Executive Summary

There can be various types of financial institution in an economy. Depository and non depository are the common divides. Among non-depositories, there are insurance companies, leasing companies, investment bank and companies and pension fund.

But our selected company IDLC is a special type of company. It is a multi product company with various wings. It provides various types of financial services. It has very enriched leasing operation along with strong merchant banking operation. Actually it is not a suddenly established so called finance company. It has strong commitment to meet the demand for loanable fund and strengthen the capital market of the country.

That’s why we feel that stating its background is very important. After a brief introduction we discuss about the background of the company. After a short discussion about its overall business activities we directly go to our main concern, leasing and merchant banking activities of IDLC. There we discuss about its various products, terms and condition, contribution of this activities to parents companies.

From our study we get some information that amused us. As a leading leasing company it is easy to predict that it will be very successful. But as a merchant bank it is playing a very important role in building our economy. This a very important time for our capital market when most of the countries in the world is in recession. Strong merchant banking companies like IDLC can help to overcome this situation.

- 1. Introduction

1.1 Background:

We have very keen interest on financial intermediaries and their activities. They are the channel between deficit and surplus business unit. Industrialization is the prerequisite for development and it always requires huge capital investment. No single business unit is able to meet the demand of all the organization. Only cumulative fund collected from all the people who has surplus can meet this huge demand. And financial intermediaries are performing this important duty of gathering this fund. Our present concern IDLC finance is one of these intermediaries. But its importance is more than others because it is simultaneously playing the role of various finance companies and thus contributing to the development of the country as a supplier of loanable fund and more importantly, as a market maker. That’s why we have decided to prepare this report on IDLC.

1.2 Origin of the reportThis term paper is a course requirement of “F-304: Financial Institution and Market”. Our honorable course instructor M. Kismatul Ahsan assigned us the topic and the report was conducted on IDLC finance Ltd. We are very glad to have his suggestion and guidelines in this regard. The report mainly focused on the leasing company’s functions, source of fund, investment and rules and regulation regarding leasing company. But as capital market is one of the highest concerns of today’s financial institutions, we also focus on the capital market activities of the firm.

1.3 Objectives of the report:

The main objectives of the report are given below:

To understand the financial institutions overall activities through the markets.

Gather some practical knowledge on different financial companies’ activities.

Thinking about the present course of action relate with the present condition.

Point out leasing activities performed by IDLC.

Capital market activities of IDLC.

1.4 Data source:

The main sources of data are as follows:

The data on lease finance and merchant banking and lessee compatibility were collected from the organizational visit to the IDLC’s corporate office.

The company information and other related information which are given on the repot were collected from the monthly business review and the annual report of the company.

1.5 Time period :

The time period covered in the study is for the period 2007 because of the unavailability of recent information.

1.6 Limitation :

The major limitations that the study faced were as follows:

Getting the internal data of the company for the recent period is difficult. Because most of the organizations don’t want to share those information with outsider.

The analysis required complete information about all kinds of product. But the necessary data on all products at the same period were not available.

Some of the necessary assumptions that were theoretically given were not at all consistent with the general practice.

As lack of knowledge and depth of understanding might have hindered our ability to produce an absolutely authentic and meaningful report.

This kind of study requires more time. So the constraint of time was a major limitation.

2. Company Background

IDLC finance ltd. started its journey in 1985, as the first ever leasing company of the country. IDLC was licensed as a financial institution by the country’s central bank, Bangladesh Bank, following the enhancement of the financial institution Act 1993. Over the last two decades, IDLC has grown in tandem with the country’s transition into a developing country and has emerged as Bangladesh’s leading multiproduct financial institution.

Become the best performing and most innovative financial

solutions provider in the country.

Create maximum possible value for all our stakeholders by

adhering to the highest ethical standards

For their Customers

Relentless pursuit of customer satisfaction through delivery of top quality services.

For their Shareholders

Maximize shareholders’ wealth through a sustained return on their investments.

For their Employees

Provide job satisfaction by making IDLC a centre of excellence with opportunity for career development.

For the Society

Contribute to the well being of the society, in general, by acting as a responsible corporate citizen.

Long term maximization of stakeholders’ value.

Corporate Philosophy

Discharge our functions with proper accountability for all our actions and results and bind us to the highest ethical standards.

Create synergy by combing high quality and strategically balanced portfolios.

Provide a range of financial products and services to our customers under one roof.

Strengthening our position in capital market operation.

Balanced diversification of funding sources.

Maximize corporate value through sustained high quality growth.

Strengthening corporate governance practices.

IDLC always places highest priority to the national interest. Utmost importance is always attached to country’s growth and prosperity.

IDLC employees are trained with the object of developing good leaders rather than good managers.

IDLC places emphasis on creativity and innovation to achieve organizational excellence.

IDLC believes in adherence to the highest ethical standards.

In accordance with approved and agreed Code of Conduct, IDLC employees shall:

Act with integrity, competence, dignity and in an ethical manner when dealing with customs, colleagues, agencies and public.

Act and encourage others to behave in a professional and ethical manner that will reflect positively on IDLC employees, their profession and on IDLC, at large.

Strive to maintain and improve the competence of all in the business.

Use reasonable care and exercise independent professional judgment.

Not restrain others from performing their professional obligations.

Maintain knowledge of and comply with all applicable laws, rules and regulations.

Disclose all conflicts of interest.

Deliver professional services in accordance with IDLC policies and relevant technical and professional standards.

Respect the confidentiality and privacy of customers, people and others with whom they do business.

Not engage in any professional conduct involving dishonesty, fraud, deceit or misrepresentation or commit any act that reflects adversely on their honesty, trustworthiness or professional competence.

IDLC employees have an obligation to know and understand not only the guidance contained in Code of Conduct, but also the spirit on which it is based.

| May 23, 1985 | Incorporation of the company |

| February 22, 1986 | Commencement of leasing company |

| May 18, 1986 | Signing of first leasing company |

| October 01, 1990 | Establishment of branch in Chittagong, the main port city |

| March 20, 1993 | Listed in Dhaka Stock Exchange |

| September 10, 1994 | Licensed by Bangladesh Bank for deposit taking |

| February 07, 1995 | Licensed as a Non Banking Financial Institution under the Financial Institution Act, 1993 |

| July 02, 1995 | Licensed by Bangladesh Bank as an off-shore financier in the Export Processing Zones |

| November 25, 1996 | Listed in the Chittagong Stock Exchange |

| May 27, 1997 | Commencement of Home Finance and Short term Finance operations |

| January 22, 1998 | Licensed as a Merchant Banker by the Securities and Exchange Commission |

| January 15, 1999 | Commencement of Corporate Finance and Merchant Banking operations |

| January 29, 2004 | Opening of the first retail focused branch at Dhanmondi |

| November 22, 2004 | Launching of Investment and Management Services “Cap Invest” |

| February 7, 2005 | Issuance of First Securities Zero Coupon Bonds by IDLC Securities Trust 2005 |

| February 27, 2005 | Signing of MOU for strategic alliance between IDLC and SBI Capital Markets Limited, India |

| September 18, 2005 | Launching of Local Enterprise Investment Centre, a centre established for the development of SMEs with the contribution of the Canadian International Development Agency of the Government of Canada |

| May 18, 2006 | Opening Merchant Banking branch in the port city Chittagong |

| July 1, 2006 | Relocation of Company’s Registered and Corporate Head Office at own premises at 57, Gulshan Avenue |

| September 18, 2006 | Commencement of operation of IDLC Securities Limited, a wholly owned subsidiary of IDLC |

| March 14, 2007 | Launching of Discretionary Portfolio Management Services “Management Cap Investment” |

| August 5, 2007 | Company name changed to IDLC Finance Limited from Industrial Development Leasing Company of Bangladesh Limited |

| December 3, 2007 | IDLC Securities Limited Chittagong Branch commenced operation |

| December 18, 2007 | IDLC Securities Limited DOHS Dhaka Branch opened |

FUNDS & INVESTMENTS

IDLC’s source of funds and investments include:

Long Term Sources of Funds:

Common equity investment

Preferred equity investment

Bonds

Short Term Sources of Funds:

Term deposit schemes

Debentures

Securitized bonds

Investment of Funds:

Lease finance

Term finance

Domestic factors of accounts receivable

Bill/invoice discounting

Work order finance

Corporate real estate finance

Real estate developer finance

Home loans with home loan shield

Home equity loans

Car loans for individuals

Business loan

Machinery loans

Double loan

Festival loan

Corporate Services:

Project finance appraisal

Project loan syndication

Working capital arrangement

Syndication agency services

Refinancing arrangement

Corporate financing advisory

Securitization of receivables

Trusteeship management

Professional supports to the SMEs

Merchant Banking and Portfolio management services:

Investor discretionary/Non- discretionary portfolio management services

IPO advisory

Issue management

Underwriting

Investment advisory

Placement of Equity, debenture and bonds

Custodial services

Internal Partnership/ affiliations:

As manager of the local enterprise investment center, with contribution of the Canadian international development agency of the govt. of the Canada, IDLC plays an active role in the development of the country’s private sector by providing financial and professional support to the small and medium enterprises, who wish to expand and improve their products and services. This is the first direct partnership by CIDA with a local private sector entity in a developing country.

Subsidiaries:

IDLC securities limited, a fully owned subsidiary of IDLC, offers full-fledged international standard brokerage service for retail and institutional clients, it has seats on both the Dhaka and Chittagong stock exchange. It is also a depository participant of depository of Bangladesh.

IDLC always concentrates on delivering high value to its stakeholders through appropriate trade off risk and return. A well structured and productive risk management system is in place within the company to address risks relating to credit, market, liquidity and operations. Risk grading is assigned at the inception of lending considering the industry, business, financial and management risk associated with the financing. The company has different committees for risk management and appropriate internal control measures are also place to mitigate risk.

Credit Risk:

Credit Risk is the possibility that a borrower or counter party will fail to meet agreed obligations. Thus managing credit risk for efficient management of financial institution has become the most crucial task. Given the fast changing, dynamic global economy and the increasing pressure of globalization, liberalization and consolidation it is essential that FIs have robust credit risk management policies and procedures that are sensitive and responsive to these changes. At IDLC, credit risk may arise in the following forms:

. Default Risk

. Exposure risk

. Recovery risk

. Counter party risk

. Related party risk

. Legal risk

. Political risk

To encounter and mitigate credit risk the following control measures are in place at IDLC:

. Multilayer approval process

. Policy for sector and group exposure limit

. Mandatory search for credit report from credit information bureau

. Looking into payment performance of customer before financing

. Annual review of clients

. Adequate insurance covariance for funded assets

. Vigorous monitoring and follow up by special assets management team

. Strong follows up of compliance of credit policies by operational risk management department

. Taking collateral

. Seeking external legal opinion

Market Risk:

Market risk refers to the fluctuation in a variety of markets such as interest rates, prices of securities where the values of assets and liabilities can change and there exists the risk of incoming losses.

The asset liability committee of the company regularly meets to assess the changes in interest rate, market conditions, carry out asset liability maturity gap analysis, re-pricing of products and thereby to monitor and control interest rate risk. To encounter market risk IDLC is negotiating for facilities that matches the maturity structure with ideal interest rate, maintaining a balanced diversification in investments and prudent provisioning policies. IDLC has also strong access to money market and credit lines at a competitive rate through good reputation, strong earnings, financial strength and credit rating.

Liquidity Risk:

Liquidity risk arises when a company is unable to meet the short term obligation to its lenders and stakeholders. This arises form the adverse mismatch of maturities of assets and liabilities.

Liquidity requirements are managed are managed on a day-to-day basis by the treasury division which is responsible for ensuring that sufficient funds are available to meet short term obligation, even in the crisis scenario and for maintaining a diversity of funding sources. The asset liability committee also oversees the asset liability maturity position and recommend and implement appropriate measures to encounter liquidity risk.

Operational Risk:

Operational risk is the potential loss arising form a breakdown in company’s systems and procedures, internal control, compliance requirements or corporate governance practices, which results in human error, fraud, failure, damage of reputations, delay to perform or compromise of the company’s interests by employees. Operational risk may arise from the following:

. Turnover of trained staff

. Risk of insider dealings

. Leakage of sensitive information

. Shortcomings of organizational structure

. Risk of falling in credit ratings

. Money laundering

. Changes in statutory requirements

. Technological obsolescence

In particular, the following risk management measures are present at IDLC to address operational risk:

. Effective internal audit function throughout the organization with direct access of chief internal auditor to the audit committee and board

. Suitable delegated authority level

. Awareness throughout the organization on “know your customer” policy

. Maintenance of assets through maintenance agreement with vendor

. Proper risk transfer measure by taking insurance coverage for all assets of the company

. Infusing organizational values and ethics in employees

. Strict compliance of employees’ code of conducts

. Creating conducive working environment for the staff

. Implementation of computer basis MIS system

Business Volume Risks:

At IDLC, business volume risk may arise in the form of risk of falling business volumes and market shares, risk of being overtaken and losing leadership position and risk of over trading which may affect profitability due to volatile revenues and reduced spread earnings, credit ratings and reputation. To encounter and mitigate this type of risk, IDLC takes the following measures:

. Innovative and convenient financial products and services

. Taking prompt action on customer complaints

. Frequent assessment of client’s satisfaction

. Regular review of performance against budget and target

. Review and analysis of competitors’ performance

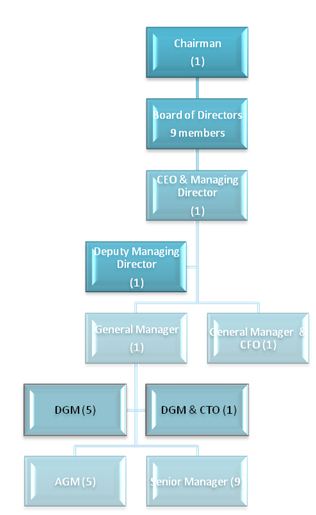

CORPORATE STRUCTURE

AWARDS AND RECOGNITION

Credit Rating:

IDLC has been assigned “AA2” (Double A Two) rating in the long term and ST-3 rating in the short term by Credit Rating Agency of Bangladesh Limited (CRAB). This has been done is consideration of IDLC’s strong ownership structure and corporate governance practices, experienced management team, improving income mix and strong retail deposit base.

Financial Institution rated in this category are considered strong, characterized by very good financials, healthy and sustainable franchise and a first rate operating environment.

ICAB National Award and SAFA Merit Award:

IDLC Finance Limited was awarded the second prize of the Institute of Chartered Accountants of Bangladesh (ICAB) National Award and South Asian Federation of Accountants (SAFA) Merit Award for the Best Published Annual Accountants and Reports for 2006 awarded by ICAB and SAFA, respectively.

These awards reflect practicing good corporate governance, compliance with the rules and regulations, preparation and presentation of financial statements and disclosure of information following International Accounting Standards and best practice set bye the ICAB and SAFA.

ICMAB Best Corporate Award for 2006:

IDLC Finance Limited received the first ICMAB National Best Corporate Award 2007 given by the Institute of Cost and Management Accountants of Bangladesh (ICMAB).

IDLC got the second prize in the financial institution category of the Best National Corporate Award 2007. the assessment criteria for the award include corporate governance practices, capital adequacy, liquidity, asset quality and profitability.

An institution is only as good as community it grows up in. IDLC’s policy is to constantly harness their social capital and opportunities for this to grow. IDLC believes that CSR does not mean just doling out largesse. Rather it means the strategic use of money and other resources to empower communities and to help people help them. They have made it a point to inculcate a deeper sense of responsibility and a stronger awareness among their staff on this issue. They have created a strong culture of corporate social responsibility at all levels and labored the point that IDLC has a significant role to play as a leading corporate citizen.

Branch network and increased SME focused operation, enabled them not only to reach remote areas and many more lives, but also provide the small entrepreneurs with lease of life which will also help in sustainable economic and social development.

With a view to contributing to poverty reduction and sustainable development in Bangladesh by supporting the development of SMEs, that are close to being ready to invest and/or export that will benefit the poor through the creation of better jobs, and ultimately sustainable livelihood, IDLC established Local Enterprise Investment Center (LEIC) in 2005. The LEIC is managed by IDLC and funded by Canadian International Development Agency (CIDA).

During the year, LEIC made initial contacts with four hundred local SMEs across a range of sectors and worked closely with fifty one new SMEs, as prospective clients, for the Center’s support. During 2007, LEIC undertook a process improvement initiative in some local software companies. LEIC also took a delegation of leading furniture companies of Bangladesh to Canada to explore long term partnership opportunities with Canadian furniture companies. A good number of seminars, workshops and focus group discussions were also organized on different topics jointly with trade bodies and Board of Investment. IDLC is expecting that through LEIC contribution, SMEs will be developed, new long-term business-to-business partnerships will be formed and good number of jobs will be created, which will help in community development, as a whole.

3. Business Activity

IDLC believe that proper and balanced diversification of products and services among different sectors is the only way to achieve their vision and ensure sustained and balanced growth. Keeping this in view, they have, in 2007, concentrated their investment in diversified products and services.

The company’s total investment portfolio as on Decembers 31, 2007 stood at Tk 12,144 million, which is 18% higher than previous year. Out of the total portfolio, lease, term loan, real estate finance and margin loan respectively represent 34%, 18%, 25%, and 11.4% of the total portfolio.

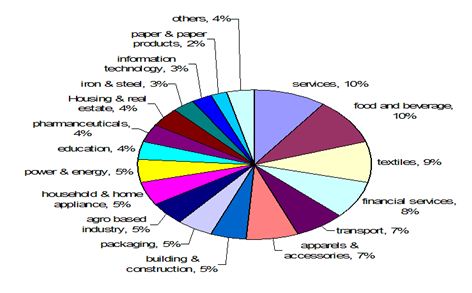

IDLC also maintains a well diversified investment portfolio in the major sectors with highest allocation to services sector at 10.29%, followed by food and beverages sector at 9.75%, textiles at 8.59%, financial services at 8.43%, transport at 7.18%, apparel and accessories at 6.88%, apparel and accessories at 6.88%, building and construction at 5.41%, packaging 5,25%, agro based industry 5.17% and so on. Their balanced diversification of investment portfolio helps them mitigate economic and sectoral risks.

OPERATIONAL PERFORMANCE OF IDLC DURING 2007

The company has completed its most successful year in 2007, despite an initial setback due to political uncertainty and overall economic slowdown. There was a marked increase in business confidence among customers during the year.

As a part of business expansion, during 2007, IDLC’s fully owned subsidiary, IDLC Securities Ltd, has opened branches in Chittagong and DOHS Mohakhali, in Dhaka, and they plan to open at least two more branches in 2008. the company’s diversified operations and subsidiaries saw a hefty growth during the year.

SMEs in Bangladesh have been making a significant contribution to the country’s economy.

However, there is large gap between their needs and access to reasonably priced funds. Under this backdrop, we have taken an initiative to increase investment in this segment, in structured manner, and created a focused and separate SME Division to cater to the financing needs to small and medium sized business enterprises. IDLC’s SME focused branch at Bogra has strengthened its financing activities in this growing sector in the northern region of the country.

IDLC’s consolidated operating result during 2007 is summarized below: (Tk in Million)

| 2006 | 2007 | Growth % | |

| Operating revenue | 1238 | 1764 | 42.5 |

| Operating expenses | 1013 | 1351 | 33.4 |

| Operating profit from merchant banking operation | 6.7 | 51.4 | 667.2 |

| Total operating profit | 231.6 | 464.9 | 100.7 |

| Profit before income tax | 236.1 | 474.5 | 101.0 |

| Net profit after income tax | 157.3 | 303.3 | 92.8 |

| Earnings per share | 78.63 | 151.66 | 92.9 |

| 2006 | 2007 | Growth % | |

| Operating revenue | 1238 | 1764 | 42.5 |

| Operating expenses | 1013 | 1351 | 33.4 |

| Operating profit from merchant banking operation | 6.7 | 51.4 | 667.2 |

| Total operating profit | 231.6 | 464.9 | 100.7 |

| Profit before income tax | 236.1 | 474.5 | 101.0 |

| Net profit after income tax | 157.3 | 303.3 | 92.8 |

| Earnings per share | 78.63 | 151.66 | 92.9 |

During the year under report, the Company has deposited Tk. 232 million to the Government Exchequer as corporate income tax, withholding tax and VAT

4. Company Services

IDLC starts as a leasing company. As leasing is its primary work, we discuss about its leasing activities. But now merchant banking is one of its prime concerns. That’s why among all activities of IDLC, we will discuss about its leasing and capital market activities

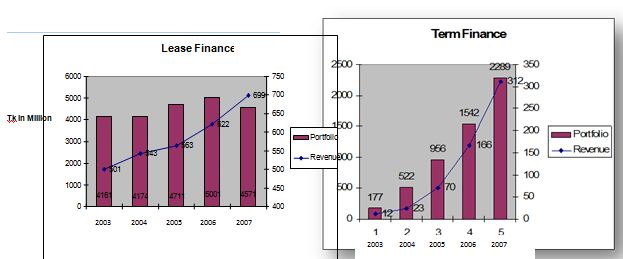

Amid intense and increasing competition amongst the financial institutions as well as the commercial banks, IDLC maintained its leadership position in the market. During 2007, the Company executed Tk 2977 million in leases and term loans, compared to previous year’s Tk. 2875 million. The lease and term loans portfolio at the end of the year saw a marginal growth of 4.08% over previous year. This year they have concentrated more on quality portfolio rather than volume achievement. With the creation of a separate SME Division, the financial institution expects to continue its drive to diversify its client base, maintain portfolio quality and improve service quality, which, they believe, will enable them to maintain a sustainable growth in this operation.

Lease Financing:

Rather than having capital tied in one purchase, leasing allows utilizing that capital elsewhere to general higher profits, it also reduces cash outflow. As appraisal and documentation processes are simple, prompt and convenient service would ensure quick implementation of the project. Since IDLC owns the equipment the leased equipment does not appear on lessee’s balance sheet, its financial ratios also improve. Raising new equity or debt for capital expenditure has many constraints which can be avoided when company opt for leasing. When organization’s budget does not allow it to buy equipment, leasing can make the acquisition possible. Since rental payments are decided in advance, budgeting becomes easier. Lease rentals are treated as revenue expenditure and are entirely deductible for tax purposes. This provides a greater tax benefit for you in comparison to borrowing.

Because of all this facilities organizations are very much interested in lease financing. This interest creates opportunities for IDLC. That’s why it has invested lots of money in lease financing and till now it proves to be profitable enough to continue.

Terms, conditions and rules regarding leasing

1. Anything that belongs to the category of equipment and machinery for any industrial plants, office automation, medical treatment diagnosis, transportation etc comes under the purview of equipment leasing.

2. Lessee has the liberty to decide equipment, supplier, terms and conditions including price. IDLC will buy the equipment of lessee’s choice.

3. Lease term means the non-cancelable period during which lessee can use the leased equipment exclusively. Generally it ranges from 3 to 5 years.

4. The actual purchase price and other incidental expenses including financial expenses and all bank charges shall constitute the acquisition cost and would be capitalized at the time of execution.

5. Lease rental is determined based on acquisition cost and lease term. Monthly lease rental is most common, however, quarterly or half yearly payment can also be considered.

6. Lease contract is based on the basis of negotiated terms and estimated acquisition cost.

7. The lease is executed on the basis of actual acquisition cost on delivery or installation of the equipment. At the time of execution the actual payment schedule is fixed and lessee is required to start paying the rental. Lessee is required to arrange the insurance coverage on the leased equipment for the entire lease term.

8. Lessee is required to maintain the leased equipment in good operating condition, though insurance shall cover most of the abnormal risks.

9. At the expiry of lease term, lessee may

Renew the lease on a year to year basis at a predetermined lower rental

Return the equipment to IDLC.

Purchase the equipment from IDLC at negotiated price.

Real Estate Finance:

Although the real estate and housing industry experienced a setback in 2007, with drastic fall in sales, IDLC’s housing finance operation witnessed a marginal growth of 4.0% in disbursements. However, revenue saw a hefty growth of 42.7%. the housing finance assets as at the close of the year stood at Tk 3065 million, 25.5% higher than the previous year. They believe that this operation will continue to grow with increasing retail customer base in years ahead.

Car Loans:

During the year under report, the Company disbursed Tk 177 million, a marginal 3.5% higher than the previous year’s disbursement of Tk 171 million. This operation has, however, earned revenue of Tk 44.3 million during the period, which is 79.3% higher than previous year. This operation is facing enormous competitions, with commercial banks offering lower rates and showing aggressive operation, in this market with strong marketing team and branch network. However they have mounted a strong campaign and are optimistic that this operation will disburse expected volumes and earn reasonable revenue in the future.

Now we have reached the most desired part of the report. In order to strengthen the capital market of Bangladesh the newest initiative of the government and the regulatory bodies has been to promote merchant banking because merchant banking can enhance the capability of capital market and strengthen it. IDLC Security Limited, a subsidiary of IDLC finance Limited, is one of the most important merchant bank of Bangladesh. We can understand the activities of IDLC Securities Limited as a merchant bank from the graph below.

IDLC obtained Merchant Banking license from Securities & Exchange Commission (SEC) in 1998, aiming to provide capital market related services to our valued customers.

The core strength of IDLC’s Merchant Banking Division may be derived from immensely utilizing the diverse experience and deep knowledge that IDLC has gathered through its financing and advisory activities during the last twenty (20) years. In other words, the accumulated experiences and knowledge have found a natural course to the division for its proper utilization and value addition. This is particularly true as the financing system is becoming more market oriented and the division is well poised to play significant role in the new economic setting.

The division is staffed with some of the most qualified and innovative personnel in the country. Moreover, the professionals at IDLC maintain the highest degree of financial and business ethics in all transactions with their customers.

The division, at present, encompasses two major businesses – Portfolio Management, and Issue Management and Underwriting – which serve both the demand and supply sides of the capital market.

IDLC provides comprehensive non discretionary portfolio management services including trades execution and margin loan under its investment account called ‘Cap Invest’. We are capable of executing proper and efficient trades through our strategically allied brokerage firms.

The division is also aiming to catapult discretionary portfolio management services for high net worth individuals and businesses.

For over twenty (20) years, we have leveraged all the resources of our firm to build productive and enduring partnerships with our corporate clients. Such a steadfast relationship is the central forte of the Issue Management Group of the division.

The Issue Management group is capable of devising innovative solution for raising capital – debt and equity – from the market suiting the unique needs and constraints of the corporate clients.

With a large equity base and sound financial health, IDLC is capable of underwriting big public equity offerings and debt issuances of deserving projects.

Major Services are:

Portfolio Management

Issue Management

Underwriting

Custodial Service

Management of Own Portfolio

During 2007, IDLC’s Merchant Banking Operation earned Tk 235 million revenue which is robust 342% higher than the previous year. The operation has earned an operation profit of Tk 51.4 million, compared to last year’s tk 6.7 million. They hope that this operation will earn increasing revenue in the years ahead and will take a stronger position in the market. At the end of December 2007, total portfolio value at cost was Tk 3320 million and balance of margin loan was tk 1387 million.

Moreover, Merchant banking Operation earned BDT 134 million in capital gains during 2007 through trading of securities in the secondary market.

DESIGNATED BROKERS OF IDLC

Equity Partners Securities Limited

LRK Securities Limited

Mona Financial Consultancy & Securities Limited

SCL Securities Limited

SES Company Limited

Lanka Bangla Securities Limited

HOW IT WORKS

Portfolio management service is a high demand product in current capital market. People like to invest with additional (margin) loan expecting higher return from the total portfolio. At the same time portfolio mangers are getting a very high interest rate on this loan (IDLC charge 14.5%). Thus this contributes a major portion of the total revenue of the company. In the last year (2006) IDLC earned around 34% of its total revenue only from merchant bank operations. During this time period it managed issue and underwritings of very few companies and the rest comes from portfolio management operation.

From the introduction of portfolio management service the revenue multiplied from merchant bank wing. Beginning three years its contribution was less than 1%. But for the last two years the revenue generation from this sector was excessively high. And major of them are coming from portfolio management service. For this reason, the IDLC expecting more returns from this sector in upcoming years.

IDLC has a significant contribution to asset financing to capital market in Bangladesh. In 1998, the Security Exchange commission (SEC) allowed it to carry out merchant banking. It started its operation as a merchant bank through Issue management, Issue underwriting, bridge financing and other related services since 2002. IDLC provides comprehensive non discretionary portfolio management services including trades execution and margin loan under its investment account called ‘Cap Invest’ since early of 2005. Until November 2007, its client’s number crossed 1,700 boundaries. Recently it has introduced its newest innovation of portfolio management – ‘Manage Cap’ a BDA type account service. This product is in its development stage with around 32 clients. So discussion on IDLC portfolio management limited here on Cap Invest.

CAPITAT INVEST

Cap Invest is a dynamic investment account that provides the investors with entire range of non discretionary portfolio management services, which include:

Efficient execution of trades through a panel of reputed brokers.

Extension of margin loan enabling the investors to earn enhanced return.

Registration of the securities, collecting dividend, and bonus shares.

Subscription of the rights issues.

Completion of dematerialization process.

Keeping the securities in safe custody.

1. MAJOR FEATURES OF “CAP INVEST”

Any adult citizen of Bangladesh, corporation, and statutory body can open the account with IDLC. Cap Invest clients shall have absolute discretionary power to make investment decisions. IDLC, the Portfolio Manager, shall provide all support for efficient execution of trades. All of the client’s securities will be purchased and kept under a common omnibus depository account. But investors can not have separate BO account for transaction in other securities or agencies.

Clients are allowed to invest only in the securities carefully selected and approved by the Portfolio Manager. Clients contain the absolute power to take their own investment decisions. However, their investments shall remain within the list of approved securities, which IDLC, the Portfolio Manager regularly update after thorough and independent analysis. The clients have access to the various research materials on market, industry and companies prepared by the independent research team of the Portfolio Manager.

To facilitate the clients to enhance their return on investments through leveraging, the Portfolio Manager extend margin loan to the clients. The margin loan is of revolving nature, i.e., all sorts of cash movements adjust the loan balance. To elaborate the point, whenever additional amounts are deposited, securities sold, and dividend received, the loan balance reduces. On the contrary, whenever securities are purchased or cash withdrawn, the loan balance increases.

Investment in “Cap Invest” is considered as allowable investment for obtaining tax rebate. Additionally, capital gains from investments are currently completely tax-exempt. However, all the securities purchased for the Clients are kept in lien in favor of the Portfolio Manager.

In order to protect clients’ equity position, portfolio manager calls additional margin deposit in case his/her equity falls below a certain percentage (the percentage changes from time to time) of the debt obligation to maintain the stipulated debt to equity ratio. Such call is commonly known as ‘Margin Call’.

Trigger is a right of the Portfolio Manager to execute sale of appropriate portion of client’s portfolio, in case investor fail to provide additional deposit as required under margin call, within three (3) business days or if client’s equity falls further below a certain percentage (the percentage changes from time to time) of investor’s total debt obligation. Trigger Sale is executed to reduce client’s debt burden.

Clients can make additional deposits at any time into their account. Additional deposits increase their equity position and purchasing power. Similarly they are allowed to withdraw cash to the extent at which, after such withdrawal, their equity remains at 100% of debt obligation. Also, the cash withdrawal shall not drive their equity position below the minimum investment amount.

Clients can place their order through physically submitting the order slip to the service desks, or through telephone, e-mail, or other electronic devices. Clients are able to place both market order and limit order. Moreover clients can cancel or modify their orders subject to non-execution of the said orders.

Clients can execute trades in both DSE and CSE, provided that their preferred broker is a member of both DSE and CSE. Thus investors can select their own preferred broker. They can also change their preferred broker by applying to the Portfolio Manager.

There is no stipulated investment period for Cap Invest. Investors are free to decide their own investment horizon and operate the account accordingly. However clients receive their portfolio status report quarterly. But if they wish, they can get the report any time on demand.

Here investors’ equity is calculated by deducting the debt amount from total portfolio value, and the purchasing power is derived at certain times of the equity. The magnitude of the multiplier changes depending on the capital market circumstance.

In this investment clients are not allowed to attend the AGM/EGM of the companies. However, the portfolio manager attends the AGM/EGM behalf of the clients and cast vote in the best interest of the clients.

II. OTHER FEATURES OF “CAP INVEST”

Your investment in Cap Invest is allowable for tax rebates

Capital gains from investments are currently tax exempt

Your Portfolio Manager will administer and value your investments and provide you with custodial services

Your investment in Cap Invest is allowable for tax rebates

Capital gains from investments are currently tax exempt

Your Portfolio Manager will administer and value your investments and provide you with custodial services

Minimum investment amount is Tk. 100,000/- (Taka One Hundred Thousand Only)

You will have the choice to invest in securities carefully selected by your Portfolio Manager

III. CAP INVESTMENT – ACCOUNT OPENING

Eligibility: Any adult citizen of Bangladesh, corporation, and statutory body

Minimum Investment: TK 200,000/-

Required Document:

Passport or Nationality Certificate or TIN

• 2 copies of photographs

• Nominee Information & Photograph

IV. CAP INVESTMENT – CHARACTERISTICS

Client can avail loan of 50% of the equity (1:0.5)

Margin Call – Client will be notified when equity drops below 50% of loan.

Trigger Sale – Executed once equity drops below 30% of loan.

No separate BO account is required.

Independent trade execution.

Client can trade through any designated broker.

Client Can place additional deposit any time

Client can withdraw only after keeping deposit above 100% of the loan.

Can trade both in CSE & DSE, if the client’s broker is member of both the bourses.

Client can do netting, if equity is 80% of the loan.

Portfolio manager will ensure

• Safety of the securities.

• Collection of cash/bonus dividends

• Subscription of right share.

A client cannot:

• Withdraw physical securities from account,

• Have separate BO account,

• Deposit or transfer securities from other BO account,

• Attend the AGM/EGM of the company and cast vote.

V. CAP INVEST – FEES AND CHARGES*

Documentation Fee: Tk. 500/- (one-off)

Management fee: 1.5%p.a on securities Value, charged quarterly

Interest on margin: 14.5%p.a, charged quarterly

Brokerage Fee: 0.35% on Transaction Value

Out of Pocket and Third Party Charges (Central Depository, SMS charges etc.): On actual basis *(Fees and charges are subject to change)

MANAGED CAP

I. MANAGED CAP – ACCOUNT OPENING

Designed for high net worth individuals and institutions.

Minimum Investment

• Individual: Tk 100,000

• Institutions: Tk. 1 million

Minimum Investment horizon: 1 Year

Margin loan: Nil

Documents to be attached

Individual Applicant

o Two copies of passport size photograph

o Photocopy of Passport/ Voter ID/ Driving License/ Nationality Certificate with attested photograph and utility bill

o Authorized person’s signature and photograph (if any)

o Photograph of nominees attested by the account holder

#Corporate Account

o Photograph(s) of the director

o Photocopy of Passport/ Voter ID/ Driving License/ Nationality Certificate with attested photograph and utility bill of the signatories

o Board resolution

o Memorandum & Article of Association certified by RJSC

o Signature and photograph of the authorized person (if any)

II. MANAGED CAP – CHARACTERISTICS

#Clients Investment perspective will be determined through Investment Policy Statement (IPS)

#Additional deposit is allowable.

#Stocks are purchased collectively and are allocated based on respective orders at average price.

#Client of the Managed cap invest account have to weather the risk of portfolio performance. However portfolio manager will implement diligent risk control measures.

III. MANAGED CAP INVESTMENT – FEES & CHARGES*

#Documentation Fee: Tk 500/-

#Management Fee: 2.50% p.a., on average market value of securities, quarterly charged.

#Brokerage Fee: 0.35% on transaction amount.

#Termination Fee (below 1 year):0.50% on total asset value at market price plus cash. *(Fees and charges are subject to change)

IV. WHO CAN INVEST IN MANAGED CAP INVESTMENT?

#Provided fund of large corporations.

#Insurance companies.

#High Salaried Employees in MNCs.

#Non resident Bangladeshis, in search of investment opportunities.

V. MANAGED CAP INVESTMENT – WHY IDLC?

#IDLC Finance has dedicated capital market research wing to classify stocks for investment based on:

o Industry Outlook of a Particular Stock

o Company Analysis and Future Prospect

o Historical Performance of the Company.

o Technical Analysis.

#IDLC provides customized investment solution based on Risk & Return objective of individual investor.

#Continued vigilant monitoring of the investment.

#IDLC places the interests of the clients before its own. It has adopted high standards of professional conduct to safeguard the interests of its clients.

#IDLC places utmost importance to compliance of securities laws while managing portfolios of its clients.

#So far our performance:

Number of Clients More than 30

Total Managed Cap Portfolio Size Tk. 20 Million

Average Return 55%

#IDLC has a team of highly dedicated and competent professionals to provide you with high quality investment management services.

#IDLC has gathered vast experience in most every sector of the economy during the past two decades. IDLC translates its invaluable experiences into various research materials for the benefit of its clients.

#Leaving the investment in the professional hand, investors can be free from the stress, occurring from rigorous investment selection and monitoring process.

5. Conclusion

Despite constantly increasing competition in the market with opening of leasing divisions by commercial banks, they will put in strenuous efforts to achieve the business volumes targeted by all the departments, as well as realize their corporate objectives. Innovative and relentless marketing drive will continue to attain quality asset growth, while marinating and improving existing portfolio quality.

IDLC has succeeded immensely in it diversification efforts resulting in growth in income steams from an array of business segments. Their focus in 2008, and in the near future, will be in further growing their SME business through expansion of branch network across the country and opening dedicated SME desk in all existing branches. They will also take extra efforts to offer loans to women entrepreneurs.

The Corporate Division has been affected somewhat by the change in depreciation policy by the Government. The Division is now concentrating in offering term loans to its customers. Plans are afoot to introduce operating lease as a new product to counter the loss ob business in the financial lease segment, their mainstay since inception of the company.

The Personal Finance Division will build on its successes, until date, which have been in mortgages, auto loans and deposit mobilization. Consumer loans have just been launched to offer IDLC customers one-stop services under one roof. They have plans to open a branch ach in Old Dhaka and Syllhet in 2008 to cater to the ever increasing needs of their personal segment customers.

IDLC’s Merchant Banking Division has performed very well in 2007. They will continue their efforts to increase the customer base, both in the individual and institutional segments. They will endeavor to encourage their customers to get themselves listed on the bourses, thereby bringing in quality scrip into our burgeoning capital market. As the financial institutions are facing immense competition, the Company will try to concentrate more on capital market operation and fee generation activity and diversify its mode of investment.

With all these expansion and diversification efforts, IDLC aims to be a truly specialized financial institution focusing on SME financing and investment banking operation, while marinating its business share in corporate financing.