA. They are interested to join in the other banks than the NCCBL.

Opportunity:

a. Diversification:

NCCBL can pursue a diversification strategy in expending its current line of business. The management can consider options of starting merchant banking or diversify it to leasing and insurance. By expending business portfolio Mercantile Bank Ltd can consider business risk.

b. ATM:

This is the fastest growing modern banking concept. NCCBL can form al alliance with other contemporary banks in launching the ATM. There are some other banks have already launched ATM.

Threats:

a. Contemporary Banks:

The contemporary banks like Dhaka Bank, Prime Bank, Dutch Bangla bank, Islamic Bank Bangladesh Ltd. are its major competitors. They are carrying out aggressive campaign to attract lucrative corporate clients as well as large depositors. NCCBL should take necessary steps to compete with them. Otherwise they will affect the NCCBL strategies.

b. Multinational Banks:

The rapid expansion of multinational bank poses a potential threat to the NCCBL and other Banks also. Due to the booming energy sector, more foreign banks are expected to operate in Bangladesh. Moreover, the already existing foreign Banks such as HSBC, Standard Chartered Bank, City Bank, are formulating aggressive branch expansion strategy. The foreign banks have tremendous financial strength. It will create more threat to the NCCBL and its clients if they do not take necessary steps as soon as possible.

c. Upcoming Bank:

The upcoming private local banks can also create threats to the NCCBL. It is expected that in the next few yew years more local private bank may emerge. If that happens the intensity of competition will rise further and banks will have to develop strategy to compete with them.

Products and services:

Since the commencement of banking operation; National Credit and Commerce bank Ltd(NCCBL) has not yet only gained enormous popularity but also in successful in mobilizing deposit and loan products. The bank has made significant progress within a very short time period due to its dynamic management and introduction of various customer friendly loan and deposit products. There have also had other departments that can be termed as support and these are operations, credit administration, financial control and Human Resource.

All the products and services offered by the bank can be classified under three major heads:

Personal Banking

Deposit schemes:

n Savings Account .

n Current deposit Account.

n Locker Service.

n Fixed Deposit Receipt.

n Bearer Certificate of Deposit.

n Short Term Deposit.

Credit & loans:

n Consumer credit Scheme

Education Credit Scheme

Multipurpose loan

Loan General

n Education Credit Scheme

n Multipurpose loan

n Loan General

Foreign Currency Account:

n Resident Foreign currency Account.

n Non-Resident Foreign currency Account.

Corporate Banking

Small and Medium Business:

n Cash Credit Hypothecation (CC Hypo)

n Cash Credit Pledge(CC Pledge)

n Secured Overdraft.

n SOD against Work Orders.

Large Business

n Short Term Industrial Loan

n Mid Term Industrial Loan

n Long Term Industrial Loan

n Transport Loan

n CommercialHouseBuilding Loan

Foreign Trade

: National Credit and Commerce bank Ltd (NCCBL) provide solutions in the field of international business and trade finance.

n Letter of Credit(L/C)

n Back To Back letter of Credit(BTB)

n Loan Against Trust Receipt(LTR)

n loan Against Imported Merchandise(LIM)

n Packing Cash Credit(PCC)

n Export Development Fund(EDF)

n Payment Against Document(PAD)

n Bank Guarantee

Lease Financing:

An entrepreneur, under this scheme, may avail of the lease facilities to procure industrial machinery (without having to purchase it by down payment) with easy repayment schedule. The clients also get special rebate in their income tax payment under the scheme.

Islami Banking:

Some of the branch of NCC bank open profit loss sharing term/savings deposit amounts and also allow loans on Mudaraba, Musharaka, Murabaha system. Attractive profit is given at the end of the year after deducting the banks service fee through proper accounting.

Financial products:

Financial products of the National Credit and Commerce Bank Limited (NCCBL) are mainly in three different categories:

These are:

n Short term financing products

n Mid term financing products.

n Long term financing products.

Above categories of financing covers the following areas, which are draft with at general Credit Division.

n Agricultural sector.

n Large and medium term loan.

n Working capital financing in industrial units including small industries.

n Commercial Credit scheme and any other new product as and when launched for.

n Term loan in small industries

n Term loan in small industries.

n Term loan in commercial house building at urban area & transport loan.

n Commercial loan.

Micro Credit Financing:

To fulfill its commitment to play a vital role to its socio-economic development of the country NCC bank Ltd has introduce a small and medium scale credit scheme for its customers. The objective of the scheme is:

n To encourage and develop medium and small entrepreneurs.

n To provide credit with minimum complexity.

n To generate employment.

This scheme covers agricultural sector, small and cottage industry, service industry, household durable and consumer credit, information technology sector and energy sector. The amount of small and medium credit range from 5 Lac to 50 lacks.

Special services:

Consistent with the modern age and competing in a perfectly competitive market. The National Credit and Commerce Bank Ltd (NCCBL) has introduced some innovative banking services that are remarkable in a country like Bangladesh. T services offered by the bank are as follows:

ATM service:

The bank has joined the shared ATM network Bangladesh with a pool of 7 banks. The client of any member bank will have access to any ATM situated at different location of Dhaka city. This banks client will get 24 hours cash withdrawal and utility bills payment facility. 16 ATMs will be installed gradually in Dhaka city and the network will be extended to other cities if the country in the near future.

Credit Card:

To provide best possible customer services to its clients, the bank is going to launch Master Credit card shortly.

Money Grams:

Money Gram is one of the innovative products of the bank. This has been functioning satisfactory and rendering prompt and efficient services to the wage earners.

Swift:

The bank has become a member of SWIFT and is providing a fast and accurate communication network for financial transactions to their valued clients through uninterrupted connectivity with thousands of users institutions in 150 countries around the world.

Summary:

Modern commercial banking is very tough business; the rewards are modest but the penalties for bad banking re dangerous. Still then it has a great importance in general welfare of the country,

NCCBL has a vast opportunity to perform its regular functions with confidence and adequacy. From the inception date, NCCBL has been carrying liabilities from the NCL, which ultimately obligate the bank to its every step very cautiously. Now it almost free from that horrible experience. Now it is the time to grow at a faster rate. NCCBL offers most of the banking services offered by the other commercial banks .But it also introduce innovative and advanced services which are available in the present competitive banking world. NCCBL should start online banking service to make the service faster and attractive. NCCBL should make proper utilization of its opportunities to minimize the weakness.

Credit Procedure of NCCBL

Introduction:

The word credit derived from Latin word “CREDO’ means I believe. If we analysis this

Theme it sands for Trust & Relationship between banker and customer. Each bank heir own credit policy which generally formulated on the basis of prevailing countries Socio economic condition, political & other related aspects from time to time and as per guideline of central Bank. Actually no policy can ever be termed as final due to changing circumstances all ‘around. As a developing country, we are endeavoring to match up with the International nard where changes are made to meet the demand and requirement of the time.

National Credit & Commerce Bank Ltd. Complying the directives of Bangladesh Bank as per BRPD circular No. 17 dated 07.10.2003 have formulated our own Credit Policies indicating the areas of lending which was duly approved by our Board of Directors. ‘Accordingly in processing the credit proposal terms and conditions as per our policy are to be followed.

Importance of credit:

Credit plays a very vital role in national economy in the following ways-

➢ It provides working capital for industrialization.

➢ It helps to create employment opportunities.

➢ Credit controls almost all kinds of production activities of the country.

➢ People’s purchasing power increases for it.

➢ It brings social equity.

➢ Cash generation occurs for its successful performance.

➢ Business cycle can run well only by the help of lending system.

Nature of Credit or Advance sanctioned by NCCBL:

Lending of money to different kinds of borrowers is one of the most important functions of National Credit and Commerce Bank Ltd (NCCBL). Major amount of income of this Bank comes from its lending. NCCBL makes advances to different sectors for different purposes, such as financing in trade and commerce, imports and exports, industries, transport, house building, agriculture etc.

Direct Facilities (Funded):

1. Cash Credit: Cash credit or continuous credits are those, which form continuous debits and credits up to a limit and have an expiration date. A service charge which in effect an interest charge is normally made as a percentage of the value of purchases. Cash credit is generally allowed against hypothecation or pledge of goods. Hence cash credits are of two types-

a) Cash credit hypothecation

b) Cash credit pledge.

a) Cash credit hypothecation: Cash credit allowed against hypothecation of goods is known as cash credit hypothecation. In case of hypothecation, borrower retains the ownership and possession of goods on which charge of the lending bank is created. The documents, which create charge of the lending bank on the hypothecated goods is called letter of hypothecation.

b) Cash credit pledge: Under this arrangement a cash credit is sanctioned against pledge of goods or raw materials. By signing the letter of pledge, the borrower surrenders the physical possession of the goods under the banks effective control as security for payment of bank dues. The ownership of the goods, however, remains with the borrower. The pledge creates an implied lien in favor of the bank on the underlying merchandise.

2. Overdrafts: A loan facility on a customer’s current account at a bank permitting him to overdraw up to a certain agreed limit for an agreed period. The terms of the loan are normally that it is repayable on demand or at the expiration date of the agreement.

3. Loan against imported merchandise (LIM/LTR): This is a loan facility up to a satisfactory limit to the traders/ customers by a bank against security of the value of the imported merchandise. This item also includes loan against trust receipts.

4. PAD/BLC/BE: A loan facility provided by the banks to the customers against documents/ bills.

5. Demand Loan: The demand loan is such type of loan the repayment of which is required to be made after a formal notice is given to the borrower by the bank.

6. Export Credit: All advance facilities provided to the exporters by the banks other than cash credit.

7. Term Loan: A bank advance for a specific period repaid with interest under fixed schedules is called term loan. The term loan may be as follows-

a) Short term: up to and including 12 months.

b) Medium term: more than 12 months up to and including 60 months.

c) Long term: more than 60 months.

Important Factors Considered by NCCBL BeforeSanctioning Credit:

Though off balance sheet activities play a vital role in a bank’s earnings, still income earned out of lending accounts for major portion of income of it. This lending in other words advance may raise the standard of success of a bank to the highest possible level and at the same time can be a sole instrument for liquidation (i.e. premature death of a bank) depending on how this portfolio is handled. So following factors should be given great emphasis.

(i) Who shall get credit?

It is easier to find out a depositor than finding out a good borrower. Public money in hands of a bad borrower is never safe and secure. Then the question comes whom to lend? In a nut shell the answer is the entrepreneur who, for attaining his own pecuniary interest as well as mental satisfaction together with offering additional services and well being to the society at large, undertakes efforts to collect together various types of necessary goods, labor materials, other wealth etc and by means of application of his wisdom, foresight, creativity, devotion and self confidence, takes initiative to add additional utility and value to the collected materials and wealth by bringing change and or modification in their form. It is widely accepted that a good entrepreneur is a good borrower.

(ii) How much to lend:

Over financing and under financing is very common phenomenon in credit portfolio; neither of which is desirable as a sound principal of advance. The highest priority of consideration is that bank credit must not be extended for speculative purpose and sound credit policy always finds out actual credit need depending on nature, volume, turnover of business as well as capability of the prospective borrower, which in turns depends on the test of good entrepreneurship. The most important aspects for consideration is how much a bank can lend taking into consideration its liquidity position, loan-able fund and commitment already made.

(iii) Why to lend:

The recommending as well as sanctioning authority must ascertain and satisfy himself that all advance are for productive purpose, genuine business and trade need based and neither for speculative nor for unproductive purpose. It is primary responsibility of recommending officer to visualize whether the loan, he is recommending for will generate cash to desired extent benefit to the bank, to the borrower and to the society at large. Bank cannot afford a loan turning bad to the detriment of institution and the society and for this purpose, the recommending and sanctioning officer must be acquainted with sound principles of advance and the ways and means to analyze the risks involved with the proposal processes and the limit sanctioned.

(iv) Where to Finance:

Financial activities of a bank, depends upon portfolio management of its funds through deposit. Bank’s lending activities may be classified into following broad segments-

a) Trade and Commerce:

This segment encompasses large, medium and small business houses dealing with imported consumer items as well as shopkeepers, distributors, whole sellers, retailers and small manufacturers scattered throughout the country. Lending activities of commercial banks in this segment of trade has traditionally been carried out based on bank-client relationship built up through interaction and past track record.

b) Industries:

The domain of industrial financing basically comprises of capital financing in the form of term loans, working capital financing and financing of small and cottage industries. The term loan is financed for establishment of new industries or for BMRE of existing industries. The core of NCC Bank’s lending activities shall be the working capital financing to large, medium and small-scale industries. While track record of operational performance of the industries, credit worthiness of the entrepreneur and reasonable security coverage shall form the basis of lending policies. NCC bank also set aside some budgetary allocation to finance small-scale industries.

c) Lease Financing:

NCC Bank to keep its contribution to the growth of national GDP, accelerate the total economic development by infusing the fund in productive sector in more efficient and effective way; that’s why this bank diversify its portfolio and satisfy the customers’ need and go for lease finance for various reasons. These are setting up of small and cottage industries/projects, BMRE of existing projects, transports,

medical equipment, construction equipment and fixed assets of other productive and service oriented ventures.

d) Consumer Financing:

For the economic development and to help the fixed income group in fulfilling their demand to upgrade the living standard NCC bank introduce consumer finance scheme for:

- Household appliances.

- Furniture & fixture.

- Air conditioner.

- Fax machine and cellular phone.

- Motor cycle/ car/ micro bus

- Other equipments.

e) Real Estate and Civil Construction:

NCC bank financed in this sector on selective basis.

f) Agro-based:

Agriculture is the mainstay of Bangladesh economy being major contributor to the GDP. That’s why NCC Bank has the keen interest to contribute towards the growth of economy by financing in the agro-based firms/ industry specially- poultry, fishery and hatchery. Financing will also be provided to export oriented shrimp culture and fish processing industries.

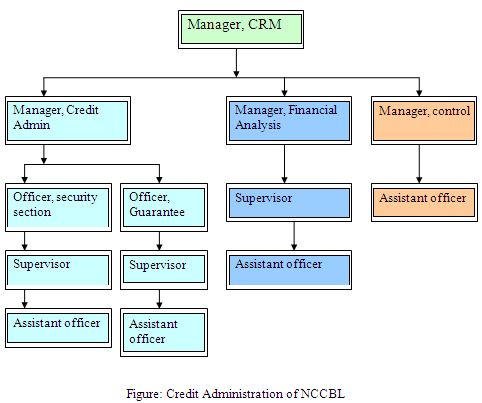

Credit Administration:

The board of directors being at the highest level of organization structure plays an important role on the credit administration. The board of directors is not directly concerned with the day to day operation of the bank. The board has delegated the authority to the managing director. The Head Office credit committee and other assigned credit officers under the guidance of the managing director approve, direct, monitor and review lending operations throughout the bank and ensure that the credit policies are adhered to and the credit operation is conducted in an effective way. In order to ensure the effective credit portfolio, the board, in turn, monitors the credit department and ensures placement of qualified officials who have got the right aptitude, formal training in finance, risk analysis, bank credit procedures as well as required experience.

Tools for appraisal credit

Besides the above-mentioned decision, the managers must ensure materialization of following safe guards for proper use and timely realization of loans, commission, interests etc and minimize the risk and hazards:

Safety of fund:

Safety means the assurance of repayment of distributed loans. This depends mainly on integrity, business behavior, and reputation

past experience in the particular line of business, financial solvency, quantum of own equity in business, capability to run own business efficiently, capacity and willingness to repay the loan etc, of the loan.

Security:

It must be ensured that repayment of the loan is secured and for this purpose manager must retain security against loan to fall back upon in case of borrower’s default. The securities must possess required basic qualities such as possession, title deed, parches etc.

Liquidity:

The borrower should have liquid asset so that he can adjust liability on demand and as much as possible loan itself should be quasi liquid so that it can be realized on demand in case of need.

Purpose:

Purpose of a loan should be production, development and economic benefit oriented.

Profitability:

This is applicable both for bank and borrower

Diversification:

Diversification means the distribute of loan to a large number of borrowers rather to a small number of borrowers. This will increase the services of the bank and it will reduce the risk of loan recovery.

National interest:

Nothing can be done legally if it jeopardizes national interest in any way

Credit restriction imposed by Central Bank:

At the time of sanctioning loan, the commercial banks must have to follow the restrictions that are imposed by the Bangladesh Bank from time to time.

Credit Strategies

General:

The bank shall provide suitable credit services and products for the market it operates.

Credit will be allowed in manners, which will in no way compromise the Banks standards of excellence and to customers who will complement such standards.

Loans and advances shall normally be financed from customer’s deposits and not out of short term temporary funds or borrowing from other banks.

All credit extensions must comply with the requirement of Bank companies Act-1991 and Bangladesh Banks instructions as may be amended time to time.

Nature of Credit or advance Sanctioned by NCCBL:

Lending of money to different kinds of borrower’s is one of the most important functions on NCCBL. Major amount of income of this bank come from its lending.

Direct facilitates:

➢ Term Loan

➢ Continuous loan

➢ Demand loan

Term Loan:

- short term industrial loan, mid term industrial loan, and long term industrial loan,

- Transport loan

- House building loan

- Loan against FDR

Short /mid/long term industrial loan:

By industrial credit we mean financing of industrial enterprise in the form of term loan. This may be categorized as follows:

n Short term industrial finance: Term of the loan is equal or less than one year.

n Mid term industrial finance: Term of the loan is up to 5 years.

n Long term industrial finance: Term of the loan is more than 5 years.

An industrial finance is allowed for the purpose:

n To set up a manufacturing facility

n To finance for BMRE where B means for balancing, M for modernization, R means for replacement and E for expansion.

n Purchasing of adequate inventories comprising of raw materials, stock in process and finished goods and extending credit to their customers.

Transport loan:

Any finance, which is given against hypothecation of vehicles like trucks, buses, marine vessel etc, is termed as transport loan. Advance under transport sector may be allowed for the following purposes:

n Purchase of imported/local assembled Buses, Minibuses, trucks etc.

n Import if reconditioned buses is subject to import regulations.

n Construction of purchase of water vessels passengers & cargo vessels locally built.

House building loan:

House building loan means loans that are given for construction of buildings or structures to be used not for residential accommodations of the borrower’ but for commercial utilization like renting or sale after the construction.

Loan against FDR:

This kind of loan is allowed by marking lien or creating charge against FDR or other financial instrument.

Credit risk grading (CRG):

➔ The credit risk analysis package provides a systematic procedure for analyzing and quantifying the potential risk. Bangladesh Bank has made it mandatory for commercial banks to use CRG for evaluating credit proposals amounting tk 1 crore.

➔ CRG format is mainly designed for all types of loan except micro credit and agricultural credit. But it is really impossible to represent all needs in a single format. So, credit officer judgments are needed in this regard.

➔ CRG at the initial stage relies too much on subjective judgment and financial risk has been given the maximum weight. Therefore there is always a chance to manipulate the ultimate risk grading.

➔ Another major impediment to the successful Credit risk analysis is that the information provided by the borrower often does not suit to feed into the CRG format. Therefore the credit officers need to employ extra time and effort to collect the relevant information from the borrower.

➔ Credit risk analysis is a lengthy process requiring sometimes even more than a month of the lack of information and its subjective nature.

Basically five factors influencing the firm’s credit risk grading. These are,

1) Financial risk

2) Business risk

3) Management risk

4) Security risk

5) Relationship risk

FINANCIAL RISK:

Financial risk is the risk which is related to firm’s financial structure. Ratio analysis is one of the factor of evaluating financial risk

BUSINESS RISK:

Business risk consider the firms type of business. That means the firms dominating power over the sector in what its operation is conducted.

MANAGEMENT RISK:

Management risk measure the efficiency of firms management is efficient or not for running the business.

SECURITY RISK:

Every bank wants to give loan on a security basis. They want to see their loan secured. Banks evaluate the firm on the basis of their capacity of refund loan & interests

RELATIONSHIP RISK:

In this case bank evaluates the relationship with client, whether the clients maintain their accounts in the particular bank (loan giver bank)or not.

Credit Monitoring and Review:

In the implied credit rules by NCCBL it is the manager’s responsibility to monitor the profile and risk aspect of the credit portfolio. Such monitoring shall be evidenced from the comments of the manager in monthly call or time to time call and visit reports of the assigned officers and be kept in the credit file with copy to Head Office. All extensions of credit have to be reviewed and graded at intervals prescribed by the Head Office. The purpose of this procedure is to monitor lending performance and to identify potential delinquent credits. The basis of review and classification are: risk of the transaction, repayment record of the borrower, collateral conditions, supporting information and documentations and the degree of conformity to bank facilities. The responsibilities for review and classification of credit facilities start at branch level and finally ends at the Head Office. Regardless of any formalized times for facility to be reviewed and formally classified by the branch manager or the concerned credit officer.

Classification of Advances:

The prime asset of any financial institution consists of its loans and advances and other investments. These assets are created primarily out of funds received from the depositors, loans and some other liabilities. The depositors as well as the investors in the institution are interested in real /realizable value of the assets of the institutions. The creditors are interested, as they want to know the depth of risk on their deposits, while the equity holders desire to be acquainted with viability of their source of income. The management of the institution as well as their supervising authority i.e. the Central Bank, evaluate the assets of the institution keeping in view the aforesaid aspects. This evaluation at stipulated intervals is called “ Classification of Advances”. It is in fact, placing all loans and advances under pre-determined different heads/ classes based on the depth of risk each and every loan has been exposed to and to bring discipline in financial sector so far risk elements concerned in credit portfolio of banks.

At present loans and advances are classified under three heads according to degree of risk element involved these are-

- Sub-standard

- Doubtful

- Bad

1.Substandard: A loan value of which is impaired by evidence that the borrower is unable to repay but where there is a reasonable prospect that the loan’s condition can be improved is considered as substandard.

2. Doubtful: A loan is doubtful when its value is impaired by evidence that it is unlikely to be repaid in full but that special collection efforts might eventually result in partial recovery.

3. Bad: A loan is considered as bad when it is very unlikely that the loan can be recovered.

Recovery of Advance:

A bank’s profitability and sustainability mostly depends on the recovery of its outstanding amount. Outstanding amount includes both principal and interest because, 80% of bank’s earnings comes from advances. A poor recovery rate indicates the weak condition of the banking operation and vice versa. But in the mid 80s, there started a loan defaulting culture, which is still in practice. As a result, banking sectors as well as the whole economy is facing a great threat from the defaulters. Money circulation has come down at its minimum level. If this cannot be checked, whole banking system of our country will collapse one day.

(i) Recovery Procedure:

Recovery procedure is a lengthy one that requires efforts of the bank, society and legal institutions. It also takes time and money. Like other banks, NCC Bank follows four steps to recover the outstanding amount. These are-

1. Reminders to the clients

2. Creating social pressures

3. Sending legal notice and

4. Legal action

These four steps are described in detail below-

1. Reminder to the client is given through a formal communication channel. A letter is written and properly signed on the bank’s papers. This letter is issued several times to remind the honorable loaner to repay his/her outstanding portion.

- If the loan amount is not yet repaid after sending a series of letters, then social pressure is created on the client by persons referred while opening account in the bank.

- Legal notice is prepared and sent by NCC Bank when above two steps fails to recover the amount. It is a threat to the borrower.

- The last and final step of the recovery procedure is the help from the court. NCC Bank sincerely tries to avoid this kind of situation for its honorable clients but cannot help doing for its own sustainability.

Loan Default:

A borrower can default for many intentional and unintentional reasons. There has been a mal practice of loan defaulting since the mid 80s. This creates a great threat to the financial institutions.

Location of main risk elements and reasons of loan default:

If the manager/sanctioning authority is aware of the prominent reasons of loan default and risk elements, he/she can take precautionary measures to minimize risk elements in recommending/sanctioning/disbursing a loan. There may be hundreds of reasons for loan default out of which following are the prominent causes-

- Sick Management

- Sick Marketing

- Sick Product

- Sick Operation

- Sick Finance

- Sick entrepreneur.

a. Sick Management: Sick Management means lack of integrity, co-operation, financial/ marketing knowledge and experience, endurance and judgment

b. Sick Marketing: It means lack of freedom, no restriction, openness (no monopoly), depth, growth and stability.

c. Sick Product: Sick product means lack of quality, competitiveness, demand and durability.

d. Sick Operation: It indicates lack of efficient machineries, skilled labor, good labor relation, utilities, raw materials, access to transport etc.

e. Sick Finance: It is lack of fund, repayment period, flexible rate of interest, matching to assets, collateral, efficient capital market etc.

f. Other reasons: They include lack of reputation, analysis of balance sheet, Lending risk analysis, adequate margin, past satisfactory performance, credit need analysis, good relation with other banks, credit information bureau report, other bank report, quality of security offered, demand etc.

Summary and Conclusion:

Policy means a set of rules and regulations to achieve a goal. Any kind of policies should be specified in written form. Otherwise different people will take its advantage. NCCBL does not have a written credit policy. As a result, branch managers as well as head office executive differ in implementing the policy. Policy should be published and maintained for the sack of NCCBL’s own interest. A large portion of the advance becomes overdue every year. It happens because of two main reasons. They are misevaluation of the borrower and economic instability of the country. NCCBL does not have a proper monitoring cell to evaluate the project financed by it at a specific interval. But NCCBL should always remember the proverb “prevention is better than cure”. It needs to be much more cautious and careful in evaluation of the borrower and the project. Then it has to monitor the advancement of the project. If the progress is not satisfactory, disbursement can be postponed. NCCBL should keep it in mind that it is dealing with the money of the general public who earn at the cost of their great hardship. So it should not play with the lives of these people. NCCBL must take a great care for credit policy making and its proper implementation.

Credit products:

As part of earning income, banks have to invest their deposits traditional and conventional methods like Cash Credit, Secured over Draft Loans in differ ere sectors: House Building, Transport & Foreign Trade, etc. All these have become us competitive and made asset Management of the company very difficult. Also opportunities have become limited thereby making benefit ratios marginal.

Considering all these; Banks have fortunate some credit schemes based on common needs, targeted areas for dispersal of their opportunities among them. These, are known as Consumer finance, Lease finance, Personal Loan, etc. Mainly these have been represented by difference banks in different name. NCCBL has recently introduced 03 (three) credit product namely personal Loan, House Renovation Loan,& Small Business Loan to supplement or consumer & lease finance schemes designed earlier.

Specialty: these are high income yielding loan.

a. Small Business Loan: It has been introduced with the following features: –

| Target group | Small Businessman who are unable to avail of loan as per existing norms of Bank. |

| Objectives | Dispersal of loan to the committed small business community |

| Limit | Up to Tk. 5.00 Lac (Maximum) |

| Eligibility | Honest, sincere & High performing having more than 5 years experience. |

| Refund mode | Monthly repayment within 3 to 5 yars |

| Rate of interest | 17% with quarterly rests with application fee Tk. 500/= |

b. Personal Loan: Salient features of the Scheme are as follows:

| Target group | Salaried people of listed organizations |

| Objectives | To meet up certain unwanted emergency expenses. |

| Limit | Up to Tk. 1.00 Lac (Maximum) |

| Eligibility | 50% of their home takes salary and employee of listed companies. |

| Refund mode | Monthly repayment within 3 to 5 years |

| Rate of interest | 17% with quarterly rests. 10% service charge with application fee Tk. 500/= |

c. House Renovation Loan: Social features are:

| Target group | Owners who are unable to meet up repairing/renovation expenses at from their own source. |

| Objectives | Renovation/repairing of dilapidated houses. |

| Limit | Up to Tk. 1.00 Lac (Maximum) |

| Eligibility | Actual owner of the house having 20 years of construction |

| Refund mode | Repayment by 60 monthly instalments. |

| Rate of interest | 17% interest with quarterly rests. 1% service charge with application fee Tk. 500/= |

d. Consumer Finance:

| Target group | People of fixed income group |

| Objectives | To procure household commodities for improving standard of living |

| Limit | Up to Tk. 3.00 Lac (Maximum) |

| Eligibility | Acquiring of listed items |

| Refund mode | Monthly repayment within 6 months to 36 months |

| Rate of interest | 17% interest with quarterly rests. 10% service charge with application fee Tk. 100/= |

E. Lease Finance: An entrepreneur, under this scheme may avail of lease facilities to procure industrial machinery and equipments, Vehicles, etc. (without having to purchase it by down payment) with easy repayment schedule on case to case basis. Rate of interest under this scheme is 15% P.A.

Recently three more credit schemes have been introduced to expand lending base of the Bank these are:

Festival Business Loan: The scheme designer to help the genuine businessmen to meet the extra finance required during festivals like, Eids, Puja, Disbursement of this loan is made in recycling order which is to be stopped 15 days before festival day. Maximum Tk. 10,000 Lac is allowable under this Scheme @ 15% interest P.A. at quarterly rest. Application fee is Tk. 500/=

g. Festival Personal Loan:The stymie formulated to meta urgency. financial except, the service holders at the time of festivals like Eids, Puma. Any salaried employee aged but 20-50 years and working in Govt. Skim Gobi. Autonomous : insurance Co., etv. are eligible to avail of this loan. The disburse Cement of this loan starts before I month of festival and continues till festival. Borrower may be allowed travail Foamy. the Tk.15,000% only for minimum 6 months but not more than 15 quarterly rest. Application fee is Tk.100/-.

h. NCC Bank Housing Loan Scheme:In order to enable the service holder/ professional businessmen in purchasing Flat/House, Constar Action of Building and renovation the, launched Housing Loan Scheme from September, 2004. The tenure of the loan is trial, years red maximum amount of loan, is Tk.5U:00 lac with interest @ 12% P.A

CC. Remittance Local and Foreign: Bank also provides remittance services to, i customers both lacal and -foreign. Foreign remittance channeled throe Money Gram and placids international and Express Money helps people in getting money within shortest possible t; from abroad. Local remittance as usual serving the people effectively.

Findings:

While working at NCCBL, MIRPUR BRANCH I have attained a newer kind of experience. After collecting and analysis data I have got some findings and recommendations. These findings are completely my personal view of point, which are given below-

- NCCBL has commitment to their prospective customers to honor its of cheque within 30 seconds after submission but unfortunately they are not able to fulfill this.

- NCCBL has yet not setup proper network system, which is very important to compete with the others in this electronic world.

- Online Banking System is available in NCCBL. which is very important to compete with others in the electronic world.

- Some branches of NCCBL has got AD license but MIRPUR BRANCH is not to get this license. For this reason MIRPUR BRANCH is losing its expected customers.

- For credit appraisal, the bank some time depends on the client for its authentication.

Recommendations:

Based on the evaluation of different aspects of NCCBL , the following recommendations have been made.

# The branch manager should ensure proper distribution of works responsibility among personnel strictly.

# NCCBL need to avoid nepotism.

# All on line banking services should be available in the branch to attract the customers.

# Credit officers must be skilled enough to understand the manipulated and distorted financial statements.

# Care should also be taken so that good borrowers are not discarded due to strict adherence to the lending policy.

# Strict Supervision must be adapted in case of high risk borrowers. Time to time visit to the projects should be done by the bank officers.

# Sitting arrangements should be available and in proper place for the officers as well as for the internees.

# Manager of the branch should monitor the activities of the officers so that the clients get efficient service.

# The average number of days required for sanctioning and disbursement of credit against specific loan proposal should be reduced.

# NCCBL need to maintain the ISG negative as the bank rate is decreasing.

# In the 2005 the growth of the investment is negative. Which is alarming situation for the bank.

# More investment should be made in the short period.

# Maintain the SLR properly. Two year the bank is failed to maintain the minimum SLR.

# Make sure the stability of the loan collection.0

# Banks EPS is not stable enough . Thats why the dividend policy may hamper. So make sure the growth of the EPS

Conclution;

I have focused and analyzed on Credit Management & its administration in NCCBL. The banking sector in any country plays an important role in economic activities. Bangladesh is no exception of that. as because it’s financial development and economic development are closely related. That is why the private commercial banks are playing significant role in this regard.

This report focused and analyzed on Credit Management & administration in NCCBL

In the past decade there has been a revolution in the communication media through the introduction of internet and other forms of secure dial-up media. This had an immense impact on all the sectors of the industry specially the banking sector. Traditionally in order to execute banking transaction a customer would require coming at the bank. But due to the introduction of electronic banking ,customers now can have access to their 7 days a week 24 hours a day and execute the transaction from their office Now due to electronic banking except cash customers are no longer require coming at the bank. It has not only benefited the customers but the bank as well. From the banks point of view this has helped prevent customers queuing up at the bank counters thus helping to minimizing the cost as well as the workload for the employees.

NCCBL can focus on their strengths to materialize the opportunities hidden for them in the banking industry and also they can work on their weakness to develop the product effectively and grab more opportunity hidden in the banking industry. With their strengths NCCBL can also reduce the threats existing in the market. They have strengths with their solid brand image and experience and skills as well, with which they are being able to satisfy the customers with their wide range of products and services.

NCCBL can overcome these hurdles and utilize the strengths, as the Bangladeshi banking industry has possessed some positive sides. Bangladesh is growing market where new businesses are coming up and in this emerging market and NCCBL can introduce its products and services effectively to the upcoming corporate. Moreover, it is an emerging market, various multinationals operating on the country will expand and new multinationals will come. These multinationals have huge need of electronic banking products for payment, collection and delivery need to manage their expanding business. They also need liquidity management for proper funding and by focusing on these opportunities; NCCBL can create an effective factor.