The report is on the performance evaluation of the foreign exchange activities of Mutual Trust Bank. This is a necessity for the successful completion of the BBA program. The report has been made with the help of MTB officials and some third party sources that are being appropriately cited. At first, the report includes a short introduction of the organization. There is the introduction to the company along with its history. The products/ services, organizational organogram and the mission- vision of the company have also been reviewed.

INTRODUCTION

One of the largest businesses carried out by the commercial bank is foreign trading. Foreign trade can be easily defined as a business activity, which crosses national boundaries. These may be between parties or government ones. No country can produce all kinds of goods. From this sense; this is the origin of foreign trade. When two countries exchange goods or services between them we can call it foreign trade. The trade among various countries falls for close link between the parties dealing in trade. The situation calls for expertise in the field of foreign operations. The

bank, which provides such operation, is referred to as rending international banking operation.

Mainly transactions with overseas countries are respects of import; export and foreign remittance come under the preview of foreign exchange transactions. International trade demands a flow of goods from seller to buyer and of payment from buyer to seller. In this case the bank plays a vital role to bridge between the buyer and seller.

In the Mutual Trust Bank Limited, Gulshan Branch, there are three peoples are working continuously with great effort and teamwork. They are quite efficient and skilled at what they do. There are more than 70 clients and 25 countries they are dealing with. They believe in teamwork and extreme hard work.

OBJECTIVE TO THE PROJECT

The general objective of the study is to gather practical knowledge regarding banking system and operation. The practical orientation gives us a chance to relate the four year, long theoretical learning of BBA Program with the practical experience. This consists the following:

- To get an overall idea about the Foreign exchange Business procedure of Mutual Trust Bank Ltd (MTB).

- To describe the organizational structure, management, background, functions and objectives of the bank.

- To examine the profitability of the bank compare to the commercial bank.

- To know the performance of foreign exchange department of MTB

- To know about the Credit products and the way of disbursement.

IMPORTANCE:

The report is essential for the completion of the Bachelors of Business Administration. It emphasizes on the foreign exchange department of Mutual Trust Bank Limited, Gulshan Branch. The foreign exchange department is one of the major departments of MTBL. The report emphasizes on the activities of the foreign exchange department. The report also includes a performance analysis of the activities of the foreign exchange department. Therefore, the report holds its importance to get an overall idea about the foreign exchange department of Mutual Trust Bank.

METHODOLOGY OF THE STUDY

The report is prepared on the basic of foreign Exchange of Mutual Trust Bank. To conduct the overall study, at first I explored the sources of Primary and Secondary information and data. Different files of the department and statement prepared by Foreign exchange department (FED) helped me to prepare this report. To present financial performance of MTB, I used the Annual Report of 2012 of Mutual Trust Bank. For preparing this report I have used some graphical representation to find out different types of analytical and interpretation.

PRIMARY DATA

- Official records of Mutual Trust Bank (MTB).

- Face to face conversation with the client.

- Personal Interview – Face-to-face conversation and in depth interview with the respective officers of the branch.

- Personal observation – Observing the procedure of banking activities followed by each department.

- Practical work exposures on different areas of the branch

SECONDARY DATA

- Study on Annual Reports of Mutual Trust Bank Limited.

- Relevant file study as provided by the officers concerned.

- Other manual information.

- Online data from MTBL website.

- Various publications on the Bangladesh Bank.

OVERVIEW OF THE ORGANIZATION

Mutual Trust Bank Limited (MTBL) is a Public Limited Company by shares in the Bangladesh, with commendable operating performance. Directed by the mission to provide with prompt and efficient services to clients, MTBL provides a wide range of commercial banking services also. The bank has achieved success among its peer group within a short span of time with its professional and dedicated team of management having long experience, commendable knowledge and expertise in convention with modern banking. With all the resources, management of the bank firmly believes that the bank would be able to encounter problems that may arise both at micro and macro-economic levels.

The Company was incorporated on September 29, 1999 under the Companies Act 1994 as a public company limited by shares for carrying out all kinds of banking activities with Authorized Capital of Tk. 38,00,000,000 divided into 38,000,000 ordinary shares of Tk.100 each. The Company was also issued Certificate for Commencement of Business on the same day and was granted license on October 05, 1999 by Bangladesh Bank under the Banking Companies Act 1991 and started its banking operation on October 24, 1999. As envisaged in the Memorandum of Association and as licensed by Bangladesh Bank under the provisions of the Banking Companies Act 1991, the Company started its banking operation and entitled to carry out the following types of banking business:

(i) All types of commercial banking activities including Money Market operations.

(ii) Investment in Merchant Banking activities.

(iii) Investment in Company activities.

(iv) Financiers, Promoters, Capitalists etc.

(v) Financial Intermediary Services.

(vii) Any related Financial Services.

The Company (Bank) operates through its Head Office at Dhaka and 86 branches. The Bank carries out international business through a Global Network of Foreign Correspondent Banks. Registered Name of the Company is Mutual Trust Bank Limited

MTB PRODUCTS AND SERVICE

Retail Banking

- Deposit Products

- Loans Products

- MTB Cards Products

Wholesale Banking

- Term Finance

- Working Capital Finance

- Trade Finance

- Offshore Banking

- Syndication & Structured Fin

NRB Banking

- NRB Savings A/C

- NRB Deposit Pension Scheme (DPS)

- NRB Fixed Deposit (NRB FDR)

SME Banking

- MTB Bhaggobati

- MTB Krishi

- MTB Mousumi

- MTB Revolving Loan

- MTB Small Business Loan

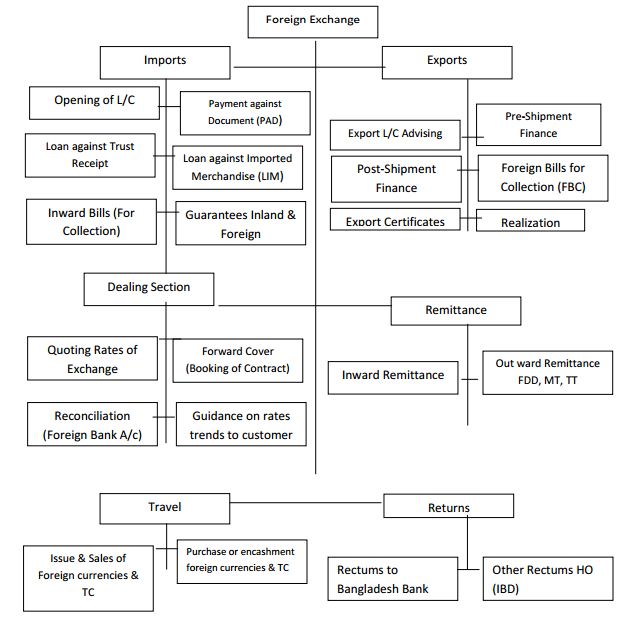

Activities of Foreign Exchange Department

FOREIGN EXCHANGE

Foreign Exchange Department is international department of a bank that deals globally. This department mainly deals in foreign currency. It facilitates international trade through its various modes of services. It bridges between importers and exporters. Some national and international laws regulate the functions of this department. Among these, Foreign Exchange Act 1947 is for dealing in foreign exchange business. Import and Export Control Act 1950, is for monitoring Documentary Credits. Governments Import & Export policy is another important factor for import and export operation for banks.

Narrow Meaning:

In the narrow sense, foreign exchange simply means the money of a foreign country. Thus, Bangladeshi TAKA is foreign exchange to an Indian and Indian rupees arc foreign exchange to a Bangladeshi. In practice, foreign exchange is often used to refer to a country’s actual stock of foreign currency.

Broader Meaning:

In the broader sense, the foreign exchange is related to the mechanism of foreign payments. It refers to the system whereby one currency is exchanged for or converted into another. Foreign exchange market is a market where foreign currencies are bought and sold by the traders to meet their obligations abroad. In accordance to the Encyclopedia Britannica, “Foreign exchange is the system by which commercial nations discharge their debts to each other.” In the words of Hartly Wethers, “Foreign exchange is the art and science of international monetary exchange.”

Foreign Exchange means the exchange of foreign currency between two countries. If we consider „Foreign Exchange as a subject, then it means all kind of transactions related to foreign currency. In other wards foreign exchange deals with foreign financial transactions. H.E. Evitt defined foreign exchange as the means and methods by which rights to wealth expressed in terms of the currency of one country are converted into rights to wealth in terms of the currency of another country.

REGULATORY REQUIREMENTS OF FOREIGN EXCHANGE

Any import and export of our country is regulated by different local and international laws and regulatory bodies. The core guidelines under the preview of which export and import of our country have to be performed are:

- Import policy

- Export policy

- Ministry of commerce circular

- Guidelines for foreign exchange transaction of Bangladesh Bank (Vol.1 &2)

- Circular issued by Bangladesh Bank

- Circular issued by National Board of Revenue (NBR)

- Circular issued by Chief Controller of Imports & Exports (CCI&E)

- Public note

Among the regulatory bodies, Chief Controller of Import and Export, Bangladesh Bank play major role in monitoring and ensuring compliance of various regulations.

WHY EXCHANGE IS TO BE CONTROLLED

Foreign Exchange is to be controlled for the following reason:

- To stabilize the rate of exchange

- To protect domestic Industries

- For proper implementation of plans

- To increases the bargaining strength

- To check over invoicing and under invoicing

- To check the black marketing and smuggling

- For regulating the international movements of good

DOCUMENTS USED IN FOREIGN EXCHANGE

LETTER OF CREDIT (L/C):

Letter of Credit L/C also known as Documentary Credit is a widely used term to make payment secure in domestic and international trade. The document is issued by a financial organization at the buyer request. Buyers also provide the necessary instructions in preparing the document. The International Chamber of Commerce (ICC) in the Uniform Custom and Practice for Documentary Credit (UCPDC) defines L/C as, “An arrangement, however named or described, whereby bank (the Issuing bank) acting at the request and on the instructions of a customer (the Applicant) or on its own behalf”. It is the most important and commonly used in connection with foreign trade. Letter of Credit is an undertaking by a banker of the importer to the exporter, to the effect that the amount of the L/C will be duly paid. The banker on behalf of the importer issues the L/C in favor of the exporter (beneficiary) and forwards the same to the exporter to the effect that the bill drawn by him shall be duly accepted and paid. It creates confidence in the mind of the exporter so far as payment of the bill is concerned. It is also facilitate the exporter to get the benefit of discounting the bill before the date lf maturity.

BILL OF EXCHANGE:

A Bill of Exchange is an instrument in writing, containing an unconditional order, signed by the maker, directing a certain person to pay on demand or on fixed or determinable future time a certain sum of money only to or to the order of a certain person or to the bearer of the instrument. From the definition – we get the features of bill of exchange. In general there are three parties likeDrawer:

- The person who prepares the bill.

- Drawee: The person who is ordered for the payment in future specified time.

- Payee: The person who deals with the bill receiver as per the order of the drawer to the drawee.

CERTIFICATE OF ORIGIN OF GOODS

A certificate of origin is a signed statement providing evidence of the origin of the goods.

COMMERCIAL INVOICE

A commercial invoice is the accounting document by which the seller charges the goods to the buyer. A commercial invoice normally including the following information:

- Date

- Name & address of buyer & seller.

- Order or contract number, quantity & description of the goods, unit price and the totalprice.

- Weight of the goods, number of packages and shipping marks & number.

- Terms of delivery & payment.

- Shipment details.

PROFORMA INVOICE OR INDENT

It is the seller‟s quotation or agreement between the seller and buyer. Here, the seller declares the rate, quantity, quality, manufacturing and other information about goods and the accepted by buyer.

PACKING LIST

Here the detailed descriptions of goods packed in cases are written. Such as total quantity in lot, per packet, total weight of the shipment etc. are written.

BASIC FORMS OF DOCUMENTARY LETTER OF CREDIT

The letter of credit can be either revocable or irrevocable. It needs to be clearly indicated whether the letter of credit Revocable or Irrevocable. When there is no indication then the letter of credit will be deemed to be a revocable L.C. The details are as follows:

Revocable letter of credit: A revocable letter of credit may be revoked or modified for any reason, at any time by the issuing bank without notification. It is rarely used in international trade and not considered satisfactory for the exporters but has an advantage over that of the importers and the issuing bank. There is no provision for confirming

revocable credits as per terms of UCPDC, hence they cannot be confirmed. It should be indicated in LC that the credit is revocable. If there is no such indication the credit will be deemed as irrevocable.

Irrevocable letter of credit: In this case it is not possible to revoke or amended a credit without the agreement of the issuing bank, the confirming bank, and the beneficiary. Form an exporter‟s point of view it is believed to be more beneficial. An irrevocable letter of credit from the issuing bank insures the beneficiary that if the required documents are presented and the terms and conditions are complied with, payment will be made.

Government letter of credit: That letter of credits, which are done by the Defense Ministry and other Ministries of the government.

Master or mother letter of credit: The L.C. which come from outside the country to the exporter from importer that is mother or master letter of credit.

Other classes of letter of credit:

Revolving letter of credit: A revolving documentary credit is one by which, under the terms and conditions thereof, the amount is renewed or reinstated without specific amendments to the documentary credit being required. The revolving documentary credit may revolve in relation to time or value. A documentary credit of this nature may be cumulative or non-cumulative. In shortly, we can say that when the L.C. is used again and again in same amount for a specific period of time that is called revolving letter of credit.

Back to Back letter of credit: Back to Back Letter of Credit is also termed as Countervailing Credit. A credit is known as back to back credit when a L/C is opened with security of another L/C. A back to back credit which can also be referred as credit and counter credit is actually a method of financing both sides of a transaction in which a

middleman buys goods from one customer and sells them to another. The practical use of this Credit is seen when L/C is opened by the ultimate buyer in favor of a particular beneficiary, who may not be the actual supplier/ manufacturer offering the main credit with near identical terms in favor as security and will be able to obtain reimbursement by presenting the documents received under back to back credit under the main L/C.

Clean or open letter of credit: The letter of credit, which provides assurance of payment bill of exchange without submission, of any export documents that is called clean letter of credit.

Confirmed letter of credit: A confirmation of a documentary credit by a bank (confirming bank) upon the authorization or request of the issuing bank constitutes a definite undertaking of the confirming bank, in addition to that of the issuing bank, provided that the stipulated documents are presented to the confirming bank or to any

other nominated bank on before the expiry date and the terms and conditions of the documentary credit are compiled with either to negotiate or to honor.

Deferred payment letter of credit: That letter of credit which expires one hundred and eighty days within this period the documents must be send to the negotiating bank.

IMPORT

The word “import” is derived from the word “port”, since goods are often shipped via boat to foreign countries. Countries are most likely to import goods that domestic industries cannot produce as efficiently or cheaply, but may also import raw materials or commodities that are not available within its borders. Mainly, imports are the goods and services that are bought by residents of a country, but made outside of the country. It doesn‟t matter what the goods or services are, or how they are sent. They can be shipped, sent by email, or even hand- carried in personal luggage on a plane. In economics, an import is any good or service brought into one country from another country in a legitimate fashion, typically for use in trade. It is a good that is brought in from another country for sale. An import in the receiving country is an export to the sending country.

IMPORTER:

The person who deals in import business obtaining Import Registration Certificate (IRC) in terms of importers, exporters and indenters from the CCI&E submitting the following papers is treated as importer-

- Valid Trade License

- National ID Card

- Asset Certificate

- VAT Registration Certificate

- Bank solvency Certificate

- Trade Association Certificate

- Certificate of Incorporation

- Memorandum and Articles of Association

STEPS FOR IMPORT L/C OPERATION – (6 STEPS OPERATION)

Step 1-Registration with CCI&E

- For engaging in international trade, every trader must be first registered with the Chief Controller of Import and Export.

- By paying specified registration fees to the CCI&E. the trader will get IRC/ERC (Import/Export Registration Certificate), to open L/C with bank, this IRC is a must.

Step 2-Determination terms of credit

The terms of the letter of credit are depending upon the contract between the importer and exporter. The terms of the credit specify the amount of credit, name and address of the beneficiary and opener, tenor of the bill of exchange, period and mode of shipment and of destination, nature of credit, expiry date, name and number of sets of shipping documents etc.

Step 3-Application by importer to the banker to open letter of credit

For opening L/C, the importer is required to fill up a prescribed application form provided by the banker along with the following documents

- Pro-forma invoice

- Demand Promissory Note

- Authority to debit account

- Tax Information Certificate

- Filled up amendment request from

- IMP form

- Insurance cover note, etc.

- Filled up LCA form

Step 4- Opening of L/C by the bank for the opener

- Taking filled up application form the importer

- Collects credit report of exporter from exporter‟s country through his foreign correspondence there.

- Opening bank then issues credit by air mail or cable followed by credit advice as asked for by the opener through his foreign correspondent or branch as the cash may be, at the place of beneficiary. The advising bank advises the credit to the beneficiary on his own form where it is addressed to him or merely hands on the original credit to the beneficiary if it is so addressed.

Step 5-Shiment of goods and submission of documents by exporter

Exporter ships the goods to the destination of the importer country and sends the documents to the L/C opening bank through his negotiating bank. Generally the following documents are sent to the Opening Banker with L/C:

- Bill of Exchange

- Bill of Lading

- Commercial Invoice

- Certification of Origin

- A certificate stating that each packet contains the description of goods over the packet.

- Packing List

- Advice Details of Shipment

- Pre-shipment Inspection Certificate

- Vessel Particular

Step 6- Lodgment of Documents by the opening Bank from the negotiating bank

After receiver the documents, the opening banker scrutinizes the documents. If any discrepancy found, it informs the importer. If the importer accepts the fault, then the opening banker will call the importer retiring the document. At this time many thing can happen. These are indicated in the following:

- Discrepancy found but the importer accepts- No problem occurs in lodgment.

- Discrepancy found and importer not agreed to accept- In this case, importer protest and send back all the documents to the exporter and request his to make in the specified manner. Here banker is not bound to pay because the documents send by exporter is not in accordance with the terms of L/C.

- Documents are OK but importer is willing to retire the documents-In this cash bank is obligated to pay the price of exported goods. Since importer did not pay bill of exchange, this payment bank is one kind of credit to the importer and this credit in banking is known as FORCED PAD.

EXPORT

A function of international trade whereby goods produced in one country is shipped to another country for future sale or trade. The sale of such goods adds to the producing nation’s gross output. If used for trade, exports are exchanged for other products or services. Exports are one of the oldest forms of economic transfer, and occur on a large scale between nations that have fewer restrictions on trade, such as tariffs or subsidies. Many companies are heavily dependent on exports for sales, any factors such as government policies or exchange rates that affect exports

can have significant impact on corporate profits.

DOCUMENTS USED IN EXPORT

When a firm sells its goods abroad, it must arrange for each export shipment to be accompanied by various documents. Depending on the country to which the goods are being sent, these documents will vary. But for exporting we can divide those documents in two types:

o Substantive Documents

o Auxiliary Documents

Substantive Document

Draft or bill of exchange:

Bill of Exchange is an instrument in writing containing an unconditional order or at a fixed determinable future time a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument.

Commercial Invoice:

Commercial Invoice is the export firm’s invoice, addressed to the foreign importer describing the goods shipped and the total price that it must pay. However, some countries require the commercial invoice to be prepared on their own forms. Such forms are called customs invoices.

Bill of lading or Airway Bill:

Bill of Lading is a document supplied to the exporter by the shipping company that is transporting the goods to their foreign destination, listing, item by item, the goods being shipped.

Auxiliary Documents

Auxiliary Documents are given below-

Cargo manifest or packing list:

When quantities, weights or contents of the various packing cases in an export shipment vary, it is usual to prepare a separate list for each case indicating its contents, weight and measurements. It also often includes the outside dimension of each case and the total cubic content and total weight of the shipment. They serve as useful supplements to the commercial invoice that accompanies the export shipment.

Certificate of Origin:

It is a document, which indicates the country in which the goods were produced, is required whenever preferential duties are claimed. Sometime, consular legalization of the document is necessary. Also, certification of the document by a Chamber of Commerce is required.

Quality control certificate:

While exporting products for which quality control certificate is obligatory, the exporter will have to submit, to the Customs Authorities, a quality control certificate issued by the appropriate authority.

Consular Invoice:

Some country required consular invoice. Countries that require a consular invoice also require a commercial invoice as additional proof of the details of the export shipment.

Certificate of free sale:

It required for pharmaceuticals and certain chemicals entering a number of countries.

Export Declaration Forms:

It is usually necessary for the exporter wishing to ship goods abroad, to fill out a form called an Export Declaration. This form required by the government whenever the value of the shipment exceeds a certain minimum amount or whenever a duty drawback is claimed; it is available at local customs offices. The document is also used for statistical purposes so that government authorities know exactly what has been exported from the country in each month and year and to which country. The information required include a description of the goods, their quantity, value and destination of the goods and whether the goods originated in the exporting country or are the goods of foreign origin being re-exported.

FOREIGN REMITTANCE OF MTBL

MEANING OF REMITTANCE

The word remittance originates from the word „remit‟ which means to transit money/fund. In banking terminology, the word- „remittance‟ means transfer of fund from one place to another and when money is transferred from one country to another then it is called Foreign Remittance. Mutual Trust Bank is an authorized dealer to deal in foreign exchange business. As an authorized dealer, a bank must provide some services to the client regarding foreign exchange and this branch provides these services through foreign remittance department. The basic function of this

department is outward and inward remittance of foreign exchange from one country to another country. In the process of providing this remittance service, it sells and buys foreign currency.

The conversion of currencies takes place at an agreed rate of exchange in which the banker quotes, one for buying and another for selling. In such transactions the foreign currencies are like any other commodities offered for sales and purchase.

REMITTANCE PROCEDURES OF FOREIGN CURRENCY

There are two types of remittance:

- Inward remittance

- Outward remittance

INWARD FOREIGN REMITTANCE

The remittance of freely convertible foreign currencies which Mutual Trust Bank Foreign Exchange branch is receiving from abroad against which the authorized dealers making payment in local currency to the beneficiaries may be termed as foreign inward remittance.

Foreign Exchange Performance Analysis

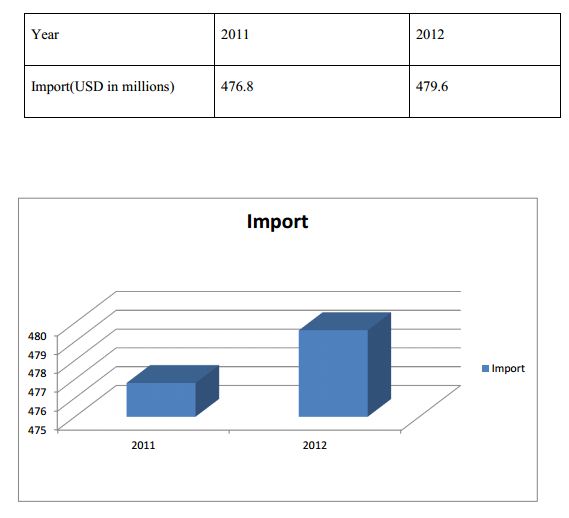

IMPORT

Import volume of MTB during the year 2012 was USD 479.6 million compared to USD 476.8 million in 2011, which showed a slight growth by 06%. The major import areas were raw materials, fabrics and accessories, chemicals, electronic goods and other consumer products, capital machinery, medical equipment and food grains (vegetable oil, rice, sugar etc.).

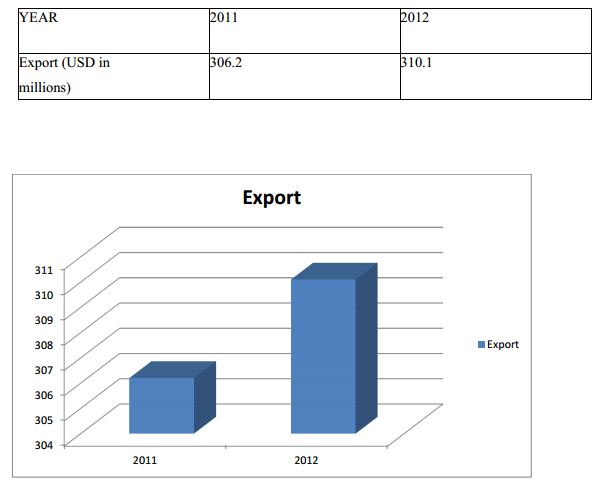

EXPORT

During 2012, total export volume of MTB stood at USD 310.1 million compared to USD 306.2 million in 2011. This reflects a slight increase in growth by 1.3%. The bank has given emphasis on export of traditional items like jute, jute goods, raw jute, leather and ready-made garments.

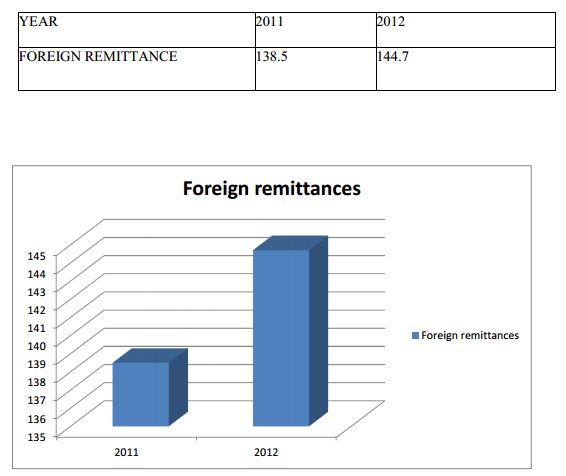

FOREIGN REMITTANCE:

In 2012 MTB procured inward foreign remittance USD 144.7 million equivalents to BDT 11.6 billion, 6.3% growth over 2011. Where, 2011 was inward foreign remittance USD 138.5 million. This growth was possible due to introduction of different instant payment products and technology including extending SWIFT, Online, EFT etc. and further efforts are being made for more speedy payments.

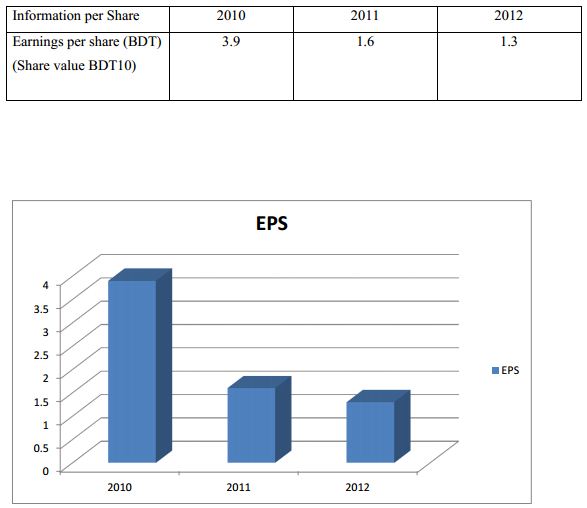

EARNINGS PER SHARE

In 20010 to 2011 the banks earning per share decreases dramatically 3.9 to 1.6. Again in 2012 EPS decreases 1.6 to 1.3 and it reflects that the growth decreases -18.8%. It‟s not a good sign for the bank and the shareholder.

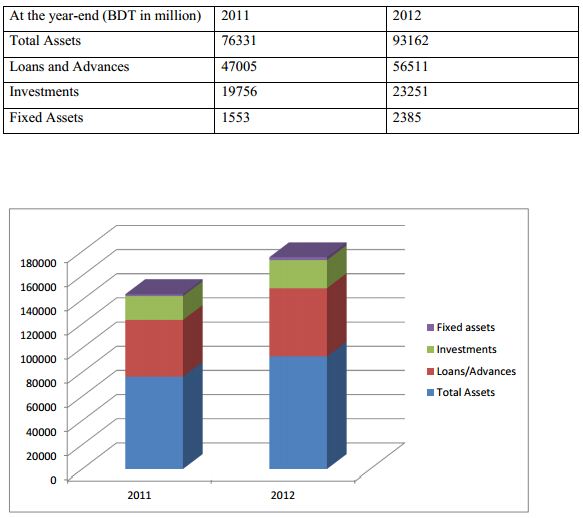

TOTAL ASSETS

The banks total assets posted a 22.0% increase in 2012, raising form BDT 76.3 billion to BDT 93.2 billion. The major contributor to this growth was the increase in Investments, which jumped by 18.0%, or from BDT 19.8 billion to BDT 23.3 billion and in loans and advances, which jumped by 20.2%, or from BDT 47.0 billion to BDT 56.6 billion. Fixed assets of the Bank also increased remarkably raised to BDT 2.4 billion from BDT 1.6 billion, an increase of 53.6%.

MAJOR FINDINGS

Banking sector being a vital sector of Bangladesh contributes a lot in the economy of the country. A Lot of new commercial bank has been established in the recent years and these banks have made the banking sector very competitive. So now, banks have to organize their operation and do their business according to the need of the market. Banking sectors no more depends on a traditional method of banking. In this competitive world, this sector has trenched its wings wide enough to cover any kind of financial services anywhere in this world. The major task for banks, to survive in this competitive environment is by managing its assets and liabilities in an efficient way. The Mutual Trust Bank is one of the leading banks in the private sector, and it gives a vast service to its customer. I observed the foreign exchange department, general banking area and also loans and advance department very carefully. With a keen attention and observation, the study has been tried to complete. The following are some extract of the major findings:

- MTB foreign exchange department is doing well and it shows the growth compare to previous year.

- Export, Import, Foreign Remittance growth rate increasing in 2011 compared to previous year.

- For the effectiveness of the foreign exchange department, MTB has divided the whole department into three major parts, which are Export, Import, and Remittance.

- The monitoring system of the foreign exchange department of MTB is excellent. The chain of command is strictly maintained here. The executives now and then visit the department, which keeps all the officers alert about their duty.

- MTB financial growth rate is not good in 2012 compare to 2011and 2010.

- MTB earning per share is decreasing and EPS is lower than average commercial Bank EPS.

- Some rules and regulations of government work as barrier for the free flow of remittance, export and import of profitable goods.

RECOMMENDATIONS

As per earnest observation some suggestions for the improvement of the situation are given below:

- To attract more clients MTB has to create a new marketing strategy, which will increase the total export import business.

- Attractive incentive packages for the exporter will help to increase the export and accordingly it will diminish the balance of payment gap of MTB.

- Long term training very much required for the foreign exchange officers.

- Bank can provide foreign market reports, which will enable the exporter to evaluate the demand for their products in foreign countries.

- New investment sector is booming rapidly. MTB should identified those untapped areas of business and invest in those sector such as Gas plant, condensed milk project, ship breaking etc.

- Effective Management Information System must be evolved by MTB so that correct decisions may be taken at correct time at policymaking level.

- Proper communication needs to establish with clients.

- Arrangement of monthly /quarterly training courses /workshops for the selected by the authority in order to promote employee to their desired level

- It is noted that “delay in service” is one of the problems faced by the clients. Attempts should be made to straighten the banking procedure.

CONCLUSION

This report is prepared to fulfill one of the requirements of BBA program to submit internship report under Business students. It is an effort to cover the foreign exchange activities in general which has been observed during the internship period in the Mutual Trust Bank Ltd. The activities of the foreign exchange department are much broader. Everything may not be covered here due to time constraint. However, the report includes enough information to get an overall idea about the foreign exchange department of Mutual Trust Bank.