The operating expense ratio (OER) is a method of calculating the cost of operating a piece of property in relation to the income generated by that property. It’s computed by dividing a property’s total operating income by its operating costs (minus depreciation). OER is mainstream in the land business, and it is a typical proportion that is utilized while doing the land investigations. In land examination, the investigators judge the expense of working property with the pay created by the property.

An investor should be on the lookout for red signs, such as greater maintenance costs, operating revenue, or utility costs, that could prevent him from buying a certain property. The recommended OER percentage is between 60% and 80% (although the lower it is, the better). It is a useful tool for comparing the costs of comparable properties. On the off chance that a specific property piece includes a high OER, a financial backer should accept it as a notice sign and investigate the matter for what reason is the OER high.

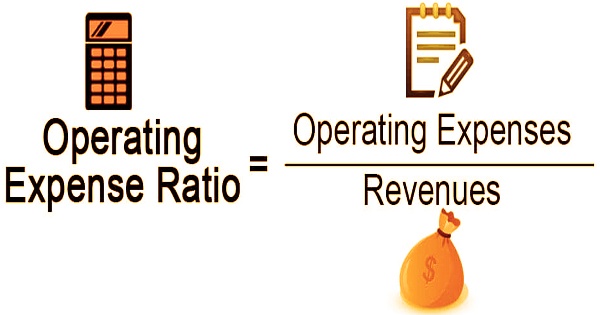

The operating expenses ratio formula is, simply, operating expenses divided by revenue:

Operating expense ratio (OER) = Operating Expenses / Revenues

Investors prefer a lower operating expense ratio (OER) since it indicates that expenses are kept to a minimum in relation to revenue. This ratio is more beneficial in the real estate industry, so let’s look at OER from that lens. There are two parts to this ratio:

- The most crucial component is the first. It’s a cost of doing business. Utilities, property management fees, upkeep, property taxes, insurance, and repairs are all examples of running expenses in the real estate market.

- The revenue is the second component. The income earned by a certain property is referred to as revenues.

The investors utilizing this proportion can additionally look to a detriment including protection, utilities, charges and support, to the gross pay, and the amount, all things considered, to the gross pay. Calculating OERs over various years may help a financial backer notification a property’s patterns in working costs. If a property’s costs increase at a faster rate than its income, the OER grows as well. As a result, the longer the investor holds the property, the more money they risk losing.

For instance, a company may have purchased a property to rent out to other smaller businesses. The corporation would look into OER to see how the property is doing.

- If the operating ratio is higher, the company would think twice about keeping the property.

- If the operating ratio is smaller, on the other hand, the corporation will view the property as a good investment.

Over the long run, changes in the OER demonstrate whether the organization can build deals without expanding working costs proportionately (i.e., if the business is adaptable). The principal things remembered for the working cost incorporate property the board, local charges, utilities, compensation, protection, expenses, supplies, fixes and support, promoting, bookkeeping charges, lawyer charges, bother control, junk expulsion, and comparative more. Instead of utilizing potential rental income to account for vacancies, investors should use effective rental revenue, which is potential rental income minus vacancy and credit losses.

Since overseeing opportunities are remembered for effective property the board, remembering opening for an OER gives a more precise image of working costs and shows where upgrades might be made. Property management fees, landscaping, attorney costs, landlord’s insurance, and basic property insurance are all additional operational expenses that investors should factor into the OER. Personal property, loan payments, and capital improvements, on the other hand, are not included in operational expenses.

In land, organizations can analyze properties by utilizing the proportion. The OER is likewise a proportion of administrative adaptability and skill that makes organizations simpler to look at. Furthermore, the OER can identify where prospective concerns, such as significant increases in power bills, may arise, allowing investors to tackle problems faster and maintain their profit margins. However, it’s worth noting that some industries have larger OERs than others.

Additionally, the operating expense ratio likewise addresses individual working costs things as a level of the successful gross pay and is additionally useful in recognizing expected issues. Comparing OERs between companies in the same industry is usually the most useful, and the distinction between “high” and “low” expenditures should be made in this context. In the real estate sector, the operating expense ratio formula is often utilized. However, that isn’t the only industry that use it. It’s also used in the service and manufacturing industries.

- The goal of using OER is to determine how much revenue a company has generated in relation to its operational expenses.

- Every business desires a lower OER. The OER is a measure of how well a firm is operating. The lower the OER, the better.

- If investors are considering a company as an investment, they must review the firm’s OER over a long period of time.

- If investors examine a company’s OER for a long time, they will notice a pattern in how the ratio between operating expenses and revenues is changing.

- After that, investors can compare that trend to the OER of other similar companies in the same industry.

- If the target firm’s OER is lower than that of other companies in the same industry, it may be the best firm to invest in. Before making a decision, investors should consider the company’s other financial ratios.

- OER assesses a company’s managers’ adaptability and competence; investors who grasp this will benefit greatly.

When considering a property investment, the OER should be utilized in conjunction with other factors such as the capitalization rate. Because depreciation can be calculated in a variety of ways, the OER can be manipulated by choosing a more advantageous form of depreciation accounting.

Information Sources: