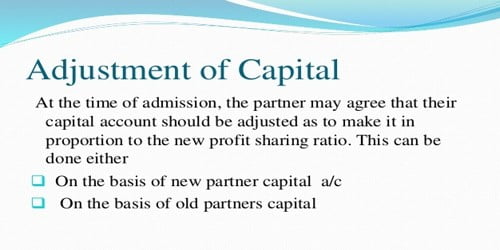

Adjustment of Capital in terms of Retirement of a Partner

When a partner retires from the business and if he is to be paid off his due amount immediately, the total capital of the firm is reduced. In case of the death of a partner, the treatment of various items is similar to that at the time of retirement of the partner. In such a case, the retiring partner may be requested to keep the amount due to him as a loan to the firm, so as to be paid gradually in the future. After making all the adjustments in the Partners Capital Account, the amount that is due to him is paid to his Legal Representative. This capital rearrangement means the contribution of partners towards capitals is rearranged on the basis of the new profit sharing ratio. On the other hand, the remaining partner may bring a necessary amount in a new profit sharing ratio or in the same agreed ratio to make payment to the retiring partner. Here, stocks are excluded but items such as prepaid expenses, receivable bills, and trade debtors are included.

Then afterward, if agreed, the capitals of remaining partners may be required to be adjusted in the new profit sharing ratio in any one of the following three ways:

(A) When the total capital is not given:

Step 1: Calculation of the total capital of the new firm as:

The total capital of the new firm = Aggregate of adjusted old capitals of remaining partners.

Step 2: Calculations of new capitals of remaining or continuing partners:

The new capital of a continuing partner= Total capital X New ratio

Step 3: Any excess of the new capital of a remaining partner, is to be paid off in cash and for the deficiency, the continuing partner has to bring in cash.

(B) When the total capital is given:

Step 1: Calculation of continuing partners’ new capital

The new capital of continuing partner= Total capital given X New ratio

Step 2: Any excess capital to be paid to and any deficiency is to be brought by the continuing partners.

(C) When the retiring partner is to be paid through cash brought by the remaining partners so that their capitals would be in accordance with new ratio:

Step 1: Calculation of the total capital of the new firm

Total capital = Aggregate of old capitals after all adjustment + Shortage of cash to make payment to retiring partner

Step 2: Calculation of new capital of continuing partners = Total capital of new firm X New ratio

Step 3: Deficiency to be brought in by the remaining or continuing partners.