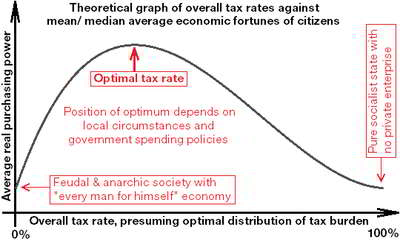

Optimal tax theory is the study of building and implementing a tax that reduces inefficiency and distortion on the market under given fiscal constraints. Generally, this criterion is made of individuals’ utility plus the optimization problem involves minimizing the distortions a result of taxation. Other items being equal, in case a tax-payer must make a choice from two mutually special economic projects which may have the same pre-tax risk and returns, usually the one with the lower tax or with a tax exemption could well be chosen by a rational actor.

Optimal Tax Theory