Introduction

Risk is inherent in all commercial operations. For Banks and Financial institutions, Credit risk is an essential factor, which needs to be managed properly. Credit risk virtually is the possibility that a borrowe r will fail to repay debt in accordance with the terms of sanction. Credit risk therefore arises from the bank’s lending operations. In the present day’s state of deregulation and globalization, banks range of activities have increased, so also are the risks. Expansion of bank’s lending operations covering new products have forced the banks to confront newer risk areas and therefore to work out proper risk addressing devices. Credit risks are so exhaustive that a single device cannot encompass all the risks. Moreover lending risks today have assumed such diverse nature, that newer techniques are to be applied to effectively contain the risks. In order to effectively contain risks, credit risk management has to be done in order to enable the bank to proactively manage loan portfolios in order to minimize losses and earn acceptable level of return for the shareholders. In the present scenario of fast changing, dynamic global economy and the increasing pressure of globalization, liberalization, consolidation and disintermediation, it is essential to undertake robust credit risk management policies and procedures, sensitive and responsive to these changes.

National Bank Limited is committed to extend high quality services to its clients through different financial products and profitable utilization of fund by undertaking various lending operations including financing trade, commerce & Industry etc. In conducting lending operations NBL always bears in mind the essence of proper risk identification and their effective management. It is also recognized that failure in proper identification and management of risks may result in a large quantum of bank advances turning into non-performing.

In the above back drop, National Bank Limited underscoring the need of an effective credit risk management process has prepared the policy guidelines for Credit Risk Management. The policy will be reviewed annually by the Board of Directors of our bank.

The policy shall be distributed to the concerned officials, all divisional Heads, Branches, Regional Offices and top management officially. The policy shall be strictly followed by all concerned. Any deviation from the guidelines to be clearly identified and justification for approval to be provides.

The main objectives of the guidelines are as under:

1) To provide directional guidelines to all concerned to analysis of risk management.

2) To adopt an appropriate working method.

3) To keep legal aspects relating to loans and advances.

4) To introduce and adopt uniform practice in working..

5) To make working procedure rational.

6) To make lending correct information based.

7) To identify proper lending area.

8) To analyze all aspects related to credit and ascertain viability of lending.

9) To make credit documentation exhaustive.

10) To ensure proper supervision, monitoring & follow up.

The guidelines have been split into the following: –

1.1 Lending Guidelines

1.2 Credit Assessment & Risk Grading

1.3 Approval Authority

1.4 Segregation of Duticontext in line with our institutional structure.

1.5 Internal Audit

Rationale of the study

As a student of a faculty of business studies, it is helpful to gain the practical knowledge about an organization and its overall activities. By doing this kind of activities, we can enrich our practical knowledge .With the application of acquired knowledge we will be able to develop ourselves and compete globally .So we can say that the rationale of this is comprehensive.

Objectives of the study

The objectives of this study are as follows:

i) To study the activities and overall performance of National Bank Limited.

ii) To have a sound understanding of credit risk management system and procedure followed in the National Bank Limited.

iii) To know overall banking activities of National Bank Limited.

iv) To analyze the CRM process of the bank and to make recommendations if needed.

v) To focus on the credit risk grading system for analyzing the credit assessment procedure of National Bank Limited.

vi) To identify the strength and weakness and secondary data available have been used in preparing in report.

Methodology of the study

The methodology includes the sample selection, sources of data and method of data analysis.

Sample selection

The organization to be discussed is National Bank Limited. All the departments and functional areas will be covered with more emphasis on credit division.

Sources of data

The study is conducted on the basis of both primary and secondary data.

1.4.2.1 Primary Data

The primary data are collected from all the departments of National Bank Limited by interviewing personnel of the respective departments. The heads of the departments or senior executives have been interviewed. However, the analysis and the explanation are the authors’ own.

Secondary Data:

The secondary data of the study are based on a review of existing brochures, documents and database of National Bank Limited. The industry best practices are largely based on Bangladesh Bank manual, guidelines and databases. Books and published articles on this topic have also been consulted.

Data analysis

The credit risk management data of National Bank Limited will be analyzed in a descriptive manner.

Scope of the study

The scope of the study is entire National Bank Limited. This report is a descriptive study which tries to focus on the theories and practices of credit risk management in the context of

the financial institutions in Bangladesh. It will not focus on the comparable credit practices of other banks. In connection with this effort, a case study has been conducted on National bank limited giving more emphasis on the credit side of the institution compared to the other sides.

Justification of the study

In recent days, people are becoming more aware about the management of their resources. As the banks do business by lending their depositors’ money, they have even more responsibility to manage their credit portfolio smoothly. Bank’s reputation is a critical factor for its success and therefore modern banks must follow appropriate guidelines, policies and relevant manuals regarding credit extension and recovery. The usage of banking service for any type of financial activities is increasing day by day. People are taking loans to start different types of businesses.

It is now very important to know the internal processes of the banks and financial institutions to make informed decisions regarding their integrity, scope, ability and capacity.

Management of credit portfolio is one of the major operations of the banks. Therefore, as a 1st generation bank, National Bank Limited should give much attention to this area and this study will attempt to analyze their efforts and draw a complete picture of their practices.

Limitations of the study

The limitations of the study are as follows:

i) The credit policies and manuals of NBL are of confidential nature and thus it is difficult to collect the necessary literature and documents within this short time.

ii) The bank officials though helpful in every respect do not have much time to explain the internal procedures.

iii) Many operations relating to the credit extension run simultaneously by different credit officials and it is difficult to capture the sequence of any particular credit proposal.

iv) A structured filing procedure is often neglected which also poses difficulty in understanding the sequential procedure.

v) Borrowers do not often have the time to cooperate in the information gathering process.

National Bank Limited: Organization

Company Profile of National Bank Limited:

National Bank Limited is one of the pioneers of first generation private commercial bank incorporated in 1983. Since inception, NBL to provide modern banking facilities to the mass people is opening branches in rural areas alongside urban areas giving due importance. Presently, the bank created a strong market base through 121 branches and 10 SME centers throughout the country. Customer’s satisfaction and involvements gets priority in our daily activities.

The bank got priority as pioneer in different sectors for taking innovate steps in development of counter’s economy and upgrading the socio-economic status of rural people. Moreover, to encourage expatriates and to generate trust in sending money through legal channel, the bank took some challenging steps and became the pathfinder.

Meeting the need of the customers through modern technology with efficiency and searching new sectors of business, the bank strives to increase its trends of growth. The not only dedicated to profit maximization, it also remains active in fulfilling its social responsibilities.

Besides participating in building national economy, NBL is always a caring bank in adding value to the assets of the shareholders. In short, these are the focus of our banking ethics.

Historical Background :

National Bank Limited has its prosperous past, glorious present, prospective future and under processing projects and activities. Established as the first private sector bank fully owned by Bangladeshi entrepreneurs, NBL has been flourishing as the largest private sector Bank with the passage of time after facing many stress and strain.

At present we have 149 branches under our branch network. In addition, our effective and diversified approach to seize the market opportunities is going on as continuous process to accommodate new customers by developing and expanding rural, SME financing and offshore banking facilities. We have opened 10 branches and 5 SME/Agri branches during 2011.

The then President of the People’s Republic of Bangladesh Justice Ahsanuddin Chowdhury inaugurated the bank formally on March 28, 1983 but the first branch at 48, Dilkusha Commercial Area, Dhaka started commercial operation on March 23, 1983. The 2nd Branch was opened on 11th May 1983 at Khatungonj, Chittagong.

Vision : Ensuring highest standard of clientele services through best application of latest information technology, making due contribution to the national economy and establishing ourselves firmly at home and abroad as a front ranking bank of the country are our cherished vision.

Mission : Efforts for expansion of our activities at home and abroad by adding new dimensions to our banking services are being continued unabated. Alongside, we are also putting highest priority in ensuring transparency, account ability, improved clientele service as well as to our commitment to serve the society through which we want to get closer and closer to the people of all strata. Winning an everlasting seat in the hearts of the people as a caring companion in uplifting the national economic standard through continuous up gradation and diversification of our clientele services in line with national and international requirements is the desired goal we want to reach.

Role of Banks in the modern Economy

The prosperity of a country depends upon its economic activities. Like any other sphere of modern socio-economic activities, banking is a powerful medium of bringing about socio-economic changes of a developing country. Agriculture, Commerce and Industry provide the bulk of a country’s wealth. Without adequate banking facility these three cannot flourish. For a rapid economic growth a fully developed banking system can provide the necessary boost. The whole economy of a country is linked up with its banking system.

Functions of the bank

The functions of the bank are now wide and diverse. Of all the functions of modern bank, lending is by far the most important. They provide both short-term and long-term credits. The customers come from all walks of life, from a small business to a multi-national corporation having its business activities all around the world. The banks have to satisfy requirements of different customers belonging to different social groups. They function as a catalytic agent for bringing about economic, industrial and agricultural growth and prosperity of the country.

Service of the Professional Personal

The officers of National Bank limited have to their credit, decades of banking experience with national / international banks at home and abroad.

A State-Of-The-Art Technology Banking

The Bank will provide a state-of-the-art technology banking such as Any Branch Banking, ATM Services, Home-Banking, Tele-Banking, etc.

Retail Banking

Bank offers individuals the best services, including to provide complete customer satisfaction:

- Deposit services.

- Current Account in both Taka and major foreign currencies.

- Convertible Taka Accounts.

- Local and foreign currency remittances.

- SME Banking.

- Any Purpose loan

Corporate Banking

National Bank Limited caters to the needs of the corporate clients and provides a comprehensive range of financial services, which include:

- Corporate Deposit Accounts.

- Project & Infrastructure Development Finance, Syndicated Finance, Linkage Finance, Investment Business Counseling, Working Capital and other finances.

- Bonds and Guarantees.

Commercial Banking Being a commercial bank, National Bank Limited provides comprehensive banking services to all types of commercial concerns. Some of the services are:

- Trade Finance.

- Commodity Finance.

- Issuance of Import L/Cs.

- Advising and confirming Export L/Cs. – Bonds and Guarantees.

- Investment advice.

Online Banking

National Bank limited offers ‘Any branch’ banking service (to limited scale) that facilitates its customers to deposit, withdraw and transfer funds through the counters of any of its branches within the country.

Merchant Banking Advisory Services

The Bank will provide Merchant Bank advisory services, offer complete packages in areas of promotion of new companies, evaluation of projects, mergers, take-over and acquisitions, liaise with the Government with regard to rules and regulations, management of new issues including underwriting support etc.

Capital Market Operation

The Bank will also introduce capital market operation which will include Portfolio Management, Investors Account, Underwriting, Mutual Fund Management, Trust Fund Management etc.

Farm and Off-Farm Credits (Rural)

Out of Bank’s social commitment towards the population at the grass-root level, it will participate in farm and off-farm credit programmers in rural Bangladesh to bring in economic buoyancy in the periphery.

Credit To Women Entrepreneurs

The Bank believes in ‘Equal Opportunity Policy’ and as such has been contemplating to introduce credit programmers for willing and talented women entrepreneurs.

Counter for Payment of Bills

Dedicated counters are available at National Bank Limited’s branches to receive the payment of various utility bills.

Other Services

- Remit funds from one place to another through DD, TT and MT etc.

- Conduct all kinds of foreign exchange business including issuance of L/C, Traveler’s Cheque etc.

- Collect Cheque, Bills, Dividends, Interest on Securities and issue Pay Orders, etc.

- Act as referee for customers.

- Locker facility for safe keeping of valuables and documents.

Deposits and advances

Deposits Schemes

Deposit of the Bank showed a continuous increase during the year and in 2010 stood at TK.102471.8 million. The growth over previous year was 33.37 percent. The growing customers’ confidence in National Bank helped the necessary broadening of customer range that spanned private individuals, corporate bodies, multinational concerns and financial institutions. The Bank introduced various products/ schemes to attract the depositors.

Cash and Balances with Banks and Financial Institutions

Cash and Balances with Bangladesh Bank was TK. 8695.31 million as against Tk. 6843.69 million in 2010. The funds are maintained to meet Cash Reserve Requirement (CRR) and Statutory Liquidity Requirement (SLR) of the Bank. TK. 1101.57 million as at 31 December 2010. The Bank maintained sufficient balances with correspondents outside Bangladesh to facilitate prompt settlement of payments under Letter of Credits commitments.

Investments

Investments of the Bank were TK. 24993.33 million showing an increase of 11.53 percent during the year under review. Investment activities centered around meeting the Bank’s SLR and were mostly in the form of Government Treasury Bills having varying dates of maturity. The average yield on the bills was 7.00% per annum.

Loans and Advances

The Bank’s total Loans and Advances stood at TK. 92003.56 million in 2010 showing a growth of 28.55 percent compared to Tk. 65129.29 million of 2009. Bank’s clientele comprised of corporate bodies engaged in such vital economic sectors as Trade Finance, Steel-Re-Rolling, Ready Made Garments, Textiles, Ship Scrapping, Edible Oil, Cement, Transport, Construction etc.

Consumer Banking

The Bank continued to offer loans under Consumer Credit Scheme to the fixed income group to enable borrowers to acquire consumer products such as household appliances, office equipment, motor vehicles, mobile phone etc.

Foreign Exchange and Foreign Trade

The bank opened a total number of 24,385 LCs amounting USD 1,117.61 million in import trade in 2010. The main commodities were scrap vessels, rice, wheat, edible oil, capital machinery, petroleum products, fabrics & accessories and other consumer items.

The bank has been nursing the export finance with special emphasis since its inception. In 2010 it handled 18,761 export documents valuing USD 559.78 million with a growth of 5.41 percent over the last year

Merchant Banking

Merchant Banking activity has lately gained popularity in our country. At the initial stage the activities would center on issue Management, Portfolio Management, pre-placement and underwriting.

Branch Network

The Bank has established a wide network of branches in urban and rural areas totaling 356. National Bank Limited is the largest Commercial Bank in Private Sector in Bangladesh.

Divisional Operations in National Bank Limited

The operations in National Bank limited are carried out through 5 separate departments:

1 General Banking (GB)

2 Cash

3 Accounts

4 Trade Finance

5 Credit

General Banking

The General Banking division, in National Bank Limited, generally performs the following functions:

a) Account opening

b) Cheque book issue

c) FDR issue and encashment.

d) Product issue and encashment

e) Account transfer from one branch to another branch

f) Pay order issue and encashment

g) Fund transfer from one account to other account

h) Inward Remittance and Outward Remittance

i) Demand Draft (DD) issue

j) Stop payment order

k) Issue of solvency certificate

l) Inward and outward clearing

Cash

Cash division is the center point of any bank. In National Bank Limited, the cash division performs an integral part of its banking operations.

The tellers in the cash division receive cash from the clients and gives necessary postings in the PIBS (National Bank Integrated Banking Software). At the time of receipt, ‘cash received’

and ‘posted’ seal is attached to the deposit slip. At the time of payment, the tellers first verify the signatures and then make payment. If the check is for a big amount, then it has to be authorized by the cash in charge and branch in charge. The seals used here are ‘cash paid’, posted’ and ‘signature verified’.

Accounts

In National Bank Limited, the accounts related information is fully computer generated. The central IT department generates several important statements such as the General Ledger, profit and Loss Account, Transaction journal, Overdraft and Advances Position, Full Balance position etc. These statements are disseminated in the network so that every branch can have access to its accounting information at the beginning of each working day.

Trade Finance

Trade Finance division operates independently in the branches and it generally deals with the followings:

a) Import L/C

b) Export L/C

c) Local & foreign Bills Purchased

d) Remittance

Import L/C

When a client comes to open an L/C, basic queries about the IRC, VAT registration number, TIN etc, are made. If the bank is satisfied with all the documents, an L/C is opened and an operational entry for L/C opening is passed in Micro Bank.

Export L/C

National Bank Limited provides money to the borrowers in terms of Packing Credit and Back to Back L/C.Packing credit is essentially a short term advance with a fixed repayment date granted by the bank to an eligible exporter for the purpose of buying, processing, manufacturing, packing and shipping of the goods meant to be exported.

Credit

The credit division is also an independent division in National Bank limited. This division basically deals with the extension of credit to the worthy clients and thus to make a profit from the interest charges. The bank invests the money of the depositors and thus the credit division has to be very cautious in terms of credit extension.

The credit division arranges for different types of loans and high emphasis is given on Small and Medium Enterprises (SMEs). It also issues bank guarantee in favor of the clients. Necessary postings are made through Micro Bank software.

Cash: Cash in hand increased by Tk.184.14 million while the balances maintained with the Bangladesh Bank and its agents increased by 30.03% at the end of the December 31, 2010. The deposit growth increased the balances with Bangladesh bank and its agents for maintaining the Cash Reserve Requirement (CRR).

Investments: Investment portfolio of NBL consisting of government and private securities as on December 31, 2010 was Tk. 24,993.33 million registering a growth of 102.95% over previous year, out of which investment in Government securities was 60.08% and rest 39.92% in private securities. The growth is due to mainly purchase of Government Treasury Bills, Debentures and stocks.

Deposits: The deposit base of the bank registered a growth of 33.37% in the reporting year over the last year and stood at Tk. 102,471.83 million. Expansion of branch network, competitive interest rate and innovative deposit products contributed to the growth.

Shareholder Equity: In 2009, 55% stock dividend was declared which increased the amount of paid up capital to Tk. 4,412.13 million in 2010. Reserve and surplus was enhanced by 142.06% consisting of statutory reserve, general reserve, retained earnings and other reserve. Total shareholder’s equity as on December 31, 2010 stood Tk. 19,105.60 million.NBL has increased the authorized capital of the bank to Tk. 17,500 million .

Current Ratio: In 2009 was the highest current ratio and 2006 was the lowest current ratio indicator of National Bank Ltd. The Bank has been decreased their current ratio 1.88 % from 2009.

Liquid Securities Indicator: This ratio compares the most government securities an institution can hold with the overall size of its asset portfolio.

Government Securities / Total Assets*100

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Liquid Securities (%) | 10.89% | 11.32% | 9.19% | 9.34% | 11.15 % |

The graphical presentation of the ratio has been shown in the following way:

Liquidity Assets Ratio: Liquidity assets ratios are a set of ratios or figures that measure a company’s ability to pay off its short-term debt obligations.

Cash+Reserve+Govt. Securities/ Total Assets*10

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Liquid Assets (%) | 19.86% | 23.96% | 21.23% |

21.69% 24.72%

The graphical presentation of the ratio has been shown in the following way:

The graph represents that, in 2010 is the highest and the 2006 is the lowest Liquidity Assets Ratio. National Bank Ltd. keeps 24.72 taka liquid assets against 100 taka total assets in 2010. National Bank Ltd. has increased their liquid assets 13.97 % from 2009. So this ratio is acceptable.

Capital Adequacy Ratio: Capital adequacy ratio (CAR) is a measure of how much capital is used to support the banks’ risk assets. It is calculated as follows:

Total Capital / Total Risk Weighted Assets *100

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Capital Adequacy Ratio (%) | 10.10% | 13.11% | 13.42% | 8.61% | 12.29% |

The graphical presentation of the ratio has been shown in the following way:

NBL always try to maintain a prudent balance between Tier-1 and Tier 2 capital. Total capital as on December 31, 2010 was tk. 19,190.79 million and capital adequacy ratio was 12.29%. Though in 2009 their capital adequacy ratio was decreased but in present scenario they improve their capital adequacy ratio.

Leverage Ratio: Leverage ratio indicate the capacity to meet up short and long term debt obligation.

Debt Equity Ratio: The Debt Equity Ratio (D/E) is a financial ratio indicating the relative proportion of shareholders’ equity and debt used to finance a company’s assets. It is calculated as follows:

Debt/Equity

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Debt Equity Ratio (Times) | 8.13 | 6.77 | 6.99 | 9.31 | 6.05 |

The graphical presentation of the ratio has been shown in the following way:

The graph represents that, in 2009 is the highest and the 2010 is the lowest Debt Equity Ratio.

Advance Deposit Ratio: Advance Deposit Ratio is the proportion of loans generated by banks from the deposits received. It is calculated as follows:

Loan & Advance/Deposit*10

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Advance Deposit Ratio (%) |

81.06

76.05

84.18

84.77

89.78

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, In 2010 Credit Deposit Ratio is higher from comparing any year. In 2010 National Bank Ltd. has given loan 89.78 taka against 100 taka deposit and in 2009 given 84.77 taka. The bank has increased their credit deposit ratio 5.92 % from 2009. In December, 2010 Bangladesh Bank Regulation was 80.5% about advance deposit ratio.

Debt Ratio: Debt Ratio is a financial ratio that indicates the percentage of a company’s assets that are provided via debt. It is calculated as follows:

Total Debt/Total Assets*100

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Debt Ratio (%) | 93.00% | 91.93% | 91.51% | 90.28% | 84.16% |

The graphical presentation of the ratio has been shown in the following way:

The graph represents that, in 2010 is the lowest and the 2006 is the highest Debt Ratio. NBL has covered 84.16% assets from debt financing in 2010. Here the graph shows the line graph fall in consistently.

Activity Ratio: Activity ratio indicates how effectively firm is utilizing its asset. Here effectively means operating efficiency of the firm.

Total Assets Turnover: Total Asset Turnover is a financial ratio that measures the efficiency of a bank’s use of its assets in generating interest income. It is calculated as follows:

Interest Income / Assets*100

Year | 2006 | 2007 | 2008 | 2009 | 2010 |

Total Assets Turnover (%) | 7.85% | 7.59% | 8.01% | 7.62% | 7.14% |

The graphical presentation of the ratio has been shown in the following way

In 2008 is the highest total assets turnover and 2010 is the lowest total assets turnover of National Bank Ltd. The bank has been decreased their total assets turnover 6.3% from 2009.

Profitability Ratio: Profitability ratio indicates that the firms net return on sales and assets.

Return on Assets (ROA): The return on assets ratio measures how efficiently profits are being generated from the assets employed. It is calculated as follows:

Net Income/ Total Asset*100

Year | 2006 | 2007 | 2008 | 2009 | 2010 |

ROA (%) | 1.19% | 2.40% | 2.36% | 2.52% | 6.05% |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, in 2010 is the highest and the 2006 is the lowest ROA indication of National Bank Ltd National Bank Ltd. has increased their ROA 140.08 % from 2009. So this ratio might be accepted.

Return on Equity (ROE): Return on equity measures a bank’s profitability by revealing how much profit a bank generates with the shareholders investment. It is calculated as follows:

Net Income/ Total Shareholder Equity*100

Year | 2006 | 2007 | 2008 | 2009 | 2010 |

ROE (%) | 16.89% | 31.57% | 28.38% | 27.53% | 48.96% |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, in 2010 is the highest and the 2006 is the lowest ROE indication of National Bank Ltd.

Earnings per Share (EPS): The portion of a company’s profit allocated to each outstanding share of common stock. It is calculated as follows:

Net Income/ Total number of shares outstanding

Year | 2006 | 2007 | 2008 | 2009 | 2010 |

EPS(TK.) | 6.30 | 6.61 | 5.33 | 4.69 | 15.55 |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, in 2010 is the highest and the 2009 is the lowest EPS indication of National Bank Ltd. The bank has been provided 15.55 taka net income against per share in 2010. National Bank Ltd. has been increased their net income 231.34 % from 2009. So this ratio may be accepted.

Net Interest Margin: Net Interest Margin (NIM) is a measure of the difference between the interest income generated by banks or other financial institutions and the amount of interest paid out to their lenders. It is calculated as follows:

(Interest Income – Interest Expense) / Total Asset

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| NIM (%) | 2.62% | 2.57% | 3.04% | 2.74% | 3% |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, in 2008 is the highest and the 2007 is the lowest Net Interest National Bank Ltd. has increased their Net Interest Margin 9.49 % from 2009. This is a good sign for the bank because interest income is the main source of revenue for a bank. So this ratio might be accepted.

Net Profit Margin: Net profit margin shows that how much profit to earn in a year.

Profit after Tax / Interest Income *100

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Net Profit Margin (%) | 13.81% | 28.87% | 26.22% | 29.55% | 71.34% |

The graphical presentation of the ratio has been shown in the following way:

The bank has been achieved extraordinary profit in 2010. The banks generated net profit 71.34 taka when interest income 100 taka in 2010. NBL has been increased their Net Profit Margin 141.42 % from 2009.Though maximization of wealth is a main objective of bank, but profit maximization is also focus .

Operating Expense Turnover: Operating Expense Turnover is the efficiency ratio gives us a measure of how effectively a bank is operating. It is calculated as follows:

Operating Exp. /Interest Income*100

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Operating Expenses Turnover (%) |

58.03%

49.76%

37.58%

44.50%

42.57%

The graph implies that, in 2006 National Bank Ltd. is the highest and in 2008 is the lowest operating expense against its interest income. In 2010 National Bank Ltd. was 42.57 tk. total operating expense against its 100 tk. interest earning. NBL has been decreased their operating expense turnover 4.34 % from 2009.

Price Earnings Ratio: Price Earnings Ratio (P/E) is a valuation ratio of a company’s current share price compared to it’s per share earnings. It is calculated as follows:

Market Price per Share/EPS

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| P/E (Times) | 12.07 | 28.03 | 13.95 | 13.77 | 12.32 |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, in 2007 is the highest and the 2006 is the lowest P/E indication of National Bank Ltd. In 2010 companies Price Earnings Ratio is 12.32 times that is better from 2008 & 2009. National Bank Ltd. has decreased their P/E 10.53 % from 2009.

Market Price per Share: Market price per share is an useful analytical tools which determine when an investment in accompanying worthwhile.

EPS* Price Earnings Ratio

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Market Price per Share (TK.) | 76.05 | 149.40 | 101.43 | 64.63 | 191.60 |

The graphical presentation of the ratio has been shown in the following way:

The graph implies that, NBL has been increased their market price per share 196.64% from 2009. The main reasons of these changes are the banks has been increased their net income 231.34 % from 2009 so ultimately increased their EPS and the percentage changes in increasing EPS are 231.56 % from 2009.

Book Value per Share: Book value per share indicates the value of each share stock. It calculated as follows:

Equity/Number of Common Shares Outstanding

The graphical presentation of the ratio has been shown in the following way: ities and Threats. It helps the organization to identify how to evaluate its performance and can scan the macro environment, which is turn would help the organization to navigate in the Turbulence Ocean of competition. Following is given the SWOT analysis of National Bank Ltd:

The reputation of the bank is increasing day by day. People are relying on this bank gradually.

Sponsors

The sponsors of the bank are some of the top companies and top business personnel of our country.

Modern Facilities and Computer

For speedy service to the customer, NBL had installed money-counting machine in the teller counter. The bank has computerized banking operation under software called PC banking. More over computer printed statements are available to internal use and occasionally for the customers. NBL is equipped with telex and fax facilities

Interactive Corporate Culture:

Credit Risk Management: A Theoretical Framework

Contemporary banking organizations are exposed to a diverse set of market and non-market risks, and the management of risk has accordingly become a core function within banks. Banks have invested in risk management for the good economic reason that their shareholders and creditors demand it. But bank supervisors, such as the Bangladesh Bank, also have an obvious interest in promoting strong risk management at banking organizations because a safe and sound banking system is critical to economic growth and to the stability of financial markets. Indeed, identifying, assessing, and promoting sound risk management practices have become central elements of good supervisory practice.

What is credit?

In banking terminology, credit refers to the loans and advances made by the bank to its customers or borrowers. Bank credit is a credit by which a person who has given the required security to a bank has liberty to draw to a certain extent agreed upon. It is an arrangement for deferred payment of a loan or purchase. (Wikipedia dictionary)

Credit means a provision of, or commitment to provide, funds or substitutes for funds, to a borrower, including off-balance sheet transactions, customers’ lines of credit, overdrafts, bills purchased and discounted, and finance leases. (Guideline on credit risk management, Bank of Mauritius)

What is credit risk?

Risk means the exposure to a chance of loss or damage. Risk is the element of uncertainty or possibility of loss that exist in any business transaction. Credit risk is the likelihood that a borrower or counter party will be unsuccessful to meet its obligation in accordance with agreed terms and conditions. (Wikipedia dictionary)

Credit risk is most simply defined as the potential that a bank borrower or counterparty will fail to meet its obligations in accordance with agreed terms (Basel Committee on Banking Supervision,2000).

What is credit risk management?

Risk management contains

Identification,

Measurement,

Aggregation,

Planning and management,

as well as monitoring of the risks arising in a bank’s overall business.

Risk management is thus a continuous process to increase transparency and to manage risks.

Identification

A bank’s risks have to be identified before they can be measured and managed.

Typically banks distinguish the following risk categories:

Credit risk

Market risk

Operational risk

Measurement

The consistent assessment of the three types of risks is an essential prerequisite for successful risk management. While the development of concepts for the assessment of market risks has shown considerable progress, the methods to measure credit risks and operational risks are not as sophisticated yet due to the limited availability of historical data.

Aggregation

When aggregating risks, it is important to take into account correlation effects which cause a bank’s overall risk to differ from the sum of the individual risks.

Planning and management

Furthermore, risk management has the function of planning the bank’s overall risk position and actively managing the risks based on these plans.

The most commonly used management tools include:

Risk-adjusted pricing of individual loan transactions

Setting of risk limits for individual positions or portfolios

Use of guarantees and credit insurance

Securitization of risks

Buying and selling of assets

Monitoring

Risk monitoring is used to check whether the risks actually incurred lie within the prescribed limits, thus ensuring an institution’s capacity to bear these risks. In addition, the effectiveness of the measures implemented in risk controlling is measured, and new impulses are generated if necessary.

Figure : Risk Management

PRISM Model of credit risk management

PRISM model is a contemporary model used in the credit risk management in modern world. It is called PRISM, an acronym for –

P = Perspective

R = Repayment

I = Intention

S = Safeguards

M = Management

Management, a PRISM component, centers on what the borrower is all about, including history and prospects. Intention or loan purpose serves as the basis for repayment. Repayment focuses on internal and external sources of cash. Internal operations and asset sales produce internal cash, whereas new debt or equity injections provide external cash sources. Internal safeguards originate from the quality and soundness of financial statements, while collateral guarantees and covenants provide external safeguards.

Prerequisites for Efficient Risk Management

In order to implement efficient risk management, sound and consistent

Methods

Processes and organizational structures and

IT systems and an IT infrastructure are required for all five components of the control cycle.

Methods

The methods used show how risks are captured, measured, and aggregated into a risk position for the bank as a whole.

Processes and organizational structures

Processes and organizational structures have to make sure that risks are measured in a timely manner that risk positions are always matched with the defined limits, and that risk mitigation measures are taken in time if these limits are exceeded.

IT systems and an IT infrastructure

IT systems and an IT infrastructure are the basis for effective risk management.

Among other things, the IT system should allow

The timely provision and administration of data;

The aggregation of information to obtain values relevant to risk controlling;

as well as an automated warning mechanism prior to reaching critical risk limits.

Why manage credit risk?

The reasons behind managing credit risks are as follows:

a) Increase shareholder value

Value creation

Value preservation

Capital optimization

b) Instill confidence in the market place

c) Alleviate regulatory constraints and distortions thereof.

Risk Strategy

A successful, bank-wide risk management requires the definition of a risk strategy which is derived from the bank’s business policy and its risk-bearing capacity. Risk strategy is defined as

the definition of a general framework such as principles to be followed in dealing with risks and the design of processes as well as technical-organizational structures; and

the definition of operational indicators such as core business, risk targets, and limits.

Limits

The definition of limits is necessary to curb the risks associated with bank’s activities. It is intended to ensure that the risks can always be absorbed by the predefined coverage capital.

Methods of Defining Limits

The risk limits in the bank’s individual business units are based on the bank’s business orientation, its strategy, and the capital allocation method selected. Such a system has to meet the following requirements:

The parameters used to determine the risks and define the limits should be taken from existing systems. The parameters should be combined using automated interfaces. This ensures that errors due to manual entry cannot occur during the data collection process.

The defined indicators should be used consistently throughout the bank. The data should be consistent with the indicators used in sales and risk controlling.

Employees should be able to understand how and why the indicators are determined and interpreted. This is intended to ensure acceptance of the data and the required measures, e.g. when limits are exceeded.

Limit Structure

The maximum risk limit is determined by the capital allocated to cover credit risks in the planning process. The bank’s organizational structure has a significant impact on the way in which the limits are designed. Besides the types of limits mentioned above, there are further limit categories:

Product, business area, country, and industry limits

Risk class limits

Limits on unsecured portions

Individual customer limits

Product, business area, country, and industry limits

Product limits can be defined, among other things, for loans to retail and corporate customers, for real estate loans, as well as for project finance. Banks with an international focus can also define country limits in order to manage their risks arising from transactions in other regions.

Risk class limits

Monitoring and limiting the concentration of exposures in certain risk classes is necessary to be able to detect a deterioration of the portfolio in time, and thus to be able to avoid losses as far as possible by withdrawing from certain exposures. (Bernanke, 2006)

Limits on unsecured portions

The definition of limits for unsecured portions restricts loans that are granted without the provision of collateral or which are collateralized only partly. These limits allow banks to manage their maximum risks efficiently, as it is easy to determine and monitor unsecured portions.

Individual customer limits

Limits for individual borrowers represent the most detailed level of risk controlling. The main purpose for their application is the prevention of cluster risks in the credit portfolio.

Rigidity of Limits

In practice, the rigidity of limits varies in terms of their impact on a bank’s business activities.

Certain limits are defined rigidly and must never be exceeded, as otherwise the viability of the bank as a whole would be endangered.

In addition, there are early warning indicators that indicate the risk of exceeding limits ahead of time.

Limit Monitoring and Procedures Used When Limits Are Exceeded

The credit decision is taken based on the borrower’s credit standing and any collateral, but independently of the portfolio risk. Such ex-post observation can result in a relatively high number of cases in which limits are exceeded, thus reducing the effectiveness of the limit stipulations.Some banks check the compliance with the limits immediately during the credit approval process. Prior to the credit decision, compliance with the relevant limits is checked in case the credit is approved. Bringing limit monitoring into play at this early stage is also referred to as ex-ante monitoring. This helps prevent the defined limits from being exceeded in the course of approving new loans. Ex-ante monitoring is quite complex.

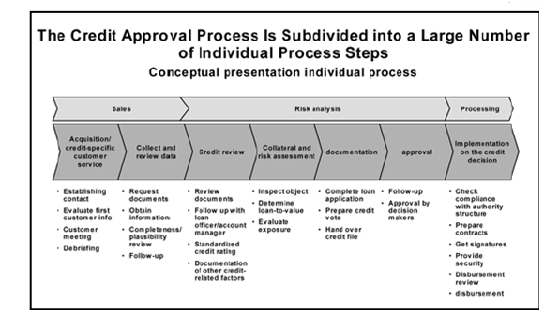

Credit Risk Management Process

Credit risk management process should cover the entire credit cycle starting from the origination of the credit in a financial institution’s books to the point the credit is extinguished from the books (Morton Glantz, 2002). It should provide for sound practices in:

4.1 Credit processing/appraisal

4.2 Credit approval/sanction

4.3 Credit documentation

4.4 Credit administration

4.5 Disbursement

4.6 Monitoring and control of individual credits

4.7 Monitoring the overall credit portfolio (stress testing)

4.8 Credit classification and

4.9 Managing problem credits/recovery

Credit Processing/Appraisal

Credit processing is the stage where all required information on credit is gathered and applications are screened. Credit application forms should be sufficiently detailed to permit gathering of all information needed for credit assessment at the outset. Financial institutions should set out pre-qualification screening criteria, which would act as a guide for their officers to determine the types of credit that are acceptable. For instance, the criteria may include rejecting applications from blacklisted customers. These criteria would help institutions avoid processing and screening applications that would be later rejected.

In the case of loan syndication, a participating financial institution should have a policy to ensure that it does not place undue reliance on the credit risk analysis carried out by the lead underwriter

As a general rule, the appraisal criteria will focus on:

a) amount and purpose of facilities and sources of repayment;

b) integrity and reputation of the applicant as well as his legal capacity to assume the credit obligation;

c)performance of the borrower in any credit previously granted by the financial institution,

d)the borrower’s capacity to repay based on his business plan, if relevant, and projected cash flows using different scenarios;

e)cumulative exposure of the borrower to different institutions;

f)physical inspection of the borrower’s business premises as well as the facility that is the subject of the proposed financing;

g)current and forecast operating environment of the borrower;

h)background information on shareholders, directors and beneficial owners for corporate customers; and

i)Management capacity of corporate customers .

Credit-approval/Sanction

Approval authorities should be sanctioned by the board of directors. Approval authorities will cover new credit approvals, renewals of existing credits, and changes in terms and conditions of previously approved credits, particularly credit restructuring, all of which should be fully documented and recorded.The approval process should be based on a system of checks and balances. Some approval authorities will be reserved for the credit committee in view of the size and complexity of the credit transaction.

Credit Documentation

Documentation is an essential part of the credit process and is required for each phase of the credit cycle, including credit application, credit analysis, credit approval, credit monitoring, collateral valuation, and impairment recognition, foreclosure of impaired loan and realization of security. Credit applications must be documented regardless of their approval or rejection. All documentation should be available for examination by the Bangladesh Bank. Financial institutions must establish policies on information to be documented at each stage of the credit cycle. For security reasons, financial institutions should consider keeping only the copies of critical documents (i.e., those of legal value, facility letters, signed loan agreements) in credit files while retaining the originals in more secure custody. Credit files should also be stored in fire-proof cabinets and should not be removed from the institution’s premises.

Financial institutions should maintain a checklist that can show that all their policies and procedures ranging from receiving the credit application to the disbursement of funds have been complied with. The checklist should also include the identity of individual(s) and/or committee(s) involved in the decision-making process.

Credit Administration

Financial institutions must ensure that their credit portfolio is properly administered, that is, loan agreements are duly prepared, renewal notices are sent systematically and credit files are regularly updated. A financial institution’s credit administration function should, as a minimum, ensure that:

credit files are neatly organized, cross-indexed, and their removal from the premises is not permitted;

the borrower has registered the required insurance policy in favor of the bank and is regularly paying the premiums;

the borrower is making timely repayments of lease rents in respect of charged leasehold properties;

credit facilities are disbursed only after all the contractual terms and conditions have been met and all the required documents have been received;

collateral value is regularly monitored;

the borrower is making timely repayments on interest, principal and any agreed to fees and commissions;

information provided to management is both accurate and timely;

responsibilities within the financial institution are adequately segregated;

funds disbursed under the credit agreement are, in fact, used for the purpose for which they were granted;

“back office” operations are properly controlled;

the established policies and procedures as well as relevant laws and regulations are complied with; and

on-site inspection visits of the borrower’s business are regularly conducted and assessments documented (L.R.Chowdhury,2004).

Monitoring and Control of Individual Credits

To safeguard financial institutions against potential losses, problem facilities need to be identified early. A proper credit monitoring system will provide the basis for taking prompt corrective actions when warning signs point to deterioration in the financial health of the borrower.

In broad terms, the monitoring activity of the institution will ensure that:

funds advanced are used only for the purpose stated in the customer’s credit application;

financial condition of a borrower is regularly tracked and management advised in a timely fashion;

borrowers are complying with contractual covenants;

collateral coverage is regularly assessed and related to the borrower’s financial health;

the institution’s internal risk ratings reflect the current condition of the customer;

contractual payment delinquencies are identified and emerging problem credits are classified on a timely basis; and

Problem credits are promptly directed to management for remedial actions.

Monitoring the Overall Credit Portfolio (Stress Testing)

An important element of sound credit risk management is analyzing what could potentially go wrong with individual credits and the overall credit portfolio if conditions/environment in which borrowers operate change significantly. The results of this analysis should then be factored into the assessment of the adequacy of provisioning and capital of the institution. Such stress analysis can reveal previously undetected areas of potential credit risk exposure that could arise in times of crisis.

Possible scenarios that financial institutions should consider in carrying out stress testing include:

Significant economic or industry sector downturns;

Adverse market-risk events; and

Unfavorable liquidity conditions.

4.7 Classification of credit

It is required for the board of directors of a financial institution to “establish credit risk management policy, and credit impairment recognition and measurement policy, the associated internal controls, documentation processes and information systems;”

Credit classification process grades individual credits in terms of the expected degree of recoverability. Financial institutions must have in place the processes and controls to implement the board approved policies, which will, in turn, be in accord with the proposed guideline.

Managing Problem Credits/Recovery

A financial institution’s credit risk policy should clearly set out how problem credits are to be managed. The positioning of this responsibility in the credit department of an institution may depend on the size and complexity of credit operations. The collection process for personal loans starts when the account holder has failed to meet one or more contractual payment (Installment). It therefore becomes the duty of the Collection Department to minimize the outstanding delinquent receivable and credit losses.

Collection objectives

The collector’s responsibility will commence from the time an account becomes delinquent until it is regularized by means of payment or closed with full payment amount collected. The goal of the collection process is to obtain payments promptly while minimizing collection expense and write-off costs as well as maintaining the customer’s goodwill by a high standard of service. The customers who do not respond to collection efforts – represent a financial risk to the institution. The Collector’s role is to collect so that the institution can keep the loan on its books and does not have to write-off / charge off.

Identification and allocation of accounts

When a customer fails to pay the minimum amount due or installment by the payment due date, the account is considered in arrears or delinquent. When accounts are delinquent, collection procedures are instituted to regularize the accounts without losing the customer’s goodwill whilst ensuring that the bank’s interests are protected.

Collection Steps

To identify and manage arrears, the following aging classification is adopted:

For all products other than credit cards:

Table 4.1: Credit recovery steps

| Days Past Due (DPD) | Collection Action |

1-14 | Letter, Follow up & Persuasion over phone (Annexure V) |

15-29 | 1st Reminder letter & Sl. No. 1 follows |

30-44 | 2nd reminder letter + Single visit |

45-59 |

|

60-89 |

|

90 and above |

|

Credit Risk Management:

The credit risk management process followed in National Bank Limited can be categorized in the following specific segments:

Mission Statement of National Bank Limited

Credit Policy Guidelines

- Lending guidelines

- Credit Assessment and Credit Risk Grading

- Approval authority

- Approval/transactions Record

- Discouraged Business Types

While National Bank will follow the policy of financing prospective, feasible & rewarding areas, it will have (as presently has) some areas, identified as discouraged. Generally the following areas will be discouraged for financing:-

- Military Equipment / Weapon Finance

- Highly leveraged Transactions

- Finance of speculative business

- Logging, Mineral Extraction / Mining or other activity that is ethically or environmentally sensitive

- Lending to companies listed on CIB black list or known defaulters

- Counter parties in countries subject to UN sanctions

- Share lending

- New Cold storage finance

- Financing Cement Industries

Loan Facility Parameters

National Bank Limited extends and will extend credit for various genuine purposes. One type of advance requires to be treated differently from other types. Depending on the type financed, ownership pattern, business mode, cash flow, security and other related matters facility parameters are to be set.

However the general parameters in facility will be as under: –

- Nature of Advance Purpose

- Limit/Amount of Facility/Maximum Size

- Margin/Equity

- Rate of Interest

- Rate of commission/charges

- Mode of disbursement

- Mode of repayment

- Security

- Validity/Maximum tenor

- General/Special conditions/ Covenants

Nature of Advances:

Each advance to be made will be categorized under one of the arranged types and will be governed under the terms & conditions related thereto.

Purpose:

Our lending will be guided by legitimate purpose. Financing for hoarding, speculative purpose and which will be utilized for degrading the character of the people will be avoided. Credit which will contribute to production, trade, commerce, import, export, development of Industries, development activities/Economic growth, infrastructural development, employment generation, poverty alleviation etc will be stressed.

Limit /Amount of facility/Maximum Size:

Facility will be considered based on assessment of requirement & justification subject to the overall lending cap as per Bangladesh Bank single party exposure limit.

Margin/Equity:

It will be the general policy of the bank to judiciously ensure stake of the borrower in any financing plan. Margin will, however, be subject to institutional policy in this regard and central bank policy where applicable.

Rate of Interest/ Commission and other charges:

Rate of interest will be charged as per declared rate of the bank. Pricing will be basically risk based. Higher price will be considered for riskier borrowers because of their higher riskinvolved (i.e lower score obtained by an obligor as per CRG score sheet is called a risky client). Similarly lower price will be considered for prime clients on the basis of their low risk (Low risk grade clients means where an obligor obtained higher aggregate score as per CRG score sheet or 100% cash covered or govt./international Top bank Guarantee).

Mode of disbursement:

In disbursing credit the bank ensures drawing for the purpose the loan has been sanctioned. Where required visit of the business/site etc are suggested and all subsequent disbursements are made conditional to full utilization of disbursed money in the preceding phase.

Mode of Adjustment/ Repayment:

For the borrower to exhibit capability to periodically adjust the drawings taken and as such to have idea regarding the rationale for continuation of the facility, adjustment mode is given. In term of lending, where revolving transaction is not allowed, adherence to adjustment stipulation ( monthly, quarterly, half yearly, yearly or otherwise) is suggested to ensure recovery of the loan disbursed.

Security:

Our bank mostly relies/will continue to rely on security based lending, taking into consideration, the character of the borrower, nature of business cash flow, environmental, economic, business and other influencing factors. In obtaining security primary and collateral security are suggested. Primary securities are valued on the basis of landed cost in case on imported goods/ ex-mill or factory price/ whole sale market price for the local goods. Collateral security of acceptable type having adequate market /sale value is accepted.

Validity/Expiry/Maximum tenor:

Validity/Expiry date for continuous credit is set at a period not exceeding 1 year. Short term loan mostly is allowed for trade/ Commerce. This expiry date is virtually the date for adjustment/review of the facility, subject to periodical and satisfactory turnover of the limit.

Such loans are allowed for adjustment in installments.

Short term : Up to 12 months.

Medium term : More than 12 months and up to 60 months.

Long term : More than 60 months.

Quality of security:

- Primary security having adequate market value is accepted .

- Perishable goods and seasonal goods are generally discouraged as primary security.

- Acceptable financial obligations are preferred.

- Receivable bills against work order/supply order funded by Foreign Agencies/ which bear adequate funding arrangements are preferred.

- Documents which are drawn in conformity with the export L/C terms ( i.e. documents which do not have discrepancies) are accepted for negotiation.

- Personal guarantee of those persons having high net worth / assets, satisfactory commitment fulfillment track record and no connection with any irregular/ classified advance are obtained.

- In syndicated financing mortgage is executed on first ranking pari passu basis.

Legal Interest Protection:

- Title searches are conducted periodically for collateral both with RJSC and land Registrar for mortgages.

- Collateral arrangements are detailed in credit proposal.

- Bank’s legal adviser establishes the required legal documentation for a borrower’s legal standing and enforcement of the bank’s interest.

- Mortgage documents are properly vetted by Bank’s legal adviser.

- Registered mortgage of property are supported by registered irrevocable general power of attorney to sell the property.

- Bank has proper inventory of standard security documentations vetted by Legal counsel.

Valuation of collateral:

- Credit administration department independently will control and match the value of cash collateral which will be liened to the bank and against which borrowings are/ will be allowed as per approval.

- Value of Inventory and machineries supplied by client will be cross checked.

- Credit administration department will ensure receivables that actually exist and that past due. Disputed and other items with impaired collateral value to be identified and removed from collateral pool.

- Value is sourced from independent appraisals addressed to the bank.

Insurance:

Bank have taken insurance policy. Insurance policy shall be taken covering all possible risks. Branches shall ensure that insurance Policy is current and renewed on a timely basis. Insurance shall be obtained from a reputed company.

Cross Border Risk:

The bank takes/ will take care of /analyze the risks involved with Cross Border lending. Risks associated with import of a commodity are kept in mind which may basically take the form of failure of the foreign supplier to: –

- Supply goods of specified standard and quality.

- Supply the contracted goods timely.

CREDIT ASSESSMENT & RISK GRADING

Credit Assessment:

A thorough credit and risk assessment is to be conducted before granting of loans, and once approved; all facilities are to be reviewed at least annually. Credit assessment will be presented, in a credit application duly signed/approved by the official of the branch.

In case an account deviates from the guidelines the same should be identified in credit applications and justification for approval should be provided by the originating officials of the branch. Bank will conduct financial analysis on a regular basis & monitor changes in the client’s financial condition.

Before sending proposal to the approving authority, the originating officials of the branch shall ensure that the following steps/formalities have been taken/completed properly and incorporated in the credit proposal appropriately:

- Current CIB Report obtained

- Repayment sources of the borrower has been established by financial analysis

- Purpose and amount with types of loan proposed by the borrower stated in the proposal.

- Earnings from the relationship properly assessed in the credit proposal.

- Pre-sanction Inspection report/call report/site visit report is in place.

- Management profile & Capital structure, Constitution, Date of Establishment are stated in the proposal.

- Experience of Borrowers, business skills, management & successions are properly mentioned in the proposal.

- Borrower’s Rating in the Industry is assessed along with overall industry concerns and borrower’s strength & weakness relative to its competitors are identified.

- Industry’s position along with supplier and buyer risk is analyzed.

- Borrower credit worthiness is established by review of, 3 years historical financial statements and past track record.

- Cash Flow analysis justifying client’s ability to repay is reflected in the credit proposal.

- Industry and Business analysis is done in the proposal.

- Credit proposals clearly mention current outstanding against all limits.

- Audited financials, Large Loan position etc. are reflected in the credit proposals.

- Branches ensure that collateral has been properly valued, verified and are managed.

- Account conduct of the borrower & his allied concerns have been done.

- Adequacy and the extent of Insurance coverage are assessed.

- Policy compliance is clearly stated in the Credit Proposal.

- Changes in pricing of facilities are highlighted in credit proposal.

- Usage of borrowed fund is confirmed through financial statement analysis.

- Borrowers Risk Grade has been done as per Bangladesh bank Guidelines examined & approved by the authorized official and stated in the credit proposal.

CREDIT MEMORANDUM (CM) / CREDIT PROPOSAL:

The Credit Memorandum (CM)/ Credit Proposal should contain:

- Correct name of Individual borrower/proprietor/partners/Directors, status in the Co., % of share holding of the directors in the co./firm. Age, present (residential) and permanent address with phone number

- Account number and date of account opening.

- Nature of business

- Constitution

- Capital structure

- Date of establishment of business/ Date of incorporation

- Date of commencement of business

- Business Net worth

- Banking relationship history

- Management profile

- Personal Net worth of the individual/proprietor/partners/directors.

- Recycling/ periodical adjustment of the existing credit facility during last 3 years.

- CIB status.

- Assigned Risk Grade.

- Credit allowing capacity of our bank (as per Bangladesh bank single Exposure limit).

- Facility Structure: –

- Nature of Advance

- Amount of Limit

- Purpose

- Margin/Equity

- Interest, Commission, Other charges

- Mode of repayment

- Validity/Expiry

- Security: –

- Primary

- Collateral

- Others

- Cost of project (where applicable): –

- Land

- Building

- Other structures

- Machineries

- Others

- Working capital assessment/ Assessment of the requirement.

- Financial highlight

- Business performance of the client/allied concerns with our bank/ other banks

- Import: –

- Export: –

- Earnings from the client (Last 3 years) and projected earnings from the relationship

- Sales profitability (Last 3 years), projected sales

- Cash Flow

- Experience of Borrowers, business skills, management & successions

- SWOT

- Major 5 Competitors

- Possible risks & Risk mitigating factors

- Other Terms, Conditions & Covenants

Risk Assessment Areas:

Borrower Analysis:

Full particulars of the proprietor, partners, directors, etc to be examined, their management capability to be ascertained. Overall performance and credit status of the allied concerns of the client i.e. group will be assessed.

Industry Analysis:

Before extending credit in an area, over all business conditions of that area/ sector will be critically examined, prospects and problems to be ascertained.

Supplier/ Buyer Analysis:

Lending decision will be preceded by an intensive analysis on whether the borrower depends on a single or a very few customer or gets the supply of the raw materials/ dealing items from a single supplier.

Historical Financial Analysis:

An analysis of a minimum of 3 years historical financial statements of the borrower shall be presented. The analysis shall address the quality and sustainability of earnings, cash flow and the strength of the borrower’s balance sheet.

Projected Financial Performance:

Where term facilities (tenor more than 1 year) are proposed, borrower’s future / projected financial performance should be provided, indicating an analysis of the sufficiency of cash flow to service debt repayments.

Adherence to lending guidelines:

Credit proposals to be prepared in line with Bank’s lending Guidelines. A credit application/proposal will clearly mention whether or not the proposal complies with the bank’s lending guidelines.

Mitigating Factors:

In credit assessment, possible risks, such as margin sustainability and / or volatility , high debt load ( leverage/ gearing ), over stocking or debtor issues, rapid growth, acquisition or expansion, new business line/ product expansion, management changes or succession issues, customer or supplier concentrations and lack of transparency or industry issues and their mitigating factors to be identified.

Loan Structure:

Amount and tenor of loan will be fixed justifiably depending on income generation prospect, Projected repayment capacity and the purpose of the loan.

Security:

Our banks’ lending will generally be adequately securitized. Securities to be obtained, will be acceptable, valuable, easily marketable & defect less.

Credit Risk Grading (CRG)

Credit risk grading is an important tool for credit risk management as it helps the Banks & financial institutions to understand various dimensions of risk involved in different credit transactions. The aggregation of such grading across the borrowers, activities and the lines of business can provide better assessment of the quality of credit portfolio of a bank or a branch. In line with the above expectation our bank will undertake gradation of credit risks taking into consideration the varied complexities involved in lending operation. CRG with the above expectation will be a mandatory replacement of LRA. (Our bank has already adopted a Credit Risk Grading System as per Bangladesh bank CRG Manual. The details of CRG are as under:-)

DEFINITION OF CREDIT RISK GRADING (CRG)

- The Credit Risk Grading (CRG) is a collective definition based on the pre-specified scale and reflects the underlying credit-risk for a given exposure.

- A Credit Risk Grading deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure.

- Credit Risk Grading is the basic module for developing a Credit Risk Management system.

USE OF CREDIT RISK GRADING

- The Credit Risk Grading matrix will allow application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a unit, line of business, the branch or the Bank as a whole.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein either a borrower or a particular exposure/facility is rated

- Risk grading would also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk profile of a Bank. It is also relevant for portfolio level analysis.

REGULATORY DEFINITION ON GRADING OF CLASSIFIED ACCOUNTS

Irrespective of credit score obtained by a particular obligor, grading of the classified names will be in line with Bangladesh Bank guidelines on classified accounts, which is extracted from “PRUDENTIAL REGULATIONS FOR BANKS: SELECTED ISSUES” by Bangladesh Bank as under:

Basis for Loan Classification:

(A) Objective Criteria:

- Any Continuous Loan if not repaid/renewed within the fixed expiry date for repayment will be treated as irregular just from the following day of the expiry date. This loan will be classified as Sub-standard if it is kept irregular for 6 months or beyond but less than 9 months, as `Doubtful’ if for 9 months or beyond but less than 12 months and as `Bad & Loss’ if for 12 months or beyond.

- In case any installment(s) or part of installment(s) of a Fixed Term Loan is not repaid within the due date, the amount of unpaid installment(s) will be termed as `defaulted installment’.

In case of Fixed Term Loans, which are repayable within maximum 5 (five) years of time: –

If the amount of `defaulted installment’ is equal to or more than the amount of installment(s) due within 6 months, the entire loan will be classified as ‘Sub-standard’.If the amount of ‘defaulted installment’ is equal to or more than the amount of installment(s) due within 12 months, the entire loan will be classified as ‘Doubtful’.If the amount of ‘defaulted installment’ is equal to or more than the amount of installment(s) due within 18 months, the entire loan will be classified as ‘Bad & Loss’.

In case of Fixed Term Loans, which are repayable in more than 5 (five) years of time: –

- If the amount of ‘defaulted installment’ is equal to or more than the amount of installment(s) due within 12 months, the entire loan will be classified as ‘Sub-standard.’

- If the amount of ‘defaulted installment’ is equal to or more than the amount of installment(s) due within 18 months, the entire loan will be classified as ‘Doubtful’.

- If the amount of ‘defaulted installment ‘is equal to or more than the amount of installment(s) due within 24 months, the entire loan will be classified as ‘Bad & Loss’.

Qualitative Judgment:

If any uncertainty or doubt arises in respect of recovery of any Continuous Loan, Demand Loan or Fixed Term Loan, the same will have to be classified on the basis of qualitative judgment be it classifiable or not on the basis of objective criteria.

But even if after resorting to proper steps, there exists no certainty of total recovery of the loan, it will be classified as ‘Doubtful’ and even after exerting the all-out effort, there exists no chance of recovery, it will be classified as ‘ Bad & Loss’ on the basis of qualitative judgment.

The concerned bank will classify on the basis of qualitative judgment and can declassify the loans if qualitative improvement does occur.

COMPUTATION OF CREDIT RISK GRADING

The following step-wise activities outline the detail process for arriving at credit risk grading.

redit risk for counterparty arises from an aggregation of the following:

Financial Risk

- Business/Industry Risk

- Management Risk

- Security Risk

- Relationship Risk

a)Evaluation of Financial Risk:

This typically entails analysis of financials i.e. analysis of leverage, liquidity, profitability & interest coverage ratios. To conclude, this capitalizes on the risk of high leverage, poor liquidity, low profitability & insufficient cash flow.

Evaluation of Business/Industry Risk:

The evaluation of this category of risk looks at parameters such as business outlook, size of business, industry growth, market competition & barriers to entry/exit..

b)Evaluation of Management Risk:

Risk that counterparties may default as a result of poor managerial ability including experience of the management, its succession plan and team work.

c)Evaluation of Security Risk:

Risk that the bank might be exposed due to poor quality or strength of the security in case of default. This may entail strength of security & collateral, location of collateral and support.

d)Evaluation of Relationship Risk:

These risk areas cover evaluation of limits utilization, account performance, conditions/covenants compliance by the borrower and deposit relationship.

According to the importance of risk profile, the following weight ages are proposed for corresponding principal risks.

Principal Risk Components: Weight:

- Financial Risk 50%

- Business/Industry Risk 18%

- Management Risk 12%

- Security Risk 10%

- Relationship Risk 10%

Principal Risk Components: Key Parameters:

- Financial Risk Leverage, Liquidity, Profitability & Coverage ratio.

- Business/Industry Risk Size of Business, Age of Business, Business Outlook Industry Growth, Competition & Barriers Business

- Management Risk Experience, Succession & Team Work.

- Security Risk Security Coverage, Collateral Coverage and Support.

- Relationship Risk Account Conduct ,Utilization of Limit, Compliance of

After the risk identification & weight age assignment process (as mentioned above), the next steps will be to input actual parameter in the score sheet to arrive at the scores corresponding to the actual parameters.

This manual also provides a well programmed MS Excel based credit risk scoring sheet to arrive at a total score on each borrower. The excel program requires inputting data accurately in particular cells for input and will automatically calculate the risk grade for a particular borrower based on the total score obtained.

The following is the proposed Credit Risk Grade matrix based on the total score obtained by an obligor.

Number | Risk Grading | Short Name | Score |

1 | Superior | SUP |

|

2 | Good | GD | 85+ |

3 | Acceptable | ACCPT | 75-84 |

4 | Marginal/Watch list | MG/WL | 65-74 |

5 | Special Mention | SM | 55-64 |

6 | Sub-standard | SS | 45-54 |

7 | Doubtful | DF | 35-44 |

8 | Bad & Loss | BL | <35 |

CREDIT RISK GRADING PROCESS

- Credit Risk Grading will be completed for all exposures (irrespective of amount) other than those covered under Consumer and Small Enterprises Financing Prudential Guidelines and also under The Short-Term Agricultural and Micro – Credit.

- Borrowers Risk Grade should be stated in the Credit Proposal.

- For Superior Risk Grading (SUP-1) the score sheet is not applicable. This will be guided by the criterion mentioned for superior grade account i.e. 100% cash covered, covered by government & bank guarantee.