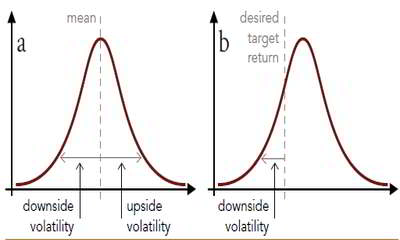

Sortino Ratio is usually a modification of the particular Sharpe ratio that will differentiates harmful volatility from general volatility by taking into account the standard change of negative tool returns, called disadvantage deviation. The Sortino ratio subtracts the risk-free fee of return on the portfolio’s return, and then divides that from the downside deviation. A large Sortino ratio indicates to find there’s low probability of a large loss. The Sortino ratio was created in 1983 by Brian M. Rom.

Sortino Ratio