Introduction

After completion of 123 credits (Out of 126 credits) in the BBA program, American International University of Bangladesh, three months organizational attachment is must. So the preparation and submission of this report is very important for the completion of the Bachelor of Business Administration (BBA). This report is outcome of the three month long internship program conducted in Prime Bank Limited, one of the reputed private commercial banks of the country.

I am doing my internship program in Prime Bank Limited, referenced to Garib-E-Newaz Branch. I am working in General Banking, Credit Department etc and observing closely all activity. The topic for my internship report is “Credit Portfolio Management of Prime Bank Limited”.

1.2 Objectives of the report

This report is prepared primarily to fulfill the Bachelor of Business Administration (BBA) degree requirement in BBA program of the faculty of business. American International University Bangladesh

1.2.1 Broad Objective

To know the credit portfolio management of Prime Bank Limited in relation to the overall industry.

1.2.2 Specific Objective

The specific objectives of this report are:

To develop knowledge and a clear understanding about credit portfolio management of Prime Bank Limited

To Identify and focuses the problems of Credit Management System of Prime Bank Limited.

To discuss the services offered by Prime Bank Limited.

To identify the major strength and weakness of Prime Bank Limited in respect to other banks.

To know about the management style and organization structure of Prime Bank Ltd.

To suggest necessary measures for the development of the bank.

1.3 Methodology of the report

Source of data:

This report is based mainly on observations that I will experience during the internship period. Data required for this report will be collected from the annual report. Apart from these, helpful information will be collected from online resources. To analyze the performance of Prime Bank Limited different statistical and financial tools such as ratio analysis, growth analysis will be done.

In order to prepare the theoretical framework of the study, exiting published textbooks, related journals, various data and research will be consulted and data will be collected from primary and secondary sources.

A. Primary data – Primary data will be collected by-

Interview

Observation

Work with them

Banking software.

B. Secondary data- Secondary information will be collected from-

a) Banks papers, b) Prospectus, c) Web site, d) MIS Report

e) Magazine f) Booklets, g) Hand note, h) Annual report

i) Other related research reports

1.4 Scope of the report

This report mainly analyzes Prime Bank’s practices about credit management activities emphasizing dispersion of the credit among various sectors and individual customers. This report consists of the writer’s observations and on the job experiences during the internship period in the credit departments of Garib-E-Newaz Branch. This report emphasizes the sequential activities involved in credit approval process, analytical techniques used by Prime Bank for credit analysis. The report also focuses on the loan monitoring techniques adopted by Prime Bank Limited both in pre-sanction and post-sanction period of a credit. Finally it recommends some measures to further strengthen its credit management.

1.5 Activity and Schedule

Also, from the inception of the internship it will take 12 weeks to finish the intended study.

| Activities | Weeks | ||||||||||||

| 1st | 2nd | 3rd | 4th | 5th | 6th | 7th | 8th | 9th | 10th | 11th | 12th | ||

| Proposal submission | ….. | …. | |||||||||||

| Questionnaire | ….. | ||||||||||||

| Data Collection | ….. | …. | …. | ||||||||||

| Analysis |

| …. | …. | ||||||||||

| Evaluate | …. | …. | |||||||||||

| Draft print

| …. | …. | |||||||||||

| Revision | …. | …. | |||||||||||

| Final Report submission | …. | ||||||||||||

1.6 Limitations of the report

The main limitation of this report is time frame. The time limit for the internship is only three months, and we have to understand the whole banking procedure and have to prepare a report within such limited time.

Management/officials are not always that much helpful regarding their confidential information.

I am working in one branch. I don’t know what procedures other branches are following and how they are managing their customers.

Chapter 2

About Prime Bank Limited

2.1 Prime Bank Limited

Prime Bank Limited is a scheduled commercial Bank under private sector established within the ambit of Bank Company Act, 1991 and was incorporated as a Public Limited Company under Companies Act, 1994 on February 12, 1995. The Bank started commercial banking operations from April 17, 1995 with the inauguration of the Bank’s Motijheel Branch at 119-120, Motijheel Commercial Area. A huge public response has enabled the Bank to keep up the plan of expanding its network. Within a span of ten years the bank has been able to deliver services to its customers through thirty-seven branches. In terms of profitability the bank has outperformed its peer banks. Operating profit of the bank in the last financial years was Tk. 3257 million.

As a fully licensed commercial bank, Prime Bank Ltd. is being managed by a highly professional and dedicated team with long experience in banking. They constantly focus on understanding and anticipating customer needs. As the banking scenario undergoes changes so is the bank and it repositions itself in the changed market condition.

Prime Bank Ltd. offers all kinds of Commercial Corporate and Personal Banking services covering all segments of society within the framework of Banking Company Act and rules and regulations laid down by our central bank. Diversification of products and services include Corporate Banking, Retail Banking and Consumer Banking right from industry to agriculture, and real state to software.

The bank has consistently turned over good returns on Assets and Capital. During the year 2007, the bank has posted an operating profit of Tk. 3257 million and its capital funds stood at Tk 6382 million. Out of this, Tk. 2275 million consists of paid up capital by shareholders and Tk. 2659.21 million represents reserves and retained earnings. The bank’s current capital adequacy ratio of 11.50% is in the market. In spite of complex business environment and default culture, quantum of classified loan in the bank is very insignificant and stood at less than 1.35%.

Prime Bank Ltd., since its beginning has attached more importance in technology integration. In order to retain competitive edge, investment in technology is always a top agenda and under constant focus. Keeping the network within a reasonable limit, our strategy is to serve the customers through capacity building across multi delivery channels. Our past performance gives an indication of our strength. We are better placed and poised to take our customers through fast changing times and enable them compete more effectively in the market they operate.

Vision

“To be the best Private Commercial Bank in Bangladesh in terms of efficiency, capital adequacy, asset quality, sound management and profitability having strong liquidity”

Mission

“To build prime Bank Limited into an efficient, market driven, customer focused institution with good corporate governance structure.

Continuous improvement in our business policies, procedure and efficiency through integration of technology at all levels”

Efforts are focused on

Delivery of quality service in all areas of banking activities with the aim to add increased value to shareholders’ investment and offer highest possible benefits to our customers.

Strategic Priorities

To have sustained growth, broaden and improve range of products and services.

The company believes that communication with, and feedbacks from its clients help it achieve its goal of providing world-class products and services. Prime Bank has engaged a relationship officer for each individual customer to address the requirements of the customer. It also constantly monitors its standards, and strives to exceed clients’ expectations.

2.2 Management Structure

2.3 Values Considered as Guiding Factors

All the activities and decisions of Prime Bank Limited are based on, and guided by, these values:

Placing the interests of clients and customers first

A continuous quest for quality in everything the company does

Treating everyone with respect and dignity

Conduct that reflects the highest standards of integrity

Teamwork- from the smallest unit to the enterprise as a whole

Being good citizens in the communities, in which they live and work

2.4 Capital Adequacy Ratio

In accordance with the instruction of Bangladesh Bank (the Central Bank of the country), the Bank adopted BIS risk adjusted capital standards to measure capital adequacy. Banks in Bangladesh are required to maintain the ratio of minimum 9.00% against risk weighted assets. The bank’s Capital Adequacy Ratio stood at 10.74% at the end of December 2008.

2.5 Equity Formation

TIER I CAPITAL

Authorised Capital

10,00,00,000 Ordinary shares of Tk 100 each Tk. 10,00,00,00,000.00

Paid Up Capital Tk. 2,84,37,50,000.00

Statutory Reserve Tk. 2,36,62,14,496.00

Surplus in profit & loss account/Retain Earnings Tk. 1,05,49,21,127.00

TIER II CAPITAL

General Provision maintained against unclassified

Loans/ investments Tk. 1,03,98,00,000.00

General provision on off-balance shit items Tk. 32,80,00,000.00

General provision on off-shore Banking Units Tk. 55,00,000.00

Revolution gains Tk. 9,01,40,000.00

Revolution reserve 50% of total Tk. 12,58,01,000.00

Exchange Equalization Account Tk. 45,23,000.00

2.6 Performance of the Bank

2.6.1 Profit and Operating Results

The Bank earned as operating profit Tk. 2463.35 million during 2008 after all provisions including the 1% general provision on unclassified Loans & Advances. Provision for income tax for the year amounted to Tk. 1231.52 million resulting into a net profit after tax of Tk 1231.83 million.

2.6.2 Deposit

A strong deposit base is necessary for the success of a Bank. During the year 2008 the Bank mobilized a substantial amount of deposits from mid-level income group people under Deposit Savings Scheme. After critical handling the Bank mobilized total Deposit of Tk. 88020.59 million as at December 31, 2008, thus recording an increase of 24.82% in comparison with Tk. 70512.37 million as at December 31, 2007. The significant growth in deposit enabled the Bank to expand its business, performing assets and also had an impact on the profit position of the bank.

2.6.3 Loans and Advance

The bank’s Loans & Advances portfolio also indicates an impressive growth. Total Loans and Advances amounted to Tk. 75156.21million in 2008 against Tk. 57683.02 million in 2007 and the growth being 30.29%, Prime Bank’s credit portfolio is well diversified and covers a wide range of businesses and industries. The sectors financed include Manufacturing, Trading, Construction, Transport, Agriculture, Fishing & Forestry, Edible Oil, Pharmaceuticals, Information Technology, and Consumer Credit amongst others. Advances constitute the most significant indicator of the health of a Bank. The Bank has formulated its policy to give priority to SMEs (small and medium enterprises) and at the same time the Bank is financing large-scale enterprises through consortium of Banks. Prime Bank is committed to maintaining a very high quality of assets. Close monitoring and efficient asset management has resulted in minimal creation (1.76 %) of classified loans to total Loans and Advances.

2.6.4 Foreign Exchange Business

International Trade constitutes the main stream of business activities of the bank. It offers a full range of trade finance and services namely, issue, advise and confirmation of Documentary Credit; arranging forward exchange coverage; pre -shipment and post-shipment finance; negotiation and purchase of export bills; discounting bill of exchange; collection of bills, inward and outward remittance etc.

Import Business: The Bank established Letters of Credit amounting to Tk. 36747.00 million during 2008; showing a growth of 44.44% over the volume of

Tk. 25440.70 million in the year 2007.

Export Business: The total export handled by the bank amounted to Tk. 19501.80 million for the year 2008 compared to Tk. 16490.10 million for 2007.

Foreign Correspondents: The number of foreign correspondents and agents of Prime Bank in 2008 stood at 501 covering most of the important business centers in different countries of the world. The Bank has maintained excellent relationship with leading international Banks and has successfully established credit lines with major Banks to support global Foreign Trade Business.

2.6.5 Investment

Investment stood at Tk 3083.81 million at the end of 2008. This consists of Tk.1, 250.80 million in Treasury Bills & Prize Bonds, Tk. 74.36 million in Debentures and Tk. 12.38 million in Shares.

2.7 Salient Features of the Bank

Prime Bank is engaged in conventional commercial banking as well as Islamic banking based on Islamic Shariah Principles.

It is the pioneer in introducing and launching different customer friendly deposit schemes to tap the savings of the people for channeling the same to the productive sectors of the economy.

For uplifting the standard of living of the limited income group of the population, the Bank has introduced Retail Credit Scheme by providing financial assistance in the form of loan to the consumers for procuring household durables.

The Bank is committed to maintaining continuous research and development to keep pace with modern banking.

The operations of the Bank are computer oriented to ensure prompt and efficient services to the customers.

The Bank has introduced camera surveillance system (CCTV) to strengthen the security services inside the Bank premises.

The bank has introduced customer relations management system to assess the needs of various customers and resolve any problem on the spot.

2.8 Products and Services

Prime Bank Limited launched several financial products and services since its inception. Among them are Contributory Savings Scheme, Monthly Benefit Deposit Scheme. All of these have received wide acceptance among the people.

2.9 Correspondence Relationship

The bank established correspondent relationships with a good number of foreign banks, namely CITI Bank N.A, American Express Bank, Bank of Tokyo, Standard Chartered Bank, Mashreq Bank and AB Bank Limited. The bank is maintaining foreign currency accounts in New York, Tokyo, Calcutta, London and many other important commercial hubs of the world. During this period the bank provided letter of credit facility on behalf of its valued customers using its correspondents as advising and reimbursing banks.

Chapter 3

Lending Process- Products, Principles and Strategies

3.0 Types of Credit offered

Prime Bank Limited offers both funded and non-funded credit facilities. The various funded and non-funded credit facilities that Prime Bank provides to its borrowers are:

3.1 Funded Facilities

The funded credit facilities are those which involve direct cash. In other words, any type of credit facility which involves direct outflow of bank’s fund on account of borrower is termed as funded credit facility. The following funded credit facilities are provided by Prime Bank Limited:

3.1.1 Cash Credit

Cash credit is a continuous loan facility usually provided to meet up working capital requirements of the customer. Cash credit can be given on hypothecation or pledge of goods but Prime Bank only provides Cash Credit on Hypothecation.

This advance is given to the retailers and whole sellers. In this credit primary security is the goods under hypothecation i.e. the goods for purchase of which the bank provides finance. This is a continuous loan and the customer can withdraw money from the account as many times a day as it wants and thus it functions as a checking account. Again the customer can deposit money as many times as it wants and is obliged to deposit the sale proceeds in the account as per terms of sanction.

Secondary security and hence collateral security is the registered mortgage of houses, land and buildings etc as provided by the customer. Prime Bank Limited encourages highly collateralized facility only. Interest rate is 14.00% p.a with quarterly compounding with special rate for corporate customers.

3.1.2 Cash Credit (Pledge)

This is another advance mode to finance the working capital requirement of the retailers and resembles Cash Credit (hypothecation). The only difference between Cash Credit (Hypothecation) and Cash Credit (Pledge) is that in case of CC(Hypo) the goods are both owned and controlled by the retailer, the loanee whereas in case of CC(Pledge) ownership of the goods lies with the borrower and control of the goods lies with the bank. The borrower deposits money in the account and releases the goods equivalent to the money deposited.

Interest rate is 14.00% p.a. For customers with exceptionally good repayment the interest rate is lowered up to 12.50% p.a. Interest rate also is dependant on the quality and marketability of the security offered.

Features of Cash Credit

A certain limit of credit amount is set at the time of initiation of Cash Credit facility

An expiration date is set, which is not more than one year

The drawings are subject to drawing power

The primary security of Cash Credit facility is stock of goods, which is hypothecated to Prime Bank Limited as collateral

With satisfactory transaction the limit may be enhanced based of the requirement of the customer

3.1.3 Over draft

Over draft facility is also a continuous loan arrangement permitting him/her to draw up to a certain approved limit for an agreed period. Here the withdrawal of deposits can be made any number of times at the convenience of the borrower, provided that the total overdrawn amount does not exceed the sanctioned limit.

Customer can return any amount at any time within the pre-fixed time of the facility. Turn over of an Over Draft facility is the most important phenomenon on which renewal of the facility depends. Over Draft facility is given to the businessmen for financing working capital requirement and high net worth individual to overcome temporary liquidity crisis.

3.1.4 Secured Overdraft

This type of loan is provided to both individuals as well as business entities. This is named so as the advance made is secured by either financial instruments like Sanchaypatra, Fixed Deposit Receipt and other financial obligations or by the bills receivable. This has following sub types:

SOD against financial Obligation

SOD against FDR

SOD against Special Scheme

SOD General

SOD against Work Order

SOF against Shares

i. This is the overdraft against lien on financial obligations like Sanchaypatra, ICB Unit certificate etc. Rate of interest ranges from 2.50% to 3.00% above the rate earned by the financial instrument e.g if the Sanchaypatra earns 10% interest, interest on loans against the Sanchaypatra ranges from 12.50% to 13.00%. However as this loan account can be transacted as many times as possible within the given validity period of one year this also meets requirement of business houses. Interesting thing that is beneficial to the loanee is that the loanee has to pay interest only on the outstanding amount e.g. if the loanee takes a loan of Tk. 50,000.00 against lien on Sanchaypatra valuing Tk. 1,00,000.00, he has to pay interest only on 50,000.00 whereas he earns interest on the whole amount of Sanchaypatra i.e. 1,00,000.00.

ii. SOD (FDR) is the overdraft against lien on FDR. The FDR may be of the same bank or other bank. In case of FDR of Prime Bank Limited, the interest rate is 2.50% above the FDR interest rate whereas for other bank’s FDR the interest is 14.00% p.a with quarterly compounding irrespective of the interest earned by the FDR.

iii. SOD against special scheme is the SOD against special schemes like CSS (Contributory Savings Scheme). In this case only 80% of the principal amount deposited by the customer is given as advance. Again the interest rate is 14.00% per annum with quarterly compounding.

iv. SOD general is the overdraft for bidding in tenders and is given as Pay Order. Whenever a government authority like Roads and Highways Division invites a tender it seeks security from the bidders so that in case of award of the work order the contractor cannot leave the job undone. To avoid the risk the authority asks the bidders to submit pay order which is highly liquid to them. Banks issue pay orders on behalf of the customer, here the contractor, through creation of a loan account in the name of the customer.

Another thing is that most of the times each individual contractor submits his bid in the name of multiple firms to increase the probability of winning the bid. This requires huge amount of money which businesses do not have always. The banks bridge the gap through extension of SOD (Earnest Money) or SOD (General) facility. The pay orders that do not win the tender are returned by the work giving authority to the contractors who submit it to the banker and thus gets rid of its liabilities. Interest rate charged by Prime Bank Limited on this facility is 14.00% p.a with quarterly rest.

v. SOD against work order is given for execution of work orders awarded by different government bodies and private companies. In this case the security is the bills receivable by the contractor from the work awarding authority following execution of work to its complete satisfaction.

The Irrevocable General Power of Attorney executed by the contractor in favor of the bank authorizing it to collect all the bills receivable by him stands as the primary security. The work awarding authority pays the bills to the bank and thus the liabilities are adjusted. Rate of interest is 14% for general customers and for top rated customers it ranges from 14.00% to 12.00% depending on the creditworthiness and bargaining power of the customer.

vi. SOD against Shares is loans given against shares as security. However, to cope with the volatility of the share market, the bank gives loans only up to 50% of the average Market value of the particular share under consideration during the last six months or the face value whichever is lower. Interest rate is 15.00% per annum. Interest is 1% higher due to higher risk of the share value fluctuation.

3.2 Hire Purchase

Hire Purchase is a type of installment credit under which the Hire Purchase agrees to take the goods on hire at a stated rental, which is inclusive of the repayment of Principal as well as interest for adjustment of the loan within a specified period.

3.3 Lease Finance

Lease financing is one of the most convenient long term sources of acquiring capital machinery and equipment. It is a very popular scheme whereby a client is given the opportunity to have an exclusive right to use an asset, usually for an agreed period of time, against payment of rent. Of late, the lease finance has become very popular in almost all the countries of the world. An obvious advantage of the lease is to use an asset without having to buy it. The lessee is obligated to make lease payments until the expiration of the lease agreement, which corresponds to the useful life of the asset.

In a capital scarce economy like ours, Lease Financing is suitable for firms to acquire Capital Machinery, Equipments, Medical Instruments, Automobiles etc. And thereby employ their own resources more advantageously in some other investments. Lease financing also helps a firm to reap significant economic benefit through tax saving and by reducing the risk of the equipments becoming obsolete due to the technological advancement.

3.3.1 Objective of Lease Finance

Prime Bank Ltd. has introduced the lease finance with the following objectives:

To assist the genuine and capable entrepreneurs for acquiring Capital Machinery and Equipments to undertake enterprises without equity.

To encourage the new and educated young entrepreneurs to undertake productive venture and demonstrate their creativity and thereby participate in the national development.

To participate in the industrial development of the country.

3.3.2 Lease Items / Equipments

Prime Bank Limited offers lease finance for acquiring the use of capital machinery, equipments, medical instruments, etc. The customers are entitled to decide the specification, price and model of the lease item/equipment. Bank will purchase the item (s) in accordance with the specifications given by the clients. However, the suppliers of the items must ensure after sales services and warranties. The price should be competitive and acceptable to the Bank.

3.3.3 Eligibility for Availing Lease finance

All genuine entrepreneurs having adequate experience and expertise are eligible to apply for Lease Finance under the scheme. The amount of Lease Finance will not generally exceed Tk. 1.00 crore, but in exceptionally good cases, the limit can reasonably be exceeded on condition that the Bank will depute an officer for close and intensive supervision of the project. In other cases of Lease Finance for amount below Tk. 1.00 crore, an officer of the Bank will supervise a number of projects at a time according to convenience.

3.3.4 Documents & Security

The entrepreneur will be required to provide the following securities:

01. The lease items will remain in the name of the Bank i.e., Bank will be the sole owner of the leased items.

02. Collateral securities having liquidation value covering at least 100% of the amount of finance.

03. Deposit of listed Shares, National Savings Certificates, ICB Unit Certificates, Assignment of Life Insurance Policies, Bank Guarantee, Insurance Guarantee etc. will also be acceptable as collateral securities.

04. In case of existing industrial units requiring BMRE, charge may be created on the existing Fixed Assets as collateral securities for the finance. In case of existing Automobile enterprises, creation of charge on the existing vehicles will also be acceptable as collateral securities.

05. i) In case of default in payment of lease rental for consecutive 2 (two) months, the Bank will take over the lease items without giving any prior notice. ii) In case of taking over the lease items by the Bank before maturity, the lessee will be liable for the loss, if any, caused to the Bank of such premature taking over. iii) The Bank will exercise close and intensive supervision of such projects. An Officer of the Bank will be engaged separately for supervision of such projects to ensure proper utilization of the lease items and timely repayment of the monthly rentals.

3.3.5 Lease Finance

After having favorable discussion on the various aspects of the Project particularly on the terms and conditions of lease financing, a customer may formally apply in specific application form designed by the Bank. The customer is required to provide detailed information on the project and its various aspects. After proper appraisal, if found suitable, Bank will draw terms and conditions of the lease.

3.3.6 Lease Agreement

After sanction of a proposal for lease finance, a lease agreement will have to be executed between the client and the Bank. The lease rental, lease deposit etc. stated in the lease agreement shall be calculated on the basis of the estimated acquisition cost of the equipment which shall be adjusted on the basis of actual costs and charges at the time of execution. After execution of the agreement, the Bank will purchase the specified items/ equipments and the customer will be under obligation to accept the equipment for the specified lease period.

The customer will be required to make a deposit equivalent to 3 (three) months lease rentals to the Bank on the date of signing of the lease agreement which shall be refunded to the client at the expiry of the lease term.

3.3.7 Procurement and Installation of Lease Equipment

Bank will place firm purchase order directly to the manufacturer / supplier on the basis of terms and conditions embodied in the agreement between the client and the supplier. The equipment is to be delivered to the selected location of the client. Bank will make full payment after confirmation of the acceptance of the equipment by the client.

In case of imported equipment, Bank will open Letter of Credit in its own name. the Custom clearance and inland transportation of the equipment to the respective locations shall be handled by the client with the co-operation of the Bank. All incidental costs in this regard shall be paid by the Bank and will be included in the acquisition cost of the equipment.

After taking delivery of the equipment, the customer will directly install it at his location as specified in the agreement with the technical assistance of the supplier, if any.

Execution:

On lease execution, the client and the Bank shall enter into an Amendment Lease Agreement reflecting the actual acquisition cost. At the same time the client will issue the certificate of the acceptance of equipment and pay the first lease rentals, insurance premium of the 1st lease year as well as any other charge to the Bank.

Acquisition Cost:

The acquisition cost shall be the purchase price and all other incidental expenses incurred by the Bank including financial expenses such as custom duty and other taxes, charges in connection with opening of L/C, insurance premium, freight, transportation, storage charge etc.

Term of Lease and Payments There Against:

The term of lease may be for a period of maximum 5 (five) years during which the lessee will have the exclusive right to use the equipment. On expiry, the lessee may have the option to renew the lease on a year to year basis at a predetermined rental or return the equipment to the Bank. Besides the above options, the lessee may purchase the lease equipment at a reasonable price upon mutual agreement.

Lessee will pay service charge or project examination fee @0.15% on the sanctioned amount subject to a minimum Tk. 3,000 and maximum Tk. 10,000 in case of acquisition of Machinery and Equipments for projects. In case of Automobile, a service charge of Tk. 500 is payable when the acquisition cost is below Tk. 10.00 lac and an amount of Tk. 1,000 is payable when the acquisition cost is Tk. 10.00 lac and above.

The lessee will pay monthly rental in advance starting from the date of execution till end of lease term. Insurance charges are payable by the lessee at actual. 1st year premium is payable on the date of execution.

3.4 Consumer Credit Products

Household Durable Loan Car Loan

Doctors Loan Advance against Salary

Any Purpose Loan Education Loan

Travel Loan Marriage Loan

CNG Conversion Loan Hospitalization Loan

Chapter 4

Lending Procedure

Lending is the main profit generating activity of a bank. Every bank should possess a lending procedure that provides correct borrower selection, quick processing, assurance of repayment and effective monitoring and supervision. The lending procedure followed by Prime Bank Limited consists of a set of sequential activities. In these sequential activities, both bank officials and potential borrowers play significant role.

4.1 Different Activities in Lending Process

The lending procedure starts with building up relationship with customer through account opening. The stages of credit approval are done both at the branches and at the corporate office level. The lending procedure is described below in sequential order:

Step-1

A loan procedure formally starts with a loan application from a client who must have an account with the bank. Branch receives application from client for a loan facility. In the application client mention what type of credit facility he/she wants from the bank including his/her personal information and business information. Branch Manager or the Officer-in-charge of the credit department conducts the initial interview with the customer.

Step-2

The bank sends a letter to Credit Information Bureau of Bangladesh Bank for obtaining a credit inquiry report of the customer from there. This report is called CIB (Credit Information Bureau) report. This report is usually collected if the loan amount exceeds Taka fifty thousand. The purpose of this report is to be informed that whether or not the borrower has taken loans and advances from any other banks and if so, what is the status of those loans and advances i.e. whether those loans are classified.

Step-3

If Bangladesh Bank sends positive CIB report on that particular borrower and if the Bank thinks that the prospective borrower will be a good one, then the bank will scrutinize the documents. Required documents are:

• In case of corporate client, financial statements of the company for the last three to five years. If the company is a new one, projected financial data for the same duration is required.

• Personal net worth of the borrower(s).

Step-4

Bank officials of the credit department will inspect the project for which the loan is applied. Project existence, its distance from the bank originating the loan, monitoring cost and possibilities are examined.

Step-5

Any loan proposal is evaluated on the basis of financial information provided by the applicant. Financial spread sheet analysis which consists of a series of quantitative techniques is employed to analyze the risks associated with a particular loan and to judge the financial soundness and worthiness of the borrower. Besides lending risk analysis is also undertaken by the bank to measure the borrower’s ability to pay considering various risks associated the loan. These quantitative techniques supported with qualitative judgment are the most important and integral part of the credit approval process used by Prime Bank Limited.

Step-6

Documents related to the collateral security offered by the customer are sent to the bank’s panel lawyer for vetting. Bank based on the expert opinion of the lawyer further process the loan proposal.

Step-7

If the proposal meets Prime Bank’s lending criteria and is within the manager’s delegated power, the credit line is approved by the manager himself. The manager and the sponsoring officer sign the credit line proposal and issue a sanction letter to the client.

If the value of the credit line is above the branch manager’s limit then it is sent to head office or for final approval with detailed information regarding the client (s), credit analysis and security papers.

Step-8

Head office processes the credit proposal and puts forward an office note if the loan is within the power of the head office credit committee. Otherwise it is sent to board if the loan requires approval from the board of directors.

Step-9

If the credit committee of the head office or the board as the case may be approves the credit line, an approval letter is sent to the branch. The branch then issues a sanction letter to the borrower with a duplicate copy.

Step-10

After issuing the sanction advice, the bank will collect necessary charge documents. Charge documents vary on the basis of types of facility, types of collateral.

Step-11

Finally loan is disbursed by the branch through a loan account in the name of the borrower and monitoring of the loan starts formally.

Chapter 5

Credit Analysis

Credit analysis is of utmost importance for the lending process to be successful. Proper credit analysis helps avoid risks in lending and brings transparency. The analysis of financial statements of the prospective borrower(s) carried on for the purpose of determining the past financial health of the borrowing unit and judging whether any future loan commitment to the unit is secured or not is known as credit analysis. Credit analysis is generally done at the branch level of lending process and the results and findings are evaluated in the corporate office.

The basic financial statements required for credit analysis are:

Balance Sheet

Income statement (Profit and Loss Account)

Cash Flow Statement.

Equity Statement

The credit analysis starts with the financial spread sheet analysis using the financial statements provided by the borrowing unit.

5.1 Balance Sheet

As at 31 December, 2008

| Particulars | Amount in Taka | |

2008 | 2007 | |

| PROPERTY AND ASSETS | ||

| Cash | ||

| In hand | 750,107,609 | 663,028,189 |

| Balance with Bangladesh Bank | 6,447,553,847 | 4,755,788,872 |

7,197,661,456 | 5,418,817,061 | |

| Balance with other Banks and financial institutions | ||

| In Bangladesh | 420,777,975 | 1,625,581,391 |

| Outside Bangladesh | 1,581,293,172 | 791,887,088 |

2,002,071,147 | 2,417,468,479 | |

| Money at call and short notice investments | ||

| Government | 20,807,924,500 | 12,090,285,095 |

| Other | 2,295,173,745 | 607,735,533 |

| 23,13,098,245 | 12,698,020,628 | |

| Loans and Advances/ Investments | ||

| Loans Cash Credits, Overdrafts/ Investments | 70,574,812,562 | 53,814,967,656 |

| Bills Purchased and discounted | 4,581,394,255 | 3,868,053,856 |

75,156,206,817 | 57,683,021,512 | |

| Fixed Assets including premises, furniture and fixture | 1,374,826,295 | 660,490,066 |

| Other Assets | 1,603,293,351 | 710,613,052 |

| Total Assets | 110,437,103,311 | 79,588,430,798 |

| LIABILITIES AND CAPITAL | ||

| liabilities | ||

| Borrowings from other banks, other financial institutions and agents | 11,397,859,931 | 3,908,694,900 |

| Deposits and other accounts | ||

| Current/Al Wadeeah current Deposits | 11,868,543,906 | 10,590,463,357 |

| Bills payable | 1,239,622,153 | 1,144,540,968 |

| Savings bank/ Mudaraba savings deposits | 6,797,681,897 | 6,027,260,878 |

| Term deposits/ Mudaraba term deposits | 68,114,743,430 | 52,750,109,722 |

| bearer certificate of deposits | ||

| other deposits | ||

88,020,591,386 | 70,512,374,925 | |

| Other Liabilities | 4,321,881,216 | 3,411,909,021 |

| Total liabilities | 103,740,332,533 | 74,315,153,436 |

| Capital/ Shareholders Equity | ||

| Paid up Capital | 2,843,750,000 | 2,275,000,000 |

| Statutory reserve | 2,366,214,496 | 1,873,543,597 |

| Revaluation Gain/(Loss) investment | 180,281,588 | 12,723,913 |

| Revaluation Reserve | 251,603,567 | |

| Other reserve | ||

| Surplus in profit and loss account/ retained earnings | 1,054,921,127 | 1,112,009,852 |

| Total shareholders equity | 6,696,770,778 | 5,273,277,362 |

| Total liabilities and equity | 110,437,103,311 | 79,588,430,798 |

| OFF-BALANCE SHEET ITEMS | ||

| Contingent liabilities | ||

| Acceptance and endorsements | 9,129,069,603 | 6,905,831,656 |

| Letters of guarantee | 13,201,578,022 | 10,480,381,241 |

| Irrevocable letters of credits | 10,323,790,924 | 14,287,797,206 |

| bills for collection | 3,599,083,644 | 1,414,716,406 |

| Other contingent liabilities | ||

36,253,522,193 | 33,088,726,509 | |

| other commitments | ||

| Documentary credits and short term trade related transactions | ||

| Forward Asset purchased and forward deposit placed | ||

| Undrawn note issuance and revolving underwriting facilities | ||

| Liabilities against forward purchase and sales | 588,912 | |

| Others | 1,561,232,858 | |

1,561,821,770 | ||

37,815,343,963 | 33,088,726,509 | |

| Other memorandum items | ||

| Value of travelers cheques in hand | 269,954 | 141,383,952 |

| Value of Bangladesh sanchay patras in hand | 311,360,300 | 1,348,897,500 |

311,630,254 | 1,490,281,452 | |

| Total off-balance sheet items including contingent liabilities | 38,126,974,217 | 34,579,007,961 |

5.2 Profit and Loss Account

For the year ended 31 December, 2008

| Particulars | Amount in Taka | ||

2008 | 2007 | ||

| Interest Income/ profit on investment | 9,095,891,683 | 7,170,099,616 | |

| Interest / profit paid on deposits, borrowings, etc | -7,126,309,515 | -5,266,592,564 | |

| Net interest/ Net profit on investments | 1,969,582,168 | 1,903,507,052 | |

| Investment income | 1,743,677,466 | 1,294,205,056 | |

| Commission, exchange and brokerage | 1,436,896,251 | 1,198,942,404 | |

| Other operating income | 627,564,412 | 419,555,862 | |

| Total operating income(A) | 5,777,810,297 | 4,816,210,375 | |

| Salaries and allowances | 899,204,898 | 725,285,435 | |

| Rent, texes, insurance, electricity etc | 203,265,914 | 159,529,399 | |

| Legal expenses | 14,164,497 | 24,728,362 | |

| Postage, stump, telecommunication etc | 78,712,209 | 60,999,650 | |

| Stationary, printing, advertisements etc | 95,990,087 | 121,691,050 | |

| Managing directors salary and fees | 7,914,344 | 9,131,448 | |

| directors fees | 2,385,044 | 2,224,444 | |

| Auditors fees | 418,000 | 791,725 | |

| Charge on loan losses | |||

| Depreciation and repaid of banks assets | 151,233,852 | 102,185,026 | |

| Other expenses | 477,666,956 | 325,779,110 | |

| Total operating expenses(B) | 1,930,955,801 | 1,559,345,650 | |

| Profit/ (loss) Before provision(C=A-B) | 3,846,854,496 | 3,256,864,725 | |

| Provision for loans/ investments | -1,115,000,000 | -350,000,000 | |

| specific Provision | -145,000,000 | -350,000,000 | |

| General provision | -5,500,000 | ||

| Provision for off-shore banking units | 118,000,000 | 210,000,000 | |

| Provision for off-balance sheet items | -1,383,500,000 | -910,000,000 | |

| Provision for diminution in value of investments | |||

| Other provision | |||

| Total provision(D) | -1,383,500,000 | -910,000,000 | |

| Total profit/(loss) before taxes(C-D) | 2,463,354,496 | 2,346,864,725 | |

| Probation for taxation | |||

| Current tax | -1,012,449,724 | -1,015,000,000 | |

| Deferred tax | -219,072,598 | 68,800,000 | |

-1,231,522,322 | -946,200,000 | ||

| Net profit after taxation | 1,231,832,174 | 1,400,664,725 | |

| Retain earning brought forward from previous year | 315,759,852 | 180,718,073 | |

1,547,592,026 | 1,581,382,798 | ||

| Appropriations | |||

| Statutory reserve | 492,670,899 | 469,372,945 | |

| General reserve | |||

492,670,899 | 469,372,945 | ||

| Retain surplus | 1,054,921,127 | 1,112,009,852 | |

| Earning per share (EPS) | 43.32 | 49.25 | |

5.3 Cash Flow Statement

For the year ended 31 December 2008

| Particulars | Amount in Taka | |

2008 | 2007 | |

| A) cash flow from operating activities | ||

| interest receipt in cash | 9,606,084,937 | 7,076,601,586 |

| Interest payments | -5,522,743,033 | -5,266,592,564 |

| Dividend receipts | 20,719,822 | 7,976,958 |

| Fees and commission receipts in cash | 1,436,986,251 | 1,198,942,404 |

| Recoveries of loans previously written-off | 85,202,572 | 415,867 |

| Cash payments of employees | -749,119,242 | -729,416,883 |

| Cash payments to suppliers | -307,191,812 | -286,567,522 |

| Income taxes paid | -941,801,045 | -476,148,788 |

| Receives from other operating activities | 745,157,044 | 419,558,862 |

| Payment for other operating Activities | -468,943,744 | -470,041,003 |

| Cash generated from operating activities before change | 3,910,351,750 | 1,474,723,317 |

| Net operating assets and liabilities | ||

| Increase/ (decrease) in operating assets and liabilities | ||

| Statutory deposits | ||

| Purchase of trading securities(treasury bills) | -1,105,739,703 | -1,197,259,262 |

| Loans and advances to other banks | ||

| Loans and advances to customers | -17,473,785,305 | -12,672,803,463 |

| Other assets | -8,819,910,712 | -3,796,358,897 |

| Deposits from other banks/ borrowings | 11,242,203,400 | 632,890,500 |

| Deposits from customers | 16,773,432,106 | 15,171,985,121 |

| Other liabilities account to customers | 95,081,185 | 616,309,220 |

| Trading liabilities | ||

| Other liabilities | 1,956,357,400 | 1,437,147,293 |

-1,244,476,429 | -378,089,488 | |

| Net cash from operating activities | 2,665,875,321 | 1,096,636,429 |

| B) Cash flows from investing activities | ||

| Debentures | 5,067,718 | 4,932,282 |

| Proceeds from sale of securities | ||

| Payments for purchase of securities | -612,475,711 | -430,320,723 |

| Purchase of property, plant and equipment | -539,366,206 | -333,719,898 |

| Payment against lease obligations | -2,785,500 | |

| Proceeds from sale of property, plant and equipment | 290,500 | 277,045 |

| Net cash used in investing activities | -1,146,483,699 | -761,616,794 |

| C) Cash flows from financing activities | ||

| Dividend paid | -227,500,000 | |

| Net cash from financing activities | -227,500,000 | |

| D)Net increase/(decrease) in cash and cash equivalents (A+B+C) | 1,291,891,622 | 335,019,635 |

| E) Effects of exchange rate change on cash and cash equivalents | ||

| F) cash and cash equivalents at beginning of the year | 7,803,285,850 | 7,468,239,215 |

| G) cash and cash equivalent at end of the year(D+E+F) | 9,095,150,472 | 7,803,258,850 |

| Cash and cash equivalents at end of the years | ||

| Cash in hand ( including foreign currencies) | 750,107,609 | 663,028,189 |

| Balance with Bangladesh Bank and its agent banks (Including foreign currencies) | 6,447,553,847 | 4,755,788,872 |

| Balance with other banks and financial institutions (Notes 4(b)) | 1,895,025,116 | 2,382,784,489 |

| Money at call and short notice | ||

| Reverse repo | ||

| Prize bonds | 2,463,900 | 1,657,300 |

9,095,150,472 | 7,803,285,850 |

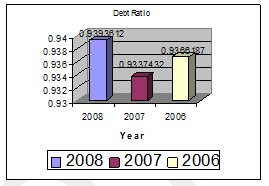

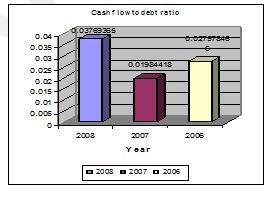

5.4 Ratio Analysis

| Components | 2008 | 2007 | 2006 |

| Total liability | 103,740,332,533 | 74,315,153,436 | 57,039,587,069 |

| Total asset | 110,437,103,311 | 79,588,430,798 | 60,899,475,793 |

| Share holders equity | 6,696,770,778 | 5,273,277,362 | 3,859,888,724 |

| Operating Cash flow | 3,910,351,750 | 1,474,723,317 | 1,573,064,318 |

| Total Debt | 103,740,332,533 | 74,315,153,436 | 57,039,587,069 |

| Net Income After Tax | 1,231,832,174 | 1,400,664,725 | 1,059,890,526 |

| Total Equity Capital | 6,696,770,778 | 5,273,277,362 | 3,859,888,724 |

| Net Interest Income | 9,095,891,683 | 7,170,099,616 | 5,198,790,368 |

| Net interest expense | 7,126,309,515 | 5,266,592,564 | 3,698,441,036 |

| Total Operating revenue | 5,777,810,297 | 4,816,210,375 | 3,232,036,163 |

| Total operating expense | 1,930,955,801 | 1,559,345,650 | 1,101,072,827 |

| Current Assets | 75,156,206,817 | 57,683,021,512 | 49,296,890,329 |

| Current Liability | 76,622,731,455 | 66,603,680,025 | 56,297,458,256 |

| Cash | 71324920171 | 54,477,995,845 | 49,469,568,369 |

| Ratio | 2008 | 2007 | 2006 |

| Debt ratio | 0.939361224 | 0.933743167 | 0.936618687 |

| Cash flow to debt ratio | 0.03769365 | 0.01984418 | 0.027578466 |

| ROE | 0.183944205 | 0.265615599 | 0.274590954 |

| ROA | 0.011154151 | 0.017598848 | 0.017403935 |

| Net Interest margin | 0.017834424 | 0.023916881 | 0.02463649 |

| Current Ratio | 0.98086045 | 0.866063579 | 0.875650373 |

| Cash Ratio | 0.930858491 | 0.81794273 | 0.878717617 |

| Debt Equity ratio | 15.49109802 | 14.09278298 | 14.7775211 |

| Leverage | 2043.083903 | 2039.130291 | 2039.590239 |

5.4.1 Debt ratio

The debt ratio compares a company’s total debt to its total asset, which is used to gain a general idea as to the amount of leverage being used by a company. A low percentage means that the company is less dependent on leverage that is money borrowed from and/or owed to others. The lower the percentage, the less leverage a company is using and the stronger its equity position. In general, the higher the ratio, the more risk that company is considered to have taken on.

Here in 2008, the debt ratio of Prime Bank Ltd has slightly increased than 2007. That means they have borrowed more money and ratio is close to 1, which is not good. Because the higher the borrowed amount, the higher the interest they have to pay to others. But that also indicates that now they are taking more risks.

5.4.2 Cash flow to debt ratio

This ratio provides an indication of a company’s ability to cover total debt with its yearly cash flow from operations. The higher the percentage ratio, the better the company’s ability to carry its total debt.

In this situation Prime Bank Ltd did well in 2008, their percentage had increased from 2075% to 3.76 %, which is very good.

5.4.3 Net interest margin

Net interest margin is a performance metric that examines how successful a firm’s investment decisions are compared to its debt situations. A negative value denotes that the firm did not make an optimal decision, because interest expenses were greater than the amount of returns generated by investments.

The graph shows us that, in 2008 the interest margin has decreased than 2007 from 0.024 to 0.018 -which means they have to be more conscious while taking optimal decisions.

5.4.4 ROA

An indicator of how profitable a company is relative to its total assets. ROA gives an idea as to how efficient management is at using its assets to generate earnings.

In 2008 ROA has decreased to 1.11% from 1.76%, which means Prime Bank Ltd is investing more money but they couldn’t generate more income against invested money- that is not good for the organization. The higher the ROA number, the better, because the company is earning more money on less investment.

It is very important for an organization to make large profits with little investment. And to do this the managers has to make wise choices in allocating its resources.

5.4.5 ROE

Return on equity measures a corporation’s profitability by revealing how much profit a company generates with the money shareholders have invested.

Here the ROE has decreased in 2008 at a high percentage from 26.56% to 18.39% than 2007 and also from 2006 as well.

5.4.6 Current ratio

It is a liquidity ratio that measures a company’s ability to pay short-term obligations. The current ratio can give a sense of the efficiency of a company’s operating cycle or its ability to turn its product into cash.

The higher the current ratio, the more capable the company is of paying its obligations. A ratio under 1 suggests that the company would be unable to pay off its obligations if they came due at that point, but it is definitely not a good sign.

Here the graph shows that the Current ratio has increased significantly from 0.866 to 0.980, which is a very good sign for any organization.

5.4.7 Cash Ratio

For a bank cash ratio is the cash held by the bank as a proportion of deposits in the bank. The cash ratio measures the extent to which a corporation or other entity can quickly liquidate assets and cover short-term liabilities and therefore is of interest to short-term creditors.

In year 2008 cash ratio also has increased significantly. That means Prime Bank Ltd has more liquid money in hand to cover its short term liabilities, which is very good for an organization.

5.4.8 Debt to equity

The debt-equity ratio is to compares a company’s total liabilities to its total shareholders’ equity. This is a measurement of how much suppliers, lenders, creditors and obliger have committed to the company versus what the shareholders have committed.

A lower the percentage means that a company is using less leverage and has a stronger equity position.

But here Prime bank Ltd has a higher Debt-Equity ratio in 2008 than 2007 and 2006 respectively.

5.5 Financial Spread Sheet Analysis

Financial spread sheet is a means of presenting the main Balance Sheet and Profit and Loss categories in a form whereby a comparison can be made between similar figures on different dates.

5.5.1 Importance of Financial Spread Sheet

1. Financial spread sheet provides a quick method of assessing business trends and efficiency.

• Asses the borrowers’ ability to repay.

• It realistically shows business trends.

• It allows comparisons to be made within industry.

2. Borrowers that provide information for financial spread sheets are more like to be good borrowers.

3. Financial spread sheet is an important tool in a disciplined organized approach to credit analysis.

4. The historic financial reports of a company are a primary indicator of its future financial position. Spread sheet allows proper analysis of financial statements.

5.5.2 Breakdown of Financial Spread Sheet

The financial spread sheet is split into four sections. These are:

a. Balance Sheet and Profit and Loss Account provide a quick and easy source of identifying trends in similar categories over a number of years.

b. Cash Flow Statement indicates the company’s ability to generate cash inflow in excess of cash outflow.

c. Ratio analysis demonstrates in the form of accounting ratios and percentages, the relationship between significant figures on different dates. This provides a quick and reliable method of

• measuring trends of profits;

• identifying the growth or correction of the business;

• Identifying strengths and weaknesses of the business.

d. The Credit Scoring System

• Z Score

• Y Score

5.6 Credit Scoring System (Z- Score and Y- Score)

The credit scoring system is a quantitative technique to assess the risks associated with a particular loan project in terms of numerical number.

5.6.1 Purpose of Credit Scoring System

It uses a combination of financial ratios to produce a rating, which is an indication of a company’s management ability and financial strength.

The credit scores are intended to highlight inherent weaknesses in financial statements. They are not designed to provide a definitive answer as to whether a loan proposal should be approved or declined.

As with all financial ratios, the trend is just as important as the score. Down trend requires investigation even when the score is satisfactory.

5.6.2 Calculation of “Z” Score

Z score is a credit scoring system which is applied to large manufacturing companies of the following categories:

Public companies quoted on Dhaka Stock Exchange and Chittagong Stock Exchange.

Government owned or quasi government companies.

Other companies with a sale of over Tk. 50 crore.

The formula (which can be also be used manually) to calculate the “Z” score is as follows:

Z = 0.012 X 1 + 0.14 X2 + 0.033 X3 + 0.006 X4 + 0.999 X5

Where,

X 1 = Working Capital / Total Assets

X2 = Retained Earnings / Total assets

X3 = Earnings before Interest and Taxes / Total Assets

X4 = Equity / Total Liabilities

X5 = Sales / Total Assets

Variables X1 to X4 must be calculated as absolute percentages.

Variable X5 is calculated in terms of whole number, not in absolute percentage.

5.6.3 Interpretation of “Z” Score

A score higher than three (3) rates a “Good Risk”.

A score of less than three (3) indicates further investigation is necessary.

A score of less than 1.81 evidences an inherent weakness and a probability of the company falling within two years.

A consistent downward trend requires investigation even when the score is satisfactory.

5.6.4 Calculation of “Y” Score

“Y” score is a credit scoring system which is applied to all trading companies. The formula (which can be used manually) calculates five ratios and awards points to each according to a particular table.

The ratios are:

Current Ratio (CR) = Current Assets / Current Liabilities

Quick Ratio (QR) = (Cash + Equivalents + Accounts Receivables) / Current Liabilities

Liquidity Ratio (LR) = (Cash + Equivalents) / Current Liabilities

Assets Ratio (AR) = Total Assets / Total Liabilities

Return on Investment (ROI) = Net Profit for the Year / Ending Net Worth.

Cash includes cash in hand; cash in bank and securities (short term investments). It does not include restricted cash i.e. margins.

Accounts receivables are after allowances for bad debt and receivables from directors, employees and special transactions are excluded.

Net profit is after tax. But before payment of dividend, profit for periods of less than a year must be annualized before ROI is calculated.

Table-4: Interpretation of “Y” Score

| Points | CR | QR | LR | AR | ROI |

| 4 | 2.00 | 1.00 | 0.40 | 2.75 | 0.10 |

| 3 | 1.67 | 0.75 | 0.30 | 2.00 | 0.075 |

| 2 | 1.33 | 0.50 | 0.20 | 1.67 | 0.05 |

| 1 | 1.00 | 0.25 | 0.10 | 1.33 | 0.025 |

| 0 | Less | Less | Less | Less | Less |

A total score of less than twelve (12) evidences an unusual degree of risk and a strong reliance of security.

The formula is very dependent on liquidity ratios. Low scores indicate that a close review of the components of working capital is required. Inventory will likely form a high percentage of current assets.

Again the trend is just as important as the actual score.

5.6.5 Comparison between “Y” and “Z” Scores

If the two scores appear contradictory review of each of the components of ratios of the lower score is necessary. The weak ratios should be identified and an explanation of such weakness is to be provided.

If the “Z” score is satisfactory and the “Y” score is not, then review of sales to total assets ratio is necessary. If that ratio and the sales to working capital ratio are high the company is probably over trading.

5.7 Lending Risk Analysis-

In a modern society, banks are uniquely important because of their ability to create money. Lending comprises a very large portion of a Bank’s total assets and forms the backbone of the Bank. Interest on lending constitutes the highest proportion of income of a bank. As such, credit quality remains the prime indicator of a bank’s success. Unsound Credit reduces the ability of a bank to provide credit towards good borrowers and undermine liquidity and solvency. Therefore good lending practice is very important for the profitability and success of a bank.

Lending is a judgment, which depends on the ability to assess the shortcomings in the proposal and identify the risks involved. The ability to take proper and timely measures to minimize the risk is very important for the purpose.

The modern concept of lending has shifted from the security-oriented approach to a business viability one. The emphasis is given on the likelihood of repayment, business viability, management competence and management integrity of the proposed debtor. As the prevailing legal system of the country makes it difficult for the bank to realize collateral, the ultimate security of the bank is the commercial success of the borrower. Adequate emphasis on management and business risks is as such more important as analysis of security risk.

The Financial Sector Reform Project (FSRP) designed a Lending Risk Analysis (LRA) package which provides a systematic procedure for analyzing and quantifying the potential credit risk. Bangladesh Bank has made it mandatory for commercial Banks to use LRA for evaluating credit proposals amounting to Tk. 1.00 Crore and above.

Chapter 6

Creation of Charges on Securities

Creation of charges on securities is an important and essential part of lending process. To make a loan legally sound, charge should be created properly on the security taken and in a lawful manner.

6.1 Security

In simple terms security means things deposited as a guarantee of an undertaking or loan, to be forfeited in case of default. Taking security simply means acquiring a claim on an asset or assets so that, if repayment is not made as planned, the assets taken as security can be realized to obtain repayment. For this, security is considered as insurance against emergency.

Prime Bank Ltd charges two types of securities from its potential borrowers. These are:

Primary Security: Primary security is the purpose for which the credit facility has been provided. The value of primary security is never less than the exposure.

Secondary Security: Secondary security is additional security to cover additional risk.

6.2 Attributes of Good Security

Prime Bank Limited ascertained some attributes that a good security must possess. These are:

Marketability

Easy ascertainment of value

Stability of value

Storability

Low cost of labor and supervision

Transportability

Transferability

These attributes are very important for liquidating the security when necessary.

6.3 Charge

In simple words, charge means establishing legal rights on the property of the debtors so that the creditor can realize such property to repay the loan in case of default.

Types of Charges

Prime Bank Limited exercises two types of charges, which are:

Fixed Charge: It is a charge that is made specially to cover definite and ascertained assets of permanent nature or assets capable of being ascertained and defined, e.g., charges on land and building or heavy machinery.

Floating Charge: It is a charge on a property, which is constantly changing, e.g., stock-in-trade.

6.4 Modes of Creating Charges on Security

Prime Bank Limited creates charges on security by the following method:

Mortgage

Lien

Assignment

Set-off

6.4.1 Hypothecation

Hypothecation is a charge against property for an amount of debt where neither ownership nor possession is passed to the creditor. Though the borrower is in actual physical possession but the constructive possession remains with the bank as per the deed of hypothecation. The borrower holds the possession not in his own right as the owner of the goods but as an agent of the bank.

Precautions Taken by Prime Bank on Hypothecation

The position of the banker under hypothecation is not as safe as under a pledge. The borrower may fail to give possession of the goods hypothecated to the bank, or sell the entire stock or borrows from another banker on the security of the same goods.

This facility is given only to persons or business houses of high reputation and sound financial standing.

The banker periodically inspects the hypothecated goods and the account books of the borrower to ascertain the position of stocks under hypothecation.

The borrower is asked to submit a statement of stock periodically giving correct position about the stocks and its valuation and declaration that the borrower possesses clear title to the same.

An undertaking is taken from the borrower that he would not charge the same goods to some other bank or persons.

A nameplate of the bank mentioning that the stocks are hypothecated to it is displayed at a conspicuous place in the business premise of the borrower for public notice.

Stocks should be fully insured against fire, riot, strike, theft and other risks.

6.4.2 Mortgage

As per Transfer of Property Act-1882, section 58 (a), a ‘mortgage’ is the transfer of an interest in specific immovable property for the purpose of securing:

The payment of money advanced or to be advanced by way of loan

An existing or future debt or

The performance of an engagement which may give rise to a pecuniary liability

[

The transferor is called “mortgagor” and the transferee is called “mortgagee”, the principal money and the interest payment which is secured for the time being are called “mortgage money” and the instrument by which the transfer is effected called “mortgage deed”.

Prime Bank Limited exercises only two types of mortgage which are:

Legal Mortgage: Where without delivering possession of the mortgaged property, the mortgagor binds himself personally to pay mortgage money and agrees expressly or impliedly that in the event of his failing to repay according to his contract, the mortgagee shall have a right to cause the mortgaged property to be sold and the proceeds of sale to be applied so far as may be necessary in payment of the mortgage money, the transaction is called a simple or legal mortgage. But the mortgagee has no power to sell the property without the intervention of the court. Therefore when an interest of the specific property under such mortgage is transferred by registration of deed i.e. mortgage deed is termed as registered mortgage or legal mortgage. However, with the enactment of Money Loan Court Act the bank can now directly sell the mortgaged properties.

Equitable Mortgage: According to section 58 (f) of the Transfer of Property Act, where a person delivers to a creditor or his agent documents of title to immovable property, with the intention to create a security thereon the transaction is called a “mortgage by deposit of title deeds” or “equitable mortgage”.

6.4.3 Lien

Lien implies right of the creditor in possession of goods or securities belonging to a debtor to retain until a debt due from the latter is paid. Lien is different from other forms of charges on the ground that it does not require any specific agreement, written or oral to support it. The right of lien arises in law out of business dealings between parties- the person in possession of the goods of securities and the owner.

6.4.4 Assignment

An assignment means a transfer by one person a right, property or debt (existing or future) to another person. The person who assigns the right, property or debt is called the assignor. The person to whom the right etc. is assigned is called the assignee.

Legal Assignment

Prime Bank Limited practices only legal assignment where:

An assignment deed is in writing duly signed by the assignor and the intention to pass by assignment is very clear.

The transfer of actionable claim is absolute.

The assignee informs the assignor’s debtor about the assignment and also gets the confirmation of the notice and debt.

6.4.5 Set-off

Set-off means the total or partial merging of a claim of one person against another in a counter claim by the latter against the former. It is in effect the combining of accounts between a debtor and a creditor so as to arrive at the net balance payable to one or the other. It is a right, which accrues to the bank as a result of the banker customer relationship.

Ingredients of Set-off

Mutual debts for sum certain

Debts must be due immediately

Debts must be in the same right

No agreements to the contrary

Right of set-off

The decision and judgment in different cases reveal that the following cases where branches can exercise the right of set-off:

To combine two or more accounts of the same customer in the same branch of Prime Bank.

To combine two or more accounts of a customer maintained in different branches of the same bank.

To adjust the surplus amount of the sale proceeds or realization of the securities held as cover for one particular debt for liquidation of any other debt after realization of that particular debt.

Chapter 7

Monitoring Techniques Used

Supervision and monitoring of a loan denotes continuous checking and assessing the borrower, his business and his willingness to repay the loan based on some predetermined manners. Supervision generally starts immediately after the selection of the borrower and monitoring starts when the project/activity enters implementation although these terms are also interchangeably used. Proper supervision and monitoring, act as a substitute of collateral.

7.1 Purpose of Credit Monitoring in Prime Bank

The purposes of credit monitoring are pointed out below:

To prevent loan classification

To return flow of fund

To ensure compliance of terms and conditions

To obtain feedback from the borrowers

To take timely corrective action regarding a particular loan

7.2 Credit Administration as a Tool for Credit Monitoring

To ensure that all security documentation complies with the terms of approval and is enforceable.

To monitor insurance coverage to ensure appropriate coverage is in place over assets pledged as collaterals and is properly assigned to the bank.

To control loan disbursement only after all terms and conditions of approval have been met, and all security documentation is in place.

To maintain control over all security documentation.

To monitor borrower’s compliance with covenants and agreed terms and conditions, and general monitoring of account conduct/performance.

To minimize credit losses, monitoring procedures and systems should be in place that provides an early indication of the deteriorating financial health of a borrower.

7.3 Risk Grading as a Tool of Credit Monitoring

The system should define the risk profile of borrower’s to ensure that account management, structure and pricing are commensurate with the risk involved. Risk grading is key measurement of a Bank’s asset quality, and as such, it is essential that grading is a robust process. All facilities should be assigned a risk grade. It is recognized that the banks may have more or less risk grades; however, monitoring standards and account management must be appropriate given the assigned Risk Grade.

7.4. Corrective Measures

When it becomes inevitable to face an adverse situation regarding a particular loan, Prime Bank Limited takes corrective measure to mitigate the situation as much as possible. The following corrective measures are taken in this regard:

Reviewing the documents and situation from legal point of view

Working out strategy and action to face the problem

Loss is evaluated against the security realization value

Deciding on whether to stay or leave the project and reclassification is done accordingly

Visiting the client continuously to find any way out

Then all efforts are put forward for negotiation

Ultimately legal actions are taken when all measures fail

7.5 Loan Monitoring Through Continuous Reporting

Prime Bank Limited also monitors its credit portfolio through continuous reporting to Bangladesh Bank. For this purpose Bank uses six forms (CL-1, CL-2, CL-3, CL-4, CL-5 and CL-6) in accordance with the nature of loan and advances.

Cl-1 is the compilation of the 5 other reports which covers different loan categories including the staff loan.

CL-2 is used to report continuous loan.

CL-3 is used to report demand loan.

CL-4 is used to report for loan repayable within maximum 5 years.

CL-5 is used to report term loan of over 5 years.

CL-6 is used to report short term agricultural loan.

Chapter 8

SWOT Analysis

Every organization over the years of its operation generates some strength and some weaknesses which are solely internal and not dependent on the externalities. Opportunity and threats are on the contrary out of control of an organization and are thus absolutely external. Prima Bank Limited has many things to its credit as strengths while like any other bank has some weaknesses. Prime Bank Limited always is abreast of the market trend and proactive to adopt any market changes and explore opportunities.

8.1 Strengths

Superior quality: Prime Bank Limited is a bank with a difference and is committed to maintaining a positive difference from its peer bank. This is reflected in all its activities and services offered. All the employees bear this slogan in their hearts and this is manifested in their behavior with the customers.

Prime Bank Limited has a very well educated and professional management. All the Directors of the bank are highly qualified and eminent business personalities of the country. This is one of the most distinct competitive advantages of the bank.

Dynamism: Prime Bank is always ahead of its competitor bank in different innovative policy implementation. Prime Bank has pioneered various lending policies that were subsequently incorporated by other banks.

Wide coverage of the bank with its 67 branches across the country has broadened the horizon of its service. This increased network of branch has strengthened its position in the industry.

Prime Bank Limited is a sister concern of Prime Finance & Investments Limited, Prime Insurance Limited and Prime Islami Life Insurance Limited. This has helped the bank build a brand image and to differentiate easily from other banks.

All the levels of the management of Prime Bank Limited are solely directed to maintain a culture for the betterment of the quality of the service and development of a corporate brand image in the market through organization wide team approach and open communication system.

The key contributing factor behind the success of Prime Bank Ltd is its employees, who are highly trained and most competent in their own field. The bank runs a training institute which organizes training on all areas of banking operation throughout the year to upgrade the performance of its employees.

Excellent Working Environment: Prime Bank Limited provides its workforce an excellent place to work in. Total complex has been centrally air-conditioned. The interior decoration was done exquisitely with the choice of soothing colors and blend of artistic that is comparable to any overseas bank.

8.1.1 Strength related to Credit operation:

Huge Capital Fund: Prime Bank Limited has a capital fund of Tk. 247.61 crore as on 31.12.2008 with paid up capital being equal to Tk. 100.00 crore. Practically this is the second largest bank in the private sector in terms of capital fund and is next to Islami Bank Bangladesh Limited. This huge capital fund has increased the business power of the company as the maximum amount of loan that can be disbursed to a single customer or group depends on the capital fund. This is because no bank can give funded facility more than 15% of its capital fund to a single customer as per central bank directive which was done to avoid concentration of credit and risk exposure.

Delegation of Credit sanctioning authority: Unlike many other banks Prime Bank Limited believes in the authority delegation among the executives of the bank depending on the hierarchy. The bank has authorized its executives and branch managers to sanction and disburse loans depending upon the security offered by the customer. This has improved the processing of loans and accelerated credit approval. Customers do not have to wait for long time indecisively. This faster service has been successful to address the immediate fund requirement of the customers.

Segregation of Corporate division from the credit risk management and credit Administration unit: The Bank in line with the Bangladesh Bank directive has segregated credit risk management unit from credit administration and sanctioning unit. Corporate division functions as the credit marketing unit and sends the potential lending proposals to the credit risk management unit where the lending proposals are meticulously scrutinized to judge the financial feasibility and repayment capacity of the customer. Credit administration unit monitors the repayment of the loans and supervises documentation. This has helped to improve asset quality of the bank and reduce default loans.

Involvement of high caliber young personnel: Prime Bank believes in the power, speed and capacity of younger generation. The bank has thus involved very young and promising young in its credit operation. This people with great analytical ability and speed have significantly bettered the credit processing.

Sectoral Allocation of Credit: The Board of Directors of the bank has put the ceiling on the amount of loan that can be sanctioned in a single industry. This has great significance as the bank loan is diversified among different industries. So the possibility of failure due to down turn in any industry is low.

Efficient Fund Management: The treasury department of the bank is very skilled in fund raising in terms of matching the maturity of its deposit and loans. The bank takes deposits with the minimum interest rate to maintain the spread.

Emphasis on Small and Medium Enterprises: Small and Medium Enterprises are expected to be the growth engine of the economy of all developing countries in the near future. This is because these countries suffer from lack of sufficient investment capital and technology to compete with the developed countries. Prime Bank Limited eyeing the opportunities for growth in the sector has formed a special small and medium enterprise unit. This unit takes care of all investment proposals under the head of SME finance. These customers are highly remunerative as they not tough bargainers and stay loyal to the bank. And the possibility of bank’s failure due to default is less.

Augmented focus of Retail Credit: Since all the big customers are highly price sensitive they are not highly remunerative to the bank. Prime Bank has formed a retail credit unit to look after the retail credit aimed at increasing the living standard of the people. The bank is trying to inflate the retail credit portfolio. Although the possibility of default is to some extent higher retail credit is remunerative. Again the possibility of bank’s failure is low.

8.2 Weaknesses

Non-availability of ATM Booths: Prime Bank Ltd has installed ATM machines, but the number of ATM booths is very few. Though PBL customers can use DBBL ATM booths for transactions but still Prime Bank Ltd should increase the number of their own ATM booths.