ORIGIN OF THE REPORT

After completion of 8 semesters in the BBA Program of IIUC, 12 weeks’ organizational attachment is a must and the author completed his internship period in Eastern Bank Ltd (EBL), one of the reputed Private Commercial Banks of the country. During this 12-week period, he has worked in the SME department of the bank. While working in the department he has gone through the standard operating procedures carried out by the bank and understood them well. Also he was able to understand the regulatory compliance issues proposed by Bangladesh Bank (BB) regarding credit management practices.

OBJECTIVE OF THE REPORT

The main objective of this internship report was to get a practical exposure to credit Payment System of Eastern Bank Limited and the roles the commercial banks playing in this area. Besides, this repot will was meant to revolve around some specific objectives. Such as

- To provide a brief idea about the functions of the various departments.

- To make a SWOT analysis of the bank’s overall performance on the basis of the experiences shared during the rotation period and give acclamations, if any.

- Learning the system of credit payment by Eastern Bank Limited.

- Factor influencing in credit decision.

- To know about the function of credit risk management.

- To know the process of monitoring credit.

- To know about the Credit risk rating.

SCOPE OF THE STUDY

The scope of the study is limited to SME, Principal Branch only. Their was no intention whatsoever, to focus on how the loan and advances were marketed to the customers, how the relationships were built and how each customers were followed up or handled by the Relationship Mangers. Purpose of the report would be to focus on how the credit management practice is being carried out by the respective department like what is modus operandi, what are the evaluation techniques followed by the officers during evaluating a loan proposal and so on so forth. Also the report won’t cover various legal issues regarding disbursement and recovery procedures of a loan. And finally entire risk management issues in the report will revolve around SME loan proposals only.

LIMITATIONS

- The following limitations are apparent in the report—

- Time is the first limitation as the duration of the program was of 12 weeks only.

- Another limitation of this report is Bank’s policy of not disclosing some data and information for obvious reason, which could have been very much useful.

SOURCES OF DATA

- Primary sources of data: Direct conversation with the employees of Eastern Bank Limited.

- Secondary Sources of data: Annual Reports of the bank, different reports, operational manual for the employees, Bangladesh Bank Circulars, Bank Database and various other publications and websites.

METHODOLOGY

- For understanding the procedure of banking operations, the author had observed the operations and worked with the officers at the same time. He had interviewed the EBL Officials for getting more information.

- For the analysis part, data have been collected from the loan proposals and other documentation packages of the bank.

Overview of the Bank

History and Background of Eastern Bank Limited

The emergence of Eastern Bank in the private sector is an important event for the banking industry in Bangladesh. In 1991, when the Bank of Credit and Commerce International (Overseas) BCCI had collapsed internationally, the operation of this bank had been closed down in Bangladesh. Taking into account, the welfare of the BCCI employees and its depositor’s interest, the Bangladesh Bank, under the Reconstruction Scheme, then gave permission to form a bank named Eastern Bank Limited, which would take over all the assets, cash and liabilities of BCCI in Bangladesh, with effect from 16th August 1992. Thus Eastern Bank Limited started functioning as a public limited company on August 8, 1992 with the objective to carry out banking business in and outside of Bangladesh

It started its business as a scheduled bank with only four branches, which included Principal Branch and Motijheel Branch in Dhaka, Agrabad Branch in Chittagong and another branch in Khulna.In July1993, when the bank got its Authorized Dealership from Bangladesh Bank, then it started its expansion of branches. Six and three new branches were opened in 1994 and 1995 respectively. The very next year they inaugurated two more branches. At present, it has twenty-two branches, which are scattered, all over the major cities of the country in major business areas.

It started its operational activities initially with an authorized capital of TK 1000 million, divided into 10 million shares of TK 100 each and paid up capital of Tk. 310 million.

At 2002, the paid up capital stood at TK 720 million but the authorized capital remained unchanged at Tk 1000 million. The general public held 83.42 % of its shares while institutional investors held the rest. At present EBL is one of the fastest growing commercial banks in the country and the largest capital based bank in Bangladesh. As of December 2005 its paid up capital was TK 828 million.

The initial shareholders were the National Commerical Banks, various government agencies and some of the depositors who had agreed to accept shares in the new bank in lieu of their deposits. The first Board of Directors of EBL constituted under government supervision, consisted of seven directors from various business and professions. Eastern Bank Limited was under government control until the end of 2000 and therefore there were alot of deficiencies in management. In 2001, the board of directors bought in new professional management from various foreign banks who have been trying to modernize the bank ever since. At present Mr. M Ghaziul Haque and Mr. K. Mahmood Sattar are heading Eastern Bank Limited as the Chairman and Managing Director respectivefully

EBL’s Vision

EBL Vision is to become the Bank of Choice by transforming the way it does business and developing a truly unique financial institution that delivers superior growth and financial performance and be the most recognizable Brand in the financial services in Bangladesh.

EBL dreams to be the bank of choice of the general public, which includes both the consumer and the corporate clients. They want to build such an image that whenever people think of a bank, they will think of Eastern Bank. They have introduced state of the art banking technology, which has made banking easier and hassle-fee for all. It has adopted the tag line “Simple math, the philosophy of easy banking” and has changed its logo to reflect the changes that are taking place in EBL.

In order to achieve superior growth and financial performance for its shareholders, EBL is radically transforming the way it does business. The bank has already restructured from the traditional geographic matrix (branch based banking) to business unit matrix. The bank is also centralizing most of the business functions in the head office to ensure greater control and efficiency.

EBL’s mission

In line with its vision EBL has developed a mission statement, which reads as follows:

- We will deliver service excellence to all our customers, both internal and external

- We will constantly challenge our systems, procedures and training to maintain a cohesive and professional team in order to achieve service excellence

- We will create an enabling environment and embrace a team based culture where people will excel

- We will ensure to maximize shareholder’s value

Present Business Philosophy

The philosophy of the present management of EBL is to develop the bank into an ideal and unique banking institution. EBL wants to be different from other privately owned commercial banks operating in Bangladesh. They want to be a leader in the industry rather then being a follower. They want to be a leader in providing quality service to customers so that customers can get something additional from their services.

Till 2000, EBL operated in a Geographical Matrix, where the business of the bank was concentrated on the twenty-two branches divided into zones. But in 2001, the new management led by the Managing Director, Mr. Mahmood Sattar changed the geographic matrix structure of EBL into Business Matrix structure. The bank has been restructured into three main businesses, which are responsible for earning the incomes of the bank, These are:

- Corporate Banking

- Consumer Banking

- Treasury Banking

All other departments of the bank act as support units for these three units and help them in every possible way. Under this arrangement, the responsibilities and function of the branches have been reduced dramatically. Many of the activities like credit evaluation and approval, monitoring of loans, trade services etc are now centralized in the Head Office. The branches of the bank are termed now as the “Sales and Service Centers” whose primary focus is on delivering services to corporate and consumer clients and building and maintaining relationship with them

Objectives

EBL’s primary objectives are the following:

- To maintain a satisfactory deposit mix

- To grow its credit extension service to corporate as well as individual customers

- To increase its diversification of loan portfolio and geographical coverage

- To reduce present operating expenses further so as to increase earnings before tax

- To reduce the burden of non-performing assets.

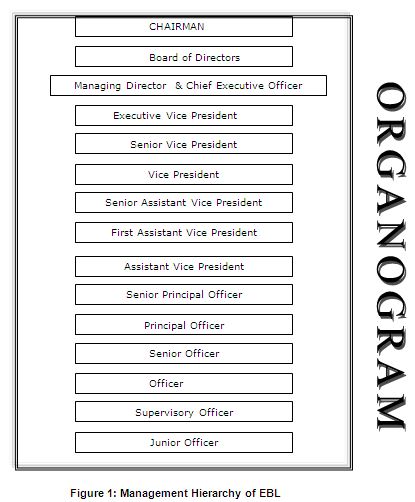

Management Aspect

Like every other business organization, the top management makes all the major decisions. The board of directors being at the highest level of organizational structure plays an important role in policy formulation, but it is not directly concerned with the day-day operations of the bank. They have delegated this duty to the management committee. The board mainly establishes the objectives and policies of the bank. There are three committees of the board for different purposes.

They are the following:

1. Executive committee comprising of seven members of the board.

2. Committee of the board for Administrative purpose

Committee to examine Bad Loan cases

The Chief Executive Officer (CEO) who is assisted by three Executive Vice-presidents (EVPs) looks after the day-to-day affairs of the Bank. Human Resources Department, Managing Director’s Secretariat and Audit and Compliance Department are under direct control of the CEO. The three Executive Vice President are in charge of Operations, Credit and Corporate Banking respectively. They control the affairs of these departments through the managers who are in charge of various departments under these divisions.

Mid and lower level employees get the direction and instruction from the top executives about the duties and tasks they have to perform. The chief executive provides the guideline and broad direction to the managers and employees, but delegates responsibility for determining how tasks and goals are to be accomplished.

Division of EBL

All policy formulations and its execution are carried out at the head office. There are eleven major divisions in EBL, which are the following:

a) Corporate Banking Division

b) Credit Risk Management and Administration

c) Consumer Banking Division

d) Brand Management Division

e) Trade Services Division

f) International Division

g) Human Resources Division

h) Information Technology Division

i) Audit and Compliance Division

j) Finance and accounts Division

k) Special Asset Management Division

l) Administration

The structures and functions of each of these divisions of EBL are described below: –

Corporate Banking Division

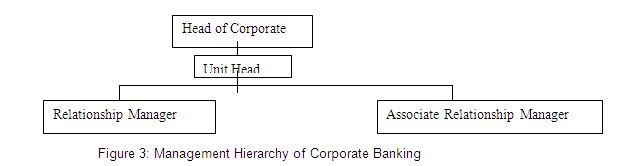

Corporate Banking Division came into existence because of the restructuring of EBLs business processes. Previously all the loan disbursement and monitoring activities were carried out by the officers of individual branches, which resulted in poor management and control of the process. To improve the poor management and control of the process, Eastern Bank decided to centralize its loan disbursement and monitoring activities. A separate Corporate Division was created which started operation on 10th January 2002. This division is responsible for bringing in profitable new corporate clients and retaining present clients by meeting their various needs. Corporate Banking provides various banking service such as products, credit facilities and financial solutions which addresses the diverse financial needs of corporate customers, public and private limited companies, NGOs and sole proprietorship concerns. It is also responsible for resolving credit issue problems and developing relationship between the customer and the bank.

The whole corporate division is divided into two areas. Area one comprises of Dhaka and Outstation Branches whereas Area two comprises Chitagong branches. Area one consists of six relationship units. Five units in Area one are responsible for looking after the bank’s assets and one unit is responsible for liabilities, while Area two has three asset units and one liabilities unit. Every asset unit has a unit head, who is in charge of that unit. Generally one Relationship Manager (RM) and one Associate Relationship Manager (ARM) work under the Unit Head. All Units head work under the Head of Corporate and they report directly to him. The management hierarchy of the Corporate Banking Division is given below:

Services of Corporate Banking:

- Structuring of Facilities for Corporate customers.

- Providing Financial Solutions

- Advisory Services

- Arrange Loan Syndications

- Developing Relationship between the Clients and the Bank

- Processing credit and other approvals for credit and other facilities. Provides a one stop service for Credit facilities.

- Handles pricing issues and Wallet Sizing Exercises to maximizes the earnings of the Bank as well as of the Client

- Coordinating service delivery of all EBL distribution channels (Sales and Service

- centers, Trade Services, Treasury, Credit issues as required for the customer.

- Ensures corporate customer’s complaints are addressed.

- Relationship Teams of EBL are available to serve you.

The main functions of this division are as follows:

- Targeting corporate clients and building business relationships with them

- Designing customized service for the clients

- Evaluating financial strength of the client

- Making possible recommendations for further expansion

Credit Risk Management and Administration

The main objective of this division is to evaluate the credit worthiness and debt payment capability of the present customers and loan applicants. The respective branches send all loans and advances proposals from the prospective borrowers to the Head Office Credit Risk Management (HOCRM) for approval. If this department finds the loan proposal attractive, it either approves it or sends it to the board for approval. It is responsible also for setting prices for credit facilities given to clients and ensuring that it is being implemented in the branches. This department also monitors the various loan accounts of the branches and prepares various statements for Bangladesh Bank.

The main responsibilities of the Credit Risk Management functions are:

- Oversee the bank’s credit policies, procedures and controls relating to all credit risks arising from corporate/commercial/institutional banking, personal banking, & treasury operations

- Approve risk transactions within their delegated authority and advise on credits which exceed such limits

- Ensure implementation of credit facilities through an independent Credit administration function

- Implement review and control policies on all lending portfolios

- Manage individual problem credits and monitor the distressed assets portfolio within EBL’s risk parameters

- Recommend provisions for loan losses complying central banks rules and norms

- Review lending programs and provide recommendations for approval.

The Credit Risk Management Department is assisted by the Credit Administration Department, who is primary concerned with the post- approval functions of the division. Credit Administration critically tracks and monitors the following:

- Credit expiry

- Past dues

- Excess over limit

- Document deficiency

- Reporting

Credit Administration is involved in basically two broad functions:

- Loan Monitoring

- Documentation

Loan monitoring

The most important aspects of this part are:

- Follow approval terms

- Proper loan disbursement

- Monitor interest payment

- Monitor Principal repayment

- Balance with general ledger

Documentation

The important functions of this part are:

- Look at sanction terms

- Fill up loan documentation checklist

- Ensure Proper loan documentation

- Obtain client sign off

- Filing with the Registered Joint Stock Corporation (RJSC)

- Registered mortgage deed execution

Consumer Banking Division

The consumer banking division deals with the financial needs of all the individual customers of the bank. The consumer banking activities are being carried out through the twenty-two branches of Eastern Bank Limited operating countrywide. Among these branches ten branches are located in Dhaka, five in Chittagong, three in Sylhet and one each in Khulna, Jessore, Bogra and Rajshahi. Previously these branches used to conduct all kind of business activities, including processing credit issue, conducting trade service, consumer service etc. But after the restructing process, all the branches are now mainly focusing only on delivering service to individual customers. EBL before did not have many attractive consumer products. However, Ebl has decided to give more focus on consumer banking and is developing modern delivery channels like ATMs, telebanking, internet banking, credit cards etc and many other new consumer products and services to meet specific financial demands of the customer as well as to make their life easy and convenient.

The main functions of this division are:

- Settlement of accounts

- Building strong relationship with individual customers

- Identifying individual needs of the customer and thus helping design products that will meet their need

- Providing locker services

- Providing ancillary services.

- Providing consumer loans

SME Banking

Small and Medium Enterprises (SME) in Bangladesh contributed 25% of gross domestic product (GDP) and 80% of the industrial jobs of the country in 2004. According to ADB, the country’s estimated 6 million SMEs and micro enterprises firms of less than 100 employees have a significant role in generating growth and jobs. This is a sector that has its own distinct needs and requires specialized focus. Eastern Bank Ltd. (EBL) has launched SME Banking in early 2005 with this view in mind.

At EBL:

- Provide SMEs with easy access to financing.

- Deliver products that ensure superior returns to our customers.

- Orient customers with industry trends, regulatory issues etc, for their success.

- Value long term relationship banking.

SME Banking is an integrated specialized area of the Bank, which addresses the diverse financial needs of Small and Medium Enterprises.

Local Business Houses (Private Limited Companies), Sole Proprietorship Concerns, Partnerships etc are considered to be our SME Customers. Services provided by SME Banking are as follows:

- Structuring of Facilities for SME Customers.

- Develops understanding of customer businesses and advises Financial Solutions

- Developing Relationship between the Clients and the Bank

- Processing credit facility requirements and arranging approvals for credit facilities.

- Handles pricing issues and Wallet Sizing Exercises to maximizes the earnings of the Bank as well as of the Client

- Ensures SME customers’ complaints and Service issues are promptly addressed.

- Coordinates activities of support unit Credit Administration unit which prepares security documentation, security registration, and CIB related issues.

The SME banking comprises two different segments, Small and Medium segments.

Small Segment:

The small segment of SME Banking handles small loans i.e. from Taka 100,000 up to 50, 00,000. This segment has various products for their customers, but currently only two products are available. Their products are namely:

- ASHA

- PUNJI

ASHA LOAN:

ASHA loan is a loan which is provided to the customers without any securities and for the first time the client can avail this loan for a period of one year. The officers at first carefully justify several criteria under which an ASHA loan can be fallen. The business has to be operated for at least 2 years and their turnover of sales to be justified for the amount of loan applied for.

Eligibility for an ASHA loan:

- Any sole proprietorship, partnership firms having minimum 2 years of successful business operation

- Monthly cash flow to support the proposed loan installment

PUNJI LOAN:

Features:

- Any business purpose loan from Tk. 1,000,000 to TK. 5,000,000

- To be repaid within maximum 36 months( next loan is repayable within 60 months)

- Collateral security required along with charge on business assets

- Loan repayable in equal monthly installment

Eligibility:

- Any sole proprietorship, partnership firms or private limited companies having minimum 3 years of successful business operation

- Monthly cash flow to support the proposed loan installment

Equal monthly installment sample:

For Tk. 1 lac: in 12 month BDT 9,074

in 18 month BDT 6,286

in 24 month BDT 4,897

in 36 month BDT 3,516

Medium Segment:

The medium segment of the SME Banking department functions almost like the corporate banking department of EBL. Mid segment of SME deals with various lending products of the Bank such as:

- SOD

- OD

- CC (Cash credit)

- SLC

- ULC

- LG

- LTR

- PAD

- Demand loan

- Term loan

- Time loan

- FDBP

- LDBP

Here are some products and services described so far I could understand on my practical work with the officers:

Brand Management Division

Although EBL is in the banking business for quite sometime its brand image has not grown strong and in order to succeed in the competitive bank environment it needs to enrich its brand equity. So far EBL has shunned any sort of promotional tools except for a few inconspicuous billboard advertisements, signboards and newspaper recruitment advertisement. However a new department called “Brand Management” has been set up in 2001 to give a new and enhanced brand identity to EBL. This department supervises the planning of advertisement campaigns for EBL’s products and analyzing customer feedbacks. With the aid of an advertising agency the logo and stationary of EBL has been changed and eye-catching brochures, calendars and posters have been prepared which are displayed at the sales & service centers.

Trade service division

Trade services are a major operational department of EBL. It deals with issues regarding to export, import and guarantees. It performs the job of financing and facilitating foreign trade. There are separate units operating within the trade services department in EBL. Those are:

- Export

- Import

- Guarantee

The major functions of Trade Services include the followings:

- Issuance of Letter of Credit

- Advising of Letter of Credit

- Negotiating documents

- Collection of Payments

- Facilitating trade by arranging loans to cater different needs of the clients

International division

International Division is responsible for assisting the authorized branches to deal in foreign trades, that is import and export business on account of the customers of the bank by giving approval for transactions and controlling them at various stages. It deals with all correspondents of foreign banks having arrangement with the bank

The functions performed by this division are as follows:

- Carrying out correspondent banking relationship

- Supervising of foreign exchange transaction of other units

- Supervising sale/ purchase of foreign currencies

Human Resources Division

The employees are Eastern Banks most valuable resource. Having competent and professional employees is becoming increasingly important in today’s competitive world and EBL has a significant competitive advantage in this respect. Many of its employees have worked here since the BCCI time and therefore have vast experience in their respective fields. New employees are recruited with sound academic background and wherever needed proper training is given to the employees after recruitment to equip them for their responsibilities.

The Mission of Human Resource division (HR) is to make EBL the Employer of Choice. The main functions of the division are:

Building Employer Image: The HR department has taken steps in building relationship with recognized educational institutes in order to create positive awareness about EBL as an employer. They have done this by extending internships to students, sponsoring student events and by participating in job fairs run by different universities.

Staffing: Another important task of the HR division is to prepare all formalities regarding appointment and joining of the successful candidates.

Training: HR department emphasizes on training and developing their employees through various training programmes held at the Bank’s own Training Center at Shantinagar and various outside locations, like Bangladesh Institute of Bank Management to enhance the skills of their employees, to help them deal better with their job responsibilities

Performance Appraisal of Employees: The employees of EBL are given an annual target performance based on a discussion between the employee and his or her supervisor. At year-end, a performance evaluation called Annual Classified Report (ACR) is carried out based on the target. Increments, bonuses and promotions are given to EBL employees based on this performance evaluation.

Information Technology Division

Previously, Eastern Bank had a very low level of automation. But in 2001, when the new management took over, they gave huge emphasis on computerizing the bank’s operations. After two years, almost all the operations in the bank are now automated. The Bank is also shifting to a new IT platform, which aims at maintaining, operating and strengthening the technology base of the bank, to enable error free production of information that ensures ongoing efficiency and profitability of operation. A world class banking software called Flex Cube has been installed which will centralize operations and provide Online Banking, Internet Banking, Automated Teller Machine, Telephone Banking and credit card facility etc.

With this implementation of state-of-the-art Information Technology, the IT division has become an important contributor to the bank’s overall efficiency and profitability. At present the IT department serves the following functions:

- Development of software for banks operation according to need, their maintenance and purchase of new software

- Maintenance of computer hardwares and upgrading the PCs whenever required

- Training the staff so that they can perform on the automated environment

- Troubleshooting with the new software

Audit and Compliance Division

The main function of this division is to provide legal assistance to the branches and to ensure strict adherence of rules and policies by all concerned officials of the bank through routine and surprise inspection and audit. The functions of this division are as follows:

- Implementing rescheduling process of stuck up loan to the branches for obtaining repayment schedule through strong persuasion and serve final notice as the condition required.

- Monitoring the individual cases with respect to their securities, value of securities and finally review of possibility of recovery of bank’s stuck-up classified loan

- Investigating suspicious or irregular matters being directed by higher management and being requested by branch in charges too

- Time to time follow up of stuck- up-advances of branches and keeping the branches under constant pressure

- Inspecting all branches operations at least once in a year

- Carrying out surprise audit as felt necessary

Finance and accounts division

The finance and accounts division is important for any bank because its task is to

- Maintain daily liquidly position, treasury bills, call money etc

- Monthly-accrued interest calculation of all interest-bearing accounts and amortization of all fixed and other assets

- Preparation of statement of accounts and profit and loss account for the bank and annual report of the bank

- Weekly deposit and advance analysis of the bank

- Cost of fund analysis.

Special Asset Management Division

Special Asset Management (SAMD) deals with all the classified accounts in the bank loan portfolio, mainly accounts which have fallen into substandard, doubtful and loss category. The responsibilities of the Special Asset Management Department are the following:

- Monitoring and controlling the classified accounts through monthly reporting and quarterly review

- Actively follow up with borrower for recovery

- Negotiating and restructuring debts wherever feasible on its own and in association with the concerned relationship manager

- Preparing a consolidated report of all bad loans written off on a quarterly basis and submitting the report to the head of credit risk management and Managing Director and CEO.

Administration

This department looks after the administrative matters and supply of all tangible goods to the branches. Some of the main functions of the division are as follows:

- Make arrangement for branch opening such as making lease agreement, internal decorations etc

- Print all security papers and bank stationery

- Purchase stationery items and distribute it to the branches

- Advertise in the different media about tender notice, general meetings and public interest

Strengths of the Bank

The strengths of the bank are the following:

Up till 2000, EBL carried out its operation like every other local bank. All of its branches acted as single banks and did everything from marketing to loan processing to relationship maintaining. In 2001 EBL changed its traditional way of doing business. Rather than operating as a geographical matrix, EBL started operating as a business matrix. The functional areas were separated and redefined as business units. This has allowed management to operate more efficiently.

The new organizational culture has resulted in centralized processes. Before the branches were empowered to do almost everything within limits. They were responsible for marketing, loan processing, account activity monitoring and other transactions. Their accountability did not go beyond sending statements to the head office annually. Under the current system management has more control on the overall bank and its day-to-day operations. As a result loan defaults have been lower because the Corporate Division and the Risk Management Division, at Head Office, scrutinize the loan proposals along with the branch managers

From 15 March 2003, EBL has started using Flex cube- a banking software, which caters to all the needs of retailer, corporate, treasury and investment Banking. Flex cube enables EBL to remain associated between all its branches and business units.

of the Bank has made the structure flat that has facilitated decentralization among the functional division. As a result, the decision-making procedure has become quick. Moreover, the management has greater control over the activities of the Bank.

Weakness of the Bank

The weaknesses of the bank are the following:

- In the new structure, each functional division is tall within the division and delegation of authority is also centralized. It has a significant effect over the whole institution because middle and lower level employees are becoming more frustrated as they are loosing their decision making power.

- As the organization is moving towards semi-multinational culture, some employees are resisting the change as they are accustomed with traditional banking system and do not want to change.

- Unimpressive Physical Layout: The physical layouts of several of the EBL branches are quite unappealing. Some are located at inconspicuous locations with dull premises. The interiors of Principal and Head Office are not properly decorated. These features of the Bank may create wrong impression in the customers mind, especially the ones who come for the first time.

Threats of the Bank

The following are the threats of the bank:

- Technological Obsolence: EBL has started using a very modern and sophiscated IT platform. The bank plans to change its entire business philosophy based on the uniqueness of this product and ancillary infrastructure. However, like every other novelty, this system has the risk of being obsolete as technological changes are coming very quickly and continuously.

- It faces constant threat from other local and multinational banks that are continuously trying to come up quickly with more new innovative products that appeals to customers first.

Opportunities of the Bank

The following are the opportunities for the bank:

- Day by day many banks are providing evening service to their customers. EBL can make necessary arrangements to implement it.

- Now a days many banks have introduced Islamic banking. Starting Islamic banking section can be an effective tool to grab the potential market segment.

Financial Ratio Analysis of Eastern Bank Limited

Conducting the financial ratio analysis is important for any bank, because it helps us to measure its performance, that is how adequately a bank meets the objectives of its shareholders (owners), employees, depositors and other creditors and other borrowing customers. So to get an overall picture of the performance of Eastern Bank Limited, it’s financial ratio analysis have been carried out in the following section.

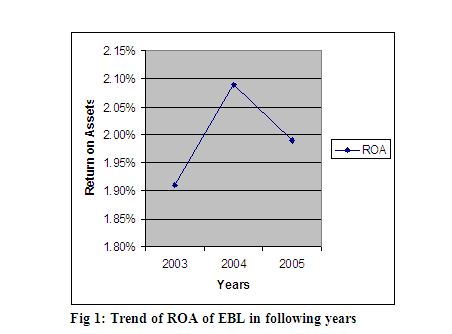

Return on Assets:

The return on assets is an indicator of a banks managerial efficiency. It indicates how capable the management of the bank has been in converting the banks assets into net earnings ie how much profit a company is able to generate for each dollar of asset invested.

Return on Assets = Net Income after Taxes

(ROA) Total Assets

| 2003 | 2004 | 2005 | |

| Net Income After Taxes | 357,771,944 | 483,365,229 | 546,515,028 |

Total Assets | 18,715,682,398 | 23,047,667,908 | 27,399,954,469 |

ROA | 1.91% | 2.09% | 1.99% |

From Figure 1 it can be observed that from Year 2003 to Year 2004 the return on assets had increased for Eastern Bank Limited. This indicates that the managers were efficient in converting the banks assets into net earnings. From Year 2004 to 2005 the ROA on investment decreases slightly, because the rate of increase of net income after taxes from 2004 to 2005 is less then the rate of increase of net income after tax from 2003 to 2004. The net profit in 2004- 2005 was slighty lower because the operating expenses of the bank went up, the salary and employee allowances were increased, while at the same time the bank spent a large amount of its money on business development, awareness of brand building, in the mass market of EBL’s product and services using electronic and print media. Overall from 2003- 2005 the ROA has increased which indicates that the company has been able to generate more profit for each dollar of asset invested.

Return on Equity:

The return on equity measures the rate of return flowing to the banks shareholder. It measures the net benefit that the stockholders have received from investing their capital in the financial firm.

Total equity capital

| 2003 | 2004 | 2005 | |

| Net Income After Taxes | 357,771,944 | 483,365,229 | 546,515,028 |

Total equity | 2,320,898,168 | 2,630,624,772 | 3,071.336,910 |

ROE | 15.42% | 18.37% | 17.79% |

From the above figure it can be seen that from Year 2003-2004 the ROE of EBL increased. This was because the rate of increase of net profit after taxes was high from 2003 to 2004. The wages did not increase substantially from 2003- 2004, the advertising costs did not increase so much, because aggressive advertising was not being carried out and other expenditures of the bank did not increase so significantly, so net profit increased rapidly from 2003-2004. But from 2004-2005 the operating costs increased significantly because of increase in salaries and allowances, increase in advertising and other expenditures, causing the rate of increase of net profit after tax to increase slightly.

The net interest margin measures how large a spread between interest revenues and interest cost management has been able to achieve by close control over earning assets and the pursuit of the cheapest sources of funding. The net interest margin is calculated using the following formula:

Interest income- Interest Expense

Total asset

| 2003 | 2004 | 2005 | |

| Interest income (a) | 1,682,551,683 | 1,894,252,122 | 2,373,288,995 |

| Interest expense (b) | 928,450,655 | 949,203,013 | 1,365,455,642 |

| (Interest income – Interest expense) (c) | 754,101,028 | 945,049,109 | 1,007,833,353 |

| Total asset (d) | 18,715,628,398 | 23,047,667,908 | 27,399,954,469 |

| NIM= c/d | 4.03% | 4.10% | 3.68% |

From the above figure we can see that the net interest margin has increased slightly from 2003- 2004. It has increased from year 2003-2004 because the rate of increase of interest revenue is higher relative to rate of increase of the interest expenses during the year. From 2004-2005 both interest revenue and interest expense has increased, but the interest expense has increased proportionately more then interest revenue, causing the net margin to dip slightly in value. Overall we can say that the management has been efficient in controlling revenue and expense cost since the net interest margin has not fluctuated so much, with slight deviation from one year to another

Net Non interest margin:

The net non interest margin measures the amount of noninterest revenue stemming from deposit service charges and other service charges the financial firm has been able to collect (called fee income) relative to the amount of noninterest costs incurred (including salaries and wages, repair and maintenance of facilities and loan loss expenses). The net non-interest revenue is calculated using the following formula:

Total assets

| 2003 | 2004 | 2005 | |

| Noninterest revenue (a) | 302,271,256 | 347,052,574 | 583,776,899 |

| Noninterest expense (b) | 297,600,339 | 399,670,759 | 535,794,924 |

| Total asset (c) | 18,715,682,398 | 23,047,667,908 | 27,399,954,469 |

| Net Non Interest Margin= (a-b)/c | 0.025% | -0.22% | 0.18% |

From the above table it can be seen that in 2003 net non-interest margin was positive. In 2004 it became negative whereas it increased and became positive again in 2005. Net-non interest margin was positive in 2003 because the non-interest revenue exceeded the interest expense. In 2004, the rate of increase of non- interest revenue was at a much slower pace then the rate of increase of non-interest expense causing the non-interest expense to exceed the non-interest revenue and eventually the net non -interest margin to be negative. Non

interest revenue increased because the firms operating expenses went up significantly. It implies that the bank was inefficient in controlling its noninterest expenses. In 2005 net non interest margin showed signs of increasing because the bank focused more on increasing its fee based income and service charges as a result its noninterest revenue exceeded the noninterest expense causing the net non interest margin to be positive and to be increasing.

Net operating margin:

The net operating margin measures how efficient the management has been in ensuring that its revenue grows faster then its rising costs. The net operating margin is calculated using the following formula:

Total operating revenue- Total operating expense

Total assets

| 2003 | 2004 | 2005 | |

| Total operating revenue | 1,056,372,284 | 1,292,101,683 | 1,591,610,252 |

| Total operating expense (b) | 297,600,339 | 399,670,759 | 535,794,924 |

| Total asset (c) | 18,715,682,398 | 23,047,667,908 | 27,399,954,469 |

| Net operating margin=(a-b)/c | 4.05% | 3.87% | 3.85% |

Trends in net operating margin of EBL

EBL has a decreasing trend in net operating margin from 2003 to 2004, with neglible decrease from 2004-2005. This is because during this period although the net interest margin increased, the net non interest margin decreased and became negative causing the net operating margin which is the combination of net interest margin and net non interest to decrease. In 2004-2005, although the net interest margin decreased from 2004 to 2005, but the net non-interest margin increased from being negative in 2004 to be positive in 2005, causing the net operating margin to decrease very slightly.

Asset Utilization Ratio:

The asset utilization measures the efficiency of the management in managing the company’s asset, so as to obtain more operating revenue for the company. The asset utilization ratio is calculated using the following formula:

Operating revenue

Total assets

| 2003 | 2004 | 2005 | |

| Total operating revenue(a) | 1,056,372,284 | 1,292,101,683 | 1,591,610,252 |

| Total asset (b) | 18,715,682,398 | 23,047,667,908 | 27,399,954,469 |

| Asset utilization ratio | 5.64% | 5.60% | 5.80% |

Trends in Asset Utilization Ratio in EBL

From 2003-2005 the asset utilization ratio in Ebl has been decreasing slightly with increase from 2004- 2005. This suggests that management has started to utilize its assets better to get higher yield from those assets.

Equity multiplier:

The equity multiplier measures how many dollars of assets can be supported by each dollar of equity (owners capital) and therefore how much of the firms assets must rely on debts. The equity mutiplier is calculated using the following ratio:

Total equity capital

| 2003 | 2004 | 2005 | |

| Total Assets (a) | 18,715,682,398 | 23,043,468,479 | 27,396,601,059 |

| Total equity capital(b) | 2,320,898,168 | 2,630,624,772 | 3,070,915,605 |

| Equity multiplier= a/b | 8.06x | 8.75x | 8.92x |

The equity multiplier of EBL has not increased so much from 2003 to 2005. It implies that the equity financing of the bank has increased slightly over the years and the bank has relied more on debt financing to finance its asset. There is less equity to finance the assets as a result there is less chance of failure risk on the part of the bank. The less the risk, the less the potential for high returns to the stockholders.

Earning spread:

Earning spread measures the effectiveness of the bank’s intermediate function in burrowing and lending money and also the intensity of competition in the bank’s market areas. Earning spread is calculated using the following ratio:

Total Interest Bearing Liabilities

| 2003 | 2004 | 2005 | |

| Interest income (a) | 1,682,551,683 | 1,894,252,122 | 2,373,288,995 |

| Earning asset (b) | 14,899,341,367 | 19,372,147,401 | 22,766,465,066 |

| Total interest expense (c) | 928,450,655 | 949,203,013 | 1,365,455,642 |

| Total interest bearing liabilities(d) | 9,470,899,794 | 12,471,732,216 | 16,572,184,346 |

| Earning spread=(a/b)-(c/d) | 1.49% | 2.17% | 2.19% |

Trends in earning spread of EBL

The earning spread of EBL is slightly increasing although the ongoing competition in the banking sector, which is the emergence of new banks, have decreased the earning spread of many banks. The bank has been able to earn slightly more income from its loan and advances then the interest rate, it has paid on the deposit to its customers, causing the earning spread to increase slightly from 2003-2004 with being more or less being stable from 2004-2005. It implies that the bank costs of fund- the interest rate that it has given to its customers on its deposits is slightly less then the revenue it has been able to generate from the loan and advances it has given out.

Liquidity risk

The liquidity risk is the probability that an individual or institution will be unable to raise cash precisely when cash is needed at reasonable cost and in the volume required. Liquidity risk is calculated using the following formula:

Cash assets+ Government securities

Total assets

| 2003 | 2004 | 2005 | |

| Cash Assets | 2,616,869,846 | 1,866,935,656 | 2,078,786,587 |

| Government securities | 3,331,354,100 | 4,041,035,400 | 4,663,009,900 |

| Total assets | 18,715,682,398 | 23,047,667,908 | 27,399,954,469 |

| Liquidity risk | 31.78% | 25.63% | 24.61% |

Liquidity risk indicator of Eastern Bank

It can be observed from the above diagram that EBL’s liquidity risk is increasing slightly as the cash and marketable security has increased less in proportion to total assets.

Cash assets include vault cash held on the financial firm’s premises, deposits held at Bangladesh Bank and deposits held with other depository institution.

Main Events of Eastern Bank Limited

- In 2002, Eastern Bank introduced its High Performance Account

- There was facility agreement signing ceremony between EBL and Pacific Bangladesh Telecolm Ltd in 2002.

- Loan agreement was signed between EBL and Transcom Beverages Ltd in 2002.

- There was agreement-signing agreement between EBL and ITCL. EBL joined Q-Cash Shared ATM Network in 2003.

- In September 2003, EBL launched its EBL Savings Insurance Accounts

- The state of the art IT platform of Flexible, a world class banking software was being implemented in carrying out transactions in the bank in 2003.

- EBL Auto Loan scheme was launched in 2004.

- There was Debenture Loan Signing Agreement between EBL and United Leasing Company in 2004.

- Offshore Banking Business was introduced in 2004.

- EBL SME & Bengaline Joint Promotion was carried out in 2005.

- EBL signed a structured finance deal with Singtel in 2005.

- In 2006 the Bank has introduced several kiosks in different locations in Dhaka.

Business Development Activities of 2005

As part of the ongoing business development program the Consumer and SME banking unit has signed joint promotion programs with major restaurants of Dhaka, Electra International, Rahim Afroz, Banglalink etc. In 2005 the bank has launched high yielding loans like Auto Loan, Jiban Dhara Loan etc.

In 2005 the bank felt the importance of creating its own remittance business to manage the recent foreign exchange crisis and the foreign exchange price volatility and as part of the remittance business development program the bank signed agreement with some of the renowned Money Exchange houses in the Middle East for instance Al Mona Exchange Company in Dubai and Al-Mullah International Exchange Company in Kuwait.

In 2005 the newly formed corporate finance unit effected various syndication and advisory transactions with customers like Karooni Knit Composite Ltd (KKCL), Shun Shing Power Limited and Pacific BD Telecolm Ltd etc. There is continuous emphasis being given on developing the deposit base.As part of the deposit building program the bank run various promotion activities to build its High Performance Account (HPA) and Savings Portfolio as well as its Fixed Deposit portfolio.

Products and Services Offered by EBL

Categories of SerVices of Eastern Bank Limited:

Eastern Bank Limited is capable of handling all the banking needs of customers and is always available to provide personalized one-stop services. The services are customized and confidential. The different categories of services that EBL offers are as follows:

Retail Banking

The Retail Banking Division comprises the domestic branch network with the specialized customer credit, real estate finance. Retail banking deals with the banking services to the individuals. Eastern Bank’s retail banking strategy is aimed at keeping as closely in tune with their customers’ needs as possible and further improving the quality of advisory services. As a result, EBL offers different product ranges to different target groups. It includes the following;

Deposits Services: Individuals may open current, savings, STD, fixed deposit accounts.

Wage Earners Services: EBL offers a few innovative schemes to Bangladeshi wage earners working overseas.

Institutional Banking

Eastern Bank Limited offers various services to foreign mission, NGOs and voluntary organization, consultants, airlines, shipping lines, contractors, schools, colleges, universities, donor agencies and consultants.

The services include the following:

- Deposit services

- Current accounts in both Taka and major foreign currencies.

- Convertible Taka accounts

- Local and foreign currency remittances.

- Various types of financing to cater to the banking requirements of multinational clients.

Corporate Banking

A professional account management team caters to the needs to corporate clientele and provides a comprehensive range of financial services to national and multinational companies. Its services include:

- Corporate deposit accounts

- Projects finance investment, constancy and other finances.

- Syndicated loans.

- Local and international treasury products.

- Bonds and guarantees.

- Skilled and responsive attention to varying lending needs.

Commercial Banking

Being a commercial Bank EBL provides comprehensive banking services to all types of commercial concerns. Some of the services are:

- Trade finance

- Issuing of import L/Cs.

- Advising and confirming export L/Cs.

- Bonds and guarantees.

- Investment advice.

- Project finance opportunities for import substitution and export oriented project.

- Leasing: It is a very flexible arrangement, which is tailored to suit most requirements of its clients. Lease financing by Eastern Bank is a unique means of funding a firm’s need for capital equipment without actually lending to the firm.

Correspondent Bank

Services to correspondent banks include:

- Current accounts services where settlement is necessary.

- Issue bonds and guarantees in support of their customer business.

- Advise letter of credit and negotiation of documents.

- Market intelligence and status report.

Products and Services offered by EBL

Easter Bank Limited is a commercial bank, which has to operate under the rules and regulations of Bangladesh Bank for schedule commercial banks. It has highly skilled and qualified professional staffs, which are capable of handling all the banking needs. An officer who is responsible for all activities done in that department specially supervises each section. Its services are personalized and backed by a poor level of automation.

Services Offered by the Bank

The business of bank is to provide financial services to customers. Their goodwill and trust alone have made the banking industry a pillar of strength in society. The future growth of the banking industry and its profitability depends on customer satisfaction. EBL provides various financial services. In addition, some special services are offered that helps the bank to keep pace with competitive market.

CREDIT PRODUCT:

Eastern Bank around twenty four credit products, of which twenty are funded and four non-funded. It is observed that only few products are marketed with particular fascination on overdraft and cash credit which are supposed to be a very high-risk product and least effective from control point of view. Efforts should be made to sell other products keeping in mind customer’s need and in line with their cash flow cycle and thereby ensure effective credit monitoring.

LIST OF CREDIT PRODUCTS OF EASTERN BANK LIMITE

| NAME | DESCRIPTION | PURPOSE | RISK FACTOR | TENOR/ VALIDITY |

| PAD | iPayment Against Document. | iAdvance Against Sight L/C iForced Loan. | iRecourse on Title to Import Document. | i21Days per Bangladesh Bank. |

| CC (HYPO) | *Cash Credit Against Hypothecation of Inventory and Book Debts. | iTo Finance Inventory. iOther Business Operations. iGeneral Purposes. | iRecourse on Sales. iEver Green. | i12 Month. |

| CC (PLEDGE) | iCash Credit Against Pledge of Inventory and Hypothecation of Inventor. | iTo Finance Pledge Inventory. | iRecourse on Pledge Inventory. iHigh Monitory Risk. iEver Green | i12Months. |

| ACCEPTANCE | iAcceptance Against ULC. | iTo Finance Assets throughu Banker’s Acceptance. | iRecourses on Sales. | i12Months. |

| OAP | iOwn Acceptance Purchase. | iTo Refinance Banks Acceptance. iForced Loan. | iNo Recourse Clean Finance. Ever Green. | i12Months. |

| LBPD | iLocal Bill Purchased. | iTo Purchase/Discount Against .Loan. iUpfront Interest to be Realized. | iRecourses on Banks thru Acceptance. iResidual on Client. | i45/180Days. |

| LAFBD | iLoan Against Foreign Bill Documentary. | iTo Purchase/Discount Export Doc, Against Export Contract Sight/ Usance. iUpfront Interest to be Realized (diff in FX Rate). | iRecourse on export Doc. Payment risk Residual on Client. | i45/180Days. |

| SLC | iSight Letter of Credit. | iFor Importation. | iRecourse on Title to Import Document. | i12Months. |

| ULC | iUsance Letter of Credit. | iFor importation. | iRecourse on Sales. | i12Months |

LG | *Letter of Guarantee.

| iFor Contractual Obligation. | *Performance Risk. *Ever Green. | *Specific Period. *Open Ended. |

| PC | iPacking Credit Against Export L/C& Export Order. | iTo Finance Export L/C. iPre–shipment Finance. | iPerformance Risk. iLien on Export L/C. | i180 Days. |

| SOD | iSecured Overdraft. | iGeneral Purposes. | i100% Cash Covered. *No Credit Risk. iEver Green.

| i12 Months. |

| OD | iOverdraft Against Other Collateral | iGeneral purposes | iHigh Credit Risk iRecourse on Sales iEver green | i12 months |

| Import Loan (Hypo) | iImport Loan Against Hypothecation Inventory and Book Debts | iTo Finance Import L/C or Against Contract.

| iRecourse on Sales. | i180 Day. |

| Import Loan (Pledge) | i Import loan Against Imported Merchandise Pledged and Hypothecation of Book Debts. | i To Finance Import L/C Merchandise under Pledged. | iRecourse on Pledge Inventory. iHigh Monitory Risk. | i180 Days. |

| Demand Loan (Hypo) | iDemand Loan Against Hypothecation of Inventory and Book Debts. | iTo Finance Inventory Procure Locally. iTo Finance Duty/Tax. | iRecourse on Sales. | i180 Days. |

| Demand Loan (Pledge) | iDemand Loan Against Pledge Inventory Procedure Locally and Hypothecation of Book Debts. | iTo Finance Inventory Procure Locally under Pledge.

| iRecourse on Pledge Inventory. iHigh Monitory Risk. | i180 Days. |

| Time Loan | iTime Loan Against Other Security | iTo Finance Fixed / other Asset. | iRecourse on Sales iCollateralize by Fixed /other Assets. | i12 Months. |

| Time Loan | iTime Loan Against Foreign Bill-Clean | iTo Finance Export Contract | iClean Finance Performance Risk. | i120 Days |

| Term Loan | iTerm Loan Against Fixed assets. | iTo Finance Fixed Assets. | iRecourse on Fixed Assets High Risk. | iOver 12 Months. iMax 7 Years.

|

| BCP (Foreign) | iBankers Cheque Purchase (Foreign) | iTo Purchase /Discount Foreign Currency. ..Drafts/Payment Order. iUpfront Interest to be Realized. | iRecourse on Banks.

iResidual on Client. | i30 Days. |

| BCP (Local) | iBankers Cheque Purchase (Local). | iTo Purchase /Discount Bank Draft /Pay Order. iUpfront Interest to be Realized. | iRecourse on Banks.

iResidual on Client. | i30 Days. |

| Fwd FX | iForward Contract. | iCover Exchange Risk Against Letters of Credit. | iPerformance Risk. | i180 Days. |

Secured Overdrafts (SOD):

It is a continuous advance facility. By this agreement, the banker allows his customer to overdraft his current account up to his credit limits sanctioned by the bank. The interest is charged on the amount, which he withdraws, not on the sanctioned amount. MBL sanctions SOD against different

- The processes of extending SOD are as follows –

- The party must have a current A/C with the branch.

- If the ownership of the firm is proprietorship, then a trade license must be submitted and in case of a limited company, all the documents required to open a current A/c should be submitted. The financial statements of the concerned firm should also be submitted.

- The party must maintain a good transaction with the branch and have a good turnover rate.

- The party will apply to the officer in charge of credit department (SME) of the branch for SOD arrangement.

- The concerned officer will prepare a “Credit Memorandum (CM)”, where he writes about the business concern, details of proprietors/ directors of the concern, management structure, the existing credit facilities, the particulars about the facilities that asked for-such as margin limit, date of expiry, details of security, and any other relevant information. Then the proposal is sent to the Head Office for approval.

- The credit risk management (CRM) department analyzes the proposal and scrutinizes all the factors regarding this proposal. If they are satisfied then they approves the proposal. The proposal is declined if this department thinks the applicant is not worthy to get loans. They sometimes approve the proposal with some additional conditions.

- Then the head office approval is sent to credit Administration department and this department is supposed to do the formalities regarding security documentation which are to be kept under banks custody.

- After all necessary documentation, this department issues two copies of sanction letter, one is given to client and another is kept with the Credit Admin department In both the sanction letter the client signs after accepting all the terms and conditions.

- If the client accepts all the conditions of the sanction letter and likes to avail the facility, then the amount sanctioned is loaded in a separate OD account. Now the client can avail this overdraft facility anytime from the bank.

Cash Credit (CC):

Cash Credit (CC) is an arrangement by which a banker allows his customer to borrow money up to a certain limit. It is operated like overdraft account. Depending on the needs of the business, the borrower can draw on his cash credit account at different time and when he gets money can adjust the liability. Depending on charging security there are 2 forms of cash credit-

Cash Credit (Hypothecation

The mortgage of movable property for securing loan is called hypothecation. Hypothecation is a legal transaction whereby goods are made available to the lending banker as security for a debt without transferring either the property in the goods or either possession. The banker has only equitable charge on stocks, which practically means noting. Since the goods always remain in the physical possession of the borrower, there is much risk to the bank. So, it is granted to parties of undoubted means with the highest integrity.

Cash Credit (Pledge

Pledge is the bailment of goods as security for payment of a debt or performance of a promise. Bailer in this case of called the “Pawnor” and the bailee is called the “Pawnee”. In a contract of pledge, pawnor must deliver the goods pledged to the Pawnee either actually or constructively. Transfer of possession in the judicial sense, is essential in the valid pledge. In case of pledge, the bank acquire the possession of the goods or a right to hold goods until the repayment of credit with a special right to sell after due notice to the borrower in the even of non-repayment. The legal framework in this regard is the “Contract act-1872”.

Processes of opening a CC A/C are shown in the following flow chart-

- The interested party must have a current account and good transaction with the branch.

- Applies for cc hypothecation or cc pledge arrangement.

- The concerned officer prepares a “Credit Proposal” detailing all relevant information.

After getting the cash credit arrangement, the banker will issue a cheque-book for withdrawing cash from account. Whenever the CC account holder wants to withdraw cash from the account, the cash officer will scrutinize the amount of cheque in order to make sure that the total drawing does not exceed the sanctioned limit.

The charge documents required for opening a CC account are as follows-

- Demand Promissory Note (DP Note)

- Letter of Agreement

- Revival Letter

- Letter of Continuity

- Letter of Hypothecation/Pledge

- Letter of Guarantee

- Memorandum of Deposit of Title Deed (in case of CC hypothecation arrangement)

- Stock Report

- Letter of Disclaimer

Purchases & Discount of Bills:

Purchase and Discount of Bills is also a special form of advances, MBL normally purchase demand bills of exchange that are called “Drafts” accompanied by documents of title to goods such as Bill of Lading, Railway or Truck Receipt. The purchase of bills of exchange drawn at an issuance, i.e., for a certain period maturing on a future date and not payable on demand or sight is termed as discounting a bill and the charge recovered by Bank for this is called “Discount”.

GUARANTEE:

The branch offers three types of Guarantee that are as follows:-

Tender or Bid Bond Guarantee:

The tender guarantee assures the tenderee that tenders shall uphold the conditions of his tender during the period of the offer as binding and that he / she will also sign the contract in the event of the order being granted.

Performance Guarantee:

A Performance guarantee expires on completion of the delivery or performance. Beneficiary finds that as a guarantee, the contract will be fulfilled in every respect and can retain the guarantee as per provision for loan time. This can be counteracted by including a clause stating that the supplier can claim under the guarantee, by presenting an acceptance certificate signed by the buyer.

Payment Guarantee:

This makes guarantee that the party will make payment after completion of the work

LOAN PROGRAMS/ SCHEMES:

The Bank provides Loans and Advance to Individual, Business entities group, Industries etc. It provides loan to both Trading and Manufacturing concern on Hypothecation and Pledge basis. Industrial loan also extended by the bank on Hire Purchase basis. Loan also provided by the bank for Foreign trade against imported materials and Confirmed L/C. Bank has two types of loan programs:

LOAN: Loan in the form of revolving credit and frequent Repayment and Adjustment.

ADVANCES: Loan in one shot disbursement and at a time repayment. The bank allows advanced on secured basis. Security and Collateral in the node of cash, quasi-cash and goods /real estates are taken by bank commonly.

BASIC INFORMATION OF LOAN:

Trade Finance, Finance against work order, Individual loans against security, Purchase of bills/Bill discounting, Letter of credit.

No minimum amount is fixed up. Amount is fixed on the basis of requirement.

Rate of Interest (Floating rate): Rate range from 14% to 17%.

- Normal client – 16%

- Special or valued client – 14%.

(Computed interest is charged on daily product basis and interest realized quarterly).Term of Loan: 1-12 months, Loan can be adjusted earlier.

Mode of repayment:

Loans: Repayment is made any time in case of revolving credit.

The entire receivables including interest is repaid and adjusted at the end of term loan. No debit balance should be in the account.

Security/Collateral: Hypothecation / Pledge of raw materials, Stocks, Hypothecation of furniture, Fixture and machinery and other goods, Building and other immovable properties and DP note.

LOAN PROCESSING COST:

Actual basis. Appraisal fee: 5% – 1% of the total loan sanctioned.

Legal fee: Examination and technical assistance fee (in case of project).

LOAN PROCESSING TIME:

It varies with the nature of loan – Trade finance – 1-2 weeks-Loan Proposals require BOD approval-3 weeks-Secured overdraft (SOD) – IF a third party issue the financial instrument than it may take more time. Otherwise, within a day by the manager .In case of a big amount of short term finance, if requires BOD approval and so, it may take even a month to sanction.

PAPER/ DOCUMENTS REQUIRED:

Security documentation includes Accepted sanction letter, Letter of continuity, Letter of Revival, Demand promissory note, Personal guarantee of the client, Letter of authority, Letter of lien, Trade license, Tax identification number, Business plan, Cash flow statement, Fund flow statement, Balance sheet, Income statement, etc.

Procedures for giving advances

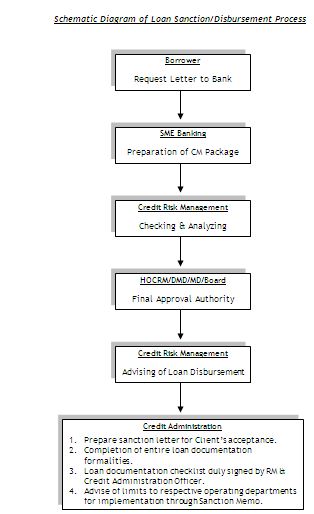

EBL usually follows these steps for sanctioning any kind of advances as available with the branch-

First step:

The prospective borrower will submit a request letter to the branch for loan

Second step:

After receiving the request letter, EBL sends a letter to Bangladesh Bank for obtaining a report from CIB (Credit Information Bureau). The purpose of the report is to being informed that whether the borrower has taken loan from any other bank(s); and if taken, whether these loans are calcified or not.

Third step:

After receiving CIB report, if the bank thinks that the prospective borrower will be a good borrower, then the bank will scrutinize the document. In this stage, the Bank will look whether the documents are properly filled up and signed.

Fourth step:

This is the processing stage. The branch will prepare a Proposal. The proposal contains following relevant information-

- Borrowers name

- Business Address

- Factory address

- Country of Incorporation:

- Sector / Code:

- Operating CASA Acc No:

- Company Established:

- Relationship Since:

- GROUP POSITION

- PURPOSE OF REQUEST:

- PURPOSE OF FACILITY

- REPAYMENT SOURCE

- COLLATERAL / SECURITY/ SUPPORT

- TERMS & CONDITIONS:

- Declaration:

- All procedures in respect of opening of Account have been complied with.

- All necessary documents establishing the borrower’s legal entity have been obtained.

- Existing Securities / Banking documentations and collaterals with their valuation have been checked and they are in order.

- Documents establishing that proposed facility is within authorization and borrowing powers of the applicant have been obtained.

- All Assets offered as security / collateral have been verified to be free from all encumbrances.

- Security documents as prescribed have been obtained along with complete set of borrowing documents.

- The borrower is a Director / Shareholder of our Bank.

- The borrower is a Director / Shareholder of other Bank. If yes, which Bank.

- The borrower is a Director of any Non Bank Financial Institution (NBFI). If yes, which Financial Institution

- CIB report dated __/__/____ from Bangladesh Bank is satisfactory and is in file.

17. BOARD OF DIRECTORS/ PARTNERS/ SOLE PROPRIETOR:

18. MANAGEMENT:

19. LEGAL STATUS & COMPANY BACKGROUND (Include the locations of the

Business, Project, Factory, Machinery details):

20. MANAGEMENT EVALUATION, RISK & MITIGANTS:

21. INDUSTRY / LINE OF BUSINESS:

22. MAJOR COMPETITORS/ COMPETITIVE POSITION / RISK & MITIGANTS:

(Market share, Revenue & margin comparison with the competitors to be provided)

23. STATUS OF THE BORROWER WITH COMPETITOR BANKS N/A

24. RELATIONSHIP HISTORY, PROFITABILITY AND ACCOUNT STRATEGY: New Account

25. FINANCIAL EVALUATION:

26. ANALYSIS OF SOURCES OF REPAYMENT (Financial, Security, Collateral etc):

27. BORROWER/ OBLIGOR RISK GRADING: N/A

28. ISSUES/ EXCEPTIONS RELATING TO DOCUMENTS, SECURITIES AND TERMS/ CONDITIONS & COVENANTS:

29. JUSTIFICATION OF LIMIT, FACILITY STRUCTURE & RECOMMENDATION:

The branch has to send the proposal to the head Office. Head Office will prepare a minute and submit it before the Credit committee.

Fifth step:

After receiving the sanction advice, the branch will collect necessary document. These documents are:

- Joint promissory note

- Single promissory note

- letter of undertaking

- Loan disbursement letter

- Debit figure confirmation sheet

- Letter of continuity

- Letter of authority

- Letter of revival

- Right of recall the loan

- Letter of guarantee

- Letter of indemnity

- Trust receipt

- Hypothecation of goods

- Hypothecation of vehicles

- Counter guarantee

- Letter of lien

- Letter of lien

- Letter of lien in case of advance against FDR

- Letter of lien and authority of advances to third parties against fixed deposit/call deposit/special deposit or margin or margin deposit

- Letter of authority to encash FDR

- Letter of agreement for packing credit

- Letter of guarantee for opening L/C

- Charges over bonds or certificates or shares etc. by third party to secure specific and general liability

- Memorandum of deposit of title deeds

- Hypothecation of goods to secure a demand cash credit or overdraft/loan amount Guarantee by third party.

Sixth step:

After verifying all the documents the branch disburses the loan to the borrower. A “Loan Repayment Schedule” is also prepared by the branch and is given to borrower.

Seventh step:

After the disbursement of the loan the bank follows the borrower in the following manner-

- Constant Supervision, Monitoring & Follow-up.

- Working Capital assessment.

- Stock report.

- Break Even analysi

Eighth step:

The loans are repaid in installments. These installments are according to bank directives. Some loans are repaid all at a time. If any loan is not repaid the notices served to the customer. Sometimes legal actions also taken for recover the loan.

Charging Security

EBL charges the following two types of securities-

1. Primary security

2. Collateral security

The modes of charging securities usually followed by the branch are as follows—

a.Pledge

b.Hypothecation

c.Lien

d.Mortgage

e.Assignment

f.Set-off

Lien:

Lien is the right to retain possession and not right of ownership Bank’s lien is general lien over its own financial obligation to clients. Property under line cannot be realized / sold and proceeds thereof cannot be appropriated without notice to the owner and sometimes without court’s order.

Hypothecation:

This is mortgage of movables by an agreement and here neither possession nor ownership is transferred. Hypothecated goods cannot be sold out/disposed of off without notice and court’s order. However, if a special power of attorney is taken in that case it can be disposed off without going to the court.

Pledge:

Pledge is the bailment of goods as security of payment of debt or performance or promise. Here, title and ownership are not transferred. Pledge goods may be sold out and proceeds thereof may be appropriated towards adjustment of Liability in case of failure of the borrower to repay of fulfill the terms and conditions. MBL has no charge of this type.

Mortgage:

Mortgage is the transfer of interest of immovable property to secure the repayment of money advanced. Ownership remains with the mortgagor. In case of equitable mortgage, court’s order is necessary and in case of registered mortgage court’s order is not necessary for sale/disposal of the mortgaged property for adjustment of advance. the legal framework in this regard is the “Transfer of Property Act-1982”.

Assignment:

Assignment means the transfer of any existing or future right, properly or debt by one person to another. The person who assigns the property is called the assignor and the person to whom it is transferred is called the assignee. This charge is applicable to Book Debts, Insurance Polity etc.

Set-Off:

Set-off means the total or partial merging of a claim of one person against another in a counter claim by the latter against the former. Set-off arises when a debtor or his creditor wishes to arrive at the figure owing between them when separate accounts or debt are involved.

Loan Classification, Provisioning Policies, Risk Management Framework & Recovery Strategies of Eastern BankLoan classification:

When the borrower fail to pay installments timely, banks ranks the client in three classes according to the risk associated with the client. Any Loan if not repaid/renewed within the fixed expiry date for repayment will be treated as irregular just from the following day of the expiry date. This loan will be classified as

- Sub-standard: if it is kept irregular for 6 months or beyond but less than 9 months.

- Doubtful: if for 9 months or beyond but less than 12 months and

- Bad Debt: if for 12months or beyond.

Policy on loan classification of EBL:

The process of gradually upgrading the policies on loan classification and provisioning to the international level is going on. Measures have been taken to strengthen the credit discipline and the process of classification has been simplified. The following revised policies on loan classification and provisioning has been issued.

Categories of Loans: All loans and advances will be grouped into 3(Three) categories for the purpose of classification, namely

Continuous Loan

Demand Loan

Fixed Term Loan and

The loan Accounts in which transactions may be made within certain limit and have an expiry date for full adjustment will be treated as Continuous Loans. Examples are: CC, OD etc.

The loans that become repayable on demand by the bank will be treated as Demand Loans. If any contingent or any other liabilities are turned to forced loans (i.e. without any prior approval as regular loan) those too will be treated as Demand Loans. Such as: Forced LIM, PAD, FBP, and IBP etc.

The loans, which are repayable within a specific time period under a specific repayment schedule, will be treated as Fixed Term Loans.

Basis for Loan Classification of EBL:

Objective Criteria:

(a) Any Continuous Loan if not repaid/renewed within the fixed expiry date for repayment will be treated as irregular just from the following day of the expiry date. This loan will be classified as Sub-standard if it is kept irregular for 6 months or beyond but less than 9 months, as `Doubtful’ if for 9 months or beyond but less than 12 months and as `Bad-Debt’ if for 12months or beyond.

(b) Any Demand Loan will be considered as Sub-standard if it remains unpaid for 6 months or beyond but not over 9 months from the date of claim by the bank or from the date of forced creation of the loan; likewise the loan will be considered as Doubtful’ and Bad/loss if remains unpaid for 9 months or beyond but not over 12 months and for 12 months and beyond respectively.

(c) In case any installment(s) or part of installment(s) of a Fixed Term Loan is not repaid within the due date, the amount of unpaid installment(s) will be termed as `defaulted installment’.

(i) In case of Fixed Term Loans, which are repayable within maximum five years of time: –

If the amount of ‘defaulted installment is equal to or more than the “amount of installments” due within 6 months, the entire loan will be classified as “Sub-standard”.

If the amount of ‘defaulted installment is equal to or more than the amount of installments due within 12 months, the entire loan will be classified as ”Doubtful”.

If the amount of ‘defaulted installment is equal to or more than the ‘amount of installments due within 18 months, the entire loan will be classified as ”Bad & Loss.”

(ii) In case of Fixed Term Loans, which are repayable in more than five years of time: –

If the amount of `defaulted installment’ is equal to or more than the amount of installments due within 12 months, the entire loan will be classified as ‘Sub-standard.’

If the amount of `defaulted installment ‘ is equal to or more than the amount of installments due within 18 months, the entire loan will be classified as ‘Doubtful’.

If the amount of ‘defaulted installments ‘is equal to or more than the amount of installments due within 24 months, the entire loan will be classified as ‘Bad-Debt’.

Explanation: If any Fixed Term Loan is repayable at monthly installment, the amount of installments due within 6 months will be equal to the amount of summation of 6 monthly installments. Similarly, if repayable at quarterly installment, the amount of installment(s) due within 6 months will be equal to the amount of summation of 2 quarterly installments.

Qualitative Judgment:

If any uncertainty or doubt arises in respect of recovery of any Continuous Loan, Demand Loan or Fixed Term Loan, the same will have to be classified on the basis of qualitative judgment be it classifiable or not on the basis of objective criteria.

If any situational changes occur in the stipulations in terms of which the loan was extended or if the capital of the borrower is impaired due to adverse conditions or if the value of the securities decreases or if the recovery of the loan becomes uncertain due to any other unfavorable situation, the loan will have to be classified on the basis of qualitative judgment.