An aggregate in economics is a summary measure. It is an economic measurement of the total amount of demand for all finished goods and services produced in an economy. The aggregation problem is the difficult problem of finding a valid way to treat an empirical or theoretical aggregate as if it reacted like a less-aggregated measure, say, about the behavior of an individual agent as described in general microeconomic theory. It is expressed as the total amount of money exchanged for those goods and services at a specific price level and point in time. Examples of aggregates in micro- and macroeconomics relative to less aggregated counterparts are:

- Food vs. apples

- Price level and real GDP vs. the price and quantity of apples

- Capital stock vs. the value of computers of a certain type and the value of steam shovels

- Money supply vs. paper currency

- General unemployment rate vs. the unemployment rate of civil engineers.

In Economics, the aggregate may be used to refer to a lot of terms, say, Aggregate Demand, Aggregate Supply, Aggregate Expenditure, etc.

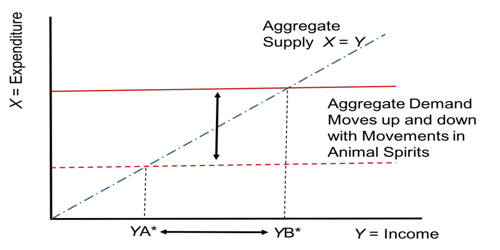

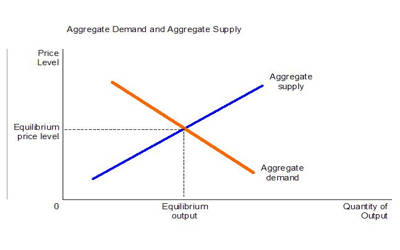

- Aggregate Demand: It is the total demand for all the final goods & services in an economy at a particular time. It is the sum of consumption, investment, government expenses, and net exports.

- Aggregate Supply: It is the total supply of goods and services produced within an economy at a particular time. It is the total output an economy produces at a given price level.

The standard theory uses simple assumptions to derive general, and commonly accepted, results such as the law of demand to explain market behavior. It represents the total demand for goods and services at any given price level in a given period. An example is the abstraction of a composite good. It considers the price of one good changing proportionately to the composite good, that is, all other goods. It is the total demand by domestic and foreign households and firms for an economy’s scarce resources, less the demand by domestic households and firms for resources from abroad. If this assumption is violated and the agents are subject to aggregated utility functions, restrictions on the latter are necessary to yield the law of demand. As a result of the same calculation methods, the aggregate demand and GDP increase or decrease together. The aggregation problem emphasizes:

- How broad such restrictions are in microeconomics

- Use of broad factor inputs (“labor” and “capital”), real “output”, and “investment”, as if there was only a single such aggregate is without a solid foundation for rigorously deriving analytical results.

Franklin Fisher notes that this has not dissuaded macroeconomists from continuing to use such concepts.