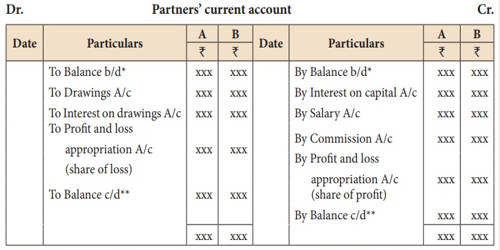

Fluctuating Capital Account of Partners

Fluctuate means anything having unpredictable ups and downs. Under this method of keeping partners’ capital account, only one capital account of partners is opened. This account will record not only the original capital contribution but also the transaction between the partners and the firm. It includes partners’ drawings, commission, interest on capital, bonus, salary to partners and so on as the case may be. Each partner will have his separate capital account, which will be credited by his initial investment and any additional capital introduced during the year will also be credited to his capital account.

When the capitals of partners are fluctuating, all adjustments with regards to the interest in capitals, interest on drawings, partners’ salaries, etc. are passed through the capital accounts of the partners. This account is fluctuating whenever there is a presence of any transaction influencing the concerned account. All the adjustments leading to a decrease in the Capital are shown on the Debit side of the Capital Account. It is that method of keeping the account of the partners in which the capital in the account of the partner keeps fluctuating. For example, Drawings by Partners and interest comes on the debit side of the Capital account. All the adjustments leading to an increase in the Capital are shown on the Credit side. The balance of each partner’s capital account will be shown in the balance sheet. The debit balance of a partner’s capital account is shown on the asset side and credit balance is shown on the liability side.

Fluctuating capital account method is usually preferred by partners; however, they can also use fixed capital account according to their business and preference. Whenever there is a system of fluctuating capital account no maximum limit can be put on the partner’s drawings as is maintained in the fixed capital account system.

Characteristics –

- Two accounts are prepared: Capital Account and Current Account,

- The capital balance remains unchanged,

- Both Capital and Current Accounts appears in the Balance sheet,

- If this method is used then it must be specified in the Partnership Deed,

- Fixed Capital Account will always show a Credit Balance.