Executive Summery

Export import Bank of Bangladesh Limited (EXIM Bank) is one of the leading private commercial bank in this country. EXIM Bank Limited follows the rules and regulations proscribed by the Bangladesh Bank for scheduled Commercial Banks. There is large number of small savers with small amount of adequate knowledge about complicated investment affairs. The Bank provides them with safety, liquidity, return, and safety of savings. The functions of the bank cover a wide range of banking and functional activities to individuals, firms, corporate bodies and other multinational agencies.

A Bank is an economic institution whose main aim is to earn profit through exchange of money & credit instruments. The banking sector of Bangladesh is passing through a tremendous reform under the economic regulation. Currently this sector is becoming extremely competitive with the arrival of multinational banks as well as emerging and technological infrastructure, effective credit management, higher performance level and utmost customer satisfaction. This internship report has been prepared on the “General Banking System & Marketing Activities at EXIM Bank Limited”

This internship report is a partial requirement for the Masters in Business Administration (MBA). As a part of the internship program, I placed at Savar branch. During the Three month long internship program I have taught lot about commercial banking operations of this organization specially the general banking activities and also marketing practice of EXIM Bank of Bangladesh Limited.

This report not only explores EXIM Bank Limited activities as one of the leading non-government companies, but also highlights the role of EXIM Bank Limited in the financial sector of Bangladesh. The internship program helped me a lot to implement my theoretical knowledge into practical Work environment.

Here I give detail explanation about the general banking activities & also give the brief explanation about launching of Islami Banking etc. I also try to cover General Banking System & Marketing Activities and marketing activities of EXIM Bank Ltd. in the Project Part.

Before concluding the report I have represented my suggestions that I think necessary to materialize for the prosperity of the bank.

Introduction:

Internship is the partial fulfillment of the requirement for the degree of Master’s in Business Administration (MBA). This report outcome of the three month Internship program conducted in Exim Bank Ltd., Savar Branch, one of the reputed Shariah Based Schedule Commercial banks of the country.

Banks are the primary contributor to the economy of a country. So it can be said that commercial bank is a profit making institution that hold the deposits of individuals and business in current and savings accounts and then uses these funds to make loans. Exim Bank plays an important role in economic development of a nation. At presents all kinds of financial transactions including general banking, investment, export and import transactions are done through banks. People are now dependent to do their all kinds of business transactions with Bank by general banking, investment activities, foreign exchange and other related activities of Bank.

Banking sector in Bangladesh has been pursuing the policy of expansion and growth of branches and at the same time banking process is becoming faster, easier. They are coming with innovative ideas and products. In order to survive in the competitive field of the banking sector, all banking organization are looking for better service opportunities to provide these to their customer.

Origin of the report:

As a mandatory requirement of the Master’s in Business Administration (MBA) program, under Department of Business Administration, The University of Asia Pacific, and the report is entitled “General Banking System & Marketing Activities at EXIM Bank Ltd.” has been prepared. The project for reporting has been selected with consultation of my academic advisor, Jesmin Sultana, Associate Professor of MBA Program, Dept. of Business Administration and the organizational supervisor, Mr. Md. Osman Ali Miah (SAVP), EXIM Bank Ltd.

Background of the Study:

The internship Program of MBA (The University of Asia Pacific) is designed to focus on theoretical and professional development of the student to take them business as a professional as well as service as a career. The program is three-month duration. The internship program provides the opportunity to the students to practice their theoretical knowledge into the practical field. In this purpose, I was assigned to EXIM Bank Ltd. Savar Branch for my practical orientation.

Students are required to prepare an internship report under the guidance of supervising teachers on a selected subject matter to highlighting his experience and to conduct an in-depth analysis on the subject matter. I have tried my level best to present my experience of the practical orientation in this report.

Rational of the study:

I want to work on this topic, for my internship report. The topic of this report is “General Banking System & Marketing Activities at EXIM Bank Ltd.” which is related to the marketing topic. As I have completed my internship in EXIM Bank Limited so this topic helps me how they can civilizing the service of the bank and making changes to suit the customer needs. Bank is the major financial institution in business state. Performance of the bank plays important role in overall countries economic situation. So I would like to inform about the General Banking System& Marketing Activities at EXIM Bank Limited also its performance in General Banking System department.

Objective of the Study:

The Primary Objectives Of The Study Are:

To fulfill the requirement for the completion of (MBA) program. .

To know the current performance of this bank.

Understand the Islamic Sariah Based general banking of Exim Bank Limited, Savar Branch.

Secondary Objectives Of The Study Are:

Understand present an overview of Exim Bank Limited.

To know about General Banking facility provided by Bangladesh bank.

To know about the operational activities of Exim Bank Ltd. Based on Islami Sariah

Scope of the Study:

EXIM Bank is a very well known Bank in the private sector. This report is a model of the Banking service offered by EXIM BANK LIMITED. The scope of this report is limited to the overall explanation of the company, its services, and its place in the market and its marketing strategy. The scope of the study is limited to organizational setup, functions. During three months internship work in the EXIM Bank Ltd. Basically it is the measurement of General Banking System& Marketing Implication on the EXIM Bank and also overall explanation of the Bank, its services, position, marketing strategies, functions, and performances. Determine the level of General Banking System & Marketing Implication regarding General Banking, credit approval, monitoring technique and credit pricing of EXIM Bank Limited.

Every Bank, at branch level provides broadly three types of banking services. Namely: (see the operational definitions part for details)

Methodology of the Study:

Methodology includes direct observation; face-to face discussion with Employees of different departments, study of files, circular etc and practical work. This study includes both quantities and qualitative data. However, this report is basically quantitative in nature. In all the cases depending on the requirements data have been collected from different sources.

Source of Information:

Nature of the study: Conclusive.

Sources of information: Both primary and secondary information sources were used to complete this report.

Primary Data: Primary data were collected by discussion with the employees.

Secondary Data: Secondary information was collected from Annual report and web side of EXIM bank Limited. Various books, journals, manuals, are also followed for the study

Types of research: This is an applied research. The findings of this research help to find the level of General Banking System& Marketing Implication regarding General Banking, Credit Approval and foreign exchange division of EXIM Bank Limited.

Basic research method: A conclusive research is conceded out to describe the research objectives. Two types of research techniques are used. Namely: Secondary Data Analysis. Secondary data sources are consulted like previous reports, publication, different journal and the Internet.

Historical Background and Current Performance

Introduction of the Bank:

Export Import Bank of Bangladesh Limited (EXIM bank) is one of leading private commercial banks in Bangladesh. This Bank came in to operation as scheduled commercial bank on 3rd August 1999 as per rules and regulations of Bangladesh Bank. Of its very beginning EXIM Bank Bangladesh limited was known as BEXIM Bank Limited. But some legal constraints the bank renamed as EXIM Bank, which means Export Import Bank of Bangladesh Limited. At present the bank is performing its work all over the country by 62 Branches. The bank has migrated all of its conventional banking operation into Shariah based Islamic banking since July, 2004. In order to harmonize with the speed and efficiency of the current financial market, they have bought software T-24 supplied by Switzerland based IT company Temenos. They have taken initiatives to set up a wide spread network of ATM Machines throughout the country. EXIM Bank has already launched “EXIM KISHAN” an agricultural product in line with the directive of Central Bank for agricultural investment. Corporate Social responsibility (CSR) is one of the most concerned areas of the Bank. The bank has contributed generously in humanitarian activities as well as social and cultural activities including undertaking scholarship programs. It has also came forward in beautification of Dhaka city, founding foot over-bridges at crowded points of the city and creating income generating welfare schemes.

Historical Background:

Export Import Bank of Bangladesh Limited was established in the year 1999 under the leadership of Late Mr. Shahjahan Kabir, Founder Chairman who had a long dream of floating a commercial bank which would contribute to the socio-economic development of our country. He had a long experience as a good banker. A group of highly qualified and successful entrepreneurs joined their hands with the founder chairman to materialize his dream. Indeed, all of them proved themselves in their respective business as most successful star with their endeavor, intelligence, hard working and talent entrepreneurship. Among them, Mr. Nazrul Islam Mazumder who is an illuminated business icon in the Garments business in Bangladesh became the Honorable Chairman after the demise of the honorable founder chairman. He is also the chairman of Bangladesh Association of Banks (BAB). Under his leadership, BAB has emerged as an effective forum for exchanging views on problems being faced by the banking sector of Bangladesh and for formulating common policy guidelines in addressing such problems.

This Bank starts functioning from 3rd August, 1999 with its name as Bengal Export Import Bank Limited. On 16th November 1999, it was renamed as Export Import Bank of Bangladesh Limited with Mr. Alamgir Kabir as the Founder Advisor and Mr. Mohammad Lakiotullah as the Founder Managing Director respectively. Both of them have long experience in the financial sector of our country. By their pragmatic decision and management directives in the operational activities, this bank has earned a secured and distinctive position in the banking industry in terms of performance, growth, and excellent management. Under the leadership of Mr. Lakiotullah, the Bank has migrated all of its conventional banking operation into Shariah Based Islami Banking in the year July 2004.

In the year 2006, Mr. Kazi Masihur Rahman became the Managing Director of the bank when Mr. Lakiotullah left the bank after completion of his successful 7 years as MD. Mr. Kazi served in the bank for next five years. Under his leadership, the bank has been placed on a state of the art centralized IT platform with two modern data centers where world renowned core banking software TEMENOS T24 is running along with some alternate delivery channels like ATMs and SMS banking.

Vision of EXIM Bank

“Together Towards Tomorrow”

Export Import bank of Bangladesh Limited as the name implies, is not a new type of bank in global but is the first in Bangladesh. It believes in togetherness with its customers, in its march on the road to growth & progress with services. To achieve the desired goal, it has intention to pursuit of excellence at all stages with a climate of continuous improvement. Because it believes, the line of excellence is never ending. It also believes that its strategic plans & business networking will strengthen its competitive edge over in rapidly changing competitive environment. Its personalized quality services to customers with the trend of constant improvement might be cornerstone to achieve its operational success.

Mission of EXIM Bank

The Bank’s mission gives emphasis to:

The bank has chalked out the following objectives in order to ensure smooth achievement of its goals:

|

|

|

|

|

|

|

Corporate Culture

During the last two decades Corporate Culture has become an important theme in business as an intangible concept which clearly plays a meaningful role in corporations, affecting employees and organizational operations. It is not the only determinant of business success or failure, a positive culture can be a significant competitive advantage over organizations with which a firm competes. We, as an amenable bank, believe if the employees identify with the culture, the work environment tends to be more enjoyable, which boosts morale and leads to increased levels of teamwork, sharing of information, and openness to new ideas.

Organogram of EXIM Bank

Shariah Council of the Bank

To guide, monitor and supervise the banking activities complying shariah principle, a learned Shariah Council is working in this bank since inception of its Islami banking branches, which has become more effective after transformation of its operation from traditional to fully Shariah based Islami banking system. The council is consists of 11 members who are prominent ulemas, reputed bankers and eminent economists of the country. Professor Moulana Muhammad Salah Uddin is the Chairman of the council.The Board of Directors has formed a Sharia Supervision Board for the Bank. Their duty is to monitor the entire Bank’s transactional procedures and assuring its Sharia compliancy. The tasks of the Sharia supervisor is summary is replying to queries of the Bank’s administration, staff members, shareholders, depositors and customers, follow up with the Sharia auditors and provide them with guidance, submitting reports and remarks to the Fatwa and Sharia Supervision Board and the administration, participating in the Bank’s training programs, participating in the supervision over the Allqtisad Allslami Magazine and handling the duty of being the General Secretary of the Board.

Objectives of Islami Banking:

- Islami Banking system plays very important role in the Muslim nation. As 90% people of our country are Muslim, the bank wants to compete the market.

- For interest free banking financing arrangements.

- To follow Quran, Sunnah and Shariah Rules.

- Due to profit sharing features of Islami Banking, Banks and entrepreneurs have a shared profit in the outcome of an investment, which fortes economic development.

- To establish equity & justice in the society through the legitimate business & income.

- Try to bring diversity in the investment portfolio in accordance with the need and demand of the time and nature of business by introducing various investment methods & techniques.

- Co- ordinate the economic development with the social development.

Concept of Islamic Banking: The concept of Islamic banking represents a radical departure from traditional banking. Islamic Banking has to derive its inspiration from the religious edicts of Islam and its operations within the framework of the teaching of Islam. The most distinctive feature of Islamic Banking is the prohibition of interest (Riba) in all forms to transaction. Because “Allah” forbid the Riba (interest) but permits trade. The most important verses read as follows “O believes, take not double and redoubled interest and fear God so that you may prosper (Sura 3 [Al-Imran] verse 130). The Islamic banks organize their operations on the basic of profit/ Loss sharing and other modes, which are permitted in Islam.

Islamic banking has been defined in a number of ways: – An Islamic bank is a financial institution whose status rules and procedures expressly state its commitment to the principal of Islamic shariah and to the banning of the receipt and payment of interest on any of its operations.

According to Dr.Shawki Ismail Shehta. “It is there for natural and indeed imperative for an Islamic bank to incorporation in its functions and practices commercial investment and social activities as an institution designed to promote the civilized mission of an Islamic Economy”.

It is clear from the definitions given above that an Islamic bank is not merely a financial intermediary; it involves direct participation in business on the principals of sharing of profit and losses aiming at ensuring social equity and justice.

Important Objectives of Islamic Banking: The important objectives of Islamic banking are:

- Make the best effect to penetrate into the entire society with particular emphasis on low-income groups

- Allocate part of the savings collected in each community to project directly related to the community itself.

- Allocate part of the available funds to the small enterprises and not only to save big business and procedures

- Be aware that when managing its zakat funds the Islamic banks should allocate to overcome part of these funds to securing Qard Hasan(interest free loans). This Qard Hasan Should is directed to opportunities that would serve development, such as creating jobs in order to convert unemployed persons into productive elements within the society or assisting small businesses their financial problems.

- Make effort to turn banking institution as business share institutions from merely loan institutions.

- Try to bring diversity in the investment portfolio in accordance with the need and demand of the time and nature of business by introducing various investment methods & techniques

- Create efficient management engineer through conducting jointly the business Enterprises and production activities.

- Link loans and advances with efficiency based method in Lieu of security oriented. As a result a large number of potential but efficient poor entrepreneurs are able to deploy there service and labor for the productive and innovative activities.

- Establish equity and justice in the society thought the fair distribution of profit Loss Sharing.

- Implement a compulsory ruling of sharia by abolishing the interest mechanism from the banking system.

- Establish priority of labor and production as a source of profit earning and Growth of capital.

- Finance in income generating activities for fulfillment of the basic needs of the poor mass.

- Finance for the balanced development of the country’s agricultural industrial and commerce sectors to help reduce the ill effects of discriminating investment or development narrowed down the gap between the rich and poor and frame and investment plan on micro level basis.

- Discard various types of corruption fraud forgeries misuse or under use of potential recourses and establish strong culture of moral discipline in conformity with the tenets of Islamic Sharia.

- Invest in the country’s potential utilized sector insuring the best uses of the Endowed resources by the God and Coordinate the economic development with the social development.

Features of Islamic Banking: The main features of Islamic banking may be grouped as under

- Prohibition of interest in all forms of transaction.

- Undertaking business and trade activities on the basis of fair and legitimate (Halal) profits.

- Giving Zakat

- Prohibition of monopoly business.

- Investment pattern is designed to promote welfare of the disadvantaged.

Characteristics of Islamic Banking: The distinct characteristics of Islamic Banks may be explained as follows-

- The basis of interest whether it is fixed floating, prepaid, deferred, deducted or in any other form that is strictly prohibited by Islam and Islami base bank follow this.

- The relationship between Islamic banks and their customers is not that of creditor and debtor but one of participation in risks and rewards.

- Unlike conventional bank, which pool capital funds and depositor’s funds, an Islamic bank keeps the two segregated in order not to mix the profit corned on its own fund (capital plus current balances repayment or which is guaranteed) with the profit corned on investor’s funds which are accepted on a profit and loss sharing basis. This enables the banks to calculate the profit due to investors correctly.

- Islamic banks are multipurpose banks since they pay the role of commercial Bank, Investment banks and development banks.

- When Islamic banks employ their resources for production purposes they do not offer cash loans, as is the cash with conventional banks, but operates though participation (Musharaka) / partnership.

- Some other form of Islamic contract, such as Mudaraba, Murabaha, Ijara etc.

While the role of non-Islamic banks is to attract financial resources and lend them so as to make profit, the Islamic banks mobilize financial resources in Order to use them to develop the society as a whole. Profit is no doubt, kept in sight but that is not the sole objective of investment.

Difference between Conventional Financial System (CFS) and Islamic Financial System (IFS):

Conventional Financial System (CFS):

A financial system which is traditionally based and working on Riba or interest principle which is irrelevant of or ignores or separates the religious life of a man from the economic life can be defined as CFS. The conventional financial system is of two types:

1) Socialistic F.S & 2) Capitalistic F.S – both systems have been provide inefficient to establish economic balance in the society.

Islamic financial System (IFS):

A financial system that is based on Islamic principles & values, which eliminates Riba and ensures a profit sharing mechanism in the financial system is called IFS. It may be characterized by the absence of interest bared financial institution & transactions, doubtful transactions or gharry, stock of companies dealing in unlawful activities, unethical or immoral transaction such as market manipulation insider trading, short selling etc.

Islamic banking principles combine a value maximization concept with the principle of justice for the wider welfare of the society. These principles offer a means to create value and elevate the standard of living of people in general through commercial pursuits. However, it is felt that much operational work and in – depth research work has to be undertaken to allow the Sharia Based Islami bank to flourish with highest quality and strength. Exim Bank has launched islami banking system and it is very good news that Exim Bank Ltd. has become more effective after transformation of its operation from traditional to fully Shariah based Islami banking system. All the branches perform their activities according to the Shariah based Islami banking system.

General Banking

Introduction:

Exim Bank General Banking System department does the most important and basic work of the bank. Its other departments are liked with this department. Exim Bank also played a vital role in deposit mobilization of the branch. According to customer demand Exim Bank provides different types of account and special types of saving scheme under general banking. On the basic of customer demand and its proper functioning and excellent customer service this department is divided into various sections namely as below:-

- Accounts Opening Section

- Local Remittance section

- Bills and Clearing Section

- Accounts Section

- Cash Section

Accounts Opening Section:

This section deals with opening of different types of accounts. Account opening department plays a vital role in the operation of banking. Opening of an account binds the banker and the customer into a contractual relationship. It is also deals with issuing of checkbooks and different accounts openers. A customer can open different types of accounts though this department.

Classification of Bank Account

Bank has two types of deposit account, and they are-

A. Operating Account

B. Non-Operating Account

A. Operating Account: This type of account is operated by the account holder of the Bank. There are mainly two types of accounts and they are-

(I) Al-Wadia Current Deposit account (ACD): Current account is an account where numerous transactions can be made by the account holder within the funds available in its credits. Current account is mainly suitable for businessman though nobody is debarred from opening such an account for any purpose. Requirements to open an account are almost same to that of savings account except the initial deposit and the introducer must be the saving or current account holder. Some important points are as follows-

- Minimum opening deposit of Tk.3000/= is required.

- There is no withdrawal limit.

- No interest is given upon the deposited money.

- Minimum Tk.3000/= balance must be always maintain all the time.

Local Remittance Section: Carrying cash money is troublesome and risky. That’s why money can be transferred from one place to another through banking channel. This is called remittance. Remittances of funds are one of the most important aspects of the commercial banks in rendering services to its customers.

Types of remittance:

- Between banks and non banks customer

- Between banks in the same country

- Between banks and central bank in the same country

- Between central bank of different customers.

The main ways used by Exim Bank for remitting funds are:

- 1. Payment order (PO)

- 2. Demand Draft (DD)

- 3. Telegraphic Transfer (TT)

4.4.1. Pay Order (PO): This is an instrument issued by the branch of a bank for enabling the customer/ purchaser to pay certain amount of money to the order of a certain person/ firm/ organization/ department/office within the same clearinghouse area of the pay order-issuing branch. The issuing branch and the paying branch are same.

Procedure of P.O. issue:-

- Obtain PO application form duly filled in and signed by the applicant.

- Receive the amount in cash/transfer with commission amount.

- Issues pay order.

- Enter in pay order register.

Commission for PO: Exim Bank charges different amount of commission on the basis of payment order amount. The bank charges for pay order are given in the following chart:

Commission & VAT for PO

Total amount of PO | Commission | VAT |

Up to Tk. 10,000.00 | Tk. 25.00 | Tk. 4 |

Tk. 10,001.00 to Tk.100,000.00 | Tk. 60.00 | Tk. 9 |

Tk. 1,00,001.00 to | Tk. 120.00 | Tk. 18 |

| above |

Demand Draft (DD): This is an instrument through which customers money is remitted to another person /firm /organization in outstation from a branch of one bank to another outstation branch of the same bank or to a branch of another bank (with prior arrangement between that bank with the issuing bank). On the way by which the issuing branch gives instruction to the payee/ drawer branch to pay certain amount of money to the order of certain person/firm/ organization.

Issuing procedure of D.D:

a) Obtain demand draft application form duly filled in and signed by the purchaser /applicant.

b) Receive the amount in case/ transfer with prescribed commission and postage amount.

c) Insert test number.

d) Enter in the D.D. register.

e) Issue advice to the payee branch.

Payment procedure of D.D:-

a) Examine generally of the D.D. viz. Amount, verify signature, test, series, etc.

b) Enter in the DD payable register.

c) Verify with the ICBA /test etc.

d) Pass necessary vouchers.

Clearing Section: Cheques, Pay Order (P.O.), Demand Draft (D.D.) collection of amount of other banks on behalf of its customer are a basic function of a Clearing Department.

Clearing: Clearing is a system by which a bank can collect customers fund from one bank to another through clearing house. Clearing House is a place where the representatives of all member banks meet together and settle mutual obligations of banks arising out of cheques & other instruments drawn on one bank and deposited with another bank for collection, under a special arrangement. The characteristic of the clearing house is that at the time of coming to this place the representative of many bank brings with him all cheques etc drawn on other banks along with schedules and delivers the cheques to the clearing house and receives cheques etc drawn on his bank and on the basis of cheques etc. delivered & received the mutual obligations between banks is ascertained and settled through their respective bank accounts maintained with the Central Bank or any other bank which conducts the clearing house.

Member of Clearing House: EXIM Bank of Bangladesh Limited is a scheduled bank. According to the article 37(2) of Bangladesh Bank order, 1972, the banks which are the member of the clearing house, called as Scheduled Banks. The scheduled Banks clear the cheque drawn upon one another through the clearing house.

Types of clearing:

Outward Clearing: When the Branches of the Bank receive cheque from its customers drawn on the other Banks within the local clearing zone for collection through Clearing House, it is Outward Clearing. Outward Clearing Procedure:-

- Receipt of instrument with paying in slip.

- Checking of instrument & paying in slip.

- Affixing of seal

- Special Crossing seal.

- Clearing Seal (Instrument & Paying in slip)

- Endorsement Seal with signature.

- Singing of counterfoil and returning it with seal to the depositor.

- Separation of instrument from paying in slip.

- Sorting of instrument bank wise and branch wise.

- Preparation of schedule- branch wise.

- Preparation Bank wise schedule.

- Preparation of clearing House sheet.

- Making of entries in Clearing Register (Outward)

- Preparation of vouchers.

- Sending of instruments to main branch with schedule.

- Collection of credit advice from Main Branch.

Inward clearing: When the Banks receive cheque drawn on them from other Banks in the Clearing House, it is Inward Clearing. Inward Clearing Procedure:-

- Receipt of instruments with schedule.

- Checking of instruments.

- Sending of instruments to different Departments/Sections for posting

- Preparation of Vouchers and sending of credit advice to main branch.

Accounts Section:

Account department is called the nerve Center of the bank. In banking business, transactions are done every day and these transactions are to be recorded properly and systematically as the banks deal with the depositors’ money. Improper recording transactions will lead to the mismatch in the debit side and in the credit side. To avoid these mishaps, the bank provides a separate department; whose function is to check the mistakes in passing vouchers or wrong entries of fraud or forgery. This department is called as Accounts Department. If any discrepancy arises regarding any transaction this department report to the concerned department.

Workings of this department

- Recording the transactions in the cashbook

- Recording the transactions in general and subsidiary ledger

- Preparing the daily position of the branch comprising of deposit and cash.

- Preparing the daily Statement and Affairs showing all the assets and liability of the branch as per General ledger and Subsidiary ledger separately.

- Preparing the monthly salary statements for the employees.

- Preparing the weekly position for the branch which is sent to the Head Office to maintain Cash Reserve Requirement (CRR).

- Preparing the weekly position for the branch which is sent to the Head Office to maintain Statutory Liquidity Requirement (SLR).

- Preparing the budget for the branch by fixing the target regarding profit and deposit so as to take necessary steps to generate and mobilize deposit.

- Recording of the vouchers in the Voucher register.

Cash Section:

Banks as a financial institution, accept surplus money from the people as deposit and given them opportunity to withdraw the same by cheque, etc. but among the banking activities, cash department plays an important role. It does the main function of a commercial bank i.e. receiving the deposit and paying the cash on demand. As this department deals directly with the customer, the reputation of the bank depends much on it. The functions of a cash department are described below:

Function of cash Department

| Cash Payment |

|

| Cash Receipt |

|

Cash packing:-After the banking hour cash is packed according to the denomination. Notes are counted and packed in bundles and stamps with initial.

Allocation of Currency:-Before starting the banking hour all tellers gave requisition of money though “Teller cash proof Sheet”. The head teller writes the number of the packet denomination with in “Reserve Sheet” at the end of the day; all the notes remained are recorded in the sheet.

Passing the check:

After verifying the above – mentioned things the officer passes it to the computer section for more verification. After that it is passed to the officer to make payment. By putting “seal the cash officer make it clear to pay. The cash officer gives the cash amount to the holder and record in the cash paid register.

Deposit Section: The function of the deposit section is very important. It is fully computerized. The officer of the deposit section maintains account number of all the customer of the bank. They are used different code number for different account. By this section a depositor/drawer can know what the present position is if his/her account. From the history and origin of the banking system we know that deposit collection is the main function of the bank.

Accepting deposits: The deposits that are accepted by EXIM bank of Bangladesh Limited like other banks may be classified in to,

a) Demand deposits

b) Time Deposits

Demand deposits: These deposits are withdrawn able without notice, e.g. current deposits. EXIM Bank of Bangladesh Limited Accepts demand deposits through the opening of:

a) Current account

b) Savings Account

Time deposits: A deposits which is payable at a fixed date or after a period of notice is a time deposit. EXIM bank of Bangladesh Limited accepts time deposits through Fixed Deposit Receipt (FDR), Short Term Deposit (STD). While accepting these deposits, a contract is done between the bank and the customer. When the banker opens an account in the name of a customer, there arise contracts between the two. This contract will be valid one only when both the parties are competent to enter into contracts. As account opening initiates the fundamental relationship& since the banker has to deal with different kinds of person with different legal status, EXIM Bank of Bangladesh Limited official remain very much careful about the competency of the customers. The Local Remittance section of EXIM bank of Bangladesh of Bangladesh Limited is also issues FDR. They are also known as time deposit of time liabilities.

Financial Highlights Amount in million Tk.

| Sl. | Particulars | 2008 | 2009 | 2010 | 2011 | 2012 |

| 01. | Authorized Capital | 3500 | 3500 | 3500 | 10000 | 10000 |

| 02. | Paid-up Capital | 1713.76 | 2142.2 | 2677.75 | 3373.96 | 6832.27 |

| 03. | Statutory Reserve | 810.88 | 1134.64 | 1532.55 | 2092.97 | 3154.76 |

| 04. | Deposits | 35032 | 41546.57 | 57586.99 | 73835.46 | 94949.40 |

| 05. | Investment (General) | 32641.27 | 40195.24 | 53637.68 | 68609.91 | 93296.65 |

| 06. | Investment (Shares on Securities) | 2233.25 | 2457.72 | 2894.02 | 2189.54 | 6012.86 |

| 07. | Foreign Exchange Business | 96175.1 | 117900.14 | 156434.57 | 162604.61 | 227966.60 |

| a) Import Business | 49596.7 | 61399.4 | 78540.49 | 83911.51 | 129570.73 | |

| b) Export Business | 46234.6 | 55790.42 | 76465.62 | 76240.77 | 95359.45 | |

| c) Remittance | 343.8 | 710.32 | 1428.46 | 2452.33 | 3036.42 | |

| 08. | Net Profit after Tax | 650.29 | 930.84 | 1096.63 | 1694.1 | 3476.01 |

| 09. | Investment as a % of total Deposit | 93.18% | 96.75% | 93.14% | 92.92% | 98.26% |

| 10. | No. of Foreign Correspondent | 246 | 256 | 278 | 333 | 354 |

| 11. | Number of Employees | 1020 | 1104 | 1312 | 1440 | 1724 |

| 12. | Number of Branches | 30 | 35 | 42 | 52 | 62 |

| 13. | Return on Assets after tax (ROA) | 1.73% | 2.00% | 1.83% | 2.19% | 3.54% |

Financial overview of the EXIM Bank:

The performance of the bank was very significant both in terms of development and achievement in the year of 2012. As at 31 December 2012, total asset and liability of the bank were Tk. 113070.98 million and Tk. 100596.13 million respectively as against Tk. 83329.34 million and Tk. 76612.13 million respectively as on 31 December 2011. In 2012, the bank successfully mobilized Tk. 94949.40 million of deposits through its 62 branches and disbursed investment of Tk. 93296.65 million against deposit of Tk. 73835.46 million and investment of Tk. 68609.91 million respectively in 2011. In 2012, the bank earned operating profit of Tk. 5893.79 million with and annual growth of 85.23% comparing of Tk. 3181.78 million in 2011. The return on assets (ROA) after tax was 3.54% for the year 2012 which was 2.19% in previous year.

Capital and reserve fund:

While inception in 1999, the banks Authorized Capital was Tk. 1000 million and paid up capital was Tk. 225 million subscribed by the sponsors. Its authorized capital was enhanced to Tk. 3500 million in the year 2008. Banks authorized capital was further augmented to Tk. 10000 million in 2011. In the year 2012 Bank changed the denomination of share from Tk. 100 to Tk. 10 as well as the market lot from 50-100 shares and raised Tk. 6832.27 million as paid up capital.

Deposit:

Deposit is the principal source of fund invested to generate revenue in banking business. The total deposit of the bank stood at Tk. 94949.40 million as on 31 December 2012 against Tk. 73835.46 million of the previous year with an increase of Tk. 21113.94 million at a growth rate of 28.60%. The main strategy for increasing deposit base is maintaining competitive rates of profit and providing satisfactory services to the customers.

Investment (General):

Total investment of the bank was Tk. 93296.65 million as on 31 December 2012 against Tk. 68609.91 million as on 31 December 2011 showing an increase of Tk. 24686.74 million with a growth rate of 35.98% the bank performs appropriate investment risk analysis while approving investments to customers in order to maintain quality of assets.

Import business:

In the year 2012 bank handled BDT 129570.73 million against import business through 39855 letters of credits which is 54.41% higher from the previous year.

Export business:

Export business of the bank stood at BDT 95359.45 million in 2012 by handling 37096 numbers of documents with a growth of 25.08% in comparison with the previous year.

Foreign remittance:

Bank grasped BDT 3036.42 million remittances in the last year. It was BDT 2452.33 million in 2011 which means the growth rate on 2012 is 23.82%

Performance of All Branch of EXIM Bank Ltd: Amount in Crore Taka

Profit Earned In 2012 Compared With 2011 | ||||

| Branch Name | Profit in 2011 | Profit in 2012 | Increase/Decrease | Increase/Decrease % |

| 1.MotiJheel | 111.94 | 120.24 | 8.30 | 7.41% |

| 2.Panthapath | 19.23 | 17.65 | -1.58 | -8.20% |

| 3.Agrabad | 36.95 | 43.17 | 6.22 | 16.83% |

| 4.Khatungonj | 25.56 | 32.85 | 7.29 | 28.50% |

| 5.Gazupur | 2.84 | 4.85 | 2.01 | 70.91% |

| 6.Imamgong | 11.98 | 11.20 | -.79 | -6.59% |

| 7.Gulshan Branch | 95.24 | 108.18 | 12.95 | 13.59% |

| 8.Sonamuri | 2.35 | 5.30 | 2.95 | 125.26% |

| 9.Sylhet Branch | 3.70 | 5.21 | 1.51 | 40.97% |

| 10.Nawabpur | -4.43 | -2.11 | 2.32 | -52.31% |

| 11.Nrayangonj | 21.40 | 27.12 | 5.72 | 26.71% |

| 12.Shimrail | 3.26 | 4.38 | 1.11 | 34.15% |

| 13.Rajuk Avenue | 34.37 | 28.46 | -5.91 | -17.20% |

| 14.New Eskaton | 5.17 | 8.19 | 3.02 | 58.36% |

| 15.Uttara Branch | 27.85 | 30.20 | 2.34 | 8.42% |

| 16.Laksham | 1.95 | 4.12 | 2.18 | 111.88% |

| 17.Mirpur Branch | 8.17 | 9.70 | 1.53 | 18.78% |

| 18.Jubilee Road | 7.52 | 9.37 | 1.85 | 24.55% |

| 19.Elephant Road | 12.31 | 9.27 | -3.04 | -24.66% |

| 20.Mawna Chowrata | 3.96 | 5.21 | 1.25 | 31.65% |

| 21.Bogra Branch | 4.28 | 2.72 | -1.57 | -36.63% |

| 22.Jessore Branch | 2.30 | 2.94 | .65 | 28.10% |

| 23.Malibag | 3.25 | 5.11 | 1.85 | 56.98% |

| 24.Ashulia | 2.71 | 3.03 | .32 | 11.91% |

| 25.Ashuganj | 1.13 | 2.03 | .90 | 79.23% |

| 26.CDA Avenue | 4.80 | 6.07 | 1.28 | 26.65% |

| 27.Chowmuhani | .38 | 1.15 | .77 | 202.17% |

| 28.Satmasjid Branch | 9.34 | 10.26 | .92 | 9.87% |

| 29.Bashundhara | 4.08 | 3.35 | -.73 | -17.90% |

| 30.Fenchuganj | .89 | 1.87 | .98 | 110.71% |

| 31.Comilla Branch | 1.76 | 1.92 | .16 | 9.13% |

| 32.Savar Branch | 1.68 | 2.15 | .47 | 28% |

| 33.Molvibazar | .58 | .22 | -.36 | -62.10% |

| 34.Rangpur Branch | .90 | 1.01 | .11 | 11.91% |

| 35.Karwan Bazar | 9.14 | 11.98 | 2.84 | 31.10% |

| 36.Modaforgonj | .08 | .60 | .53 | 696.00% |

| 37.Kustia Branch | 1.32 | .56 | -.76 | -57.79% |

| 38.Rajshahi | .32 | .59 | .28 | 86.88% |

| 39.Head Office | 20.42 | 20.38 | -.03 | -0.16% |

| 40.Golapgonj | .68 | 1.08 | .40 | 57.99% |

| 41.Chhagalnaiya | .10 | .35 | .25 | 264.05% |

| 42.Naria Branch | -.22 | .08 | .29 | -135.11% |

| 43.Khulna Branch | -.26 | .06 | .32 | -121.42% |

| 44.Pahartoli | .78 | 1.09 | .30 | 38.71% |

| 45.Palton Branch | 1.59 | 2.14 | .55 | 34.71% |

| 46.Board Bazar | .39 | 2.70 | 2.31 | 588.08% |

| 47.Bahadarhat | -.06 | 1.07 | 1.13 | -1807.66% |

| 48.Shitakundo | -.22 | .06 | .28 | -127.09% |

| 49.Faridpur | -.44 | .02 | .45 | -103.44% |

| 50.Barishal | -.88 | -..74 | .14 | -15.97% |

| 51.Biani bazaar | -.19 | .29 | .48 | -252.77% |

| 52.Nobigonj | -.31 | -.12 | .20 | -62.14% |

| 53.Panchoboti | -.46 | -.28 | .17 | -37.96% |

| 54.Feni Branch | -.54 | -.40 | .13 | -24.59% |

| 55.Dinajpur | -.67 | .21 | .88 | -131.17% |

| 56.Keranigonj | -.22 | -.31 | -.09 | 40.97% |

| 57.Bishwanath | -.13 | -.55 | -.42 | 315.24% |

| 58.Goala Bazaar | -.13 | -.53 | -.41 | 322.22% |

| 59.Thakur Bazaar | -.05 | -.62 | -.57 | 1133.36% |

| 60.Sonargoan | 00 | -.34 | -.34 | 00% |

| 61.Banani Branch | 00 | -1.43 | -.1.43 | 00% |

| 62.Basurhat Branch | 00 | -.08 | -.08 | 00% |

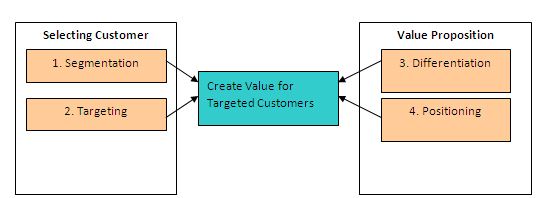

Customer-Driven Marketing Strategy by EXIM Bank Ltd.: EXIM Bank Ltd. has some strategy or techniques to get desired customer base. EXIM Bank can’t serve all people of our country because of its capacity limitation. So EXIM Bank divides the market into meaningful customer groups (segmentation), Choose a specific groups to serve (Targeting), and then differentiate its offering to attract customer attention.

Segmentation Strategy of EXIM Bank Ltd: EXIM Bank Ltd. has divided the market into different segment which are given here:

By Region: Whole country is divided into seven region or Division.

By Religion: Population of our country is comprised of different religion such as Muslim, Hindus, and Christian & Buddhist etc

By Occupation: Professional, Technical, Businessmen, Farmers, Housewives, and Students etc.

Social Class: Lower lowers, upper lowers, Working class, Middle class, Upper middle class, Upper uppers etc.

2. Targeting Strategy of EXIM Bank Ltd: EXIM Bank Ltd. follows both undifferentiated & differentiated marketing strategy for targeting their whole market. EXIM Bank Ltd. targets whole market, it offers same services to all class people of the society, people from any status, religion, and area can get the services of EXIM Bank Ltd. It offers convenient services like, Deposit, Investment and Foreign exchange products/services to its customer through 62 Branches. It also follow the differentiated marketing strategy by providing or offering some special product/service scheme to a particular segment of customers, like Agricultural loan only for the farmer, Student Account & Student loan, Hazz deposit scheme only for the Muslim customer etc.

3. Differentiation: The main differentiation is that although EXIM Bank Ltd. is Export Import based schedule commercial bank but at the same time it also a shariah Based Islami Bank. Such as, it offers the customer interest (Riba) free banking service. Interest is strictly prohibited in Islam. So religious minded Muslims always prefer islami Bank. EXIM Bank Ltd invests in the productive sector. Bank works as a partner with its clients.

4. Market Positioning Strategy: EXIM Bank Ltd. is the first Export Import based Commercial Bank in Bangladesh. And they positioned their bank as Islami Shariah based schedule commercial bank. As it is an Islami Shariah based bank so the People who are Muslim have faith in EXIM Bank services. EXIM Bank Ltd. believes in togetherness with its customers, in its march on the road to growth & progress with services. To achieve the desired goal, it has intention to pursuit of excellence at all stages with a climate of continuous improvement. So, the Customer will motivate to its philosophy & be loyal to its services.

Integrated Marketing Communications (Promotion Mix) used by the EXIM Bank Ltd: Marketing communications focus on immediate awareness, image, or preference goals in the target market. But today marketers are moving toward viewing communications as managing the customer relationship overtime. In banking industry relationship is based on trust. Clients always seek security and safety as well as swift service. EXIM Bank Ltd. provides banking services to its client. Target customers are the people of all class of our society. EXIM Bank Ltd. emphasize mostly on social welfare as well as on its business performance. General Banking System& Marketing Implications their motto. So customers spread positive word of mouth. Besides this they promote their services through different media, such as:

Advertisement:

- Television Advertising (New Branch Opening).

- Newspaper Ads (New Branch Opening & Special Offers).

- Magazine & Journals.

- Billboard.

- Calendar & Note Books.

- Prospectus.

- Annual Report. Etc

Advertisement Provided On:

1. Television Advertising: EXIM Bank Ltd. informs its target customers through television ads especially when a New Branch is likely to open. Television Ads help people to know the location and date of commencing banking services in their localities.

2. Newspaper Advertising: Bank publishes advertisement of launching a branch and other special offers in different Daily Newspaper. It is needed to inform the customer about new services such as ATM booth location, Xpress money service, Address change of a Branch, Consumer banking, Household durables services etc. Newspaper ads are the most effective media for these services.

Different National Dailies chosen for ads are:

- The Daily Prothom Alo

- The Daily Naya Diganta

- The Daily Amar Desh

- The Daily Sangram

- The Daily star

- The Bangladesh Observer etc.

3. Magazine & Journals: Advertisement of consumer banking such as household durables schemes, Special scheme for medical instrument, office furniture, computer, car investment scheme and other services offered by the bank is published through this media.

4. Billboards: EXIM Bank Ltd. doesn’t use the billboard but Digital and plastic signboard of different branches also a kind of advertising. ATM Booth located in different areas of the cities represent the bank’s logo.

5. Calendar & Note Books: Bank publishes wall calendar, desk calendar, diary, note books and provides to its clients and different parties. Calendars of EXIM Bank Ltd. is composed of Calligraphy, Historical location of Islam which motivates people to the Islam.

6. Prospectus & Annual Report: EXIM Bank Ltd. publishes prospectus to collect shareholders and bondholders. Annual report is published for the purpose of declaring dividend, equity and asset of the bank. Annual report must be submitted parties like Bangladesh Bank, Shareholders, different research firms and interested groups.

SWOT Analysis: SWOT Analysis is the detailed study of an organization’s exposure and potential in the perspective of its strength, weakness, opportunity and threat. These facilities of the organization help to make their existing line of performance and also forecast the future to improve their performance in comparison to their competitors. As through these tools, an organization can also study its current position, it can also be considered as an important tool for making changes in the strategic management of the organization.

Strengths:

- a. EXIM Bank of Bangladesh Limited has already established a favorable reputation in the banking industry of the country. It is one of the leading private sector commercial banks in Bangladesh. The bank has already shown a tremendous growth in the profit and deposits sector.

- EXIM Bank of Bangladesh Limited has provided its banking service with top leadership and management position. The upper management of Exim bank is highly skilled and qualified. The board of Directors headed by its chairman Mr. Md. Nazrul Islam is skilled person in business world. Alamgir Kabir, the advisor of the bank is reputed senior chartered accountant having 30 years vast experience in accounts, audit, finance and banking at and abroad. Mr. Md. Fariduddin Ahmed, as the MD of the bank management team. The top management officials have all worked in reputed banks and their years of banking experience, skill and expertise will continue to contribute towards further expansion of the bank.

- EXIM Bank of Bangladesh Limited has already achieved a high growth rate accompanied by an impressive profit growth rate in 2012. The number of deposits and the loans and advances are also increasing rapidly.

- EXIM bank has an interactive corporate culture. The working environment is very friendly, interactive and informal and there are no hidden barriers while communicate between the superior and the employees. This corporate culture provides as a great motivation factor among the employees.

- Their deposit base is very strong and they have strong Financial Resources.

- As Islamic Shariah Based bank EXIM bank of Bangladesh Limited has a prominent Shariah Council and they can provide different types of Islamic banking products.

- Their leadership is good as well as they have top management level team.

Weakness:

- a. ATM BOOTH service of EXIM Bank Limited is not good still at now because Bank has only 37 ATM booths all over the country. An internal survey conduct at Savar shows that only 18% customers are satisfied with their ATM services.

- b. As EXIM Bank Limited is a Shariah based Islami Bank so there is lack of aggressive advertising in TV, Magazine etc.

- c. The service quality of EXIM Bank Limited is good & higher than Prime Bank, Dhaka bank or Dutch Bangla Bank or any govt. Bank, but this service quality is not sufficient for the bank to compete with the multinational Bank located in our country like, HSBC bank, Standard Chartered Bank etc.

- d. High reliance on Head Office, as the Branch actually doesn’t have any autonomy. So, very often it is found that prompt decision making is hampered when necessary.

- e. Some of the job in EXIM Bank of Bangladesh Limited has no growth or advancement path. So lack of motivation exists in persons filling those positions. This is a weakness of EXIM Bank of Bangladesh Limited that it is having a group of unsatisfied employees.

- f. The main important thing is that the bank has no clear mission statement and strategic plan. The banks not have any long-term strategies of whether it wants to focus on retail banking or become a corporate bank because they practice both of these. The path of the future should be determined now with strong feasible strategic plan.

- g. In terms of promotional activities, EXIM Bank of Bangladesh Limited has to more emphasize on that because an internal survey conduct at Savar shows that only 27% customers are fully satisfied the bank promotional activities. Bank need to follow aggressive marketing campaign.

Opportunity:

- a. In order to reduce the business risk, EXIM Bank has to expand their business portfolio. The management can consider option of starting merchant banking or diversify into leasing and insurance sector.

- b. Opportunity in retail banking lies in the fact that country’s increased population is gradually learning to adopt consumer finance. The bulk of our population is middle class. Different types of retail lending products have great appeal to this class. A wide variety of retail lending products has very large market. EXIM Bank Limited already practices the retail banking and it is a opportunity to this bank.

- c. A large number of private banks coming into the market in the recent time. In this competitive environment EXIM Bank of Bangladesh Limited must expand its product line to enhance its sustainable competitive advantages. In that product line, they can introduce variety of credit card and debit card system for their potential customer and Bank need to increase it ATM booth quantity.

- d. In addition of those think, EXIM Bank of Bangladesh Limited can introduce special corporate scheme for the corporate customer or officer who have an income level higher from the service holder. At the same time, they can introduce scheme or loan for various service holder and the scheme should be separate according to the professions, such as engineers, Lawyers and doctors etc.

- e. As EXIM Bank Limited is Export Import and Islami Shariah based Bank and 90% population of our country is Muslim so there is large market for this bank to target their customer because Muslim people will prefer the Shariah based Bank.

Threats:

- All sustain multinational banks and upcoming foreign, private banks create enormous threats to Exim Bank Limited. If that happens the intensity of competition will rise further and banks will have to develop strategies to compete against the foreign banks.

- The depreciation of Taka against US dollar rate is a great threat to foreign exchange transaction and profitability for EXIM Bank of Bangladesh Limited.

- c. The default risks all terms of loan have to be minimizing in order to sustain in the financial market. Because default risk leads the organization towards to bankrupt. EXIM Bank of Bangladesh Limited has to remain vigilant about this problem so that proactive strategies are taken to minimize this problem if not elimination.

Recommendations:

- Their ATM BOOTH is not available everywhere. So the bank needs to increase their ATM BOOTH in different places of their branch operational area.

- Bank need to do aggressive marketing activities to make popular their Visa Islamic Card and also to attract the customer.

- The Bank should reduce the profit rate on loans product and keep it reasonable. Because 19% profit rare is comparatively high and customer notice about this.

- As it is Export Import based commercial schedule bank so, it is very essential that all branches must have AD service because some customer notice that they face problem for not availability of this service and need to depend on the support of Head Office.

- Bank must need to increase their promotional activities to promote their products and services.

- The bank should introduce new products to the market by doing proper research and development. Consumers are not getting the suitable loan for their own purpose. They should emphasis on proper research and development of proper products according to the driven market consumer preference.

Conclusions:

Lots of new commercial banks have established in last few years and the bank has made these banking sectors very competitive. So, banks have to organize their operation and do their operations according to their need of market. We moved a long way from the time when the banks were only deposit taking and money lending institution. Modern banking is an outcome development driven by changing financial activities and lifestyle. Bangladesh has not lagged behind. Banks are required to participate in the nation building activities and act as agent for banking about socioeconomic changes.

It is a great pleasure for me to have practical experience to EXIM Bank Limited, Savar Branch. Without practical knowledge, it is not possible for me to compare the academic knowledge & practical knowledge. Since the time is very limited to learn the all the sectors of a Bank. If the duration of internship can be increased, then it is possible to learn all the Banking activities more properly.

To compete in the environment of advancing technology and faster communication the EXIM Bank Limited should depend more heavily on the quality service and information technology. EXIM Bank Limited should be connected through wide area network. So that all the informational and service can be accessed from any branch of the world.

No doubt about it that EXIM Bank Limited achieves superior position in our Banking industry but to cope with customer EXIM Bank Limited should think how to make its service proactive. To compete with other Banks operation in Bangladesh, EXIM Bank Limited should introduce easier way for faster processing of credit analysis.

Overall customers are satisfied about the services provided by Exim bank Ltd. To capture whole market they need do more market research to develop and improve the products and services that will meet the expectations of near 100% customers.

As a leading new generation Bank EXIM Bank Limited is contributing significantly to the economy of Bangladesh with a promising future. I can hope that EXIM Bank Limited will be able to spread their business with increasing various schemes & other utility services.