Executive summery

EXIM Bank Ltd. as the name implies is not a new type of bank in some countries on the global but is the first of its kind in Bangladesh. Its main objective is to provide necessary support to the exporters and importers of the country. So foreign exchange activities get the highest concentration by the bank.

The Rajuk branch recently has achieve Authorized Dealership licenses from Bangladesh Bank. The impact of this licensee can not be analyzed as an activity was started from July. But some problem are identified and suggestion and recommended to overcome those problems.

Before the licensee the percentage of foreign exchange income on total income shows a growing rate. So, it is expecting that if proper strategies are taken the impact of foreign exchange income will show a significant improvement.

Besides as the Bank is setup with an objective to support international transaction. So, the bank should provide specialized and efficient services to its target customer.

Introduction

International Islamic University Chittagong offers one year & two years M. B. A. program. The program includes a compulsory internship program of 3 credits, which starts after the completion of 3rd semester. The intern needs to submit a report on whatever he learns from the internship. As a student of M. B. A. program I was also bound to complete the internship program and submit a report. I had completed my internship in the Export Import Bank of Bangladesh Limited, Rajuk Avenue Branch. And prepare a report on the “An overview of foreign exchange business of EXIM Bank LTD.”

EXIM Bank Ltd. as the name implies is not a new type of bank in some countries on the global but is the first of its kind in Bangladesh. Its main objective is to provide necessary support to the exporters and importers of the country. So foreign exchange activities get the highest concentration by the bank.

The Rajuk branch recently has achieve Authorized Dealership licenses from Bangladesh Bank. The impact of this licensee can not be analyzed as an activity was started from July. But some problem are identified and suggestion and recommended to overcome those problems.

Before the licensee the percentage of foreign exchange income on total income shows a growing rate. So, it is expecting that if proper strategies are taken the impact of foreign exchange income will show a significant improvement.

Besides as the Bank is setup with an objective to support international transaction. So, the bank should provide specialized and efficient services to its target customer.

Object of the study

This study focuses on the following specific objective:

- The report is aimed for an overview of foreign exchange business of EXIM Bank LTD.

- To know the operation of foreign exchange.

- To know the income from this section.

- To know the impact of this income on profitability of the branch.

- To suggest necessary measures for the development of the Bank

Methodology of the study

۞ Sources of Data / Information

Data/information of the study have been collected from both sources i.e. Primary and secondary sources.

۩ Primary sources

- Conversation with bank officers.

- File study.

- Desk work.

- Personal observation.

۩ Secondary sources

- Annual report of EXIM bank.

- Different publication of EXIM bank.

- Different books and journals.

۞ Data processing

After the editing phase the collected data were analyzed by using necessary table.

Scope of study

The scope of study is limited to the Export Import Bank of Bangladesh Limited. This Dissertation Report covers all the offers and services provided by Export Import Bank of Bangladesh Limited to its elite group of customers. The report also covers the respective account holders- their stature, class and diversity. The customers included in this report are provided with the privilege of the luxury of firstly a personal Financial Consultant assigned as relationship manager and secondly, a group of dedicated sales executive for the respective organizations who will visit their office premises on regular frequency to meet their banking needs, in order to provide them seamless professional services in a convenient manner.

Limitation of the study

The study also has some limitations. First of all data finding of EXIM bank of Bangladesh limited was a trouble some work because of shortage of time. Secondly, adequate and in-depth well-organized literature was not available because a few researchers endeavored to work on such project in the past. It is a private bank so; they maintain some sort of secrecy in giving information to the general public. The officers of EXIM Bank of Bangladesh Limited are always busy with their works. As a result they could not make enough time to talk to me.

- This Report doesn’t show the total banking practices of EXIM Bank of Bangladesh ltd. Some Department were ignored for study due to the time constraint.

- Some data could not been collected for secrecy of the management.

- The time stipulated for the Dissertation program for clear understanding the Banking practices of EXIM Bank of Bangladesh ltd. was not adequate enough.

- There are some lacking in data collection from other Banks due to their privacy.

As the branch is new one and the Authorized licenses has been achieved two years ago so, their was not an enough scope to analyzed the impact.

Plane and presentation

Both description and analytical methods are used to present the findings. The report is divided into six sections. These sections are – Introduction (1st section), Industry overview (2nd section), Organization overview (3rd section), Foreign Exchange (4th section), Project Part (5th section), Findings & Recommendation (6th section).

Industry overview

banking system in Bangldesh(historical place)

Bangladesh inherited its banking structure from British regime and had 44 banks and other financial institutions before the partition of India in 1947. Till liberation of Bangladesh all banks were privately owned and thus the benefits/facilities of banking were enjoyed by only a small elite group of persons and the banks in private sector played a traditional role without fulfilling socio- economic objectives of a welfare state.

After liberation of the country, all the banks were nationalized with a view to utilizing the services of the banks in conformity with Government policy for achieving socialistic pattern of society.

The main objective of nationalization of banks was to ensure that the banking system serves a much wider section of the commodity by dispensing credit to the poorest and the weaker section of the society and also to remove the regional disparities by helping in development of backward areas. Banks serve better the needs of development of the economy in conformity with national policy and objectives formulated by the Government that means society with wealth distributed as equitably as possible.

The Bangladesh banks (Nationalization) order enacted in 1972 nationalized all banks foreign ones. Six nationalized banks were formed through merging the existing banks of that period.

The decades of the eighties witnessed the active operation of both the NCBs and PCBs (local and foreign) in the banking market. There were no domestic privet commercial banks in Bangladesh until 1982. The nationalized bank could not play the due role in the implementation of Government program and policy. So to create competition in the banking sector, Government decided to allow private investment in setting-up of local private commercial banks along with the nationalized commercial banks operating in the country.

The Uttara bank in 1983 has been transferred to private sector. Thereafter, in 1986 the Pubali bank and Rupali bank has been transferred to private sector and some more commercial banks came up in 1983 and initiated to moderate growth in banking sector. Despite slow growth in number of individual banks, there had been a relatively higher growth of branches of nationalized commercial banks (NCBs) during 1973-83. Private banks in foreign collaboration have also been allowed to function in the country only where such collaboration is considered to be helpful in attracting substantial foreign investment in the country and also introduces new area of banking activities.

During eighties, the banks operate under strict regulatory framework. NCBs primarily lent to agricultural, industrial and export sectors following the Government directives while private and foreign bank lending primarily went to trade and commerce. A number of problems were manifested in the banking sector in that time. To mention a few, these are inadequate mobilization of savings, widespread loan defaults and delinquencies, in inefficient credit delivery, which ultimately resulted in a retarded economic growth. In the mid-eighties, revamping the financial sector was felt as a step in the right direction. The Bangladesh Government appointed a national commission on Money, Banking and Credit (NCMBC) to undertake a major study on the financial sector in late 1984, which submitted its report in 1986 suggesting that the reform should be brought about for addressing the problem of loan delinquencies and restoring the financial stability.

In the early nineties, the economy has taken in to liberalization process as adopted in different fields through launching structural adjustment program. In order to redress the structural and problems facing the financial sector as identified by NCMBC, a good number of reform measure were introduced in 1990 via World Bank supported Financial Sector Reform project (FSRP). At the initial stage two major policy reforms viz. flexible interest rte and loan classification and provisioning were took place. Other reform measures include abolition of financial system and introduction of rediscounting facility by the central bank, establishment of capital adequacy standards, recapitalization of the NCBs, strengthening of central bank supervision, enactment of banking related legislation and amendments thereto providing wider power to central bank, checking insider lending, incorporating legal provisions for loan recovery, development of human resources through training, etc.

The commercial bank were allowed adequate freedom in various areas of banking operations including fixation of deposits and lending rates, service charges selection of loan portfolio others which were then administered and regulated by central bank. The FRSP continued its operation till 1996. In May 1997, another project named “Consolidate Bank Restructuring project (CBRP)” funded by the World Bank was undertaken to further consolidate, strengthen and make the banking sector more dynamic. Besides, a high powered Banking Reform Committee (BRC) was formed in order to carry forward the reform process in the financial sector. The committee submitted its report in December 1999 and recommendation are under active consideration of the Government.

Overview ot the exim bank of Bangladesh ltd.

Intoduction of exm bank of Bangladesh limited

In Bangladesh, there are many types of Bank, which are formed as commercial banks. But above all, EXIM Bank of Bangladesh Limited is a new kind of private commercial bank. The full elaboration of EXIM Bank of Bank of Bangladesh Limited is Export Import Bank of Bangladesh Limited. Initially, the name of the bank was BEXIM Bank Limited that means Bengal Export Import Bank Limited. Later the management decided to change the name of the bank as EXIM Bank of Bangladesh Limited because of the case lodged Beximco group of industries. EXIM Bank of Bangladesh Limited was incorporated as public Limited companies in Dhaka, Bangladesh on 3rd August, 1999. It was started under the experienced and able leadership of Late Shajan Kabir who was the Chairman of the Bank. After his death, Mr. Nazrul Islam has been selected as the Chairman.

Export Import Bank of Bangladesh Limited (EXIM Bank Ltd.) that was named before as Bengal Export Import Bank Limited (BEXIM Bank Ltd.) being newly formed commercial bank of the country with a distinctive identity was opened in 3rd August; 1999. The bank received the certificate of incorporation no. C-37864 (2164)/99 under the companies Act (Act-XVIII) of 1994. It also received the certificate for commencement of business on the same date by the section 150(2) under company’s Act. Apart from the Head office in Dilkusha C/A, it started its first local branch in Motijheel C/A simultaneously in order to provide all kinds of banking support to the clients. On the second December of 1999 they opened their second branch in Panthapath.

Slogan of exm bank-together towards tomorrow

Export Import Bank Ltd. as the name implies is not a new type of bank in some countries on the global, but is the first of its kind in Bangladesh. It believes in togetherness with its customers, in its march on the road to growth and progress with services. To achieve the desired goal, it has intention to pursuit of excellence at all stages with a climate of continuous improvement. Because it believes, the line of excellence is never ending. It also believes that its strategic plans and business networking will strengthen its competitive edge over in rapidly changing competitive environment. Its personalized quality to the customers with the trend of constant improvement might be cornerstone to achieve its operational success.

Mode of the exm bank-local bank global network

The word EXIM implies the meaning its operations. Though it is a new type of bank in Bangladesh, it is familiar with so many countries in the whole world through foreign banking. Its motto is to provide quality services to the customers all over the world. So the mode of the bank “Local Bank Global Network” is completely adjustable with operation.

The bank has a sound capital base. Its authorized capital is Tk. 1,000.00 million while its initial paid up capital is Tk. 225.00 million subscribed by the sponsors. To solidify its capital base further, the paid up capital will further raise to Tk. 450.00 million within a reasonable period by public offering of shares of the company. The sponsors of the bank are leading business personalities and reputed industries.

The bank was started under the experienced and decent leadership of Late Shajan Kabir who was the chairman of the bank. After his death Mr. Nazrul Islam Mazumder has been selected as the chair man. Mr. Alamgir kabir, the advisor of the bank is reputed senior Chartered Accountant having 30 years vast experienced in Accounting, Audit, and Finance & Banking at home and abroad. The bank will be immensely benefited from the able leadership of the chairman and the valuable advice and guidance of the advisor.

Mr. Mohammad Lakiotullah, the managing director of the bank, is widely trained at home and abroad, having three decades of long experience in banking profession in and outside the country.

To make EXIM bank the finest banking institution of the country, the workforce has been futuristic in outlook, professional in attitude and honest in reputation.

The attention of the bank is to become a most disciplined bank with a distinctive corporate culture. The personals of EXIM bank believe in shared meaning, shared understanding and sense making. Their people see and understand events, activities, objects and situation in a distinctive way. They are able to mould their manner and etiquette, character and individuality to suit the purpose of the bank and the needs of the customer, who are of paramount importance to them. The people of the bank see themselves as a tight knit team/family that believes in working together for growth.

Customer service and automation

To err in human and forgiveness is a proverb, the bank believes it, but the customer might not accept it. Because, for a service the customers pay for, they want it 100% defect free. So, to face situation the bank has drawn its motto i.e. continuous improvement of customer service. Altered expectations of the customers have shifted the focus from resource base productivity to value base productivity. To operate on the globalize environment, the bank is equipped all units of the bank with modern technology, such as on line computer network, telex, fax, E-mail etc. For the services of its customers round the clock, it has intention to install ATM at suitable place.

Social commitment

The purpose it’s banking business is, obviously to earn profit, but the promoters and the equity holders are aware of their commitment to the society to which they belong. The bank is committed to keep a chunk of the profit aside and/or spent that for socio-economic development work through trustee and in patronization of art, culture and sports of the country. It wants to make a substantive contribution to the society where it operates, to the extent of its separable resources.

corporate information at a glance

Registered Name : Export Import (EXIM) Bank of Bangladesh

Limited

Registered Head Office : Printers Building, (5th floor)

5 Rajuk Avenue,

Motijheel, C/A

Dhaka -1000

Phone – 9566764, 9553872, 9561604, and

9566418.

E-Mail – eximho@bdonline.com

Telex – 642527 Eximho BJ

Fax – 880 -2-9556988.

Data of corporation : 3rd August, 1999.

Chairman : Mr. Nazrul Islam Majumder.

Managing Director : Mohammad Lakiotullah

Auditor : Rahman Rahman Huq

Chartered Accountants

Authorized capital : Tk 1, 000.000 million

Paid up capital : Tk 313.875 million

Number of Branches : 28

Mechanism

Commercial Banking is the core work of EXIM Bank of Bangladesh Limited. The bank renders all kinds of customer service ranging from individual to corporate tittles, both private and public and government projects.

Planning

Planning approach in EXIM Bank of Bangladesh Limited is to maintain from top to bottom management authority to achieve the goal. The corporate branch of the bank is mainly responsible for planning. International department financial control, internal audit etc. provide all sources of assistance and information to implement the strategy in both long-term and short-term planning.

Staffing

EXIM Bank of Bangladesh Limited recruits people on the basis of merit so that quality services can be provided to the customers. There are two kinds of recruit’s, namely-

- Management trainee and

- Non management trainee.

They are given training to equip themselves for efficient service.

Control and guidance

Authoritative and participatory to level management exists in the bank. Departmental managers have been assigned responsibilities for day to day function. Physical sitting arrangement is so arranged in the office that superiors can monitor the jobs of subordinates. This situation creates better cooperation and ensures better services.

Bank of exm bank of Bangladesh limited

At present, EXIM Bank of Bangladesh has 20 branches of which 14 are Dhaka, 3 are in Chittagong, one is in Sylhet, one is in Noakhli and one is in Comilla. And 6 branches are proposed which is open soon.

Branches are at follow:

A) Dhaka branches:

- Motijheel Branch

- Panthapth Branch

- Gulshan Branch

- Imumgong Branch

- Narayangonj Branch

- Shymrail Branch

- Rajuk Avenue Branch

- Uttara Branch

- New Elephant Road Branch

- Nowabpur Branch

- Mirpur Branch

- New Eskaton Branch

- Dhanmondi Branch

- Gajipur Branch

B) Chittagong branches:

- Agrabad Branch

- Khatungong Branch

iii. Jubilee road Branch

C) Sylhet branch.

D) Sonimory branch.

E) Laksham Branch.

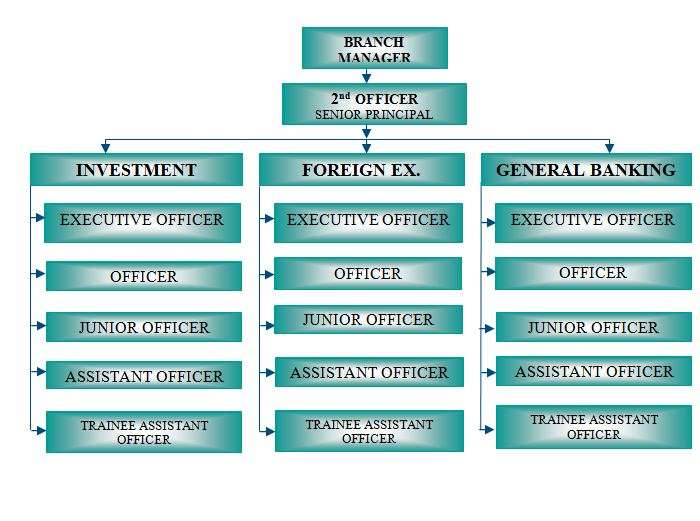

Organogarm

Organgaram of the (Export Import) EXIM Bank of Bangladesh Ltd. are show in next page. Pleas see the next page.

۞ Serial number Based on position

Figure 1: Organization Structure of EXIM Bank Ltd.

۞ Organogram of ever Branch’s

Figure 2: Organization Structure of ever Branch’s, EXIM Bank Ltd.

The activities of the exm bank

The activities of EXIM bank can be classified into broadly three classes,

- General Banking Division (GBD).

- Credit and Advance Division (CAD)

- Foreign Exchange Division (FED)

General banking

The main activities of general banking division are as follows;

a) Accounts Opening.

b) Issuing check books and account closing.

c) Remittance.

d) Clearing Department.

e) General Enquiries.

f) Customer complaints.

g) IT Department.

Credit /lone and advance

EXIM bank provides various types of loan to individual and organizations. The main three type’s loans are;

a) Cash credit,

b) Consumer credit, and

c) Security overcomes.

Foreign e exchange

The department deals with export and Import activities are called foreign Exchange department. At the beginning of my internship work the Rajuk branch doesn’t have foreign exchange license, so in that time they use the license of Motijheel branch. Now the Rajuk branch gets the foreign exchange license. And they start the work from 1st June, 04. The widely used terms in this division are described briefly following:

Export

When any organization/company want to sale any goods or services to the buyer in live in another country, is called export the goods/services. In this regard, the seller needs a Latter of Credit (L/C) from the buyer for the confirmation of payment.

Import

When any organization/company want to buy any goods or services from the seller live on other country, is called import the goods/services. In this regard the buyer needs to open a Letter of Credit (L/C) to the name of seller’s company for the confirmation of payment.

Letter of credit

The documentary credit is a commitment on the bank’s part to place an agreement at the seller’s disposal on behalf of the buyer under precisely defined conditions.

The terms documentary credit

In actual practice, a number of different expressions have emerged for this type of business, all of which basically mean the same thing “Documentary Letter of Credit”, “Commercial Letter of Credit”, “Letter of Credit”, “L/C”, “Elcee”, “LOC” or “Letter de Credit”.

The main parties to documentary credit

- Buyer (Importer).

- Seller (Exporter).

- L/C Issuing Bank (Buyer’s Bank).

- Advising Bank (Issuing bank correspondent at seller’s place).

- Negotiating Bank (Seller’s Bank).

(Some time the advising bank and the negotiating bank become the same bank)

Main function of exm bank of Bangladesh

The name of the bank gives a clear idea about its operation. A commercial bank handle all sort of traditional Banking business including introduction of awed range of savings and credit product, retail banking and ancillary services with the support of modern technology and professional management. But the EXIM Bank of Bangladesh Limited emphasizes on its function in export and import trade handling and financing, development of entrepreneurship as a private sector. Such financing of export oriented industries will enhance wealth, quotes more employment opportunities, helps formation of capital and reduces imbalance in the balance of payment of the country.

Other operations

The bank does all traditional banking business including Islamic Banking services in selective branches.

- Deposits, which are the lifeblood for the bank, among the other modes, are mobilized through a variety of saving scheme. The bank also handles Traveler checks, Credit cards. Consumer credit facilities, Inland and foreign remittance of the fund and operates in the money market.

- In capital market operations, it engages itself in share and securities business, mutual fund management and brokerage house activities.

- Bank is poised to extend L/C facilities to its importer/exporter.

- Customers through establishment of correspondent relations and Nostro Accounts with leading Banks all over the world.

- The bank trades and commerce with added emphasis on foreign exchange. The bank also adopts Micro-credit and Agro-credit schemes.

Foreign exchange

Foreign exchange can simply be defined as a process of conversion of our currency into another. A well-known author of some popular books on foreign exchange, Dr. Paul Einzig tells that the foreign exchange means a system or process of conversion of one national currency into another and of transferring money from one country into another.

In ordinary sense “Foreign Exchange” means foreign currency which refers to the rate of exchange the price of one unit of foreign exchange in terms of another country. But in its complete sense, Foreign exchange means the mechanism, the media used and rate at which these media are exchanged with another.

In terms of the F.E.R act, 1947 as adopted in Bangladesh “Foreign Exchange” means foreign currency and includes all deposits, credits and balances payable in foreign currency as well as all foreign currency instruments like, cash currency notes, checks, drafts, bill of exchange, traveler’s cheques, postal money order, commercial letter of credit etc.

Exchange control

Exchange control means licensing the use of “foreign exchange” earning of the country. In Bangladesh the exchange control is administered be Bangladesh Bank under the provisions of F.E.R act, 1947 as adopted in Bangladesh.

Authorized dealers in foreign exchange

In exercise of the powers conferred be the F.E.R act, 1947, Bangladesh Bank has issued license to certain scheduled Banks to deal in foreign exchange. These Banks are known as authorized dealers.

Licenses are also granted to persons or firms by Bangladesh Bank to foreign exchange currency instruments. Ex.-T/C, cash currency, notes, and coins. They are known as authorized moneychanger. The authorized moneychangers are not however, authorized to make any other transaction in foreign exchange.

Types of foreign exchange business

۞ Financing the import of goods and services

- Facility to open documentary credit.

- Collection of the bill and repatriation of fund.

- Effecting remittance abroad.

- Clearance of imported goods and the storage.

- Lending money against imported merchandise.

Financing the export of goods and services

1. Advising export credits.

- Collection and negotiation of foreign bill and repatriation of proceeds.

Receiving packing credit facility to exporter

Miscellaneous services

- Sale and purchase of foreign exchange.

- Providing credit information of foreign correspondents.

- Implementation of foreign exchange regulations.

- Issuing and countersigning guarantees on behalf of foreign correspondents.

- Forward cover of exchange.

- Maintenance and profitable use of balances of foreign exchange abroad within prescribed limits.

- Issuance of T/C Drafts wex Dev, Bond.

- Maintenance of wage Earner’s foreign currency accounts, N.F, CD A/cs.

i. Collection of T/C drafts, cheques, F.M.O, PMO etc.

- Reporting of all transactions to Bangladesh Bank.

Mechanism of export- import

IMPORTER SIDE

۩ Applicant

Who requests his bank issue Letter of Credit (L/C) in terms of the arrangement with the seller.

۩ Issuing Bank (Buyer)

The Bank that agrees to the request of the applicant and issues its letter of Credit in terms of the instructions of the applicant.

۩ Advising Bank

The Bank, usually situated in the seller’s / Beneficiary’s country (most of the time with which there exists corresponding relationship with the Buyer’s / Issuing Bank).

۩ Beneficiary (seller)

Beneficiary of the documentary Letter of Credit.

۩ Negotiating Bank (seller’s / Beneficiary’s Bank)

The Bank, which makes payment to the exporter after scrutinizing the documents submitted by the exporter with the original L/C then it is called Negotiating Bank.

۩ Confirming Bank

Sometimes, issuing bank request advising bank or another bank to add confirmation to the Letter of Credit. When that bank does this then such bank is called confirming bank. So, advising bank can be acted as confirming bank.

۩ Reimbursing Bank

This is the bank that is nominated by the issuing bank to pay (It is also known as paying bank) or to accept drafts. It can be situated in another country. In this connection it is to say that American Express Bank and Net West Bank act as Reimbursing Bank in the case of EXIM Bank. The account, which maintains EXIM Bank with Nat West Bank and American Express Bank, is called “Nostro Account” and in reverse the account, which is maintained by Nat West Bank and American Express Bank with EXIM Bank is called “Vostro Account”. And the account maintained by American Express Bank and Nat West Bank is called “Loro Account”.

۞ Local currency vs. Foreign currency

Each country its own nation currency which performs the traditional functions of money, an unit of account, a medium of exchange, a store of values etc. useful possession of the local currency provides the holder with the requisite purchasing power in the home country. Thus, US dollars, Swiss francs or similar currencies, in spite of their strength in the international money and exchange markets, cannot convenient serve as a measure of value or unit of account in Bangladesh because they are not local medium of exchange. These are foreign currencies. They have a practice in relation to our own currency in the sane way as rice or jute or any other tradable goods have a price in terms of taka and price will vary.

۞ Different types of foreign currency account

۩ Private foreign currency account

Authorized dealer (AD) branches may open foreign currency accounts without prior approval of Bangladesh Bank on the name of:

- Bangladesh nationals residing abroad.

- Foreign nationals residing abroad or in Bangladesh.

- Foreign Firms registered abroad and operating in Bangladesh or abroad

- Foreign mission and their expatriate employees

- Diplomatic bonded warehouse (Duty free shops) licensed by the custom authorities.

- Local and joint venture constructing firms employed to execute projects by the foreign donor / international donor agencies.

Payment may be made freely abroad from this F.C. A/Cs to the extent of credit balance lying therein.

No payment in the foreign exchange maybe made to or on behalf of any resident in Bangladesh.

If the F.C A/Cs are maintained in the form of term deposit for a minimum period of 90 days authorized dealer branch that may pay interest in admissible rate.

Bangladesh nationals working and earning abroad including self employed Bangladeshi immigrants proceeding abroad on employment may open F.C A/Cs ever without initial deposit. They may operate the accounts themselves or nominate other persons in Bangladesh for this purpose. The accounts can be opened either in Pound Sterling, US dollar, Deutsche Mark or Japanese Yen at the option of account holder. These types of F.C A/Cs are commonly known as wage earnings F.C A/Cs.

۩ Non-resident foreign currency deposit account (NFCD A/C)

All non-residents Bangladeshi nationals and persons of Bangladesh origin including those who having dual nationality and ordinarily residing abroad may

maintain interest bearing time deposit accounts named “Non-residing foreign currency deposit accounts with the Ads”.

Bangladeshi nationals serving with Embassies / High Commissions of Bangladesh in foreign countries and also the officers / staff the government / semi-government departments / nationalist banks and employees of body corporate posted abroad or deputed with international and regional agencies like IMF, World Bank, IDB, ADB etc. during their assignment abroad may open such accounts.

Account may be opened with funds transferred from exist foreign currency accounts maintained by the wage earnings with Ads in Bangladesh.

The accounts are in the nature of term deposits maturing after one month, three months, six months and one year. The accounts may be maintained in Dollar, Pound Sterling, Deutsche Mark or Japanese Yen, initially with the minimum amount of UD $ 1,000.00 or Pound Sterling £ 500.00 or equivalent. Accounts may be opened against remittances in other convertible currencies after conversion of those into USD, PS, DM and JY.

These accounts may be maintained as long as the account holder desire. Eligible persons are also allowed to open such accounts with six months of their return of Bangladesh.

The will pay interest and deposit into the accounts at the Eurocurrency deposit rate. In case of per-mature repayments, the interest amounts will be for-feted to the depositing AD.

Foreign nationals and companies / firm registered and / or incorporated abroad, banks, other financial institutions including 100% foreign owned industrial units in foreign processing zone of Bangladesh are also allowed to open and maintain NFCD accounts with Ads. The minimum amount of the deposits in such case should be US $ 25,000.00 or its equivalent in Pound Sterling, Deutsche Mark or Japanese Yen.

۩ Resident foreign currency deposit account (RSCD A/C)

Persons ordinarily resident in Bangladesh may open and maintain Resident Foreign Currency Deposit (RFCD) accounts with foreign exchange brought in at the time of their return from travel abroad. Any amount brought in With declaration to customs authorities in form FMJ and up to US $ 5,000.00 brought in without declaration can be credited to such account.

Balances in these accounts shall be freely transferable abroad. Fund from these accounts may also be issued to account holders for the purchase of their foreign travel in usual manner (i.e. with endorsement in passport and ticket, up to US $ 300.00 in the form of cash and the remainder in the form of T.C.).

These accounts may be opened in US Dollar, Pound Sterling, Deutsche Mark or Japanese Yen and may be maintained as long as account holder desires.

Interest in foreign exchange shall be payable on balances in such accounts if the depositors are for a term of not less than one month and balances is not less than US $ 1,000.00 or Pound Sterling £ 500.00 or its equivalent.

۩ Convertible and non-convertible taka accounts

Ads may open convertible taka account in the names of foreign organizations / nationals viz. Diplomatic missions, UN organizations, Non profit international bodies, foreign contractors and consultants engaged for specific project under the govt. agencies and the expatriate employees of such mission/ organizations who are resident in Bangladesh.

These accounts may be credited with foreign currency brought in or remitted from abroad or transferred from a foreign currency account or another convertible taka account. No money emanating from a business originating in Bangladesh and otherwise reportorial to Bangladesh can be credited to these accounts.

A convertible taka account may be debited for payments in foreign currency abroad, for local expenses, for transfers to foreign currency accounts or other convertible taka accounts or for credits to a non-convertible taka account.

Foreign organizations/their expatriate personnel as mentioned above may maintain non-convertible taka account with Ads without prior approval of Bangladesh Bank. These accounts may be credited with fund from convertible taka accounts with remittances from authorized sources including profit from STD.

Profit bearing STD accounts (7-30 days special notice) may also be opened in the name of foreign organization / national / charitable organization/ UN organizations with Ads. Profit is ruled on balances of these accounts that will be disbursed locally in non-convertible taka and no part of the earned profit will be remittable abroad.

۩ Blocked accounts / non-resident blocked taka accounts

The FER Act confers powers on the Bangladesh Bank to “Block” accounts in Bangladesh of any person resident outside Bangladesh and to direct that payment of any sum due to a non-resident may be made only to such a blocked account.

A blocked account means an account opened as a blocked account at any branch or office in Bangladesh of a bank authorized in this behalf by the Bangladesh Bank or an account blocked by order of the Bangladesh Bank.

A blocked account may be opened in the name of a resident of Bangladesh unless it is held jointly with non-resident. An authorized dealer (AD) or an existing “Free” account blocked except under directions from Bangladesh bank may open no blocked account.

The Bangladesh bank issue special instructions regarding operations an individual blocked account. In the absence of any such special instructions, on payable into or withdrawal from blocked accounts may be made unless prior approval of the Bangladesh bank has been obtained.

Balances held in blocked accounts may be invested in “approval securities” expressed to be payable in taka or may be placed on fixed deposit with the bank which the account is held subject to prior approval of Bangladesh bank.

۞ Foreign exchange dealing spot

Foreign exchange involves the exchange of one currency into another. Exchange of one currency to another currency involves a number of steps: one is “where” and another is “When” to deliver the funds. The rate of exchange needs also to be settled before a deal is concluded.

۩ Settlement country

When a deal is made the parties to the deal arrange the settlement. A deal normally involves two currencies. So, settlement takes place in the two counties whose currencies are used.

۩ Spot settlement

Unlike merchandise bought and sold off the shelf foreign currencies can not be delivered immediately except perhaps bank notes.

۞ Value date

This principles or practice of delivery on the same date is known as value date and the transactions are known as the value dated transactions. The idea is that both the parties receive their respective currencies on the same date.

۞ Selling and buying rates

Foreign exchange is a two-way conversion. A sale transaction normally involves conversion of local currency into foreign currency: one foreign currency is sold against another. A buying transaction involves conversion of in foreign currency into domestic currency or, in some cases another foreign currency.

۞ Cross-rate

A cross rate is an exchange rate, which is calculated from two other rate. For example, taka/pound sterling rate can be calculated as a cross rate between US $/taka and US $/pound sterling.

۞ Authorized dealer’s rates to the customers

Depending in the nature of transaction, a bank would quote the rate to the customers taking into account its ancillary costs associated with the transactions. The basic rate as elsewhere in the world, is the TT rate. TT rate are based on the principle of value compensates or value here and value there and do not involve loss or profit. It also does not require elaborate documentation for payment to the beneficiary. Thus when buying pound sterling from the customer, the bank will make payment to the customer at the TT (buying) rate, if the sterling amount has already been paid into the bank’s Nostro account in the U.K. TT rate will apply for buying a foreign currency bank draft, Mail transfer or any other instrument against which the issuing bank has already paid the value to the drawer bank’s account with it self or another bank even though the money is not transferred through TT or Telex. When selling foreign currency by means of TT, DD or other Means, the bank applies the TT or DD selling rate.

۞ Forward exchange transactions

A forward exchange is a transaction between a bank and another party- a customer or another bank – involving delivery of a foreign currency against local currency at an agreed exchange rate on a specified future date or within an agreed time frame. The important features of forward exchange are: first, the rate of exchange and the value date are agreed upon in advance at the time the deal is concluded. Second, no money is paid or received until the settlement date, sometimes, though the bank may ask for a margin deposit from the customer, the only thing that distinguishes a forward exchange transaction from the spot transaction is that a spot deal is settled immediately while a forward deal is settled on a future date or within a definite time frame at an agreed rate.

۞ Forward and future contract

Foreign exchange literature frequently refers to “futures” contracts, and they are sometime confused with forward contract. The philosophy that works behind “forward”, “swap” and “futures” is the same but the letter is of fairly recent origin.

Project part

Background of the report

In Bangladesh there are many types of bank, i.e. Government, semi government, private, Islamic and foreign banks. Although some banks are operating by the head of the government but foreign banks and some private banks are doing well in banking arena. The general customers of Bangladeshi are facing various types of problem like taking bribe, undue inflation, and decimation in dealing with the local government bank. On the other hand, privet banks and foreign banks are giving their best services to customers. As a result the customer of private banks and foreign banks are increasing day by day.

This report could be very useful for those, who want to have a brief knowledge about Foreign Exchange & impact of income from Foreign Exchange Business on profitability of Export Import bank of Bangladesh Limited and can compare the service of this bank with the local bank.

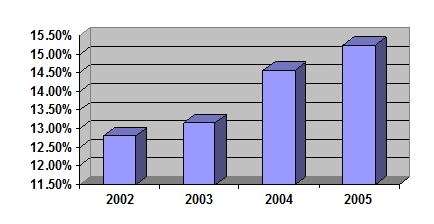

Foreign exchange income

On 1st June, 2000 the branch has got the authorized dealership licenses. So, it is expecting a higher income from this business.

Title / Years | Amount in Million | |||

2002 | 2003 | 2004 | 2005 | |

| Foreign Exchange Income | 731.74 | 1036.92 | 1663.43 | 2389.24 |

| Total Income | 5705.94 | 7874.24 | 11411.82 | 15682.36 |

| % of foreign exchange income on total income | 12.82% | 13.16% | 14.58% | 15.24% |

Table: Percentage of foreign exchange income on total income.

Graphical representation forming exchange income

Graphical representation of foreign exchange income on total income:

Information regarding income is available up to December 31st 2005. Thus licenses was achieve on June it has to work through the Motijheel branch on June as SWIFT machine was not set up. The actual activities on their Owen licenses were started from July 2000. But information collected was not possible regarding July income.

From the above table, it is found that percentage of foreign exchange income on total income shows increasing rate. As income under the dealership licenses is not deductible that is the branch will not have to pay 30% of its income to Motijheel branch, obviously the income will be increased.

As the dealership license has been achieved more income is expected to be earned. Before the dealership licenses was available the main sources of foreign exchange income export and import. Now the branch is avail to earn income from remittance also. Beside, more clients will be attracted in export, import business.

Sources of foreign exchange income

The foreign exchange income is mainly come from Import section, export section and Remittance section. But the Rajuk branch foreign exchange income come from Import section and export section at present.

۞ Import section

۩ Opening of Letter of credit

Documents required for opening a Letter of Credit are as follows;

- L/C application and agreement from duly filled and signed by proposed importer.

- Exchange control copy of L/C authorization form.

- Indent or preformed invoices (one kind of price list describing the details on the items wanted to import).

- Insurance cover note with premium paid receipt.

- Offing sheet.

- L/C opening sheet.

- L/C forms (in set) FEX-1(A).

- L/C amendment form FEX-1 (B).

- L/C forwarding form FEX-1(C).

- IMP form (set in quadruplicate).

- Liability voucher.

- Voucher for L/C advising charge and realizing of margin.

۩ Procedure, Scrutiny, Lodgment and Retirement

Imports and exports (control) Act 1950 regulate the import and export trade of the country. There are a number of formalities which on importer has to fulfill before import goods.

Procedures of import

The procedures which follow at the time of import are as follows:

- The buyer and seller conclude sales contact provided for payment by documentary credit.

- The buyer instructs his bank (the issuing bank) to issue a credit in favor of the seller/exporter/beneficiary.

- The issuing bank then send message to other bank (advising bank/conforming bank), usually situated in the country of seller, advise or conform the credit issued.

- The advising/conforming bank then informs the seller through his bank that the credit has been issued.

- As soon as the seller receives the credit, if the credits satisfy him then he can reply that he can meet its terms and conditions, he is in a position to load the goods and dispatch them.

- The seller then sends the documents evidencing the shipment to the bank where the credit is available (the nominated bank). This can be issuing bank or conforming bank, bank named in the credit as the paying, accepting or negotiating bank.

- The bank then cheeks the documents against the credit. If the documents meet the requirement of the credit, the bank then pay, accept or negotiate according to the terms of credit. In the case of a credit available by negotiation, issuing bank will negotiate with recourse.

- The bank, if other then the issuing bank, sends the documents to the issuing bank.

- The issuing bank cheeks the documents and if they found that the document has meet the credit requirements, they released to the buyer upon payment of the amount due or other terms agreed between his and the issuing bank.

- The buyer sends transport documents to the courier who wills then proceeds to deliver the goods.

Scrutiny

Generally import bills following documents and order of their scrutiny should be as under:

a) Forwarding schedule of negotiating bank.

b) Bills of exchange.

c) Invoice.

d) Bills of lending.

e) Insurance.

f) Certificate of origin.

g) Any other documents.

Lodgment

Lodgment includes

a) Scrutinize the shipping documents meticulously.

b) Conversion of foreign currency into Bangladesh currency.

c) Enter the Shipping documents in Inward Foreign Bills Register.

d) Inform the importer to deposit balance amount of L/C and to release the necessary document.

e) Prepare and pass the lodgment voucher.

Retirement of import bills

a) Importer will deposit the claim amount.

b) Banker will prepare and pass retirement voucher.

c) Certifying Invoices.

d) Passing of Vouchers.

e) Entry in the register.

f) Endorsement in the B/E and transport document i.e. B/L AWB, TR etc.

At the end of the total procedure, taking the retirement of import bills/clearing certificate from the bank, the importer will clear the goods from the port through the clearing agent and forwarding agent.

On the other hand, completing the above all steps the issuing bank will prepare Foreign Exchange transaction schedule and send one copy to international division of head office and another copy to reconciliation.

۩ Back to Back Letter of Credit and its operation

Back to Back Letter of Credit defined as a credit which is opened at the instruction and the request of the beneficiary of the original/Muster export Letter of Credit on the Strength credit.

Back to Back is a term given to an ancillary credit, which arises where the seller uses the credit, granted to him by the issuing bank to his supplier. Sometimes Back to Back credits are called counter veiling credits, i.e. credit and counter credit.

۞ Export section

Literally, the term export, we mean that carrying of anything of from one country to another. On the other hand bankers define export as sending of visible things outside the country for deal. Export trade plays a vital role in the development process of an economy. With the export earning, we meet import bills.

Like any other business it needs registration. The chief controller of import and (CC&E) makes export registration. For registration, prospective exporters required to apply through Q.E.X.P form the CC&E along with the following documents:

- Trade license.

- Income tax clearance

- Nationality Certificate.

- Bank’s solvency Certificate.

- Asset Certificate.

- Registered partnership deed.

- Memorandum & Association of articles/certificate of incorporation.

Advising of L/C

The import information/ terms and conditions of the L/C are some times communicated by the L/C opening/ issuing bank (buyers’ bank) to the exporter’s bank through cable/telex which is followed by the original L/C, the following points are generally covered in cable L/C:

a) Name of the importer.

b) Name of the exporter.

c) Description of goods (in short).

d) Expiry date of L/C.

e) Types of L/C (Revocable/Irrevocable).

f) Shipment date.

g) Name of the reimbursing bank.

h) Name of their nominated dealer etc.

Export Form

All export of which the requirement of declaration vide para-1 of chapter XXI of exchange control manual of Bangladesh bank applies must be declared on the EXP forms by the customer, now issued by the authorized dealers.

Discrepancy and Indemnity

After the shipment of goods, the exporter submits export documents to authorized dealer for negotiation of the same. Here authorized dealer is exporter’s bank. The banker is to ascertain that the documents are strictly as per the term of L/C. Before negotiation of the export bill, the banker should scrutinize and examine each and every document with great care and must be go through the original L/C. in the time of scrutiny, any kind of lacking can be found by the banker. This is called discrepancy. The discrepancy may be classified as major or minor. There are may be some discrepancies which are removable. If the discrepancies are minor, the exporter bills against submission of indemnity. Documents with discrepancies should be negotiated. With the permission of the exporters, such documents are to be sent on collection.

Negotiation

T the time of negotiation the checklist/ required documents are as follows:

- Commercial invoice 8 copies (4 original).

- Custom invoice of importers country.

- Packing list 8 copies (4 original).

- Certificate of origin (original).

- Inspection certificate by the agent of importer.

- Acknowledgement letter indicating received sample/ approval letter.

- Frightful letter etc.

۞ Remittance section

Remittance can be classified broadly into two types:

a) Outward remittance, and

b) Inward remittance.

۩ Outward Remittance

Outward remittance include sell of foreign currency by TT, MT, Drafts, Traveler cheque and as well as payment against import into Bangladesh. Outward remittance can be classified into two types. These are as follows:

- Private remittance, and

- Commercial remittance.

Private remittance

Family remittance facility, remittance of membership fees/Registration fees etc, Education, Remittance of evaluation fees, Travel, Health and Medical, Seminars and Workshops, Foreign national, Remittance for hajj, Other private remittance – official and Business Transaction.

Commercial remittance

Opening of branches or subsidiary companies abroad, remittance by shipping companies, airlines and courier service, remittance of royalty and technical fees, remittance on account of training and consultancy, remittance of profits of foreign firms/ branches, remittance of dividend, subscriptions to foreign media services, costs / fees for renters monitors, advertisement of Bangladeshi products in mass media abroad, bank charges, sundries.

۩ Inward Remittance

Inward remittance includes purchase of foreign currency by TT, MT, Drafts, Purchase of export bills and Traveler cheque. But due to lack of promotional activities the branch is failure to attract new customer for existing export and import business.

Findings and recomendation

Finding of the study

The study has following major findings:

- The activities of the bank is mainly divided three types: General banking, loan and advance and Foreign exchange.

- The foreign exchange income mainly is sourced by export and import business.

- The foreign exchange income shows an increasing rate.

- The income is expected to increase due to amendment of licenses.

- The bank has not taken any promotional activities to attract new customers.

- Thus the bank has achieved authorized dealership licenses, it has not required supplicant employees to meet the new customer.

۞ Strength &weakness of the organization

۩ Strength

Management: EXIM bank is processing the management skill in every part of internal division, such as credit and advance division, Human Resource Management division. The span between management is remarkable shorter.

Operation: EXIM bank avoids bureaucracy. Since it gas performed with 20 branches till today. It maintains the quick response through the better managerial skill. Strong communication between all levels of management helps in quick decision-making, which is followed by the bank.

Cohesion: Communications derives cohesion for the bank, which is motivating all the levels of management in togetherness.

Customer services: “Clients are the Partners” the bank believes in any suggestion from them are heartily acceptable. The employees of the bank are very helpful to give information and suggestion to their customers as well as reliable for customer service. Strengths in management skill, cohesion and avoiding bureaucracy help the bank in creating valuable services to their customers.

۩ Weakness

Competitiveness: The bank is bit of backward in sense of marketing. Other banks are issuing credit cards, introducing International Money Transferring, Electronic cash, networking system in whole Bangladesh controlled by the head office and expansion of Marketing Research and Development.

Promotional Activities: The bank can not avoid the importance of marketing promotions. But it needs a full-equipped marketing department. Advertising and Promotional activities are very simple in the department of the bank.

۞ Strength &weakness of the foreign exchange division

۩ Strength

The Rajuk avenue branch of the EXIM bank Ltd. has experience and self-motivated personals in foreign exchange division. They are very efficient and friendly to their tasks as well as customers. As per bank policy, EXIM bank Ltd. gives much more facilities to its valuable customers regarding export and import. Such as local Documentary bills for collection (LDBC) and local documentary bills for purchase (LDBP).

۩ Weakness

The Rajuk avenue branch of the EXIM bank Ltd. have its own license for foreign trading at some few years ago of my internship. Another thing is the Rajuk Avenue branch has one or two expertises in foreign exchange division. It does not have sufficient assistants for doing deskwork. Such as, keeping entry in the record books.

As the main objective of the bank is to support international transaction, so bank should have sufficient arrangement to meet the objective. By analyzing the whole report conducted for Export Import Bank of Bangladesh Limited, the recommendations could be made of the following issues to improve the overall performance:

- They should keep practicing on the modern banking system: such as on line banking and introduce the management information system to prove the competency within the local and global arena.

- There must be clear allocation of responsibilities, authority and accountability. Scope should be given for quicker decision making. Top down communication must occur at a full pace of commitment.

- There could be work desk interchange for job satisfaction by escaping the typed work.

- Marketing activities should be introduces more promotional activities such as social well fair.

- The entire department should be well informed regarding their goals and objective. It is essential to execute company objective into individual targets.

- The bank may take the initiative to develop an effective research and development center to get innovative ideas to capture the competitive markets.

- Job satisfaction and motivating instruments need for the bank. Such as rewarding system for better performance.

- Job description should be clarified and proper training should be imported to improve the performance of bottom level management.

- Every branch should have the separate new customer information booth for getting general information, which can avoid interrupting other working people.

- The bank should recruit some assistants for foreign exchange division of Rajuk branch to meet the new customer strong enough to satisfy present customer as well as to attract.

- The bank needs to publicize the facilities they are giving for foreign exchange and needs to credit scope to introduce new importers & exporters.

- Since the bank is renowned for export and import, the bank should introduce the new concept with flexibility in order to increase the number of importers and exporters.

- The bank has the provision for doing internship program but there is no organized program for internship. The bank can properly utilize the internees at minimum cost.

tried level best to cover all the necessary information of foreign exchange division and overview of EXIM bank so far. As we know the meaning of the EXIM bank, the bank is very much clear about its objective. All the division of EXIM bank, Rajuk Avenue branch are concerned regarding their responsibility, behavior towards their clients, admiralty, integrity and development of performance of the accomplishment of the bank’s goal.

In this report, it is the tried level best to cover all the necessary information of foreign exchange division and overview of EXIM bank so far. As we know the meaning of the EXIM bank, the bank is very much clear about its objective. All the division of EXIM bank, Rajuk Avenue branch are concerned regarding their responsibility, behavior towards their clients, admiralty, integrity and development of performance of the accomplishment of the bank’s goal.

The branch is new one. So, the impact cannot be properly analyzed. Moreover the authorized dealership license has been recently achieved. It is expecting if properly utilize the license the impact will be at satisfactory level.

Thus, I would like to conclude this report at such stage, where we have discussed all the relevant matter in detail and hope, if the bank goes ahead along with its present performance, the bank will be the top one in the country in respect of its loyalty, profitability, service and atmosphere. I believe that this two months internship program at EXIM bank of Bangladesh limited will definitely help me to realize my further carrier in the job market.

- Export Import Bank of Bangladesh Limited Annual Report and Accounts 2005.

- Newspaper – Prothom-Alo, Articles: “Celebrating 100 Years in Bangladesh”, Date of Publication: 19th January-2006.

- Rajuk Avenue branch of Export Import Bank of Bangladesh Limited.

- Different publication of EXIM bank.

- Conversation with bank officers, File study, Personal observation, Desk work.