Executive Summary

Islami Bank Bangladesh Ltd. (IBBL) started commercial operation on March 30, 1983 under the ambit of Banking Company’s Ordinance 1962 later on the Banking Companies Act, 1991 as the first interest free Shariah based commercial bank with an objective of catering Islamic Shariah based financial products. At present IBBL is operating with 207 Branch different areas of the country. In conventional bank the investor is assured of a predetermined rate of interest whereas, IBBL promotes risk sharing between provider of capital (investor) and the user of funds (entrepreneur).

IBBL, Kawran Bazar Branchmobilizes deposit on Mudaraba (Profit sharing) and Al-Wadiah (current account) basis under the Islamic Shariah. The depositors of Kawran Bazar Branchare business partners of it and they share the profit or loss of the business. For the better use of the depositor’s fund, the IBBL, Kawran Bazar Branchinvests its funds as per different modes of investment or financing by Islamic Shariah. Most of the investment of IBBL, Kawran Bazar Branchare on the by Bai- Mode (buying & selling) and HPSM. In this mode branch sells specified goods to the clients on cost plus agreed upon profit or at a negotiable price payable after a certain fixed period. The other ideal mode of IBBL, Kawran Bazar Branchis Musharaka (partnership). In Musharaka, Kawran Bazar Branchshares profit/loss of the business with the client. In 2009 IBBL, Kawran Bazar Branchinvests under Bai-Murabaha mode 23.57%, Bai-Muajjal mode 6.80%, Bai-Salam 0.58%, Higher Purchase under Shirkatul Melk (HPSM) 54.19%, and Musharaka mode 13.33%, Quard 1.39%, Foreign Bill Purchase (FBP) 0.10%.

The percentage of recovery of investment of IBBL, Kawran Bazar Branchis nearly 90 to 95% because bank considers strongly the entrepreneurs efficiency and integrity as well as five C’s such as capacity, character, capital, condition, and collateral. From the last 3 years, IBBL, Kawran Bazar Branchinvestment is progressing in a greater extent. Investment of the bank increased to Tk.1532.341 million as on 31st December 2008, from Tk. 1755.893 million as on 31st December 2008 and showing an increase of Tk. 2186.550 million up to 31/12/2009. This increased investment growth of the bank is due to the thrust given to promote investment for effective utilization of depositors’ fund.

So, overall investment performance of IBBL, Kawran Bazar Branchis increasing day by day. Because most of the people in our country are religious minded and they want to invest their money according to Islamic Shariah. Moreover people of all walks of life can easily transact with IBBL comparing to other commercial private banks in the country.

Introduction

1.1 Origin of the Report

This Internship Report has been preparing under the Internship program, an indispensable part of the Bachelor of Business Administration (BBA) program. For the internship purpose, I chose Islami Bank Bangladesh Ltd. (IBBL), Kawran Bazar Branch hand prepare this report on the investment related activities of the organization.

1.2Significance of the study

Islami Bank Bangladesh Ltd. is the biggest Bank in Bangladesh in private sector. There are a few number

Of private Banks that can compete with IBBL. The Banking system aiming to gain the goal of Islamic

economy through setting a well designed Islamic Monitory system. Regarding use of money Islam has

Its clear-cut instruction through some distinctive guidelines. Avoiding interest (Riba), restricting

exploitation & speculation etc. are major guidelines in this process. So Islamic Banking system is doing

Banking business under Islamic guide lines.

1.3Objective of the Study

The primary objective of this report is to observe the investment related activities for the Investment Department of Islami Bank Bangladesh Ltd., Mirpur-10 Branch. The other objectives include:

· To understand the different modes of investment.

· To familiarize with the various investment schemes.

· To get the practical exposure of the banking activities.

· To adapt with the corporate environment.

· To understand the investment policy of IBBL with other banks.

1.4 Scope of the Study

In this report I have focused on all the qualitative which include profiles of IBBL, investment modes like Bai mode, Profit & loss sharing, bearing mode, Rent sharing mode, different schemes of investment such as household durable schemes, housing investment scheme, transport investment scheme, car investment scheme, investment scheme for doctors small business investment scheme, rural development scheme, etc. and lastly financial performances have been depicted.

1.5 Methodology of the Study

Methodology is the process or system through which a study is being carried out for the purpose of collection of information that is required is collection with the study for reaching a conclusion on that

Study.

This section of the report contains three Questionnaires, as follows:

a) Questionnaires for common Clients

b) Questionnaires for Investors

c) Questionnaire for Banking

1.6 Data collection method

The data required for this study were collected from both primary and secondary sources; however, majority of the information was collected from secondary sources.

a) Primary source

Primary data was collected form

- Branch Manager & Second Officer.

- Face to face conversation with employees and staffs.

- Practical work experience.

- Face to face conversation with clients.

b) Secondary source

The secondary data has been collected from

- Annual Report of Islami Bank Bangladesh Limited.

- Various prescribed forms of investment were analyzed.

- IBTRA Library.

- Manuals of Investment of IBBL.

- Different text books & materials.

- Website of the Islami Bank Bangladesh Limited.

- The major portion of the data source used for this report is a secondary one.

1.5 Limitation of the Report

I have faced some problems during preparing my report:

· Lack of experiences has acted as constraints in the way of meticulous exploration on the topic.

· Lack of current information.

· Shortage of time for preparing the report in order.

· The study was conducted mostly on secondary data.

Background of Islami Bank Bangladesh Limite

2.1 History of Islami Bank Bangladesh Ltd.

In the late seventies and early eighties, Muslim countries were awoken by the emergence of Islami Bank which provided interest free banking facilities. There are currently more than 300 interest free institutions all over the world. Islami Bank now a days not only operate in almost all Muslim countries but have extended their wings to the western world to serve both Muslim and non Muslim customers. In case of Islami Banking, the establishment of Mitghamar Local Savings Bank in 1963 is said to be a milestone for modern Islami Banking. The history of Islami Banking can nevertheless be traced back to the birth of Islam.

In 1974, Bangladesh signed the Charter of Islamic Development Bank and committed itself to reorganise its economic and financial system as per Islamic Shariah (legal framework of Islamic Ideology).

In 1978, Bangladesh recommended in Islamic Foreign Minister Conference in Senegal towards systematic efforts to Islamic Banking.

In 1980, Foreign Minister Conference in Pakistan where Bangladesh Foreign Minister Prof. Shamsul Hoq, proposed for taking steps for Islamic Banking. Further, Bangladesh Bank sent representation abroad to study Islamic Banking System. Also, International Seminar held in Dhaka inaugurated by Bangladesh Bank Governor for early introduction of Islamic Banking.In 1981, President of the Peoples Republic of Bangladesh addressed the 3rd Islamic Summit Conference held at Makkah and Taif suggested, ”The Islamic countries should develop a separate banking system of their own in order to facilitate their trade and commerce.”

In 1982, IDB visited Bangladesh for study. They found contributions done by Islamic Economics Research Bureau (IERB) and Bangladesh Islamic Bankers Association (BIBA); they mobilized the seminars, public opinion through symposia & workshop. Professional activities reinforced by Muslim Businessman Society (now reorganized as Industrialists and Businessman Association). The body mobilized mainly equity capital for emerging Islamic Bank. Finally, in 1983 Islami Bank Bangladesh Limited (IBBL) came out to take the challenge of doing banking business.Islami Bank Bangladesh Limited (IBBL) is considered to be the first interest free bank in Southeast Asia. It was incorporated on 13-03-1983 as a Public Company with limited liability under the companies Act 1913. The bank began operations on March 30, 1983, with major share by the foreign entrepreneurs.

IBBL is a joint venture multinational Bank with 63.92% of equity being contributed by the Islamic Development Bank and financial institutions. The total number of branches in 2010 stood at 232. Now the authorized capital of the bank is Tk. 10,000 million and Paid op capital is Tk. 6,177.60 million.

2.2 Islamic Banking

Islamic bank is a financial institution whose status, rules and procedures expressly state its commitment to the principle of Islamic Shariah and to the banning of the receipt and payment of interest on any of its operations. -OIC

Ziauddin Ahmed says, “Islamic bank is essentially a normative concept and could be defined as conduct of banking in consonance with the ethos of the value system of Islam.”

It appears from the above definitions that Islamic bank is systems of financial intermediation that avoids receipt and payment of interest in its transactions and conducts its operations in a way that it helps achieve the objectives of an Islamic economy. Alternatively, this is a banking system whose operation is based on Islamic principles of transactions of which profit and loss sharing (PLS) is a major feature, ensuring justice and equity in the economy. That is why Islamic bank is often known as PLS-banks.

2.3 Mission

To establish Islamic banking through the introduction of a welfare oriented banking system and also ensure equity and justice in the field of all economic activities, achieve balanced growth and equitable development through diversified investment operations particularly in the priority sectors and less developed areas of the country. To encourage socio-economic uplift and financial services to the low-income community particularly in the rural areas.

2.4 Vision

Our vision is to always strive to achieve superior financial performance, be considered a leading Islamic bank by reputation and performance.

· Our goal is to establish and maintain the modern banking techniques, to ensure the soundness and development of the financial system based on Islamic principles and to become the strong and efficient organization with highly motivated professionals, working for the benefit of people, based upon accountability, transparency and integrity in order to ensure stability of financial systems.

· We will try to encourage savings in the form of direct investment.

· We will also try to encourage investment particularly in projects which are more likely to lead to higher employment.

2.5 Objectives of Islamic Bank

The primary objective of establishing Islamic Bank all over the world is to promote, foster and develop the application of Islamic principles in the business sector. More specifically, the objectives of Islamic bank when viewed in the context of its role in the economy are listed as following:

To offer contemporary financial services in conformity with Islamic Shariah;

To contribute towards economic development and prosperity within the principles of Islamic justice;

Optimum allocation of scarce financial resources; and

To help ensure equitable distribution of income.

2.6 Essential Features of Islamic Bank

Prohibition of interest

The traditional capitalist banking system depends on interest. It receives interest for providing loans and pays interest for taking loans. The spread between these two interests is the source of its profit. But according to Islamic Shariah all types of interest is banned. So, Islamic bank does not carry on business of interest and it completely avoids the transaction of interest.

Investment based on profit

After departing from interest, the alternate ways of income for Islamic bank is investment and profit. Thus IBBL gives up any transaction of interest and makes investments based on profit. Bank distributes its profit to its depositors and shareholders.

Investment in Halal business

Islamic Shariah has banned the business of haram goods. For example, Islam not only forbids the drinking of alcohol but also banned any business of alcohol. Therefore, Islamic bank does not get any haram business and only do halal business.

Halal paths and procedures

Islamic Shariah also rejects any haram path or process in case of a halal business. Therefore, Islamic bank system only allows the halal path procedures of halal business.

2.7 Distinguishing Features of Conventional and IBBL

The distinguishing features of the conventional banking and IBBL are shown below:

2.8 Corporate information at a glance (As on July, 2009)

| Date of Incorporation | 13th March 1983 |

| Inauguration of 1st Branch (Local office, Dhaka) | 30th March 1983 |

| Formal Inauguration | 12th August 1983 |

| Share of Capital | |

| Local Shareholders | 41.77% |

| Foreign Shareholders | 58.23% |

| Authorized Capital | Tk.10,000.00 million |

| Paid-up Capital | Tk.6,177.60 million |

| Deposits | Tk.244,292.14 million |

| Investments (including Investment in Shares) | Tk.214,615.80 million |

| Foreign Exchange Business | Tk.462,370.00 million |

| Number of Branches | 212 |

| Number of SME Service Centers | 20 |

| Number of Shareholders | 52,164 |

| Manpower | 9588 |

2.9 Products & Services of the Bank

IBBL has the scope to explore the market niche through various types of IBBL instruments. IBBL offers wide range of IBBL products and services. It provides Mudaraba Savings Deposit, Mudaraba Term Deposit, Mudaraba Special Savings (Pension), Al-Wadeeah Current Account, Mudaraba Savings Bond, Mudaraba Monthly profit Deposit, Mudaraba Special Deposit, Mudaraba Hajj Savings, Mudaraba Muhor Savings, Mudaraba Foreign Currency Deposit, and Mudaraba Waqf Cash Deposit.

2.10 Structure of the organization:

Internship Position and Duties

3.1 Internship Duties and Position

I have done my internship program in Islami Bank Bangladesh Ltd. at Kawran Bazar Branch. It is one of the leading commercial private banks in our country. This bank was established in 1983 based on Islamic sahriah. Their vision is strive to achive superior financial performance and be considered a leading Islamic bank by reputation and performance. Especially I want to say about Kawran Bazar Branch. This branch is one of the busiest Branches. My internship program duration was for total 60 days. It was designed by Islami Bank Training and Research Academy (IBTRA). First 15 days I have done theoretical class in IBTRA. Then I went to the Kawran Bazar Branchfor practical experience with 45 days where I have learned properly Islamic banking and financial system. I got a lot of information and gather experience about IBBL as well as interest free banking system. After completion of theoretical part, I have gone to Kawran Bazar Branch.

3.2 Kawran Bazar Branch

I worked 45 days in this branch. In this branch, there were 66 employees. This branch is very busiest compare to other Branches. They were very pleased for me. All of them were very cooperative with me. I was working under several sections which are explained below:

3.2.1 Account opening section

I worked total 3 days in this section. This section is one of the busiest sections in this branch. Because, a new client can enter the banking system, to opening new account. Lot of customer arrive and try to collect information for account opening. I provided information about the account opening requirements to their clients. Customers need two copies passport size photo, commissioner certificate, introducer sign and nominee photo for their account opening.

3.2.2 Information Section

Lot of customers arrives every day for collecting information about the products, facilities, foreign exchange of this branch. Clients wanted to know the balance of their account by coming to this branch personally or by phone. They come to collect account statement, certificate, 7 days notice, address change, sign change, account transfer in this section.

3.2.3 Clearing Section

I worked total 4 days in this section. The main responsibilities were to receive several cheques from clients. I also attached seal in the front and the back side of the cheque for clearing. My responsibility was to ensure account number, account holder name, the accuracy of Tk. In figure & in words which are properly stated in Bank’s cheques. After confirming these cheques were sent to my boss. He was responsible for entry to the computer & completing other tasks.

3.2.4 Telegraphic Transfer (TT), Pay Order (PO) & Demand Draft (DD) Section

When any telegraphic transfer reached to the branch, I enter them in debit voucher, where I ensure that name, account Number, TT number and dates are correctly printed on the TT Voucher. Hence I make sure the signature of two officers and lastly send this voucher to the computer department. In PO & DD leaf, where I ensure name of the organization, drawer branch, date & amount of money and signature of two officers.

3.2.5 Investment Section:

I worked total 12 days in this section. Although Islami Bank Bangladesh Ltd. (IBBL) has been the most profitable banking organization in Bangladesh since the last few years but it has also got some limitations. These limitations exist in their operations, management and environment of the Bank. When I engaged in the IBBL Kawran Bazar Branch, then I able to talk some of clients, employees of this Branch and also talk about Banking Activities of this Branch. The investment procedures, modes of investment & its limitations that are found in the period of my internship are given below:

3.2.5.1 Investment Procedures of IBBL

There are three types of investment Mechanism. Every mechanism of investment is strictly followed investment procedures. These are as follows:

- Selection of the client

- Application stage

- Appraisal stage

- Sanctioning stage

- Documentation stage

- Disbursement stage

- Monitoring and Recovery stage

3.2.5.3 Modes of investment & its limitations

Bai-Murabaha:

This mode is binding upon the Client to purchase from the Bank. The Bank sells the goods at a higher price (Cost + Profit) to earn profit. The cost of goods sold and profit mark-up therewith are separately and clearly be mentioned in the Bai-Murabaha agreement. After purchasing of goods the Bank must bear the risk of goods until those are actually sold and delivered to the Client/buyer.

Bai-Muajjl:

This mode is binding upon the Client to purchase from the Bank but bank is not bound to declare the cost of goods and profit mark-up separately to the client. Stock and availability of goods is a pre-condition for Bai-Muajjal agreement. The responsibility of the bank is to purchase the desired goods at the disposal of the client to acquire ownership of the same before signing the Bai-Muajjal agreement with the client. Bank must bear the risk of goods until those are actually sold and delivered to the client/buyer.

Bai-Salam:

Bai-Salam is a mode of investment allowed by Islamic Shariah in which commodity(ies)/product(s) can be sold without having commodity (ies) /product(s) either in existence or physical /constructive possession of the seller. If the commodity (ies)/product(s) are ready for sale, Bai-Salam is not allowed by Islamic Shariah Shariah. Then the sale may be done either in Bai-Murabaha or Bai-Muajjall mode of investment.

Istishna’a:

It is a binding contract and no party is allowed to cancel the Istishna’a contract after the price is paid and received in full or in part or the manufacturer starts the work. It facilitates the manufacturer sometimes to get the price of the goods in advance, which he may use as capital for producing the goods.

Higher purchase under Shirkatul Melk:

In case of Hire Purchase under Shirkatul Melk, the asset / property involved is jointly purchased by the Hire (Bank) and the Hirer (Client) with specified equity participation under a Shirkatul Melk Contract in which the amount of equity and share in ownership of the asset of each partner (Hire Bank & Hirer Client) are clearly mentioned. Under this agreement, the Hire and the Hirer becomes co-owner of the asset under this transaction in proportion to their respective equity participation.

Mudaraba:

Most of investment of IBBL is formed under Mubaraba Mode. It is a form of partnership where one party provides the funds while the other provides the expertise and management. Any profits generated are shared between two parties on a pre-agreed basis, while capital loss is exclusively borne by the partner providing the capital. But IBBL is an expert organization in business sector so they face less failure and if there is any loss they can overcome it by other sector.

Musharakah:

The partners (entrepreneurs, bankers) share both capital and management of a project so that profits will be distributed among them as per ratio, where loss is shared according to ratio of their equity participation.

Investment division is the most important for all banks. In investment division maintain all types of investment procedures of Kawran Bazar Branc hand support the branch to take different types of initiatives. So I am prepared to report mode of investment as result majority time I work in the Investment department.

Different Modes of Investment of IBBL

4.1 Introduction

Investment is the action of deploying funds with the intention and expectation that they will earn a positive return for the owner. Funds may be invested in either real assets or financial assets. When resources are used for purchasing fixed and current assets in a production process or for a trading purpose, then it can be termed as real investment. Specific examples of financial investments are: deposits of money in a bank account, the purchase of Mudaraba Savings Bonds or stock in a company. Since Islam condemns hoarding savings and a 2.5 percent annual tax (Zakat) is imposed on savings, the owner of excess savings, if he is unable to invest in real assets, has no option but to invest his savings in financial assets.

4.2 Objectives and Principles of Investment

The objectives and principles of investment operations of the Bank are:

- To invest fund strictly in accordance with the principles of Islamic Shariah.

- To diversify its investment portfolio by the size of investment, by sectors (public & private), by economic purpose, by securities and by geographical area including industrial, commercial, and agriculture.

- To ensure mutual benefit both for the bank and the investment-client by professional appraisal of investment proposals, judicious sanction of investment, close and constant supervision and monitoring thereof.

- To make investment keeping the socio-economic requirement of the country in view.

- To increase the number of potential investors by making participatory and productive investment.

- To finance various development schemes for poverty alleviation, income and employment generation with a view to accelerating sustainable socio-economic growth and uplift of the society.

- To invest in the form of goods and commodities rather than give out cash money to the investment clients.

4.3 Investment Modes of IBBL

The investment modes of IBBL are set by head office of the bank and then followed by selected

branches. Thus, efforts have been made in this report to reveal the investment modes of IBBL in order to explore the investment modes of IBBL, Mirpur-10 Branch.

When money is deposited in the IBBL, the bank, in turn, makes investments in different forms approved by the Islamic Shariah with the intention to earn a profit. Not only a bank, but also an individual or organization can use Islamic modes of investment to earn profits for wealth maximization. Some popular modes of IBBL’s Investment are discussed below.

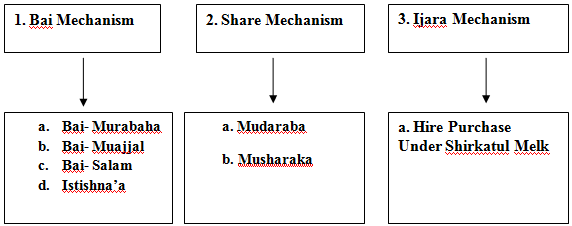

Islami Bank Bangladesh Ltd. operates its investment activities mainly through three (3) mechanisms:

4.3.1 Bai- Mechanism:

Under Bai- Mechanism Islami Bank Bangladesh Ltd. practiced different kinds of investment modes. These are given below:

4.3.1.1 Bai-Murabaha (Contract Sale on Profit)

Meaning and Definition:

“Bai-Murabaha” means sale on agreed upon profit. Bai-Murabaha may be defined as a contract between a Buyer and a Seller under which the Seller sells certain specific goods permissible under Islamic Shariah and the Law of the land to the buyer at a cost plus an agreed profit payable today or on some date in the future in lump-sum or by installments. The profit may be either a fixed sum or based on a percentage of the price of the goods.

Features of Bai- Murabaha:

- A client can make an offer to purchase particular goods from the bank for a specified agreed upon price, including the cost of the goods plus a profit.

- A client can make the promise to purchase from the bank, that is, he is either to satisfy the promise or to indemnify any losses incurred from the breaking the promise without excuse.

- It is permissible to take cash/collateral security to guarantee the implementation of the promise or to indemnify any losses that may result.

- Documentation of the debt resulting from Bai-Murabaha by a Guarantor, or a mortgage, or both like any other debt is permissible. Mortgage/Guarantee/Cash Security may be obtained prior to the signing of the Agreement or at the time of signing the Agreement.

- The bank must deliver the goods to the client at the date, time, and place specified in the contract.

- The purchase price of goods sold and profit mark-up shall separately and clearly be mentioned in the agreement.

- The price once fixed as per agreement and deferred cannot be further increased.

- It is permissible for the Bank to authorize any third party to buy and receive the goods on Bank’s behalf. The authorized must be in a separate contract.

Application of Bai-Murabaha:

Murabaha is the most frequently used form of finance in IBBL throughout the world. It is suitable for financing the different investment activities of customers with regard to the manufacturing of finished goods, procurement of raw materials, machinery, and other required plant and equipment purchases. It is used widely about 53%.

4.3.1.2 Bai-Muajjal (Deferred Sale)

Meaning and Definition:

“Bai-Muajjal” means sale for which payment is made at future fixed date or within a fixed period. In short, it is sale on Credit. The Bai-Muajjal may be defined as a contract between a buyer and a seller under which the seller sells certain specific goods, permissible under Shariah and law of the country, to the buyer at an agreed fixed price payable at a certain fixed future date in lump sum or in fixed installments.

Features of Bai-Muajjal:

- It is permissible and in most cases, the client will approach the bank with an offer to purchase a specific good through a Bai-Muajjal agreement.

- It is permissible to make the promise binding upon the client to purchase the goods from the bank.

- It is permissible to take cash/collateral security to guarantee the implementation of the promise or to indemnify the bank for damages caused by non-payment.

- It is also permissible to document the debt resulting from Bai-Muajjal by a Guarantor, or a mortgage or both, like any other debt. Mortgage/Guarantee/Cash security may be obtained prior to the signing of the Agreement or at the time of signing the Agreement.

- All goods purchased on behalf of a Bai-Muajjal agreement are the responsibility of the bank until they are delivered to the client.

- The bank must deliver the goods to the client at the time and place specified in the contract.

- The bank may sell the goods at a higher price than the purchase price to earn profit.

- The price is fixed at the time of the agreement and cannot be altered.

- The bank is not required to disclose the profit made on the transaction.

4.31.3 Bai- Salam (Advance Payment)

Meaning and Definition:

“Bai- Salam” means advance sale and purchase. Bai-Salam may be defined as a contract between a buyer and a seller under which the seller sells in advance the certain commodity/products permissible under Islamic Shariah and the law of the land to the buyer at an agreed price payable on the execution of the said contract and the commodity/products are delivered to the buyer as per specification, size, quality, quantity at a future time in a particular place.

Features of Bai- Salam:

· Bai-Salam is a mode of investment allowed by Islamic Shariah in which commodity(ies)/product(s) can be sod without having the said commodity(ies)/ product(s) either in existence or physical /constructive possession of the seller. If the commodity (ies)/product(s) are ready for sale, Bai- Salam is not allowed in Shariah. Then the sale may be done either in Bai-Murabaha or Bai-Muajjall mode of investment.

· Generally, industrial and agricultural products are purchased/sold in advance under Bai-Salam mode of investment to infuse finance so that product is not hankered due to shortage fund/cash.

· It is permissible to obtain collateral security from the seller client to secure the investment from any hazards via non-supply/partial supply of commodity (ies)/product(s), supply of low quality commodity (ies) /product(s).

· It is also permissible to obtain Mortgage and /or Personal Guarantee from a third party as security before the signing of the Agreement or at the time to signing the Agreement

· Bai-Salam on a particular commodity (ies)/product(s) or on a product of a particular field or firm cannot be affected (for Agricultural Product(s) only).

· The seller (manufacturer) client may be made agent of the Bank to sell the goods delivered to the Bank by her provided a separate agency agreement is executed between the bank and the client (agent).

Application of Bai- Salam:

Salam sales are frequently used to finance the agricultural industry. Banks advance cash to farmers today for delivery of the crop during the harvest season. Thus banks provide farmers with the capital necessary to finance the cost of producing a crop. Salam sale are also used to finance commercial and industrial activities. Once again the bank advances cash to businesses necessary to finance the cost of production, operations and expenses in exchange for future delivery of the end product. In the meantime, the bank is able to market the product to other customers at lucrative prices. In addition, the Salam sale is used by banks to finance craftsmen and small producers, by supplying them with the capital necessary to finance the inputs to production in exchange for the future delivery of products at some future date.

4.3.1.4 Istishna’a

Meaning and Definition:

Istishna’a is a contract between a manufacturer/seller and a buyer under which the manufacturer/seller sells specific product(s) after having manufactured, permissible under Islamic Shariah and Law of the Country after haying manufactured at an agreed price payable in advance or by go downs within a fixed period or on/within a fixed future date on the basis of the order placed by the buyer.

Features of Istishna’a:

· Istishna’a is an exceptional mode of investment allowed by Islamic Shariah in which product(s) can be sold without having the same in existence. In the product(s) are ready for sale. Istishna’a is not allowed is Shariaf. Then the sale may be done either in Bai-Murabaha or Bai-Maajjal mode of investment. in this mode, deliveries of goods are deferred and payment of price may also be deferred.

· It facilitates the manufacturer sometimes to get the price of the goods in advance, which he may use as capital for producing the goods.

· It gives the buyer opportunity to pay the price in some future dales or by go downs.

· It is a binding contract and no party or is allowed to cancel the Istishna’a contract after the piece is paid and received in full or in part or the manufacturer starts the work.

· Istishna’a is specially practiced in manufacturing and industrial sectors; however, it can be practiced in agricultural and constructions sectors also.

Application of Istishna’a:

The Istishna’a contract allows IBBL to finance the public needs and the vital interests of the society to develop the Islamic economy in accordance with Islamic teachings. For example Istishna’a contracts are used to finance high technology industries such as the aviation, locomotive and ship building industries. In addition, this type of business transaction is also

used in the production of large machinery and equipment manufactured in factories and workshops. Finally, the Istishna’a contract is also applied in the construction industry such as apartment buildings, hospitals, schools, and universities to whatever that makes the network for modern life. One final note, the Istishna’a contract is best used in those transactions in which the product being purchased can easily be measured in terms of the specified criteria of the contract.

4.3.2 Share Mechanism:

4.3.2.1 Mudaraba (Investment made by the entrepreneur)

Meaning and Definition:

The word Mudaraba has been derived from Arabic word “Darb/Darbun” which means “Travel”. Thus the word Mudaraba means travel for undertaking business.

It is a form of partnership where one party provides the funds while the other provides the expertise and management. The first party is called the “Sahib-Al-Maal” and the latter is referred to as the “Mudarib”. Any profits accrued are shared between the two parties on a pre-agreed basis, while capital loss is exclusively borne by the partner providing the capital.

Features of Mudaraba:

- Bank supplies capital as Sahib-Al-Mall and the client invest if in the business with his

- Administration and management is maintained by the client.

- Profit is divided as per management.

- Bank bears the actual loss alone.

- Client can not take another investment for that specific business without the permission

- of the bank.

4.3.2.2 Musharaka (Partnership based investment)

Meaning and Definition:

The word “Musharaka” has been derived from Arabic words “Sharikat” or “Shirkat”. In Arabic Sharikat and Shirkat means partnership or sharing. Thus the word “Musharaka” means a partnership between two or more persons or institutions.

Musharaka means a partnership established between two or more persons or institutions for purpose of a commercial venture participated both in the capital and management where the profit may be shared between the partners as per agreed upon ratio and the loss, if any is to be borne by the partners at per capital/equity ratio.

In this case of Investment, “Musharaka” meaning a partnership between the Bank and the Client for a particular business in which both the Bank and the Client provide capital at an agreed upon ratio and manage the business jointly. Share the profit as per agreed upon ratio and bear the loss, if any in proportion to their respective equity.

Bank may move itself with the selected Client for conducting any Shariah permissible business under Musharaka mode.

Features of Musharaka:

- Bank and client both supply capital unequally/equally.

- Profit is divided as per agreement and actual loss is divided as per equity.

- Client will maintain all accounts properly bank or its agent may verify or audit it.

- Banks can advice the client in such a business in respect of the businesss

- All partners can participate in the management of the business and can work for it.

- The liability of the partner is normally unlimited. Therefore, all the liabilities shall be borne proportionately by all the partners.

4.3.3 Ijarah Mechanism:

4.3.3.1 Hire Purchase Under Shirkatul Melk

Meaning and Definition:

Hire Purchase Under Shirkatul Melk is a Special type of contract that has been developed through practice. Actually, it is a synthesis of three contacts:

i) Shirkat

ii) Ijarah and

iii) Sale

These may be define as follows:

i) Shirkatul Melk: ‘Shrkat’ means partnership. Shirkatul Melk means share in ownership. When two or more persons supply equity, purchase an asset and own the same jointly and share the benefit as per agreement and loss in proportion to their respective equity, the contact is called Shirkatul Melk. In the case of Hire Purchase under Shirkatul Melk, IBBL purchase assets to be leased out, jointly with client under equity participation, own the same and share benefit jointly till the full ownership is transferred to the client.

ii) Ijara: The term Ijara has been derived from the Arabic words “Air” and “Ujrat” which means consideration, return, wages or rent. This is really the exchange value or consideration, return, wages, rent of service f an asset. Ijara has been defined as a contract between two parties, the Hiree and Hirer where the Hirer enjoys or reaps a specific service or benefit against a specified consideration or rent from the asset owned by the Hiree. It is a hire agreement under which the Hiree to a Hirer against fixed rent or rentals hires out a certain asset for a specified period.

iii) Sale: This is a sale contract between a buyer and a seller under which the ownership of certain goods or asset is transferred by seller to the buyer against agreed upon price paid / to be paid by the buyer.

Thus, in Hire purchase under Shirkatul Melk mode both the Bank and the Client supply equity in equal or unequal proportion for purchase of an asset like land, building, and machinery, transport etc. Purchase the asset with that quit money, own the same jointly, share the benefit as per agreement and bear the loss in proportion their respective equity. The share, part of portion of the asset owned by the bank is hired out to the client partner for a fixed rent per unit of time for a fixed period. Lastly the bank sells and transfers the ownership of its share/part/portion to the client against payment of price fixed for the either gradually part by part or in lump sum within the hire period or after expire of the hire agreement.

Stages of Hire Purchase Under Shirkatul Melk:

Hire Purchase under Shirkatul Melk Agreement has got three stages:

1) Purchase of asset under joint ownership of the lessor and the lessee.

2) Hire, and

3) Sale and transfer of ownership by the lessor to the other partner – lessee.

Features of Hire Purchase Under Shirkatul Melk:

· In case of Hire Purchase Under Shirkatul Melk transaction the asset/property involved is jointly purchased by the lessor (bank) and the lessee (client) with specified equity participation Under a Shirkatul Melk contract in which the amount of equity and share in ownership of the asset of each partner (lessor bank and lessee client) are clearly mentioned. Under this agreement the lessor and the lessee become co-owners of the asset under transaction in proportion to their respective equity.

· In Hire Purchase Under Shirkatul Melk Agreement the exact ownership of both the lessor (bank) and lessee (client) must be recognized. However, if the partners wish and agree the asset purchased may be registered in the name of any one of them or in the name of any third party clearly mentioning the same in the Hire Purchase Shirkatul Melk Agreement.

· The share/part of the purchased asset owned by the lessor (bank) is put at the disposal possession of the lessee (clients) keeping the ownership with him for a fixed period under a hire agreement in which the amount of rent per unit of time and the benefit for which rent to be paid along with all other agreed upon stipulations are clearly stated. Under this agreement the lessee (client) becomes the owner of the benefit of the asset not of the asset itself, in accordance with the specific provisions of the contract that entitles the lessor (bank) the rentals.

· As the ownership of leased portion of asset lies with the lessor (bank) and rent is paid by the lessee against the specific benefit, the rent is not considered as price or part of price of the asset.

· In the Hire Purchase Under Shirkatul Melk Agreement the Hire (Bank) does not sell or the Hirer (Client) does not purchase the asset but the Hire (Bank) promise to sell asset to the Hirer (Client) part by part only, if the Hirer (Client) pays the cost price / equity / agreed price as fixed for the asset as per stipulations within agreed upon period on which the Hirer also gives undertakings.

· The promise to transfer legal by the Hire undertakings given by the Hirer to purchase ownership of the hired asset upon payment part by part as per stipulations are effected only when it is actually done by a separate sale contract.

· As soon as any part of Hire’s (Bank’s) ownership of the asset is transferred to the Hirer (Client) that becomes the property of the Hirer and hire contract for that share / part and entitlement for rent thereof lapses.

· In Hire Purchase under Shirkatul Melk Agreement, the Shirkatul Melk contract is affected

from the day the equity of both parties deposited and the asset is purchased and continues

up to the day on which the full title of Hire (Bank) is transferred to the Hirer (Client).

· The hire contract becomes effective from the day on which the Hire transfers the possession of the hired asset in good order and usable condition to the Hirer, so that the Hirer may make the agreement.

· Effectiveness of the sale contract depends on the actual sale and transfer of ownership of the asset by the Hire to the Hirer.

4.4 Investment Processing of IBBL:

Generally a bank takes certain steps to deliver its proposed investment to the client. But the process takes deep analysis. Because banks invest depositors fund, not banks’ own fund. If the bank fails to meet depositors demand, then it must collapse. So, each bank should take strong concentration on investment proposal. However, Islami Bank Bangladesh Limited (IBBL) makes its investment decision through successfully passing the following crucial steps:

(1) Selection of the client

Here, investment taker (client) approaches to any of the branch of Islami Bank Bangladesh Limited (IBBL). Then, he talks with the manager or respective officer (Investment). Secondly, bank considers five C’s of the client. After successful completion of the discussion between the client and the bank, bank selects the client for its proposed investment. It is to be noted that the client/customer must agree with the bank’s rules & regulations before availing investment. Generally, bank analyses the following five C’s of the client:

- Character;

- Capacity;

- Capital;

- Collateral; and

- Condition.

(2) Application stage

At this stage, the bank will collect necessary information about the prospective client. For this reason, bank informs the prospective client to provide and/or fill duly respective information which is crucial for the initiation of investment proposal. Generally, here, all the required documents for taking investment have to prepare by the client himself. Documents that are necessary for getting investment of IBBL is prescribed below:

- Trade License photocopy (for proprietorship);

- Abridged pro forma income statement;

- Attested copy of partnership deed (for partnership business);

- Prior three (03) years’ audited balance sheet (for joint stock company);

- Prior three (03) years’ business transactions statement for the musharaka/mudaraba investment;

- Abridged pro forma income statement for the musharaka/mudaraba investment;

- Attested copy of the Memorandum of Association (MOA) & Articles of Association (AOA) for the joint stock company;

- Attested copy of the Tax Identification Number (TIN)- including final assessment;

- Tenders of the proposed assets (in case of HPSM);

- Detailed summary of the sundry debtors and creditors (including both time & schedule);

- Summary of the personal movable & immovable assets; and others.

(3) Appraisal stage

At this stage, the bank evaluates the client and his/her business. It is the most important stage. Because, on the basis of this stage, bank usually goes for sanctioning the proposed investment limit/proposal. If anything goes wrong here, the bank suddenly stops to make payment of investment.

In order to appraise the client, Islami Bank Bangladesh Limited (IBBL) provides a standard

F-167B Form (Appraisal Report) to the client for gathering all the information. The original copy of the appraisal report is enclosed in the appendix chapter. However, the following contents are presented from that appraisal report:

- Company’s/Client’s Information.

- Owner’s Information.

- List of Partners/Directors.

- Purpose of Investment/Facilities.

- Details of Proposed Facilities/Investment.

- Break up of Present Outstanding.

- Other Liabilities of the Client/Group.

- Previous Banker’s Information.

- Details of Sister/Allied Concerns.

- Allied Deposit as on.

- Business/Industry Analysis.

- Relationship Analysis.

- Asset-Liability position of the client as per Audited Balance Sheet.

- Working Capital Assessment.

- Risk Grade.

- Particulars of the godown for storing MPI/Murabaha goods.

- Insurance Coverage.

- Audit Observation.

- Security Analysis.

(4) Sanctioning stage

At this stage, the bank officially approves the investment proposal of the respective client. In this case client receives bank’s sanction letter. Islami Bank Bangladesh Limited (IBBL)’s sanction letter contains the following elements:

- Investment Limit in million.

- Mode & amount of investment.

- Purpose of investment.

- Period of investment.

- Rate of return.

- Securities

- Cash/Goods security

In allowing Murabaha investment and amount of cash security is generally realized from the client (amount depends on the nature of goods, creditworthiness of the client, collateral security obtained etc.) which is converted to goods security after purchase of goods purchased out of bank’s investment and client’s cash security is pledged to the bank, kept under bank’s custody before its delivery to the client on payment. Example: If, for a Murabaha investment cash security is fixed at 25% Bank’s investment stands at 75% on the total goods purchased. For example, if cost of total goods purchased is Tk.100000 Bank’s investment will be Tk.75000 and client’s cash security will be Tk.25000.

Bank | Client | Total cost of goods |

Tk. 75000 (75%) | Tk. 25000 (25%) | Tk. 100000 (100%) |

(5) Documentation stage

At this stage, usually the bank analyses whether required documents are in order. In the documentation stage, Islami Bank Bangladesh Limited (IBBL) checks the following documents of the client:

I. Tax Payment Certificate.

II. Stock Report.

III. Trade License (renewal).

IV. VAT certificate

V. Liability statement from different parties.

VI. Receivable from different clients.

VII. Other assets statement.

VIII. Aungykar Nama.

IX. Ghosona Potra.

X. Three (03) years net income & business transactions.

XI. Performance report with the bank.

XII. Account Statement Form of the bank.

XIII. Valuation Certificate

- Particulars of the Proposal.

- Particulars of the Mortgagor.

- Particulars of the Properties.

XIV. Outstanding liability position of the bank.

XV. CIB (Credit Information Bureau) Report.

(6) Disbursement stage

At this stage, bank decides to pay out money. Here, the client gets his/her desired fund or goods. It is to be noted that before disbursement a “site plan” showing the exact location of each mortgage property needs to be physically verified.

(7) Monitoring & Recovery stage

At this final stage of investment processing of the Islami Bank Bangladesh Limited (IBBL), bank will contact with the client continually, for example- bank can obtain monthly stock report from the client in case of micro investment. Here, the bank will keep his eye on over the investment taker. If needed, bank will physically verify the client’s operations. Also if bank feels that anything is going wrong then it tries to recover its investment fund from the client.

4.5 Investment Schemes of IBBL:

The salient features of the investment policy of Islami Bank Bangladesh Limited are to invest on the basis of profit and loss sharing system in accordance with the tenets and principles of Islamic Shariah. Profit earning is not the only motive and objective of the bank’s investment policy rather emphasis is given in attaining social good and in creation employment opportunities.

In fact, the bank since its inception has been working for the uplifted and emancipation of the unprivileged, downtrodden, and neglected section of the people and has taken up various schemes for their well being. The objectives of these schemes are to raise the standard of living of low-income group, development of human resources, and creation of awareness for self employment.

4.5.1 Household Durable Scheme (HDS)

In a developing country like Bangladesh people of middle and lower class especially service holders with limited income find it difficult to purchase articles like refrigerator, television, cot, almirah, wardrobe, sofa-set, pressure cooker, sewing machine etc. which are part of modern and decent living. They cannot enhance the standard and quality of life to the desired level due to the constrain of their limited income. Islami Bank Bangladesh Limited has, therefore, introduced Household Durables Investment Scheme that has already created great enthusiasm among the people and received tremendous response from them.

Objectives

- To assist the service holders with limited income in purchasing household durables.

- To assist the fixed income group in raising the standard of living.

- To create opportunity for the service holders to enjoy the benefit of modern and sophisticated living and at the time lead a decent and honest life.

Items of HDS

a. Refrigerator/Deep freeze.

b. Television.

c. Radio/Two-in-one/Three-in-one.

d. Motor cycle/Bi-cycle.

e. Air cooler/ Air conditioner.

f. Personal computer.

g. Washing machine.

h. Furniture, viz. cot, almirah, sofa-set, wardrobe, carpet etc.

i. Sewing machine.

j. Kitchen appliances like oven, toaster, blender, pressure cooker etc.

k. Electronic generator: IPS, UPS etc.

l. Power generator, motor pump/power pump etc.

m. CI sheet, Rod, Wood etc.

n. Gold ornaments

o. Tube-wels

p. Mobile telephone set

q. Medical/Engineering Equipment/Machinery

r. Educational equipment/Machinery, books etc.

Amount

- For doctors, Engineers, Architects, Chartered Accountants, FCMAs the Ceiling of the investment of the Bank will be –

a. Dhaka City: Maximum Tk.3,00,000.00

b. Other Metropolitan Cities: Maximum Tk.2,00,000.00

c. Other Municipal Areas: Maximum Tk.1,00,000.00 - For Depositors Tk. 2,00,000.00

- For others: Tk.1,00,000.00

- NCOs of Bangladesh Armed Forces, Teachers of Primary Schools, Private School & Colleges and other professionals: Maximum Tk. 35,000.00

- For Students : Maximum Tk. 40,000.00

Rate of Return:15%.

Period of Investment:Maximum two years.

Mode of Investment:Bai-Muajjal.

Equity

Minimum 25% of the total value of the articles. The client shall have to deposit the amount of equity in his Mudaraba Savings/Investment Account with the concerned branch before the disbursement of investment.

Disbursement

- After sanction of investment and deposit of required equity by the client, the Branch shall supply to the concerned investment client the desired articles within seven days by procuring them by way of pay-order/cheque/draft etc. favouring the supplier.

- For ensuring the ownership of the Bank over the goods, all papers and documents related to the procurement of the goods shall remain in the name of the Bank and Bank’s sticker shall remain affixed over the same. The ownership shall be transferred in favor of the client after full adjustment of the dues to the Bank.

Security

The investment client shall execute/provide the following documents in order to secure the investment.

- All required charge documents as per rules of the Bank.

- A written undertaking to the effect that the monthly installments shall be paid regularly.

- Personal guarantee of another person, preferably family member

Procedure for Application

Interested clients shall apply in prescribed form to the concerned Branch. The application shall have to be duly recommended by the Divisional Chief of the organisation where the applicant serves. Form and booklet outlining the rules and procedures of the Scheme may be obtained from the selected Branches of the Bank on payment of Tk. 25.00 only.

4.5.2 Housing Investment Scheme (HIS)

One of the basic human needs is to have a house to live in. A house is an abode of peace and happiness. Housing has now become an acute problem in the country, specially in the towns, cities and metropolis. With their limited income, it has become almost impossible on the part of the lower middle class, middle class and sometimes, even for upper middle class to solve their housing problem. To meet this basic human need, Islami Bank Bangladesh Limited is committed to contribute to this end to provide a peaceful and happy living. The Bank has introduced ‘Housing Investment Scheme’ with the objective to ease and minimize the housing problem and assist service holders and professionals with limited income in materializing their dream of becoming owner of houses.

Objectives

- To extend the benefits of the investment of the Bank under the Scheme to different sections of the people.

- To assist in solving the existing housing problem of the country.

- To assist the service holders and professionals with fixed income to arrange for houses of their own.

- To extend the investment facilities of the Bank to every nook and corner of the country, by size of investment, by sector of investment and on the basis of geographical area.

- To make investment facilities easily available under Islamic Shariah to those people who do not want to avail investment facilities from interest-based financial institutions.

Eligibility

Initially the following categories of people shall be eligible to apply for availing investment facilities under this Scheme:

1. Officials of the Defense Forces.

2. Permanent Officials of Government, Semi-Government and Autonomous

Organizations.

3. Teachers of the established Universities, University Colleges & Medical Colleges.

4. Graduate Engineers, Doctors and established professionals.

5. Bangladeshi Officials of reputed Multinational Companies, International Financial

Organizations, Donor Agencies, Foreign Embassies etc., and Official of

local established & reputed Public Limited Companies.

Rate of Return:13%

Mode of Investment: Hire Purchase Under Shirkatul Melk (HPSM)

Period of Investment

- The maximum period of investment shall be generally 15 years. However, the period of investment shall be determined on the basis of the proposal of the client, the amount of investment (for which the client has applied) and the ability of the project or client to repay the dues.

- Reasonable gestation period for construction be allowed considering the size of construction and Bank’s investment.

Bank’s Rent

The Bank, in accordance with its normal practice shall decide rent on the investment. The clients, who will repay the entire dues in time or before the stipulated time by way of payment of all due installments regularly, they will be allowed rebate on the rent.

Security

- Personal guarantee of the clients, his/her spouse, adult son(s) and daughter(s) shall have to be obtained.

- Mortgage of land and building to be constructed thereon, apartment/flat/house in favor of the Bank till the full payment of dues to the Bank.

- An undertaking from the client as well as from the dependants (nominees) to the effect that the retirement benefits including Provident Fund will be appropriated towards adjustment of the house building investment liability of the client prior to any other appropriation, if the liability relating thereto or any part of it remains unadjusted at the time of getting the retirement benefits.

Procedure for Application

Interested persons shall have to apply in prescribed form of the Bank through the Branch of the concerned area. The Bank shall sanction investment if the proposal is found acceptable after examination of its viability and profitability. The Bank reserves the right to sanction or reject any investment proposal.

4.5.3 Real Estate Investment Program (REIP)

Professionals, Service-holders, Businessmen, Real Estate Developer and other categories of people who are not entitled for availing investment facilities under Housing Investment Scheme, shall be eligible under this programme. Investment is to be extended to build new houses and for extension/ completion of the house already constructed, commercial building, shopping complex, flat/apartment etc.

Rate of Return:13%

Mode of Investment:HPSM

Investment Limit:No specific limit

Duration:10 years

4.5.4 Transport Investment Scheme (TIS)

The role of modern communication is most vital for the socio-economic growth and uplift of a developing country like Bangladesh. A sound and efficient communication network is the pre-requisite for sustained development through the expansion of trade, commerce and industry. In this backdrop the demand for road and water transports has increased manifold throughout the country. Moreover, the use of modern transports has increased keeping pace with the rise of the standard of living of the professionals. Considering all these facts, Islami Bank Bangladesh Limited has introduced ‘Transport Investment Scheme’. Under this scheme investment on easy terms is being extended to the existing successful businessmen in road and water transports and potential entrepreneurs in this sector for different types of road and water transports. Besides, Multinational companies, established business houses and well to do officials and professionals can become owner of various kinds of transports through Hire Purchase under this scheme.

Mode of Transports

- Road Transports

- Private car, microbus, jeep, pick-up van.

- Bus, truck, minibus.

- Auto-rickshaw, tempo.

- Ambulance.

- Water Transports

- Cargo vessel of maximum 500 ton capacity.

- Ocean going vessel of maximum 800 ton capacity.

Target Group

- Bus/Truck/Minibus

- Successful individual/businessman/firm engaged in transport business and potential individual/ businessman/firm who intends to take-up transport as business.

- Private Car/Microbus/Jeep

- Permanent Officials of Government, Semi-government, Autonomous Bodies, Corporations, Banks and Financial Institutions.

- Established Businessman and Business Establishments.

- Officials of Defence Forces.

- Professionals: University Teachers, Doctors and Engineers.

- Experienced Person/Firm engaged or interested in transport business (Rent-a-car).

- Preference will be given to those person and firms who are already engaged in transport business.

- Auto Rickshaw/Tempo/Pick-up van

- Persons/Businessmen/Firms who have already proved themselves successful in the transport business and those efficient and potential persons/businessmen/firms who are interested to take small transport as business, may apply for investment to purchase auto-rickshaw, tempo and pick-up van.

- Ambulance

- Established Clinics and Hospitals.

- Water Transport

- Experienced and successful Persons and Businessmen engaged in water transport business.

Rate of Return:15%

Mode of Investment:Hire-Purchase Shirkatul Meelk(HPSM).

Period of Investment:

- Maximum 3 years from the date of delivery of the vehicle.

Rent of Investment

The Bank as per existing rules shall charge rent on investment. Clients, who will repay the entire investments within the stipulated period or earlier by way of regular payment of instalments, shall be given rebate over the rent.

Security

- The ownership of the vehicle shall remain in Bank’s name till full repayment of investment including rent.

- The client shall have to mortgage immovable properties as collateral security.

- In case of Officials of Government, Semi-Government and Autonomous Bodies, personal guarantee of the officer of the same grade or of superior grade and in case of officials of public limited company or business houses, corporate guarantee of the employer/ chairman/managing director shall have to be provided.

Supervision

Bank officials or appointed agents of the Bank reserve the right to inspect the vehicle at any time in any place where it is kept or found in order to ascertain its overall condition.

4.5.5 Car Investment Scheme (CIS)

Car is considered as an essential mode of transport in the modern society, particularly by a section of the officials, business houses and business executives and established professionals for movement in discharging their duties and responsibilities punctually and efficiently. Many of these categories of people cannot purchase a car on payment of entire purchase value at a time out of their own sources. To meet this need Islami Bank has introduced the ‘Car Investment Scheme’ for the mid and high ranking officials of government and semi-government organizations, corporations, executives and directors of big business houses and companies and also for persons of different professional groups on easy payment terms and conditions.

Objectives

- To meet the demand of senior officials of different organizations, established business houses and companies and persons of various professional groups who essentially need a car but cannot afford to purchase on payment at a time.

- To assist in minimizing transport problem in the private sector and help the mid and high ranking officials and professionals with fixed income in the improvement of their standard of living.

- To extend the range of Bank’s investment facilities to various sections of people in line with the ideals of the Bank.

- To diversify the investment portfolio of the Bank by size, sector and volume.

Eligibility

Permanent senior officers/executives of the following organizations:

Category-A

- Government Organizations.

- Semi-Government Organizations/Autonomous Bodies/Corporations.

- Banks.

- Commissioned Officer of Armed Forces, BDR, Police and Ansars.

- Teachers of the Universities, Government Colleges.

Category-B

- Executives/Directors of big companies and business houses of repute.

- Members of all other professional groups having good income.

The clients, in both the categories, must be within age group of 27-50 years with minimum 6 (six) years unexpired service in case of service holders. In all cases the clients must have sufficient capacity to pay the installments in due time to the satisfaction of the Bank. The Bank reserves the right to regret the sanction of any proposal not found suitable.

Bank’s Investment

Bank’s investment is maximum Tk. 3.50 lac per client against purchase cost of the vehicle. Registration and comprehensive insurance cover shall be in the name of the Bank. The clients shall have to bear all subsequent expenses relating to blue book, registration, first party insurance, tax token, fitness certificate etc.

Client’s Equity

Minimum 30% of the purchase cost of the vehicle. The amount of equity shall have to be deposited with the Bank before disbursement of Bank’s investment.

Rate of Return:15%

Period of Investment

Period of investment is maximum 4 (four) years from the date of disbursement or delivery of the vehicle to the client, whichever is earlier.

Mode of Investment

a. Hire Purchase

b. Hire Purchase Shirkatul Meelk.

Security Requirements

The following shall be obtained as security against bank’s investment under this Scheme:

(a). In case of clients falling under category-A of eligibility criteria:

- Personal guarantee of the investment client.

- Personal guarantee of any of the officers of the rank and status equal to the client or an officer of higher rank.

- The guarantee shall have to be duly authenticated by the competent authority of the organization/institution where the client serves.

- Employer’s certificate to the effect that the client is in permanent service of the organization. The net pay and pay scale of the client is to be mentioned in the certificate.

- An undertaking from the client to the effect that in case of his failure to pay regular installments, the amount is to be deducted from his salary at source for adjustment of dues to the Bank.

(b). In case of clients falling under category B of eligibility criteria, any of the following additional collateral/securities are required:

- Mortgage of land

- Bank Guarantee

Supervision

Bank may engage supervising agents to supervise, monitor and recover the investments under the Scheme. The cost of the supervision charge shall be recovered from the client along with rent. Insurance

The vehicle shall be covered by first party (comprehensive) insurance covering all possible risks throughout the investment period at the cost of the client. The client shall have to ensure timely renewal of insurance and payment of premium.

Registration

The car shall have to be registered in the name of the Bank only. After payment of the entire investment of the Bank including the charges etc., the car shall be transferred in the name of the clientby the client.

Inspection

For the purpose of inspecting the status, operation and custody of the vehicle, the Bank or its authorized agent has the right, at all reasonable time, to enter into the house, office, factory, garage or the premise of the client where the vehicle is kept.

4.5.6 Investment Scheme for Doctors (ISD)

Islami Bank Bangladesh Limited has taken the initiative an introduced the “Doctors Investment Scheme” to ensure modern treatment and medical facilities available to the people through extension of Bank’s investment facilities for self-employment of newly graduated doctors and at the same time extending investment facilities to the established medical practitioners to procure modern and sophisticated medical equipment.

Objectives

- To provide investment facilities for establishment of chambers, clinics, pharmacies and procurement of medical equipment by the unemployed medical graduates and thus to provide self- employment.

- To assist newly passed unemployed medical graduates to establish clinics by way of formation of groups by 5 doctors.

- To assist specialists and consultant physicians to procure specialised medical equipment for extending improved treatment to the people.

Rate of Return:14%

Investment Ceiling and Period:

Category Maximum Ceiling Maximum Period

1. Self employed doctors settled Tk. 5.00 lacs 5 years

in district town

2. Self employed doctors settled Tk. 5.00 lacs 5 years

in Thana towns

3. Specialists/Consultant physicians Tk. 10.00 lacs 5 years

for modern and sophisticated

medical equipment

4. Newly graduate unemployed Doctors Tk. 5 lacs to every doctor and 5 years

Group for establishment of clinics, maximum Tk. 25 lacs to a group

Purchase of machinery, equipment, of 5 doctors

accessories and other goods.

Mode of Investment

a. Hire Purchase Shirkatul Melk : For purchase/procurement of medical equipment and appliances, motor cycle and other items.

b. Bai-Muajjal : For establishment of Chambers, Clinics and purchase of medicines etc.

Security

1. The ownership of the medical equipment, appliances etc. and the motor cycle supplied by the bank on Hire Purchase-Shirkatul Melk basis, shall remain with the bank.

2. Against Bank’s investment, the clients shall have to mortgage property at least equal to the value of investment by the Bank. However, in case of investment (other than clinic) for self-employment of the newly graduated doctors the condition of mortgage of property may be relaxed, if they are unable to offer mortgage of property as security against investment. The investment clients shall have to provide personal guarantee of person(s) acceptable to the bank, in such cases.

4.5.7 Small Business Investment Scheme (SBIS)

Islami Bank, as welfare oriented financial institution, is committed to generate employment and bring about an overall improvement in the socio-economic condition of the people and the quality of their life. The Bank, to make effective contribution in this respect, has taken-up a special programme and introduced ‘Small Business Investment Scheme’ to make the small traders, entrepreneurs and neglected unemployed youths of urban and rural areas self-reliant by providing them required financial support.

The following benefits will be achieved through implementation of this scheme:

- Gradually it will help to alleviate poverty and minimize unemployment.

- It will help small traders and entrepreneurs to become self-reliant and to improve their quality of life through capital formation.

- It will create opportunity for the unemployed youths to engage themselves in in-come generating activities.

- It will help to expand the market for locally produced goods by increasing productivity of small traders and entrepreneurs.

Eligibility of the Clients

- Investment clients must be permanent residents of the command area of the branch through which they intend to avail investment facilities and they must have valid trade license and shops or selling centers.

- Small business and entrepreneurs, who are already engaged in trade and business but cannot run their operations smoothly for shortage of fund/capital, will also be eligible to avail investment facilities under the Scheme.

- Investment shall also be extended to those poor and asset-less unemployed youths who are honest, efficient, physically and mentally capable with drive and initiative, especially those who have ability to run business.

- Besides the above categories, investment facilities under this Scheme shall also be extended to small and cottage industries and service sector.

Sectors of Investment

a) Livestock

b) Fishery

c) Agro-processing

d) Manufacturing

e) Trading/shop keeping

f) Transport

g) Services

h) Agriculture Implements and Forestry

i) Others.

Rate of Return:14%

Ceiling of Amount

- For Dhaka & Chittagong : Maximum up to Tk. 1,00,000/- per client Metropolitan

Branches depending upon their requirements.

- Branches in other Divisional : Maximum up to Tk. 75,000/- per client District

Head Quarters depending upon their requirements.

- Branches other than Divisional: Maximum up to Tk. 50,000/- per client & District

Head Quarters depending upon their requirements.

Mode of Investment

A. Hire Purchase Shirkatul Meelk : For all kinds of machineries i.e. equipments &

transport sector.

B. Bai-muajjal-TR : For trading shop keeping, agro-processing and

raw materials for manufacturing purposes.

Period of Investment

- In case of HPSM : Maximum 24 months.

- In case of Bai-muajjal-TR : Maximum 12 months.

Client’s Equity

- For HPSM investment : Maximum 20% on cost price of the Machineries/vehicles.

- For Bai-muajjal-TR : Nil.

Security

For Investment up to Tk. 30,000.00

- Hypothecation of existing and future stock of goods. Ownership of machines & equipments shall remain in Bank’s name.

- Personal guarantee of financially sound respectable 2 (two) persons/prominent businessmen acceptable to the Bank shall have to be given.

- Collateral security may be relaxed considering the feasibility of investment and client’s ability and sincerity.

For Investment over Tk. 30,000.00

- Hypothecation of existing/future stock of goods. Ownership of machines & equipments shall remain in the Bank’s name.

- The client shall have to give mortgage of immovable properties to the Bank.

Mudaraba Savings Account

It is compulsory that every client must open a Mudaraba Savings account. Each client should built savings by way of deposit in this account a sum of Tk. 10.00 each month for every Tk. 1,000.00 of investment. No chequebook shall be issued against this account. Money can be withdrawn from this account if there is no liability against the client.

Supervision

For effective supervision and smooth operation of the scheme, required number of supervisors shall be engaged at the field level. For this purpose the investment client shall have to pay at the time of investment a sum at the rate of 2% per annum of investment as supervision fee. In case of investment for 2 years, supervision charge shall be 4% i.e. 2% per year.

4.5.8 Agriculture Implements Investment Scheme (AIIS)

In order to bring revolutionary changes in the agricultural sector by adopting modern agricultural technology replacing the age-old traditional way of cultivation and increasing the use of fertilizer. This can only be done by collective efforts of both public and private sectors. Islami Bank Bangladesh Limited is a welfare oriented Bank. It can play positive and important role in the economic development, progress and uplift of the country by investing in the agricultural sector. The Bank has, therefore, introduced “Agriculture Implements Investment Scheme” to provide power tillers, power pumps, shallow tubewells, thrasher machine etc. on easy terms to the unemployed youths for self-employment and to the farmers to help augment production in agricultural sector.

Types of Agriculture Implements

- Power tillers

- Thrasher Machine

- Any other agricultural implements proposed by the branch and which has local demand.

These implements may be of any popular brand. Any locally manufactured brand, which has large demand, is also acceptable. The choice of investment clients shall be given preference in this regard.

Eligibility of Investment Clients

- Educated or half-educated rural youths, educated or illiterate farmers and any person ready to accept agriculture as business may apply for investment facilities under this scheme. Preference shall be given to those applicants who have passed S.S.C. or above.

- The applicant farmer should posses sound health and his age must be minimum 18 years and maximum 50 years. Person who is willing to take agriculture as business, his age must be between 18 to 45 years. If the applicant is educated or half educated youth than his age must be between 18 to 35 years.

- The applicant must be physically and mentally fit and willing to operate the machine himself.

- Applicant must be a permanent resident of the concerned area and be willing to stay and work there.

Rate of Return: 13%

Period of Investment:Two Years

Mode of Investment:Hire Purchase Shirkatul Melk.

Security

- The agricultural implements to be supplied to the investment client shall remain in the name of the bank till the repayment/adjustment of the dues to the bank.

- Collateral security of immovable property equal to the amount of Bank’s investment backed by irrecoverable general power of attorney.

- Client, who is unable to offer collateral security of immovable property, shall have to provide personal guarantee of two respectable persons acceptable to the Bank. Guarantors should preferably be client’s father/guardian or teacher.

Supervision

1. The overall supervision of the investment shall be the responsibility of the concerned branch.

2. For supervision at the field level the Bank, may engage educated unemployed youths of the concerned area as per rules of the Bank. Supervision fee at the rate 2% over investment may be charged from the investment client for this purpose.

5.1 Investment Performance of IBBL

5.1.2 Sources of Funds

The financial resources of the IBBL consist of ordinary capital resources comprising paid-up capital and reserves, and funds rose through borrowings from the central bank and other banks (inter-bank borrowing), and issue of Islamic financial instruments. The major part of their operational funds is, however, derived from the different categories of deposits accepted on the Islamic principles of Al-Wadiah (safe custodianship) and Mudaraba (trust financing). For the sake of ease of understanding we call these two sources as ‘Primary’ and ‘Secondary’. These are discussed as under.

Primary Sources

(1) Paid-Up Capital