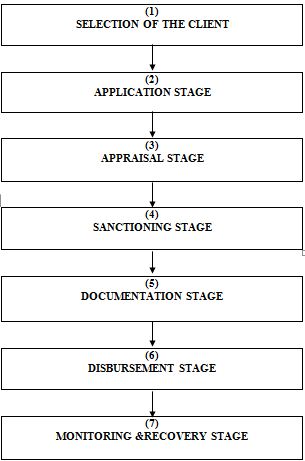

Generally a bank takes certain steps to deliver its proposed investment to the client. But the process takes deep analysis. Because banks invest depositors fund, not banks’ own fund. If the bank fails to meet depositors demand, then it must collapse. So, each bank should take strong concentration on investment proposal. However, IBBL, Mirpur-10 Branch makes its investment decision through successfully passing the following crucial steps:

(1) Selection of the client

Here, investment taker (client) approaches to IBBL, Mirpur-10 Branch. Then, he talks with the manager or respective officer (Investment). Secondly, bank considers five C’s of the client. After successful completion of the discussion between the client and the bank, bank selects the client for its proposed investment. It is to be noted that the client/customer must agree with the bank’s rules & regulations before availing investment. Generally, bank analyses the following five C’s of the client:

- Character;

- Capacity;

- Capital;

- Collateral; and

(2) Application stage

At this stage, the bank will collect necessary information about the prospective client. For this reason, bank informs the prospective client to provide and/or fill duly respective information which is crucial for the initiation of investment proposal. Generally, here, all the required documents for taking investment have to prepare by the client himself. Documents that are necessary for getting investment of IBBL, Mirpur-10 Branch are prescribed below:

- Trade License photocopy (for proprietorship);

- Abridged pro forma income statement;

- Attested copy of partnership deed (for partnership business);

- Prior three (03) years’ audited balance sheet (for joint stock company);

- Prior three (03) years’ business transactions statement for the musharaka/mudaraba investment;

- Abridged pro forma income statement for the musharaka/mudaraba investment;

- Attested copy of the Memorandum of Association (MOA) & Articles of Association (AOA) for the joint stock company;

- Attested copy of the Tax Identification Number (TIN)- including final assessment;

- Tenders of the proposed assets (in case of HPSM);

- Detailed summary of the sundry debtors and creditors (including both time & schedule);

- Summary of the personal movable & immovable assets; and others.

(3) Appraisal stage

At this stage, the bank evaluates the client and his/her business. It is the most important stage. Because, on the basis of this stage, bank usually goes for sanctioning the proposed investment limit/proposal. If anything goes wrong here, the bank suddenly stops to make payment of investment.

(Appraisal Report) to the client for gathering all the information. The original copy of the appraisal report is enclosed in the appendix chapter. However, the following contents are presented from that appraisal report:

- Company’s/Client’s Information.

- Owner’s Information.

- List of Partners/Directors.

- Purpose of Investment/Facilities.

- Details of Proposed Facilities/Investment.

- Break up of Present Outstanding.

- Other Liabilities of the Client/Group.

- Previous Banker’s Information.

- Details of Sister/Allied Concerns.

- Allied Deposit as on.

- Business/Industry Analysis.

- Relationship Analysis.

- Asset-Liability position of the client as per Audited Balance Sheet.

- Working Capital Assessment.

- Risk Grade.

- Particulars of the goodown for storing MPI/Murabaha goods.

- Insurance Coverage.

- Audit Observation.

- Security Analysis.

(4) Sanctioning stage

At this stage, the bank officially approves the investment proposal of the respective client. In this case client receives bank’s sanction letter. IBBL, Mirpur-10 Branch sanction letter contains the following elements:

- Investment Limit in million.

- Mode & amount of investment.

- Purpose of investment.

- Period of investment.

- Rate of return.

- Securities

(5) Documentation stage

At this stage, usually the bank analyses whether required documents are in order. In the documentation stage, IBBL, Mirpur-10 Branch checks the following documents of the client:

- Tax Payment Certificate.

- Stock Report.

Trade License (renewal).

- VAT certificate

- Liability statement from different parties.

- Receivable from different clients.

- Other assets statement.

- Aungykar Nama.

- Ghosona Potra.

- Three (03) years net income & business transactions.

- Performance report with the bank.

- Account Statement Form of the bank.

- Valuation Certificate

- Particulars of the Proposal.

- Particulars of the Mortgagor.

- Particulars of the Properties.

- Outstanding liability position of the bank.

(6) Disbursement stage

At this stage, bank decides to pay out money. Here, the client gets his/her desired fund or goods. It is to be noted that before disbursement a “site plan” showing the exact location of each mortgage property needs to be physically verified.

(7) Monitoring & Recovery stage

At this final stage of investment processing of the IBBL, Mirpur-10 Branch bank will contact with the client continually, for example- bank can obtain monthly stock report from the client in case of micro investment. Here, the bank will keep his eye on over the investment taker. If needed, bank will physically verify the client’s operations. Also if bank feels that anything is going wrong then it tries to recover its investment fund from the client.