EXECUTIVE SUMMARY:

Banks are the financial institutions that play a very useful and dynamic role in the economic life of every modern state. Banks support industrial developments, business expansion job creation etc. Banks accept deposit from public and private loans to them. The spread between the interest of loan and deposit is bank’s profit. There are various types of Bank in our society. There are nationalized, many private commercial, specialized etc. The commercial Bank’s are playing role in the economic development of the country the nationalized commercial Bank’s role is not less important. The services of International Finance Investment and Commerce (IFIC) Bank include Corporate banking Retail banking and Consumer Banking spread over from industry to agriculture, and real state to software. This bank HRD department is well decorated and thousands of book available here. The IFIC bank life history is comparatively long from others banks. The IFIC has formulated General Loan Scheme, Car Loan, Easy Loan, Flexi Loan, Thikana Loan, Cash Credit loan, Peshajibi Loan, Possession Loan, Lease Finance, and Small & Medium Enterprise (SME), Consumer Credit Scheme, Hire Purchase, etc. The General loan schemes are applicable to individual/firm/industries for a specific purpose but for a definite period and generally repayable by installments. The Lease financing is one of the most convenient long-term sources of acquiring capital, machinery and equipment. To more facilities IFIC Bank expansion service area. They are doing many types of bill collection, bill payment, locker service Q-Cash service. Another point is IT section of IFIC Bank. There are introducing foreign exchange department. To doing foreign exchange business following different types of L\C. IFIC bank are doing cross-sectional function with banks and financial institutions abroad.

IFIC Bank follows some credit principles at the time of extending credit. These are safety, liquidity, and purpose of loan, security, and loan repayable on demand & invest in several sectors. At the time of pricing a loan, the cost of fund, administrative expense, cost of capital and risk is considerable.

INTRODUCTION

Origin of the report:

The report has been prepared under the internship program at International Finance Investment and Commerce Bank LTD as a requirement of MBA program of Department of Finance The Millennium University.

Background of the problem:

The whole study has been conducted in the perspective of operation of the 1st generation banks which joined the banking sector dominated by NCBs in Bangladesh are putting mixed performances. Some banks have kept themselves competitive while others made way for the multinational and recently established local banks. IFIC Bank LTD is one, of the broad based banking company in Bangladesh. It has as many as 90 branches in Bangladesh and overseas. To know exactly how the bank is performing from almost 25 years after its establishment is what led this study take place.

Purpose:

The purposes of this report cognates the internship purpose. The internship objective was to gather practical knowledge and experience the corporate working environment with the close approximation to the business firm and the experts who are leading and making strategic decisions to enhance the growth of a financial institution. To this regard this report is contemplating the knowledge and experience accumulated from internship program. With the set guidelines and report by the Faculty of Business of The Millennium University. and with the kind advice of both the Organization and Internship Supervisor this report comprise of an organization part and a project part.

Objectives:

The principal objective of the study is to understand how exactly this particular bank is doing in an ever changing and competitive banking industry. Apart from that, objectives were to have an understanding about performance of the 1st generation banks which have not been able keep themselves so competitive but still remain profitable. To have anticipation about the future prospects of the bank is another of them.

Methodology:

It needed information and data of various subjects and sources. To meet such requirements frequent visits to executives of IFIC Bank ltd has been Made. In addition to that, discussion with the employees of the bank, particularly, Choumuni Brach, Begumgonj, Noakhali different records of the branch were analyzed besides day to day activities.

Data collection

Mentioned below are the sources from which information were collected in

preparing the report on general banking operation of IFIC bank LTD.

Primary Sources

• Interview with executives of Choumuni Brach, Begumgonj, Noakhali and Loan advance & loan Department, Head Office IFIC Bank ltd.

• Observation while working in Choumuni branch as an intern.

Secondary Sources

Secondary sources played a great role in the study. There were various sources like:

• IFIC annual reports from 2003 upto 2008.

• Profile of IFIC Bank LTD.

• General Banking operation.

• Other necessary literature.

• Profile of different dimensions

Data analysis

Data were analyzed to find out the state of performances put by the bank which is quite subjective. Qualitative information were first analyzed through different process to figure out indicators.

scope:

the report ranges from an overall introduction of this particular bank to the project part which concentrates on how well the bank has been operating for last 3 years.

Limitations:

Like many organizations in Bangladesh, information are not well structured in many cases and some important information were not accessible due to confidentiality excuses. Moreover bank officers are quite, busy with their own work & lack of combination so sometimes observations and to some extent assumptions were needed. Dealing with qualitative data creates limitations due to their subjectivity.

Suggestions:

The report would feature a part providing some recommendations to do better and explore opportunities in the future. Though easier said than done the bank is not doing up to it’s potentials. Some suggestions have been made.

Activities

Choumuni Branch, Begumgonj, Noakhali, IFIC Bank LTD

History of IFIC Bank Limited:

2.1 The IFIC Bank, what you see today, came into existence in 1976 as a Finance Company under the name and style International Finance and Investment Company Limited (IFIC). IFIC was incorporated as Public Limited Company on 8′h October 1976, with an Authorized Capital of Tk. 20 core and a Paid up Capital of Tk 10 core. IFIC commended its operation on 28th February, 1977 with an Issued and Subscribed Capital of Tk. 5.00 core, contributed

by leading private sector entrepreneurs in the country; six international banks and two state owned financial institutions namely Bangladesh Shilpa Bank and Bangladesh Shllpa Rill Sangstha. Mr. Jahurul Islam was elected the first chairman of the Board of Directors of IFIC.

IFIC was established, at the instance of the Government, with primary objectives of carrying on banking business abroad through subsidiaries, affiliates and branches and investment ancl financial business in the country.

IFIC, in pursuit of its objectives, explored possibilities for establishing presence in Hong Kong, Malaysia, Maldives and several other countries. Out of which prospects in Malaysia and Maldives looked particularly in the share capital with limited management control, in one of the existing bank. Simultaneously dialogue was established with the Government of the Republic of Maldives for setting up the country’s first national bank with IFIC participation in the capital and its managing Bank for them for a specific period. Negotiations with Malaysia failed at a matured stage over the price of shares offered to IFIC. Negotiations with the Government of Maldives were successfully concluded. Cumulating in the establishment of the country’s first national Bank namely the Bank of Maldives Limited. IFIC took 40% of the equity of the Bank of Maldives Limited, with the majority 60% being subscribed by the Government of the Republic of Maldives and other Government Agencies.

Under an agreement, management was vested in IFIC. The Bank of Maldives limited, managed by senior officials seconded by the president of Maldives. The Bank of Maldives Limited, under the stewardship of IFIC has made commendable progress, establishing itself as the dominant Bank, in face of competition from four foreign banks operating in the Country. The Bank started earning profit from the very first year of its operation and opened another three more branch and one exchange booth in the same year.

During the meantime in May 1979, IFIC secured permission of the Bangladesh Bank to providing the following additional services.

function as a Merchant Bank in the country;

1. Accepting deposits generated out of remittances by wage earners abroad.

2. Accepting foreign currency deposits.

3. Opening import letters of credit under Wage Earners Scheme.

- Extension of credit facilities covering imports under Wage Earners Scheme.

IFIC started extending above mentioned Merchant Banking services creating a favorable impact in the market, building up a satisfied clientele, sound reputation in the international banking field and above all increasing its profitability manifold.

In 1980, the Government took a decision to allow establishment of Banks in the private sector. In pursuance of this decision, private sector sponsors of IFIC decided to approach the Government for changing the character of IFIC from that of a finance company and Merchant Bank to that of a full fledged Commercial Bank on fulfilling the conditions laid down in this regard.

On negotiation with authorities it was decided that.

01. IFIC will become a full-fledged Commercial Bank under the name and style International Finance and Investment Company Limited.

02. IFIC Bank would be sponsored by the existing Private Sector Share Holders/Directors with the Government retaining a minority share.

03. Capital will be restructured with an Authorized Capital of ” Tk. 10 core and Paid up Capital of Tk 8 core to be subscribed as under:

| Private Sector Sponsor | 508 i.e. | Tk. 4.00 core |

| General public | 108 i.e. | Tk 0.80 core |

| Government of the Peoples | 408 i.e. | Tk 3.20 core |

| Republic of Bangladesh | Tk. 8.00 core |

04. IFIC Bank in addition to conducting commercial banking would continue to pursue its objectives of establishing, subsidiaries, affiliates and branches abroad.

IFIC on receipt of necessary permission, and on restructuring & complying with necessary formalities emerged as IFIC Bank on 24th of June 1983.

IFIC Bank did not have to look back since then, but forged ahead creating a niche for itself in the banking scenario both in the country and aboard. IFIC Banks deposits which stood at Tk12.88 core at the end ’83 increased to Tk 2990 core at the end of 2007. The Banks profit which was Tk 1.30 core in ’83 increased to Tk 113.09 at the end of 2007.

IFIC Bank within a short span of its existence has earned a reputation for the quality of its services and its name is taken with respect by the banking public and with reverence by its competitors. Pursuing its objectives the IFIC Batik, has established an affiliate exchange company in the Sultanate of Oman in June 85 currently named Oman-International Exchange Company LLC.

The Exchange Company in Oman, managed by officials seconded from IFIC.’, is channeling substantial foreign exchange remittances to Bangladesh and commenced earning profit in the very first year of its operation. IFIC Bank is actively exploring possibilities of establishing a branch in Italy and affiliates in USA, UK and other places.

Meanwhile the Bank has already established a Joint Venture with Nepali Sponsors which is called NBBI, (Nepal Bangladesh Bank Limited). Currently 17 branches are operating in under the name of NBBL. IFIC Bank today has 30 affiliates abroad and 70 branches in the country, with 4 more branches to be established shortly. The IFIC family on date consists of 1996 members.

Employee Profile:

All the divisions are headed by vice president (VP) Senior Vice President (SVP) or First Vice President (FVP). The branches of IFIC headed by Senior Vice President (VP) or office dependent on the gradation of the branch.

The main strength for any service organization is it’s efficient and experienced personnel,. In banking sector, customer’s perception about the bank is dependent on the service and performance of the personnel. Therefore the presence of well-educated and trained personnel plays the vital role of business for any commercial bank. IFIC Bank tries to give best service to it’s clients. That’s why IFIC sets appropriate personnel for appropriate place and position. The personnel are educated, skilled and with wide experience in banking sector.

Total manpower stood at 1883 as on December 31, 2005. Out of them 1301 were officers and 582 were staff. The no of female employees at the date were 205.

Year | Total |

1995 | 1565 |

1996 | 1549 |

1997 | 1614 |

1998 | 1624 |

1999 | 1659 |

2000 | 1700 |

2001 | 1737 |

2002 | 1755 |

2003 | 1868 |

2004 | 1895 |

2005 | 1990 |

2006 | 2014 |

2007 | 1997 |

Functions:

- Provide banking service to common people through the network of branches.

- Mobilization of savings of the people and safe all types of deposit account.

- Makings advantages, especially for providing activities and generally for other commercial and socioeconomic needs.

There are two types of basic functions, which are deal in the banking business in this branch. For each type of Function there is an individual department. The departments are as follows:

- General Banking Department.

- Loans and Advance Department.

General Banking Function:

General banking division is the most important point of all activities. It is the storage point for all kinds of transaction of foreign exchange division, loans and advance department and itself.

General banking department is generally deals with the following sections

- Deposit section

- Bill Section

- Cash section

- Accounts Sections

- Dispatch Sections

- Administrative Section

Bill Section

The bill section can be discussed by the following topics:

One of the most important aspects of commercial banks in rending services to its customer.. One of the most important aspects of commercial banks in the rending service to its customers..

Considering the urgency and nature of transaction, the mode if bank remittance may be categorized as:

- Demand Draft (DD

- Telegraph Transfer (TT)

- Payment Order (PO)

Demand Draft (DD):

At first the customer has to submit an application to get the DD from. Then the customer has to fill up the form about the requirement with the code number of receiving bank. In case of issuing DD serial number is important both the receiving and the payment bank. DD payment can be made with advice or without advice. For blanching the bank account individual advice is given for the each DD.

Telegraphic Transfer (TT) :

A telegraphic transfer is a method of remittances, which is effected by the bankers through a code telegrams attested by secret check single on receipt of which the paying office pay the amount to the payee by his account. The TT commission was calculated as per BB (Bangladesh Bank) rate min TK. 257- and telex charge to be taken from customer is TK. 307- per minute.

Pay Order (PO):

A pay order that contains an order to pay for a specific amount. It is an instrument for the bank. In the beginning stage PO was issued only to effect local payment of banks own. But at the present it is issued to the customer the can purchase to deposit as security money or earnest money. It earns payment to the payee as the money deposited by the purchaser of PO is kept in bank own a/c named “Payment Order A/C”. Payment of this instrument to be made form the branches it has been issued. It is not transferable.

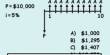

Charges of Issuing of Payment Order:

| Range (TK) | TK (charge) |

| Up to TK. 1000 | 10 |

| Above TK. 1000 to 10000 | 25 |

| Above TK. 10000 to 50000 | 50 |

| Over TK. 50000

| 100 |

Bill collection:

This Bank the bill collection is some type. By the following topics:

- Issuing bill / DD, Pay order,

- Clearing

- Transfer and Delivery

- OBC and IBC (Out of bills collection and Inward bills collection)

Issuing bill:

There are two types of remittance:

1. Inward

2. Outward

The commercial banks Remittance facilities to its customer to enable them to avoid risk arising out of that or loss in carrying cash money from one place to another place. Banks take the risk and ensure payment to the beneficiary in exchange of a little benefit as exchange or commissions.

Clearing:

Under this type of transaction the dept which arising among the different banks with in the clearing are settled systematically. Clearinghouse of Bangladesh Bank where they’re the agent of different bank sit and performs this task.

Transfer:

Transfer with the same bank of different branches with in the clearing areas. In

the purpose the dept arising out of different branches of the same banks are

settled systematically through and delivery.

OBC & IBC (Outward & Inward Bill Collection):

This is the transaction out side the clearing are and the debts that arise for transaction among the different branches of different banks are settled through outward and inward bill collection.

Cash section:

This is an important section perform very vital role in the banking business. Main task of this section is receiving and payment of cash to the customer. For daily. transaction branches office bring necessary amount form the head office through a requisition from signing both the desk office and the manager of general banking department.

Account section:

Account section is the of any bank for the transaction that occur m everyday during the banking period of all those transaction re to maintain a balance and account section maintain all of those accountability. Although cash section maintains account in the computer for which \they use software named Bexi Bank & Mysis. Every though they are to maintain some ledger book.

General banking Service:

- Cash deposit and withdrawals

- Cash Deposits

- Fund transfer

- Checkbooks requisition

- Account statements

Types of deposit accounts are mainly operated in the bank are as follows:

- Current Deposit Accounts (CD)

- Savings Deposit Accounts (SB)

- Short Term.’ Short Notice Deposit Accounts (STD, SND)

- Fixed Deposit Receipt (FDR)

- Cumulative Deposit Account (PSS / DPS / MSS/ APS etc)

Types of Account Holders:

- Individual

- Joint Accounts

- Trading Concern-

a) Accounts of proprietary concern.

b) A/Cs of Partnership Concern:

c) A/Cs Limited Companies

d) Accounts of Liquidations

- Specials Types of Accounts:

- Illiterate person

- Married women

- Pardanishin Women

- Lunatic person

- Drunker

- Insolvent Account

- Blind person

- Official Receivers Account

- Attorney Account

- Minor Account

- Executor / Administrator

- Trust Account

05. Officials Accounts:

- Accounts of Government

- Corporation

- Autonomous bodies

06. Non Trading Concern:

- Accounts of Clubs, Societies

- Institution Accounts

A current account is a running and active account. Holder of such account can freely deposit or withdraw money as many times as he feels necessary in a working day.

Current deposit are parts of Demand Deposits: The special Characteristics of such accounts are as follows:

- Minimum amount for Current deposit: Current Deposit Accounts shall be opened with a minimum of Tk. 2.000/= (Case varies from bank to bank)

- Interest and Incidental Charge:

- Interest on balances of current deposit accounts shall not be allowed (exceptions are there)

- Incidental charges prescribed by bank from time to time shall be realized from current deposit accounts having minimum balance below Tk. 2000/= during last 6 (SIX) months of each half yearly closing. charges is Tk. 150/=

- Closing charges prescribed by bank– shall ‘ be realized at time of closing down of a current deposit account, our bank– charge is Tk. 200/=

- Loan facilities on Current Account : The account holders enjoy certain privileges compared to the saving account holder CD account holder provided overdraft facilities.

40. It is for business only: A account may be an individual firm, Company, club association or a body corporate after duly meeting all the formalities. Since it is assumed to be a business account, banks discourage opening of current account for non business purpose.

05. According to BRDD circular no. 01 dated 04.10.2001 in case of individual or joint name account selection of nominees is must. Nominee’s death of the proposed depositor shall be selected by the depositor.

Savings Bank Deposit Accounts:

- Minimum amount for Savings Deposit Accounts: Savings Deposit accounts shall be opened with a Minimum of Tk. 1,000/=

- One account in One name: Not more than one account may be opened in one name by an individual.

- Interest applied: A11 accounts are to be made up-to-date before half yearly- closing and interest accrued there on shall be added to the respective balances at the rates as advised by the bank– form time to time.

- Withdrawals are subject to Restrictions: Withdrawals from Savings Bank account twice a week up to a maximum of 25% of balance which can be made with prior notice (i.e. 7 days notice) otherwise customer has to forgo interest for that particular month.

- Chequing facilities: Up to 1987 there were savings accounts with both chequing and non chequing facilities. Currently, however all savings accounts are entitled to have cheque facilities.

- Nature of Liquidity : Conceptually savings accounts are supposed to be liquid in nature. But because of restriction in withdrawal as per central banks instruction only 10 percent of savings deposits as demand liabilities and the rest 90 percent is treated as time liabilities.

- Bank Discretion:

- The bank at its discretion may realize a sum of Tk.100/- for each cheque returned unpaid for the reason of insufficient balance.

- Stop issuance of new cheque book or any form to a customer, without assigning any reason.

- Close the account.

- Non Overdrawing: No savings bank account shall be allowed to be overdrawn.

Short Term Deposit Account (STD) :

- The deposit held in’ these accounts shall be payable on short notice.

- Minimum amount for STD Accounts: STD account shall beopenedwith minimum balance of Tk. 25,000/= only.

- Interest is lower: The rate of interest in such types of deposits is lower, because the bank holds the fund for a short notice.

- Suitable for Corporation: Such accounts are suitable for the firm/corporation / public bodies etc., Which have excess fund for their disposal for a short time. They earn some interest out of this.

- High Liquidity: These types of deposits are highly liquid in nature, though not equivalent to the liquidity of the current account.

Fixed Deposit Accounts:

- Period of Fixed Deposit: Fixed deposit shall be opened for a fixed period, verifying a from 3 months to 3 years or above and are payable at a fixed date of maturity. In our bank we prefer filed deposit far a period of 1 month. 3 month, 6 month & 1 year.

- Rate of Interest: Interest on filed deposit accounts shall be paid at rates fixed by bank from time to time, depending on their period of maturity. As the duration increases, rate of interest also increases.

- Payment of interest:

a. Interest shall be calculated at maturity N.-here the period of maturity is one year or less.

b. Where the maturity of a deposit exceed one year. interest shall be calculated at the end of its anniversary.

c. The depositor will have the option to with draw interest so accumulated or may leave the interest with the principal to be compounded.

- Separate Contract: Each time a fixed deposit account is opened, it shall be considered as a separate contract and various in the name of the members of the same amount shall be treated as one deposit.

- Withdrawal of money through FDR is restricted.

- Fixed Deposit receipt is not a negotiable instrument.

- Premature Enmeshment may be allowed.

- Time liability: Fixed deposits are treated as the time liability of the banks.

09. Loan can be availed: Against FDR loan may be granted as per rules of the Bangladesh Bank.

Deposit Pension Scheme / Pension Savings Scheme (PSS):

- Pension Saving Scheme (PSS) account may be opened in the name of individual, name of Bangladesh National who have attained at the age of 18 years.

- Opening of joint account under the scheme is not permissible.

- A depositor under the scheme would be required to deposit minimum Tk. 500/= minimum of Th. 5000/= per month for a period of 3 years and 5 years.

- There shall be maximum of 4 accounts (Tk. 500/-, Tk. 1000/-, Tk. 2000/- and Tk. 5000/-) may be opened in the name of the same person.

- On completion of subscription period, the depositor would be entitled to receive the accumulated amount together with accrued interest thereon as per rule in the lump sum or to receive pension in monthly installments for a period ranging 6 years to 10 years.

Findings:

Opening of Account is a way to establish relationship between Banker and customer. On satisfaction of its requirement and verification of geniuses and with proper introduction it may open Account. A person who competent center into contract can open Bank Account. It should be very careful In selecting our customer. Before opening an account it must satisfy ourselves about the identify and other details of the proposed account opener. This is essential so that no fictitious person, incapable of making a valid contract opens an account 04th the Bank.

Type of Accounts :

The Bank allows its customers to open various types of deposit Accounts. These are as follows :

- Current Deposit Account.

- Savings Deposit Account.

- Short Term deposit Account.

- Fixed deposit Receipt.

- Pension Savings Scheme Account.

- Bearer Certificate of Deposit.

- Wage Earners’ deposit Account.

- Special purpose deposit Account.

- Monthly Income Scheme deposit Account.

- Cheque card deposit Account.

- Restricted (Blocked) deposit Account.

Types of Account Holders:

It open bank accounts an different types or accounts holders as mentioned below:

- Individual.

- Joint Account.

- Proprietorship Account,

- Partnership Account.

- Private. Limited Company Account.

- Public limited Company Account.

- Trustee Account.

- Liquidators Account.

- Executors/Administrator Account.

- Clubs/Associations/Societies Account.

- Co-operatives Accounts.

- Non-Govt. Organizations Accounts.

- Accounts of Local Bodies, Municipal Corporation, District Councils etc.

To meet the requirement of law, we obtain an introduction from a respectable person known to the Bank or by a person having already duly introduced Account with the Bank.

Why Introduction in opening New Account?

- Legal protection of a Banker.

- Precaution against fraud.

- Safeguard in case of inadvertent overdraft.

- Absolve the Banker from the charge of negligence of duties.

- Introducer helps to obtain confidential opinion on the customer.

System & Procedures for opening Account:

The following System & Procedures to be completed while opening of Account:

- Filling of Account opening Form.

- Submission of photograph of opener.

- Submission of photograph of Nominee.

- Signature on Account opening Form with date and Signature on Specimen Signature card signed by the opener.

- Signature of Nominee an the Nomination From.

- Introduction on Account opening Form.

- The signature of Introducer to be verified by Authorized Officer before of opening of Account.

- Submission of required documentation’s.

- Signature of the Account holder on the specimen Signature card to be admitted by the authorized Officer.

- Manager’s, Authorized Officer approval for opening Account.

- Account opening Form shall be pasted in a File in numerical order.

- The Specimen Signature Card shall be placed in the card Box in numerical order under control of an authorized officer and to be scanned in the Computer for record/reference,

- Letter of thanks to be sent to the Account holder and to the introducer on Bank’s Standard Form.

Documents required for opening Accounts:

Submission of required documents is a must for opening any types of Account. Requirement of document will vary depending on type of Accounts and account holders.

Individual Account:

The following individuals can open Bank Account,

- Private Individual single or Joint Account.

- Married Women.

- Illiterate person.

- Pardanashin Lady.

But we can not open Account of

- Lunatic

- Person Of unsound mind.

- Bank rupts.

Any individual of 18 years Age Irrespective of sex, caste, creed and religion can open Savings or Current Accounts on submission of following documents.

- Duly filled In Account opening Form with date and Signature on Specimen Signature card.

- Passport size photograph of opener and Nominee.

- Passport or Voter Identify Card.

- Word Commissioner certificate.

- Tax Identification Number (TIN)

- Duly filled in KYC (Know Your Customer) Information Sheet & Transaction profile (TP).

Joint Account :

More than one person can constitute joint Account. Requirement of documents for opening Joint Accounts is as follows:

- Duly Filled in Account opening Form with date and Signatures on Specimen signature card with joint signature.

- Passport size photograph of joint Account openers & their nominee.

- Passport or voter identify card of each person.

- Ward Commissioner certificate of each person.

- Tax Identification number of each person.

- Account operation Instruction “Either or Survivorship”

- Duly filled in KYC information sheet & Transaction profile.

Solo Proprietorship Firm.

A business or trading concern owned by a single adult person is sole Proprietorship concern. Requirement of documents for opening sole Proprietorship Account is as follows :

- Dully filed in Account opening Form with date and Signature on Specimen Signature Card.

- Passport size photograph of the proprietor of the firm and nominee.

- Upto date trade license.

- Passport or Voter identity Card.

- Tax identification Number.

- Certificate from Chamber of Commerce.

- Duly filled in KYC & TP.

Partnership firm :

A business concern owned and managed by more than one person is called partnership firm. The persons who have entered into Partnership business are called partners and the name under which the business is carried is called Partnership firm. Requirement of documents for opening Partnership Account are:

- Duly filled In Account opening Form with date and Signature on Specimen Signature Card.

- Passport size photograph of the partners operating the Account and photograph of nominee.

- Partnership deed duly notarized / registered.

- Passport or Voter Identity Card.

- Tax Identification Number.

- Certificate from Chamber of Commerce.

- Partnership letter signed by all the partners of the firm.

- Instruction letter for operating the Account signed by all the partners.

- Duly filled in KYC of each Partner TP.

Private Limited Company Account:

A corporate body formed and registered under companies Act with limited members and liability having certificate of Incorporation issued by Registrar of Joint Stock Companies is called Private Limited Company, The minimum number of share holder for constitution of Private Ltd. Company is 02 (Two) and Maximum number is 50 (Fifty).

Requirement of documents for opening Private Limited Company Account are:

Duly filled In Account opening Form with date and Signature on Specimen Signature Card.

Passport size photograph of the Directors operating the Account.

Resolution of Board of Directors for opening and operating the Account.

Certified copy of Memorandum of Association of the Company.

Certified copy of Articles of Association of the Company.

Certificate Of Incorporation Issued by the Registrar of Joint Stuck Companies.

Upto date list of Directors.

Certificate from Chamber of Commerce.

Tax Identification Number.

Duly filled in KYC of each Directors & TP.

Public Limited Company Account :

A corporate body formed and registered under Companies Act with limited liability of the share holders and with no upper ceiling of shareholding having both certificate of incorporation and certificate of commencement issued by the Registrar of Joint Stock Companies is called Public. Limited Company. Minimum number of Member is 07(Seven) the there is no restriction an maximum number in case of Public Limited Company.

All the document required for opening Account of Private Limited Company will be required for opening Account of Public Limited Company.

In addition to the above mentioned documents for opening of Public Limited Company Account, Certificate of commencement will be required.

Trustee Account:

A trustee 4s a person to whom confidence Is reposed by law. Trustee is given control of an estate, usually of the deceased, for the benefit of persons who are called beneficiaries.

For opening Trustee Account the following documents are essential.

1. Trust Deed.

2. Instruction letter for operating of trustee Account as per deed.

Minor’s Account :

A person who has not yet completed 18 years of Age is called Minor.

According to law of contract minors can not open Sank Account. But as per Negotiable Instrument Account, 1881 minors can negotiate negotiable instruments i.e. cheque, Bill of exchange or promissory note.

As such, Minors are allowed to open Savings Accounts in the following way:

(a) In the name of Minor himself.

(b) In the joint name of the minor and his/her legal guardian,

c) In the name of “ABC natural guardian of X”

In addition to the required documents tile following documents must be obtained for opening of Minors Account. .

1. Birth certificate of Minor.

2. Record of deed of the guardian of the minor.

Accounts of illiterate persons:

We may open any Account of an illiterate person if lie Is a major.

In addition to other required documents the following procedures to be followed for opening Account of an illiterate persons.

- Thumb impression of the illiterate to be obtained on both Account opening form and Specimen Signature Card.

- Identification marks of the Illiterate to be noted in Account opening form & Specimen Signature Card under authentication at authorized officer.

- Terms & conditions of the Account opening to be explained to him.

- Photograph or the Illiterate person to be replaced by new one after reasonable period.

- Letter of undertaking to be obtained from the Illiterate person to the effect that withdrawals from the Account to be allowed only when he personally visit the branch and put his thumb impression in presence of an authorized officer.

Accounts of Clubs and Societies :

Before opening any Accounts in the name of Clubs and Societies, other than the required documents we also obtain the following documents.

- Laws and Bye Laws of Clubs/Societies.

- List of office bearer.

- Registration certificate of Clubs/Societies (if any).

- Resolution of Board / Management Committee of Clubs/Societies for opening and operation of such Account.

SWOT Analysis

Strengths:

- IFIC is very ancient bank in banking sector, they builds strong reputation in time.

- The top management of the bank, the key strength for the IFIC has contributed heavily towards the growth and development of the bank.

- Strong network through out the country and provide quality of service to every level of customer.

- IFIC has been founded by as group of prominent entrepreneurs of the country.

- The corporate culture of IFIC is very much interactive compare to our other local organization.

Weakness:

- Advertising and promotion is one of the weak points of IFIC . IFIC bank does not have any effective plan for aggressive marketing activities.

- At the entry level and mid level officers experience considerable low remuneration packages that some other local banks.

- There are a very little practicing tools for increasing motivation in the workers by the management.

Opportunity:

- IFIC can pursue diversification strategy in expanding its current line of business.

The management can consider options for starting merchant banking or diversity in leasing and insurance. By expanding business portfolio, IFIC can shrink business risk.

- The credit facility offered by IFIC has attracted security and status conscious businessmen and with as service holders with higher income group.

IFIC should move towards the On-line banking operations. It is high time that they should go for this because some banks are already in to the On-line banking operation.

Enter new markets or segments.

Expand product line to meet broader range of customer need.

Threats:

The Central Bank exercises street control over all banking activities in local banks like IFIC. Some times the restriction impose barrier in the normal operations and policies of the bank.

Rival bank easily copy the product offering of IFIC .There fore the is in continuous of product innovation to gain temporary advantage over its Competitors.

Sometime political loans are the threat for this banking service.

The worldwide trend of mergers and acquisition in financial institution is causing concentration the industry and competitors are increasing in power in their respective areas.

As preciously mentioned, the world is advancing towards e-technology very fast .Through IFIC has taken effort to join the stream, it is not possible to complete the mission due to poor technological infrastructure of our country.

Due to existence of unsaved demand in financial sector ,it is expects that more financial institutions will introduced in the industry very shortly ,and we have already seen such cases in our country that lots of new banks are coming in the scenario with new services. IFIC should always be prepared for the competition in the coming years.

My Experience and Learning Points:

- IFIC Bank Ltd. has experienced a lot of change in the financial conditions of some of them favored it others did not.

- IFIC Bank with its wide ranging branch network and skilled personnel provides prompts and personalized services like issuing: Demand Draft, Telegraphic Transfer, Mail Transfer, Pay Order, and Transfer of fund by special arrangement.

- Remittance services are available at all branches and foreign remittances may be sent to any branches by the remitters favoring their beneficiates.

- Remittances are credited to the account of beneficiaries instantly of within shortest possible time.

- IFIC Bank has corresponding banking relationship with all major banks located in almost all the countries or cities. Expatriate Bangladeshis may send their hard earning foreign currencies through those banks of may contract renowned banks nearby to send their money to their dear ones in Bangladesh.

- Bank’s credit management is suffering as well. Although it has a separate Credit Management and Recovery Division under Head Officer, credit management has been up to the mark.

- IFIC Bank offers credit to almost all sector of commercial activities having productive purpose.

- The loan portfolio of the bank encompasses a wide range of credit programs covering many items.

- Credit facilities are offered to Individuals, Businessman, Small and Big business houses, Traders, Manufactures, Corporate bodies etc.

- loan provided to the rural people for agricultural production and firm activities.

- Loan pricing systems customer friendly.

- Prune customers enjoy prime rate in lending and other services.

- Employee’s workload is not uniform with respects to their grade.

- Some workers have negative attitude towards modernization.

- No satisfactory promotional activates are done and promotional mixes are hardly undertaken. IFIC Bank has poor coordination among different section.

Recommendations:

IFIC Bank ltd has may things to do to explore it’s vast potentials and to get out of the menacing state it is. It would be a tremendous task. It would cover almost every single desk of all the branches of the bank. First of all, the bank should [form a committee to study the problems form their point of view. Moreover the intern would tike to point out some aspects where the bank can work.

1) Bank’s profit has to be increased it can be done different ways. Through cost -sacking people, or other possible ways. Or revising the service charges and interest of different products it offers. The bank should increase charges as it’s charges are little too low in comparison to the other banks.

2) IFIC may also work extra hard on credit management,. It’s high non performing loans are eating up it’s profit and ass etc. This non performing loans trend may be stopped by

a) Rearranging the credit proposal form -that should be more evaluative and factual.

b) decision making may be decentralized as the banks credit issue decisions are made exclusively by the Managing Director and Boards of Directors. Some authority can be given to the branch level officers like managers, second officers, as they would know more about the prospective clients.

c) a study can be held on the various factors influencing repayments of loans.

Conclusion:

IFIC Bank Ltd is one of the first generation banks which were formed in early 80s to compete the market dominated by NCBs. Since then IFIC has been operating quite competitively. The bank extended its operation oversea in Nepal, the Maldives, and Oman. It made high amount of profit over the years. However it’s only recently the bank has put some bad figures against its name. This is a wake-up call for the bank. IFIC Bank ltd should and more importantly can come forward and recover itself from this situation. IFIC bank has one of the largest sizes in banking industry, and it is quite efficient and dynamic Board of Directors. Through some proper steps mentioned earlier the bank can get itself back and establish itself as a leading bank in the market.

However to be honest IFIC is in a cross road it can go anyway. It can go to the wrong way or it can go to the right way. If the threat is not perceived and responded, bad trend would continue to fall and it can get even worse. Consequently in the near future it can remain as a history.

IFIC Bank ltd to be exact is a bank which started with immense hope and performance well for some years and then it lost the track. Now has no competitiveness. Only a huge effort can save it.