Executive Summary

In the age of modern civilization bank is playing its spending role to keep the economic development wheel moving. The corporation of the bank is needed in every economic activity. In fact there is hardly any aspect of development activity where state inspired or otherwise where bank do not have role to play.

Shahjalal Islami Bank Limited (SJIBL) commenced its commercial operation in accordance with principle of Islamic Shariah on the 10th May 2001 under the Bank Companies Act, 1991. SJIBL has diversified its service coverage by opening new branches at different strategically important locations across the country offering various service products both investment & deposit. SJIBL desires to be the unique modern Islami Bank in Bangladesh and to make significant contribution to the national economy and enhance customers’ trust & wealth, quality investment, employees’ value and rapid growth in shareholders’ equity. Islamic Banking, in essence, is not only interest free banking business, it carries deal wise business product thereby generating real income and thus boosting GDP of the economy. Banking sector plays vital role for economic development of Bangladesh. Foreign exchange department of commercial banks facilitates the import and export of a country and thus develops the international trade. SJIBL has been flourishing as the largest private sector bank with the passage of time after facing many stress and strain. Foreign exchange department of this bank is well renowned.

ShahJalal Islami Bank Limited, a growing private sector commercial bank started its operations from May 2001 and have been progressing throughout the years of operations in Bangladesh. Since its establishment ShahJalal Islami Bank Limited has opened 64 branches in different cities such as Dhaka, Chittagong, Sylhet, Khulna and in many other commercial areas in Bangladesh. In the near future, more branches are to be inaugurated to provide better quality of banking service to the customers.

Today’s world economy is totally dependent on the exports or import and the volume of the international transaction has grown enormously. Similarly, annual capital flows occur among the nations worldwide. So the international trade and investment of this magnitude would be possible because of availability of foreign currencies. Foreign exchange market makes it easy to accumulate foreign currencies at requires. The trading of foreign currencies take place in foreign exchange market whose primary function is to facilitate international trade and investment

The broad objective of the study was to conduct the performance analysis of the foreign exchange department of ShahJalal Islami Bank Limited over the years of its operation in the Commercial Banking sector in Bangladesh. The specific objectives identified are to relate theoretical knowledge with practical experience in several functions of the bank, find out the position of SJIBL through the comparative analysis and the trend analysis, and present the current situation of Export, import, foreign remittance in SJIBL, analyze the financial performance of the foreign exchange department of ShahJalal Islami Bank Limited over the years of banking operations, and to find out the factors that may create the foreign exchange risk and also find out ways to minimize the foreign exchange risks.

The report was made on the basis of primary and secondary data. Primary data have been collected through discussions with the officers of the foreign exchange department of the bank. Secondary data have been collected from the bank’s record books, publications, annual reports, websites and other sources. For analyzing the data and explaining the performance both tables and graphs have been presented.

In current business world is very dynamic and fast changing. That’s why every professional have to have clear concept regarding this changes and he/she need to conform to these changing environments. In order to become a real professional peoples needed to enter into practical business world. A professional is a person who is skilled in the theoretical, scientific and practical aspect of an occupation and who performs with a high degree of competence. This internship program assists me to develop professional attitude towards banking business. The export department deals with export L/C, import department deals with import L/C and remittance section deals with the money transaction all over the world.

The whole banking activities of SJIBL are divided into four parts, General Banking section, Credit Section, Cash section & Foreign exchange section. One of the largest businesses carried out by the commercial bank is foreign trading. The trade among various countries falls for close link between the parties dealing in trade. The situation calls for expertise in the field of foreign operations. The bank, which provides such operation, is referred to as rending international banking operation. Mainly transactions with overseas countries are respects of import; export and foreign remittance come under the preview of foreign exchange transactions.

SJIBL involves import and export trade of various types of commodities. The imported commodities are pulses, raw cotton, spices, fruits, dry chilies, onion, garlic, alum’s, oilcake food grains, fertilizer, electronic goods, machinery, and others. The export commodities are Garments, knitwear, shrimps, Jute &Jute goods, rice bran, frozen fish, saw dust, coconut shell, cotton rags, etc. In 2009, 41.12 % of the total import trade was made for pulses. In 2009, 75% of the total export trade was made for shrimps. SJIBL considers customers as the heart of the organization. It always takes into consideration customer’s interest. The bank has been equipped with modern technology to facilitate import and export. It has also become a member of SWIFT. The import and export trade have been increased through this bank.

Foreign remittance’ means purchase and sale of freely convertible foreign currencies as admissible under Exchange Control Regulations of the country. That means transfer of fund from one place to another place in foreign currency. Foreign remittances pay a significant role in contributing to the growth of overall foreign exchange business. Remittance means the portion of migrant workers’ earning sent back from the country of employment to the country of origin (ILO, 2000). There are basically two types of remittance inward remittance and outward remittance. Our local banks are largely collect inward remittance.

There are two ways of sending remittance – formal channel and unofficial channel. Banks, exchange houses and different money transfer companies are the players of the official channel. Unofficial channel of remittance (called hundi) is illegal and prohibited under rules and regulations of the country. I am planning to arrange the full contents of the report in different parts so that the report progressively anchors to a desired destination of understanding. The paper will present a report of analysis about foreign exchange remittance and its growth and profitability of SJIBL in comparison with other conventional banks.

ShahJalal Islami Bank Limited management believes that in the coming years the Bank will try its level best to sustain its earning capacity and maintain a steady growth. With the current performance of the Bank and with little improvement here and they will certainly make ShahJalal Islami Bank Limited one of the best Private Bank in Bangladesh in the near future.

CHAPTER-1

1.0 Introduction

Economy of a country and its banking system are alike “Siamese Twin”. By mobilizing the capital of an economy, banking system plays a significant role to ensure economic growth. Bangladesh’s banking sector consists of central bank (named as Bangladesh Bank), Commercial banks, Development Banks and Specialized Financial Institutions. The Commercial banks comprise of Nationalized Commercial Bank (NCB), Local Private Bank, Foreign Private Bank, and Islamic Bank. In recent years, we observe a mushroom growth in the banking sector in Bangladesh. The very active and boisterous presence of private sector has stirred competition among the traditional commercial banks. Now, there are 52 private banks (41 domestic and 11 foreign) operating in Bangladesh. Facing the fierce competition, Government is now also considering the privatization of one of the NCBs (Agrani Bank, Janata Bank, and Sonali Bank) (Bangladesh Economic Review, 2006).

Banking sector, considered as ever growing child, in any country plays a pivotal role in setting the economy in motion and in its development process, while the banking structure -the number and size distribution of banks in a particular locality and the relative market power of specific banking institutions determines the degree of competition, efficiency and performance level of the banking industry.

The very active and lively presence of private sector has stirred competition among the traditional Commercial Banks. The shadow of fierce competition in banking industry can be observed through the recent achievement of the Private Commercial Banks.

The competition to pursue clients and imitate one another is so intense that one bank lures efficient staff of another bank offering higher facilities to get better edge. Private Commercial Banks often introduce new and diversified financial products to provide wider option to customers. Without having an effective customer base, it becomes difficult for any bank to compete and sustain in the competitive market for the banking services.

In order to retain and attract new customers towards any particular bank, the bank management needs to have a clear operational efficiency and must thoroughly analyze the scopes for further development. Therefore it is a key area for the commercial banks to closely monitor their performance level which comprises the functional units, that provides services to its clients. So, taking the opportunity to highlight the analysis of the performance of the different functional units and prepare the study for my internship, I was allowed to share the practical experience with Shah Jalal Islami Bank Limited, Satmosjid Road Branch.

Shahjalal Islami Bank Limited (SJIBL) commenced its commercial operation in accordance with principle of Islamic Shariah on the 10th May 2001 under the Bank Companies Act, 1991. SJIBL has diversified its service coverage by opening new branches at different strategically important locations across the country offering various service products both investment & deposit.

Remittance generates remarkable benefits for the home country economy in terms of micro and macroeconomic impacts. The remitters most of whom were unemployed in the home country are now getting employed in the host country. On the other hand, the inward remittance is causing employment generation domestically by reinforcing national savings, capital accumulation and investment.

1.1 Origin of the Study

This report is originated as the course requirement of the MBA program of BangladeshUniversity of professionals (BUP). The internship program has been conducted at Shahjalal Islami Bank Limited. As practical orientation is an integral part of the MBA course requirement, this report will take real life exposure of the research process in MBA course.

1.2 REPORT REVIEW

The report has six main parts. The brief overviews of the parts are as follows:

ü Part One: Report introduction along with objectives, mission, and vision scope.

ü Part Two: An overview of Berger Paints Bangladesh Limited including its history, ownership and organizational structure, vision, mission and core values, core technology, departments, SWOT analysis, competitions profile, strategies and product and services.

ü Part Three: This part of the report entails Research part.

ü Part Four: Data Processing and Analysis part (MS Excel and SPSS)

ü Part Five: The summary of findings is presented in this part.

ü Part Six: Conclusion and recommendation are drawn in this part of the report.

1.3Schedule of Activities

Questionnaire Design | 5 days | ||||

Data collection | 10 days | ||||

Data Analysis & interpretation | 10 days | ||||

Report Writing & Presentation

Finishing & Printing | 12 days |

3 days | |||

chapter-2

OVERVIEW OF THEORGANIZATION

2.1 Corporate profile of SJIBL:

Shahjalal Islami Bank Limited (SJIBL) was incorporated on 1st April, 2001 under the companies Act, 1994. SJIBL commenced its operation on May 10, 2001 by opening its first branch, i.e. Dhaka Main Branch at 58, Dilkusha, Dhaka obtaining the license from Bangladesh Bank, the Central Bank of Bangladesh. Its corporate head office is situated at 10,Dilkusha Commrcial Area, Jiban Bima Bhaban,Dhaka-1000, Bangladesh. Authorized capital of SJIBL is TK. 2,000 million and paid up capital is TK. 1,872 million.

Shahjalal Islami Bank Limited (SJIBL) is a Islamic bank based on Islamic shariah. There is a Shariah council, which is entrusted with the responsibility for ensuring that the activities of the bank are being conducted on the precepts of Islam. SJIBL is one of the leading first generation private sector banks in Bangladesh, which provides all kinds of commercial banking services to the customer. The bank went for IPO in the month January-February 2007.

The bank has grown significantly over the last 10 years in operation. The initial paid up capital of the bank was TK. 205 million subscribed by the sponsors in the year 2001, the capital and reserve of the bank as on 31st December 2007 stood at TK. 3,041 million including paid up capital TK. 1,872 million.

Shahjalal Islami Bank Limited (SJIBL) commenced its commercial operation in accordance with principle of Islamic Shariah on the 10th May 2001 under the Bank Companies Act, 1991. During last nine years SJIBL has diversified its service coverage by opening new branches at different strategically important locations across the country offering various service products both investment & deposit. Islamic Banking, in essence, is not only INTEREST-FREE banking business, it carries deal wise business product thereby generating real income and thus boosting GDP of the economy. Board of Directors enjoys high credential in the business arena of the country, Management Team is strong and supportive equipped with excellent professional knowledge under leadership of a veteran Banker Mr. Md. Abdur Rahman Sarker.

SJIBL desires to be the unique modern Islami Bank in Bangladesh and to make significant contribution to the national economy and enhance customers’ trust & wealth, quality investment, employees’ value and rapid growth in shareholders’ equity.

Corporate Information

| Name of the Company | Shahjalal Islami Bank Limited |

| Legal Form | A public limited company incorporated in Bangladesh on 1st April 2001 under the companies Act 1994 and listed in Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited. |

| Commencement of Business | 10th May 2001 |

| Auditors | M/S. Syful Shamsul Alam & Co. Chartered Accountants Paramount Heights 65/2/1 Box Culvert Road (level-6) Purana Paltan, Dhaka-1000 Phone: 88-02-9555915, 9560332 |

| No. of Branches | 64 |

| No. of ATM Booth | 14 |

| No. of SME Centers | 06 |

| Off-Shore banking Unit | 01 |

| Authorized Capital | Tk. 4,000 million |

2.2Mission and Vision of SJIBL

Mission of SJIBL

- To provide quality services to customers

- To set high standards of integrity

- To make quality investment

- To ensure sustainable growth in business

- To ensure maximization of Shareholders’ wealth

- To extend our customers innovative services acquiring state-of-the-art technology blended with Islamic principles.

- To ensure human resource development to meet the challenges of time

Vision of SJIBL

To be the unique modern Islami Bank in Bangladesh and to make significant contribution to the national economy and enhance customers’ trust & wealth, quality investment, employees’ value and rapid growth in shareholders’ equity.

Motto of SJIBL

Committed to cordial service.

2.3 Objectives of SJIBL

From time immemorial Banks principally did the functions of moneylenders or “Mohajans” but the functions and scope of modern banking are now a days, very wide and different. They accept deposits and lend money like their ancestors, nevertheless, their role as catalytic agent of economic development encompassing wide range of services is very important. Business commerce and industries in modern times cannot go without banks. There are people interested to abide by the injunctions of religions in all sphere of life including economic activities. Human being is value oriented and social science is not value-neutral. Shahjalal Islami Bank believes in moral and material development simultaneously. “Interest” or “Usury” has not been appreciated and accepted by “the Tawrat” of Prophet Moses, “the Bible” of Prophet Jesus and “the Quran” of Hazrat Muhammad (sm). Efforts are there to do banking without interest Shahjalal Islami Bank Limited avoids “interest” in all its transactions and provides all available modern banking services to its clients and wants to contribute in both moral and material development of human being. No sustainable material well-being is possible without spiritual development of mankind. Only material well-being should not be the objective of development. Socio-economic justice and brotherhood can be implemented well in a God-fearing society.

The objectives of Shahjalal Islami Bank include:

To conduct interest-free and welfare oriented banking business based on Islamic Shariah.

To implement and materialize the economic and financial principles of Islam in the banking arena.

To contribute in sustainable economic growth.

To help in poverty alleviation and employment generations.

To remain one of the best banks in Bangladesh in terms of profitability and assets quality.

To earn and maintain a ‘Strong’ CAMEL Rating

To introduce fully automated systems through integration of information technology.

To ensure an adequate rate of return on investment.

To maintain adequate liquidity to meet maturing obligations and commitments.

To play a vital role in human development and employment generation.

To develop and retain a quality work force through an effective Human Resources Management System.

To ensure optimum utilization of all available resources.

To pursue an effective system of management by ensuring compliance to ethical norms, transparency and accountability at all levels.

2.4 Goals of SJIBL

Shahjalal Islami Bank Ltd. will be the absolute market leader in the number of loans given to small and medium sized enterprises through out Bangladesh. It will be a world-class organization in terms of service quality and establishing relationships that help its customers to develop and grow successfully. It will be the Bank of choice both for its employees and its customers, the model bank in this part of the world.

2.5 Strategies of SJIBL

The strategies of Shahjalal Islami Bank include:

To strive for customers’ best satisfaction

To manage and operate the Bank in the most efficient manner

To identify customers’ needs and monitor their perception towards meeting those requirements

To review and update policies, procedures and practices to enhance the ability to extend better service to customers.

To train and develop all employees and provide them adequate resources so that customers’ needs are reasonably addressed.

To promote organizational effectiveness by openly communicating company plans, policies, practices and procedures to employees in a timely fashion

To cultivate a congenial working environment

To diversify portfolio both in the retail and wholesale markets

To increase direct contact with customers in order to cultivate a closer relationship between the bank and its customers.

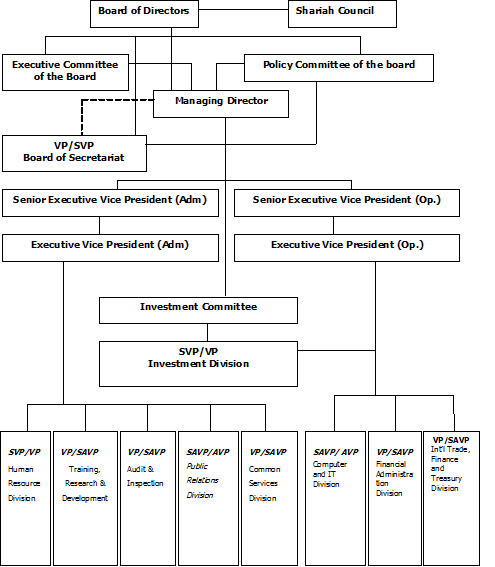

2.6 Organ Gram of SJIBL

2.7 Management Hierarchy of SJIBL

Managing Director (MD) | |

Deputy Managing Director (DMD) | |

Senior Executive Officer (SEO) | |

Executive Vice President (EVP) | |

Senior Vice President (SVP) | |

Vice President (VP) | |

Senior Assistant Vice President (SAVP) | |

Assistant Vice President (AVP) | |

First Assistant Vice President (FAVP) | |

Junior Assistant Vice President (JAVP) | |

Senior Executive Officer (SEO) | |

Executive Officer (EO) | |

First Executive Officer (FEO) | |

Junior Executive Officer (JEO) | |

Assistant Executive Officer (AEO) | |

Senior Officer (SO) | |

Officer | |

Management Trainee Officer | |

Trainee Senior Officer | |

Staff | |

Figure 2. Management Hierarchy of SJIBL

2.8 Principal Activities of SJIBL

The bank is carrying out commercial, corporate, investment and retail banking related services to its customers through its branches following the provisions of the Bank Company Act 1991 as follows:

- Deposits taking & Cash withdrawal

- Extending investments to corporate organization, retail, and small & medium enterprise

- Trade financing, project financing, working capital financing

- Lease and hire purchase financing

- Issuance of Debit Card.

2.8.1 Divisions of SJIBL

All branches of Shahjalal Islami Bank Limited are divided into the following departments:

- General Banking Division

- Foreign Exchange Division

- Investment Division

- HRD Division

- Information Technology Division

2.8.1.1 General Banking Division

General banking department is one of the most important departments of any commercial bank. Basically bank provides the main services to the customer through this department. In general this section of the Shahjalal Islami Bank Limited is divided into five sections.

- Accounts opening section

- Cash section

- Remittance section

- Bills and clearing section

The deposit of SJIBL stood at Tk.36,484.24 million as on 31.12.2008 as against Tk.22,618.19 million of 31.12.2007 registering an increase of Tk. 13,866.05 million, i.e. 61.31% growth. SJIBL so far launched the following deposit products:

- Ai-Wadiah Current Deposit

- Mudaraba Savings Deposit

- Mudaraba Short Notice Deposit

- Mudaraba Term Deposit Receipt

- MTDR-Special Scheme

- Mudaraba Foreign Currency Deposit

- Mudaraba Millionaire Scheme

- Mudaraba Monthly Income Scheme

- Mudaraba Double/Triple Benefit Scheme

- Mudaraba Monthly Deposit Scheme

- Mudaraba Hajj Scheme

- Mudaraba Housing Deposit Scheme

- Mudaraba Lakhopoti Deposit Scheme

- Mudaraba Mohor Deposit Scheme

- Mudaraba Education Deposit Scheme

- Mudaraba Marriage Deposit Scheme

Table 2. The Deposit-mix of the Bank as bellow:

| SL.NO. | Nature of Deposit | Taka in million | Percentage of Total Deposit |

| 1. | Ai-Wadiah Current Deposit | 1,266.56 | 3.47% |

| 2. | Mudaraba Savings Deposit | 1,863.52 | 5.11% |

| 3. | Mudaraba Short Notice Deposit | 765.11 | 2.10% |

| 4. | Mudaraba Term Deposit | 21,190.16 | 58.08% |

| 5. | Mudaraba Schemes Deposit | 9,426.65 | 25.84% |

| 6. | Other Deposits | 1,972.24 | 5.40% |

| Total | 36,484.24 | 100.00% |

(Shahjalal Islami Bank Limited, 2009)

2.8.1.2 Foreign Exchange Division

Banks play a very important role in effecting foreign exchange transaction of a country. Mainly transactions with overseas countries are in respect of imports; exports and foreign remittance come under the purview of foreign exchange department. Banks are the vital sectors by which such transactions are settled. Central Bank records all sorts of foreign exchange transactions. The other banks dealing with foreign exchange are to report to Bangladesh Bank regularly (viz. daily, monthly, quarterly, yearly etc.). The foreign exchange department consists of three sections. They are:

- Import section

- Export section

- Foreign remittance section

2.8.1.3 Investment Division

Total investment of the bank stood at TK. 32,918.77 million as on 31.12.2008 as against TK.20,616.61 million of 31.12.2007 registering an increase of TK.12,302.16 million, i.e. 59.67% growth. The bank is careful in deployment of the fund. Mode wise investments portfolio as on 31.12.2008 is given below:

Table 3. Mode wise investments portfolio

| SL.NO. | Mode of Investment | Taka in million | Percentage of Total Investment |

| 1. | Murabaha | 7,353.61 | 22.34% |

| 2. | Bi- muajjal | 13,224.94 | 40.17% |

| 3. | Hire-Purchase and Ijara | 5,436.44 | 16.60% |

| 4. | Investment against L/C | 106.13 | 0.32% |

| 5. | Bill purchased/ discounted | 3,721.76 | 11.31% |

| 6. | Investment against scheme deposits | 557.61 | 1.69% |

| 7. | Quard | 168.33 | 0.51% |

| 8. | Others | 2,322.95 | 7.06% |

| Total | 32,918.77 | 100.00% |

(Shahjalal Islami Bank Limited, 2009)

The Bank entertains good investment-clients having credit-worthiness and good track record. The Bank has got a few investment Schemes to provide financial assistance to comparatively less advantaged group of people; which are:

- House hold durable scheme

- Small Business investment program

- Small Entrepreneur investment Program

- Medium Entrepreneur investment program

- Housing investment program

- Rural investment program

- Car Investment Scheme

- Women Entrepreneur Investment Scheme

Apart from that, a number of new schemes are introduced in the year 2008, they are as follows:

- Investment for Self-employment

- Investment Scheme for Executives

- Investment Scheme for Doctors

- Investment Scheme for marriage

- Investment Scheme for CNG conversion

- Investment Scheme for Overseas Employment

- Investment Scheme for Education

2.8.1.4 Human Resources Division

SJIBL believes that employees are the most valuable resource. SJIBL thinks that the survival of the bank is highly connected with the service quality and employee satisfaction. Through these, the bank plans to increase the performance of the staffs and provide better service to the customers. Through providing proper training, rewards and recognition SJIBL empowers its employees with knowledge. Total manpower of the Bank stood at1601 as on 31st December 2009 as against 555 of 31st December 2007. (Shahjalal Islami Bank Limited, 2009)

2.8.1.5 Information Technology & Computer Division

Local Area Network (LAN) and Wide Area Network (WAN) system already been developed for automation and upgradation of the services in the Bank. IT & Computer Division of the bank has arranged trainings on different issues for the employees in 2009. (Shahjalal Islami Bank Limited, 2009)

2.9 Major differences between Conventional Bank & SJIBL

The major differences between conventional bank SJIBL and are mentioned below:

| Conventional Bank | SJIBL |

| 1. The functions and operating modes of conventional bank are based on manmade principles. | 1. The functions and operating modes of SJIBL are based on the principles of Islamic Shariah. |

| 2. The investor is assured of a predetermined rate of interest. | 2. In contrast, it promotes risk sharing between provider of capital (investor) and the user of funds (entrepreneur). |

| 3. It aims at maximizing profit without any restriction. | 3. It also aims at maximizing profit but subject to Shariah restrictions. |

| 4. It does not deal with Zakat. | 4. SJIBL collects and distributes Zakat. |

| 5. It can charge additional money (compound rate of interest) in case of defaulters. | 5. SJIBL has no provision to charge any extra money from the defaulters. |

| 6. The conventional banks give greater emphasis on credit-worthiness of the clients. | 6. SJIBL gives greater emphasis on the viability of the projects. |

| 7. The status of a conventional bank, in relation to its clients, is that of creditor and debtor. | 7. The status of SJIBL in relation to its clients is that of partners, investors and trader. |

2.10 SWOT Analysis Of SJIBL

A particular SWOT analysis discloses the following issues for an organization that an organization achieved over the time of its operation by analyzing its both internal and external environment:

ü “S”- Strengths

ü “W”-Weakness

ü “O”-Opportunities

ü “T”-Threats

The SWOT analysis of Shahjalal Islami Bank Ltd. is shown below:

2.10.1 Strengths:

Provides of good quality services: Having the reputation of being the provider of good quality services among its potential customers.

Differentiated Islamic Banking Products: SJIBL has several types of differentiated Islamic Banking Products (both deposit and investment) with unique features and facilities, which are so much helpful for enhancing the economic growth.

Wide range of financial products/services: Having wide range of financial products/services. Particularly the GB department has obtained most of the clients’ reliability in providing services by offering various financial schemes.

Good investment portfolio: SJIBL never invest all types of business area for that case their portfolio is very good.

Low Balance Requirement: Relatively low minimum balance/deposit requirement to maintain an account with the Bank.

Satisfactory business growth: From the star of the business in 2001 SJIBL run their business successfully and their business growth is very much satisfactory.

Experienced Top management: Management of SJIBL is very efficient and they always take correct decision for give better service to the customer.

Strong correspondent relationship: SJIBL maintains strong relationships with other commercial banks & a member of SWIFT service.

Strong Capital: SJIBL has strong capital base and maintain all the statutory requirements to be a good Bank.

Comfortable liquidity position: Shahjalal Islami Bank Limited always maintains a comfortable liquidity position in the market.

Achieve goodwill from the clients: SJIBL has already achieved a strong goodwill among the clients.

Strong concentration on Investment: Investment Division is the heart of SJIBL and main business area of the bank. Bank gives loans to the client by judging their business and concern how the clients repay the loan

Strong monitoring Process: Investment terms and conditions are monitored, financial statements are received on a regular basis, and any covenant exceptions are referred to the branch manager for timely follow up.

Strictly follow rules and regulations: The terms and conditions strictly followed by the authority of the bank that’s why SJIBL has low risk in loan defaultation.

Co-operative & skilled personnel: SJIBL has skilled personnel who are very much specialized in interacting with clients, (particularly in Investment department).

2.10.2 Weaknesses:

Complexity in account opening: Various complex requirements demanded by the Bank to open a new account.

Low geographic coverage: SJIBL’s branch expansions growth is not in satisfactory level. Outside the Dhaka division they have only 8 branches.

Limited delegation of power: For the sanction the loan branch has no power. All power in handed in the head office.

Lengthy Process for sanction the loan: All power in the head office for that case for sanctioning loans it takes more time.

No bank guarantee power: No branch has any bank guarantee power.

Conservative mind setting in working: SJIBL working structure is very much conservative and for that case its growth is slow than other bank.

Lack of strong and attractive promotional activities: It is an Islami perspective bank, so it spends money for promotional activities in a low rate.

2.10.3 Opportunities:

Perception of Islami bank: Strong appetite for Islamic financial services among the people of Bangladesh.

Give higher interest rate: Possibility to generate very high rate of return as compared to fixed rate of interest from other bank

Demand Endless: Banking industry is an industry with an endless demand in the future.

Concentration in Other business area: It has an opportunity in SME and Agro based business.

Credit card Facility: If in future SJIBL provide to the client credit card in dual currency then it can be differentiated from other commercial bank.

Merge with Same nature bank: Expansion of existing Banking networks through merge with other Islamic Banks will facilitate the bank to enjoy the competitive advantage.

Be Prepare in competitive advantage: A large number of private Banks coming into the market in the recent time. In this competitive environment Shahjalal Islami Bank must expand its product line to enhance its sustainable competitive advantage.

Credit card Facility: If in future SJIBL provide to the client credit card in dual currency then it can be differentiated from other commercial bank.

Wide Banking networks: The bank should establish a wide range of banking network in the country and outside the country.

2.10.4 THREATS:

Lack of awareness: Lack of awareness regarding the Islamic Banking system among the people of Bangladesh.

Products name difficulty: Name of the products is so much difficult to understand and very much confusing, such as – Mudaraba, Murabaha.

Increase financial institutions merging: The worldwide trend of mergers and acquisition in financial institutions causing problem.

Money rate devaluation: Frequent taka devaluation and other rate fluctuation is causing problem for the bank.

Guideline: Lack of adequate guideline by the Central Bank on the basis of Islamic Shariah.

Competition increase: Increased competition from fellow Islamic Banks and Other Commercial Private Banks (PCBs).

Lacking in fund collection procedure: Limitation (as an Islamic Bank) to borrow from the money market (short term funds), which may produce a threat to the liquidity of the Bank.

Market pressure: Market pressure for dollar ($) crisis is increasing day by day.

Government rules and regulations: Unfavorable Government rules and regulation created regarding Banking business that hampers their business procedure.

Economic and political situation: Unfavorable economic and political climate, such as high inflation rate & continuous devaluation of money.

Increase financial institutions merging: The worldwide trend of mergers and acquisition in financial institutions causing problem.

Government rules and regulations: Unfavorable Government rules and regulation created regarding Banking business that hampers their business procedure.

CHAPTER-3

LITERATURE REVIEW

3.1 Measures for Promoting Exports in the Short and Medium Terms[1]

India has emerged victorious in the recent recession, which started in the US and engulfed the whole world in a short span of time. India could be able to secure a respectable rate of growth of 6.7 per cent during 2008-09, which is the second highest in world after China. This was mainly because of the domestic-led demand of the Indian economy and stimulus measures initiated by the government at the fiscal and monetary policy levels. However, the exports of India suffered a great deal as a result of the sagging demand in the world economy in general and its main trading partners’ economies in particular. Except for the months of November and December, the previous months of the current fiscal year 2009-10 witnessed negative export growth rates. This in spite of the array of trade policy initiatives announced by the government under the Export-Import (EXIM) Policy 2009-10. These were incentive measures to promote exports. They mainly comprised extension of the Duty Entitlement Passbook (DEPB) scheme up to 2010, making the Export Promotion Capital Goods (EPCG) scheme more attractive, enhancing incentives for Export-Oriented Units (EOUs)/Special Economic Zones (SEZs), etc. Some product-specific and market-specific incentives, which were already in place, were also made more attractive. However, much more is desirable to promote exports not only in this crisis time but also for the long term. Though the World Trade Organisation (WTO) provisions have squeezed the policy space for the promotion of exports, still there are many WTO-compliant areas where the government can pay due attention.

The whole gamut of measures to promoting exports can be divided into two broad categories—price measures and non-price measures. The price measures are supposed to enhance the competitiveness at the price front, whereas the non-price factors give competitive edge in areas other than the price front. The former category includes devaluation of currency, all kinds of indirect and direct tax benefits to exporters etc., whereas the latter one comprises the upgradation of quality of product, fast delivery of consignment, post-sale services etc. The price factors are of short term in effect because they can be emulated easily by the competitor country in a short span of time. For example, if the government initiates the devaluation of the currency, which is the most popular measure at the price front, it would make exports competitive at the price front in the international market, unless the exports are not much import-intensive. This would be immediately increasing sales in the international market (supposing there is the price elastic demand and enough supply of the product). However, having experienced the decrease in demand of their products, the competitor countries might also initiate the same measure neutralizing its effect. So the effect of price factors can be easily neutralized in the short term by the competitor countries.

As far as the non-price factors are concerned, they have long-lasting impact and cannot be matched easily by the competitor countries. For example, improving the export infrastructure, both soft and hard, to fast deliver export consignments would have a long lasting impact on the country’s exports. However, it would not be as easy as the price factors to be implemented, but once effected, they would have a long-lasting effect on exports, which cannot be easily neutralized by the competitor country.

International transaction (export) faces many barriers. They can be broadly categorised under sub-headings—tariff barriers and non-tariff barriers. The tariff barriers in general have come down substantially the world over under the multilateral negotiations of the WTO, regional trading negotiations and unilateral initiatives. Barring some countries, like the African ones, and some sensitive commodities, the tariffs have come down across all tariff lines and countries. The conventional non-tariff barriers, like quota, have also been scaled down a great deal. However, currently new non-tariff barriers decide the competitive edge of the country concerned. These include trade facilitation conditions of the country and capacity to meet sanitary, phyto-sanitary and technical standards, among others. One estimate suggests that one-third of the cost of international trade is attributable to transportation cost, which includes carrying goods from the production site to the exporter’s sea port or airport, meeting all documentation-related formalities, shipping/air cost and finally costs relating to taking the goods to consumers in importing countries. All these costs reflect in the price of one’s exported commodity which, in turn, decides the competitiveness of commodity vis-à-vis the domestically-produced good and goods imported from competitor countries. Thus the trade facilitation cost is an important determinant of deciding the country’s competitiveness in the international market. The trade facilitation cost is even higher for the agricultural and mineral items, as the transportation cost is the positive function of weight. It is higher for the heavier goods than the lighter ones. (De 2010)

Though in this crisis time, price factors might bring immediate respite for the exporters (supposing the competitor countries do not respond in a similar fashion), the non-price factors will have long-term effects and they cannot be matched easily by the competitors. Among the non-price factors, some of them can be easily implemented with relatively less effort and time. For example, soft infrastructure, including export and import procedures, can be improved with relatively less effort in the short run. Though the initiative to streamline the system has already been taken, still a lot more is desirable at this front. India’s trade facilitation index value constructed by combining three variables—procedures to exports, days to exports and costs to exports—is not comparable even with many ASEAN countries, leave alone the Western countries. (RIS 2010) As per the Doing Business Report (2008) of the World Bank, exporting a consignment takes 17 days along with dealing with eight documents and costing US $ 945 in India, whereas in Malaysia exporting a consignment takes 14 days, deals with seven documents and costs US $ 345. The EU averages for the same are 11 days, five documents and almost US $ 940. As per the Logistic Performance Index of the World Bank, India stands at the 47th rank with the average being 3.22 points in the list of 150 countries. So there is much scope for improvement on this score.

Trade facilitation (soft infrastructure) has been found a statistically significant factor affecting trade flow. In one World Bank study, it has been found that 10 per cent improvement in export custom procedures would enhance the export performance by 15.8 per cent and 17.1 per cent for the merchandise exports and manufactured exports respectively. (Broadman 2007) In the same way, an increase in internet services by 10 per cent in the exporter country would enhance the exports of all products and manufactured products by 1.9 per cent and 2.2 per cent respectively. (Broadman 2007) The sensitivity (elasticity) of Indian exports to trade facilitation is more than to the tariff rate as per the estimation of the gravity model carried out by the author. The soft infrastructure can be improved in the short run with some conscious efforts for better coordination of various agencies involved in trade and capacity-building programmes of the staff. E-trading/filing is still operating on papers, which can be made operational with less efforts in a short time.

Likewise, of late the capacity to meeting sanitary and phyto-sanitary standards for agricultural products and technical standards for other manufactured products is significant for exporting especially to the developed countries. Conforming to these standards is difficult mainly for the small scale industries (SSIs). Educating the businesses, especially the SSIs, about these standards and establishing testing laboratories and certificate-giving agencies would be helpful in this regard. Financial and technical assistance to the SSIs to upgrade their technology would also go a long way in this direction. The government is already doing work in this area. However, there is a need to intensify efforts in this crisis time.

Another area that can be exploited in this crisis time with relatively less effort is diversifying Indian exports geographically. Though country-specific incentive schemes are already there, a lot more is desirable. India has traditionally relied more on the countries of the North for its exports. It is advisable to identify new markets from the South. For example, there is much scope to increase exports to the African countries. The African countries, in spite of being prominent allies of India politically, always figure less favourably in India’s economic priority list, albeit of late some efforts have been initiated by the Indian Government to strengthen economic ties with these countries. Major policy initiatives by India after year 2000 included the Focus Africa Programme, TEAM-9 Initiative, Pan-African E-Network, India-Africa Partnership Conclaves and India-Africa Summit. A major thrust to Indo-African economic relations came after the conclusion of the Indo-African Summit, held in 2008 in New Delhi, with the aim of promoting trade and investments between India and the African countries.

All these initiatives resulted in a steep increase of Indian exports to Africa during the last 10 years. Exports from India to Africa have increased about five fold from US $ 1.69 billion in 2001 to US $ 8.80 billion in 2007. However, it is still below the potential. More institutional backing by the government coupled with private business chambers’ efforts to identify business opportunities in various new markets by organising business meets would go a long way in this regard. The research institutes may also be helpful on this count. In fact, the major problem is the dearth of information and misconceptions about the new markets impeding exports. This seems to be reason as to why exporters always feel satisfied with conventional markets. Finding new markets requires research, which entails cost. This is an area where the government can chip in. It would be WTO-compliant also as it would fall under the permitted category of subsidies. Another region for diversifying Indian exports might be the Latin American countries. Let alone these distant markets, even within SAARC nations many commodities which India can export to the rest of the member countries at competitive prices are imported from outside the bloc partly for lack of knowledge. (Das 2010)

Searching new markets from the South is also strategically significant for India in the long run. The current financial crisis has exposed the imbalances in the world economy. It has exposed many weaknesses in the present world economic system and the US economy. The confidence in the US economy as the ‘power house’ of the world economy has been shaken. It has been widely realised that the US cannot live forever beyond its means, a privilege it has been enjoying for long as a result of its currency being the main reserve currency in the international monetary system. It gives it seniorage benefits, which have been permitting it to maintain the current account deficit continuously for a long time. (Agarwala 2009) However, having realised the danger of the present system, it is advisable for India to start finding new markets from the South, as there are strong chances of reshuffling of the composition of demand in the world economy. To make the world system more stable, it is a good idea that the US learns to save and Asia, regarded as the saving glut, learns to spend more. In the near future, there is a chance of substantial devaluation of the US currency. It would be in the long-run interest of India to step up the demand for its exports away from the conventional markets to the South, which has a strong possibility of growth in the future.

The government can initiate the process of strengthening the institutional mechanism with these countries. For example, India does not have any operating regional trading bloc (RTB) with the African countries, though a few are in the process of negotiations. One regional trading bloc is being negotiated with the Southern Africa Customs Union (SACU) and another bilateral trading arrangement with Mauritius is in the process of negotiations. The IBSA, including India, Brazil and South Africa, is also in the pipeline. India has two preferential trade agreements with the Latin American countries—one, with Chile and another, with MERCOSUR. It is advisable to expedite the process of negotiations in Africa to operationalise these RTBs early and replicate the same process with the other countries of the continent on the basis of thorough research for the economic viability of the RTBs. The results of these initiatives might fructify in short to medium terms.

The Government of India, with the help of the Export-Import (EXIM) Bank, can increase the line of credits (LOCs) to these countries for various infrastructure projects with the arrangement of buying machineries and equipments from India. The EXIM Bank of India has many lines of credits (LOCs) operating in Africa, Asia, the CIS, Latin America and the Caribbean. As on November 30, 2008, the Bank had 114 LOCs operating in 94 countries with credit commitments aggregating US $ 3.75 billion. They are meant to facilitate the import of project-related equipments and services from India on deferred payment terms. These can be further increased. These will bring a win-win proposition for India and the poor countries availing this facility. On the one hand, it would provide the much-needed help from India to these countries for developing their infrastructure; on the other hand, it would provide the impetus to Indian exports at this crisis time.

One reason as to why Indian exporters do not prefer to export to these new markets from the South is that they do not have proper trade-facilitating financial institutions. Conducting international trade requires the involvement of banks in both the countries. There is a lack of institutional capacity in the financial sector in these economies. The Indian Government can help these economies on this count as well. The EXIM Bank of India has already helped many poor countries in establishing their EXIM banks. These efforts can be further intensified.

¨

On the price front, it is advisable to make the Indian economy more cost-effective. Though after the 1991 reform programme many initiatives in this regard were initiated, many areas are still not addressed. One such area is making the cost of capital (lending interest rates) more competitive. Apart from the business cyclic conditions, the lending interest rates in an economy are decided by the cost of reserve which the bank is supposed to pay, the cash reserve ratio (CRR), statutory liquidity ratio (SLR), operating cost of banks etc. Though the CRR, SLR and bank rates are coming down over the years, the lending rates are still not competitive in comparison to the world standard. The main reasons are the administered rates fixed by the government on certain savings, such as post office monthly savings, Public Provident Fund, Kisan Vikas Patra etc., and the high operating cost. Banks are paying attention of late on the operating cost by being more technology-savvy. However, administered interest rates are still coming in the way of banks reducing their deposit rates to the level dictated by the market fundamentals for the fear of losing deposits to other instruments offering administered interest rates, which are higher than the market-determined rates. This, in turn, eventually reflects in higher lending rates. Doing away with administered interest rates would help in reducing overall lending rates in the economy. This measure will be WTO-consistent.

The incentive schemes to promote exports should be designed in such a way which could generate the maximum growth of exports. The export items can be divided into two categories—dynamic export items and non-dynamic export items. Dynamic export items are those which have been experiencing high growth rates for the last many years, whereas non-dynamic ones are having low growth rates, though they may hold high shares in total exports. As per the four-level HS classification, the dynamic products the world over are only 125 items. Out of these dynamic items, India exports 40 items. In the last recovery time, these items played a significant role in reviving India’s overall export growth rate. This time also, these items are expected to record high export growth rates in the period of recovery. There is a need to focus on these dynamic products for the incentive schemes.

For the medium to long term, the hard part of export infrastructure can be improved. These include improving inland roads/railway lines to ports, enhancing warehousing and cold storage facilities, improving port/airport capacity to handle export consignments fast etc.

Another area which can be taken care of in the medium to long term is going for network production, which is the modern way of organising production. Of late, technological advances in information technology, logistics and production have allowed corporations to divide value chains into functions performed at different countries (based on comparative advantages) by either foreign subsidiaries or contract suppliers. These comparative advantages can stem either from the availability of some special raw material or availability of a certain kind of labour market. For example, as the product goes through many stages before it reaches the consumers as the final product, some stages require relatively low skilled labour, whereas other stages of production require semi-to high-skilled labour. Relatively less-developed countries have cheap low- and semi-skilled labour, whereas relatively developed countries have medium- to high-skilled labour. Thus a range of countries can be incorporated in the network production to cut the cost. There has been a rapid growth of intra-industry network trade in parts and components relative to conventional inter-industry trade of late.

The countries of the North and ASEAN countries could be able to increase their competitiveness through this process. India can also follow the same strategy by engaging the South Asian countries, with which it has the South Asian Trade Agreement (SAFTA), and other countries. Regional trading arrangement is a facilitator for the network production, as components and parts can be traded without tariff and non-tariff barriers. India has also tried network production recently. The Indian tyre company, CEAT, is a typical example: it established an export-oriented tyre plant in Sri Lanka to cater to its growing markets in Pakistan, Middle East and other countries. This will take the advantage of abundant resource of natural rubber available in Sri Lanka. This can be emulated in other areas also, especially relating to buyer-driven network production, such as food, textiles, furniture, etc. It is also possible in the services sector. Medical tourism is one such area. Back-up offices of Indian companies in other relatively less-developed countries (having low wage rate) with reasonable computer-skilled labour is yet another potential area. Medical tourism would increase directly services export, whereas the back-up office would give competitive edge to the main product lines on the price front in the international market.

3.2 ADB signs deals with 12 banks to boost export-import trade (The Financial Express: 18.12.2009) The Asian Development Bank (ADB) has signed deals with 12 local private Tcommercial banksT for expansion of its TTrade FinanceT Facilitation Programme (TFFP) in Bangladesh. Under the agreement, the banks will be able to offer more trade financing support to their clients particularly exporters and importers through Tinternational banksT. The banks are Bank Asia Ltd., BASIC Bank Ltd., Dhaka Bank Ltd., Dutch Bangla Bank Ltd., Eastern Bank Ltd., Export Import Bank of Bangladesh Ltd., National Bank Ltd., Premier Bank Ltd., Prime Bank Ltd., Southeast Bank Ltd., Standard Bank Ltd., and United Commercial Bank Ltd. The signing ceremony was held at a local hotel on 17.12.2009 morning. Chief executives and senior officials of the banks concerned were present on the occasion. “We’ve taken the TFFP aiming to increase trade volume regionally as well as globally,” Steven Beck, head of Trade Finance Capital Markets and Financial Sectors Division and Private Sector Operations Department of the ADB, told. Under the programme, the triple-A rated ADB provides loans and guarantees through, and in conjunction with, local and international banks to back trade transactions.

Import duty on 18 Bhutanese products to be withdrawn The government is going to withdraw entire import duty from 18 major exportable products from Bhutan including some industrial raw materials, fresh fruits and spices to boost bilateral trade with the neighbouring country. South Asian department of foreign ministry has urged the NBR to take necessary steps to withdraw import duty from the import items following a commitment by Prime Minister Sheikh Hasina during her recent visit to the country.The PM has made the commitment to enhance bilateral trade with Bhutan during her visit on November 6-9. She has announced that Bangladesh will reduce tariff on 18 commodities imported from Bhutan from the existing rate of 15 per cent to zero. Bangladesh is enjoying duty-free access of her products to Bhutan. “We will issue an order in this connection after getting directive from the finance minister,” said National Board of Revenue (NBR) Chairman Nasir Uddin Ahmed. Bangladesh imports products worth $14 million annually from Bhutan while it exports products worth $1.3 million.

(The Financial Express: 20.12.2009 17)

3.3 Local Forex Market: “what volatility”?[2]

Overall in 2009, the dollar gained marginally by 0.46%, beginning the year at 68.95 and closing at 69.27, most of the gain coming in the last two months. Strict regulatory supervision and intervention ensured very little volatility throughout the year that was full of uncertainty in the aftermath of the global financial meltdown and jitters about economic recovery. Towards the later part of the year, import of petroleum, fertilizer and scrap vessels created some demand for the dollar in an otherwise lackluster year when most banks only saw influx of dollars for which the only buyer was the central bank.

While the other Asian currencies rebounded from the spectacular drop the year before, BDT was protected from appreciating in the interest of the remittance recipients and exporters. While free-market economists may frown up on such a strategy, we would like to point out that during the tumultuous period of 2008, while other Asian economies such as India, Korea, SriLanka saw severe weakening (20-30%) of their currencies, BDT remained fairly resilient losing only 0.5%. At that time, while exporters were demanding forced depreciation of the BDT, it protected the importers and inflation. The apprehension and fear of negative remittance growth was proven wrong by the expatriateBangladeshis, and a record amount of remittance boosted the country’s forex reserves.

During the year, moderate export growth, declining import cost, and a record breaking inward remittance figure pushed the country’s forex reserves to double digits for the first time in history. It was quite unpredictable that our Forex reserve would grow by nearly 100% during the year from $5.35bn in Jan09 to $10.34bn to close out the year.

Bangladesh Bank also revised scheduled bank’s net open position (NOP) limit twice this year to accommodate more FCY to be held by the banks. Bangladesh Bank also withdrew the restriction on FX Forwards. HSBC concluded world’s first ever BDT FX Option by combining a CALL and a PUT option to create a zero premium collar for its customer.

3.4 Rising inflation, fall in remittance overshadow export earnings[3]

Rising trend of inflation, fall in remittance inflow and infrastructural constraints did not give Bangladesh a chance to relax in the outgoing year (2010) although it has overcome the economic meltdown successfully, reports UNB.

Mirza Aziz said that the flow of remittance witnessed a sharp fall in the year 2010 and it is one of the worrying factors. “The remittance inflow decreased as a result of sliding trend of manpower export.” He said that like the previous years, infrastructural problem including energy and power crisis remained one of the disappointing aspects of the country’s economy this year.

He mentioned that the external aid disbursement has also slowed down during the year.

Mirza Aziz mentioned that increasing investment for achieving accelerated growth, ensuring food security and addressing the climate change issues will be the main challenges for the grand alliance government in the coming year.“The investment ratio to GDP stood at around 24 percent over the last 4-5 years and it should be taken to 30-32 percent for accelerated growth,” Bangladesh Institute of Development Studies (BIDS) director general Mustafa K Mujeri, while talking to the agency, said that the year 2010 witnessed a mixed trend of economic activities.

Mujeri said the agricultural sector witnessed a good production but the external sector seemed to experience pressure due to the remittance fall. “The external sector falls under pressure if there is no good remittance growth. Fall in remittance growth also put pressure on balance of payment.”

On inflation, he said that it still remains high; especially the food inflation causes difficulties for the general masses. Terming energy and power crisis as the main barrier towards investment, Mujeri said the government should speed up its efforts to resolve crisis. The annual average inflation, however, remained steady at 8.12 percent in the month, putting a brake on the rising curve since November 2009.

3.5 Trends in Migration Flows from Bangladesh[4]

Overseas employment contributes significantly to the economic development of the country. From the inception of manpower export in 1976 to 2008, manpower having strength of about 6.57 million has been exported. Including first seven months of 2009, total number of manpower exported to foreign countries was about 6.8 million (BMET, 2009). Only in 2008 about 0.88 million people have migrated for foreign employment. With a few exceptions, manpower export has been increasing every year. Table 1 shows the trends in oversees employment from the period of 1976 to 2007 by using various categories of four-year total. Only 69116 Bangladeshis had gone abroad for employment during 1976-1979 and during 2004-2007, this figure has reached to about 1.74 million. During 1992-1995, manpower exports accounted for 0.81 million, which is about 52 percent higher than the period of 1988-1991. There was slight decrease in population migration during 2000-2003 and the rate of decrease was 8.95 percent than the previous period (1996-1999). In 1999, altogether 268182 persons migrated; the figure dropped to 222686 in 2000 and further to 188965 in 2001 (BER, 2008). The probable reasons for this may be multiple. One reason may be due to the stiff competition from new labour-exporting countries like Nepal, Vietnam and Cambodia, which have recently entered the international labour market and supply cheaper labour. Another reason may have been the rise in unemployment in some Arab countries, which has spawned policy decisions to indigenise the labour force. In doing so the Arab countries increased the cost of formal emigration, which has decreased the number of formal migrants. A large number of Bangladeshis are also believed to have gone to the Middle East through irregular channels (Siddiqui, 2003). Moreover, there is a sharp decrease in the manpower export in the first seven months of 2009 which is largely due to the ongoing world-wide economic crisis of last year. From January to July 2008, a total of 572098 manpower was exported abroad. But this figure dropped to only 288903 during the same period of 2009, which is about half of the last year (Bangladesh Bank, 2009).

According to Chami, et al, 2005 based on panel data (annual) of 87 countries during the period of 1980-2003 suggests that while host country GDP has statistically positive impact on remittances, home country GDP, presence of multiple exchange rates and black market premia, restrictions on holding foreign exchange deposits have significant negative impact on the same. Variables like financial development, political risk, law and order, relative investment opportunity were found to be of little significance in influencing inward remittance flows. The study also estimated that removal of all exchange rate distortions led remittances increased to increase by 1-2 percent of GDP[5].

CHAPTER-4

4.1 Problem Statement

The problem statement of this report is as follows:

“Foreign exchange trading and its risk management: A Critical evaluation of Foreign exchange operations of Shah-jalal Islami Bank Limited”.

4.2 Background Of The Problem

Several studies has been conducted on foreign exchange operation & performance (growth, income) analysis foreign and remittance inflow channel but a very few studies has been conducted on developing this channel with policy implication. In our country many workers send remittance but they and their family face many problems when remittance sends. For that reason, the existing public evidence is of limited relevance in identifying the appropriate channel and inflow remittance policy.

Trade is an integral part of the total developmental effort and national growth of all economies including Bangladesh. It particularly plays a central role in the development plan of Bangladesh where foreign exchange scarcity constitutes a critical bottleneck. So, in my research I want to find out many problems, procedures and how to improve along with policy implication with the concern for the foreign exchange operation; the relationship between the income and the expenditure in the foreign exchange department.

Export trade can largely meet ‘foreign exchange gap’, and export growth would increase the import capacity of the country that, in turn, would increase industrialization, as well as overall economic activities. Bangladesh’s import needs are substantial; hence the need to rapidly increase exports is immediate. In order to finance the imports and also to reduce the country’s dependence on foreign aid, the Government of Bangladesh has been trying to enhance foreign exchange earnings through planned and increased exports. However, the global trade scenario has exposed structural limitations of the Bangladesh economy, posing a variety of challenges for the country that has underdeveloped technology and a low capital base.

In this paper I have discussed about the composition, performance and trends of foreign trade of Bangladesh. In the process, we examine Bangladesh’s export and import performance & also find out the necessary key factors that can boost up foreign exchange growth rate and also find out the ways to minimize the foreign exchange risks.

4.3 Research Objectives

4.3.1 Broad/General Objective

To study of the Foreign exchange trading and its risk management: A Critical evaluation of Foreign exchange operations of Shah-jalal Islami Bank Limited and make an industry analysis on the banking sector of Bangladesh.

4.3.2 Specific Objectives

The specific objectives are given below:

- To find out how Foreign Trade and Foreign Exchange is operating in SJIBL.

- To find out the strengths, weaknesses, opportunities and threats of Foreign Exchange department of SJIBL.

- To find out the position of SJIBL through the comparative analysis and the trend analysis.

- To present the current situation of Export, import, foreign remittance in SJIBL.

- To analyze the growth rate of income & expenditure and also to find out the relationship between the income & expenditure of the Foreign Exchange Department of the SJIBL.

- Analyze the total performance of Export, Import & Remittance of SJIBL.

- To analyze the relationship between unemployment rate and foreign remittance inflows.

- To analyze the relationship between GDP and foreign remittance inflows.

- To find out existing problems of Foreign Exchange of Bangladesh.

- To find out the factors that may create the foreign exchange risk and also find out ways to minimize the foreign exchange risks.

- To formulate alternative strategies for solving the problems.

- To recommend some better solutions for solving the problems.

- To formulate an implementation plan for the recommended steps.

4.4 Research Questions and Hypotheses

4.4.1 Research Questions and Hypotheses For Evaluating the performance of the Foreign Exchange Department of Shah Jalal Islami Bank Limited.

Question01: Is there any significant relationship between the income and expenditure of the foreign exchange department (Export, Import, and Remittance)?

Justification: To operate the foreign exchange procedures for earning more in the foreign exchange department (Export, Import, Remittance) have to bear some expenditure. This question may help to find out the relationship between the income and expenditure and the direction between these two variables also. To find out is the foreign exchange department is in the profitable situation or not. It will be profitable if as the income increases and the expenditure decreases.

Hypothesis 01: There is a strong negative relationship between the income and expenditure of the whole foreign exchange department (Export, Import, and Remittance).

Question02: Is there any significant relationship between the GDP growth rate and the overall foreign exchange growth rate of SJIBL.

Justification: This question may help us to analyze the relationship between the GDP growth & the export, import & foreign remittance growth trend. And from the trend analysis we can find out the how well the Shahjalal Islami Bank is performing. From that we can also predict that how much contribution is added to the BD GDP growth by the SJIBL.

Hypothesis02: There is a positive relationship between the GDP growth rate and the export, import & remittance growth rate of SJIBL.

Question03: Is there any significant relationship between the overall export, import & remittance growth trend of Bangladesh with the export, import & remittance growth trend of SJIBL?

Justification: This question may help us to analyze the performance of foreign exchange department of SJIBL in compared to the overall foreign exchange performance of Bangladesh. This may help us to know really that bank’s FOREX is performing well or not, how it performing, which policy implication will help for better performance in future.

Hypothesis03: There is a positive relationship between the overall export-import & remittance growth rate of BD with the export-import & remittance growth rate of SJIBL.

Question04: Is there any relationship between the unemployment rate and remittance growth from last 5years data?

Justification: This question may help to identify the relationship between the unemployment rate and the remittance growth. Normally as the unemployment rate decreases the remittance growth should go up. Because as people become more employed in abroad automatically they can earn more; as a result, they can be able to send more money through remittance. Remittance growth will be increased.

Hypothesis04: There is the negative relationship between the unemployment rate and foreign remittance.

4.4.2 Research Questions and Hypotheses For Analyzing The Foreign Exchange Risk Management of the Shah Jalal Islami Bank Limited.

Research Question05: What is the impact exchange rate fluctuation in evaluation of foreign exchange risk?

Justification: Foreign Exchange Risk arises from exchange rate movements which may affect the profit of the Bank. The introduction of market based exchange rate of Taka has resulted in both trading opportunities and associated Foreign Exchange Volatility risk.

Hypothesis05: Exchange rate fluctuation has a greater impact on the foreign exchange risk.

Research Question06: Is there any significant impact in minimizing the risk through the proper customer information analysis?

Justification: Customer information is very much important in this division. The management should properly examine all the information that the customer submitted. Any falsification of the customer may create huge loss in the bank. So, before opening L\C, or incase of remittance all the information should be examined properly.

Hypothesis06: Accurate customer information has a positive impact on reducing foreign exchange risk.

Research Question 07: What are the factors that can raise the foreign exchange risk?

Justification: It is obvious that to reduce the foreign exchange risk the bank must have to find out the present state of the economy. They must have to overlook at the total foreign trade situation of the whole economy and also find out where the problems have been occurred which factors are creating the problem. According to CPD Task Force Report (policy brief on “Macroeconomic Policies”) there are some reasons that create the foreign exchange risk. The reasons are:

(a) Erosion of competitiveness of the economy leading to fall in exports

(b) Further rise in petroleum prices in the global market precipitating more pressure on the foreign exchange reserve

(c) Unforeseen and sudden setbacks in crop production necessitating cash imports of food grains

(d) Lagged emergence of inflationary pressure triggered by crop loss or any other exogenous factor.

Hypotheses07: There is a positive relationship between the factors (such that Erosion of competitiveness, inflationary pressures, unemployment, sudden setbacks in crop reduction, and also rise in petroleum prices) and the foreign exchange risk.

4.5 Scope and Limitations of the Study

4.5.1 Scope

This report will cover only banking industry prevailing in Bangladesh and here I focus on Shahjalal Islami bank & the Dhaka bank only; and my area of doing survey is the Dhaka city only for the time limitations. It would be a great endeavor if the report could incorporate the international standard and comparison among other industrial and service sectors.

4.5.2 Limitations

Limitations for doing this report are as following:

- Time Constraint

- A structured filing procedure is often neglected which also poses difficulty in understanding the sequential procedure.

- The bank officials though helpful in every respect do not have much time to explain the internal procedure.

- Sometimes it may be impossible to contract with a few members of respective banker and NRB families for the research work. It would be more resourceful for the report if more interviews could be taken.

- The experts of our country, who could have put their valuable views on the report, were highly committed and therefore were unavailable for interviewer.

The main problem may be faced in preparing the paper will be the inadequacy and lack of availability of required data. This report is an overall view of “foreign exchange Operation” of SJIBL.

4.6 Methodology Of The Study

4.6.1 Types of the Study

This study will be the applied research as it will find out different factors that would affect the foreign trade and the foreign remittance inflows in Bangladesh at present state and also find out the ways to minimize the foreign exchange risk. At first an exploratory research was be conducted to clarify and define the nature of the problem. It would make possible to design the research questions and questionnaire and to formulate the hypotheses in details. Then a conclusive research through the descriptive method will be carried out to examine the relationship and describe this.

4.6.2 Basic Research Method

This study will be carried out mainly through the quantitative research method. But trough the observation and face to face conversation with the officers I could not ignore to collect data. Secondary data analysis and pilot study will be use for conducting this method. After that, a sample of respondents will be surveyed through the face to face interview.

4.6.3 Sampling

The basic of sampling is that by selecting some of the elements in a population, I may draw conclusions about the entire population. There are several compelling reasons for sampling, including:

- Lower cost

- Greater accuracy of results

- Less time, etc.

4.6.4 Target Population

There will be two types of populations to be surveyed. One group is the clients who are involved with the foreign exchange department of the bank and the other would be the employees (officers) of the bank.

4.6.5 Sampling Technique

The research will be based on probability and non- probability sampling method. Out of the probability sampling methods, random sampling will be used. Judgmental sampling method will be followed from the random sampling.

4.7 Sample Size Determination

Sample size calculation is concerned with how much data we require to make a correct decision on particular research. If we have more data, then our decision will be more accurate & there will be less error of the parameter estimate. This doesn’t necessarily mean that more is always best in sample size calculation. A statistician with expertise in sample size calculation will need to apply statistical techniques and formulas in order to find the correct sample size calculation accurately.

Using appropriate formula that means the proportion it can be found out as determined follows:

NZ2pq

n =

Nd2 + Z2pq

Where,

N = Population size

n = Sample size

p = Estimated population proportion

q = 1-p, or estimated proportion of failures

d =Precision level or magnitude of the error, the maximum error between the true population and the sample proportion

Z = The confidence level in standard error units

4.7.1 Sample Size for the bankers

Total number of scheduled banks is 49 banks. Of them 4 are nationalized commercial banks, 28 local private commercial banks, 12 foreign banks and the rest 5 are development financial institutions (DFIs). But of them I will choose only two banks; one is Shahjalal Islami Bank Limited and another is Dhaka Bank Limited.

But the number of employees of these two banks in the whole Dhaka city is unknown. That’s why my sampling method for the bankers is-

Z2pq

n =

d2

Where,

n = Sample size

p = Estimated population proportion

q = 1-p, or estimated proportion of failures

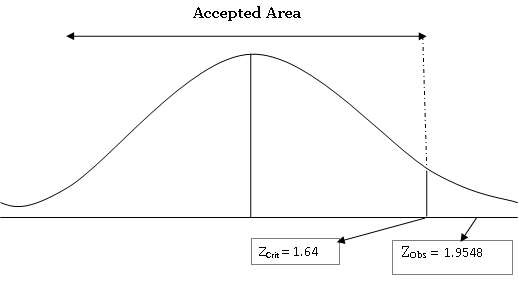

Z = The confidence level in standard error, at 90% confidence level it is 1.64

d =Precision level or magnitude of the error, the maximum error between the true population and the sample proportion; Here it is 10% = 0.10

So,

n= (1.64)2*0.5*0.5/ (0.10)2

= 67.24

= 68 (rounding the value)

In this case for my convenient (time & other limitations) I will take 50 bankers from the foreign exchange department of the five different branches of the two banks. That will ultimately support the judgmental sampling method. So, I will choose total bankers from the Dhaka Bank Ltd, & Shahjalal Islami Bank Ltd.

4.8 Data Gathering Instrument