SUMMARY OF THE PROJECT

1. Name of the Project : Magic Cake – ATZ Ltd.

2. Business Type : An cake manufacturing company

3. Form of Business : Partnership

4. Source of Finance : Individual Capital & Bank Loan

5. Product/Service

(We Sell) : Pasty & Cake

6. Product/Service

(We Buy) : Sugar, Butter Oil, Egg, Different Bourbon Flavors, Custard Powder.

7. Brands : Magic Cake

8. Number of Employees : 101-185

9. Main Customers : Customer of Residential Commercial Area in Bangladesh.

- 10. Factory : In House

- 11. Management Certification : HACCP ISO 9001:2000

- 12. Location : Our project location is setting in;

Sub Project Area | Location |

| Project 1 | House 12, Road 16, Uttara, Dhaka.Head office of “Magic Cake” |

| Project 2 | Banani Bazar, Banani, Dhaka. |

| Project 3 | Road 27, Dhanmondi, Dhaka. |

| Project 4 | 27 Agrabad, Chittagong |

| Project 5 | Rose Vally Road, Sylhet |

| Project 6 | Laboni Sea-Beach, Cox’s Bazar |

| Project 7 | Nogor Vabon Road, Rajshahi. |

Figure-1: Locations of the Business

13. Objective : We have two types of objective:

Internal Objective:

- To earn profit

- Wealth maximization

- Make a strong Brand

To expand the business in abroad.

External objective:

- To reduce unemployment in Bangladesh

- To ensure the quality product

- Providing scholarship for the poor student

14. Product items: Our Production Item is setting in;

Name | Weight |

| Magic Cake- Milk Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Chocolate Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Strawberry Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Lemon Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Orange Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Mango Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Fruit Chocolate | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Cherry Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Banana Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Peanut Butter Flavor | .2, ½, 1, 2 and 5 lb |

| Magic Cake- Pumpkin Flavor | .2, ½, 1, 2 and 5 lb |

Figure-2: Product Item for Business

MANAGEMENT ASPECT

1. Corporate Set – up:

Magic Cake is a partnership business. In our project “Magic Cake” is a cake and pasty manufacturing organization. The Managing Director of the proposed project is Tahmina Akter Tani and the Director is Mahmuda Sultana Tania. The particular of Board of Directors:

Name of the Directors | Extent of Shareholding | Status |

| Tahmina Akter Tani | 30% | Managing Director |

Mahmuda Sultana | 40% | Director |

Mr. X | 30% | Brand Ambassador |

Figure-3: Board of Directors

We expected that, we have enough ability to do well in our business. And we are very much hopeful because our Brand Ambassador Mr. X is a star cricketer in Bangladesh.

2. Legal structure of the proposed company:

The managing directors of the company select a structure about the power of selected employee. The structure will follow a chain of commend rules. Here manager will get supreme power of the company. But every important issue will submit to the board of director. Where Managing director, departmental head and also adviser must have the right to give the opinion.

TECHNICAL ASPECT

TECHNICAL ASPECT

1. Project Land & Location:

We try to form a Partnership business, which create a renowned brand. And for proper distribution of our product we will made seven factories in different location of our country. These are:

Tk: “000”

Sub Project Area | Location | Area of Land | Tk. Per Katha | Total Cost (Tk.) |

| Project 1 | House 12, Road 16, Uttara, Dhaka. |

Head office of “Magic Cake”5 Katha

6,000,000

30,000

Project 2Banani Bazar, Banani, Dhaka.5 Katha (1 floor)

2,800,000

14,000

Project 3Road 27, Dhanmondi, Dhaka.5 Katha

2,750,000

13,750

Project 4Rose Vally Road, Sylhet10 Katha

720,000

7,200

Project 527 Agrabad, Chittagong10 Katha

500,000

5,000

Project 6Labpni Sea-Beach, Cox’s Bazar10 Katha

300,000

4,500

Project 7Nogor Vabon Road, Rajshahi.10 Katha

262,500

2,625

Total

77,075

Figure-5: Land Cost per Project

2. Buildings:

For this business we need building or factory. That’s why in every project we should make 2 or 3 stories building. What we used for store room, production room, managers room, guest room, garage etc.

Tk: “000”

| Sub Project Area | Storey | Total Cost (Tk.) |

| Project 1 | 3 Storey | 7,000 |

| Project 2 | 1 Storey | 4,000 |

| Project 3 | 2 Storey | 3,050 |

| Project 4 | 3 Storey | 3,000 |

| Project 5 | 2 Storey | 2,500 |

| Project 6 | 2 Storey | 2,500 |

| Project 7 | 2 Storey | 2,000 |

Total | 24,050 |

Figure-6: Building Cost per Project

3. Machinery & Equipment:

For this project we need foreign and local machinery. We will purchase our foreign machinery from Italy. The machinery purchase from Italy, are:

Tk: “000”

| Machine Name | Cost Per Machine | Quantity | Total Cost |

| Auto Oven | 5,200 | 10 | 50,200 |

| Auto Machine for Steam | 2,500 | 7 | 1,750 |

| Auto Machine for Color Layer | 220 | 8 | 1,760 |

| Auto Machine for Mixture | 180 | 7 | 1,260 |

| Fizzer Machine for Store | 800 | 7 | 5,600 |

Total | 60,570 |

Figure-7: Machinery & Equipment Cost

- The total imported duty is (60,570,000*9%) 5,451,300 Tk.

- We also purchase some local machinery which takes more then 15,600,000 Tk.

- There has some installation cost of Tk. 23,700,000 (7 projects).

- The amount of IDCP is 2,691,639 Tk.

- The total amount ofMachinery & Equipment is 108,012,939 Tk.

4. Sub contract:

We also involve in some sub-contract. The main elements of sub-contract are:

- Cover Box

- Cake Board

- Sticker or paper cover

- Carton for packet

- Dresses of employee

Marketing Analysis

1. Justification of setting up the business:

The demand of the Cake and Pasty in Bangladesh is increasing day by day. Because of, the economical situation and the total GDP of Bangladesh is growing up. It is indicate that our total income level is stronger then previous time. As a result when the income level of a country is increased then we can say that, the demand of luxury product is also increased. Due to our income level situation, a branded Cake and Pasty is not luxury for us. And the demand of ice cream is increasing rapidly. So we belief that set up an ice cream factory is a good decision for us.

2. PEST Analysis

- Political Analysis:

The political situation of Bangladesh is not enough good. The rules and regulations are always changed by changing a political leader. Moreover, Hartal, hindrance, procession and meeting in the road are also a big threat for the organization. As a result, it will very tough for the organization to predict the actual yearly revenue. But it is a matter of hope that, now a days political restless situation is decreasing day by day. And also government takes some initiative against Hartal, procession and meeting.

- Economical Analysis:

The economical situation of Bangladesh is not so good. There is huge economical discrimination. In the upper class people of city area, the per capita income is very much high where our average per capita income is below 700$. In the rural area people have a very few knowledge about technology and the new food item and flavor. Moreover their income level is very much low. And that is why upper class people is our main target consumer.

- Social Analysis:

Bangladeshi people are very much voluptuous. So Cake and Pasty is not a segmented product in Bangladesh. All classes of people have the ability to purchase an ice-cream. So we segmented our product price by depending on consumer expenditure level. As a result we think that consumer will like our product. School going children always like to take an Cake and Pasty in their leisure period. And we also try to give a shape of our Cake and Pasty box as a gift pack like birthday cake.

- Technological Analysis:

Bangladesh is a developing country. So it is very tough for us to get all kind of technological support from Bangladesh. Moreover there have some shortage of skilled engineer for solving the technical problem. As a result we are bound to purchase our machinery from abroad.

- 3. Cake and Pasty factory and its growth:

The growth of Cake and Pasty factory is stopped in Bangladesh. Because some leading Cake and Pasty factory (Coopper’s, Hot Cake, Mr. Baker and Bakeman ) dominate the Bangladesh Cake and Pasty market. And there are also some small factories. But they are surviving in this sector.

| Company | Market Share |

| Coopper’s | 30% |

| Hot Cake | 21% |

| Mr. Baker | 15% |

| Bakeman | 10% |

| Others | 24% |

| Total | 100% |

Figure-8: Cake and Pasty Factories Growth in Percentage

4. SWOT Analysis:

| 4.1 Strength | 4.2 Weakness |

| |

| 4.3 Opportunity | 4.5 Threat |

|

Figure-9: SWOT Analysis for Business

- Demand & Supply Analysis of Cake and Pasty industry:

The demand of branded cake in urban area is very much high then the people of rural area. Urban areas people are very much concern about brand. 33% rural people cannot aware about a brand cake where more than 92% people in urban areas people are very much concern about the brand of a cake. So we can say that, in urban area we have Fixed 8% and in rural area 33% consumer can divert into our product, if we can full fill their demand easily. Without these in many area of Bangladesh people cannot purchase an ice cream because of the high price. So, we will provide an economy price for the people of the rural area.

Area/Location | Cake and Pasty Brand Market Share | |||

Igloo | Polar | Savoy | Others | |

| Urban Area | 56% | 24% | 12% | 8% |

| Rural Area | 40% | 22% | 5% | 33% |

Figure-10: Market Share of Different Brand

6. Detail Information on Local Supply:

In Bangladesh the raw materials of cake is available. And the supplier company also ensures the quality of the raw material. The dealer of sub contract organization also ensured the quality of the product. But the availability of machinery of cake is not available in Bangladesh. So for setting up an ice cream factory it is necessary to purchase machinery from abroad.

- Supply Gap:

In the below we mentioned about the demand, supply and supply gap Cake and Pasty in Bangladesh. Last year the demand of Cake and Pasty was 31,025,000 lb, where the supply was only 17,680,000 lb. As a gap result were 13345. And the gap is increasing day by day.

lb: “000”

| Year | Demand | Supply | Supply Gap |

| 2007 – 2008 | 25550 | 15300 | 10250 |

| 2008 – 2009 | 31025 | 17680 | 13345 |

| 2009 – 2010 | 36498 | 20060 | 16438 |

| 2010 – 2011 | 42454 | 22178 | 20276 |

Figure-11: Supply Gap of Ice-cream

- Present & projected market demand of the project ‘Magic Cake’:

lb: “000”

Year | Demand |

| 2007 – 2008 | 25550 |

| 2008 – 2009 | 31025 |

| 2009 – 2010 | 36498 |

| 2010 – 2011 | 42454 |

Figure-12: Present & projected market demand

- Present & projected Supply of the project ‘Magic Cake’:

lb: “000”

Year | Supply |

| 2007 – 2008 | 15300 |

| 2008 – 2009 | 17680 |

| 2009 – 2010 | 20060 |

| 2010 – 2011 | 22178 |

Figure-13: Present & projected Supply

- Present & projected Supply Gap of the project ‘‘Magic Cake’:

lb: “000”

| Year | Demand | Supply | Supply Gap | Our Contribution | Real Gap |

| 2007– 2008 | 25550 | 15300 | 10250 | —- | 10250 |

| 2008 – 2009 | 31025 | 17680 | 13345 | —- | 13345 |

| 2009 – 2010 | 36498 | 20060 | 16438 | —- | 16438 |

| 2010– 2011 | 42454 | 22178 | 20276 | 15000 | 5276 |

Figure-14: Present & projected Supply Gap

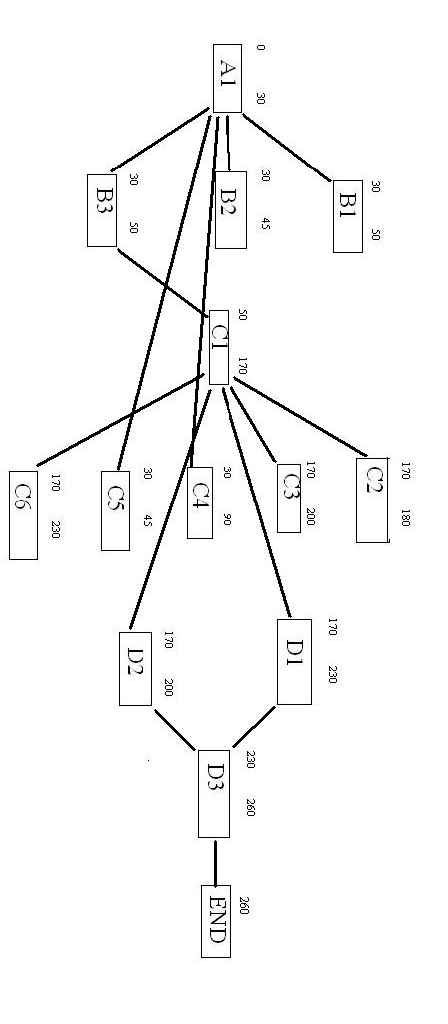

Network Technique

In our project we have a lot of small work. And some works dependent works and some are independent works. Our project work is given below by network diagram.

Task Predecessor Time (days)

A1- Land Purchase ——— 30

B1- License for Business A1 20

B2- Other Paper A1 15

B3- Building Design A1 20

C1- Construction B3 120

C2- Insurance Policy C1 10

C3- Foreign Agreement C1 30

C4- Construction of PDB A1 60

C5- Vehicle Purchase A1 15

C6- Safety equipment purchase C1 7

D1-Machinery Important C1 60

D2- Purchasing Local Machinery C1 30

D3- Machinery Installation D1, D2 30

Financial Analysis

Financial Analysis

1. Fixed Cost of the Business:

Tk: “000”

Item | Local Cost | Foreign Cost | Total |

| Land(7 project: Table 4) | 77,075 |

| 77,075 |

| Building | 24,050 |

| 24,050 |

| Imported Machinery | — | 60,570 | 60,570 |

| Imported Duty | 5,451 |

| 5,451 |

| Installation Fee | 23,700 |

| 23,700 |

| IDCP | 2,691 |

| 2,691 |

| Local Machinery | 15,600 |

| 15,600 |

| Vehicles | 77,000 |

| 77,000 |

| Furniture | 2,200 |

| 2,200 |

| Computer | 9,800 |

| 9,800 |

| Office Equipment | 700 |

| 700 |

| Safety Equipment | 350 |

| 350 |

| Deposit to PDB | 550 |

| 550 |

| Pre-operating Expense | 400 |

| 400 |

| Consultancy Fee (0.75% of the Project Cost) | — |

| 2,251 |

| Initial Investment of the Business: |

|

| 302,388 |

Figure-18: Fixed Cost of the Business

- Deposit to PDB:

Tk: “000”

Sector | Cost |

| Gas | 140 |

| Water | 100 |

| Electricity | 180 |

| Telephone | 80 |

| Internet Line | 50 |

Total: | 550 |

Figure-19: Cost of PDB

2. Financial Plan for Business:

Tk: “000”

Item | Bank’s Investment | Client’s Equity | Total | |||

Amount | % | Amount | % | Amount | % | |

| Land | 77,075 | 100 | 77,075 | 100 | ||

| Building | 19,240 | 80 | 4,810 | 20 | 24,050 | 100 |

| Imported Machinery | 78,550 | 85 | 13,861 | 15 | 92,412 | 100 |

| Local Machinery | 7,800 | 50 | 7,800 | 50 | 15,600 | 100 |

| Vehicles | 57,750 | 75 | 19,250 | 25 | 77,000 | 100 |

| Others | 16,251 | 100 | 16,251 | 100 | ||

| Total | 163,340 |

| 139,047 |

| 302,388 |

|

Figure-20: Financial Plan for Business

3. Means of Finance:

Bank’s Investment – 163,340,998 (54.02%)

Client’s Equity – 139,047,975 (45.98%)

Total: 302,388,973 (100%)

4. Debt Equity Ratio:

Debt-Equity Ratio = Bank’s Investment / Client’s Equity = 54.02: 45.98

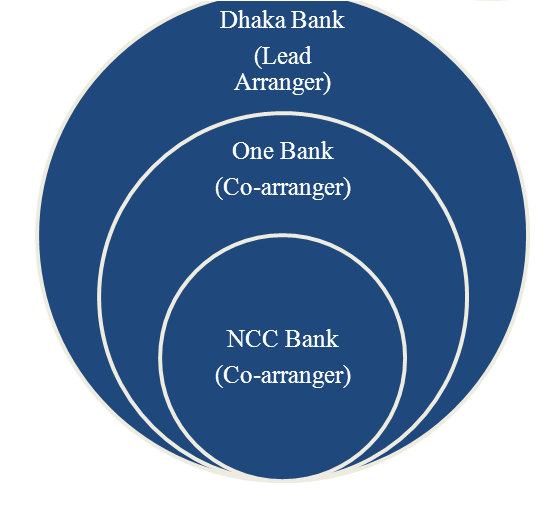

5. Syndicate Finance:

Dhaka Bank is going to participate 55% of total loan amount. It hires One Bank and NCC Bank to for a syndicate for sanctioning the loan. The Co-arranger banks will participate the loan amount by using ratio 6:4

Figure-21: Lead arranger & Co-arranger

- Syndicate Finance in Percentage:

Tk: “000”

Bank Name | % in Syndicate Finance | Amount |

Dhaka Bank | 55% | 166,313 |

One Bank | 27% | 81,645 |

NCC Bank | 18% | 54,430 |

Total | 100% | 302,388 |

Figure-22: Bank Investment in Syndicate

Cost of Goods Sold:

Tk: “000”

Item | Total |

| Raw material cost | 41,157 |

| Wages & salaries | 26,340 |

| Depreciation | 21,721 |

| Total | 89,218 |

Figure-23: Cost of Goods Sold

Sales Estimate: Tk: “000”

Product Name | Description | ||

Love (per Peace) | Quantity (Per day) | Total (Annually) | |

| Magic Cake- Milk Flavor | 14.00 | 5000 | 21000 |

| Magic Cake- Chocolate Flavor | 11.00 | 4000 | 13200 |

| Magic Cake- Strawberry Flavor | 10.00 | 4000 | 12000 |

| Magic Cake- Lemon Flavor | 20.00 | 3000 | 18000 |

| Magic Cake- Orange Flavor | 07.00 | 5000 | 10500 |

| Magic Cake- Mango Flavor | 23.00 | 1500 | 10350 |

| Magic Cake- Fruit Coktle | 60.00 | 1500 | 27000 |

| Magic Cake- Cherry Flavor | 110.00 | 2000 | 66000 |

| Magic Cake- Banana Flavor | 205.00 | 250 | 15375 |

| Magic Cake- Peanut Butter Flavor | 490.00 | 50 | 7350 |

| Magic Cake- Pumpkin Flavor | 16.00 | 1000 | 4800 |

Total | 205575 | ||

Figure-24: Revenue from Sales

Raw Material Cost:

Tk: “000”

Item | Amount |

| Flour | 28,850 |

| Butter Oil | 5,300 |

| Egg | 2,001 |

| Different Bourbon Flavors | 3,006 |

| Others | 2,000 |

| Total | 41,157 |

Figure-25: Total Cost of Raw Materials

- Subcontract:

Tk: “000”

Sl. No. | Subcontract | Total Cost |

| 1 | Cake and Pasty box | 9,120 |

| 2 | Stick of Ice-Cream | 2,250 |

| 3 | Sticker or paper cover | 3,795 |

| 4 | Carton for packet | 5,500 |

| 5 | Dresses of employee | 360 |

| Total: | 21,025 |

Figure-26: Purchasing Price from Subcontract

1. Wages and Salaries:

Tk: “000”

Description | Persons | Salary (individual) | Salary (annually) |

Managing Director | 1 | 42,000 | 504 |

Manager | 8 | 30,000 | 2,880 |

Top level employee | 22 | 22,000 | 5,808 |

Mid level employee | 30 | 18,000 | 6480 |

Driver | 22 | 14,500 | 3,828 |

Distributor | 22 | 10,000 | 2,640 |

Lower level employee | 50 | 7,000 | 4,200 |

Total | 26,340 | ||

Figure-27: Wages & Salaries Expenses

Depreciation Schedule:

Tk: “000”

Item | Cost | % | Total |

| Land | 77,075 | — | — |

| Building | 24,050 | 5% | 1,202 |

| Machinery | 108,012 | 8% | 8,641 |

| Vehicle | 77,000 | 15% | 11,550 |

| Furniture | 2,200 | 12% | 264 |

| Computer | 320 | 20% | 64 |

| Total |

| 21,721 | |

Figure-28: Depreciation from Fixed Asset

Administrative Expenses:

Tk: “000”

Item | Amount |

| Wages & Salary | 48732 |

| Subcontract | 21,025 |

| Bill of PDB | 4500 |

| Others | 500 |

| Total | 74757 |

Figure-29: Administrative Expenses

Financial Expense:

Tk: “000”

Item Amount % of rate Interest

Bank loan 163,340 12% 19,600

Earning Forecast:

Tk: “000”

Description | Amount |

| Revenue earning | 205,575 |

| (-) C.O.G.S | 89,218 |

| Gross Profit | 116,357 |

| (-) Adm. Expense | 74,757 |

| Operating Profit | 41,600 |

| (-) Financial Expense | 19,600 |

| Net Profit Before Tax | 22,000 |

| Tax Holiday | 00.00 |

| Net Profit After Tax | 22,000 |

Figure-30: Net Profit Analysis

Social Cost Benefit Analysis

1. Social Cost: Tk: “000”

Items | Private Angle | Economic Angle |

| Imported Machinery | 92,412 | 92,412 |

| Local Machinery | 15,600 | 15,600 |

| Vehicles | 77,000 | 77,000 |

| Furniture | 2,200 | 2,200 |

| Computer | 9,800 | 9,800 |

| Office Equipment | 700 | 700 |

| Safety Equipment | 350 | 350 |

| Cake and Pasty cost | 41,157 | 90,150 |

| Subcontract | 21,025 | 21,025 |

| Salary and Wages | 26,340 | 25,000 |

| Others | 550 | 550 |

| Total | 260,794 | 309,787 |

Figure-31: Social Cost Analysis

2. Social Benefit: Tk: “000”

Items | Private Angle | Economic Angle |

| Foreign Currency | 92,412 | 92,412 |

| Backward Linkage | 127,225 | 21,025 |

| Contribution to GDP | ——- | 26,340 |

| Local Demand | 205,575 | 205,575 |

Total | 425,212 | 345,352 |

Figure-32: Social Benefit Analysis

3. Net Benefit:

Private Angle : 425,212 – 260,794 = 164,418

Economic Angle : 345,352 – 309,787 = 35,565

Conclusion

From the above analysis we can easily say the project of Magic Cake is going to successful one. The min objective of every is to earn profit by fulfill the demand of customers but in case of our business the first objective is social benefit. And we ensure social benefit through our product quality and supply testy and healthy items. From the market analysis we can see the demand of our product. We also ensure