Introduction:

Beximco Pharmaceuticals Ltd. Since its inception in 1979 has continued with its relentless strive to maintain leadership position in the Bangladesh Pharmaceutical Industry even in the new millennium. The healthcare welfare of the society remains to be their uncompromising objective. They provide the highest quality medicines at an affordable price to cater to the needs of the millions of people of the country. Regular introduction of innovative products in line with the needs of their customers have been the key to the company’s success over the years.

Ever since the start of our journey in late seventies they have successfully maintained the quality of their products throughout, thereby earning the trust and faith of the society. Ingenious approaches on manufacturing, R&d and marketing remain the strategic objective during 2010 and beyond.

Origin of The Study:

This report will be prepared as a part of the internship program which is an integral part of the BBA program under the Dept. of Accounting & Information Systems in the Faculty of Business Studies, University of Dhaka. The organization attachment was started on 18th July, 2010. This report on “Financial Performance Analysis of Beximco pharmaceuticals Ltd(BPL)” was assigned by academic supervisor Mohammad Moniruzzaman,ACA, Lecturer of Dept of Accounting & Information Systems, Faculty of Business Studies, University of Dhaka.

Purpose of The Study:

The purpose of the study is to make an analysis of Financial Performance of BPL in terms of Pharmaceuticals Industry. This study will attempt to understand the financial conditions of BPL on different segments such as liquidity, profitability & solvency. The purpose is also to make recommendations for improving the financial stability and soundness of different services provided to the shareholders of BPL. It is also the purpose of the researcher to help the management by providing an idea to take appropriate decisions about the quality of the investing & financing in future

Scope of the study:

The scope of this study was strictly confined to the annual report & personal contact with the employees of BPL. To collect the information I worked in the finance section & cost & budget section of BPL. All other data related to the financial analysis was collected from web sites of BPL & other related company

Methodology of the study:

For smooth and accurate study everyone have to follow some rules & regulation. The study impute were collected from two sources:

- Primary sources

- Practical desk work

- Face to face conversation with the officers

- Direct observations

- Face to face conversation with the client

- Secondary sources

- Annual report of BPL

- Files & Folders

- Daily diary (containing my activities of practical orientation in BPL) maintained by me

- Various publications on BPL

- Websites

Research Objectives:

- Broad objective

To assess and find out the financial conditions of the firm to analysis how much the company is capable of doing business properly in future.

- Specific objective

- To give a brief overview of Beximco Pharmaceuticals Limited.

- To analyze the trends of major income statement items.

- To determine the measure of financial performance.

- To give a clear picture about the financial performance of BPL in last four years.

- To give some idea about its management and organizational structure.

- To understand the limitation of the operation.

Contact methods:

To collect data for the report I use two types of contact method. I use personal or face to face contact method.

Limitations of the study:

- There were some restrictions to have access to the information confidential by concern authority.

- Time and cost constraints also other limitations regarding this analysis.

- Lack of experience of the researcher.

- Analysis was based mainly on financial statements.

PHARMACEUTICALS INDUSTRY IN BANGLADESH

BACKGROUND OF PHARMACETICALS INDUSTRY:

The pharmaceuticals sector is a high technology and knowledge-intensive industry in Bangladesh. The industry has two-tier structure. The largest firm accounts for the majority of the R&B investment in the industry and hold the majority of patents. There are a large number of smaller firms producing mostly for local markets. The pharmaceuticals industry is heavily regulated.

Once a products is brought to market, pharmaceuticals companies spend heavily on marketing and promotion. The larger drug companies maintain a large sales force, which makes direct regular contacts with individual prescribing physicians and other pharmaceuticals decisions makers. The money spent on marketing is huge. Pharmaceuticals marketing efforts are not only directed at physicians and consumer; drug companies have also sought to directly influence pharmacist to induce customer to change their drug consumption habits.

The nature of competition in this industry differs between the two sets of firms. The second tier of firms holds fewer patents and relies primarily on manufacturing off patent generic medicals medicines or patent medicines under lenience. Competition between these firms takes the conventional from of competition on price, cost efficiency and quality. It contrast, a few large research-based pharmaceutical companies invest heavily in R&D and hold the bulk of the patents, and can often enjoy substantial market power while these patents are in force. For these companies, competition is not primarily on the basis of price, but rather on the basis of marketing and innovation. Theses companies compete to develop entirely new drugs which treat new medical conditions, improve upon existing drugs, or serve as substitute for existing patented drugs. Some large pharmaceutical companies in these tiers export and compete in international markets.The scenario of pharmaceutical industry can be depicted in two parts-before the Drug policy ordinance, 1982 and after the drug policy ordinance, 1982. Before the ordinance there were 177 pharmaceutical companies in the country but local production is used to be dominated by multinational drug companies that manufactured 75% of total production. 25 medium sized national companies manufactured about 15% of total production. 133 small local based companies produced the remaining10%. The multinational companies where fully armed with modern technology for producing sophisticated essential drugs, but they were only engaged, a large extent, in formulation of simple drugs including many useless products. At that time, the unregulated drug market of the country had very little of favorable conditions for pharmaceuticals to over price their products. Near monopoly market conditions mean that local firms could not compete effectively with these multinational market tycoons.

A grate change was noticeable in the pharmaceutical industry after the drug policy ordinance of 1982. The total national production of pharmaceuticals has risen by a substantial 63%; the value of essential drugs made in national factories has gone up to 140% over the four years. At present there are 250 national based and 7 multinational based pharmaceutical companies in Bangladesh.

PROFILE OF BEXIMCO GROUP:

About Beximco-Group:

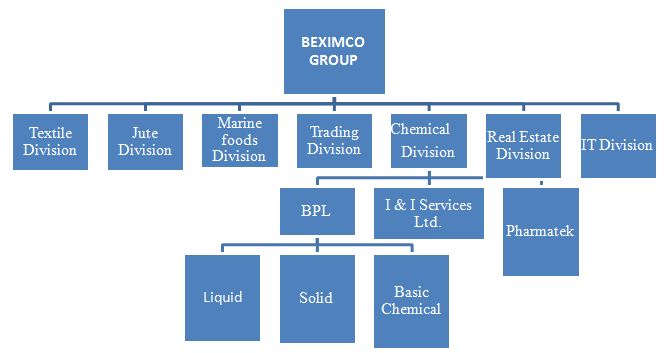

Beximco Groups of companies comprise of 8 divisions, which operates 34 companies. In the course of its growth, it has created industrial and management capabilities that will serve the country for generations to come.

Figure: Beximco Group

List of Major Companies including the Beximco Group:

| Division | Company |

| Textile Division | Padma Textile Mills Ltd. |

| Beximco Synthetics Ltd. | |

| Beximco Apparels Ltd. | |

| Beximco Knitting Ltd. | |

| Beximco Textiles Ltd. | |

| Beximco Denims Ltd. | |

| Beximco Fashions Ltd. | |

| Beximco Fabrics Ltd. | |

| Chemical Division | Beximco Pharmaceuticals Ltd. |

| Pharmatek Chemicals Ltd. | |

| I & I Services Ltd. | |

| Real Estate & Construction Division | Beximco Engineering Ltd. |

| Shinepukur Holdings Ltd. | |

| Trading Division | Bangladesh Export Import Ltd. |

| Beximco Holdings Ltd. | |

| Jute Division | New Dacca Industries Ltd. |

| Sonali Ansh Ltd. | |

| Esses Exporters Ltd. | |

| Marine foods Division | Beximco Foods Ltd. |

| Beximco Fisheries Ltd. | |

| Information Technology Divisions | Beximco Softech Ltd. |

| Beximco Systems Ltd. | |

| Beximco Computers Ltd. | |

| Bangladesh Online Ltd. | |

| Others | Shinepukur Ceramics |

| Gammatech Ltd. |

Table: Major companies of Beximco Group

The number of companies in each division is different. The companies of Beximco group in relation to division have been elaborated as follows:

Beximco Textile Division

From fiber to fabric, the BEXIMCO Textile is a truly integrated undertaking. The Textile Division has the capability to offer a complete product range for the export and domestic textile markets. The goal of the Textile Division is to become the preferred partner the for source of high quality fabrics and clothing from Bangladesh. With highly advanced technology and emphasis on developing local human resources, the Textile Division has the potential to make an important contribution to the nation’s growing ready made garments export sector.

Beximco Jute Division

The golden fiber provided the genesis of today’s BEXIMCO Group. As one of the staple exports of Bangladesh over the years, jute has been a mainstay of the country’s economic landscape. The BEXIMCO jute Division is the world’s largest jute yarn and twine manufacturer and exporter with 12% of the world jute and twine trade. Annual exports are currently over 20,000MT. BEXIMCO was the pioneer in manufacturing specialized jute yarn and twine for Ax Minister carpet and continues to explore new product and market opportunities worldwide. Until the jute business has got the setback in international market this division was one of the prime contributor to the group and the country as well. Beximco Real Estate & Construction Division:

The two critical needs of the country for the next decade and beyond are infrastructure and housing. The Real Estate and Construction Division aims to develop service and product offerings, which are second to none in its areas of core concentration.

BEXIMCO Engineering Ltd.(BEL)has been providing high quality civil engineering and consulting services to both the government and private sector for over a decade and was the largest sub-contractor on the historic 4.8 km. Long Jamuna Bridge. The firm is also involved in a number of road development and infrastructure projects.

Shinepukur Holding Ltd. Real Estate Division although real-estate developers have mushroomed in Dhaka and other urban areas over the years, Shinepukur Holdings Real Estate division was begun with mission to segment the real-estate market and develop demographically specific housing projects.

Marine Foods Division

Diversification into milk-fish production to supplement the traditional harvests of tiger prawn and sea bass has been a boon for Beximco Fisheries Ltd. With the pilot project in the coastal Cox’s Bazar area in full swing, the year has been better than the past years for the Marine Food Division. This group added significantly to the group through success in fisheries business. The turn over of the group was also boomed by the contribution of the export of marine foods to international market.

Beximco Trading Division

This division holds the initial business trend of Beximco, indeed. It looks for the opportunity of import-export commodities that have the in the market. This division is really dynamic and high profit contributing to the group with a brand portfolio that includes Wartsilla SA ( generation equipment), Arjo Wiggins ( security & treasury papers) of France, and Dupont Inc.( Chemicals), Sterling Diagnostic Imaging Inc.( film products) and Valvoline Inc.( petroleum products and industrial lubricants) of the USA. The Trading Division also represents overseas marine food buyers acting as a source of agent on their behalf and providing quality control.

Beximco IT Division

The companies included in this Division are Beximco Computers, Beximco Systems, and BOL online. Beximco Computers Ltd. is still the nation’s largest volume re-seller of IBM PCs. With the launch of a new version of BexiBank, an integrated multi-user, multitasking banking application system Beximco Computer Ltd.’s software is in use at over 300 branches of 15 major banks nationwide.

Beximco’s first foray into education, Beximco Systems Ltd. is joint venture collaboration with the largest information technology institute of India, NIIT. Molded after NIIT’s highly successful training centers across India, the NIIT Centers in Bangladesh have the highest growth rate of any NIIT facility for enrollment levels in its short courses and degree programs.

Bangladesh Online Ltd.(BOL), Beximco’s Internet Company launched its operation in August of 1998. The company has the fastest access among ISPs in Bangladesh. This division to serve groups interests in the most booming sectors of the world that is Information Technology. Since it started operation it proceeded very fast and became the market leader soon. It is pioneer company in Bangladesh to offer complete solution of automation. It also introduces the brand IT products to this country.

BEXIMCO PHARMACEUTICALS LTD.

Beximco pharmaceuticals Ltd: An overview

Beximco pharmaceuticals Ltd.(Beximco Pharma) belongs to Beximco Group, the largest private sector industrial conglomerate in Bangladesh which has diversified into textiles, apparels, pharmaceuticals, ceramics, aviation, real estate, ITC & media, and energy sectors. Most of these companies are actively being traded in the stock exchanges of Bangladesh with a total market capitalization of more than $1.65 billion. Incorporated in the late 70s. Beximco pharma begain as a distributor, importing products from global MNCs like Bayer, Germany and Ujohn ,USA and selling them in the local market, which were later manufactured and distributed under licensing arrangement. Since then, the journey continued, with a vision to go a long way and today, beximco pharma is one of the largest exporters of medicines in Bangladesh, winning National Export(Gold) Trophy for a record three times. Beximco Pharma’s manufacturing facilities have been accredited by major global regulatory bodies, and it has expanded its geographic footprint to 40 countries. The company has the unique distinction of being the only company in Bangladesh to get listed on AIM of London stock Exchange.

Beximco pharma produces pharmaceutical formulations and active pharmaceutical ingredients, having a current portfolio of more than 400 products and a dedicated team of more than 2500 employees. In its long journey over three decades, the simple principle on which it was founded remains the same: producing high-quality generics and providing better access to medicines at a much affordable cost. The company continues to adhere to the global standards and takes initiatives to remain more competitive in order to maintain its strong track record.

Beximco Pharmaceuticals Ltd (BPL) is a leading manufacturer of pharmaceutical formulations and Active Pharmaceutical Ingredients (APIs) in Bangladesh. The company is the largest exporter of pharmaceuticals in the country and its state-of-the-art manufacturing facilities are certified by global regulatory bodies of Australia, Gulf nations, Brazil, among others. The company is consistently building upon its portfolio and currently producing more than 400 products in different dosage forms covering broader therapeutic categories which include antibiotics, antihypertensives, antidiabetics, antireretrovirals, anti asthma inhalers etc, among many others. With decades of contract manufacturing experience with global MNCs, skilled manpower and proven formulation capabilities, the company has been building a visible and growing presence across the continents offering high quality generics at the most affordable cost.

Ensuring access to quality medicines is the powerful aspiration that motivates more than 3000 employees of the organization, and each of them is guided by the same moral and social responsibilities the company values most.

Beximco Group established a very significant milestone in the history of the country’s chemical industry. The plant not only met 90% of the country’s demand for two vital raw materials, ampicillin and amoxycillin but also started selling these to overseas markets. BPL received the Export Gold Trophy in 1994-95 for its exports of these two basic chemicals making it the first pharmaceutical company in Bangladesh to win the Export Trophy.

This division is involved with the following companies:

- Beximco Pharmaceuticals Ltd.

- I & I Services Ltd.

- Pharmatek Chemicals Ltd.

Beximco Pharmaceuticals Ltd.

Beximco Pharmaceuticals Limited was incorporated in Bangladesh as a public company with limited liability, on 17th March 1976 and commercial operation on 1st October 1980. The company went for public issue of shares in 1985, and its shares are listed in the stock exchanges in Bangladesh. And it is the leading pharmaceutical manufacture in Bangladesh. BPL started its operations in 1980 with product made under license of Bayer AG Germany; products made under license of Upjohn Inc. USA followed. Beximco Groups of as the name reveals not only produce drugs, they are also producing many other items like Textile, Holding, Marinated food etc. They are growing g15% (approx.) per year. Growth of any industry more than 10% is considered high growth industry all over the world. This rapid Growth rate is the second highest growth rate compared to the garment industries of our country. Principal Activities and Nature of operations; The company owns and operates a modern Pharmaceuticals drugs and medicines and sells them in the local and foreign markets.

While Pharmaceutical companies in many developed countries have lost their luster; the business is still highly attractive in Bangladesh. Beximco pharmaceuticals is an industry leader in Bangladesh Pharmaceutical Industry. Many of its products are brand leaders in their respective fields. The current status of BPL is that it is one of the largest producers of quality medicines both at home and abroad. It is engaged in manufacturing, marketing and export of pharmaceuticals finished products and raw materials. BPL products are sold more than 16 countries across 3 continents (Asia, Europe, Africa). The company continuously investing in the latest technology and manufacturing facility to meet the growing demand for its product and it is constantly expanding its already diversified product portfolio to better serve the community.

Pharmatek Chemicals Ltd

Pharmatek Chemicals Ltd. is the leading bulk producer of Paracetamol on Bangladesh. It caters to almost 60% of the local market and supplies its products to both national and multinational companies operating in Bangladesh. The company is managed and operated by BPL under a long-term management contract.

I & I Services Ltd.

I & I Services Ltd. is the distribution wing of the Chemical Division. It maintains a large distribution network and covers 20,000 customers nationwide every month. A highly sophisticated order processing system, logistic facilities in terms of vehicles, depots and a team of professional sales staff keep pace with the ever-increasing market demand for timely execution of orders and quality services.

Mission statement of BPL:

BPL has a remarkable mission statement, which is being seriously pursued in its thoughts and actions. An increasing amount of contribution is ploughed back into social causes BPL’s commitment, duties and responsibilities to the human society and nation.

When human society continuing to improve it should not be benefited to BPL itself, but it should positively contribute to the nation and society where we live. The BPL authority believes that they manufacture and sell medicine to provide health, happiness, and smile back in life of their fellow citizens. We intend to help realize the ultimate aspiration for lifetime of good health. It is BPL’s responsibility to ensuring a healthier tomorrow for the people which they believe as their responsibility.

Organization mission refers managements viewpoint towards is our business. A mission statement broadly outlines the organization’s future direction and serves as a guiding concept for what the organization is to do and to become.

“Each of our activities must benefit and add value to the common wealth of our society. We firmly believe that in the final analysis we are accountable to each of the constituents with whom we interact, namely our employees, our customers, our business associates, our fellow citizens and share holders.”

Vision Statemen of BPL :

Vision is the long-term outlook i.e. over the years, the company is growing from strength to strength, and consistently delivering on its promise of performance. In 2009 it achieved sales growth of more than 21% outperforming the industry growth an consolidated its position in the domestic market.

“We strongly believe our investments in expanding capacity and upgrading our facility will provide the necessary impetus for sustainable growth. Our major focus currently remains on development of international markets and now we are aggressively pressing ahead with our strategy which is crucial to the company’s future-particularly for building presence in developed markets.

We are confident that company’s sustained growth in the next few years will allow us to increase export turnover manifold ensuring our presence in the most regulated markets, and we are now well on course in terms of our product line, robust manufacturing and marketing platforms” (Annul report 2009)

Corporate Governance Structure Of BPL

Composition of the Board:

The management of BEXMCO PHARMA is simply exceptional in comparison to any other listed companies in this country. It has a blend of professionalism and wisdom, which plays a key role in managing the champion organization. The Board of Directors includes:

A S F Rahman Chairman

Salman F Rahman Vice Chairman

Nazmul Hassan Managing Director

Iqbal Ahmed Director

Mohammad Abul Qasem Director

Osman Kaiser Chowdhury Director

Abu Bakar Siddiqur Rahman Director

Dr. Farida Huq Director

Advocate Ahsanul Karim Director

Dr. Abdul Alim Khan Independent Director

A dedicated Management committee and Executive Committee make sure that BEXMCO PHARMA achieves its target with sheer professionalism. The committees are:

- Management Committee

- Executive Committee

- Company Secretary

The Management Committee

Nazmul Hassan Managing Director

Osman Kaiser Chowdhury Member of the Board of Directors

Ali Nawaz Chief Financial Officer

Afsar Uddin Ahmed Director, Commercial

Rabbur Reza Chief Operating Officer

Lutfur Rahman Director, Manufacturing

Zakaria Seraj Chowdhury Director, Sales

Mohd. Tahir Siddique Executive Director, Quality

A R M Zahidur Rahman Executive Director, Production

Jamal Ahmed Choudhury General Manager, Accounts & Finance.

The Executive Committee:

Osman Kaiser Chowdhury Member of the Board of Director

Nazmul Hassan Managing Director

Rabbur Reza Chief Operating Officer

Ali Nawaz Chief Financial Officer

Afsar Uddin Ahmed Director, Commercial

The Company Secretary:

Md. Asad Ullah, FCS

Company Profile of BPL

Company Profile: Beximco Pharmaceutical

Corporate Headquarter 17 Dhanmondi R/A , Road No. 2

Dhaka 1205 Bangladesh

Operational Headquarter 19 Dhanmondi R/A, Road No. 7 Dhaka 1205, Bangladesh

Factory 126 Kathaldia, Tongi, Gazipur

Year of Establishment 1976

Commercial Production 1980

Status Public Limited Company

Business Lines Manufacturing and marketing ofpharmaceutical finished products,large volume parenterals, Small volume parenterals, Ophthalmic preparations, Nebulizer Solutions and Active Pharmaceutical Ingredients (APIs)

Overseas Offices & Associates UK, USA, Pakistan, Myanmar, Singapore, Kenya, Yemen, Nepal, Czech Republic, Vietnam, Cambodia and Sri Lanka.

Export Markets Bhutan, Cambodia, Czech Republic, Vietnam, Cambodia, Czech, Republic, Germany, Hong

Kong, Iran, Iraq, Kenya, Malaysia,

Mozambique, Myanmar, Nepal, Pakistan, Philippines, Russia, Singapore, South Korea,

Sri Lanka, Thailand, Ukraine,

Vietnam, Yemen.

Authorized Capital(Taka) 9,100 million

Paid-up Capital(Taka) 1,511.49 million

Number of Shareholders Around 151,149,296

Stock Exchange Listings Dhaka Stock Exchange, Chittagong Stock

Exchange and AIM of London Stock

Exchange

Number of Employees 2,500

FINANCIAL STATEMENT ANALYSIS OF BPL FROM YEAR 2006-2009

Vertical Analysis

Horizontal Analysis

Ratio Analysis

Industry Analysisof Introduction:

Financial Statement Analysis must be made in order to understand the financial position of the Company’s. This is done with the help of the following criteria of statement. Different methods are followed to analyze the financial statement. The most widely used methods are

- Vertical analysis

- Horizontal analysis &

- Ratio Analysis.

These methods are discussed in the following pages

Vertical analysis:

vertical analysis sometimes is referred to as “common-size analysis” because all of the amounts for a given year are converted into percentages of a key financial statement component.

For example: on the income statement, total revenue is 100% and each item is calculated as a percentage of total revenue. On the balance sheet, total assets are 100% and each asset category is calculated as a percentage of total assets. In the balance sheet equation, total assets are equal to total liabilities plus equity; thus, each liability and/or equity account is also calculated to be a percentage of this total (i.e., total liabilities and equity are 100%). Vertical or common-size analysis allows one to see the composition of each of the financial statements and determine if significant changes have occurred. We will use the balance sheet information of BPL in the following pages to explain how one might prepare a four year vertical analysis.

Vertical Analysis helps to know the followings:

- Vertical analysis of a balance sheet will answer questions relating to asset, liability, and equity accounts, such as the following:

- Vertical analysis of an income statement helps answer questions such as the following:

- What percentage of total assets is classified as current assets? Current liabilities comprise what percentage of total liabilities and stockholders’ equity?

- Inventory makes up what percentage of total assets? Is this changing significantly over time? If so, is it increasing or decreasing? These answers could lead to additional questions such as the following: If it is increasing, could this indicate that the company is having trouble selling its inventory? If so, is this because of increased competition in the industry or perhaps obsolescence of this company’s inventory?

- Accounts receivable makes up what percentage of total assets? Is this changing significantly over time? If so, is it increasing or decreasing? (These answers might lead to additional questions such as the following: If it is increasing, could this indicate that the company is having trouble collecting its receivables? If it is decreasing, could this indicate that the company has tightened its credit policy? If so, is it possible that the company is losing sales that it might have made with a less strict credit policy?)

- What is the composition of the capital structure? In other words, total liabilities make up what percentage of total assets and total stockholders’ equity makes up what percentage of total assets?

- What percentage of revenues is cost of goods sold?

- What is the gross profit percentage?

- What is the mix of expenses (in terms of percentages) that the company has incurred in this period?

Beximco Pharmaceuticals Ltd.

Comparative Income Statements (Common-size Analysis)

For the year ended Dec: 31 2006- Dec: 31 2009

| Particulars | 2006 | percent | 2007 | percent | 2008 | percent | 2009 | percent |

| Net sales Revenue | 3,702,317,159 | 100% | 3,597,024,812 | 100% | 4,010,167,059 | 100% | 4,868,254,915 | 100% |

| Cost of goods sold | (1,971,231,333) | -53% | (1,967,509,975) | -55% | (2,002,871,181) | -50% | (2,566,206,626) | -53% |

| Gross Profit | 1,731,085,826 | 47% | 1,629,514,837 | 45% | 2,007,295,878 | 50% | 2,302,048,289 | 47% |

| Operating Expenses | (984,562,332) | -27% | (974,736,690) | -27% | (1,008,501,030) | -25% | (1,300,765,878) | -27% |

| Administrative Expenses | (150,285,977) | -4% | (145,544,701) | -4% | (153,464,243) | -4% | (215,192,547) | -4% |

| Selling, Marketing and Distribution Expenses | (864,276,355) | -23% | (829,191,989) | -23% | (855,036,787) | -21% | (1,085,573,331) | -22% |

| Profit from Operations | 746,523,494 | 20% | 654,778,147 | 18% | 998,794,848 | 25% | 1,001,282,411 | 21% |

| Other Income | 56,201,142 | 2% | 19,625,795 | 1% | 686,510 | 0% | 198,986,379 | 4% |

| Finance cost | (253,318,784) | -7% | (254,742,392) | -7% | (249,654,298) | -6% | (289,427,992) | 22% |

| Profit Before Contribution to WPPF | 549,405,852 | 15% | 419,661,550 | 12% | 749,827,060 | 19% | 910,840,798 | 19% |

| Contribution to Workers’ Profit participation /welfare Funds | (26,162,183) | -1% | (19,983,883) | -1% | (35,706,050) | -1% | (43,373,371) | -1% |

| Net Profit Before Tax | 523,243,669 | 14% | 399,677,667 | 11% | 714,121,010 | 18% | 867,467,427 | 18% |

| Income Tax Expense | (52,585,106) | -1% | (46,609,789) | -1% | (168,779,737) | -4% | (242,727,120) | -5% |

| Current Tax | (35,402,549) | -67% | (57,661,278) | -124% | (173,720,430) | -103% | (242,727,120) | -5% |

| Deferred Tax (Expense)/Income | (17,182,557) | -33% | 11,051,489 | 24% | 4,940,693 | 3% | ||

| Profit After Tax Transferred to Statement of changes in Equity | 470,658,563 | 13% | 353,067,878 | 10% | 545,341,273 | 14% | 624,740,307 | 13% |

Beximco Pharmaceuticals Ltd.

Comparative Balance sheet(Common-size Analysis)

For the year ended Dec: 31 2006- Dec: 31 2009

| ASSETS | 2006 | Percent | 2007 | Percent | 2008 | Percent | 2009 | percent |

| Non Current Assets | 8,555,119,221 | 71.40% | 9,029,643,482 | 75.54% | 11,957,773,787 | 80.69% | 12,975,195,529 | 65.23% |

| Property, Plant and Equipment-Carrying Value | 8,513,136,381 | 71.05% | 8,992,942,392 | 75.23% | 11,921,072,697 | 80.44% | 12,966,587,178 | 65.19% |

| Intangable Assets | – | – | – | – | – | – | 5,726,525 | 0.03% |

| Investment in Shares | 41,982,840 | 0.35% | 36,701,090 | 0.31% | 36,701,090 | 0.25% | 2,881,826 | 0.01% |

| Current Assets | 3,357,393,266 | 28.02% | 2,923,775,458 | 24.46% | 2,861,891,654 | 19.31% | 6,916,737,893 | 34.77% |

| Inventories | 1,754,440,288 | 14.64% | 1,652,480,291 | 13.82% | 1,505,288,093 | 10.16% | 1,722,953,284 | 8.66% |

| Spares & Supplies | 234,530,326 | 1.58% | 242,034,855 | 1.22% | ||||

| Accounts Receivable | 430,240,095 | 3.59% | 499,680,792 | 4.18% | 503,916,401 | 3.40% | 694,111,730 | 3.49% |

| Loans, Advances and Deposits | 591,613,938 | 4.94% | 685,915,465 | 5.74% | 544,509,106 | 3.67% | 699,204,450 | 3.52% |

| Short Term Investment | – | 2,500,000,000 | 12.57% | |||||

| Cash and cash Equivalents | 581,098,945 | 4.85% | 85,698,910 | 0.72% | 73,647,728 | 0.50% | 1,058,433,574 | 5.32% |

| TOTAL ASSETS | 11,982,512,487 | 100.00% | 11,953,418,940 | 100.00% | 14,819,665,441 | 100.00% | 19,891,933,422 | 100.00% |

| SHAREHOLDERS’ EQUITY AND LIABILITIES | ||||||||

| Shareholders’ equity | 7,949,920,425 | 66.74% | 8,250,939,647 | 69.03% | 10,450,202,145 | 70.52% | 10,885,706,614 | 54.72% |

| Issued share capital | 1,040,973,120 | 8.74% | 1,145,070,430 | 9.58% | 1,259,577,470 | 8.50% | 1,511,492,960 | 7.60% |

| Share Premium | 1,489,750,000 | 12.51% | 1,489,750,000 | 12.46% | 1,489,750,000 | 10.05% | 1,489,750,000 | 7.49% |

| Excess of Issur Price over face Value of GDRs | 1,689,636,958 | 14.18% | 1,689,636,958 | 14.14% | 1,689,636,958 | 11.40% | 1,689,636,958 | 8.49% |

| Capital Reserve on Merger | 294,950,950 | 2.48% | 294,950,950 | 2.47% | 294,950,950 | 1.99% | 294,950,950 | 1.48% |

| Tax Holiday Reserve | 394,834,828 | 3.31% | 442,354,953 | 3.70% | 0 | |||

| Revaluation Surplus | 442,354,953 | 3.70% | 1,711,174,747 | 11.55% | 1,617,361,714 | 8.13% | ||

| Reetained Earnings | 3,039,774,569 | 25.52% | 3,189,176,356 | 26.68% | 4,005,112,020 | 27.03% | 4,282,514,032 | 21.53% |

| Non-Current Liabilities | 1,435,171,264 | 12.05% | 2,074,506,357 | 17.35% | 1,767,431,029 | 11.93% | 6,684,775,166 | 33.61% |

| Long Term Borrowing-Net Off Current Maturity (Secured) | 1,159,409,947 | 9.73% | 1,776,449,778 | 14.86% | 1,446,600,500 | 9.76% | 1,924,933,065 | 9.68% |

| Fully Convertible,5% Dividend, Preference Share | 0.00% | 4,100,000,000 | 20.61% | |||||

| Liability for Gratuity & WPPF | 213,357,859 | 1.79% | 246,704,610 | 2.06% | 274,419,253 | 1.85% | 307,425,614 | 1.55% |

| Deferred Tax Liability | 62,403,458 | 0.52% | 513,514,969 | 4.30% | 46,411,276 | 0.31% | 352,416,487 | 1.77% |

| Current Liabilities and Provisions | 2,527,420,798 | 21.22% | 1,627,972,936 | 13.62% | 2,602,032,267 | 17.56% | 2,321,451,642 | 11.67% |

| Short Term Borrowings | 1,302,816,980 | 10.94% | 907,582,327 | 7.59% | 1,461,666,227 | 9.86% | 1,451,326,354 | 7.30% |

| Long Term Borrrowings-Current Maturity | 712,122,930 | 5.98% | 343,604,498 | 2.87% | 648,165,841 | 4.37% | 308,820,056 | 1.55% |

| Creditors and other payables | 365,255,938 | 3.07% | 271,814,118 | 2.27% | 263,176,822 | 1.78% | 409,898,122 | 2.06% |

| Accrued Expenses | 117,936,620 | 0.99% | 60,052,739 | 0.50% | 81,776,450 | 0.55% | 79,094,905 | 0.40% |

| Dividend Payables | 13,012,146 | 0.11% | 3,285,324 | 0.03% | 3,169,568 | 0.02% | 1,727,724 | 0.01% |

| Income Tax payable | 16,276,184 | 0.14% | 41,633,930 | 0.35% | 144,077,359 | 0.97% | 70,584,481 | 0.35% |

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | 11,912,512,487 | 100.00% | 11,953,418,940 | 100.00% | 14,819,665,441 | 100.00% | 19,891,933,422 | 100.00% |

Horizontal Analysis:

Horizontal analysis focuses on trends and changes in financial statement items over time. Along with the taka amounts presented in the financial statements, horizontal analysis can help a financial statement user to see relative changes over time and identify positive or perhaps troubling trends.

Beximco Pharmaceuticals Ltd

Comparative Income Statement(Horizontal Analysis)

For the year ended Dec: 31 2006- Dec: 31 2009

| Particulars | 2006 | percent | 2,007 | percent | 2008 | percent | 2009 | percent |

| Net sales Revenue | 3,702,317,159 | 100% | 3,597,024,812 | 97.2% | 4,010,167,059 | 108% | 4,868,254,915 | 131% |

| Cost of goods sold | (1,971,231,333) | 100% | (1,967,509,975) | 99.8% | (2,002,871,181) | 102% | (2,566,206,626) | 130% |

| Gross Profit | 1,731,085,826 | 100% | 1,629,514,837 | 94.1% | 2,007,295,878 | 116% | 2,302,048,289 | 133% |

| Operating Expenses | (984,562,332) | 100% | (974,736,690) | 99.0% | (1,008,501,030) | 102% | (1,300,765,878) | 132% |

| Administrative Expenses | (150,285,977) | 100% | (145,544,701) | 96.8% | (153,464,243) | 102% | (215,192,547) | 143% |

| Selling, Marketing and Distribution Expenses | (864,276,355) | 100% | (829,191,989) | 95.9% | (855,036,787) | 99% | (1,085,573,331) | 126% |

| Profit from Operations | 746,523,494 | 100% | 654,778,147 | 87.7% | 998,794,848 | 134% | 1,001,282,411 | 134% |

| Other Income | 56,201,142 | 100% | 19,625,795 | 34.9% | 686,510 | 1% | 198,986,379 | 354% |

| Finance cost | (253,318,784) | 100% | (254,742,392) | 100.6% | (249,654,298) | 99% | (289,427,992) | 114% |

| Profit Before Contribution to WPPF | 549,405,852 | 100% | 419,661,550 | 76.4% | 749,827,060 | 136% | 910,840,798 | 166% |

| Contribution to Workers’ Profit participation /welfare Funds | (26,162,183) | 100% | (19,983,883) | 76.4% | (35,706,050) | 136% | (43,373,371) | 166% |

| Net Profit Before Tax | 523,243,669 | 100% | 399,677,667 | 76.4% | 714,121,010 | 136% | 867,467,427 | 166% |

| Income Tax Expense | (52,585,106) | 100% | (46,609,789) | 88.6% | (168,779,737) | 321% | (242,727,120) | 462% |

| Current Tax | (35,402,549) | 100% | (57,661,278) | 162.9% | (173,720,430) | 491% | ||

| Deferred Tax (Expense)/Income | (17,182,557) | 100% | 11,051,489 | -64.3% | 4,940,693 | -29% | (242,727,120) | 686% |

| Profit After Tax Transferred to Statement of changes in Equity | 470,658,563 | 100% | 353,067,878 | 75.0% | 545,341,273 | 116% | 624,740,307 | 133% |

Beximco Pharmaceuticals Ltd.

Comparative Balance sheet(Horizontal Analysis)

For the year ended Dec: 31 2006- Dec: 31 2009

| ASSETS | 2006 | percent | 2007 | Percent | 2008 | Percent | 2009 | Percent |

| Non Current Assets | 8,555,119,221 | 100% | 9,029,643,482 | 106% | 11,957,773,787 | 140% | 12,975,195,529 | 152% |

| Property, Plant and Equipment-Carrying Value | 8,513,136,381 | 100% | 8,992,942,392 | 106% | 11,921,072,697 | 140% | 12,966,587,178 | 152% |

| Intangable Assets | 5,726,525 | 100% | ||||||

| Investment in Shares | 41,982,840 | 100% | 36,701,090 | 87% | 36,701,090 | 87% | 2,881,826 | 7% |

| Current Assets | 3,357,393,266 | 100% | 2,923,775,458 | 87% | 2,861,891,654 | 85% | 6,916,737,893 | 206% |

| Inventories | 1,754,440,288 | 100% | 1,652,480,291 | 94% | 1,505,288,093 | 86% | 1,722,953,284 | 98% |

| Spares & Supplies | 100% | 234,530,326 | 242,034,855 | |||||

| Accounts Receivable | 430,240,095 | 100% | 499,680,792 | 116% | 503,916,401 | 117% | 694,111,730 | 161% |

| Loans, Advances and Deposits | 591,613,938 | 100% | 685,915,465 | 116% | 544,509,106 | 92% | 699,204,450 | 118% |

| Short Term Investment | 100% | 2,500,000,000 | ||||||

| Cash and cash Equivalents | 581,098,945 | 100% | 85,698,910 | 15% | 73,647,728 | 13% | 1,058,433,574 | 182% |

| TOTAL ASSETS | 11,982,512,487 | 100% | 11,953,418,940 | 100% | 14,819,665,441 | 124% | 19,891,933,422 | 166% |

| SHAREHOLDERS’ EQUITY AND LIABILITIES | ||||||||

| Shareholders’ equity | 7,949,920,425 | 100% | 8,250,939,647 | 104% | 10,450,202,145 | 131% | 10,885,706,614 | 137% |

| Issued share capital | 1,040,973,120 | 100% | 1,145,070,430 | 110% | 1,259,577,470 | 121% | 1,511,492,960 | 145% |

| Share Premium | 1,489,750,000 | 100% | 1,489,750,000 | 100% | 1,489,750,000 | 100% | 1,489,750,000 | 100% |

| Excess of Issue Price over face Value of GDRs | 1,689,636,958 | 100% | 1,689,636,958 | 100% | 1,689,636,958 | 100% | 1,689,636,958 | 100% |

| Capital Reserve on Merger | 294,950,950 | 100% | 294,950,950 | 100% | 294,950,950 | 100% | 294,950,950 | 100% |

| Tax Holiday Reserve | 394,834,828 | 100% | 442,354,953 | 112% | ||||

| Revaluation Surplus | 100% | 442,354,953 | 100% | 1,711,174,747 | 100% | 1,617,361,714 | ||

| Retained Earnings | 3,039,774,569 | 100% | 3,189,176,356 | 105% | 4,005,112,020 | 132% | 4,282,514,032 | 141% |

| Non-Current Liabilities | 1,435,171,264 | 100% | 2,074,506,357 | 145% | 1,767,431,029 | 123% | 6,684,775,166 | 466% |

| Long Term Borrowing-Net Off Current Maturity (Secured) | 1,159,409,947 | 100% | 1,776,449,778 | 153% | 1,446,600,500 | 125% | 1,924,933,065 | 166% |

| Fully Convertible,5% Dividend, Preference Share | 100% | 4,100,000,000 | 100% | |||||

| Liability for Gratuity & WPPF | 213,357,859 | 100% | 246,704,610 | 116% | 274,419,253 | 129% | 307,425,614 | 144% |

| Deferred Tax Liability | 62,403,458 | 100% | 513,514,969 | 823% | 46,411,276 | 74% | 352,416,487 | 565% |

| Current Liabilities and Provisions | 2,527,420,798 | 100% | 1,627,972,936 | 64% | 2,602,032,267 | 103% | 2,321,451,642 | 92% |

| Short Term Borrowings | 1,302,816,980 | 100% | 907,582,327 | 70% | 1,461,666,227 | 112% | 1,451,326,354 | 111% |

| Long Term Borrowings- Current Maturity | 712,122,930 | 100% | 343,604,498 | 48% | 648,165,841 | 91% | 308,820,056 | 43% |

| Creditors and other payables | 365,255,938 | 100% | 271,814,118 | 74% | 263,176,822 | 72% | 409,898,122 | 112% |

| Accrued Expenses | 117,936,620 | 100% | 60,052,739 | 51% | 81,776,450 | 69% | 79,094,905 | 67% |

| Dividend Payables | 13,012,146 | 100% | 3,285,324 | 25% | 3,169,568 | 24% | 1,727,724 | 13% |

| Income Tax payable | 16,276,184 | 100% | 41,633,930 | 256% | 144,077,359 | 885% | 70,584,481 | 434% |

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | 11,912,512,487 | 100% | 11,953,418,940 | 100% | 14,819,665,441 | 124% | 19,891,933,422 | 167% |

Ratio Analysis:

Ratio means one number expressed in terms of another. Ratio analysis is the process of determining and interpreting numerical relationships based on financial statements. A ratio is a statistical yardstick that provides a measure of the relationship between variable and figures. This relationship can be expressed as percent or as a time. Ratio analysis is based on the notion that the analysis of absolute figures may not be the best means available of assessing on organizations performance and prospects.

Ratio analysis is used by all business and industrial concerns in their financial analysis. Ratios are considered to be the best efficient execution of managerial function like planning, forecasting, control etc.

Different ratios are used in Statement analysis:

The different ratios, which used in the study of analysis of financial performance of Beximco pharmaceutical limited. These are given in the following:

- Liquidity Ratio

- Activity Ratio

- Leverage Ratio

- Profitability Ratio

- Cash to Debt Ratio

Liquidity Ratio

1.Current Ratio:

Current assets are received as relatively liquid which means they can generate cash in a relatively short time period. Current liabilities are debts that will come due within a year. Of the current ratio is low, the firm may have difficulty in meeting short run commitment as they mature. If the ratio is too high, the firm may have an excessive investment in current assets or to be under utilizing short term credit. The standard term is 2.1 desired but there are deviations.

Current Ratio= Current assets / Current Liabilities

| Current Ratio of BPL |

(Figure in thousand)

Particulars

Years

2006200720082009Current Assets335739329237752,861,8916,916,737Current Liabilities252742016279722,602,0322,321,451 Source: Annual Report of BPL from 2006-2009

| Current Ratio | 1.33 | 1.80 | 1.10 | 2.98 |

From the above calculation we can see that the current ratios of BPL from the years 2006-2008 are moderate, through these ratios gradually decrease in year by year but 2007 are moderately increased. It means it can meet its short-term obligations but the company may fall in problem if their short term liabilities to be paid quickly. In 2009 current ratio increased it means that it can meet its short term liabilities promptly

2. Quick Ratio:

Quick ratio measures the firm’s ability to meet short-term obligations from its most liquid assets in this case, inventory is not included because, it is generally for less liquid than other current assets.

From the above calculation we can see that the quick ratio of BPL is one-year increase and one year decreases from 2006-2008 gradually and in 2009 quick ratio highly increased. It implies that it can meet its short-term liabilities by its own assets and it is least liquid assets. So BPL quick ratio is satisfactory and desirable.

3. Cash flow from operation ratio:

It measures liquidity by comparing actual cash flows (instead of current and potential cash resources) with current liabilities. This ratio avoids the issues of actual convertibility to cash, turnover and the need for minimum levels of working capital (cash) to maintain operation.

The ratio of 2007 & 2009 was low from other years, but in 2006 & 2008 it goes very high . The high CFO ratio is good because it indicates the company’s capacity to meet short-term obligations by comparing actual cash flow with current liabilities. So, the cash flow from operation ratio is not so good.

4. Net Working Capital Ratio:

It is a summary ratio that reflects the amount of working (operating) capital needed to maintain a given level of net assets. It is the relationship between net working capital and net assets. It measures the firm’s potential reservoir fund.

Net Working Capital Ratio = Net Working Capital / Net Assets

Note: Net working capital (NWC) = Current Assets – Current Liabilities.

Leverage Ratio

5. Debt to Total Asset Ratio

The debt ratio measures the position of total assets financed by the firm’s creditors. The higher the ratio, the greater the amount of other people’s money being used to generate profits. A high ratio shows a large share of financing by the creditors, relatively to the owners, who have large claim against the assets of the firm, a lower ratio implies a smaller claim of the creditor’s standard ratio is 60:40.

This ratio moderately lower 2006-2009 but 2008 are very low. So the BPL credit proportion is some lower relatively the owners through it is decrease year by year. The BPL performance of Debt to Total Assets ratio is very good because the higher Debt to Total Assets Ratio implies the greater risk that the company may be unable to meet its maturing obligation.

6. Debt to Equity Ratio:

A higher debt equity ratio implies that high proportion of long-term financial is from debt sources. Long-term creditors generally prefer to see a modest debt equity ratio means greater protection and a greater stake in the company’s future.

Debt to Equity Ratio = Long-Term Debt / Shareholders Equity

Here we can see, the debt to equity ratio of BPL down or flat year by year. The overall performance is good. BPL have greater protection and stake so they can increase its long-term borrowing.

7. Time Interest Earned Ratio:

The time interest earned ratio sometimes called interest coverage ratio. It reflects the firm’s ability to pay interest out of earning.

Activity Ratio

8. Inventory Turnover:

A low inventory turnover implies a large investment in inventories relative to the amount needed to services sales. The high inventories turnover shows that inventories are too small and it may be that the firm is constantly running short of inventory, thereby losing customers.

From the above calculation we can say that the Inventory Turnover Ratio of BPL is decrease gradually from 2006-2009 which is better for the firm. Because it does mean they prefer to storage their products for appropriate or limit times. So the activity or liquidity of BPL is satisfactory. And inventory turnover of BPL has the large investment in inventories relative to the amount needed to service sales.

9. Average Collection Period:

The average Collection Period indicates the firm’s efficiency, in the collecting on its sales. It may also reflect the firm’s credit. If customer take more time to pay, then the collection period will generally be greater. A long collection period is not necessarily bad, since a stringent credit policy regarding customers its pay faster may load to a reduction on sales.

Average Collection Period = Accounts receivable / Average Credit Sales per Day

| Average Collection Period Ratio | 41.84 | 50.01 | 44.90 | 51.33 |

The average collection period should lower which will better. From the above calculation we can see that the average collection period of BPL decreases 2006-2009 year. BPL credit sales collection period is not so bad. So it means BPL their credit should be collected. It shows the good firm efficiency.

10. Fixed Assets Turnover:

The ratio indicates how intensively the fixed assets of the firms are being used. An inadequately ratio implies excessive investment plant and equipment relative to all value at the output being produced.

Fixed Assets Turnover = Sales / Fixed Assets

| Fixed Assets Turnover Ratio | 0.43 | 0.40 | 0.34 | 0.38 |

From the above calculation we can see that Fixed Assets Turnover ratio has decreased 2006-2008 gradually and moderately increased in 2009. It shows the firms efficiency where its assets have used. The maximum fixed assets turnover ratio is good for the company. So, the BPL fixed assets turnover ratio is not so bad.

11. Total Assets Turnover:

Total Assets Turnover reflects how well the company’s assets are being used to generate sales. The high total assets turnover is good for the company running and low reflects bad impact.

Total Assets Turnover = Sales / Total Assets

| Total Assets Turnover Ratio | 0.31 | 0.30 | 0.27 | 0.24 |

We can see that the total assets turnover decreased gradually from year 2006-2009. It is not so bad for BPL. It means the more efficiently its assets have been used which measure probably the greatest interest to the management.

12. Receivable Turnover:

The receivable turnover ratio measures the effectiveness of the firm’s credit policies. It also indicates the level of investment in receivable needed to maintain the firm’s sales level.

Receivable Turnover: Sales

Average trade receivable

Note : Average trade receivable = TR of during year + TR of previous year

Turnover Ratio :

Receivable turnover should be computed using only trade receivable in the numerator in order to evaluate operating performance. In case of BPL, we can see that the increasing level of receivable turnover. It is not good for companies because they do not prefer to sell their productions in cash. And for this reason the average trade receivable of BPL is high.

13. Payable Turnover:

Although accounts payable are liabilities rather than assets, their trend is significant as they represent an important source of financing for operating activities. The time spread between when suppliers must be paid and when payment is received from customers is critical for wholesale and retail with their large inventory balance.

Sales Payable Turnover = Average accounts payable

In 2006-2009 year the payable turnover was increased gradually, but in year 2007 are some decreases. The BPL’s borrowing and loan money is not huge amount and it also represents an important source of financing for operating activities, so that the payable turnover of BPL ration is good.

Profitability Ratio

Gross profit Margin:

The gross profit margin reflects the effectiveness of pricing policy and of productive efficiency. That is how well the purchase or production cost of goods is controlled. If raising the price of the firm’s product increases the gross margin, the product may become uncompetitive, producing a falloff in sales. Therefore a company may find it advantage to lower the price and therefore lower the gross profit margin if it increase sale so much as to increase total profit.

Gross Profit X 100

Gross profit Margin (%) = Sale

From the analysis of BPL, the gross profit margin increases year- by – year, though material cost regularly increased due to high rate and also increased other direct and indirect expense. The GPMR of BPL implies the efficiency is developed day to day at the production area especially in year 2008

15. Net profit Margin:

Profit margin on sales provides little useful information since it means the effectiveness of sales in producing profit with the effect of the method of financing on profit ( since net income is after deduction of interest on debt and of taxed, which are affected by interest). The higher firms NPM, the better the firm’s position. A NPM could ensure adequate return to the owners. Alternatively low NPM has the opposite implication.

Net profit Margin (%) = Net Income / Sales *100

The NPM ratio is satisfactory at the study of the BPL, but it’s decreased in 2007. In year 2007 it was 9.81% which couldn’t ensure adequate return to the owners. But the average position of BPL for NPM is satisfactory.

16. Return on total assets:

Return on total assets is the total after corporate tax return to stockholder and lenders on the total investment that they have in the firm. It is the rate of return earned by the firm as a whole for all its investors, including lenders. The higher ROA of firms represents the better position.

Return on Total Assets, % = Net Income + Interest Expenses X 100

The ROA ratio is satisfactory of the study of the BPL. But it is decreased in year 2006-2009. In the year 2006 it was 6.00%, which were highest until the recent year. last year the ratio was decreased to 4.60%. But the overall performances were better

17. Return On Equity (ROE)

According to this ratio, profitability has measured by dividing the net profits after taxes but before preference dividend by the average total shareholders’ equity. The return on common equity (ROE) measures the return earned on the common stockholder’s investments in the firm. Generally the higher the return, the better off is the owners. Return on equity is therefore the best measure of the company’s success in fulfilling its goal.

ROE = (Net Income / Stockholders Equity) *100

he ROE Ratio decreased in year 2006-2009 and in year 2008 the ratio was decreased to 3.35%. Although the BPL’s ROA of two year was low but the overall performances was better.

18. Earning Per Share (EPS):

Earning per share measures the profit available to the equity holders on a per share basis. The perfect available for the ordinary shareholders are represents by otherwise the residential income of the firm.

EPS = Net profit after tax / Number of ordinary share outstanding:

The EPS of BPL has increased over the 2006-2009. But the it decreased in 2008 to 3.61. The reason was the net income decreased in last two years and the no. of outstanding shares was increased. The number of shares outstanding has to count from recent year and added with the bonus recent shares of those years. The higher EPS is good for the company. So EPS of BPL position is not so good.

19. Dividend per Share (DPS):

Dividend per Share is the dividends paid to the shareholders on a per share basis. In other words, DPS is the net distributed profit belonging to the shareholders dividing by the number of ordinary share outstanding.

Here the DPS of BPL decreased in last 2 years because the cash dividend increases and number of shares outstanding was increased. But in 2006 and 2007 increased because cash dividend was higher and number of shares outstanding was lower. The overall performance of BPL for dividend per share is not so good.

Dividend Payout Ratio:

The Dividend Payout Ratio indicates the percentage of each Tk. Earned that is distributed to the owners in the form of cash.

Dividend Payout Ratio = (Dividend Per Share / EPS) *100

We can see in year 2007 the DPS was 48.70%, which is higher than the next years. As BPL is a well established “mature” firm. So it tends to have higher payout ratios. Then it measures the good relationship between the earnings belonging to the shareholders and the dividend paid to them. The Dividend payout ratio is not good for last two years. It decreased from 48.70% to 8.72% which is very much lower in terms of earnings as well as shareholders.

Industry Analysis ofIntroduction:

In an industry analysis, any number of key characteristics should be considered at some point. In this case things that must be considered are market capitalization, turn over, market performance, past sales and earnings performance, the performance of industries, the attitudes of the government towards the industries, labor conditions within the industries, the competitive conditions as reflected in any barriers to entry that might exist, and stock prices of firms in the industry relative to other earning. After comparing these things with BPL we have evaluated, BPL is “A” category pharmaceuticals company enlisted in Dhaka Stock Exchange 3 July, 1985 and Chittagong Stock Exchange 11 June, 1995 and AIM (Alternative Investment Market) 21 October, 2005, and face value of share is Tk. 10. Since it is “A” category company, it is regular in holding the AGM and its last AGM was held 15th June 2010. At present the number of shares out-standing 151,149,296 and the amount of paid up share capital is Tk. 1,511,493(in thousands). General public and institutions is 50.97%, Foreign Investors is 27.66%, Sponsors / Directors is 2.75%, and ICB investors account is 10.46% of total share capital. The net profit after tax is Tk. 624,740,307 and earning per share at the current time is Tk. 4.13, dividend per share is Tk. 0.36, the price earning ratio is 37.72.

| Particulars | Years | |||

| 2006 | 2007 | 2008 | 2009 | |

| Market Price per share on year ended 2009 (Tk.) | 53.7 | 58.9 | 167.7 | 155.8 |

| Earning Price per Share (Tk.) | 4.67 | 3.08 | 3.61 | 4.13 |

| Dividend per Share (Tk.) | 1.55 | 1.50 | 0.69 | 0.36 |

| Dividend Payout Ratio | 33.20% | 48.70% | 19.11% | 8.72% |

| Price Earning Ratio | 13.06 | 21.04 | 46.45 | 37.72 |

Year Ended Market Price:

From the above table it is clear that the market price of the share increased very high from the year 2006-2009,. The year-ended market price of share pf BPL is shown in the following figure:

The reasons of Increase in year-ended market price are- increase in Earning Per Share(EPS), increase in Dividend Per Share in 2008, Increase in Dividend Payment whether in cash dividend or Stock dividend and above in price earning ratio. The reasons of increase in year-ended market price are the opposite of decrease in year-ended market price.

Earning Per Share:

EPS calculations made over years indicate whether or not the firms earnings power on per share basis has changed over that period. The EPS of the company should be compared with other companies of the same industry. EPS simply shows the profitability of the firm on a per-share basis, it does not reflect how much is paid as dividend and how much is retained in the business. But to know the stock value of the firm, it acts as a valuable index. However, the EPS of the BPL over the last four years is shown as follows:

This EPS Decrease gradually in year 2006-2009, and year 2007 decreased & 2008 slightly increased. The growing up EPS defines the years’ Net profit increased and the downing up EPS defines the years’ Net profit Decreased. This increase was more in year 2006 than other years. Moreover, its number of outstanding shares was almost remained consistent over the years except 2006 and 2007.

Dividend Per Share:

The net profit after taxes belongs to shareholders. But the income, which they really receive, is the amount of earnings distributed such as dividend. Therefore, to know the strength of the stock of a particular company, many investors may be interested in DPS rather than EPS. DPS is the earnings distributed to ordinary shareholders dividend by the number of ordinary shares outstanding. The DPS of the BPL for the last five years are given below:

DPS of BPL in year 2006 was high, because in this year company’s EPS was good. And last three years gradually decreased. In this years company has given shareholders 5% cash and 10% stock dividend. Another reason was that its RPS decreased but the number of share out-standing goes up in this year.

Dividend Payout Ratio:

Since the D/P ratio per share cannot be a true yardstick to measure the strength of the stock of the particular company, D/P ratio serves as an important criterion to give the investors of the financial performance of that company. The more dividends are paid, the more shareholders become convicted of the financial strength of the company. However, excessive dividend payment impairs the growth opportunity of that company because the company losses the opportunity to invest in the profitable interest. The D/P ratio of BPL for the last five years is shown is follows:

The D/P ratios are gradually decreased in year 2006-2009. D/P ratio increased significantly because DPS did not increased proportionately with EPS. Another reason was that management kept significant portion retained earnings. In year 2006-2007 are increase of D/P. The reason of increase in D/P ratio is the opposite of decrease in D/P ratio.

Price-Earning Ratio:

The Price-Earning Ratio is widely used by the security investors to value the firm’s performance as expected by the investors. It indicates investor’s judgments or expectations about the firm’s performance. Management is also increased in this market appraisal of the firm’s performance and will like to find the cause if the P/E ratio declines. P/E ratio reflects investors’ expectations about the growth in the firms’ earnings. Industries differ in their growth prospectus; accordingly, the P/E ratio for industries varies widely. The P/E ratio of BPL for the last four years is given below:

The P/E ratio decreases until in years 2006-2009 then it was increased in year 2008 and again decreased in year 2009. The decrease reason was decrease in share price. The way of share price decreased the EPS increases. The P/E ratio was greater in 2008 because there was a huge increase in the market price per share of them. Moreover, the increase in P/E ratio indicates the earning performance of BPL overall good.

SWOT ANALYSIS:

Strengths:

- BPL currently manufactures about 452 products with different dosage forms under different brand names. Many of its products enjoy the status of brands leaders in the market.

- Sales of the formulation products increased by 2.55% and export by 6.65%.

- Beximco Pharma has successfully captured the local pharmaceutical market and enjoys a commending share of 9% of the entire market.

- BPL believes that the use of different type of information system.

- BPL using different type of technology for move their company to carrying innovation forward.

- BPL has secured market niche in the market by following cost leadership strategies as well as aggressive promotional activities. The companies strong support to the medical community has gained its brand locality form the doctor.

Weakness:

- BPL has a narrower product line and number of products than its principle competitor in the market.

- The company produces so many product variation for that reason some time feels confuse what to suggest BPL product.

- BPLs distribution network is not working as good as its competitor in the urban area. Opsonin , Acme is doing well in this area than BPL.

- Warehouse management system is not well so there are always they face store problem for storage problem.

Opportunities:

- The market is expected to grow by 9% to 15% per annum for the next 5 years. The next stage growth is expected to come from backward integration to manufacturing processes that are difficult to imitate products and exports.

- The WTO agreement extended in 2016 instead of 2005 for the LDC only in pharmaceutical company.

- The company start to produces kind of injectables comparing. The injectables market is a large one so they can easily competes their rival companies.

- Entered into nine new international markets in Asia, Middle East, Pacific Islands, Africa and Central America. Registered 107 new products in different overseas markets.

- In Bangladesh pharmaceutical companies are considered as growing company. So there are lots of opportunities in this field.

- Cost of producing product cost low their close competitor it will help them to charge low price of the product it given huge market opportunities in Middle-East and North Africa nation.

- BPL is one among the few pharmaceuticals companies in the world that are currently producing technology driven CFC-free HFA MDIs. Based in the very encouraging responses that we are getting for our MDI products particularly for our Non-CFC MDIs from Central and Latin America and Middle East Countries, we have undertaken a project to add another 10 million units capacity plant beside our existing MDI facility. The project is progressing as planned.

- Therapeutic Goods Administration (TGA), Australia and Joint Inspection Committee of the Ministry of Health of Gulf Cooperation Council (GCC) countries completed audit of the new Oral Solid Dosage (OSD) and Metered Dose Inhaler (MDI) & Spray manufacturing facilities.

- Signed a ling term arrangement with the Global Supply Division of UNICEF (Denmark) to supply 60,000 units CFC free metered dose inhaler product over a two year contract period give enormous market opportunities.

- During the year, BPL have some project to build facility to manufacture Small Volume Parenterals (SVP), Opthalmic and Nibulizer Solutions progressed as acheduled. Hopefully as planned, they will be able to commence marketing of these products soon . They are now expediting the process of adding more lines to their existing Oral Solid Dosage Facility.

Threats:

- In most case the product cost of BPL is higher than that of other companies because of high cost of maintaining quality products, high distribution cost etc. In the context of Bangladesh economic structure, BPL is in fear of loosing market in the rural areas.

- In Bangladesh the copyright act is not applied by the government appropriately which creates continually threats for the company as its competitors easily copy its products.

- Because of political unrest and poor infrastructure facilities BPL faces problems in Local marketing.

- BPL also facing treats forms its Indian counterparts as they are offering their products at lower price than it.

- After 2015 they face lot of challenge for TRIPS purpose.

- Overall sales declined by 2.84%.

7. Findings

Liquidity:

Liquidity reveals that BPL has enough current assets than previous years to pay the obligations. The liquidity position of the company is acceptable because it’s current ratio is 1.33,1.8,1.1,2.98 respectively from year 2006 to 2009 and Quick ratio is 0.63,0.89,0.52,2.24 respectively. Quick ratio is below 1 from 2006 to 2007. It does not comprise the standard value .

Financial Solvency & Flexibility:

The solvency dimension of BPL is not so strong. Its interest coverage ratio stood at 3.17,2.64, 4 & 4.15 from year 2006 to 2009 . There was a decline in coverage ratio. Higher value is expected for paying the interest obligation.

BPL total debt to equity ratio stood at 0.24, 0.26, 0.2 & 0.21 respectively which is down or flat year by year. It indicates that BPL has greater protection and stake so they can increase its long-term borrowing.

The operating performance of BPL is good. That means it’s profit margin is more or less flat or increase over the year

Working capital of the company is not satisfactory. Company should focus on the working capital for expansion of the business & payment for short term obligations.

At last I can conclude that overall performance of the company is satisfactory.

Recommendation:

After analysis of different financial performance measures and comparing with other particular industry BPL financial performance is comparatively high and sometimes this company’s second position. Improve the recommended sectors if these are possible. The recommended sectors are given below:

- Leverage of the company indicates that BPL using more equity capital than long term debt capital, which is not a good signal for the company because it indicates lacking of outsourcing.

- Considering the comparative company data BPL is clearly behind from the main competitor like Square in the context of activity ratio.

- The possible causes of fall of return on asset, return on equity ratio are rising in the cost of production, administration, finance cost.

- BPL may reduce their operating and non-operating expenses in order to increase the profitability of the company.

- BPL should organize seminar, campaign and do some promotional activities to provide proper knowledge and used about medicine.

- Evaluation for the good performance of the employees by introducing award and incentives.

- BPL should try to perform some social responsibility like providing free doctors and medicine facility to any rural areas for particular period of time.

- Overall performance measurement shows BPL not only provide operational performance but it also provide better work environment to the employee, exclusive salary structure and contribution to the social welfare.

Conclusion:

Beximco Pharmaceuticals Limited (BPL) is one of the well-known names in the business sector of Bangladesh. The company was at top three or four years ago. Still now , the company showing its growth.The company can’t perform well without its internal performance evaluation. One of the popular techniques to evaluate the performance is ratio analysis. And i used the same techniques to evaluate the performance of BPL.BPL is one of the market leader and in some cases market leader in the pharmaceuticals industry of Bangladesh, It is gradually expanding its assets and able to proper utilize its assets well. The overall financial position of the company may be said to satisfactory over the years. Since BPL is a good concern of Beximco Group, so the position may again be improved if management becomes more careful of income and expenditure, using of working capital.