Performance of the Trust Bank Limited

Trust Bank Limited is a scheduled commercial bank established under the Bank Companies Act 1991 and incorporated as a public limited company under the companies act, 1994 in Bangladesh on 17 June 1999 with primary objective to carry on all kinds of banking businesses in and outside. As on 31 December 2006, the bank had 18 branches. By the 31 October 2008 the bank has opened another ten branches gearing the total number as 30. The comparative performance of the bank among different years appears as follows:

A) TREND ANALYSIS:

ANALYSIS FROM THE BALANCE SHEET:

For the purpose of analysis the financial data of 2005, 2006, 2007 and 2008 have been taken

based on the availability of the data. The key points of the financial statements take the following figure:

| Particulars | 2008 | 2007 | 2006 | 2005 |

| Authorized Capital | 2000000000 | 2000000000 | 2000000000 | 1000000000 |

| Paid-up Capital | 50,00,00,000 | 500000000 | 500000000 | 350000000 |

| Statutory Reserve | 21,46,77,986 | 113138916 | 67881642 | 24604805 |

| Shareholders’ Equity | 115,42,61,983 | 991972309 | 870685941 | 454301755 |

| Fixed Assets | 14,60,54,811 | 110616082 | 86179587 | 61369226 |

| Total Assets | 2119,75,92,200 | 1478,21,51,192 | 12059710225 | 7858833009 |

| Total Deposits | 1898,59,51,094 | 12704902083 | 9314952180 | 4483256901 |

| Long-term Debt | 42,60,00,000 | 660000000 | 1430000000 | 2340000000 |

| Loans and Advances | 1318,80,92,885 | 9738323349 | 6804448553 | 4358314092 |

| Investment | 326,03,72,599 | 2447953778 | 3220777070 | 1896920200 |

a AUTHORIZED CAPITAL:

The Authorized Capital of the bank was Tk 100.00 crore in 2005 which was increased in subsequent year 2006 by twofold. In 2007 and also in 2008 the authorized capital stands for the same worth of Tk. 200.00 crore. It is due to the bank’s future expansion philosophy and to keep rein with the market competitiveness and also for the requirement of Bangladesh Bank circular.

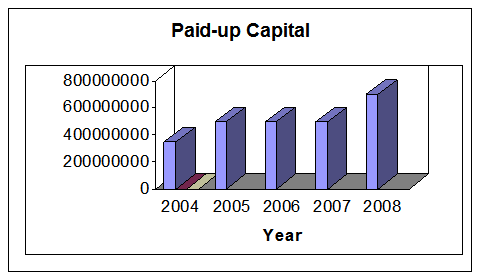

b PAID-UP CAPITAL : The paid-up capital was also increased by Tk 15.00 crore in 2005 materializing the total value of Tk50.00 Crore. The increment was done because of the bank’s future expansion philosophy and to keep rein with the market competitiveness. In the year 2008 the bank increased its Paid-up capital up to Tk.70.00 Crore by issuing shares through IPO.

The paid-up capital was also increased by Tk 15.00 crore in 2005 materializing the total value of Tk50.00 Crore. The increment was done because of the bank’s future expansion philosophy and to keep rein with the market competitiveness. In the year 2008 the bank increased its Paid-up capital up to Tk.70.00 Crore by issuing shares through IPO.

c SHAREHOLDERS’ EQUITY:

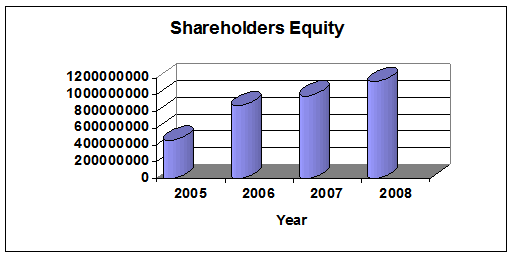

The equity of the Shareholders in 2005 was Tk.454,301,755. In 2006 it has increased by 91.65% as the total of Tk.870,685,941. In 2005, it was amounted Tk.991,972,309 being the increase of 118.38% on that of 2005. In the year 2008 the Shareholders Equity stood Tk.115,42,61,983 which was 154.07% higher than the year 2005. It is due to the expansion of the bank and the financial more strength of the army Welfare Trust.

d STATUTORY RESERVE :

d STATUTORY RESERVE :

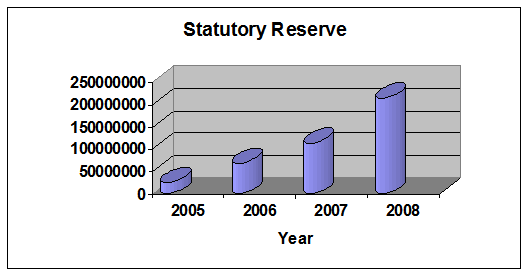

In 2005, the Statutory Reserve of the bank was Tk. 24,604,405 which stands at Tk. 67,881,642 in the year 2006. It was an increase by a gross amount of Tk 43,276,837 or by 175.88% on that of 2005. In 2007, the Statutory Reserve stands at Tk. 113,138,916, an increase by 359.83%. In the year 2008 the Statutory Reserve was near about double than the year 2007. It is due to the rise of the bank’s overall capital and the regulation under the Banking Act 1991 to keep a certain percentage (20%) of share capital or profit as statutory reserve.

In 2005, the Statutory Reserve of the bank was Tk. 24,604,405 which stands at Tk. 67,881,642 in the year 2006. It was an increase by a gross amount of Tk 43,276,837 or by 175.88% on that of 2005. In 2007, the Statutory Reserve stands at Tk. 113,138,916, an increase by 359.83%. In the year 2008 the Statutory Reserve was near about double than the year 2007. It is due to the rise of the bank’s overall capital and the regulation under the Banking Act 1991 to keep a certain percentage (20%) of share capital or profit as statutory reserve.

e FIXED ASSETS :

Fixed assets include Furniture and Fixture, Office equipment, Motor vehicles, office renovation and leasehold land. The depreciation on the fixed assets is charged on straight line basis at the following rates:

Furniture and Fixture 10% p.a

Office equipment 20% p.a

Motor vehicles 20% p.a

Office decoration 12% p.a

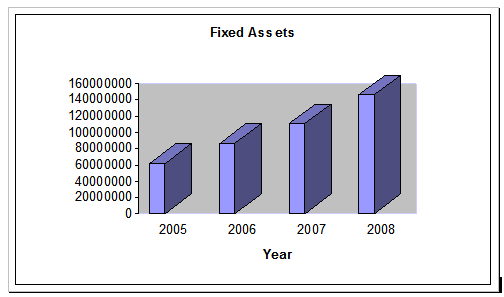

Fixed assets after deducting accumulated depreciation were in 2005 Tk.61,369,226, in 2006 Tk.83,971,729 , in 2007 Tk.110,616,082 and in 2008 Tk.14,60,54,811. It is because of the expansion of branches during that period.

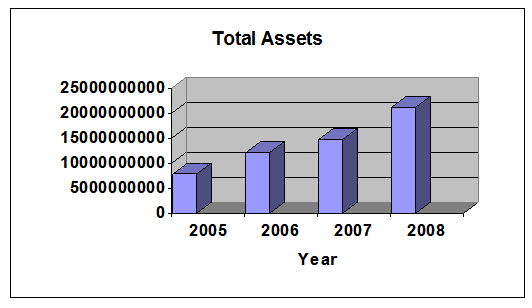

f TOTAL ASSETS :

f TOTAL ASSETS :

Total assets of the bank consists of –

Total assets of the bank consists of –

- Cash in hand and with Bangladesh Bank and Sonali Bank.

- Balance with other banks and financial institution.

- Money at call and short notice.

- Loan and Advances.

- Fixed assets (Furniture and Fixture, Office equipment, Motor vehicles, Office Renovation and LeaseholdLand)

- Other Assets

Total Assets of the bank was Tk.7, 858,833,009 in 2005 and Tk.12, 085,815,830 in 2006- a 53.786% increment. The value of total assets stood at Tk.14,807,905,231 in 2005-a 88.42% increase. It shows the advancement of the bank responding the market.

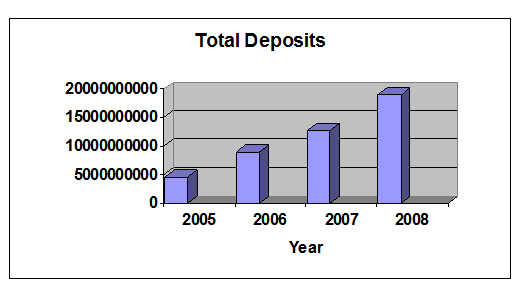

g TOTAL DEPOSITS :

The Total Deposit of the bank was-

| 2008 | 2007 | 2006 | 2005 |

| 1898,59,51,094 | Tk. 12,704,902,083 | Tk. 9,042,183,740 | Tk. 4,483,256,901 |

The pictorial graph and the subsequent numerical figure show that the deposit collection was more than double than that of 2005. In 2007, total deposit was increased by 40.5% than the deposit of accumulated in 2006. So it is vivid from the viewpoint of deposit collection the performance of the bank in 2006 was far better than 2007 and in 2008 the position was much much better than 2007.

The pictorial graph and the subsequent numerical figure show that the deposit collection was more than double than that of 2005. In 2007, total deposit was increased by 40.5% than the deposit of accumulated in 2006. So it is vivid from the viewpoint of deposit collection the performance of the bank in 2006 was far better than 2007 and in 2008 the position was much much better than 2007.

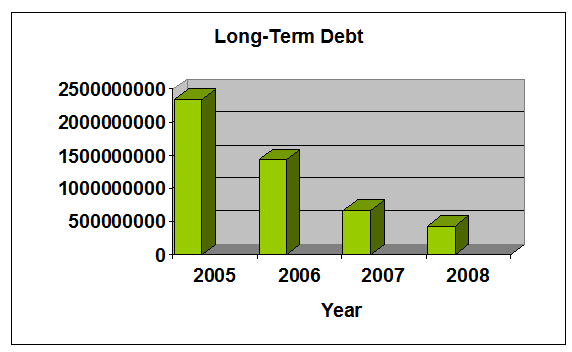

h LONG-TERM DEBT :

Here, the long term debt represents the borrowing from other banks, financial institutions and agents. The illustration depicts that the long term debt of the bank significantly decreased in 2007. The year wise actual long term debt was as follows:

| 2008 | 2007 | 2006 | 2005 |

| Tk.42,60,00,000 | Tk.660,000,000 | Tk1,430,000,000 | Tk.2,340,000,000 |

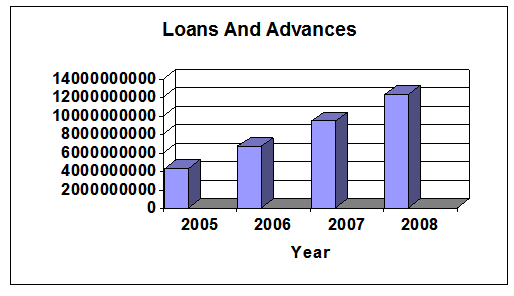

i LOANS AND ADVANCES :

i LOANS AND ADVANCES :

Loans and advances of the bank constitute different purpose loans (repair and maintenance of dwelling house, customer durable loan scheme, car loan, term loan, loans against Trust Receipt etc), cash credit (cash credit, cash collateral) and overdraft (normal overdraft, secured overdraft).The total loans (excluding bill purchased & discounted), cash credits and overdrafts etc. for the four years was as follows-

| 2008 | 2007 | 2006 | 2005 |

| Tk.1232,30,04,330 | Tk.938,34,59,513 | Tk.669,04,08,551 | Tk.432,78,26,794 |

The graphical and numerical presentation depicts that loans and advances increased by 54.6% in 2006 and 116.82% in 2007 (taking 2005 as the base year). The growth level of loan and advances is about the same rate both in 2007 and 2008.

j INVESTMENT :

j INVESTMENT :

Investment includes investment in government securities and investment in shares. The numerical figure of investment appears as follows:

| 2008 | 2007 | 2006 | 2005 |

| 326,03,72,599 | Tk. 2,447,953,778 | Tk. 3,220,777,070 | Tk. 1,896,920,200 |

Overall investment increased by 69.79% in 2006 being a total of Tk 3,220,777,070. But in 2007 the value of investment decreased by Tk 772,823,292 or 24% in comparison with that of 2006. In the year 2008 the overall investment was increased by 33.19% than the year 2007. The graphical presentations of Yearly Investments are as follows:

ANALYSIS OF THE PROFIT AND LOSS ACCOUNT:

The profitability of any business concern can be understood by analyzing the Profit And Loss Account of that concern. Profit And Loss Account shows the revenue generated, corresponding expenditure and the resulting profit or loss. Analysis of the Profit And Loss Account of the Trust Bank Ltd. exhibits the following summarized information:

| Particulars | 2008 | 2007 | 2006 | 2005 |

| Gross Income | 222,32,73,678 | 1444597936 | 1046361480 | 535499256 |

| Gross Expenditure | 171,55,78,329 | 1218311568 | 829977294 | 467354988 |

| Profit before Tax | 50,7695,349 | 226286368 | 216384186 | 68144268 |

| Profit after Tax | 26,26,95,349 | 121286368 | 216384186 | 68144268 |

| Tax paid | 245000000 | 105000000 | —- | —- |

a OPERATING INCOME :

In this competitive market this bank earned Tk.1, 444,597,936 in 2007 which is 38.06% greater than the gross income of 2006. It clearly indicates that this is a growing organization and will continue its success in the coming years.

b OPERATING EXPENDITURE:

Here the ratio of expenditure in 2007 has decreased than that of previous year. But the percentage of expenditure has increased @ 46.79% in 2007 which is more than the percentage increase in the Gross revenue.

c PROFIT BEFORE TAX :

The Actual Profit before Tax of the bank was as under:

| 2008 | 2007 | 2006 | 2005 |

| 507,695,349 | Tk. 296,261,558 | Tk. 216,384,186 | Tk. 68,114,268 |

From the information mentioned above a comment can be made that Year-2006 was its “Golden Age”. But in 2007 it also increased its “profit before tax” and gained a honorable position in the banking sector. In the year 2008 the Bank earned a remarkable Profit which is near about double than the profit of the year 2007.

d PROFIT AFTER TAX :

The Actual Profit after Tax of the bank was as under :

2008 | 2007 | 2006 | 2005 |

| 262,695,349 | Tk. 121,286,368 | Tk. 216,384,186 | Tk. 68,114,268 |

And the amount for the provision of tax was –

2008 | 2007 | 2006 | 2005 |

| 245,000,000 | Tk. 105,000,000 | Tk.52500000 | Tk. 26250000 |

From the above mentioned statement, it is vivid that the net profit touches the peak in 2006 by accomplishing a stunning rise of 217.68%. But the journey of increasing profit can be backward in 2007. The After Tax Net Profit went down by 43.95% in 2007 comparing the profit of 2006 the Provision for Tax played a significant role in this respect. Of course, the After Tax Net Profit in the year 2008 shows the upper trend which was 116.59% higher than the year 2007.

NUMBER OF BRANCHES:

| Particulars | 2005 | 2006 | 2007 | 2008 |

| Number of Branches | 15 | 18 | 26 | 30 |

Like other commercial banks it has not centralized its branches only in Dhaka and around Dhaka. It is trying hardly to spread the banking benefits to the door of general people. So it added three new branches in the Year-2005, four new branches in 2006 and six new branches in the year 2007.

TREND OF OTHER FINANCIAL STATEMENT ISSUES:

| Sl No | Particulars | 2008 | 2007 | 2006 |

| 01 | Total contingent liabilities & Commitments | 7885,364,349 | 4681077063 | 3123318980 |

| 02 | Amount of classified loans during current year | 174369437 | 128967084 | 216384186 |

| 03 | Provisions kept against classified loans | 63676000 | 58000000 | 41293255 |

| 04 | Provision surplus/Deficit | – | 2315796 | – |

| 05 | Interest earning assets | 18608058132 | 13,401,393,133 | 11,380,077,637 |

| 06 | Non-interest earning assets | 2589534068 | 1,406,512,098 | 679,632,588 |

| 07 | Incomes from investment | 170817002 | 194,479,592 | 177,745,964 |

| 08 | Earning per share | 52.54 | 24.26 | 44.16 |

| 09 | Net income per share | 52.54 | 24.26 | 44.16 |

B) RATIO ANALYSIS:

| SL no | Particulars | 2008 | 2007 | 2006 |

| 01 | Capital Adequacy Ratio | 9.31 | 12.49% | 15.20% |

| 02 | Credit Deposit Ratio | 69.46 | 76.65% | 75.25% |

| 03 | Percentage of classified loans against total loans and advances | 1.32 | 1.32% | 1.47% |

| 04 | Cost of fund | 8.47 | 7.53% | 7.60% |

| 05 | Return on Investment(ROI) | 20.05 | 10.88% | 23.01% |

| 06 | Return on Assets(ROA) | 1.24 | 0.82% | 1.79% |

| 07 | Price Earning Ratio | N/A | N/A | N/A |

Comment: Although the cost of fund went down in 2007 by 0.07%, the profitability of the bank was declining. Return on Investment went down significantly by 12.13% and the Return on Assets also went down by more than half i.e. 0.97%. Moreover, there was a shortage of capital adequacy in 2007 as the ratio fell down from 15.20% to 12.49%, although the Credit in response to Deposit increased by a little bit, by 1.40%. So it can be said that investment was not efficiently made. Concentration should also be given to the Capital, Deposit and Credit Management.

CHAPTER FIVE

DISCUSSION AND FINDINGS

SWOT Analysis of Trust Bank Limited:

SWOT Analysis is an important tool for evaluating the company’s Strengths, Weaknesses, Opportunities and Threats. It helps the organization to identify hoe to evaluate its performance and can scan the macro environment, which is turn would help the organization to navigate in the TurbulenceOcean of competition. Following is given the SWOT analysis of The Trust Bank:

STRENGTHS:

Sponsors:

The Trust Bank has founded by The Army Welfare Trust. The main sponsor for this bank is Sena Kalyan Sangstha. The chairperson of this bank is Chief of Army Staff and directors are also appointed by the sangstha, that’s why the sponsor does not have any problem for the fund.

Top Management:

The top management of the bank, the key strength for The Trust Bank has contributed heavily towards the growth and development of the bank. The top management officials are army’s highest position holder, so they have a good idea about the current situation.

Company goodwill:

The Trust Bank has created a good reputation in the banking industry of the country. Their main customers are army persons. The popularity of this bank is increase day by day also in the general public area.

Retail Banking:

The bank has already lunched retail-banking division to sell their products as well as increase customers or clients.

Modern Facilities and Computer:

From the very beginning The Trust Bank tries to furnish their work surroundings with modern equipment and facilities. For speedy service to the customer, The Trust Bank had installed money-counting machine in the teller counter. The bank has computerized banking operation under software called PC banking. More over computer printed statements are available to internal use and occasionally for the customers. The Trust Bank is equipped with telex and fax facilities.

Rousing Branches:

From the formative stage of The Trust Bank tried to furnish their branches by the impressive style. Their well-decorated branches gets attention of the potential customer, this is one kind of positioning strategy. The Millennium Branch is also impressive and is comparable of foreign banks.

Interactive Corporate Culture:

The corporate culture of The Trust Bank is very much interactive compare to other local organization. This interactive environment encourages the employee to work attentively. Science the banking jobs is very much routine work oriented and lovely environment boots up the work capability of the employees.

Online Banking:

It is so important for every bank because today’s world is very much dependent on computer which means E-banking. By offering such kinds of facilities TBL increase clients and maximize customer’s satisfaction.

Attractive location:

TBL branches location are attractive that most of branches are located near the army cantonments and also charming location, which convey historical evidence.

Infrastructure facilities:

TBL’s maintains good infrastructure inside and outside at the office that brings positive feelings about the banks in the minds of the customers. EX-separate room for manager and others senior officers which keep the individual personality.

Micro credit

There is a micro credit division, which is strength of TBL. Islamic banking Introduction of Islamic Banking

WEAKNESSES:

Limitation of Information System (PC Bank):

PC bank is not comprehensive banking software. It is desirable that a more comprehensive banking system should replace PC bank system.

Hierarchy Problem:

The hierarchy problem treated as a weakness for The Trust Bank, because the employee will not stay for a long. So there will be a chance of brain drain from this bank to other bank.

Advertisement Problem:

There is another weakness for The Trust Bank is advertisement. Their media coverage is so much low that people do not know the bank thoroughly.

Limited Branches:

Limited branches are another weakness of TBL among most other commercial bank.

OPPORTUNITIES:

Diversification:

The Trust Bank can pursue diversification strategy in expanding its current line of business. They do not serve not only the army but also the general people.

Business Banking:

The investment potential of Bangladesh is foreign investors. So EBL has opportunity to expand in business banking.

Credit Card:

There is an opportunity to launch Credit Card in Bangladesh by EBL. Beside this, EBL can acquire services for cards like VISA, MASTER CARD etc. So that they can enhance the market based card service.

New Branches:

TBL has great opportunity to expand branches in different EPZ and other commercial areas.

Expand Micro Credit Program:

This is the possible way to earn more profit by limited investment. If TBL emphasize in this

division it has huge opportunities to maximize their profit among other divisions.

THREATS:

Contemporary Banks:

The contemporary banks of The Trust Bank like: Dhaka Bank, Dutch Bangla Bank, National Bank, Mutual Trust Bank, Mercantile Bank are its major rivals. They are carrying out aggressive campaign to attract lucrative clients as well as big time depositors. The Trust Bank should remain vigilant about the steps taken by these banks, as these will in turn affect The Trust Bank strategies.

Multinational Bank:

The Rapid expansion of multinational bank poses a potential threat to new PCB’s. Due to the booming energy sector, more foreign banks are expected to operate in Bangladesh. Moreover, the existing foreign banks such as HSBC, AMEX, CITI N.A, and Standard Chattered Grindlays are now pursing an aggressive branch expansion strategy. Since the foreign banks have tremendous financial strength, it will pose a threat to local bank to a certain extant in terms of grabbing the lucrative clients.

Default Culture:

Default culture is very much familiar in our country. For a bank, it is very harmful. As The Trust Bank is new, it has not faced it seriously yet. However as the bank grows older it might become big problems.

Others:

- Poor economical condition of our country.

- Entrance of new private commercial banks

- Different attractive service offered by some foreign banks.

- Daily basis interest on deposit offered by some Multinational banks.

- Existing cards service of different banks.

CONCLUSION AND RECOMMENDATION

CONCLUSION

Trust Bank limited pursues decentralized management polices and gives adequate work freedom to the employees. This results in less pressure for the workers and acts as a motivational tool for them, which gives them, increased encouragement and inspiration to move up the ladder of success. The profit earned by the bank is used to the welfare activities of the Trust. The economic service of the bank is open to all caste and class of people. The bank is formatting and accomplishing various welfare projects and activities for the socio economic infrastructural development of the country and the active participation to the up gradation of the comparative feeble class of the society, instead of accumulating profit. It has also been linked with many foreign banks to facilitate the foreign currency transfer by the members of armed forces working in the UN and emigrant Bangladeshi. The report is aimed at studying and understanding the various services offered by TBL to its clients. In addition, the report also studies how Trust Bank Limited has maintained growth in its general banking business by maintaining and enhancing its relationship with its clients.

The success of Trust Bank limited is largely credited to its friendly, co-operative approach, understanding the special banking needs of each and every client and concern for the benefits and welfare. From the beginning, the prime objective of Trust Bank limited was to increase capitalization, to maintain disciplined growth and high corporate ethics standard and enhance the health of the share holders. Its customer service is very much impressive than of other financial institutions. Their effective strategy, time demand offerings, up to date rules and regulations to cope with international market and their friendship customer services easily impress the clients. So, now Trust Bank limited is in leading position in Financial Institutional sectors in Bangladesh. The financial performance of the bank in recent years is pretty well. Moreover, any laxity in operational ground can considerably be compensated through the cordial services provided by a staff of talented officers or employees.

Proper financial system of a country can contribute towards the development of that country’s economy. In our country Bangladesh, banks have a leading power to its financial system. For this reason, the banks should have a potential role to make our financial system.

In this arena, private commercial banks are playing a vital role in the development of our economy. But Govt. and Bangladesh Bank play a crucial role to the private commercial banks.

RECOMMENDATION

Through conducting this study I have acquired some practical knowledge about export import business in Bangladesh & and other relevant matters. Now I would like to provide some recommendation which may be helpful to promote the export import business of The Trust Bank Limited as well as Bangladesh. As per earnest observation some suggestions for improvement of the situation are given below:

- For attracting more clients The Trust Bank Limited has to create a new marketing strategy which will increase the total export import business.

- Effective and efficient initiative is necessary to recover the default loans.

- Attractive incentive package for the exporter will help to increase the export and accordingly it will diminish the balance of payment gap of The Trust Bank Limited.

- Introduction of attractive WES which will increase the remittance.

- For the foreign exchange officials long terms training very much essential.

- For a sound and stale foreign exchange operation, The Trust bank Limited should give more emphasis on the foreign exchange department.

- Foreign exchange operation of other renowned commercial banks is more dynamic and less time consuming. The Trust Bank Limited should take some initiative to compete with those banks.

- Bank can provide foreign market reports which will enable the exporter to evaluate the demand for their products in foreign countries.

BIBLIOGRAPHY

- Commercial Bank Management -by Peter S. Rose

- Bank Management & Financial Services – by Peter S. Rose & Sylvia C.Hudgins

- Annual Reports of Trust Bank Ltd. – for the Year 2005, 2006, 2007 & 2008

- Trust Bank Manual – on General Banking

- Office Circular of Trust Bank Ltd – Dated 27.06.07, Ref.TBL/HO/CR/016/07, & Dated: 15.08.07, Ref.TBL/HO/CR/017/07 .

- Auditors Reports on Trust Bank Ltd. -2003, 2004, 2005 & 2006.

- National Board of Revenue – Ref. JARABO/TAX-7/A: A: B: /04/2007/210, Dated: 05.11.2007

- BIBM Library, – Annual reports & Internship reports on Commercial Banks.

- TBL Training Institute -Synopsis.

- Annual Reports of Bangladesh Bank

- Bangladesh Bank Bulletin

- Brochure of Trust Bank Ltd.

- E-mail of Trust Bank Ltd.

- Personnel of TBL Principal Br