Methods for Accounting Treatment of Containers

Accounting for containers is very important if you pack your product in containers before selling it to your consumers. Every businessman wants to maximize his profits. For this, he wants to increase his sales. Containers play an important role in increasing sales. It is to determine profit or loss from the container. Goods are very often packed into bottles, boxes, bags, cans, drums, etc. for the purpose of preserving, transporting and marketing. These packing materials, which are called packages, containers or empties, are durable as well, as reusable.

To calculate the cost of packaging and to record is very necessary. For accounting purposes, the containers can be divided into two types: (a) Non-returnable containers and (b) Returnable containers.

(a) Non-returnable Containers

The accounting for non-returnable containers can be exercised under the following two conditions:

- When a separate charge is made

- When a separate charge is not made

(i) When a separate charge is made

A separate charge for containers could be made even though the containers are non-returnable. If the cost of packages is not included in the sale price, the cost is charged from customers separately in addition to the price of the goods sold. To record such transactions, a container account is opened debiting opening stock of containers, purchases and credited with the amount charged to customers and closing stock of containers. In this case, the Package Account is opened. The separate charge made to the customer is recorded in Sales Day Book in a separate column. This Account is debited with an opening stock of containers and purchases. Since the separate charge made to customers for the containers is higher than the cost of the containers, the container stock account will, therefore, shows the profit or loss on the containers for the period. It is credited with the amount charged to customers and closing stock.

(ii) When no separate charge is made

Some packages are such which cannot be returned by the customers. For instance, toothpaste, scent, oil, etc. Therefore, the manufacturer or seller includes the cost of such containers in the selling price of the goods. Their remaining with the products is essential. Hence, in this case, a container stock account is opened debiting opening stock of empties, purchases and credited with closing stock. The difference between the debit total of container stock account with the credit total is the cost of containers consumed. In certain cases, some cases or packages, if returned, cannot be used again. The cost of containers consumed could be transferred to profit and loss account as distribution expenses or charged to trading or manufacturing accounts.

(b) Returnable Containers

When containers are returnable, there are two alternatives for accounting treatment:

- When no separate charge is made

- When a separate charge is made

(i) When no separate charge is made

In this case, no separate charge is made for the packages or containers. The packages, tins, boxes, bottles, etc. are necessary for packaging goods. While selling such types of well-packed goods, a provision could be made with the customers for the returns of such types of containers. The provision of repair and maintenance is also necessary to make the container moveable regularly. When no separate charge is made even for the returnable container, it is being expected that the customer will return the container within a specified period. If the customer returns the containers on time his account will be credited with the value less than the original cost of the container. This is carried out for maintaining the provision of depreciation.

(ii) When a separate charge is made

Under this method, returnable containers are considered to be special items for trading account. When a separate charge is made for the returnable container, there are various methods to deal with the situation. The price of the containers is charged separately to customers. But widely used methods are as follows:

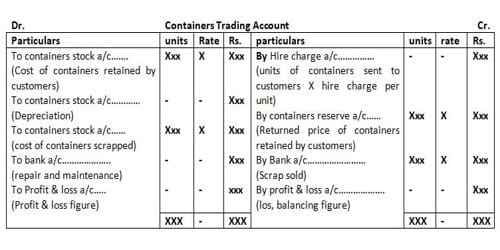

(1) With opening containers stock and trading account

- Containers stock account

- Containers trading and profit and loss account

- Containers reserve/suspense/deposit account

(2) Without opening containers stock account separately

- Containers trading and profit and loss account

- Containers reserve/suspense/provision account.

Information Source: